Determinants of Farming Households’ Credit Accessibility in Rural Areas of Vietnam: A Case Study in Haiphong City, Vietnam

Abstract

:1. Introduction

2. Literature Review

2.1. The Concept of Rural Credit Accessibility

2.2. Determinants of Access to Rural Credit in Some Developing Countries and Vietnam

3. The Rural Credit Markets in Vietnam

4. Materials and Methods

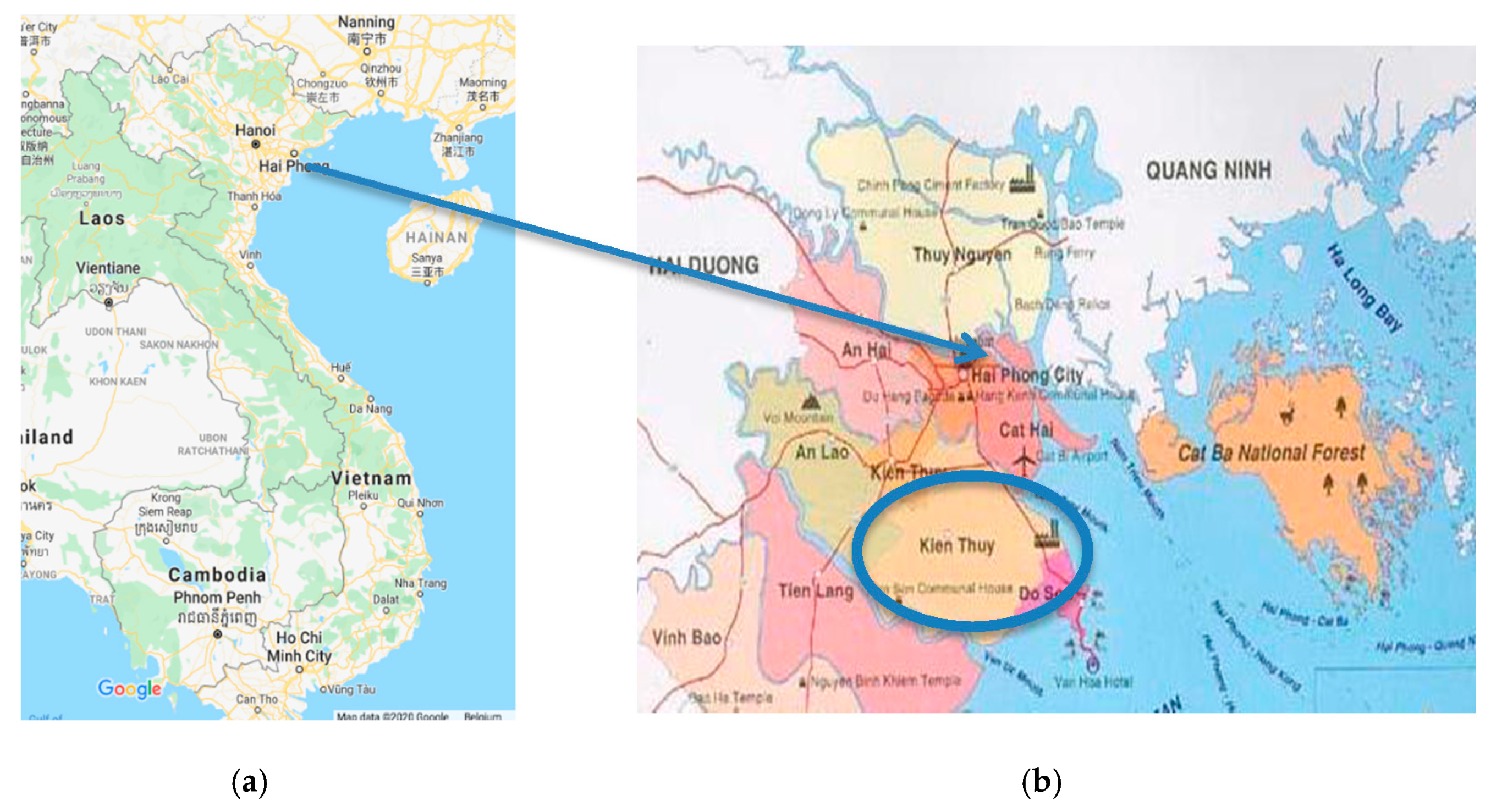

4.1. Selection of the Study Area

4.2. Data Collection

4.3. Empirical Models

4.4. Socioeconomic Description of the Sample

5. Results and Discussion

5.1. Determinants of Households’ Participation in the Credit Markets

5.2. Determinants of Borrowing Amounts of Households

6. Conclusions and Implications

Author Contributions

Funding

Conflicts of Interest

References

- Soubbotina, T.P.; Sheram, K. Beyond Economic Growth: Meeting the Challenges of Global Development; World Bank Publications: Washington, DC, USA, 2000. [Google Scholar]

- Guirkinger, C. Understanding the coexistence of formal and informal credit markets in Piura, Peru. World Dev. 2008, 36, 1436–1452. [Google Scholar] [CrossRef]

- HPSO. Haiphong Statistical Year Book; Statistic Publisher: Hanoi, Vietnam, 2018. [Google Scholar]

- Diagne, A.; Zeller, M.; Sharma, M. Empirical Measurements of Households’ Access to Credit and Credit Constraints in Developing Countries: Methodological Issues and Evidence; International Food Policy Research Institute: Washington, DC, USA, 2000. [Google Scholar]

- Zeller, M.; Ahmed, A.U.; Babu, S.C.; Broca, S.; Diagne, A.; Sharma, M.P. Rural Finance Policies for Food Security of the Poor: Methodologies for a Multicountry Research Project; International Food Policy Research Institute: Washington, DC, USA, 1996. [Google Scholar]

- Diagne, A.; Zeller, M. Access to Credit and Its Impact on Welfare in Malawi; International Food Policy Research Institute: Washington, DC, USA, 2001; Volume 116. [Google Scholar]

