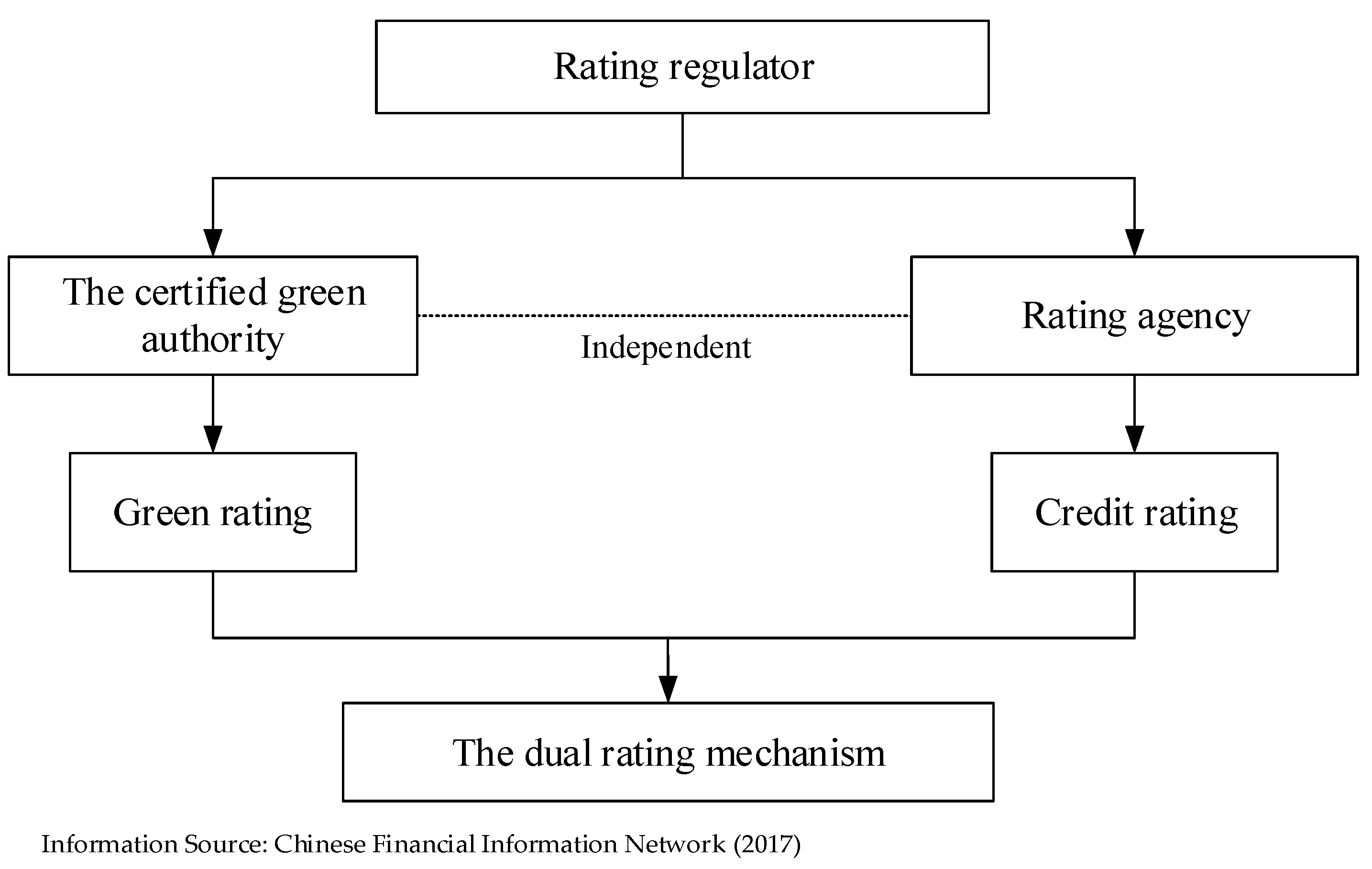

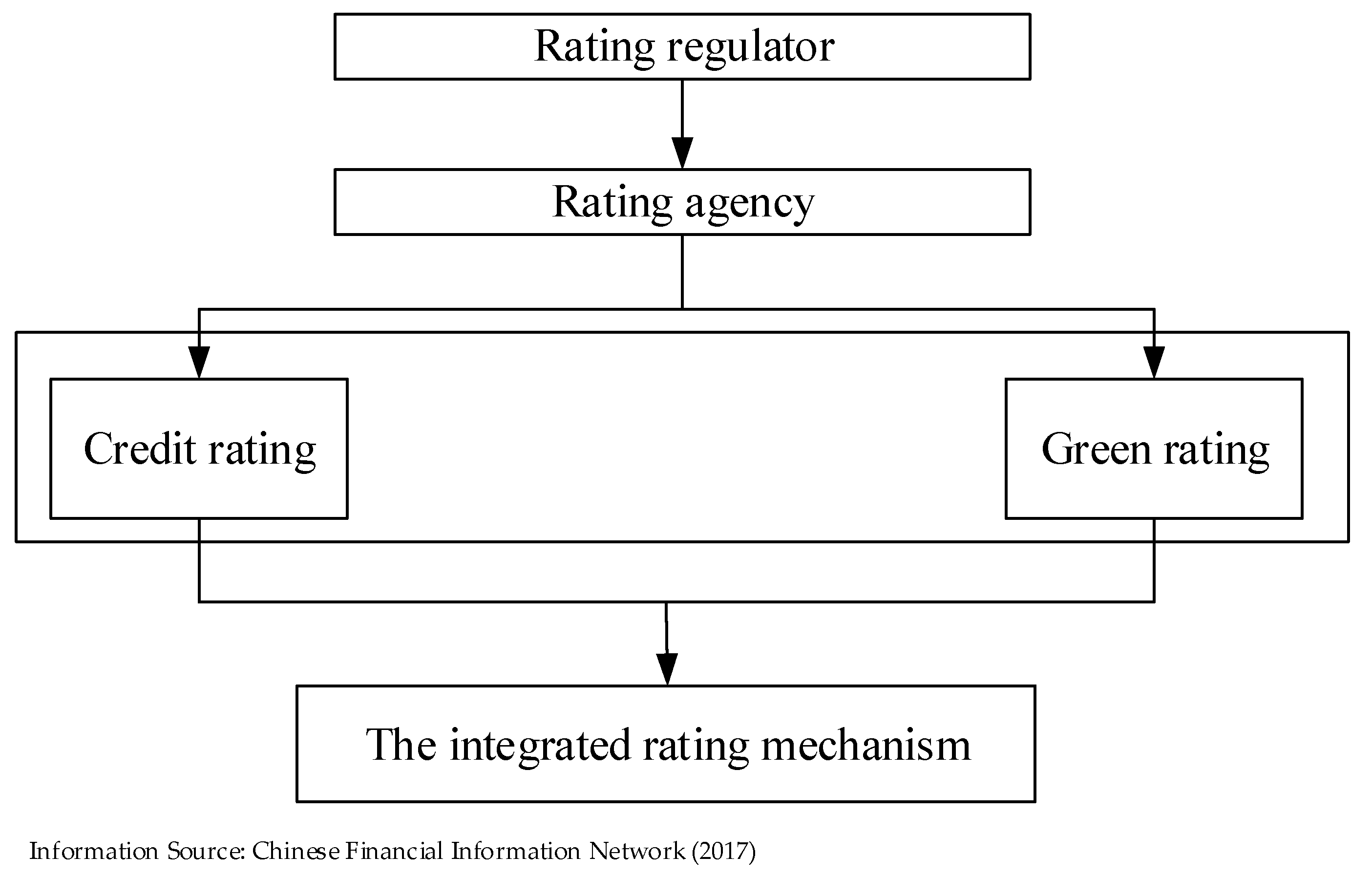

We consider a two-stage game model and utilize the incentive difference Hotelling model to discuss the impact of rating accuracy and reputation of rating agencies and certified green agencies on rating prices, rating demands and rating profits.

4.1. The First Stage of Game Model

In the first stage, the regulator cannot observe the phenomena of “greenwashing” or inflated ratings. There are no regulatory penalties in this stage. Due to the indirect issuance effect not being obvious in the first stage, we suppose that the indirect effect is .

