Can Digital Finance Accelerate the Digital Transformation of Companies? From the Perspective of M&A

Abstract

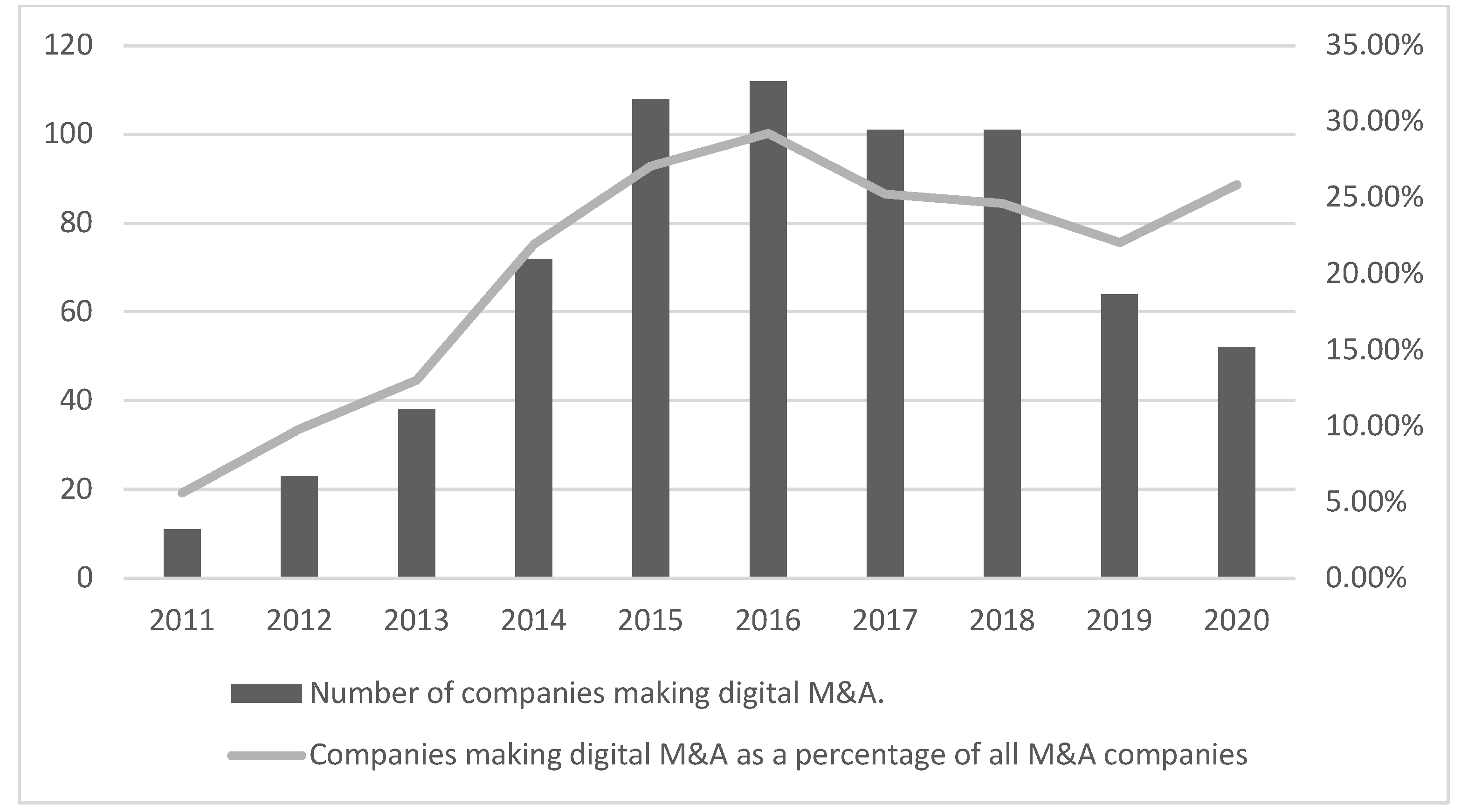

:1. Introduction

2. Theoretical Background

2.1. Digital Finance and Digital M&A

2.2. The Mediating Effect of Financing Constraints between Digital Finance and Digital M&A

2.3. The Mediating Effect of Innovation Capabilities between Digital Finance and Digital M&A

2.4. The Moderating Effect of Management Age

2.5. The Moderating Effect of Internal Control

2.6. The Moderating Effect of Bank Competition

3. Study Design

3.1. Sample Selection and Data Collection

3.2. Variable Definition

3.2.1. Explained Variable

3.2.2. Explanatory Variable

3.2.3. Mediating Variables

3.2.4. Moderating Variables

3.2.5. Control Variables

3.3. Model Setting

4. Empirical Analysis

4.1. Descriptive Statistics

4.2. Correlation Coefficient Matrix

4.3. Regression Analysis

4.4. Mediating Effect Test

4.5. Moderating Effect Test

4.6. Robustness Test

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Fitzgerald, S.; Parker, R. IDC FutureScape Webcast: Worldwide Digital Transformation 2022 Predictions. Available online: https://www.idc.com/getdoc.jsp?containerId=US48360721 (accessed on 29 October 2022).

- Guo, L.; Xu, L. The Effects of Digital Transformation on Firm Performance: Evidence from China’s Manufacturing Sector. Sustainability 2021, 13, 12844. [Google Scholar] [CrossRef]

- Wang, H.; Feng, J.; Zhang, H.; Li, X. The effect of digital transformation strategy on performance: The moderating role of cognitive conflict. Int. J. Confl. Manag. 2020, 31, 441–462. [Google Scholar] [CrossRef]

- Vial, G. Understanding digital transformation: A review and a research agenda. J. Strateg. Inf. Syst. 2019, 28, 118–144. [Google Scholar] [CrossRef]

