ESG: Research Progress and Future Prospects

Abstract

:1. Introduction

2. Analysis of ESG Literature in Top International Journals

2.1. Method

2.2. Data Collection

2.3. Bibliometric Analysis

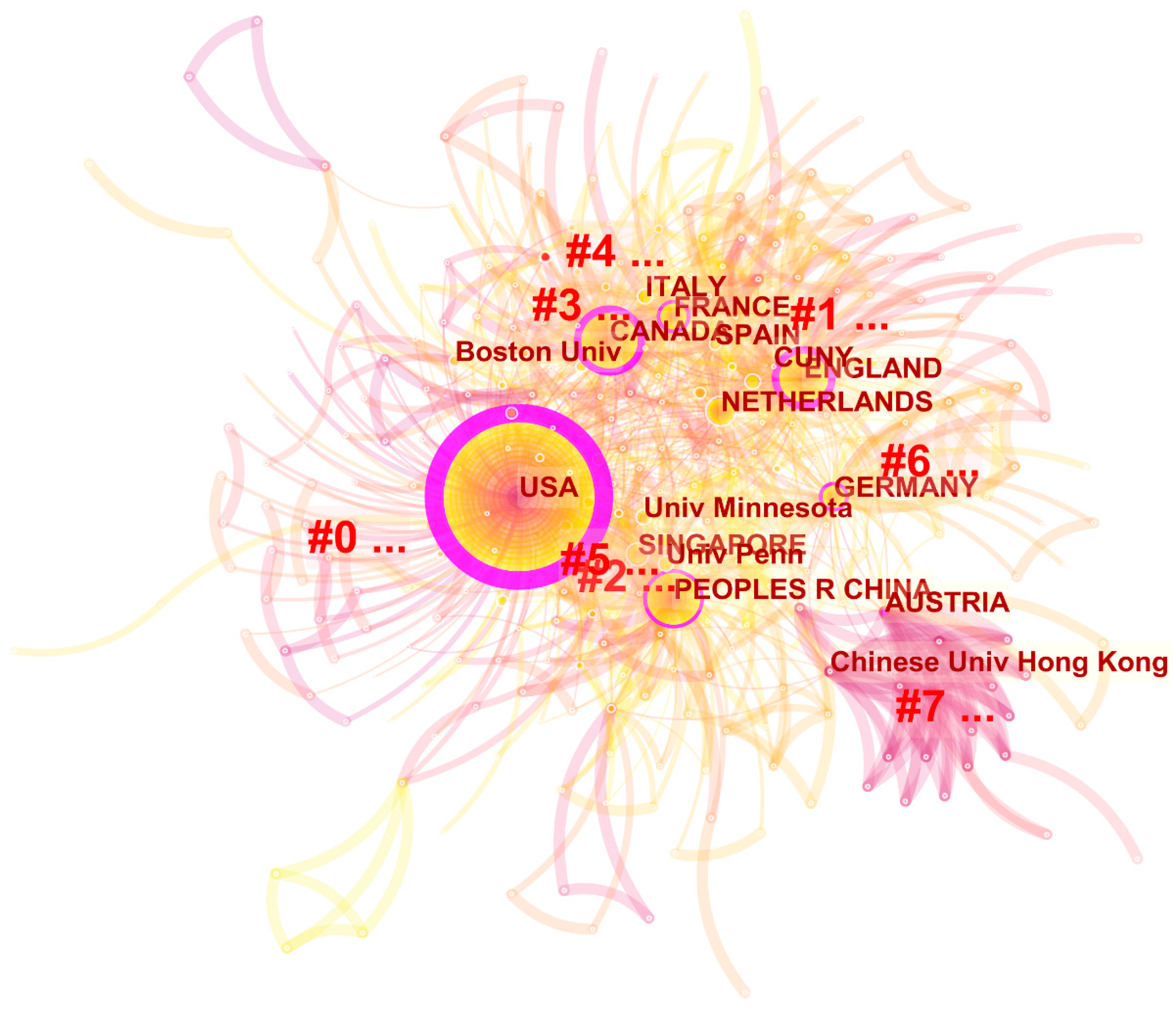

2.3.1. Analysis of Academic Community Collaboration on ESG

- Academic institutions represented by European and American countries have a high level of cooperation.

- 2.

- The cooperation network among scholars is decentralized, and the degree of cooperation is low.