Based on the principle of the Hotelling model, when

and

, we can obtain the equilibrium solutions of rating prices in the two mechanisms:

According to Equations (9) and (10), we can obtain equilibrium solutions of rating demands in the two mechanisms:

The profits of dual ratings and integrated rating in the two mechanisms are:

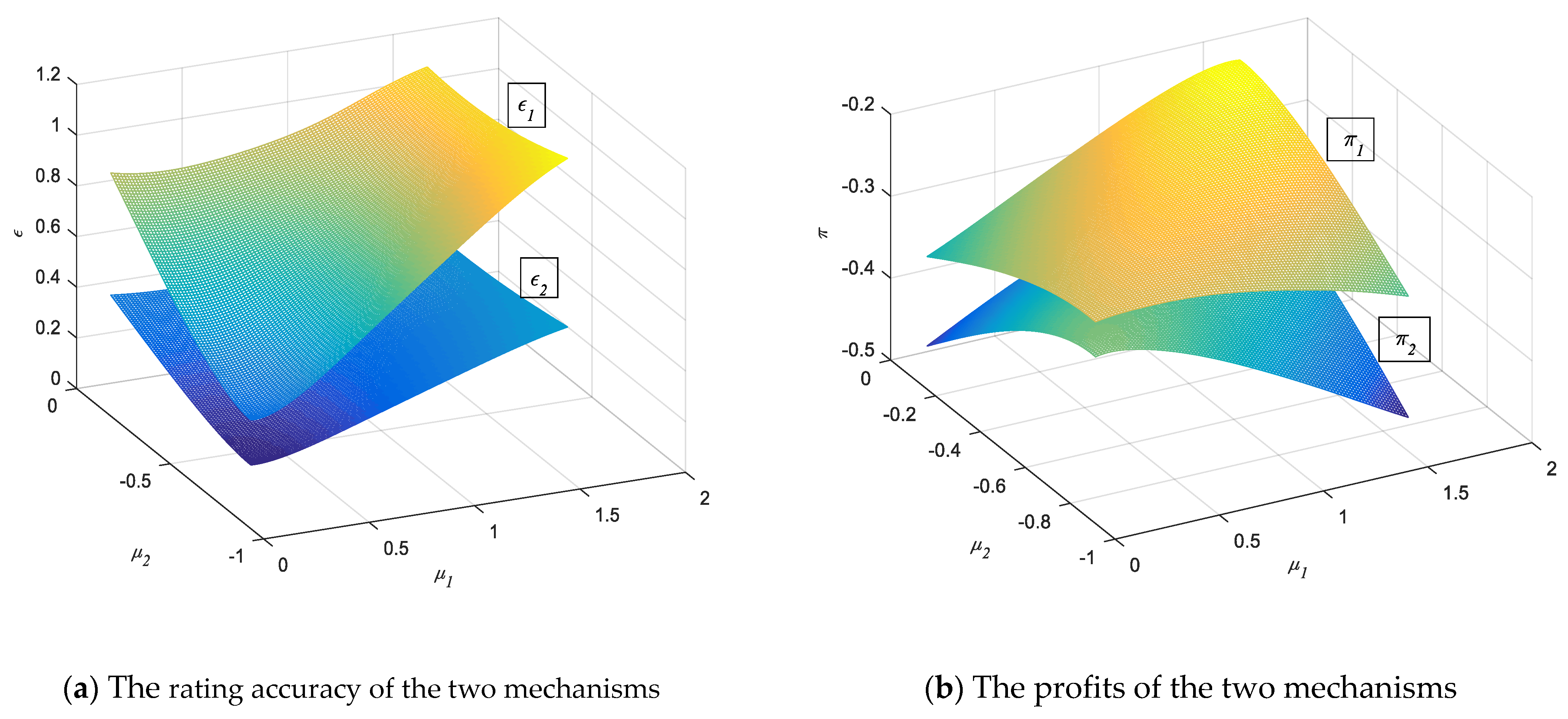

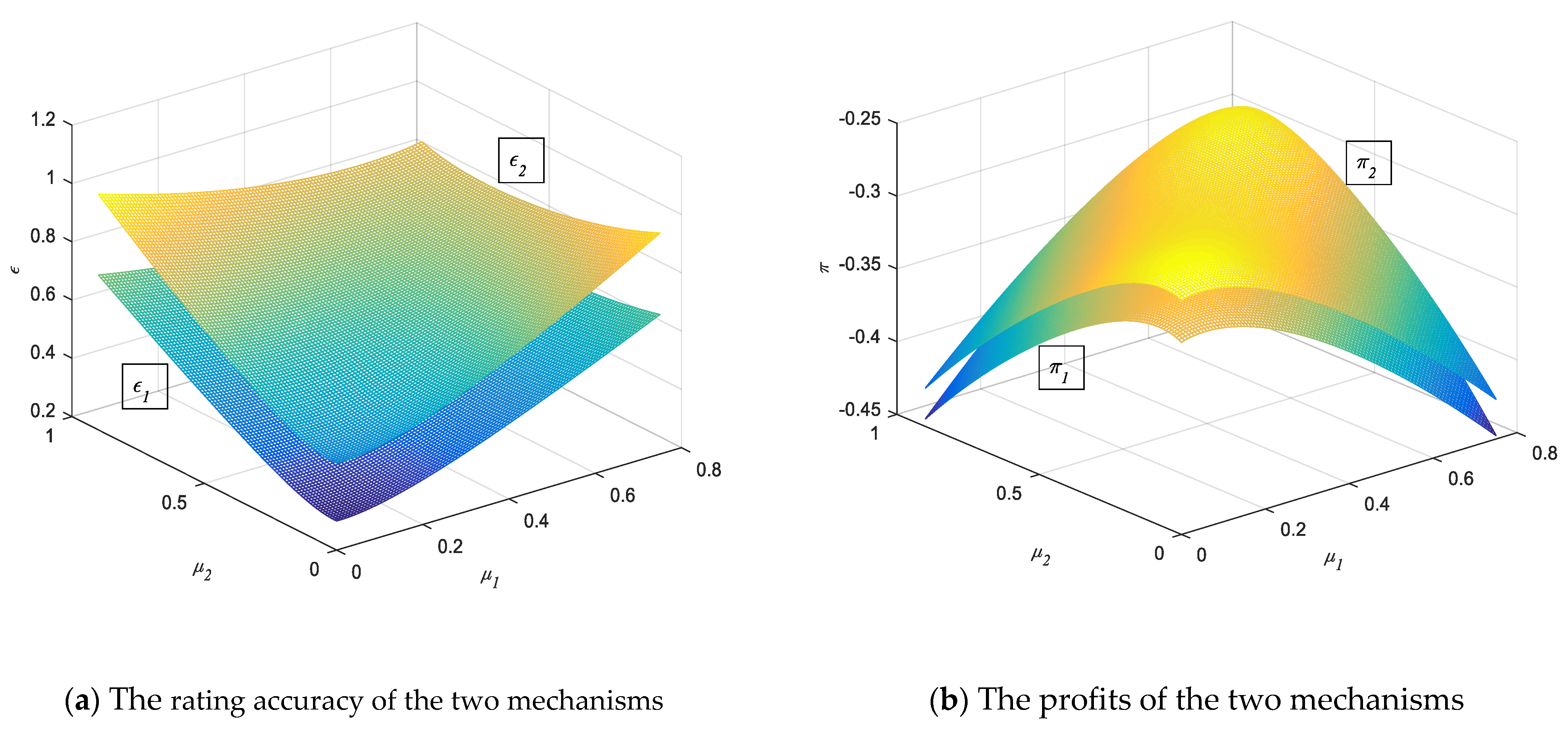

In this stage, the rating accuracy of the two mechanisms are:

Situation 1. When rating accuracyandsatisfyand , the rating accuracy is not reaching equilibrium. When the direct issuance effect in the dual rating mechanism and the direct issuance effect in the integrated rating mechanism, we have and . This demonstrates that the regulatory effect of the dual rating mechanism is better in this situation.

When the direct issuance effectin the dual rating mechanism and the direct issuance effectin the integrated rating mechanism, we haveand . This demonstrates that the regulatory effect of the integrated rating mechanism is better in this situation.

Situation 2. When rating accuracyandsatisfiesand , the rating accuracy is reaching equilibrium.