- Warner, K.S.R.; Wäger, M. Building dynamic capabilities for digital transformation: An ongoing process of strategic renewal. Long Range Plan. 2019, 52, 326–349. [Google Scholar] [CrossRef]

- Boote, J.; Harper, A.; Nielsen, J.; Kengelbach, J. Cracking the Code of Digital M&A. Available online: https://www.bcg.com/de-de/publications/2019/cracking-code-digital-m-and-a.aspx (accessed on 12 February 2019).

- Ahuja, G.; Katila, R. Technological acquisitions and the innovation performance of acquiring firms: A longitudinal study. Strateg. Manag. J. 2001, 22, 197–220. [Google Scholar] [CrossRef]

- Leroi, A.; Miles, L.; Spaulding, E.; Bacular, L.P. The Changing Rules for Digital M&A. Available online: https://media.bain.com/Images/BAIN_BRIEF_Changing_Rules_for_Digital_M_and_A.pdf (accessed on 10 February 2017).

- Huang, J.; Henfridsson, O.; Liu, M.J.; Newell, S. Growing on steroids: Rapidly scaling the user base of digital ventures through digital innovation. MIS Q. 2017, 41, 301–314. [Google Scholar] [CrossRef]

- Datta, P.; Roumani, Y. Knowledge-acquisitions and post-acquisition innovation performance: A comparative hazards model. Eur. J. Inf. Syst. 2015, 24, 202–226. [Google Scholar] [CrossRef]

- Gao, L.S.; Iyer, B. Analyzing complementarities using software stacks for software industry acquisitions. J. Manag. Inf. Syst. 2006, 23, 119–147. [Google Scholar] [CrossRef]

- FRESHFIELDS. The World of Digital M&A. Available online: https://www.freshfields.com/49f820/globalassets/our-thinking/campaigns/digital/digital-ma/freshfields-digital--ma-study.pdf (accessed on 3 December 2018).

- Kengelbach, J.; Keienburg, G.; Degen, D.; Söllner, T.; Kashyrkin, A.; Sievers, S. The 2020 M&A Report: Alternative Deals Gain Traction. Available online: https://www.bcg.com/publications/2020/mergers-acquisitions-report-alternative-deals-gain-traction (accessed on 29 September 2020).

