Socioeconomic Sustainability for Low-Income Households: The Mediating Role of Financial Well-Being

Abstract

:1. Introduction

- RQ1:

- Does financial literacy have a significant impact on the socioeconomic status of B40 households?

- RQ2:

- Does financial well-being mediate the relationship between financial literacy and the socioeconomic status of B40 households?

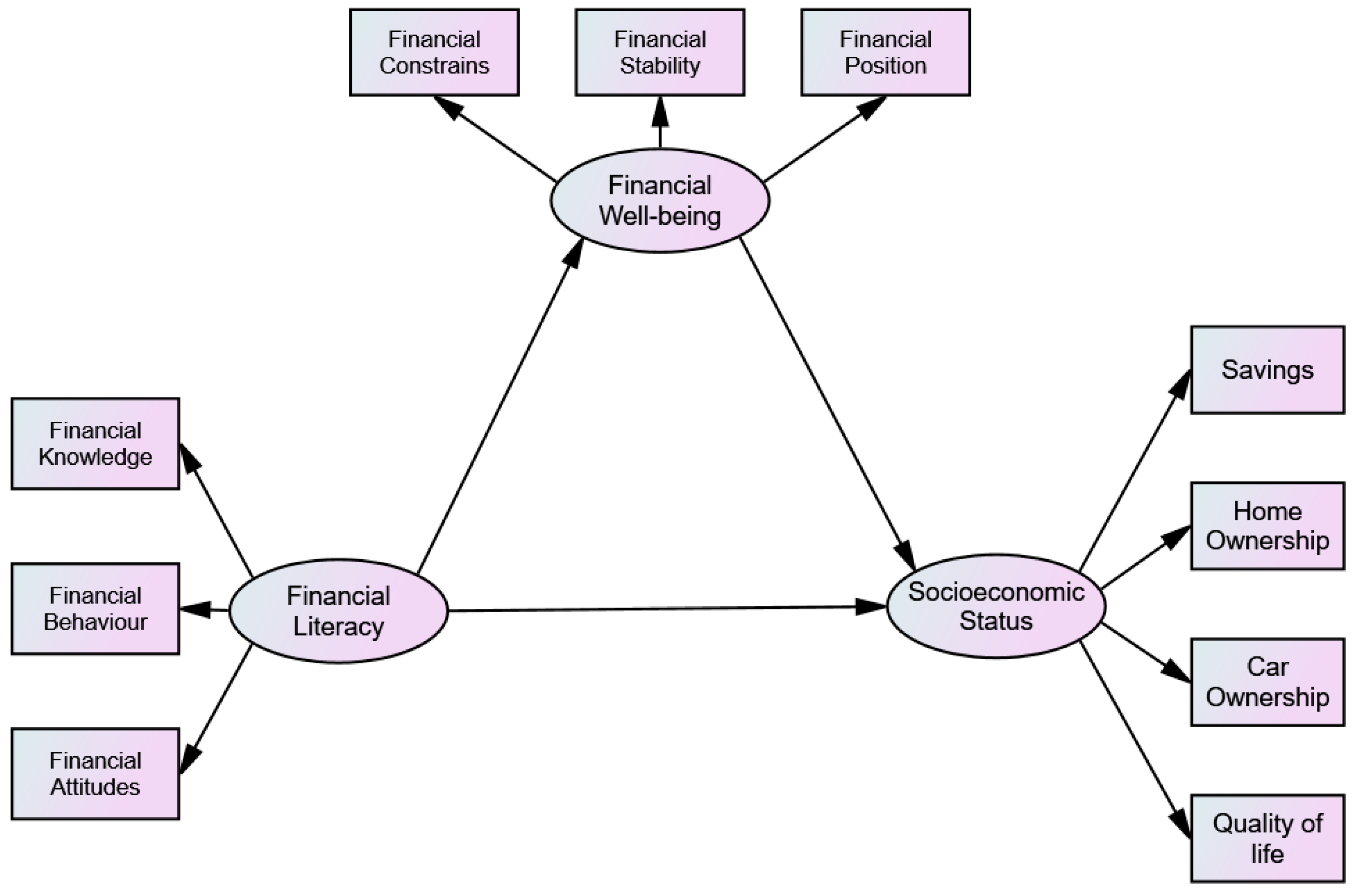

2. Theoretical Analysis and Hypothesis

2.1. Theoretical Analysis and Hypothesis Development

The Influence of Financial Literacy (FL)