- Zeller, M. Determinants of credit rationing: A study of informal lenders and formal credit groups in Madagascar. World Dev. 1994, 22, 1895–1907. [Google Scholar] [CrossRef] [Green Version]

- Lin, L.; Wang, W.; Gan, C.; Cohen, D.A.; Nguyen, Q.T. Rural credit constraint and informal rural credit accessibility in China. Sustainability 2019, 11, 1935. [Google Scholar] [CrossRef] [Green Version]

- Evans, T.G.; Adams, A.M.; Mohammed, R.; Norris, A.H. Demystifying nonparticipation in microcredit: A population-based analysis. World Dev. 1999, 27, 419–430. [Google Scholar] [CrossRef]

- Gray, A. Credit Accessibility of Small-Scale Farmers and Fisherfolk in the Philippines; Lincoln University: Lincoln, UK, 2006. [Google Scholar]

- Hananu, B.; Abdul-Hanan, A.; Zakaria, H. Factors influencing agricultural credit demand in Northern Ghana. Afr. J. Agric. Res. 2015, 10, 645–652. [Google Scholar]

- Kosgey, Y.K.K. Agricultural credit access by grain growers in Uasin-Gishu County, Kenya. IOSR J. Econ. Fin 2013, 2, 36–52. [Google Scholar] [CrossRef]

- Luan, D.; Bauer, S.; Kuhl, R. Income Impacts of credit on accessed households in rural Vietnam: Do various credit sources perform differently? Agris On-Line Pap. Econ. Inf. 2016, 8, 57–67. [Google Scholar] [CrossRef] [Green Version]

- Barslund, M.; Tarp, F. Formal and informal rural credit in four provinces of Vietnam. J. Dev. Stud. 2008, 44, 485–503. [Google Scholar] [CrossRef]

- Yehuala, S. Determinants of Smallholder Farmers Access to Formal Credit: The Case of Metema Woreda; Haramaya University: North Gondar, Ethiopia, 2008. [Google Scholar]

- Akudugu, M. Estimation of the determinants of credit demand by farmers and supply by rural banks in Ghana’s Upper East Region. Asian J. Agric. Rural Dev. 2012, 2, 189–200. [Google Scholar]

- Sebatta, C.; Wamulume, M.; Mwansakilwa, C. Determinants of smallholder farmers’ access to agricultural finance in Zambia. J. Agric. Sci. 2014, 6, 63. [Google Scholar] [CrossRef]

