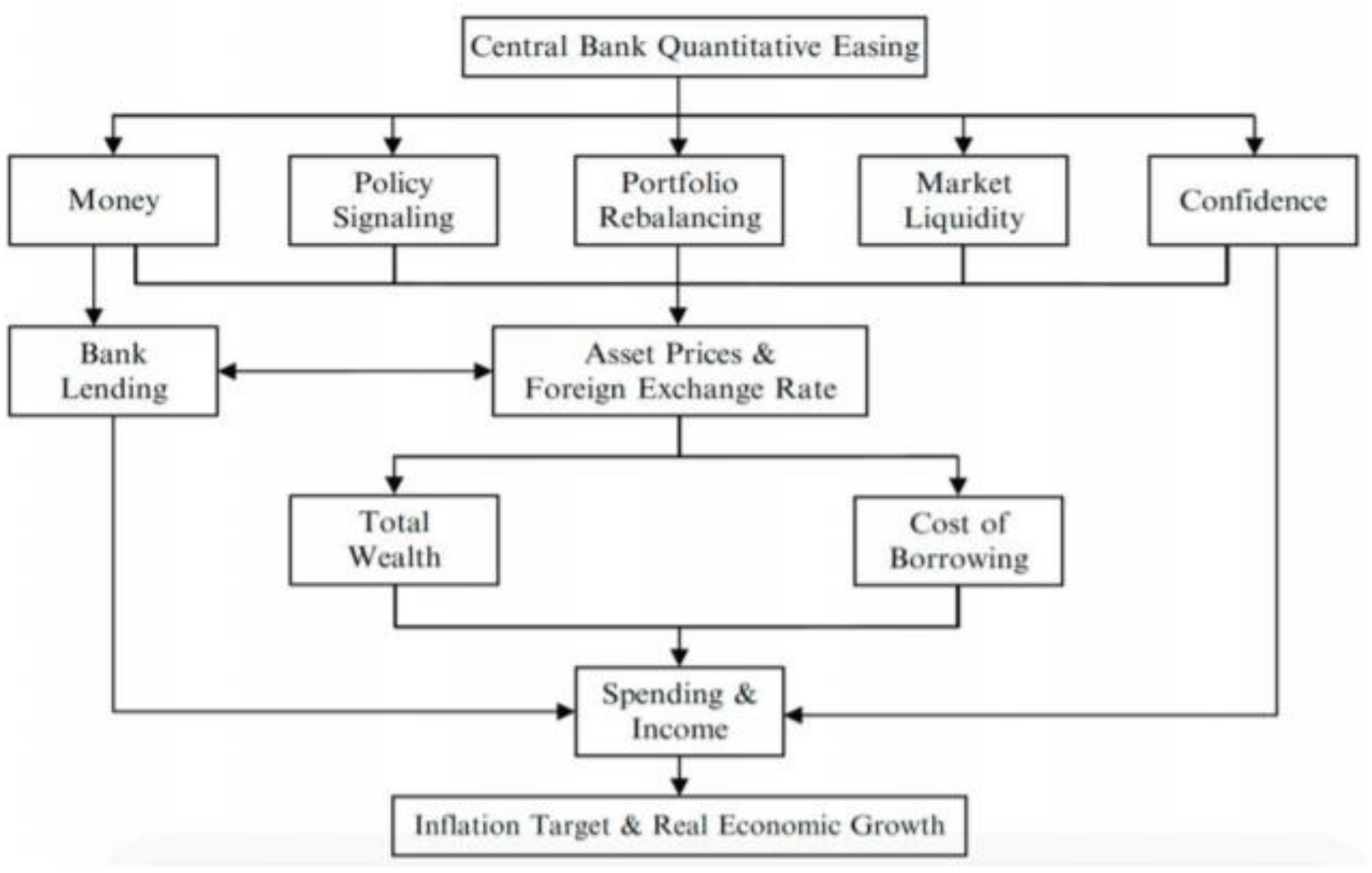

Soy Generalized Model

As already stated, an OLS with non-stationary variables would very likely generate spurious regression. All variables were found to be stationary at first difference (order of integration l (1)); therefore, the ordinary least squared regression was performed according to the following transformation.

1. OLS using variables in the first difference.

Without the pair of USD/BRL:

Results of the generalized model excluding the variable USD/BRL for soy are presented in

Table 1.

