Is Factor Investing Sustainable after Price Impact Costs? The Capacity of Factor Investing in Korea

Abstract

:1. Introduction

2. Literature Review

2.1. Stock Market Anomalies and Factor Investing

2.2. Price Impact Costs

3. Methodology

3.1. Transaction Costs Due to the Price Impact

3.2. Estimation of BHK Price Impact Factors

3.3. Factor Investment Strategy

4. Empirical Results

4.1. Data

4.2. Price Impact Coefficient

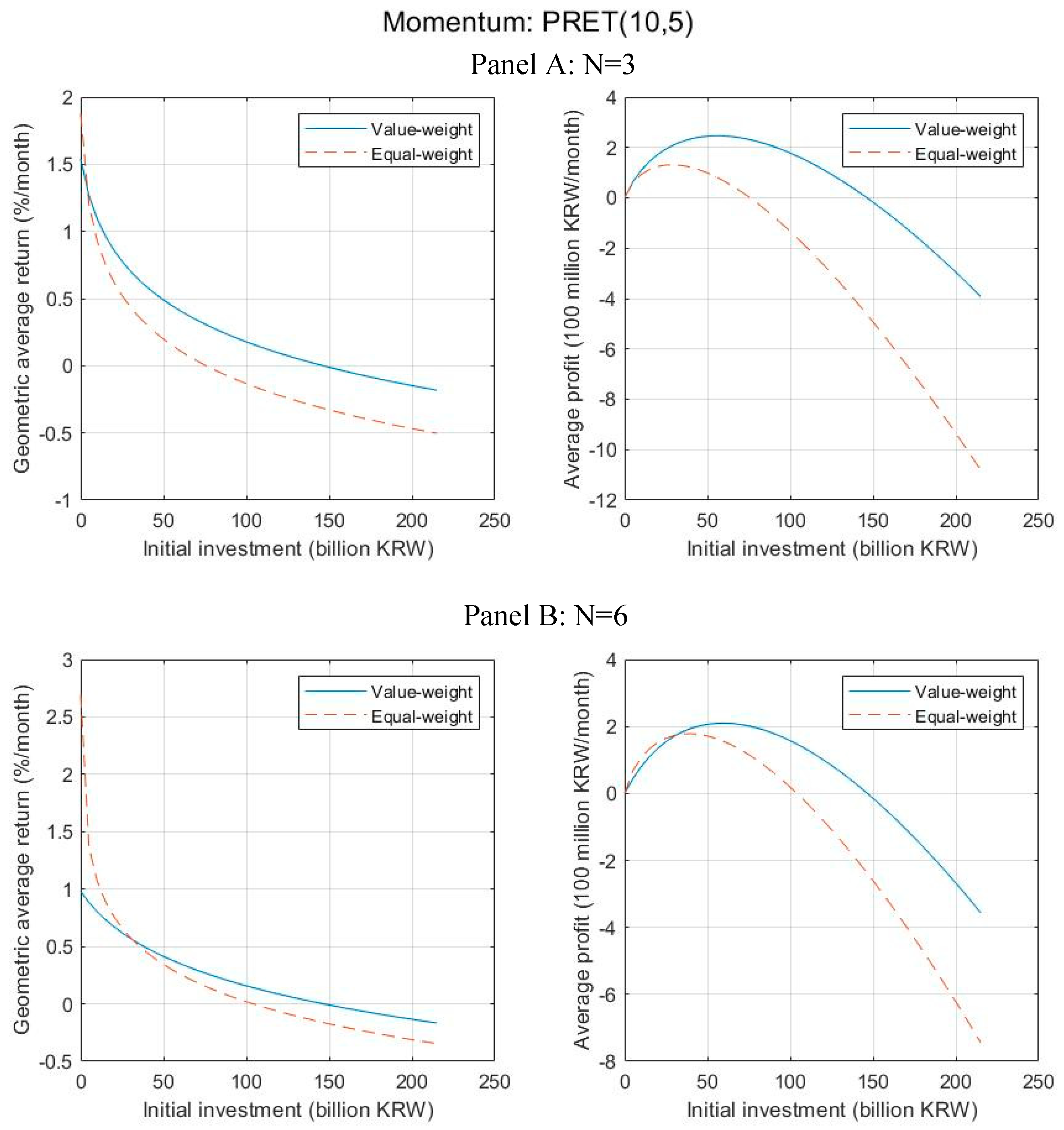