3. The Role of Financial Well-Being (FWB)

4. The Effects on Socioeconomic Status (SES)

5. Methodology

5.1. Respondents

5.2. Sampling and Data Collection

5.3. Measurement

5.4. Pilot Study

5.5. Demographic Profiles

6. Results

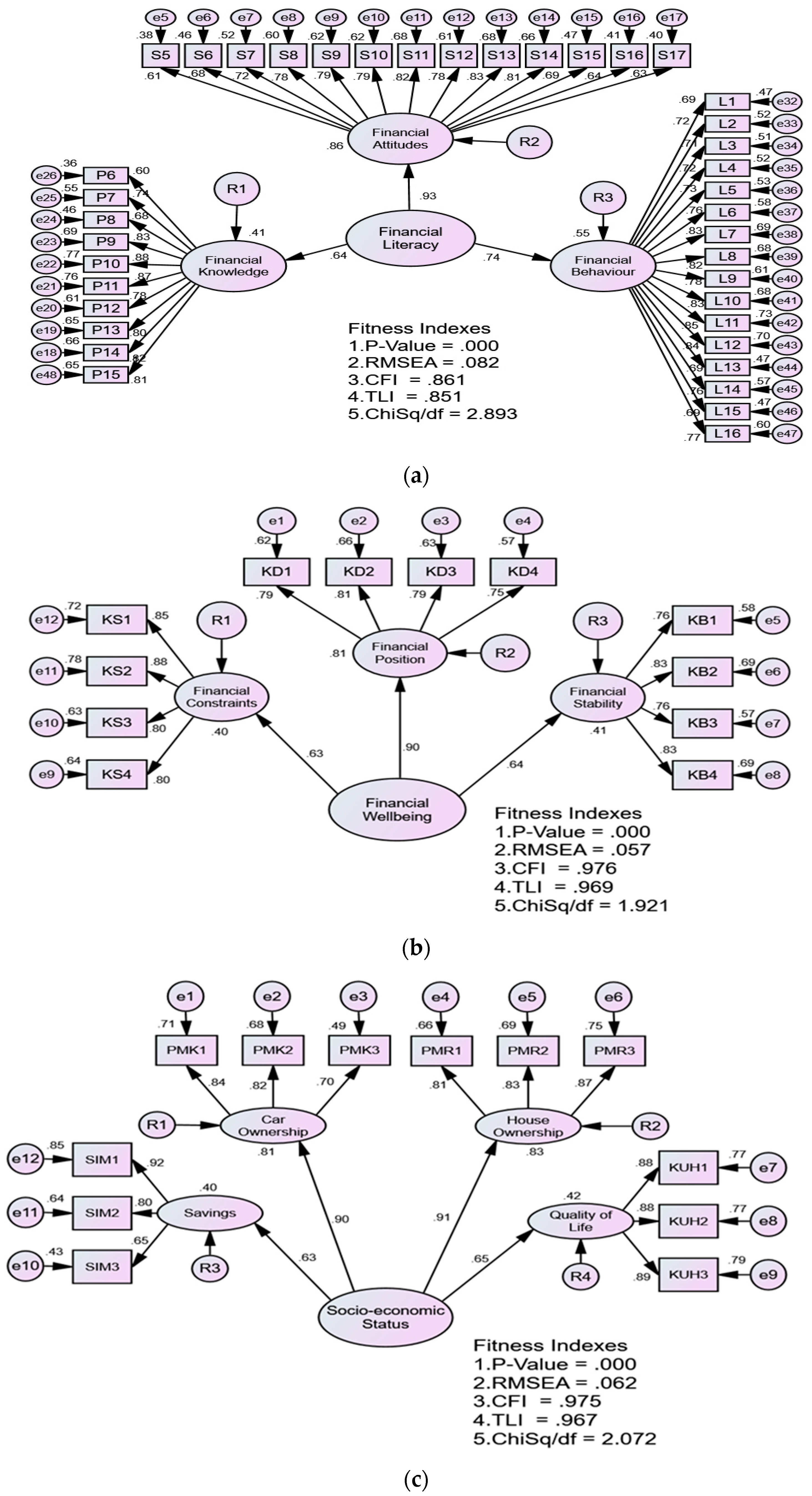

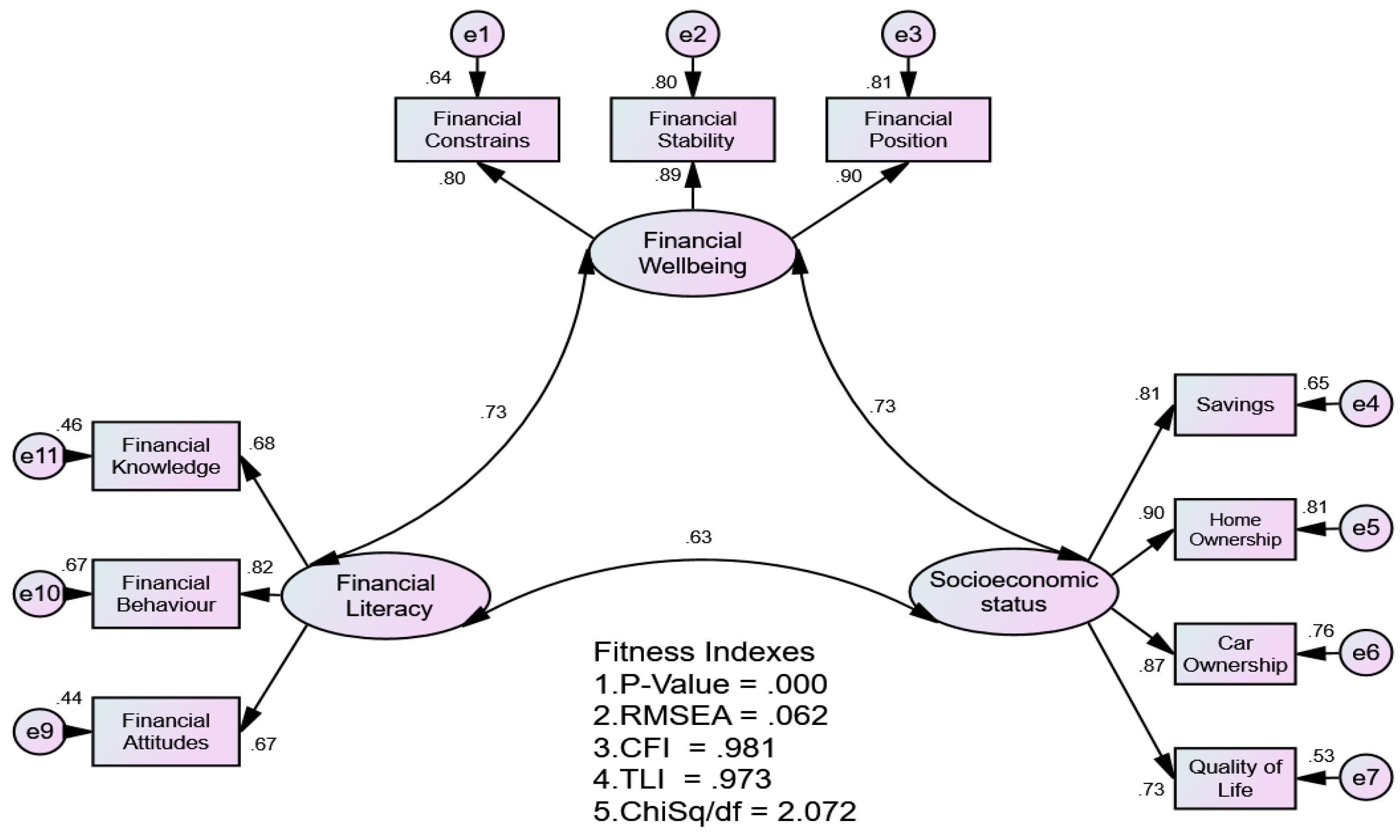

6.1. Assessment of Measurement Model

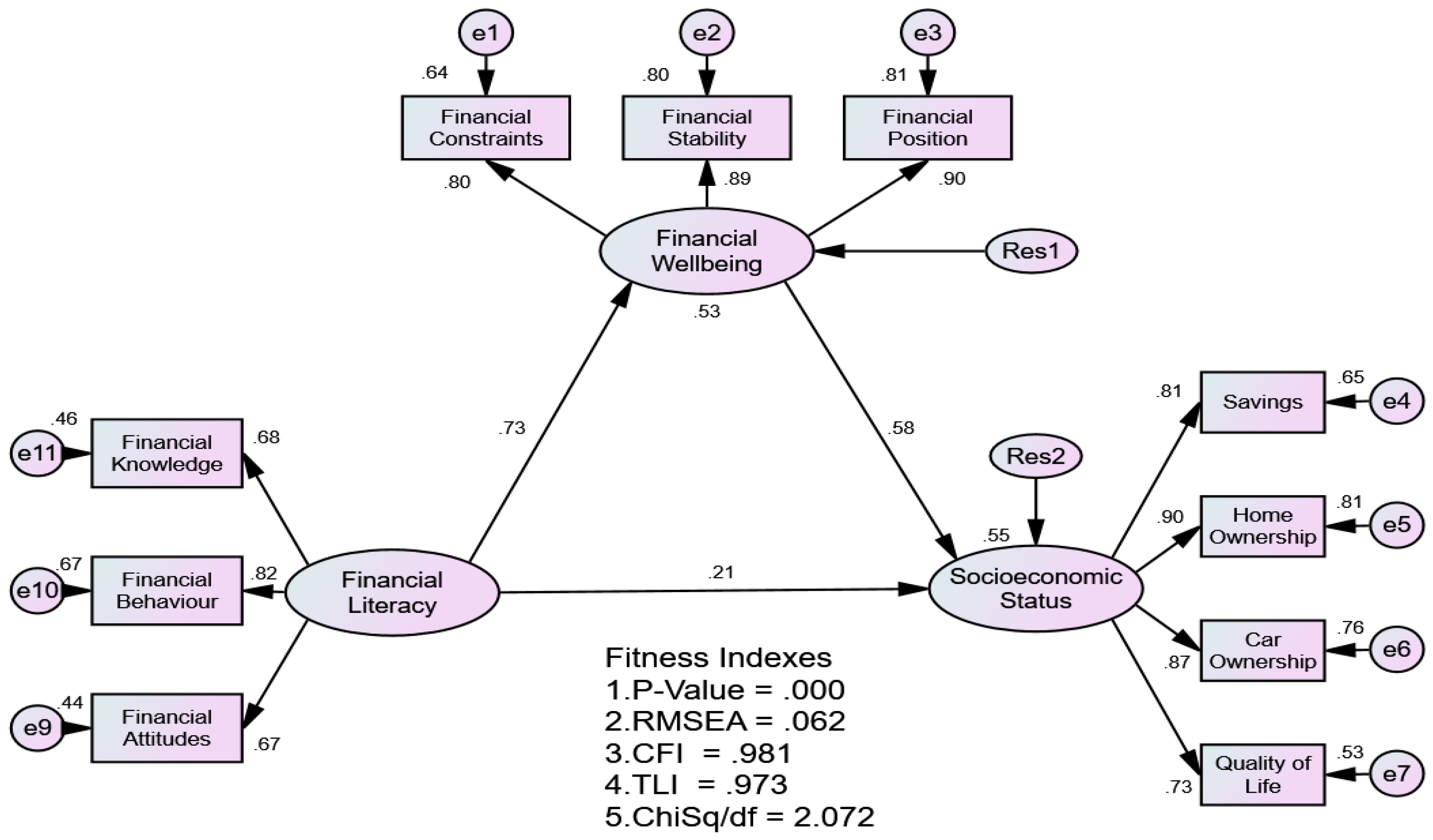