The result of this regression shows a significance at the 1% level for the regressor Fx. rate, and its coefficient shows that a change of one index unit in the dollar index would result in a decrease of USD 9.40 in the future market of soybeans. For the interest rate, the coefficient suggests that a unit decrease in this variable (in percent) would cause a decrease of USD 26.7 in the future soy markey; however, its p-value suggests no significance. The possible reasons for the insignificance of this variable will be discussed later.

We now add the variable USD/BRL, which is more relevant to soy as Brazil is the largest and most competitive producer of this agricultural commodity.

Results of the generalized model inclusive the variable USD/BRL for soy are presented in

Table 2.

The results with the variable USD/BRL vary considerably. With the inclusion of interest rate, no changes occurred; however, with Fx. rate and the newly added variable, we can observe a significant influence. Fx. rate now shows significance at the 5% level (it is no longer 1%), showing that a change of one index unit in the dollar index would result in a fall of USD 7.04 dollars in the soy contract. The pair of U.S. dollar and Brazilian Real showed high significance, at the 0.1% level, with a coefficient suggesting that a unit change in the currency pair would result in a decrease of USD 142 in the contract for soy. Such a high result is obtained only for this commodity due to its close relation to the Brazilian economy; for corn and sugar, the impact is much lower, as will be displayed in future models. As the price formation of a commodity involves many variables, and the most relevant are the ones related to the production/exploration of the commodity, a model with purely monetary indicators would have low R² (without USD/BRL 0.03169, with USD/BRL 0.08732).

2. Engle–Granger Cointegration test

As the conversion of data to first differences causes a loss of information in the time series, further testing should be conducted to establish relations between the variables. To check for a possible long-term relation between variables, we will run the Engle–Granger test for cointegration. This cointegration test is suitable for two variables; therefore, three separate tests will be performed: soy/Fx. rate and soy/interest rate. A test with the four variables together will be executed accordingly.

- (1a)

OLS: soy as the dependent variable and Fx. rate as the only independent variable.

- (1b)

OLS: soy as the dependent variable and interest rate as the only independent variable.

- (1c)

OLS: soy as the dependent variable and the pair USD/BRL as the only independent variable.

- (2)

Residuals of the regression are stored to test for cointegration.

- (3)

The test results are shown in

Table 3.

Ho: There is no cointegration between soy prices and the other variable.

H1: There is cointegration between soy prices and the other variable.

[Rejection: |t| > 1.96]

The results, in absolute terms, are higher than t-statistic 1.96. Therefore, the null hypothesis can be rejected, and we can assume that cointegration between the variables exists for all “combinations”. This result indicates a possible long-term relation between soy prices and exchange rate, between soy prices and interest rates, and between soy prices and the pair USD/BRL.

3. The equation for OLS with non-stationary data + autocorrelation of data.

If a regression was conducted without checking for stationary, the resulting equation would be:

With non-stationary data, USD/BRL would not affect the price of soy contracts—a conclusion that would not pertain in real life. Both non-stationary models have R-squared values of 0.6183.

Corn Generalized Model

1. OLS using variables in first difference.

Following the same method, two separate regressions will be tested.

Without the pair USD/BRL:

Results of the generalized model excluding the variable USD/BRL for corn are presented in

Table 4.

With similar results to soy’s first regression, for corn, Fx. rate is significant, but interest rate is not. Exchange rate is significant at the 5% level, and has milder impact on prices, as a change of one index unit in the dollar index would result in a decrease of USD 3.85 in corn future contract prices. Once again, interest rate has no influence on contract price, and its coefficient shows that a percentage change in interest rate would result in an increase of USD 1.86 in corn’s future contract prices.

After adding the currency pair to the regression, we see a very slight change.

Results of the generalized model inclusive the variable USD/BRL for corn are presented in

Table 5.

Interest rate remains irrelevant to corn’s contract prices in this model, and with these variables. However, Fx. rate shows significance at the 10% level, with a very similar coefficient. The variable of the pair of U.S dollar and Brazilian Real has significance at the 10% level as well, and suggests that a unit change in the currency pair would result in a decrease of USD 35.9 in the corn contract price, which is less than that seen for soy, but is more than that for sugar. Chinese and U.S. trade policy variables in another model, such as one specific for corn, could express a more realistic relation regarding the price formation of this commodity. As stated for soy, a model with purely monetary indicators would have low R² (without USD/BRL, 0.03873; with USD/BRL, 0.03873).