2.3.2. Statistics of Research Hotspots on ESG

2.3.3. Statistics of Research Trend on ESG

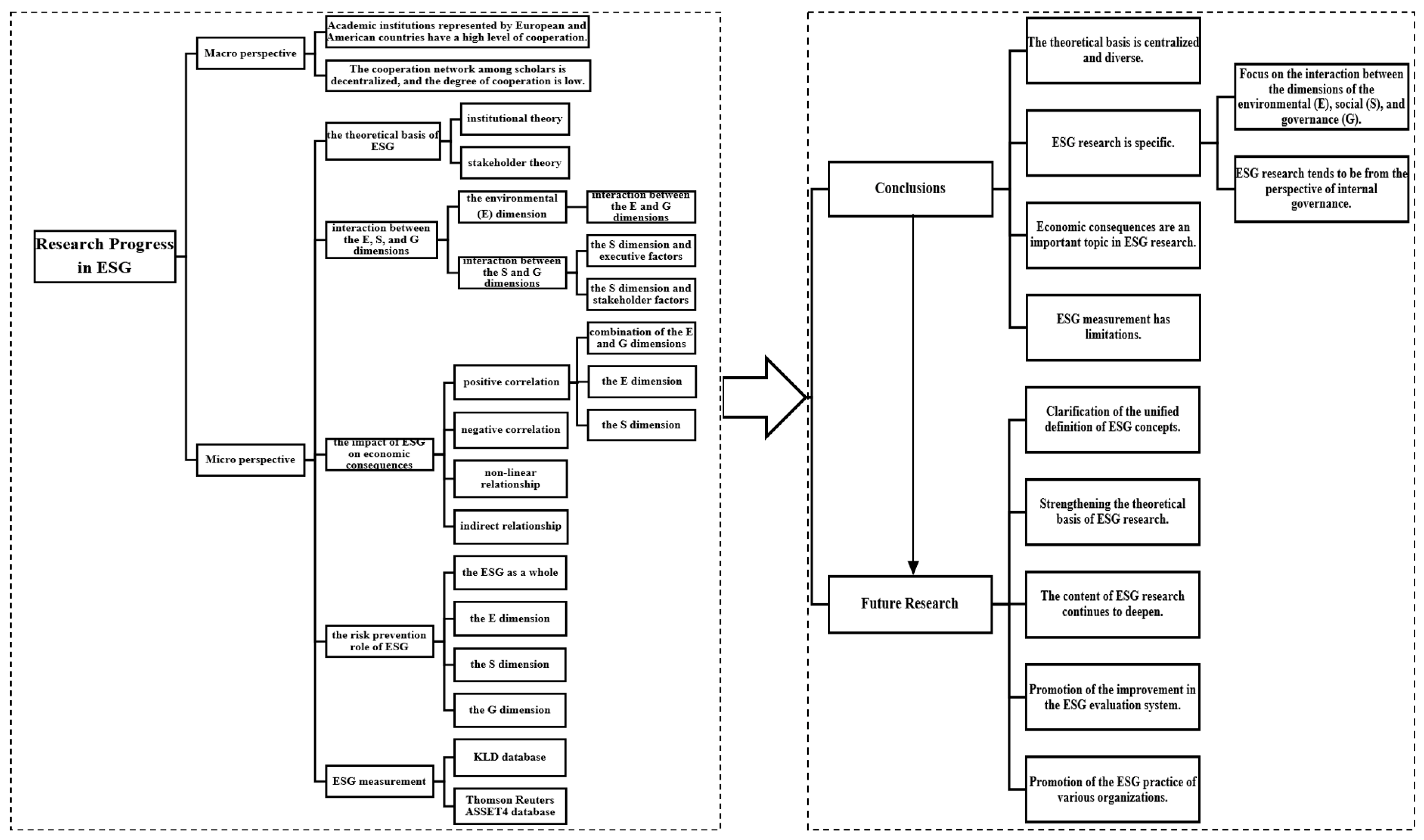

2.4. Analysis of Research Progress in ESG

2.4.1. The Theoretical Basis of ESG

2.4.2. The Interaction between the Environmental (E), Social (S), and Governance (G) Dimensions

- Interaction Research of Environmental (E) Dimension

- 2.

- Interaction between the Social (S) and Governance (G) Dimensions

- (1)

- The Social (S) Dimension and Executive Factors

- (2)

- The Social (S) Dimension and Stakeholder Factors

2.4.3. The Impact of ESG on Economic Consequences

- Positive Correlation

- 2.

- Negative Correlation

- 3.

- Non-Linear Relationship

- 4.

- Indirect Relationship

2.4.4. The Risk Prevention Role of ESG

2.4.5. ESG Measurement

- Measurement based on KLD Database

- 2.

- Measurement based on Thomson Reuters ASSET4 Database

3. Conclusions and Future Research

3.1. Conclusions

3.1.1. The Theoretical Basis Is Centralized and Diverse

3.1.2. ESG Research Is Specific

- Focus on the interaction between the dimensions of the environmental (E), social (S), and governance (G).

- 2.

- ESG research tends to be from the perspective of internal governance.