- Hanelt, A.; Firk, S.; Hildebrandt, B.; Kolbe, L.M. Digital M&A, digital innovation, and firm performance: An empirical investigation. Eur. J. Inf. Syst. 2021, 30, 3–26. [Google Scholar] [CrossRef]

- Andriushchenko, K.; Buriachenko, A.; Rozhko, O.; Lavruk, O.; Skok, P.; Hlushchenko, Y.; Muzychka, Y.; Slavina, N.; Buchynska, O.; Kondarevych, V. Peculiarities of sustainable development of enterprises in the context of digital transformation. Entrep. Sustain. Issues 2020, 7, 2255. [Google Scholar] [CrossRef]

- Zhang, L.; Chao, X.; Qian, Q.; Jing, F. Credit evaluation solutions for social groups with poor services in financial inclusion: A technical forecasting method. Technol. Forecast. Soc. Change 2022, 183, 121902. [Google Scholar] [CrossRef]

- Gomber, P.; Kauffman, R.J.; Parker, C.; Weber, B.W. On the fintech revolution: Interpreting the forces of innovation, disruption, and transformation in financial services. J. Manag. Inf. Syst. 2018, 35, 220–265. [Google Scholar] [CrossRef]

- Xue, L.; Zhang, Q.; Zhang, X.; Li, C. Can Digital Transformation Promote Green Technology Innovation? Sustainability 2022, 14, 7497. [Google Scholar] [CrossRef]

- Teece, D.J. Business models, business strategy and innovation. Long Range Plan. 2010, 43, 172–194. [Google Scholar] [CrossRef]

- Harford, J. Corporate cash reserves and acquisitions. J. Financ. 1999, 54, 1969–1997. [Google Scholar] [CrossRef]

- Denis, D.J.; Sibilkov, V. Financial Constraints, Investment, and the Value of Cash Holdings. Rev. Financ. Stud. 2009, 23, 247–269. [Google Scholar] [CrossRef] [Green Version]

- Gorbenko, A.S.; Malenko, A. The timing and method of payment in mergers when acquirers are financially constrained. Rev. Financ. Stud. 2018, 31, 3937–3978. [Google Scholar] [CrossRef]

- Xie, C.; Liu, C. The Nexus between Digital Finance and High-Quality Development of SMEs: Evidence from China. Sustainability 2022, 14, 7410. [Google Scholar] [CrossRef]

- Jagtiani, J.; Lemieux, C. Do fintech lenders penetrate areas that are underserved by traditional banks? J. Econ. Bus. 2018, 100, 43–54. [Google Scholar] [CrossRef] [Green Version]

- Lee, I.; Shin, Y.J. Fintech: Ecosystem, business models, investment decisions, and challenges. Bus. Horiz. 2018, 61, 35–46. [Google Scholar] [CrossRef]

- Fuster, A.; Plosser, M.; Schnabl, P.; Vickery, J. The Role of Technology in Mortgage Lending. Rev. Financ. Stud. 2019, 32, 1854–1899. [Google Scholar] [CrossRef] [Green Version]

- Abbasi, K.; Alam, A.; Brohi, N.A.; Brohi, I.A.; Nasim, S. P2P lending Fintechs and SMEs’ access to finance. Econ. Lett. 2021, 204, 109890. [Google Scholar] [CrossRef]

- Foley, C.F.; Manova, K. International trade, multinational activity, and corporate finance. Economics 2015, 7, 119–146. [Google Scholar] [CrossRef]

- Brown, J.R.; Martinsson, G.; Petersen, B.C. Do financing constraints matter for R&D? Eur. Econ. Rev. 2012, 56, 1512–1529. [Google Scholar] [CrossRef] [Green Version]

- Gomber, P.; Koch, J.-A.; Siering, M. Digital Finance and FinTech: Current research and future research directions. J. Bus. Econ. 2017, 87, 537–580. [Google Scholar] [CrossRef]

- Bena, J.; Li, K. Corporate innovations and mergers and acquisitions. J. Financ. 2014, 69, 1923–1960. [Google Scholar] [CrossRef]

- Norburn, D. Gogos, yoyos and dodos: Company directors and industry performance. Strateg. Manag. J. 1986, 7, 101–117. [Google Scholar] [CrossRef]

- Singh, A.; Hess, T. How chief digital officers promote the digital transformation of their companies. In Strategic Information Management; Routledge: London, UK, 2020; pp. 202–220. [Google Scholar]

- Child, J. Managerial and organizational factors associated with company performance part I. J. Manag. Stud. 1974, 11, 175–189. [Google Scholar] [CrossRef]

- Chowdhury, J.; Fink, J. How Does CEO Age Affect Firm Risk? Asia-Pac. J. Financ. Stud. 2017, 46, 381–412. [Google Scholar] [CrossRef]