- Mohieldin, M.S.; Wright, P.W. Formal and informal credit markets in Egypt. Econ. Dev. Cult. Chang. 2000, 48, 657–670. [Google Scholar] [CrossRef]

- Sharma, R.; Gupta, S.; Bala, B. Access to Credit-A Study of Hill Farms in Himachal Pradesh. J. Rural Dev.-Hyderabad 2007, 26, 483. [Google Scholar]

- Quach, H.; Mullineux, A. The impact of access to credit on household welfare in rural Vietnam. Res. Account. Emerg. Econ. 2007, 7, 279–307. [Google Scholar]

- Duy, V.Q.; D’Haese, M.; Lemba, J.; D’Haese, L. Determinants of household access to formal credit in the rural areas of the Mekong Delta, Vietnam. Afr. Asian Stud. 2012, 11, 261–287. [Google Scholar] [CrossRef] [Green Version]

- Li, X.; Gan, C.; Hu, B. Accessibility to microcredit by Chinese rural households. J. Asian Econ. 2011, 22, 235–246. [Google Scholar] [CrossRef] [Green Version]

- Okurut, F.N.; Schoombee, A.; Van der Berg, S. Credit Demand and Credit Rationing in the Informal Financial Sector in Uganda 1. S. Afr. J. Econ. 2005, 73, 482–497. [Google Scholar] [CrossRef] [Green Version]

- Saleem, A.; Jan, F.A.; Khattak, R.M.; Quraishi, M.I. Impact of Farm and Farmers Characteristics on Repayment of Agriculture Credit. Abasyn Univ. J. Soc. Sci. 2011, 4, 23–35. [Google Scholar]

- Field, E.; Torero, M. Do Property Titles Increase Credit Access among the Urban Poor? Evidence from a Nationwide Titling Program; Working Paper; Department of Economics, Harvard University: Cambridge, MA, USA, 2006. [Google Scholar]

- Chandio, A.A.; Jiang, Y. Determinants of Credit Constraints: Evidence from Sindh, Pakistan. Emerg. Mark. Financ. Trade 2018, 54, 3401–3410. [Google Scholar] [CrossRef]

- Duniya, K.; Adinah, I. Probit analysis of cotton farmers’ accessibility to credit in northern guinea savannah of Nigeria. Asian J. Agric. Ext. Econ. Sociol. 2015, 296–301. [Google Scholar] [CrossRef]

- Oboh, V.U.; Ekpebu, I.D. Determinants of formal agricultural credit allocation to the farm sector by arable crop farmers in Benue State, Nigeria. Afr. J. Agric. Res. 2011, 6, 181–185. [Google Scholar]

- Bao Duong, P.; Izumida, Y. Rural Development Finance in Vietnam: A Microeconometric Analysis of Household Surveys. World Dev. 2002, 30, 319–335. [Google Scholar] [CrossRef]

- Khoi, P.D.; Gan, C.; Nartea, G.V.; Cohen, D.A. Formal and informal rural credit in the Mekong River Delta of Vietnam: Interaction and accessibility. J. Asian Econ. 2013, 26, 1–13. [Google Scholar] [CrossRef]

- Rahji, M.; Fakayode, S. A multinomial logit analysis of agricultural credit rationing by commercial banks in Nigeria. Int. Res. J. Financ. Econ. 2009, 24, 97–103. [Google Scholar]

- Ayamga, M.; Sarpong, D.; Asuming-Brempong, S. Factors influencing the decision to participate in micro-credit programme: An illustration for Northern Ghana. Ghana J. Dev. Stud. 2006, 3, 57–65. [Google Scholar] [CrossRef] [Green Version]

- Bigsten, A.; Collier, P.; Dercon, S.; Fafchamps, M.; Gauthier, B.; Gunning, J.W.; Oduro, A.; Oostendorp, R.; Patillo, C.; Söderbom, M. Credit constraints in manufacturing enterprises in Africa. J. Afr. Econ. 2003, 12, 104–125. [Google Scholar] [CrossRef]