3.1.3. Economic Consequences Are an Important Topic in ESG Research

3.1.4. ESG Measurement Has Limitations

3.2. Future Research

- Clarification of the unified definition of ESG concepts.

- 2.

- Strengthening the theoretical basis of ESG research.

- 3.

- The content of ESG research continues to deepen.

- 4.

- Promotion of the improvement in the ESG evaluation system.

- 5.

- Promotion of the ESG practice of various organizations.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- EBA. EBA Report on Management and Supervision of ESG Risks for Credit Institutions and Investment Firms. Available online: https://www.eba.europa.eu/sites/default/documents/fifiles/document_library/Publications/Reports/2021/1015656/EBA%20Report%20on%20ESG%20risks%20management%20and%20supervision.pdf (accessed on 31 July 2021).

- PRI. What is Responsible Investment? Available online: https://www.unpri.org/an-introduction-to-responsible-investment/what-is-responsible-investment/4780.article (accessed on 31 July 2021).

- EBA. Environmental Social and Governance Disclosures. Available online: https://www.eba.europa.eu/sites/default/documents/files/document_library/Publications/Consultations/2021/Consultation%20on%20draft%20ITS%20on%20Pillar%20disclosures%20on%20ESG%20risk/963626/Factsheet%20-%20ESG%20disclosures.pdf (accessed on 31 July 2021).

- Daugaard, D. Emerging new themes in environmental, social and governance investing: A systematic literature review. Account. Financ. 2020, 60, 1501–1530. [Google Scholar] [CrossRef]

- Widyawati, L. A systematic literature review of socially responsible investment and environmental social governance metrics. Bus. Strateg. Environ. 2020, 29, 619–637. [Google Scholar] [CrossRef]

- Drempetic, S.; Klein, C.; Zwergel, B. The influence of firm size on the ESG score: Corporate sustainability ratings under review. J. Bus. Ethics 2020, 167, 333–360. [Google Scholar] [CrossRef]

- Eccles, N.S.; Viviers, S. The origins and meanings of names describing investment practices that integrate a consideration of ESG issues in the academic literature. J. Bus. Ethics 2011, 104, 389–402. [Google Scholar] [CrossRef]

- Ziolo, M.; Filipiak, B.Z.; Bak, I.; Cheba, K. How to design more sustainable financial systems: The roles of environmental, social, and governance factors in the decision-making process. Sustainability 2019, 11, 5604. [Google Scholar] [CrossRef] [Green Version]

- Yoshikawa, T.; Nippa, M.; Chua, G. Global shift towards stakeholder-oriented corporate governance? Evidence from the scholarly literature and future research opportunities. Multinatl. Bus. Rev. 2021, 29, 321–347. [Google Scholar] [CrossRef]

- Aluchna, M.; Roszkowska-Menkes, M. Integrating corporate social responsibility and corporate governance at the company level. Towards a conceptual model. Eng. Econ. 2019, 30, 349–361. [Google Scholar] [CrossRef] [Green Version]

- Garcia, A.S.; Mendes-Da-Silva, W.; Orsato, R.J. Sensitive industries produce better ESG performance: Evidence from emerging markets. J. Clean. Prod. 2017, 150, 135–147. [Google Scholar] [CrossRef]

- Chatterji, A.K.; Toffel, M.W. How firms respond to being rated. Strateg. Manag. J. 2010, 31, 917–945. [Google Scholar] [CrossRef]

- Jayachandran, S.; Kalaignanam, K.; Eilert, M. Product and environmental social performance: Varying effect on firm performance. Strateg. Manag. J. 2013, 34, 1255–1264. [Google Scholar] [CrossRef]

- Koh, P.-S.; Qian, C.; Wang, H. Firm litigation risk and the insurance value of corporate social performance. Strateg. Manag. J. 2014, 35, 1464–1482. [Google Scholar] [CrossRef]

- Flammer, C.; Hong, B.; Minor, D. Corporate governance and the rise of integrating corporate social responsibility criteria in executive compensation: Effectiveness and implications for firm outcomes. Strateg. Manag. J. 2019, 40, 1097–1122. [Google Scholar] [CrossRef]

- Kölbel, J.F.; Busch, T.; Jancso, L.M. How media coverage of corporate social irresponsibility increases financial risk. Strateg. Manag. J. 2017, 38, 2266–2284. [Google Scholar] [CrossRef]

- Surroca, J.; Tribó, J.A.; Waddock, S. Corporate responsibility and financial performance: The role of intangible resources. Strateg. Manag. J. 2010, 31, 463–490. [Google Scholar] [CrossRef]

- Muller, A.; Kräussl, R. Doing good deeds in times of need: A strategic perspective on corporate disaster donations. Strateg. Manag. J. 2011, 32, 911–929. [Google Scholar] [CrossRef]