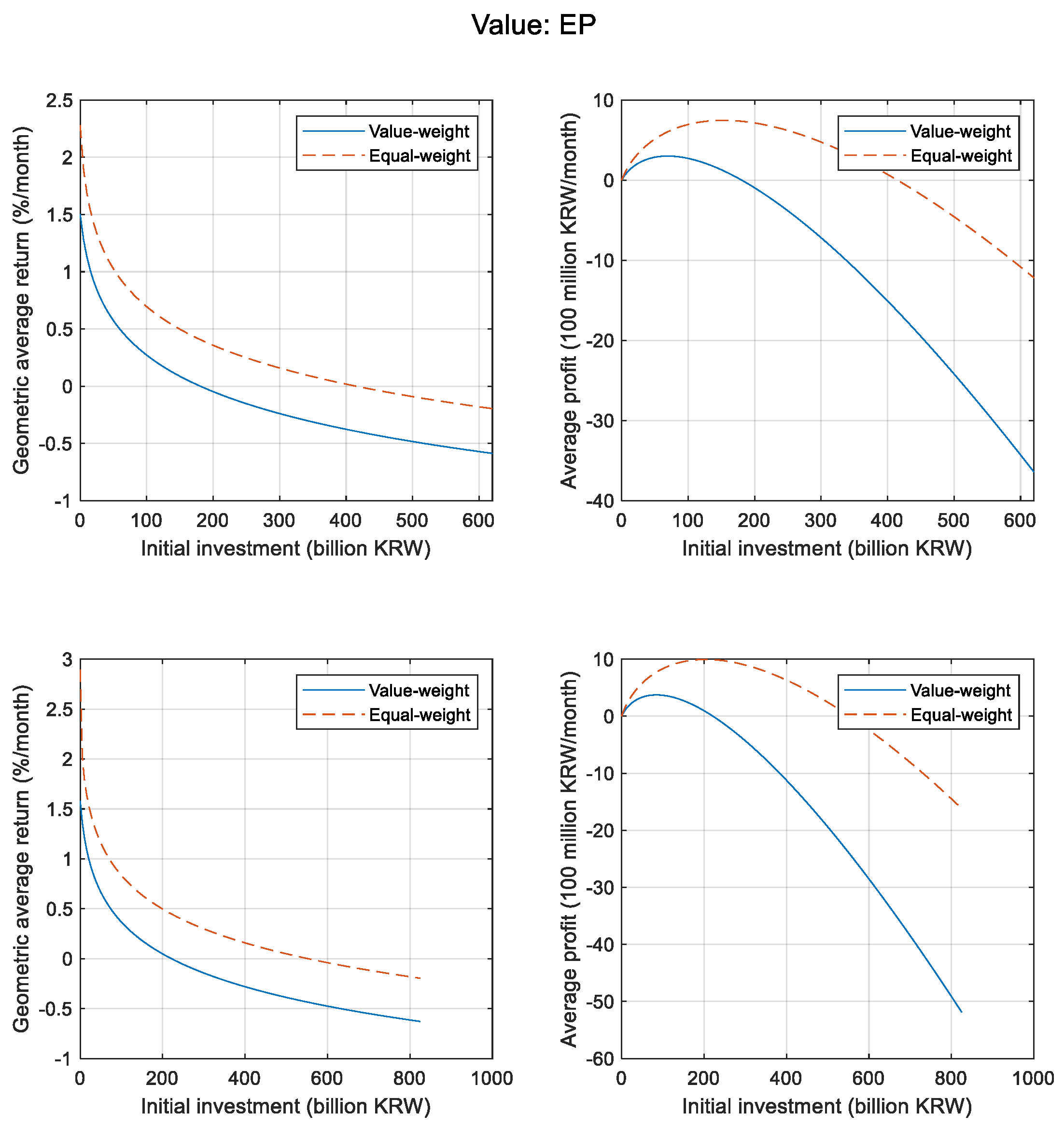

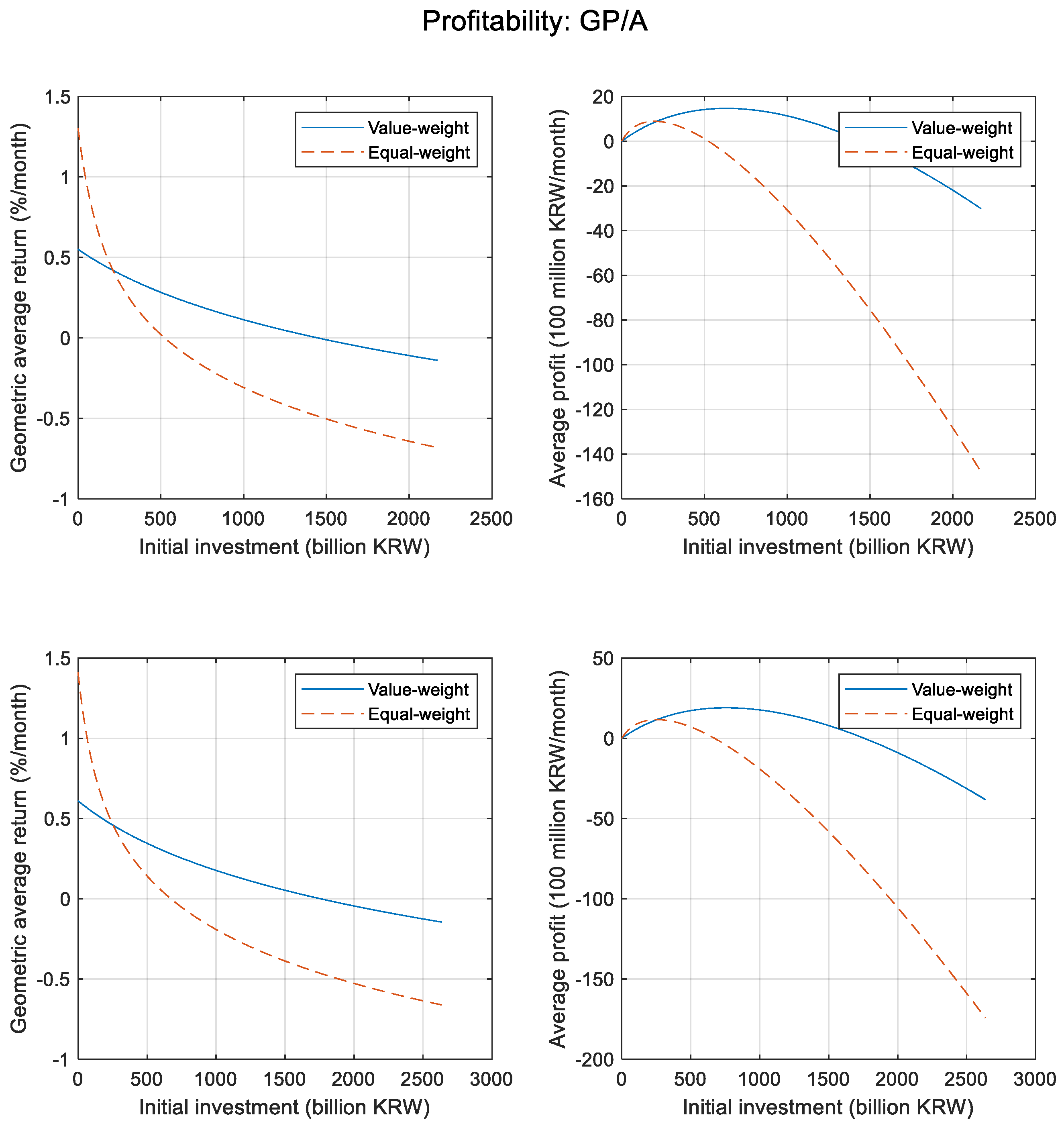

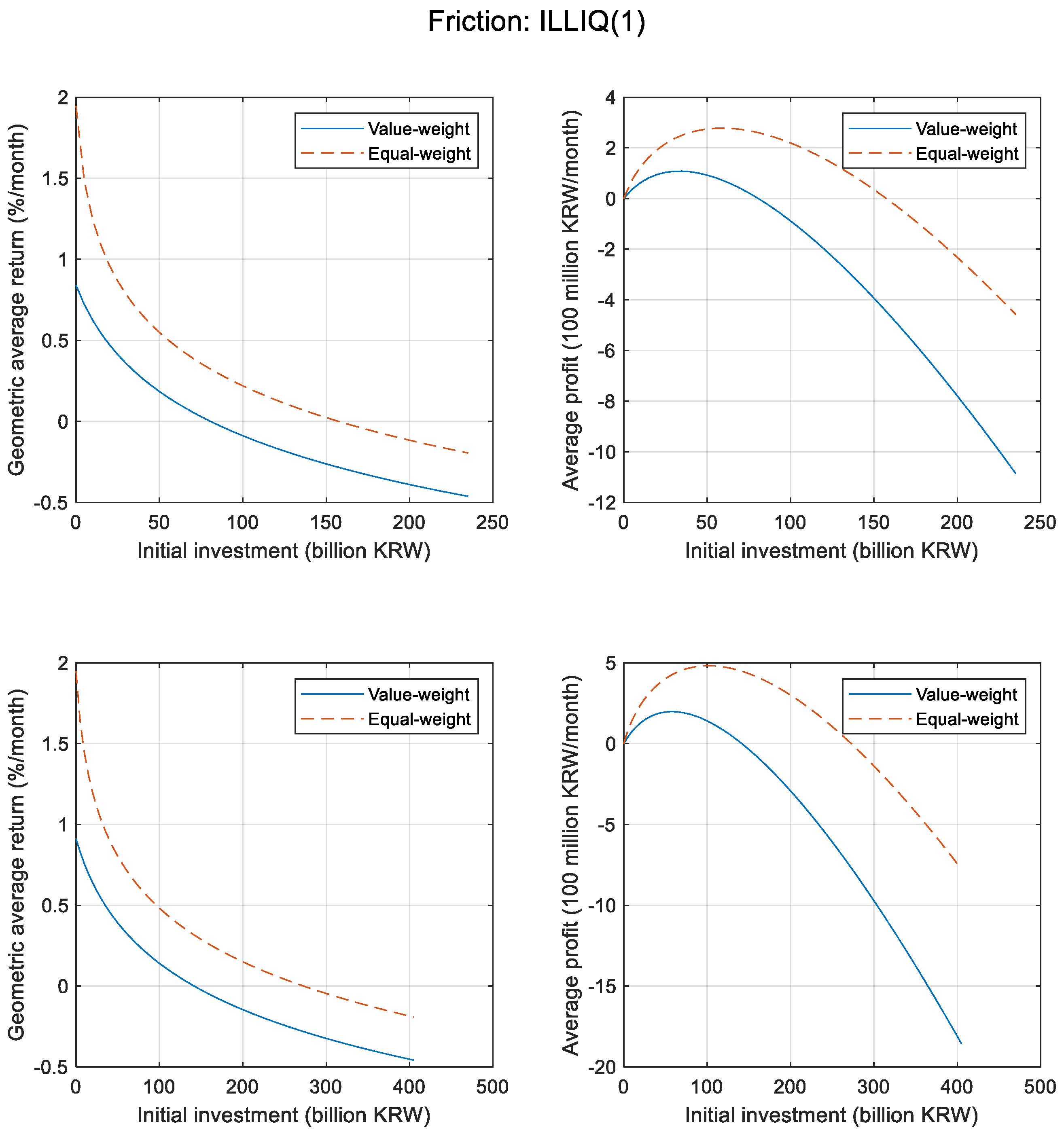

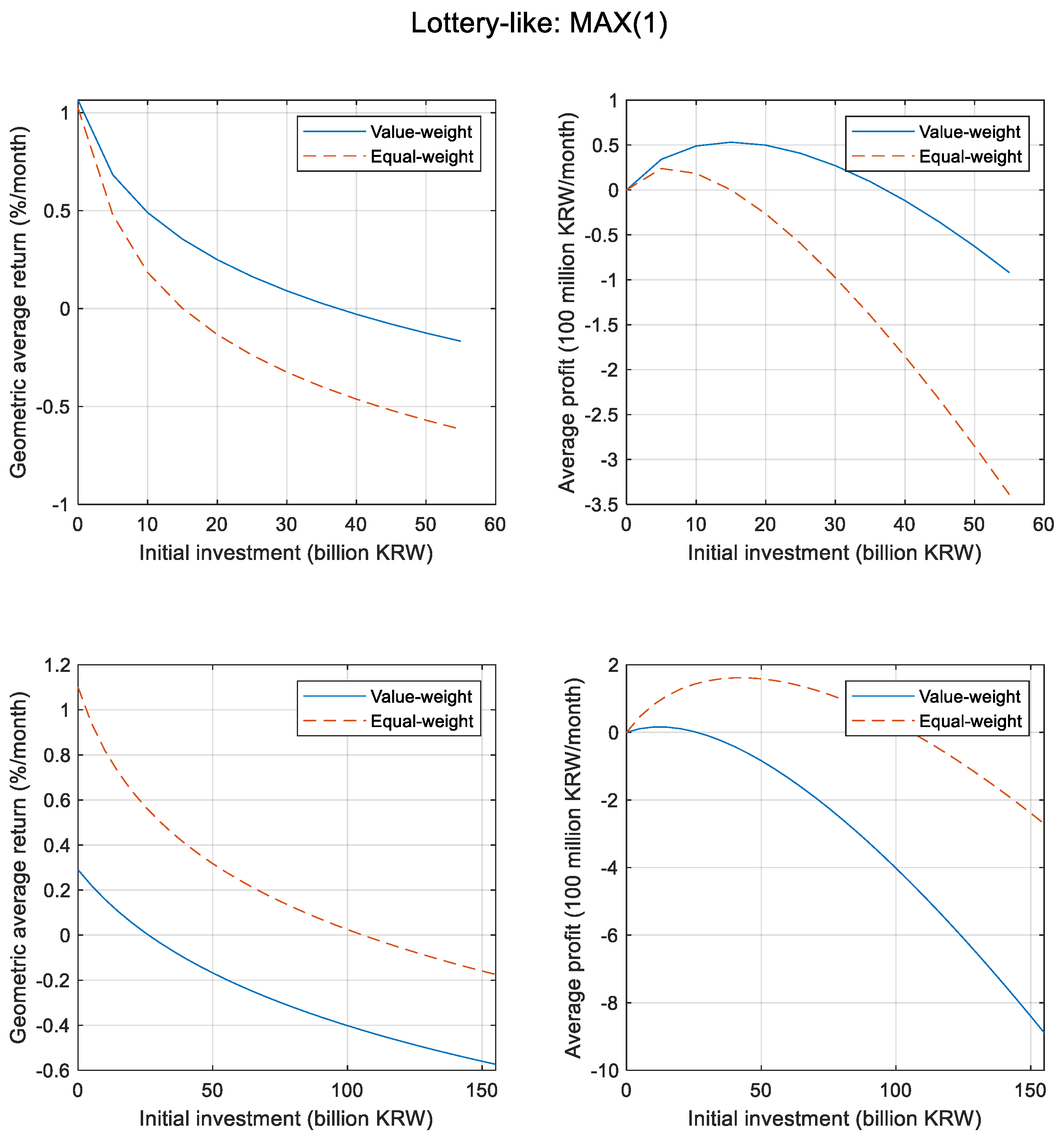

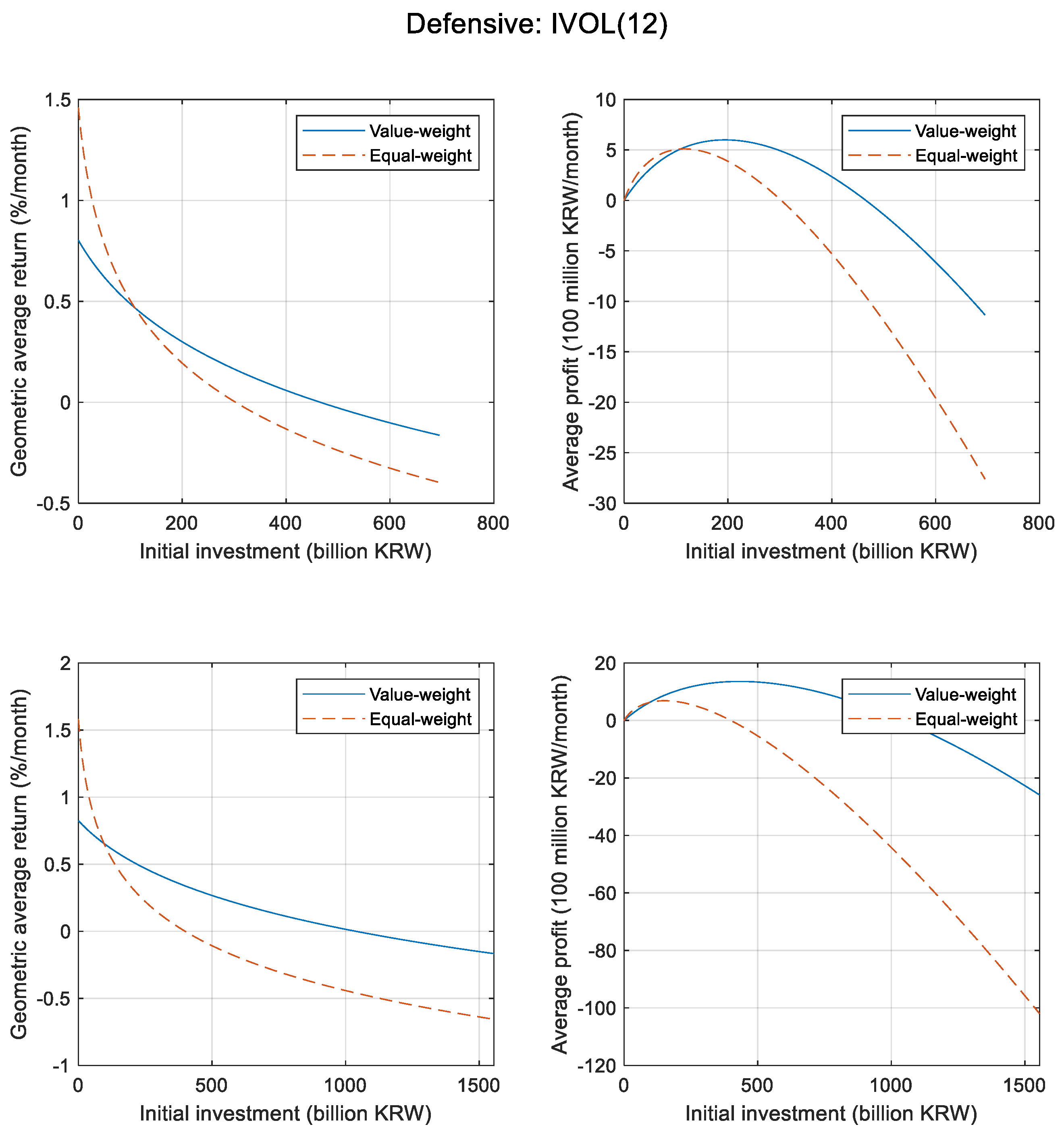

4.3. Estimation of Terminal Capacity: Break-Even Approach

4.4. Estimation of Wealth-Maximizing Capacity

4.5. Other Factor Investment Strategies

5. Discussion

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Clarke, R.; de Silva, H.; Thorley, S. Fundamentals of