- Heltberg, R. Rural market imperfections and the farm size—productivity relationship: Evidence from Pakistan. World Dev. 1998, 26, 1807–1826. [Google Scholar] [CrossRef]

- Rahman, S.; Hussain, A.; Taqi, M. Impact of agricultural credit on agricultural productivity in Pakistan: An empirical analysis. Int. J. Adv. Res. Manag. Soc. Sci. 2014, 3, 125–139. [Google Scholar]

- Hussain, A.; Thapa, G.B. Smallholders’ access to agricultural credit in Pakistan. Food Secur. 2012, 4, 73–85. [Google Scholar] [CrossRef]

- Saqib, S.E.; Ahmad, M.M.; Panezai, S. Landholding size and farmers’ access to credit and its utilisation in Pakistan. Dev. Pract. 2016, 26, 1060–1071. [Google Scholar] [CrossRef]

- Zeller, M.; Diagne, A.; Mataya, C. Market access by smallholder farmers in Malawi: Implications for technology adoption, agricultural productivity and crop income. Agric. Econ. 1998, 19, 219–229. [Google Scholar] [CrossRef]

- Linh, T.N.; Long, H.T.; Chi, L.V.; Tam, L.T.; Lebailly, P. Access to rural credit markets in developing countries, the case of Vietnam: A literature review. Sustainability 2019, 11, 1468. [Google Scholar] [CrossRef] [Green Version]

- Grootaert, C.; Oh, G.T.; Swamy, A. Social capital, household welfare and poverty in Burkina Faso. J. Afr. Econ. 2002, 11, 4–38. [Google Scholar] [CrossRef]

- Okten, C.; Osili, U.O. Social networks and credit access in Indonesia. World Dev. 2004, 32, 1225–1246. [Google Scholar] [CrossRef]

- Luan, D.X.; Bauer, S. Does credit access affect household income homogeneously across different groups of credit recipients? Evidence from rural Vietnam. J. Rural Stud. 2016, 47, 186–203. [Google Scholar] [CrossRef]

- Kochar, A. An empirical investigation of rationing constraints in rural credit markets in India. J. Dev. Econ. 1997, 53, 339–371. [Google Scholar] [CrossRef]

- Pham, T.T.T.; Lensink, R. Lending policies of informal, formal and semiformal lenders: Evidence from Vietnam. Econ. Transit. 2007, 15, 181–209. [Google Scholar] [CrossRef]

- Siamwalla, A.; Pinthong, C.; Poapongsakorn, N.; Satsanguan, P.; Nettayarak, P.; Mingmaneenakin, W.; Tubpun, Y. The Thai rural credit system: Public subsidies, private information, and segmented markets. World Bank Econ. Rev. 1990, 4, 271–295. [Google Scholar] [CrossRef]

- Nagarajan, G.; Meyer, R.L.; Hushak, L.J. Demand For Agricultural Loans: A Theoretical And Econometric Analysis Of The Philippine Credit Market/La Demande De Prêts Agricoles: Une Analyse Théorique Et Économique Du Marché De Crédit Aux Philippines. Sav. Dev. 1998, 22, 349–363. [Google Scholar]

- Ghosh, R.; Gupta, K.R.; Maiti, P. Development Studies; Atlantic Publishers & Dist: New Delhi, India, 2008; Volume 3, p. 5. [Google Scholar]

- Thornton, P.K.; van de Steeg, J.; Notenbaert, A.; Herrero, M. The impacts of climate change on livestock and livestock systems in developing countries: A review of what we know and what we need to know. Agric. Syst. 2009, 101, 113–127. [Google Scholar] [CrossRef]

- Tanaka, T.; Camerer, C.F.; Nguyen, Q. Risk and time preferences: Linking experimental and household survey data from Vietnam. Am. Econ. Rev. 2010, 100, 557–571. [Google Scholar] [CrossRef] [Green Version]

- Marsh, S.P.; MacAulay, T.G.; Hung, P.V. Agricultural Development and Land Policy in Vietnam; Australian Centre for International Agricultural Research (ACIAR): Canberra, Australia, 2006; p. 272.