6.2. Assessment of Structural Model

6.3. Hypothesis Testing and Mediation Test

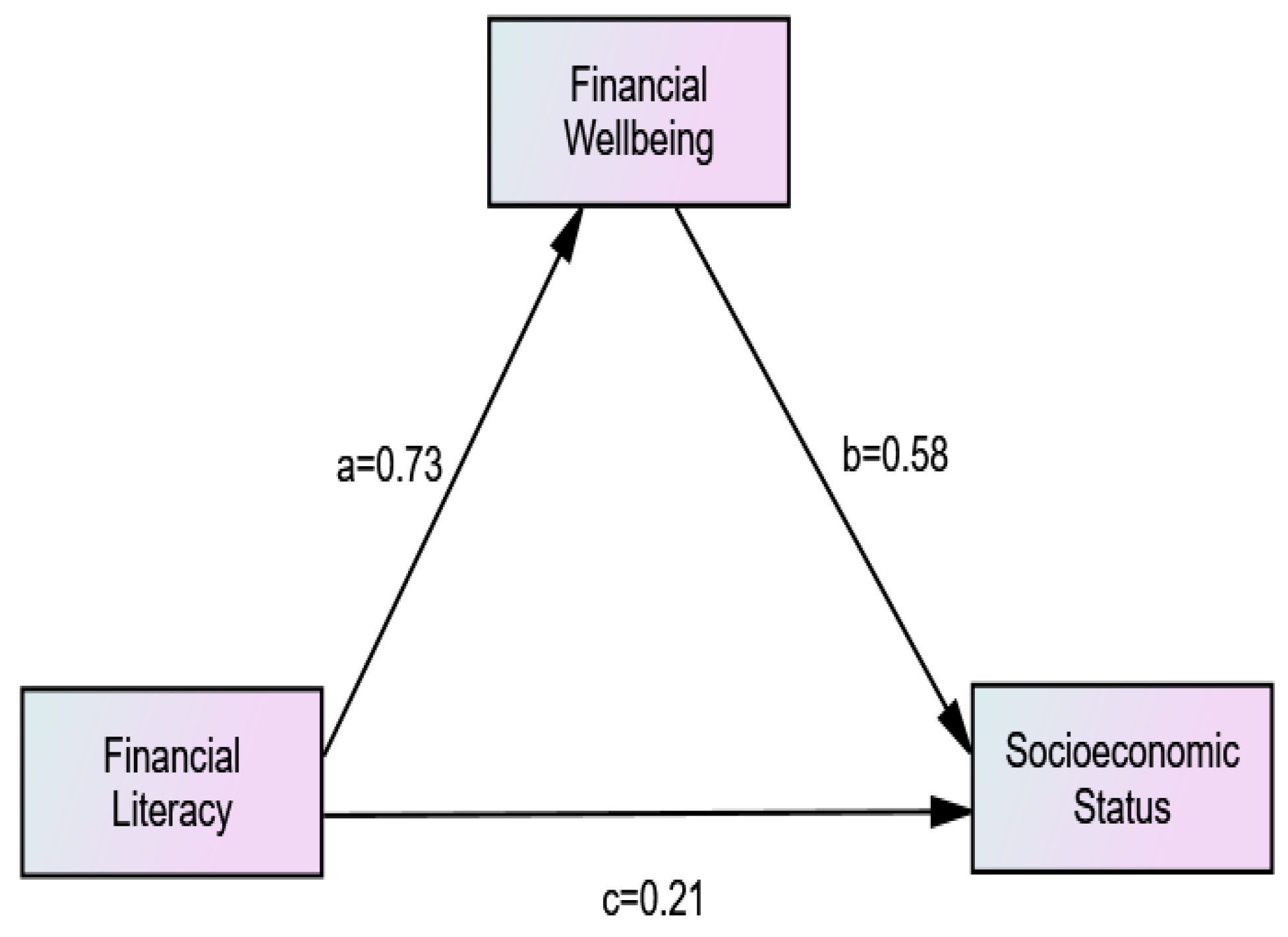

6.4. Results of The Direct and Indirect Effects

- The effect of financial literacy on financial well-being

- 2.

- The effect of financial literacy on the socioeconomic status of B40 households

- 3.

- The effect of financial well-being on the socioeconomic status of B40 households

- 4.

- The mediating role of financial well-being

- Indirect effects, a × b = 0.73 × 0.58 = 0.423

- Direct effects, c = 0.21

- Indirect effects > Direct effects = 0.423 > 0.21

- Both indirect paths a and b are significant.

- The type of mediation is partial mediation because the direct effect of c is significant.

