Co-Creation of Value and Customer Experience: An Application in Online Banking

,

,

Abstract

:1. Introduction

2. Literature Review

2.1. Customer Experience

2.2. Co-Creation of Value

2.3. Consumer-Owned Resources

2.3.1. Connectivity

2.3.2. Creativity

2.3.3. Knowledge

3. Research Methodology

3.1. Sample

3.2. Research Design

4. Results

4.1. Validation of Measuring Instrument

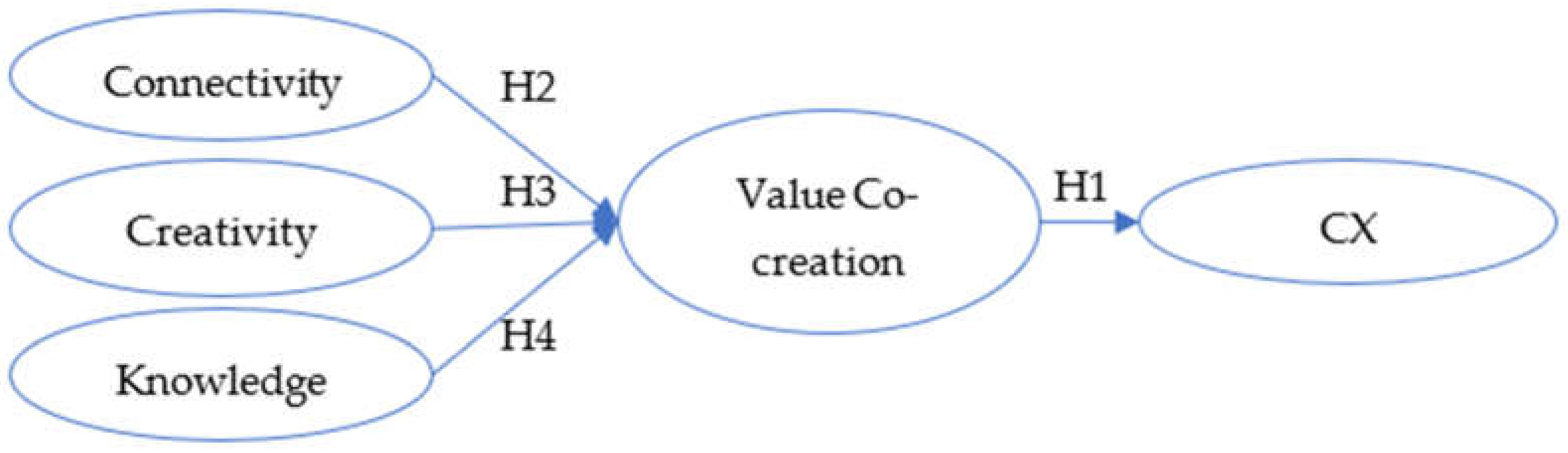

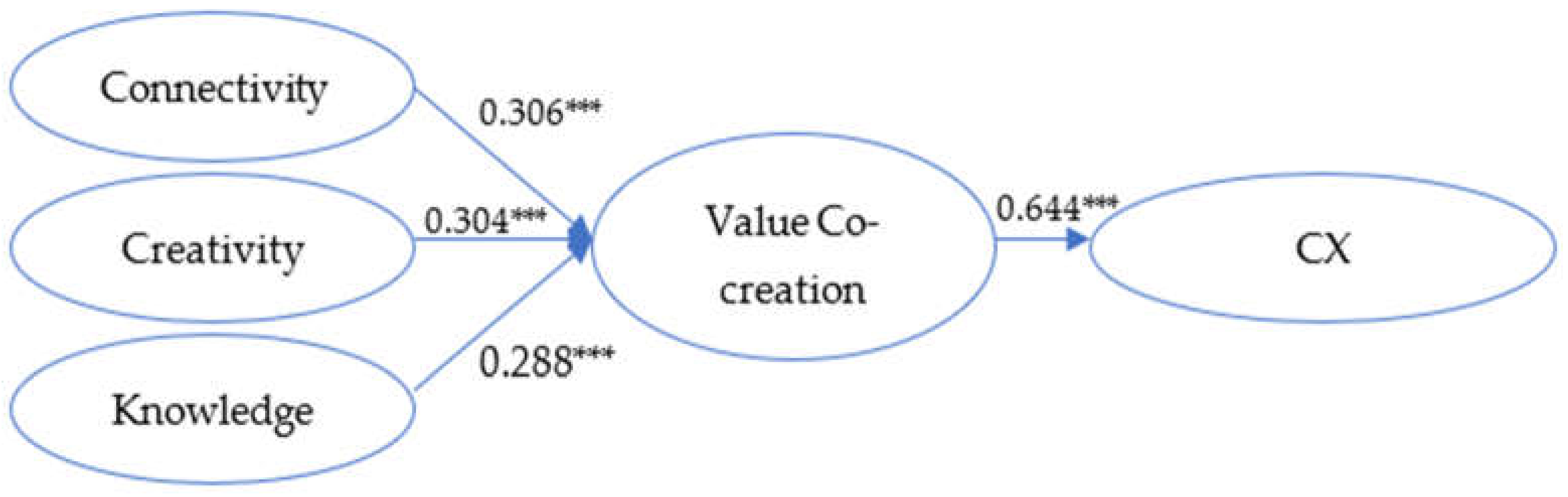

4.2. Hypothesis Testing

4.3. Discussion

5. Conclusions, Implications, and Research Limitations

5.1. Conclusions

5.2. Limitations and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- La República, D. Uso de las Oficinas Bancarias Decreció 33% en Pandemia por Aumento de Banca Móvil. Available online: https://www.larepublica.co/finanzas/uso-de-las-oficinas-bancarias-decrecio-33-en-pandemia-por-aumento-de-banca-movil-3142585 (accessed on 25 August 2021).

- La República, D. La Población No Bancarizada Cayó 8% Debido al Aumento de Aplicaciones Financieras. Available online: https://www.larepublica.co/finanzas/la-poblacion-no-bancarizada-cayo-8-debido-al-aumento-de-aplicaciones-financieras-3176466 (accessed on 25 August 2021).