- GSO. Vietnam Statistical Yearbook; Statistic Publisher: Hanoi, Vietnam, 2018. [Google Scholar]

- Dinh, Q.H.; Dufhues, T.B.; Buchenrieder, G. Do connections matter? Individual social capital and credit constraints in Vietnam. Eur. J. Dev. Res. 2012, 24, 337–358. [Google Scholar] [CrossRef]

{kind=link}

| Variables | Description |

|---|---|

| Age | Age of household head (year) |

| Gender | Gender of household head, man = 1, woman = 0 |

| Education | Education levels of household head (year of schooling) |

| Farming Experience | Farming experience of household head (year) |

| Occupation | 1 = Head of family is farmers only; 0 = otherwise |

| People in family | Total people in a family (person) |

| Dependency ratio | People without income/People in family |

| Ln_farm_land | Log of value of farm land (land for farming activities) (m2 ) |

| Ln_owned_land | Log of value of dwelling land with ownership certificate (m2) |

| Ln_agri_income | Log of value of income from agriculture production (million VND) |

| Non_agri_income | Income from non-agriculture activities (million VND) |

| Ln_total income | Log of (Agri_income + Non_agri_income) |

| Connection | 1 = having job related to government or have acquaintances in financial institutions, 0 = otherwise |

| Group membership | Member of a credit group: 1 = yes, 0 = no |

| Livestock | Value of household in cash at purchase (thousand VND) |

| Number of households | 180 samples of 4 communes |

| Unit | Minimum | Maximum | Mean | Std. Deviation | |

|---|---|---|---|---|---|

| Age | Years | 29 | 70 | 51,483 | 7802 |

| Education | Years of schooling | 5 | 12 | 8706 | 1827 |

| Farming Experience | Years | 8 | 50 | 29,183 | 7859 |

| Occupation | − | 0 | 1 | 0.639 | 0.482 |

| People in a family | Person | 1 | 6 | 2994 | 1049 |

| Dependency ratio | − | 0 | 0.67 | 0.162 | 0.221 |

| Farm land | m2 | 100 | 18,000 | 4046.056 | 2495.604 |

| Owned land | m2 | 75 | 7200 | 445.572 | 561.753 |

| Agri_income | Million VND | 20 | 1000 | 193.228 | 159.447 |

| Non_agri_income | Million VND | 0 | 360 | 67,822 | 68,976 |

| Total_income | Million VND | 30 | 1300 | 261.050 | 187.531 |

| Livestock | Million VND | 32,000 | 3030.000 | 667,983.333 | 516,065.646 |

| Network connection | − | 0 | 1 | 0.633 | 0.483 |

| Formal amount | Million VND | 20 | 1000 | 105.688 | 141.626 |

| Informal amount | Million VND | 15 | 1100 | 242.182 | 160.207 |

| Number of observations | 180 | ||||

| Total | Tu Son | Tan Phong | Ngu Doan | Ngu Phuc | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Number of HHs | % | Number of HHs | % | Number of HHs | % | Number of HHs | % | Number of HHs | % | |

| None | 18 | 10 | 2 | 4.3 | 1 | 2.3 | 5 | 11.1 | 10 | 22.7 |

| Formal | 19 | 10.6 | 3 | 6.4 | 0 | 0 | 10 | 22.2 | 6 | 13.6 |

| Informal | 53 | 29.4 | 14 | 29.8 | 16 | 36.4 | 12 | 26.7 | 11 | 25 |

| Both | 90 | 50 | 28 | 59.6 | 27 | 61.4 | 18 | 40 | 17 | 38.6 |

| Total | 180 | 100 | 47 | 100 | 44 | 100 | 45 | 100 | 44 | 100 |

| Formal Sources | VBARD | VBSP | VBARD and VBSP | PCF | PCF and VBSP | Subtotal | Total Sample |

|---|---|---|---|---|---|---|---|

| Number of HHs | 22 | 61 | 9 | 16 | 1 | 109 | 180 |

| % | 20.18 | 55.96 | 8.26 | 14.68 | 0.92 | 100 |

| Informal Sources | Relatives/Friends | Local Sellers | CSG * | Relatives & Local Sellers | CSG & Local Sellers | Money Lenders & Local Sellers | Relatives & CSG | Sub- Total | Total Sample |