7. Discussion

7.1. Discussion on the Direct Role of Financial Literacy

7.2. Discussion on the Direct Role of Financial Well-Being on the Socioeconomic Status of B40 Households

7.3. Discussion on the Mediating Role of Financial Well-Being

8. Conclusions

9. Practical Implications, Limitations, and Future Research

9.1. Practical Implications

- First, the top-level financial literacy should be improved and the socioeconomic status of B40 households should be developed.

- Second, the government should pay attention to the mechanisms of FL and FWB, as well as the SES of B40 households.

9.2. Limitations and Future Research Directions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Economic Planning Unit (EPU). Elevating B40 Households Towards a Society. Strategy Paper 2, Eleventh Malaysia Plan 2016–2020. 2016. Available online: https://www.epu.gov.my/sites/default/files/2021-05/Strategy%20Paper%2002.pdf (accessed on 31 July 2022).

- Munisamy, M.; Sahid, S.; Hussin, M. Exploratory Factor and Reliability Analysis of Financial Literacy Instrument to Assess Low-Income Groups in Malaysia. J. Soc. Econ. Res. 2022, 9, 39–51. [Google Scholar] [CrossRef]

- Munisamy, M.; Sahid, S.; Hussin, M. Content Validation and Content Validity Index Calculation of B40 Household’s Financial Literacy. Turk. Online J. Qual. Inq. 2021, 12, 1057–1072. [Google Scholar]

- Financial Education Network. National Financial Literacy Strategy. 2019. Available online: https://www.fenetwork.my/about (accessed on 31 July 2022).

- Hassan Sabri, N.I.; Alavi, K. Exploring B40 Youth Financial Planning Literacy Guided by Psychosocial Education. J. Undergrad. Discourse 2019, 3, 1–8. [Google Scholar]

- Kusairi, S.; Sanusi, N.A.; Muhamad, S.; Shukri, M.; Zamri, N. Financial households’ efficacy, risk preference and saving behaviour: Lessons from lower-income households in Malaysia. Econ. Sociol. 2019, 12, 301–318. [Google Scholar] [CrossRef]

- Mayan, S.N.A.; Nor, R.M.; Samat, N. Challenges to the Household Income Class B40 Increase in Developed Country Towards 2020 Case Study: Penang. Int. J. Environ. Soc. Space 2017, 5, 35–41. [Google Scholar]

- Bank of Central Malaysia. Annual Report; Bank of Central Malaysia: Kuala Lumpur, Malaysia, 2020. [Google Scholar]

- Siwar, C.; Ismail, M.K.; Alias, N.A.; Zahari, S.Z. The Bottom 40 per cent income group (B40) in Malaysia: Identifying trends, characteristics, issues and challenges. In B40 Empowerment: Strategic Prosperity and Socioeconomic Implications; UKM Press: Bangi, Malaysia, 2019. [Google Scholar]

- Sawandi, N.; Abu Bakar, A.S.; Shaari, H.; Saad, R.A.; Amran, N.A. Financial literacy among Malaysian: Level of financial knowledge score. J. Soc. Sci. Res. 2018, 6, 300–304. [Google Scholar] [CrossRef] [Green Version]

- Arshat, Z.; Pai, F.H.; Ismail, Z. B40 Family: Stress and Strength. J. Adv. Res. Soc. Behav. Sci. 2018, 10, 91–102. Available online: www.akademiabaru.com/arsbs.html (accessed on 31 July 2022).

- Magesvari, R.; Kenayathulla, H.B.; Ghani, M.F.A. Socioeconomic Factors Influencing the Financial Literacy Skills of Secondary School Students in Negeri Sembilan. Jurnal Kepimpinan Pendidikan 2018, 5, 10–33. Available online: http://e-jpurnal.um.edu.my/publish/JuPiDi (accessed on 31 July 2022).

- OECD. OECD Economic Surveys: Malaysia 2019; OECD: Paris, France, 2019. [Google Scholar] [CrossRef]

- Potrich, A.C.G.; Vieira, K.M.; Mendes-Da-Silva, W.M. Development of a financial literacy model for university students. Manag. Res. Rev. 2016, 39, 356–376. [Google Scholar] [CrossRef]

- Mokhtar, N.; Thinagaran, M.D.; Sabri, M.F.; Ho, C.S.F. A Preliminary Evaluation of Financial Literacy in Malaysia. J. Wealth Manag. Financ. Plan. 2018, 5, 3–16. [Google Scholar]

- Mahdzan, N.S.; Zainudin, R.; Sukor, M.E.A.; Zainir, F.; Wan Ahmad, W.M. Determinants of Subjective Financial Well-Being Across Three Different Household Income Groups in Malaysia. Soc. Indic. Res. 2019, 146, 699–726. [Google Scholar] [CrossRef]

- Azmi, S.N.; Rahman, A.; Ibrahim, S.; Muhammad, N.; Esa, M. Student Financial Management Practices. J. Bus. Innov. 2018, 3, 9–23. [Google Scholar]

- Ab Rani, N.Z.; Ghazali, R.; Siwar, C.; Isa, Z.; Ismail, M.K. The Vulnerability Factor Analysis of B40 Household Income Group in Southern Region of Kelantan using Confirmatory Factor Analysis. Acad. J. Bus. Soc. Sci. 2019, 3, 1–16. [Google Scholar]