- Portafolio Uso de Plataformas de Banca Digital Aumentó en un 59% en la Pandemia. Available online: https://www.portafolio.co/economia/en-colombia-el-uso-de-plataformas-de-banca-digital-aumento-en-un-59-durante-la-pandemia-549606 (accessed on 25 August 2021).

- Tiempo, C.E.E. Crece el Número de Usuarios de Banca Digital en Colombia. Available online: https://www.portafolio.co/economia/finanzas/crece-el-numero-de-usuarios-de-banca-digital-en-colombia-519582 (accessed on 24 August 2021).

- Akaka, M.A.; Vargo, S.L. Technology as an Operant Resource in Service (Eco)Systems. Inf. Syst. E-Bus Manag. 2014, 12, 367–384. [Google Scholar] [CrossRef]

- Vargo, S.L.; Lusch, R.F. Evolving to a New Dominant Logic for Marketing. J. Mark. 2004, 68, 1–17. [Google Scholar] [CrossRef] [Green Version]

- Ranjan, K.R.; Read, S. Value Co-Creation: Concept and Measurement. J. Acad. Mark. Sci. 2016, 44, 290–315. [Google Scholar] [CrossRef]

- Peltier, J.W.; Dahl, A.J.; Swan, E.L. Digital Information Flows across a B2C/C2C Continuum and Technological Innovations in Service Ecosystems: A Service-Dominant Logic Perspective. J. Bus. Res. 2020, 121, 724–734. [Google Scholar] [CrossRef]

- Prahalad, C.K.; Ramaswamy, V. Co-Creation Experiences: The next Practice in Value Creation. J. Interact. Mark. 2004, 18, 5–14. [Google Scholar] [CrossRef] [Green Version]