|---|---|---|---|---|---|---|---|---|---|

| Number of HHs | 1 | 91 | 7 | 19 | 18 | 3 | 2 | 141 | 180 |

| % | 0.71 | 64.54 | 4.96 | 13.48 | 12.77 | 2.13 | 1.42 | 100 |

| All Sources | Formal Sources | Informal Sources | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Coefficient | S.E. | Sig. | Coefficient | S.E. | Sig. | Coefficient | S.E. | Sig. | |

| Age | 0.032 | 0.074 | 0.671 | 0.153 | 0.108 | 0.157 | −0.057 | 0.047 | 0.223 |

| Gender | 0.179 | 0.731 | 0.807 | 2487 | 1348 | 0.065 * | −0.203 | 0.456 | 0.656 |

| Education | 0.197 | 0.204 | 0.335 | 0.025 | 0.301 | 0.935 | 0.141 | 0.138 | 0.306 |

| Occupation | 0.467 | 0.739 | 0.528 | −0.180 | 1793 | 0.920 | 0.517 | 0.477 | 0.279 |

| Group_membership | 20,449 | 3801.872 | 0.996 | 12,521 | 3746 | 0.001 *** | 0.469 | 0.553 | 0.396 |

| Ln_owned_land | −0.607 | 0.712 | 0.394 | −0.469 | 0.787 | 0.552 | −0.356 | 0.400 | 0.374 |

| Ln_agri_income | 0.267 | 0.587 | 0.650 | 0.877 | 0.956 | 0.359 | 0.723 | 0.362 | 0.046 ** |

| Dependency_ratio | −1532 | 2516 | 0.543 | 6513 | 3864 | 0.092 * | −3398 | 1644 | 0.039 ** |

| Tuson | 2.18 | 1025 | 0.033 ** | 4640 | 2403 | 0.054 * | 1089 | 0.724 | 0.132 |

| Tanphong | 2701 | 1342 | 0.044 ** | 2755 | 2561 | 0.282 | 2534 | 1152 | 0.028 ** |

| Ngudoan | 0.631 | 1076 | 0.558 | −1.301 | 2125 | 0.540 | −0.378 | 0.670 | 0.573 |

| Ln_farm_land | 0.301 | 0.847 | 0.723 | 1024 | 0.902 | 0.256 | 0.202 | 0.296 | 0.495 |

| Connection | 0.265 | 0.843 | 0.753 | 5521 | 1787 | 0.002 *** | 0.018 | 0.584 | 0.975 |

| Constant | −3445 | 8208 | 0.675 | −28,993 | 11,368 | 0.011 | −0.209 | 4067 | 0.959 |

| Observations | 180 | 180 | 180 | ||||||

| −2 Log Likelihood | 69,825 | 33,467 | 144 | ||||||

| Omnibus tests of model coefficients | Chi-square: 47,204 (Sig. 0.000) | Chi-square: 20,783 (Sig. 0.000) | Chi-square: 44,153 (Sig. 0.000) | ||||||

| Hosmer and Lemeshow test | Chi-square: 4891 (df: 8, Sig. 0.769) | Chi-square: 9329 (df: 8, Sig. 0.315) | Chi-square: 3369 (df: 8, Sig. 0.909) | ||||||