- Wiersema, M.F.; Bantel, K.A. Top management team demography and corporate strategic change. Acad. Manag. J. 1992, 35, 91–121. [Google Scholar] [CrossRef]

- Yim, S. The acquisitiveness of youth: CEO age and acquisition behavior. J. Financ. Econ. 2013, 108, 250–273. [Google Scholar] [CrossRef]

- Zhang, T.; Sabherwal, S.; Jayaraman, N.; Ferris, S.P. The Young and the Restless: A Study of Age and Acquisition Propensity of CEOs of UK Firms. J. Bus. Financ. Account. 2016, 43, 1385–1419. [Google Scholar] [CrossRef]

- Hambrick, D.C.; Mason, P.A. Upper echelons: The organization as a reflection of its top managers. Acad. Manag. Rev. 1984, 9, 193–206. [Google Scholar] [CrossRef]

- Simons, R. Control in an age of empowerment. Harv. Bus. Rev. 1995, 73, 80–88. [Google Scholar] [CrossRef]

- Cheng, M.; Dhaliwal, D.; Zhang, Y. Does investment efficiency improve after the disclosure of material weaknesses in internal control over financial reporting? J. Account. Econ. 2013, 56, 1–18. [Google Scholar] [CrossRef]

- Ribstein, L.E. Market vs. regulatory responses to corporate fraud: A critique of the Sarbanes-Oxley Act of 2002. J. Corp. L. 2002, 28, 1. [Google Scholar] [CrossRef]

- Jensen, M.C. The modern industrial revolution, exit, and the failure of internal control systems. J. Financ. 1993, 48, 831–880. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Norton, D.P. Linking the balanced scorecard to strategy. Calif. Manag. Rev. 1996, 39, 53–79. [Google Scholar] [CrossRef] [Green Version]

- Cohen, D.A.; Dey, A.; Lys, T.Z. Real and accrual-based earnings management in the pre-and post-Sarbanes-Oxley periods. Account. Rev. 2008, 83, 757–787. [Google Scholar] [CrossRef] [Green Version]

- Pham, T.T.T.; Nguyen, T.V.H.; Nguyen, K. Does bank competition promote financial inclusion? A cross-country evidence. Appl. Econ. Lett. 2019, 26, 1133–1137. [Google Scholar] [CrossRef]

- Porter, M.E. Industry structure and competitive strategy: Keys to profitability. Financ. Anal. J. 1980, 36, 30–41. [Google Scholar] [CrossRef]

- Omarini, A.E. Banks and FinTechs: How to develop a digital open banking approach for the bank’s future. Int. Bus. Res. 2018, 11, 23. [Google Scholar] [CrossRef]

- Kandilov, I.T.; Leblebicioğlu, A.; Petkova, N. Cross-border mergers and acquisitions: The importance of local credit and source country finance. J. Int. Money Financ. 2017, 70, 288–318. [Google Scholar] [CrossRef]

- Hadlock, C.J.; Pierce, J.R. New Evidence on Measuring Financial Constraints: Moving Beyond the KZ Index. Rev. Financ. Stud. 2010, 23, 1909–1940. [Google Scholar] [CrossRef]

{kind=link}

| Variable | Symbol | Notes |

|---|---|---|

| Digital M&A | M&A | Definition as above |

| Digital finance | INDEX | |

| Financing constraints | SA | |

| Innovation capability | PATENT | |

| Management age | AGE | |

| Internal control | IC | |

| Bank competition | BC | |

| Enterprise size | SIZE | Natural logarithm of total assets |

| Operating income growth rate | GROWTH | Operating income of the current year/operating income of the previous year-1 |

| Operating cash flow | CASH | EBITDA + depreciation and amortization − working capital additions − capital expenditures, then take the natural logarithm |

| Book-to-market ratio | BM | Ownership interest/Market value |

| Shareholding ratio of the largest shareholder | TOP1 | Number of shares held by the largest shareholder/number of shares outstanding |

| Proportion of independent directors | IND | Number of independent directors/Total number of board seats |