- Flammer, C.; Kacperczyk, A. Corporate social responsibility as a defense against knowledge spillovers: Evidence from the inevitable disclosure doctrine. Strateg. Manag. J. 2019, 40, 1243–1267. [Google Scholar] [CrossRef]

- Davidson, R.H.; Dey, A.; Smith, A.J. CEO materialism and corporate social responsibility. Account. Rev. 2019, 94, 101–126. [Google Scholar] [CrossRef]

- Cheng, B.; Ioannou, I.; Serafeim, G. Corporate social responsibility and access to finance. Strateg. Manag. J. 2014, 35, 1–23. [Google Scholar] [CrossRef]

- Kim, Y.; Park, M.S.; Wier, B. Is earnings quality associated with corporate social responsibility? Account. Rev. 2012, 87, 761–796. [Google Scholar] [CrossRef]

- Gao, F.; Lisic, L.L.; Zhang, I.X. Commitment to social good and insider trading. J. Account. Econ. 2014, 57, 149–175. [Google Scholar] [CrossRef]

- Hubbard, T.D.; Christensen, D.M.; Graffin, S.D. Higher highs and lower lows: The role of corporate social responsibility in CEO dismissal. Strateg. Manag. J. 2017, 38, 2255–2265. [Google Scholar] [CrossRef]

- Fu, R.; Tang, Y.; Chen, G. Chief sustainability officers and corporate social (Ir)responsibility. Strateg. Manag. J. 2020, 41, 656–680. [Google Scholar] [CrossRef]

- Tang, Y.; Qian, C.; Chen, G.; Shen, R. How CEO hubris affects corporate social (ir)responsibility. Strateg. Manag. J. 2015, 36, 1338–1357. [Google Scholar] [CrossRef]

- Petrenko, O.V.; Aime, F.; Ridge, J.; Hill, A. Corporate social responsibility or CEO narcissism? CSR motivations and organizational performance. Strateg. Manag. J. 2016, 37, 262–279. [Google Scholar] [CrossRef]

- Tang, Y.; Mack, D.Z.; Chen, G. The differential effects of CEO narcissism and hubris on corporate social responsibility. Strateg. Manag. J. 2018, 39, 1370–1387. [Google Scholar] [CrossRef]

- Hafenbrädl, S.; Waeger, D. Ideology and the micro-foundations of CSR: Why executives believe in the business case for CSR and how this affects their CSR engagements. Acad. Manag. J. 2017, 60, 1582–1606. [Google Scholar] [CrossRef]

- Chin, M.K.; Hambrick, D.C.; Treviño, L.K. Political ideologies of CEOs: The influence of executives’ values on corporate social responsibility. Adm. Sci. Q. 2013, 58, 197–232. [Google Scholar] [CrossRef]

- Gupta, A.; Nadkarni, S.; Mariam, M. Dispositional sources of managerial discretion: CEO ideology, CEO personality, and firm strategies. Adm. Sci. Q. 2019, 64, 855–893. [Google Scholar] [CrossRef]

- Gupta, A.; Fung, A.; Murphy, C. Out of character: CEO political ideology, peer influence, and adoption of CSR executive position by Fortune 500 firms. Strateg. Manag. J. 2021, 42, 529–557. [Google Scholar] [CrossRef]

- Kang, J. Labor market evaluation versus legacy conservation: What factors determine retiring CEOs’ decisions about long-term investment? Strateg. Manag. J. 2016, 37, 389–405. [Google Scholar] [CrossRef]

- Lai, S.; Li, Z.; Yang, Y.G. East, west, home’s best: Do local CEOs behave less myopically? Account. Rev. 2020, 95, 227–255. [Google Scholar] [CrossRef]

- Bertrand, O.; Betschinger, M.-A.; Moschieri, C. Are firms with foreign CEOs better citizens? A study of the impact of CEO foreignness on corporate social performance. J. Int. Bus. Stud. 2021, 52, 525–543. [Google Scholar] [CrossRef]

- Church, B.K.; Jiang, W.; Kuang, X.; Vitalis, A. A dollar for a tree or a tree for a dollar? The behavioral effects of measurement basis on managers’ CSR investment decision. Account. Rev. 2019, 94, 117–137. [Google Scholar] [CrossRef]

- Han, Q.; Jennings, J.E.; Liu, R.; Jennings, P.D. Going home and helping out? Returnees as propagators of CSR in an emerging economy. J. Int. Bus. Stud. 2019, 50, 857–872. [Google Scholar] [CrossRef]

- Luo, J.; Chen, J.; Chen, D. Coming back and giving back: Transposition, institutional actors, and the paradox of peripheral influence. Adm. Sci. Q. 2021, 66, 133–176. [Google Scholar] [CrossRef]

- Li, S.; Lu, J.W. A dual-agency model of firm CSR in response to institutional pressure: Evidence from Chinese publicly listed firms. Acad. Manag. J. 2020, 63, 2004–2032. [Google Scholar] [CrossRef]