We letandin the two mechanisms, and the equilibrium solutions of rating accuracy are: When , we haveand . This shows that the regulatory effect of the dual rating mechanism is better. When , we haveand . This indicates that the regulatory effect of the integrated rating mechanism is better.

According to the analysis of the first stage of the game model, we can conclude the following:

(1) When the rating accuracy does not reach equilibrium, the conditions of usage of the dual rating mechanism are the direct issuance effect in the dual rating mechanism and the direct issuance effect in the integrated rating mechanism.

(2) When the rating accuracy does not reach equilibrium, the conditions of usage of the integrated rating mechanism are the direct issuance effect in the dual rating mechanism and the direct issuance effect .

(3) When the rating accuracy reaches equilibrium, the conditions of usage of the dual rating mechanism are , while the conditions of usage of the integrated rating mechanism are .

The Hotelling model analysis in the first stage shows that under the circumstance that the indirect effect has no influence on the competition of rating agencies, the market share, rating cost and reputation have influence on the rating accuracy, thus affecting the applicable conditions of dual rating and integrated rating. Based on the above conclusions, we find that the applicable conditions of the dual rating mechanism and the integrated rating mechanism mostly depend on the accuracy of credit rating and green rating. Specifically, when the accuracy , increases, the regulatory authorities are more inclined to choose the dual rating mechanism. According to the direct effect of green financing projects, the selection of appropriate regulatory mechanism of rating agencies can effectively solve the problem of overrating green bonds.

4.2. The Second Stage of Game Model

In the second stage, the regulator can observe the phenomena of greenwashing and inflated ratings and give regulatory penalties . Due to the obvious indirect issuance effect in the second stage, we suppose that the indirect effect in the dual mechanism and the indirect effect in the integrated mechanism are different .

The profits of dual ratings and integrated rating in the two mechanisms are:

Based on the principle of the Hotelling model, when

and

, we can obtain the equilibrium solutions of rating prices in the two mechanisms:

According to Equations (9) and (10), we can obtain equilibrium solutions of rating demands in the two mechanisms in the second stage:

The profits of dual ratings and integrated rating in the two mechanisms are:

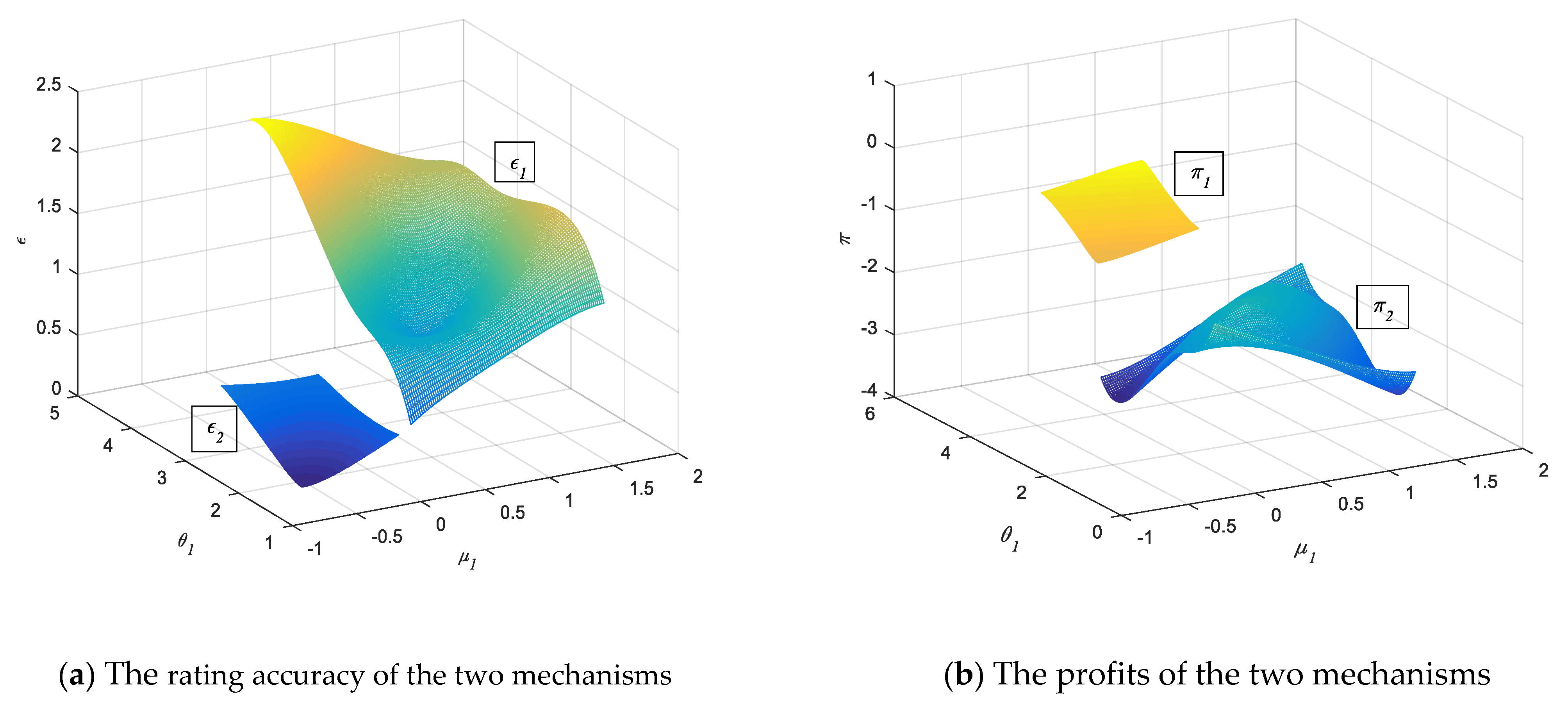

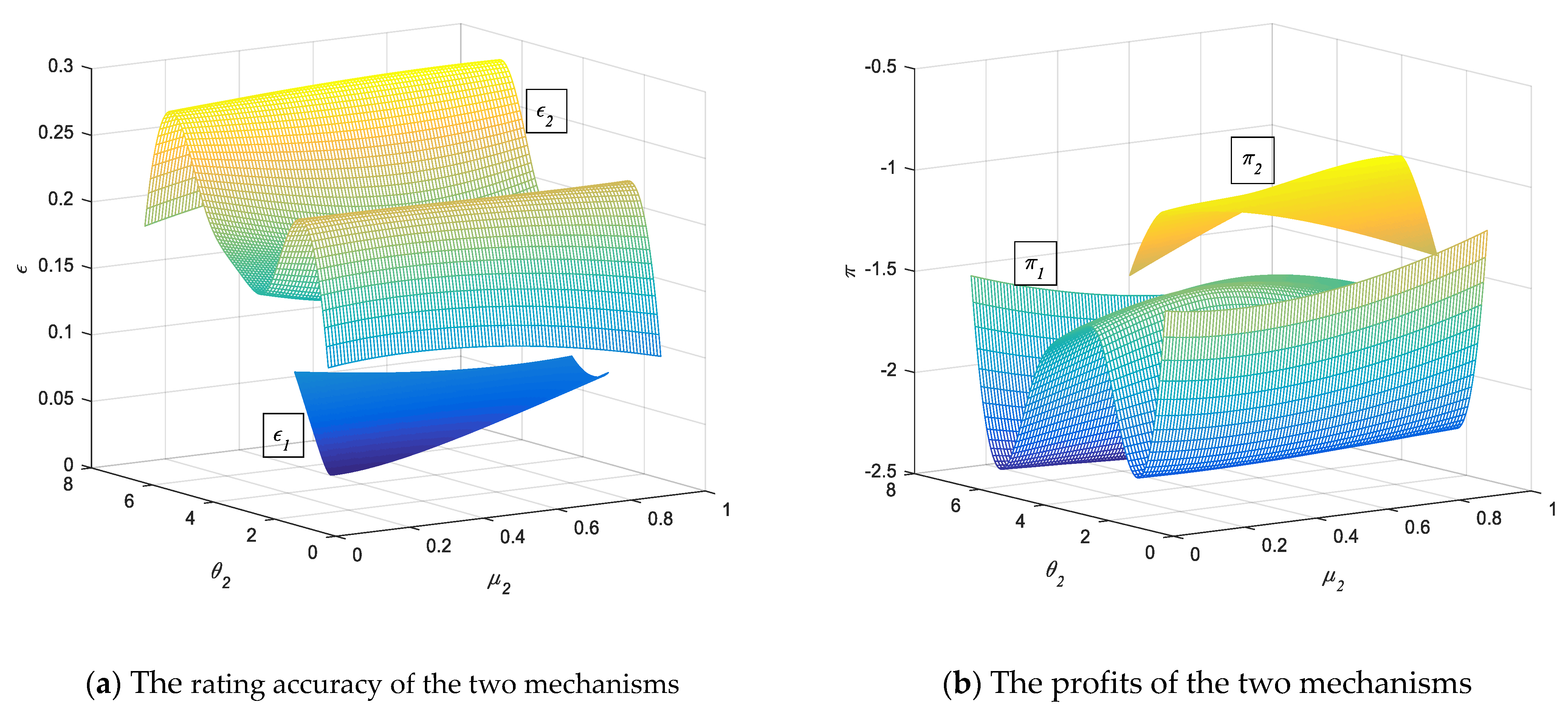

In the second stage, the rating accuracy of the two mechanisms is:

Situation 3. When rating accuracyandsatisfiesand , the rating accuracy is not reaching equilibrium. When the indirect effectin the dual rating mechanism and the indirect effectin the integrated rating mechanism, we haveand . According to the first stage of the game model, we consider the results of the first stage and can obtainand . This demonstrates that the regulatory effect of the dual rating mechanism is better in this situation.

When the indirect effectin the dual rating mechanism and the indirect effectin the integrated rating mechanism, we haveand . We consider the results of the first stage and can obtainand . This demonstrates that the regulatory effect of the integrated rating mechanism is better in this situation.

Situation 4. When rating accuracyandsatisfiesand , the rating accuracy is reaching equilibrium.

We letandin the two mechanisms, and the equilibrium solutions of rating accuracy are: Based on the results of the direct effect in the first stage, we have: When , we haveand . This shows that the regulatory effect of the dual rating mechanism is better. When , we haveand . This indicates that the regulatory effect of the integrated rating mechanism is better.

Compared with the first stage, when the regulatory penalty conditions were added in the second stage, the indirect effect of the issuance of green bonds and the rating accuracy of green bonds were also affected by the regulatory penalty conditions. According to the analysis of the second stage of the game model, we can conclude the following:

(1) When the rating accuracy does not reach equilibrium, the conditions of usage of the dual rating mechanism are the indirect issuance effect in the dual rating mechanism and the indirect issuance effect in the integrated rating mechanism.

(2) When the rating accuracy does not reach equilibrium, the conditions of usage of the integrated rating mechanism are the indirect issuance effect in the dual rating mechanism and the indirect issuance effect .