- Merz, M.A.; Zarantonello, L.; Grappi, S. How Valuable Are Your Customers in the Brand Value Co-Creation Process? The Development of a Customer Co-Creation Value (CCCV) Scale. J. Bus. Res. 2018, 82, 79–89. [Google Scholar] [CrossRef] [Green Version]

- Vargo, S.L.; Lusch, R.F. Institutions and Axioms: An Extension and Update of Service-Dominant Logic. J. Acad. Mark. Sci. 2016, 44, 5–23. [Google Scholar] [CrossRef]

- Font, X.; English, R.; Gkritzali, A.; Tian, W.S. Value Co-Creation in Sustainable Tourism: A Service-Dominant Logic Approach. Tour. Manag. 2021, 82, 104200. [Google Scholar] [CrossRef]

- Ferm, L.-E.C.; Thaichon, P. Value Co-Creation and Social Media: Investigating Antecedents and Influencing Factors in the U.S. Retail Banking Industry. J. Reailing Consum. Serv. 2021, 61, 102548. [Google Scholar] [CrossRef]

- Schreieck, M.; Wiesche, M. How established companies leverage it platforms for value co-creation—insights from banking. In Proceedings of the 25th European Conference on Information Systems (ECIS), Guimarães, Portugal, 5–10 June 2017; pp. 1726–1741. [Google Scholar]

- Mostafa, R.B. Mobile Banking Service Quality: A New Avenue for Customer Value Co-Creation. Int. J. Bank Mark. 2020, 38, 1107–1132. [Google Scholar] [CrossRef]

- Guitart, P.; Guitart and Partners. Co-Creación de Experiencias 2008. Available online: https://guitartpartners.com/es/2014/06/25/el-poder-de-la-co-creacion-para-generar-practicas-innovadoras/ (accessed on 18 June 2021).

- Lalicic, L.; Weismayer, C. Consumers’ Reasons and Perceived Value Co-Creation of Using Artificial Intelligence-Enabled Travel Service Agents. J. Bus. Res. 2021, 129, 891–901. [Google Scholar] [CrossRef]

- Mutis, J.; Ricart, J.E. Innovación En Modelos de Negocio: La Base de La Pirámide Como Campo de Experimentación. Universia Bus. Rev. 2008, Segundo Trimestre, 10–27. [Google Scholar]

- Matarazzo, M.; Penco, L.; Profumo, G.; Quaglia, R. Digital Transformation and Customer Value Creation in Made in Italy SMEs: A Dynamic Capabilities Perspective. J. Bus. Res. 2021, 123, 642–656. [Google Scholar] [CrossRef]

- Payne, A.; Storbacka, K.; Frow, P.; Knox, S. Co-Creating Brands: Diagnosing and Designing the Relationship Experience. J. Bus. Res. 2009, 62, 379–389. [Google Scholar] [CrossRef]

- Montesimos, M.D.M.T.; Suárez, J.A.G.; Fernández, J.I.P. Cambio de Paradigma En El Marketing de Destinos Turísticos: El Plan CMA Experience. Cult. Rev. Cult. Tur. 2013, 7, 4–32. [Google Scholar]

- Siqueira, J.R.; Peña, N.G.; ter Horst, E.; Molina, G. Spreading the Word: How Customer Experience in a Traditional Retail Setting Influences Consumer Traditional and Electronic Word-of-Mouth Intention. Electron. Commer. Res. Appl. 2019, 37, 100870. [Google Scholar] [CrossRef]

- Rialti, R.; Caliandro, A.; Zollo, L.; Ciappei, C. Co-Creation Experiences in Social Media Brand Communities: Analyzing the Main Types of Co-Created Experiences. Span. J. Mark. —ESIC 2018, 22, 122–141. [Google Scholar] [CrossRef] [Green Version]

- El-Jarn, H.; Southern, G. Can Co-Creation in Extended Reality Technologies Facilitate the Design Process? J. Work-Appl. Manag. 2020, 12, 191–205. [Google Scholar] [CrossRef]