2. Engle–Granger cointegration test

As done for soy:

- (1a)

OLS: corn as the dependent variable and Fx. rate as the only independent variable.

- (1b)

OLS: corn as the dependent variable and interest rate as the only independent variable.

- (1c)

OLS: corn as the dependent variable and the pair USD/BRL as the only independent variable.

- (2)

Residuals of the regression are stored to test for cointegration.

- (3)

The test results are shown in

Table 6.

Ho: There is no cointegration between corn prices and the other variable.

H1: There is cointegration between corn prices and the other variable.

[Rejection: |t| > 1.96]

The test provides evidence of a possible long-term relation between corn and each variable individually, as the null hypothesis can be rejected for all three t-statistic results. The Johansen cointegration test, which is a more sophisticated method, could be performed; however, it could not show whether the cointegration is related to the commodity specifically, and could reflect a cointegration of exchange rate and interest rate, or of USD/BRL and interest rate. This method can investigate the relations between the regressors and the commodities.

3. Equation for OLS with non-stationary data + autocorrelation of data.

This again shows the vastly different result derived from a regression with non-stationary time series.

Sugar Generalized Model

Lastly, sugar has the special characteristic of being regressed with the pair USD/INR, which analyzes the influence of the second largest sugar producer in the world, and how it behaves in a regression with the largest producer (Brazil).

1. OLS using variables in first difference.

Without the pair USD/BRL:

The regression on the first difference: Δsugar = β0 + β1 Δ FxRate + β2 Δ IntRate + ei

Results of the generalized model excluding the variable USD/BRL for sugar are presented in

Table 7.

Differently from previous regressions, both variables for sugar have no significance. In terms of the coefficient, a change of one index unit in the dollar index would result in a small decrease of USD 0.09 in the contract for sugar, and a percent change in the interest rate would implicate a reduction of USD 0.16 in the contract.

The regression with USD/BRL only shows significance for the newly added variable.

Results of the generalized model inclusive the variable USD/BRL for sugar are presented in

Table 8.

Exchange rate and interest rate did not become significant in the new regression, and their coefficients were diminished. The added variable USD/BRL showed significance at the 5% level, and its coefficient indicates that a unit change in the pair would result in a decrease of USD 1.64 in sugar contract prices. Low rates of R² persist (without USD/BRL, 0.008437; with USD/BRL, 0.008437)

To visualize the influence of the Indian Rupee, the variable USD/INR is added to the model. The model outcome after adding USD/INR into the model is presented in

Table 9.

Checking the influence of the Indian Rupee in the model:

Model 1 = with all variables; model 2 = without USD/BRL.

For the model with all variables, only USD/BRL was significant (at the 10% level), and its coefficient indicates that a unit change in the pair’s value would implicate a decrease of USD 1.29 in the sugar contract price. The Indian Rupee seems to be insignificant, as well did the other variables. However, when USD/BRL is removed from the model, USD/INR becomes significant at the 5% level, with a coefficient that indicates that a unit change in the pair’s value would implicate a decrease of USD 0.20 in the contract of sugar. As for the other two commodities, the R² is still low (with all variables, 0.039; without USD/BRL, 0.02765).

2. Engle–Granger cointegration test

- (1a)

OLS: sugar as the dependent variable and Fx. rate as the only independent variable.

- (1b)

OLS: sugar as the dependent variable and interest rate as the only independent variable.

- (1c)

OLS: sugar as the dependent variable and the pair USD/BRL as the only independent variable.

- (1d)

OLS: sugar as the dependent variable and the pair USD/INR as the only independent variable.

- (2)

Residuals of the regression are stored to test for cointegration.

- (3)

Ho: There is no cointegration between sugar prices and the other variable.

H1: There is cointegration between sugar prices and the other variable.

[Rejection: |t| > 1.96]

The Engle–Granger cointegration test suggests that there is a long-term relationship between sugar and each other variable, as all four t-statistic values were higher than 1.96.

3. Equation for OLS with non-stationary data + autocorrelation of data.

If non-stationary time series were used, the regression results would be:

{kind=link}

{kind=link}

{kind=link}