| Correct Predicted Percentage | 91.1 | 98.3 | 81.7 | ||||||

| Coefficient | S.E. | Sig. | |

|---|---|---|---|

| Age | 0.156 | 0.111 | 0.161 |

| Gender | 2529 | 1362 | 0.063 * |

| Education | 0.013 | 0.309 | 0.967 |

| Occupation | −0.040 | 1855 | 0.983 |

| Group_membership | 12,507 | 3743 | 0.001 *** |

| Ln_owned_land | −0.526 | 0.809 | 0.516 |

| ln_agri_income | 0.926 | 0.966 | 0.338 |

| Dependent_ratio | 6486 | 3928 | 0.099 * |

| Tuson | 4791 | 2485 | 0.054 * |

| Tanphong | 2868 | 2602 | 0.27 |

| Ngudoan | −1355 | 2110 | 0.521 |

| Ln_farm_land | 1008 | 0.902 | 0.264 |

| Connection | 5572 | 1838 | 0.002 *** |

| Borrowing_informal | −0.385 | 1352 | 0.776 |

| Constant | −28,795 | 11,504 | 0.012 |

| Observations | 180 | ||

| −2 Log Likelihood | 33,349 | ||

| Hosmer and Lemeshow test | Chi-square: 9243 (df: 8, Sig. 0.322) | ||

| Correct Predicted Percentage | 97.8 |

| Formal | Informal | |||||||

|---|---|---|---|---|---|---|---|---|

| Based | Extended | Based | Extended | |||||

| Coefficients | Sig. | Coefficients | Sig. | Coefficients | Sig. | Coefficients | Sig. | |

| (Constant) | 1109 | 0.378 | −0.183 | 0.898 | 0.486 | 0.511 | −0.505 | 0.597 |

| Age | 0.005 | 0.688 | 0.009 | 0.436 | 0.001 | 0.933 | 0.001 | 0.888 |

| Gender | −0.133 | 0.299 | −0.143 | 0.277 | 0.030 | 0.663 | 0.096 | 0.260 |

| Education | 0.003 | 0.934 | −0.008 | 0.829 | 0.001 | 0.961 | −0.014 | 0.556 |

| Occupation | −0.259 | 0.066 * | −0.212 | 0.140 | 0.122 | 0.122 | 0.318 | 0.002 *** |

| Group_membership | −0.997 | 0.000 *** | −0.909 | 0.00 *** | −0.047 | 0.572 | −0.063 | 0.555 |

| ln_owned_land | 0.085 | 0.443 | 0.169 | 0.198 | 0.037 | 0.547 | 0.094 | 0.262 |

| ln_agri_income | 0.239 | 0.014 ** | 0.827 | 0.000 *** | ||||

| Dependency_ratio | 0.308 | 0.418 | 0.046 | 0.916 | 0.005 | 0.983 | 0.246 | 0.428 |

| Tuson | −0.145 | 0.512 | −0.013 | 0.952 | 0.526 | 0.000 *** | 0.808 | 0.000 *** |

| Tanphong | −0.218 | 0.315 | −0.094 | 0.65 | 0.459 | 0.000 *** | 0.701 | 0.000 *** |

| Ngudoan | 0.059 | 0.776 | 0.192 | 0.345 | 0.449 | 0.001 *** | 0.746 | 0.000 *** |

| ln_farm_land | 0.238 | 0.003 *** | 0.257 | 0.001 *** | −0.026 | 0.659 | 0.041 | 0.553 |

| Connection | 0.287 | 0.185 | 0.27 | 0.216 | 0.047 | 0.605 | 0.228 | 0.050 * |

| Total people | 0.124 | 0.14 | −0.091 | 0.102 | ||||

| ln_total_income | 0.223 | 0.054 * | 0.763 | 0.000 *** | ||||

| Observations | 109 | 109 | 141 | 141 | ||||

| R square | 0.553 | 0.549 | 0.799 | 0.701 | ||||

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Linh, T.N.; Anh Tuan, D.; Thu Trang, P.; Trung Lai, H.; Quynh Anh, D.; Viet Cuong, N.; Lebailly, P. Determinants of Farming Households’ Credit Accessibility in Rural Areas of Vietnam: A Case Study in Haiphong City, Vietnam. Sustainability 2020, 12, 4357. https://doi.org/10.3390/su12114357

Linh TN, Anh Tuan D, Thu Trang P, Trung Lai H, Quynh Anh D, Viet Cuong N, Lebailly P. Determinants of Farming Households’ Credit Accessibility in Rural Areas of Vietnam: A Case Study in Haiphong City, Vietnam. Sustainability. 2020; 12(11):4357. https://doi.org/10.3390/su12114357

Chicago/Turabian StyleLinh, Ta Nhat, Dang Anh Tuan, Phan Thu Trang, Hoang Trung Lai, Do Quynh Anh, Nguyen Viet Cuong, and Philippe Lebailly. 2020. "Determinants of Farming Households’ Credit Accessibility in Rural Areas of Vietnam: A Case Study in Haiphong City, Vietnam" Sustainability 12, no. 11: 4357. https://doi.org/10.3390/su12114357