- Madsen, P.M.; Rodgers, Z.J. Looking good by doing good: The antecedents and consequences of stakeholder attention to corporate disaster relief. Strateg. Manag. J. 2015, 36, 776–794. [Google Scholar] [CrossRef]

- Flammer, C.; Luo, J. Corporate social responsibility as an employee governance tool: Evidence from a quasi-experiment. Strateg. Manag. J. 2017, 38, 163–183. [Google Scholar] [CrossRef]

- Balakrishnan, R.; Sprinkle, G.B.; Williamson, M.G. Contracting benefits of corporate giving: An experimental investigation. Account. Rev. 2011, 86, 1887–1907. [Google Scholar] [CrossRef]

- Carnahan, S.; Kryscynski, D.; Olson, D. When does corporate social responsibility reduce employee turnover? Evidence from attorneys before and after 9/11. Acad. Manag. J. 2017, 60, 1932–1962. [Google Scholar] [CrossRef]

- Farooq, O.; Rupp, D.E.; Farooq, M. The multiple pathways through which internal and external corporate social responsibility influence organizational identification and multifoci outcomes: The moderating role of cultural and social orientations. Acad. Manag. J. 2017, 60, 954–985. [Google Scholar] [CrossRef]

- Elliott, W.B.; Jackson, K.E.; Peecher, M.E.; White, B.J. The unintended effect of corporate social responsibility performance on investors’ estimates of fundamental value. Account. Rev. 2014, 89, 275–302. [Google Scholar] [CrossRef] [Green Version]

- Muller, A.R.; Pfarrer, M.D.; Little, L.M. A theory of collective empathy in corporate philanthropy decisions. Acad. Manag. Rev. 2014, 39, 1–21. [Google Scholar] [CrossRef] [Green Version]

- Gupta, A.; Briscoe, F.; Hambrick, D.C. Red, blue, and purple firms: Organizational political ideology and corporate social responsibility. Strateg. Manag. J. 2017, 38, 1018–1040. [Google Scholar] [CrossRef]

- Mun, E.; Jung, J. Change above the glass ceiling: Corporate social responsibility and gender diversity in Japanese firms. Adm. Sci. Q. 2018, 63, 409–440. [Google Scholar] [CrossRef]

- Naughton, J.P.; Wang, C.; Yeung, I. Investor sentiment for corporate social performance. Account. Rev. 2019, 94, 401–420. [Google Scholar] [CrossRef]

- Khan, M.; Serafeim, G.; Yoon, A. Corporate sustainability: First evidence on materiality. Account. Rev. 2016, 91, 1697–1724. [Google Scholar] [CrossRef] [Green Version]

- Awaysheh, A.; Heron, R.A.; Perry, T.; Wilson, J.I. On the relation between corporate social responsibility and financial performance. Strateg. Manag. J. 2020, 41, 965–987. [Google Scholar] [CrossRef]

- Mackey, A.; Mackey, T.B.; Barney, J.B. Corporate social responsibility and firm performance: Investor preferences and corporate strategies. Acad. Manag. Rev. 2007, 32, 817–835. [Google Scholar] [CrossRef]

- Barnett, M.L.; Salomon, R.M. Beyond dichotomy: The curvilinear relationship between social responsibility and financial performance. Strateg. Manag. J. 2006, 27, 1101–1122. [Google Scholar] [CrossRef]

- Matsumura, E.M.; Prakash, R.; Vera-Muñoz, S.C. Firm-value effects of carbon emissions and carbon disclosures. Account. Rev. 2014, 89, 695–724. [Google Scholar] [CrossRef]

- Godfrey, P.C. The relationship between corporate philanthropy and shareholder wealth: A risk management perspective. Acad. Manag. Rev. 2005, 30, 777–798. [Google Scholar] [CrossRef] [Green Version]

- Wang, H.; Qian, C. Corporate philanthropy and corporate financial performance: The roles of stakeholder response and political access. Acad. Manag. J. 2011, 54, 1159–1181. [Google Scholar] [CrossRef]

- Kaul, A.; Luo, J. An economic case for CSR: The comparative efficiency of for-Profit firms in meeting consumer demand for social goods. Strateg. Manag. J. 2018, 39, 1650–1677. [Google Scholar] [CrossRef]

- Manchiraju, H.; Rajgopal, S. Does corporate social responsibility (CSR) create shareholder value? Evidence from the Indian companies Act 2013. J. Account. Res. 2017, 55, 1257–1300. [Google Scholar] [CrossRef]

- Chen, Y.-C.; Hung, M.; Wang, Y. The effect of mandatory CSR disclosure on firm profitability and social externalities: Evidence from China. J. Account. Econ. 2018, 65, 169–190. [Google Scholar] [CrossRef]