Efficient Factor Investing (corrected May 2017). Financ. Anal. J. 2016, 72, 9–26. [Google Scholar] [CrossRef]

- Dimson, E.; Marsh, P.; Staunton, M. Factor-Based Investing: The Long-Term Evidence. J. Portf. Manag. 2017, 43, 15–37. [Google Scholar] [CrossRef]

- van Gelderen, E.; Huij, J. Academic Knowledge Dissemination in the Mutual Fund Industry: Can Mutual Funds Successfully Adopt Factor Investing Strategies? J. Portf. Manag. 2014, 40, 157–167. [Google Scholar] [CrossRef]

- Houweling, P.; van Zundert, J. Factor Investing in the Corporate Bond Market. Financ. Anal. J. 2017, 73, 100–115. [Google Scholar] [CrossRef]

- Kim, J.H.; Kim, W.C.; Fabozzi, F.J. Robust Factor-Based Investing. J. Portf. Manag. 2017, 43, 157–164. [Google Scholar] [CrossRef]

- Asness, C.; Frazzini, A.; Israel, R.; Moskowitz, T. Fact, Fiction, and Momentum Investing. J. Portf. Manag. 2014, 40, 75–92. [Google Scholar] [CrossRef]

- Harvey, C.R.; Liu, Y.; Zhu, H. … and the Cross-Section of Expected Returns. Rev. Financ. Stud. 2016, 29, 5–68. [Google Scholar] [CrossRef]

- Hou, K.; Xue, C.; Zhang, L. Replicating Anomalies. Rev. Financ. Stud. 2018. [Google Scholar] [CrossRef]

- Linnainmaa, J.T.; Roberts, M.R. The History of the Cross-Section of Stock Returns. Rev. Financ. Stud. 2018, 31, 2606–2649. [Google Scholar] [CrossRef] [Green Version]

- Parmler, J.; González, A. Is Momentum Due to Data-snooping? Eur. J. Financ. 2007, 13, 301–318. [Google Scholar] [CrossRef] [Green Version]

- Engelberg, J.; Mclean, R.D.; Pontiff, J. Anomalies and News. J. Financ. 2018, 73, 1971–2001. [Google Scholar] [CrossRef]

- Scharfstein, D.S.; Stein, J.C. Herd Behavior and Investment. Am. Econ. Rev. 1990, 80, 465–479. [Google Scholar]

- Banerjee, A.V. A Simple Model of Herd Behavior. Q. J. Econ. 1992, 107, 797–817. [Google Scholar] [CrossRef] [Green Version]

- Marquering, W.; Nisser, J.; Valla, T. Disappearing anomalies: A dynamic analysis of the persistence of anomalies. Appl. Financ. Econ. 2006, 16, 291–302. [Google Scholar] [CrossRef]

- Krkoska, E.; Schenk-Hoppé, K.R. Herding in Smart-Beta Investment Products. J. Risk Financ. Manag. 2019, 12, 47. [Google Scholar] [CrossRef]

- Chui, A.C.W.; Wei, K.C.J. Book-to-market, firm size, and the turn-of-the-year effect: Evidence from Pacific-Basin emerging markets. Pac.-Basin Financ. J. 1998, 6, 275–293. [Google Scholar] [CrossRef] [Green Version]