(3) When the rating accuracy reaches equilibrium, the conditions of usage of the dual rating mechanism are , while the conditions of usage of the dual rating mechanism are .

Overall, we propose three propositions based on the analysis of this model:

Proposition 1. When the rating accuracy does not reach equilibrium, the conditions of usage of the dual rating mechanism are the direct issuance effectin the dual rating mechanism, the direct issuance effectin the integrated rating mechanism, the indirect issuance effectin the dual rating mechanism and the indirect issuance effectin the integrated rating mechanism.

Proposition 2. When the rating accuracy does not reach equilibrium, the conditions of usage of the integrated rating mechanism are the direct issuance effectin the dual rating mechanism, the direct issuance effect , the indirect issuance effectin the dual rating mechanism and the indirect issuance effect .

Proposition 3. When the rating accuracy reaches equilibrium, the conditions of usage of the dual rating mechanism are , while the conditions of usage of the integrated rating mechanism are without considering the indirect effect. When the rating accuracy reaches equilibrium, the conditions of usage of the dual rating mechanism are , while the conditions of usage of the dual rating mechanism arewith considering the indirect effect.

Propositions 1–3 indicate that the direct and indirect effects of green financing projects can effectively regulate the rating accuracy of green bonds according to the improved Hotelling model of difference, and compared with the direct effect, the indirect effect has more impact on rating regulatory. The value range of direct and indirect effects of green financing projects directly determines the regulatory effect under the two rating mechanisms. Regulators can choose different green bond rating mechanisms according to the actual situation to improve the quality of China’s green bond rating.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}