- Barnett, M.L.; Salomon, R.M. Does it pay to be really good? Addressing the shape of the relationship between social and financial performance. Strateg. Manag. J. 2012, 33, 1304–1320. [Google Scholar] [CrossRef]

- Zhao, X.; Murrell, A.J. Revisiting the corporate social performance-financial performance link: A replication of Waddock and Graves. Strateg. Manag. J. 2016, 37, 2378–2388. [Google Scholar] [CrossRef]

- Hull, C.E.; Rothenberg, S. Firm performance: The interactions of corporate social performance with innovation and industry differentiation. Strateg. Manag. J. 2008, 29, 781–789. [Google Scholar] [CrossRef]

- Ramchander, S.; Schwebach, R.G.; Staking, K. The informational relevance of corporate social responsibility: Evidence from DS400 index reconstitutions. Strateg. Manag. J. 2012, 33, 303–314. [Google Scholar] [CrossRef]

- Lys, T.; Naughton, J.P.; Wang, C. Signaling through corporate accountability reporting. J. Account. Econ. 2015, 60, 56–72. [Google Scholar] [CrossRef] [Green Version]

- Hawn, O.; Ioannou, I. Mind the gap: The interplay between external and internal actions in the case of corporate social responsibility. Strateg. Manag. J. 2016, 37, 2569–2588. [Google Scholar] [CrossRef] [Green Version]

- Surroca, J.A.; Aguilera, R.V.; Desender, K.; Tribó, J.A. Is managerial entrenchment always bad and corporate social responsibility always good? A cross-national examination of their combined influence on shareholder value. Strateg. Manag. J. 2020, 41, 891–920. [Google Scholar] [CrossRef]

- Mithani, M.A. Liability of foreignness, natural disasters, and corporate philanthropy. J. Int. Bus. Stud. 2017, 48, 941–963. [Google Scholar] [CrossRef] [Green Version]

- Zhou, N.; Wang, H. Foreign subsidiary CSR as a buffer against parent firm reputation risk. J. Int. Bus. Stud. 2020, 51, 1256–1282. [Google Scholar] [CrossRef]

- Flammer, C. Corporate social responsibility and shareholder reaction: The environmental awareness of investors. Acad. Manag. J. 2013, 56, 758–781. [Google Scholar] [CrossRef] [Green Version]

- Shiu, Y.-M.; Yang, S.-L. Does engagement in corporate social responsibility provide strategic insurance-like effects? Strateg. Manag. J. 2017, 38, 455–470. [Google Scholar] [CrossRef]

- Jia, Y.; Gao, X.; Julian, S. Do firms use corporate social responsibility to insure against stock price risk? Evidence from a natural experiment. Strateg. Manag. J. 2020, 41, 290–307. [Google Scholar] [CrossRef]

- Kim, S.; Lee, G.; Kang, H.G. Risk management and corporate social responsibility. Strateg. Manag. J. 2021, 42, 202–230. [Google Scholar] [CrossRef]

- Chatterji, A.K.; Durand, R.; Levine, D.I.; Touboul, S. Do ratings of firms converge? Implications for managers, investors and strategy researchers. Strateg. Manag. J. 2016, 37, 1597–1614. [Google Scholar] [CrossRef]

- Deckop, J.R.; Merriman, K.K.; Gupta, S. The effects of CEO pay structure on corporate social performance. J. Manag. 2006, 32, 329–342. [Google Scholar] [CrossRef]

- Ioannou, I.; Serafeim, G. The impact of corporate social responsibility on investment recommendations: Analysts’ perceptions and shifting institutional logics. Strateg. Manag. J. 2015, 36, 1053–1081. [Google Scholar] [CrossRef] [Green Version]

- Kacperczyk, A. With greater power comes greater responsibility? Takeover protection and corporate attention to stakeholders. Strateg. Manag. J. 2009, 30, 261–285. [Google Scholar] [CrossRef] [Green Version]

- Lee, D. Corporate social responsibility of U.S.-listed firms headquartered in tax havens. Strateg. Manag. J. 2020, 41, 1547–1571. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Dimension | Factors | Definition |

|---|---|---|

| Environmental (E) |

| Environmental matters that may have a positive or negative impact on the financial performance or solvency of an entity, sovereign, or individual. |

| Social (S) |

| Social matters that may have a positive or negative impact on the financial performance or solvency of an entity, sovereign, or individual. |

| Governance (G) |

| Governance matters that may have a positive or negative impact on the financial performance or solvency of an entity, sovereign, or individual. |

| No. | Freq | Centrality | Year | Keywords | No. | Freq | Centrality | Year | Keywords |

|---|---|---|---|---|---|---|---|---|---|

| 1 | 234 | 0.08 | 2004 | corporate social responsibility | 26 | 22 | 0.04 | 2005 | green |