| Return on total assets | ROA | Net profit/total assets |

| Return on net assets | ROE | Net income/owner’s equity |

| GDP | GDP | Natural logarithm of total City-level GDP |

| GDP growth rates | GDPG | City-level GDP growth rate |

| Variable | N | Mean | Std | Min | Mid | Max |

|---|---|---|---|---|---|---|

| M&A | 3816 | 0.179 | 0.383 | 0 | 0 | 1 |

| INDEX | 3816 | 5.322 | 0.367 | 4.083 | 5.405 | 5.771 |

| SA | 3816 | −3.847 | 0.239 | −4.580 | −3.829 | −3.354 |

| PATENT | 3816 | 1.659 | 1.459 | 0 | 1.609 | 5.357 |

| AGE | 3816 | 50.611 | 3.540 | 42.222 | 50.571 | 59.222 |

| IC | 3816 | 6.322 | 1.016 | 3.714 | 6.504 | 6.675 |

| BC | 3816 | 0.556 | 0.497 | 0 | 1 | 1 |

| SIZE | 3816 | 22.026 | 1.113 | 19.967 | 21.881 | 25.664 |

| GROWTH | 3816 | 0.228 | 0.413 | −0.476 | 0.155 | 2.609 |

| CASH | 3816 | 10.520 | 15.676 | −21.185 | 18.462 | 22.567 |

| BM | 3816 | 0.323 | 0.160 | 0 | 0.305 | 0.754 |

| TOP1 | 3816 | 32.961 | 14.226 | 8.770 | 30.615 | 70.75 |

| IND | 3816 | 37.590 | 5.248 | 33.33 | 35.71 | 57.14 |

| ROA | 3816 | 0.043 | 0.0491 | −0.1773 | 0.042 | 0.178 |

| ROE | 3816 | 0.071 | 0.091 | −0.423 | 0.074 | 0.282 |

| GDP | 3816 | 11.564 | 0.437 | 10.176 | 11.642 | 12.579 |

| GDPG | 3816 | 7.984 | 2.580 | 1.200 | 7.870 | 16.200 |

| M&A | Index | SA | Patent | Age | IC | BC | |

|---|---|---|---|---|---|---|---|

| M&A | 1 | 0.120 *** | −0.046 *** | 0.016 | −0.058 *** | −0.011 | 0.021 |

| index | 0.136 *** | 1 | −0.075 *** | 0.079 *** | 0.130 *** | −0.139 *** | 0.291 *** |

| SA | −0.044 *** | −0.140 *** | 1 | −0.090 *** | −0.042 ** | −0.122 *** | −0.034 ** |

| patent | 0.014 | 0.083 *** | −0.085 *** | 1 | 0.063 *** | 0.063 *** | 0.151 *** |