- Rashid, N.K.A.; Nasir, A.; Awang, Z.; Alipiah, R.M. Determinants of Muslim household basic needs consumption expenditures. J. Ekon. Malays. 2018, 52, 309–323. [Google Scholar] [CrossRef]

- Krishnakumare, B.; Singh, S. Assessing the Level of Financial Literacy among Rural Households of Tamil Nadu. Ann. Agric. Res. New Ser. 2009, 40, 210–217. [Google Scholar]

- Syukri, M.S.; Farahein, N.; Samat, N. The use of Factor Analysis to Determine the Factors of Peninsular Malaysia. J. Soc. Sci. Humanit. 2018, 16, 1–18. [Google Scholar]

- Nicolini, G.; Haupt, M. The assessment of financial literacy: New evidence from Europe. Int. J. Financ. Stud. 2019, 7, 54. [Google Scholar] [CrossRef] [Green Version]

- Németh, E.; Zsótér, B. Anxious spenders: Background factors of financial vulnerability. Econ. Sociol. 2019, 12, 147–169. [Google Scholar] [CrossRef] [Green Version]

- Maki, M. Financial Literacy and Household Performance in Financial Markets. Soc. Indic. Res. 2019, 132, 799–820. [Google Scholar]

- Sang, L.T. Relationship between Financial Knowledge and Awareness of Life Insurance and Family Takaful. Malays. J. Bus. Econ. 2020, 7, 131–142. [Google Scholar]

- Never, M. Sampling in Research; IGI Global: Hershey, PA, USA, 2016. [Google Scholar] [CrossRef]

- Singh, T.; Sharma, S.; Nagesh, S. Socioeconomic status scales updated for 2017. Int. J. Res. Med. Sci. 2017, 5, 3264. [Google Scholar] [CrossRef] [Green Version]

- Azma Rahlin, N.; Awang, Z.; Zulkifli Abdul Rahim, M.; Suriawaty Bahkia, A. The Impact of Employee Safety Climate on Safety Behavior in Small and Medium Enterprises: An Empirical Study. Humanit. Soc. Sci. Rev. 2020, 8, 163–177. [Google Scholar] [CrossRef]

- Bahkia, A.S.; Awang, Z.; Afthanorhan, A.; Ghazali, P.L.; Foziah, H. Exploratory factor analysis on occupational stress in context of Malaysian sewerage operations. AIP Conf. Proc. 2019, 2138, 050006. [Google Scholar] [CrossRef]

- Shkeer, A.S.; Awang, Z. Exploring the Items for Measuring the Marketing Information System Construct: An Exploratory Factor Analysis. Int. Rev. Manag. Mark. 2019, 9, 87–97. [Google Scholar] [CrossRef] [Green Version]

- Awang, Z.; Hui LAwang, N.F. Sem Made Simple: A Gentle Approach to Learning Structural Equation Modelling; MPWS Rich Publication: Bandar Baru Bangi, Malaysia, 2015; Available online: https://www.semanticscholar.org/paper/SEM-Made-Simple%3A-A-Gentle-Approach-to-Learning-Awang/22fc1f1e889665e413ddef4d9830dcf4bce5576f (accessed on 5 June 2022).

- Al-Mhasnah, A.M.; Salleh, F.; Afthanorhan, A.; Ghazali, P.L. The relationship between services quality and customer satisfaction among Jordanian healthcare sector. Manag. Sci. Lett. 2018, 8, 1413–1420. [Google Scholar] [CrossRef]

- Rosseel, Y. lavaan: An R Package for Structural Equation Modeling. J. Stat. Softw. 2012, 48, 1–36. [Google Scholar] [CrossRef] [Green Version]

- Little, T.D. Longitudinal Structural Equation Modelling; The Guilford Press: New York, NY, USA, 2013. [Google Scholar]

- Mahfouz, J.; Greenberg, M.T.; Rodriguez, A. Principals’ Social and Emotional Competence: A Key Factor for Creating Caring School; The Pennsylvania State University: State College, PA, USA, 2019; Available online: https://www.prevention.psu.edu/uploads/files/PSU-Principals-Brief-103119.pdf (accessed on 5 June 2022).

- Credit Counseling and Management Agency. Financial behaviour and state of financial well-being of Malaysian working adults. In AKPK Financial Behaviour Survey 2018 (AFBeS’18); AKPK: Kuala Lumpur, Malaysia, 2018; Volume 2018. [Google Scholar]

- Chatterjee, S.; Kim, J.; Saerom, C. Emerging Adulthood Milestones, Perceived Capability, and Psychological Well-Being While Transitioning to Adulthood: Evidence from a National Study. Financ. Plan. Rev. 2021, 4, e1132. Available online: https://ssrn.com/abstract=4016442 (accessed on 31 July 2022). [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Household Income Classification | Explanation | Monthly Household Gross Income |

|---|---|---|

| B40 | Lower-income group. Represents 40% of Malaysians. | MYR 1–MYR 4850 |

| M40 | Middle-income group. Represents 40% of Malaysians. | MYR 4851–MYR 10,970 |

| T20 | Upper group. Represents the top 20% of Malaysians. | MYR 10,970 and above |