| 2 | 140 | 0.06 | 2004 | performance | 27 | 22 | 0.03 | 2004 | company |

| 3 | 125 | 0.07 | 2007 | sustainability | 28 | 21 | 0.01 | 2009 | reputation |

| 4 | 113 | 0.08 | 2004 | management | 29 | 20 | 0.09 | 2004 | competitive advantage |

| 5 | 83 | 0.06 | 2006 | financial performance | 30 | 20 | 0.06 | 2009 | construction |

| 6 | 80 | 0.16 | 2004 | firm | 31 | 19 | 0.06 | 2008 | capability |

| 7 | 80 | 0.12 | 2004 | impact | 32 | 19 | 0.04 | 2012 | determinant |

| 8 | 80 | 0.06 | 2007 | social responsibility | 33 | 19 | 0.02 | 2016 | CSR |

| 9 | 74 | 0.07 | 2006 | governance | 34 | 19 | 0.02 | 2007 | stakeholder theory |

| 10 | 71 | 0.1 | 2007 | strategy | 35 | 18 | 0.03 | 2011 | resource based view |

| 11 | 61 | 0.07 | 2005 | organization | 36 | 18 | 0.03 | 2009 | choice |

| 12 | 61 | 0.06 | 2004 | model | 37 | 18 | 0.02 | 2012 | corporate governance |

| 13 | 44 | 0.07 | 2006 | perspective | 38 | 17 | 0.06 | 2005 | industry |

| 14 | 38 | 0.13 | 2004 | behavior | 39 | 17 | 0.03 | 2010 | competition |

| 15 | 37 | 0.04 | 2007 | business | 40 | 16 | 0.04 | 2006 | environment |

| 16 | 33 | 0.04 | 2005 | market | 41 | 16 | 0.03 | 2012 | ownership |

| 17 | 33 | 0.02 | 2006 | responsibility | 42 | 16 | 0.02 | 2016 | financial performance |

| 18 | 30 | 0.02 | 2010 | firm performance | 43 | 15 | 0.06 | 2006 | consumer |

| 19 | 29 | 0.03 | 2011 | shareholder value | 44 | 15 | 0.02 | 2009 | information |

| 20 | 29 | 0.03 | 2007 | innovation | 45 | 15 | 0.01 | 2015 | philanthropy |

| 21 | 27 | 0.06 | 2008 | cost | 46 | 15 | 0 | 2016 | disclosure |

| 22 | 27 | 0.04 | 2011 | identity | 47 | 14 | 0.02 | 2012 | work |

| 23 | 27 | 0.03 | 2005 | legitimacy | 48 | 14 | 0.02 | 2010 | environmental performance |

| 24 | 24 | 0.01 | 2013 | risk | 49 | 14 | 0.01 | 2017 | firm value |

| 25 | 23 | 0.02 | 2011 | institutional theory | 50 | 14 | 0 | 2015 | self-regulation |

| No. | Freq | Centrality | Year | Keywords | No. | Freq | Centrality | Year | Keywords |

|---|---|---|---|---|---|---|---|---|---|

| 1 | 80 | 0.16 | 2004 | firm | 26 | 19 | 0.04 | 2012 | determinant |

| 2 | 38 | 0.13 | 2004 | behavior | 27 | 16 | 0.04 | 2006 | environment |

| 3 | 80 | 0.12 | 2004 | impact | 28 | 13 | 0.04 | 2005 | framework |

| 4 | 71 | 0.1 | 2007 | strategy | 29 | 9 | 0.04 | 2004 | consequence |

| 5 | 20 | 0.09 | 2004 | competitive advantage | 30 | 29 | 0.03 | 2011 | shareholder value |

| 6 | 234 | 0.08 | 2004 | corporate social responsibility | 31 | 29 | 0.03 | 2007 | innovation |

| 7 | 113 | 0.08 | 2004 | management | 32 | 27 | 0.03 | 2005 | legitimacy |

| 8 | 125 | 0.07 | 2007 | sustainability | 33 | 22 | 0.03 | 2004 | company |

| 9 | 74 | 0.07 | 2006 | governance | 34 | 18 | 0.03 | 2011 | resource based view |

| 10 | 61 | 0.07 | 2005 | organization | 35 | 18 | 0.03 | 2009 | choice |

| 11 | 44 | 0.07 | 2006 | perspective | 36 | 17 | 0.03 | 2010 | competition |

| 12 | 140 | 0.06 | 2004 | performance | 37 | 16 | 0.03 | 2012 | ownership |

| 13 | 83 | 0.06 | 2006 | financial performance | 38 | 12 | 0.03 | 2005 | quality |