- Füller, J.; Mühlbacher, H.; Matzler, K.; Jawecki, G. Consumer Empowerment through Internet-Based Co-Creation. J. Manag. Inf. Syst. 2009, 26, 71–102. [Google Scholar] [CrossRef]

- Zhang, T.C.; Jahromi, M.F.; Kizildag, M. Value Co-Creation in a Sharing Economy: The End of Price Wars? Int. J. Hosp. Manag. 2018, 71, 51–58. [Google Scholar] [CrossRef]

- Ramaswamy, V.; Ozcan, K. What Is Co-Creation? An Interactional Creation Framework and Its Implications for Value Creation. J. Bus. Res. 2018, 84, 196–205. [Google Scholar] [CrossRef]

- Maria, T.; Dimitris, P.; Garifallos, F.; Athanasios, G.; Roumeliotis, M. Collaboration Learning as a Tool Supporting Value Co-Creation. Evaluating Students Learning through Concept Maps. Procedia-Soc. Behav. Sci. 2015, 182, 375–380. [Google Scholar] [CrossRef] [Green Version]

- Payne, A.F.; Storbacka, K.; Frow, P. Managing the Co-Creation of Value. J. Acad. Mark. Sci. 2008, 36, 83–96. [Google Scholar] [CrossRef]

- Lorenzo, G.; Oblinger, D.; Dziuban, C. How Choice, Co-Creation, and Culture Are Changing What It Means to Be Net Savvy. Educ. Q. 2007, 30, 6. [Google Scholar]

- Woodruff, R.B. Customer Value: The next Source for Competitive Advantage. J. Acad. Mark. Sci. 1997, 25, 139–153. [Google Scholar] [CrossRef]

- Yu, C.-H.; Tsai, C.-C.; Wang, Y.; Lai, K.-K.; Tajvidi, M. Towards Building a Value Co-Creation Circle in Social Commerce. Comput. Hum. Behav. 2020, 108, 105476. [Google Scholar] [CrossRef] [Green Version]

- Neuhofer, B.; Buhalis, D.; Ladkin, A. Co-creation through technology: Dimensions of social connectedness. In Information and Communication Technologies in Tourism 2014; Springer: Cham, Switzerland, 2013; pp. 339–352. [Google Scholar]

- Prahalad, C.K.; Ramaswamy, V. The Co-Creation Connection. Strategy Bus. 2002, 50–61. [Google Scholar]

- Romero, D.; Molina, A. Collaborative Networked Organisations and Customer Communities: Value Co-Creation and Co-Innovation in the Networking Era. Prod. Plan. Control 2011, 22, 447–472. [Google Scholar] [CrossRef]

- Belanche, D.; Casaló, L.V.; Flavián, C.; Guinalíu, M. Reciprocity and Commitment in Online Travel Communities. IMDS 2019, 119, 397–411. [Google Scholar] [CrossRef]

- Cotterell, N.; Eisenberger, R.; Speicher, H. Inhibiting Effects of Reciprocation Wariness on Interpersonal Relationships. J. Personal. Soc. Psychol. 1992, 62, 658. [Google Scholar] [CrossRef]

- Im, S.; Bhat, S.; Lee, Y. Consumer Perceptions of Product Creativity, Coolness, Value and Attitude. J. Bus. Res. 2015, 68, 166–172. [Google Scholar] [CrossRef]

- Huerta, E. La Co-Creación Y El Diseño Colaborativo—ID:5eb71c85b46b9. Available online: https://xdoc.mx/documents/la-co-creacion-y-el-diseo-colaborativo-5eb71c85b46b9 (accessed on 24 August 2021).