| Variable | Code | Item Scale |

|---|---|---|

| FINANCIAL LITERACY | ||

| a. Financial Knowledge | FK1 | A budget is part of the financial planning that I need to do. |

| FK2 | A budget guides me to shop according to my ability. | |

| FK3 | My salary or wages earned is also known as income. | |

| FK4 | The setting of interest rates is determined by the bank. | |

| FK5 | The provision of 10% of income for saving is a good idea. | |

| FK6 | Interest or profit rate is a loan condition when we borrow money from banks. | |

| FK7 | The money I have spent is also known as expenses. | |

| FK8 | The budget should contain both income and expenses. | |

| FK9 | When borrowing money from the bank, I will try to get the lowest interest rate. | |

| FK10 | In my opinion, borrowing money from banks can increase costs refunds compared to using existing funds. | |

| FK11 | A purchase using a credit card is the same as being in debt to the bank. | |

| FK12 | An increase in the price of goods reduces the capacity to buy goods. | |

| FK13 | Buying goods regularly through debt will reduce the ability to buy goods (purchasing power) the next time. | |

| FK14 | My family needs to have at least 3 months of savings. | |

| FK15 | Purchase of credit or debit increases my purchasing power. | |

| b. Financial Behavior | FB1 | My purchases are according to life necessities. |

| FB2 | I compare prices before buying products that involve goods and services. | |

| FB3 | I pay the water and electricity bills before the due date. | |

| FB4 | I compare currency exchange rates before purchasing imported goods such as books and magazines. | |

| FB5 | I plan financially for the long term. | |

| FB6 | I avoid financial help from friends when desperate. | |

| FB7 | I always make a budget or balance sheet before making a purchase. | |

| FB8 | I save a fixed amount of money every month. | |

| FB9 | I get information from experienced people before buying something. | |

| FB10 | I often ask about the advantages and disadvantages of the item I want to buy. | |

| FB11 | I make sure that my financial position allows for the purchase of an item. | |

| FB12 | I care about the warranty period of an item. | |

| FB13 | I save a certain amount of money daily. | |

| FB14 | I will list the items to buy first before shopping. | |

| FB15 | I will spend money according to the list of items to be purchased. | |

| FB16 | I always list the expenses made and check back to improve my financial management level. | |

| c. Financial Attitudes | FA1 | I assume that money is to be spent. |

| FA2 | I am more concerned with the needs of the present and not the future. | |

| FA3 | I am more satisfied when money is spent. | |

| FA4 | I do not like to be in debt. | |

| FA5 | I value frugality when buying things. | |

| FA6 | I am more interested in buying used items than new items because used items are cheaper. | |

| FA7 | I wait for a bargain, sale, or promotion before buying something. | |

| FA8 | I would not expect pocket money from my husband/wife if the husband/wife faces financial constraints. | |

| FA9 | I do not want to burden my husband/wife completely in the future. | |

| FA10 | I think money is very important to fill the needs of daily life. | |

| FA11 | I will defer the purchase if I am unable to save during the month. | |

| FA12 | I am willing to reduce my expenses if my spouse has financial problems. | |

| FA13 | I will talk to my husband/wife when facing financial problems. | |

| FA14 | I will make sure all my expenses are within my budget. | |

| FA15 | I think getting into debt is not a good way to solve problems in finances. | |

| FA16 | I am confident that the way I manage my finances will affect my future. | |

| FA17 | The practice of saving is hard to do in my family. | |

| FINANCIAL WELL-BEING | ||

| a. Financial Constraints | FC1 | I am satisfied with my current financial situation. |

| FC2 | I am confident that I have enough money to live comfortably in old age. | |

| FC3 | I am confident that I have control over my finances. | |

| FC4 | I am confident that I know how to manage my finances. | |

| b. Financial Stability | FS1 | I can easily get MYR 1,000 to cover emergency needs. |

| FS2 | I am worried about my financial situation today. | |

| FS3 | I am able to plan my financial aspects well. | |

| FS4 | I am satisfied with my personal financial situation. | |

| c. Financial Position | FP1 | I am confident that my current financial resource situation is stable. |

| FP2 | I often have trouble paying monthly bills (electricity, telephone, instalments). | |