| 14 | 80 | 0.06 | 2007 | social responsibility | 39 | 12 | 0.03 | 2008 | knowledge |

| 15 | 61 | 0.06 | 2004 | model | 40 | 11 | 0.03 | 2009 | response |

| 16 | 27 | 0.06 | 2008 | cost | 41 | 10 | 0.03 | 2015 | social movement |

| 17 | 20 | 0.06 | 2009 | construction | 42 | 9 | 0.03 | 2006 | product |

| 18 | 19 | 0.06 | 2008 | capability | 43 | 7 | 0.03 | 2006 | alliance |

| 19 | 17 | 0.06 | 2005 | industry | 44 | 6 | 0.03 | 2005 | commitment |

| 20 | 15 | 0.06 | 2006 | consumer | 45 | 33 | 0.02 | 2006 | responsibility |

| 21 | 7 | 0.06 | 2006 | altruism | 46 | 30 | 0.02 | 2010 | firm performance |

| 22 | 37 | 0.04 | 2007 | business | 47 | 23 | 0.02 | 2011 | institutional theory |

| 23 | 33 | 0.04 | 2005 | market | 48 | 19 | 0.02 | 2016 | CSR |

| 24 | 27 | 0.04 | 2011 | identity | 49 | 19 | 0.02 | 2007 | stakeholder theory |

| 25 | 22 | 0.04 | 2005 | green | 50 | 18 | 0.02 | 2012 | Corporate governance |

| Keywords | Strength | Begin | End | Duration | 2004–2020 |

|---|---|---|---|---|---|

| company | 4.36 | 2004 | 2009 | 5 |  |

| framework | 4.31 | 2005 | 2014 | 9 |  |

| technology | 3.98 | 2006 | 2010 | 4 |  |

| perspective | 3.37 | 2006 | 2009 | 3 |  |

| altruism | 3.14 | 2006 | 2012 | 6 |  |

| capability | 2.99 | 2008 | 2011 | 3 |  |

| competition | 3.66 | 2010 | 2013 | 3 |  |

| consumption | 3.17 | 2012 | 2013 | 1 |  |

| choice | 3.07 | 2012 | 2013 | 1 | |

| stakeholder theory | 2.97 | 2012 | 2013 | 1 | |

| organization | 3.28 | 2013 | 2014 | 1 |  |

| philanthropy | 4.63 | 2015 | 2018 | 3 |  |

| self-regulation | 4.32 | 2015 | 2018 | 3 | |

| standard | 3 | 2015 | 2016 | 1 |  |

| financial performance | 4.75 | 2016 | 2017 | 1 |  |

| firm value | 3.67 | 2017 | 2020 | 3 |  |

| moderating role | 3.2 | 2018 | 2020 | 2 |  |

| incentive | 3.18 | 2018 | 2020 | 2 | |

| director | 2.91 | 2018 | 2020 | 2 | |

| Databases | Advantages | Disadvantages | Measurement | Scoring | Sources |

|---|---|---|---|---|---|

| KLD Database |

| / | Cumulative Addition | By accumulating all of the “strengths” items of KLD related to the research. | Lee, D. Corporate social responsibility of U.S.-listed firms headquartered in tax havens. Strateg. Manag. J. 2020, 41(9), 1547–1571. [77], etc. |

| Net Score | By accumulating the total “strengths” and the total “concerns” and calculating the difference between the them. | Jia, Y.; Gao, X.; Julian, S. Do firms use corporate social responsibility to insure against stock price risk? Evidence from a natural experiment. Strateg. Manag. J. 2020, 41(2), 290–307. [71], etc. | |||

| Thomson Reuters ASSET4 Database | Comprehensive data, focusing on finance, environment, society, and governance. |

| Measuring ESG as a whole usually uses annual environmental, social, and governance scores and constructs a corporate social responsibility index by assigning equal weight to each pillar in the three dimensions. The corporate social responsibility index is the average of the three ESG indexes, or the equally weighted average of the company’s environmental, social, and governance scores. | Kim, S.; Lee, G.; Kang, H.G. Risk management and corporate social responsibility. Strateg. Manag. J. 2021, 42(1), 202–230. [72], etc. | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, T.-T.; Wang, K.; Sueyoshi, T.; Wang, D.D. ESG: Research Progress and Future Prospects. Sustainability 2021, 13, 11663. https://doi.org/10.3390/su132111663

Li T-T, Wang K, Sueyoshi T, Wang DD. ESG: Research Progress and Future Prospects. Sustainability. 2021; 13(21):11663. https://doi.org/10.3390/su132111663

Chicago/Turabian StyleLi, Ting-Ting, Kai Wang, Toshiyuki Sueyoshi, and Derek D. Wang. 2021. "ESG: Research Progress and Future Prospects" Sustainability 13, no. 21: 11663. https://doi.org/10.3390/su132111663