- Sethi, R.; Smith, D.C.; Park, C.W. Cross-Functional Product Development Teams, Creativity, and the Innovativeness of New Consumer Products. J. Mark. Res. 2001, 38, 73–85. [Google Scholar] [CrossRef]

- Füller, J.; Matzler, K.; Hoppe, M. Brand Community Members as a Source of Innovation. J. Prod. Innov. Manag. 2008, 25, 608–619. [Google Scholar] [CrossRef]

- Casaló, L.V.; Flavián, C.; Ibáñez-Sánchez, S. Be Creative, My Friend! Engaging Users on Instagram by Promoting Positive Emotions. J. Bus. Res. 2021, 130, 416–425. [Google Scholar] [CrossRef]

- Ind, N.; Coates, N. The Meanings of Co-creation. Eur. Bus. Rev. 2013, 25, 86–95. [Google Scholar] [CrossRef]

- Potts, J.; Hartley, J.; Banks, J.; Burgess, J.; Cobcroft, R.; Cunningham, S.; Montgomery, L. Consumer Co-Creation and Situated Creativity. Ind. Innov. 2008, 15, 459–474. [Google Scholar] [CrossRef] [Green Version]

- Morales, H.H. CO-CREACIÓN: ¿DIÁLOGO ACTIVO ENTRE ORGANIZACIONES Y COMUNIDADES DE INTERÉS? In Proceedings of the Congreso de Investigación y Pedagogía III Nacional II Internacional; 15 December 2014, Bogotá, Colombia.

- Nambisan, S.; Baron, R.A. Virtual Customer Environments: Testing a Model of Voluntary Participation in Value Co-Creation Activities. J. Prod. Innov. Manag. 2009, 26, 388–406. [Google Scholar] [CrossRef]

- Kangas, M. Creative and Playful Learning: Learning through Game Co-Creation and Games in a Playful Learning Environment. Think. Ski. Creat. 2010, 5, 1–15. [Google Scholar] [CrossRef]

- Sampson, D.; Karagiannidis, C. Personalised Learning: Educational, Technological and Standarisation Perspective. Digit. Educ. Rev. 2002, 24–39. [Google Scholar]

- Kurilovas, E.; Kubilinskiene, S.; Dagiene, V. Web 3.0—Based Personalisation of Learning Objects in Virtual Learning Environments. Comput. Hum. Behav. 2014, 30, 654–662. [Google Scholar] [CrossRef]

- Barros, D.R. Entornos post-digitales, co-creacion, practicas didacticas y experiencias de usuario. In VIII Jornadas de Investigación en Disciplinas Artísticas y Proyectuales; Facultad de Bellas Artes: Madrid, Spain, 2016. [Google Scholar]

- Zhang, H.; Lu, Y.; Wang, B.; Wu, S. The Impacts of Technological Environments and Co-Creation Experiences on Customer Participation. Inf. Manag. 2015, 52, 468–482. [Google Scholar] [CrossRef]

- Kamboj, S.; Sarmah, B.; Gupta, S.; Dwivedi, Y. Examining Branding Co-Creation in Brand Communities on Social Media: Applying the Paradigm of Stimulus-Organism-Response. Int. J. Inf. Manag. 2018, 39, 169–185. [Google Scholar] [CrossRef] [Green Version]

- Trafimow, D.; MacDonald, J.A. Performing Inferential Statistics Prior to Data Collection. Educ. Psychol. Meas. 2017, 77, 204–219. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Trafimow, D.; Hyman, M.R.; Kostyk, A. The (Im)Precision of Scholarly Consumer Behavior Research. J. Bus. Res. 2020, 114, 93–101. [Google Scholar] [CrossRef]

- Kim, H.; Choi, B. The Influence of Customer Experience Quality on Customers’ Behavioral Intentions. Serv. Mark. Q. 2013, 34, 322–338. [Google Scholar] [CrossRef]

- Chin, W.W. The Partial Least Squares Approach to Structural Equation Modeling. Mod. Methods Bus. Res. 1998, 295, 295–336. [Google Scholar]

- Fornell, C.; Larcker, D.F. Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Kozinets, R.V.; Hemetsberger, A.; Schau, H.J. The Wisdom of Consumer Crowds: Collective Innovation in the Age of Networked Marketing. J. Macromark. 2008, 28, 339–354. [Google Scholar] [CrossRef]