| FP3 | I often run out of money before receiving my next paycheck. | |

| FP4 | I am worried about my overall financial position. | |

| SOCIOECONOMIC STATUS | ||

| 1. Savings | SV1 | My savings are growing now. |

| SV2 | Savings can alleviate the cost of emergency treatment expenses. | |

| SV3 | Savings can alleviate the cost of children’s education expenses. | |

| 2. Home Ownership | HO1 | I am sure I will have my own house later. |

| HO2 | I am more confident about having at least an affordable home. | |

| HO3 | I am confident and able to provide a deposit to buy a house. | |

| 3. Car Ownership | CO1 | I am sure I will have my own car later. |

| CO2 | I am more confident about having a comfortable car. | |

| CO3 | I am confident and able to provide a deposit to buy a car. | |

| 4. Quality of Life | QL1 | My life is more comfortable now than before. |

| QL2 | I was able to meet the daily needs of my family. | |

| QL3 | My family started traveling in the country more than ever before. | |

| Variable | Item | Factor Loading | CR (Above 0.6) | AVE (Above 0.5) |

|---|---|---|---|---|

| Financial Literacy | Financial Knowledge | 0.64 | 0.816 | 0.601 |

| Financial Behavior | 0.92 | |||

| Financial Attitudes | 0.74 | |||

| Financial Knowledge | P6 | 0.60 | 0.945 | 0.635 |

| P7 | 0.74 | |||

| P8 | 0.68 | |||

| P9 | 0.83 | |||

| P10 | 0.89 | |||

| P11 | 0.87 | |||

| P12 | 0.88 | |||

| P13 | 0.80 | |||

| P14 | 0.82 | |||

| P15 | 0.81 | |||

| Financial Behavior | L1 | 0.61 | 0.944 | 0.631 |

| L2 | 0.68 | |||

| L3 | 0.72 | |||

| L4 | 0.78 | |||

| L5 | 0.79 | |||

| L6 | 0.89 | |||

| L7 | 0.82 | |||

| L8 | 0.88 | |||

| L9 | 0.83 | |||

| L10 | 0.81 | |||

| L11 | 0.88 | |||

| L12 | 0.84 | |||

| L13 | 0.63 | |||

| L14 | 0.69 | |||

| L15 | 0.72 | |||

| L16 | 0.71 | |||

| Financial Attitudes | S5 | 0.82 | 0.941 | 0.617 |

| S6 | 0.86 | |||

| S7 | 0.76 | |||

| S8 | 0.83 | |||

| S9 | 0.82 | |||

| S10 | 0.88 | |||

| S11 | 0.83 | |||

| S12 | 0.85 | |||

| S13 | 0.75 | |||

| S14 | 0.69 | |||

| S15 | 0.77 | |||

| S16 | 0.89 | |||

| S17 | 0.77 | |||

| Financial Well-Being | Financial Constraints | 0.63 | 0.773 | 0.539 |

| Financial Position | 0.90 | |||

| Financial Stability | 0.64 | |||

| Financial Constraints | KS1 | 0.85 | 0.901 | 0.694 |

| KS2 | 0.88 | |||

| KS3 | 0.80 | |||

| KS4 | 0.80 | |||

| Financial Position | KD1 | 0.79 | 0.865 | 0.617 |

| KD2 | 0.81 | |||

| KD3 | 0.79 | |||

| KD4 | 0.75 | |||

| Financial Stability | KB1 | 0.76 | 0.873 | 0.633 |

| KB2 | 0.83 | |||

| KB3 | 0.76 | |||

| KB4 | 0.83 | |||

| Socioeconomic Status | Savings | 0.63 | 0.861 | 0.614 |

| Car Ownership | 0.90 | |||

| Home Ownership | 0.91 | |||

| Quality of Life | 0.65 | |||

| Savings | SIM1 | 0.92 | 0.837 | 0.636 |

| SIM2 | 0.80 | |||

| SIM3 | 0.65 | |||

| Car Ownership | PMK1 | 0.84 | 0.831 | 0.623 |

| PMK2 | 0.82 | |||

| PMK3 | 0.70 | |||

| Home Ownership | PMR1 | 0.81 | 0.875 | 0.701 |

| PMR2 | 0.83 | |||

| PMR3 | 0.87 | |||

| Quality of Life | KUH1 | 0.88 | 0.914 | 0.780 |

| KUH2 | 0.88 | |||

| KUH3 | 0.89 |

| Construct | Financial Literacy | Financial Wellbeing | Socioeconomic Status |

|---|---|---|---|

| Financial Literacy | 0.733 | ||

| Financial Wellbeing | 0.730 | 0.860 | |

| Socioeconomic Status | 0.630 | 0.730 | 0.830 |

| Construct | Path | Construct | Estimate | S.E. | C.R. | P | Result |

|---|---|---|---|---|---|---|---|

| Financial Well-being | <--- | Financial Literacy | 0.771 | 0.088 | 8.768 | 0.001 | Significant |

| Socioeconomic Status | <--- | Financial Wellbeing | 0.687 | 0.107 | 6.398 | 0.001 | Significant |

| Socioeconomic Status | <--- | Financial Literacy | 0.264 | 0.112 | 2.356 | 0.018 | Significant |

| Indirect effects (a × b) | Direct effects (c) | |

|---|---|---|

| Estimates from Bootstrap | 0.421 | 0.210 |

| Probability values | 0.002 | 0.023 |

| Test results | Significant | Significant |

| Mediation effect | The mediating effect exists because the direct effect is significant | |

| Types of mediation | Partial mediation exists because the direct effect is significant | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Munisamy, A.; Sahid, S.; Hussin, M. Socioeconomic Sustainability for Low-Income Households: The Mediating Role of Financial Well-Being. Sustainability 2022, 14, 9752. https://doi.org/10.3390/su14159752

Munisamy A, Sahid S, Hussin M. Socioeconomic Sustainability for Low-Income Households: The Mediating Role of Financial Well-Being. Sustainability. 2022; 14(15):9752. https://doi.org/10.3390/su14159752

Chicago/Turabian StyleMunisamy, Ananthan, Sheerad Sahid, and Muhammad Hussin. 2022. "Socioeconomic Sustainability for Low-Income Households: The Mediating Role of Financial Well-Being" Sustainability 14, no. 15: 9752. https://doi.org/10.3390/su14159752