| Age | −0.065 *** | 0.131 *** | −0.032 ** | 0.065 *** | 1 | 0.029 * | −0.014 |

| IC | −0.007 | −0.034 ** | −0.153 *** | 0.088 *** | 0.059 *** | 1 | −0.006 |

| BC | 0.021 | 0.293 *** | −0.026 | 0.154 *** | −0.013 | 0.023 | 1 |

| M&A | M&A | M&A | M&A | |

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| INDEX | 1.925 ** | |||

| (2.38) | ||||

| BREADTH | 1.301 ** | |||

| (2.19) | ||||

| DEPTH | 0.962 * | |||

| (1.83) | ||||

| LEVEL | 0.147 | |||

| (0.24) | ||||

| SIZE | −0.109 ** | −0.112 ** | −0.109 ** | −0.113 ** |

| (−2.25) | (−2.31) | (−2.24) | (−2.34) | |

| GROWTH | 0.173 | 0.169 | 0.173 | 0.168 |

| (1.56) | (1.53) | (1.57) | (1.52) | |

| CASH | −0.006 * | −0.006 * | −0.006 * | −0.006 * |

| (−1.84) | (−1.82) | (−1.86) | (−1.83) | |

| BM | −0.671 ** | −0.671 ** | −0.662 * | −0.670 ** |

| (−1.97) | (−1.97) | (−1.95) | (−1.98) | |

| TOP1 | −0.005 | −0.005 | −0.005 | −0.004 |

| (−1.32) | (−1.32) | (−1.32) | (−1.31) | |

| IND | 0.012 | 0.011 | 0.013 | 0.013 |

| (1.37) | (1.35) | (1.49) | (1.54) | |

| ROA | 3.515 | 3.546 | 3.639 | 3.822 |

| (1.50) | (1.51) | (1.55) | (1.64) | |

| ROE | −2.466 ** | −2.449 ** | −2.543 ** | −2.545 ** |

| (−1.97) | (−1.96) | (−2.03) | (−2.04) | |

| GDP | 0.074 | 0.094 | 0.260 * | 0.401 *** |

| (0.39) | (0.49) | (1.70) | (3.06) | |

| GDPG | 0.035 | 0.031 | 0.031 | 0.020 |

| (1.20) | (1.07) | (1.07) | (0.73) | |

| Constant | −12.468 *** | −10.060 *** | −10.394 *** | −8.215 *** |

| (−4.21) | (−4.16) | (−3.97) | (−2.65) | |

| Year | YES | YES | YES | YES |

| Industry | YES | YES | YES | YES |

| N | 3816 | 3816 | 3816 | 3816 |

| Pseudo R2 | 0.125 | 0.125 | 0.124 | 0.123 |

| SA | M&A | PATENT | M&A | |

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| INDEX | −0.793 *** | 1.843 ** | 1.478 *** | 1.830 ** |

| (−2.64) | (2.22) | (4.98) | (2.25) | |

| SA | −0.064 ** | |||

| (−1.99) | ||||

| PATENT | 0.065 * | |||

| (1.77) | ||||

| Control | YES | YES | YES | YES |

| constant | 3.302 *** | −12.612 *** | −12.135 *** | −11.660 *** |

| (3.38) | (−4.16) | (−11.65) | (−3.89) | |

| Year | YES | YES | YES | YES |

| Industry | YES | YES | YES | YES |

| N | 3816 | 3816 | 3816 | 3816 |

| Pseudo R2 | 0.241 | 0.127 | 0.290 | 0.125 |

| M&A | M&A | M&A | |

|---|---|---|---|

| (1) | (2) | (3) | |

| INDEX | 6.162 ** | 5.630 *** | 2.286 *** |

| (2.37) | (3.07) | (2.76) | |

| INDEX×AGE | −0.083 * | ||

| (−1.73) | |||

| AGE | 0.425 | ||

| (1.63) | |||

| INDEX×IC | −0.593 ** | ||

| (−2.25) | |||

| IC | 3.271 ** | ||

| (2.25) | |||

| INDEX×BC | 1.004 *** | ||

| (2.94) | |||

| BC | −5.408 *** | ||

| (−2.93) | |||

| Control | YES | YES | YES |

| Constant | −34.132 ** | −33.045 *** | −14.859 *** |

| (−2.52) | (−3.42) | (−4.74) | |

| Year | YES | YES | YES |

| Industry | YES | YES | YES |

| N | 3816 | 3816 | 3816 |

| Pseudo R2 | 0.127 | 0.125 | 0.127 |

| Adding Province Dummy Variables | Number of Digital M&A | Manufacturing Enterprises | Lag 1 Period | PSM | |

|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | |

| INDEX | 2.381 ** | 1.428 ** | 3.164 *** | 2.112 *** | 2.702 ** |

| (2.11) | (2.57) | (3.23) | (2.74) | (2.43) | |

| Control | YES | YES | YES | YES | YES |

| Constant | −13.834 *** | −8.447 *** | −12.058 *** | −11.531 *** | −12.957 *** |

| (−3.50) | (−4.25) | (−3.59) | (−4.09) | (−3.25) | |

| Year | YES | YES | YES | YES | YES |

| Industry | YES | YES | YES | YES | YES |

| Province | YES | NO | NO | NO | NO |

| N | 3816 | 3816 | 2467 | 3609 | 1143 |

| Pseudo R2/R2 | 0.136 | 0.094 | 0.050 | 0.121 | 0.129 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yu, M.; Yan, A. Can Digital Finance Accelerate the Digital Transformation of Companies? From the Perspective of M&A. Sustainability 2022, 14, 14281. https://doi.org/10.3390/su142114281

Yu M, Yan A. Can Digital Finance Accelerate the Digital Transformation of Companies? From the Perspective of M&A. Sustainability. 2022; 14(21):14281. https://doi.org/10.3390/su142114281

Chicago/Turabian StyleYu, Mingtao, and Aiguo Yan. 2022. "Can Digital Finance Accelerate the Digital Transformation of Companies? From the Perspective of M&A" Sustainability 14, no. 21: 14281. https://doi.org/10.3390/su142114281