- Chepurna, M.; Rialp Criado, J. What Motivates and Deters Users’ Online Co-Creation? The Role of Cultural and Socio-Demographic Factors. Span. J. Mark.—ESIC 2021. ahead-of-print. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Constructs | Items |

|---|---|

| Customer Experience | I would say that my experience in my bank is excellent |

| I believe I get a higher experience with my bank | |

| I think the overall experience in the whole process with my bank is excellent | |

| Co-Creation of Value | I tend to review (read) my bank’s publications on its website or social networks |

| I publish content about my bank through my social networks (original content, not shared) | |

| I share information about my bank through social networks | |

| When I purchase a financial product from my bank, I can customize it according to my interests | |

| When I want to purchase a financial product or use one of my bank’s services, and I have a concern, I use the customer service (chat, call, email, etc.) | |

| Connectivity | I feel identified with my bank’s values. |

| I am connected to other consumers of this brand | |

| I participate in one or more of the brand’s communities | |

| I socialize with other consumers of the brand | |

| Creativity | I am imaginative when interacting with the brand |

| I am creative when interacting with the brand | |

| I am curious when interacting with the brand | |

| Knowledge | I actively share our knowledge about the work with the organizers. |

| I proactively share our best practices with the organizer | |

| I interact with the organizer by sharing what we have learned from the exhibition |

| Construct | Item | β | Mean | Standard Deviation | Composite Reliability | AVE |

|---|---|---|---|---|---|---|

| Customer experience | CX1 | 0.939 | 5.11 | 1.62 | 0.966 | 0.906 |

| CX2 | 0.956 | 4.77 | 1.69 | |||

| CX3 | 0.960 | 4.83 | 1.70 | |||

| Co-creation of value | CCV1 | 0.745 | 4.27 | 2.05 | 0.858 | 0.549 |

| CCV2 | 0.689 | 2.16 | 1.72 | |||

| CCV3 | 0.712 | 2.15 | 1.76 | |||

| CCV4 | 0.757 | 4.08 | 1.96 | |||

| CCV6 | 0.795 | 4.19 | 1.92 | |||

| Connectivity | CN1 | 0.914 | 2.40 | 1.95 | 0.955 | 0.841 |

| CN2 | 0.821 | 2.54 | 1.97 | |||

| CN3 | 0.921 | 2.19 | 1.80 | |||

| CN4 | 0.912 | 2.62 | 2.00 | |||

| Creativity | CR1 | 0.961 | 3.99 | 1.86 | 0.965 | 0.903 |

| CR2 | 0.966 | 3.92 | 1.87 | |||

| CR3 | 0.922 | 4.31 | 1.87 | |||

| Knowledge | KN1 | 0.885 | 5.19 | 1.59 | 0.915 | 0.782 |

| KN2 | 0.907 | 5.27 | 1.43 | |||

| KN3 | 0.860 | 4.21 | 1.59 |

| Constructs | CCV | CX | Connectivity | Creativity | Knowledge |

|---|---|---|---|---|---|

| CCV | 0.741 | ||||

| CX | 0.644 | 0.952 | |||

| Connectivity | 0.542 | 0.283 | 0.917 | ||

| Creativity | 0.626 | 0.571 | 0.474 | 0.95 | |

| knowledge | 0.572 | 0.616 | 0.318 | 0.613 | 0.884 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Peña-García, N.; Losada-Otálora, M.; Juliao-Rossi, J.; Rodríguez-Orejuela, A. Co-Creation of Value and Customer Experience: An Application in Online Banking. Sustainability 2021, 13, 10486. https://doi.org/10.3390/su131810486

Peña-García N, Losada-Otálora M, Juliao-Rossi J, Rodríguez-Orejuela A. Co-Creation of Value and Customer Experience: An Application in Online Banking. Sustainability. 2021; 13(18):10486. https://doi.org/10.3390/su131810486

Chicago/Turabian StylePeña-García, Nathalie, Mauricio Losada-Otálora, Jorge Juliao-Rossi, and Augusto Rodríguez-Orejuela. 2021. "Co-Creation of Value and Customer Experience: An Application in Online Banking" Sustainability 13, no. 18: 10486. https://doi.org/10.3390/su131810486