- Hameed, A.; Kusnadi, Y. Momentum Strategies: Evidence from Pacific Basin Stock Markets. J. Financ. Res. 2002, 25, 383–397. [Google Scholar] [CrossRef]

- Cakici, N.; Fabozzi, F.J.; Tan, S. Size, value, and momentum in emerging market stock returns. Emerg. Mark. Rev. 2013, 16, 46–65. [Google Scholar] [CrossRef]

- Nartea, G.V.; Wu, J.; Liu, H.T. Extreme returns in emerging stock markets: evidence of a MAX effect in South Korea. Appl. Financ. Econ. 2014, 24, 425–435. [Google Scholar] [CrossRef]

- Hung, C.-H.D.; Banerjee, A.N. How do momentum strategies ‘score’ against individual investors in Taiwan, Hong Kong and Korea? Emerg. Mark. Rev. 2014, 21, 67–81. [Google Scholar] [CrossRef]

- Jegadeesh, N.; Titman, S. Returns to buying winners and selling losers: Implications for stock market efficiency. J. Financ. 1993, 48, 65–91. [Google Scholar] [CrossRef]

- Domowitz, I.; Glen, J.; Madhavan, A. Liquidity, Volatility and Equity Trading Costs Across Countries and Over Time. Int. Financ. 2001, 4, 221–255. [Google Scholar] [CrossRef] [Green Version]

- O’Neill, M.J.; Warren, G.J. Evaluating fund capacity: Issues and methods. Account. Financ. 2019, 59, 773–800. [Google Scholar] [CrossRef]

- Korajczyk, R.A.; Sadka, R. Are momentum profits robust to trading costs? J. Financ. 2004, 59, 1039–1082. [Google Scholar] [CrossRef]

- Chen, Z.; Stanzl, W.; Watanabe, M. Price Impact Costs and the Limit of Arbitrage. Yale School of Management Working Paper Ysm251 2002. Yale School of Management, revised 08 Jun 2006. Available online: https://ideas.repec.org/p/ysm/somwrk/ysm251.html (accessed on 29 July 2019).

- Frazzini, A.; Israel, R.; Moskowitz, T.J. Trading Costs of Asset Pricing Anomalies. Fama-Miller Working Paper. Available online: https://ssrn.com/abstract=2294498 or http://dx.doi.org/10.2139/ssrn.2294498 (accessed on 29 July 2019).

- Novy-Marx, R.; Velikov, M. A Taxonomy of Anomalies and Their Trading Costs. Rev. Financ. Stud. 2016, 29, 104–147. [Google Scholar] [CrossRef]

- Li, F.; Chow, T.-M.; Pickard, A.; Garg, Y. Transaction Costs of Factor-Investing Strategies. Financ. Anal. J. 2019, 75, 62–78. [Google Scholar] [CrossRef] [Green Version]

- Ratcliffe, R.; Miranda, P.; Ang, A. Capacity of Smart Beta Strategies from a Transaction Cost Perspective. J. Index Invest. 2017, 8, 39–50. [Google Scholar] [CrossRef]

- Blitz, D.; Marchesini, T. The Capacity of Factor Strategies. J. Portf. Manag. 2019. [Google Scholar] [CrossRef]

- Bertsimas, D.; Lo, A.W. Optimal control of execution costs. J. Financ. Mark. 1998, 1, 1–50. [Google Scholar] [CrossRef]

- Breen, W.J.; Hodrick, L.S.; Korajczyk, R.A. Predicting Equity Liquidity. Manag. Sci. 2002, 48, 470–483. [Google Scholar] [CrossRef] [Green Version]

- Kyle, A.S. Continuous Auctions and Insider Trading. Econometrica 1985, 53, 1315–1335. [Google Scholar] [CrossRef]

- Hasbrouck, J. Trades, quotes, inventories, and information. J. Financ. Econ. 1988, 22, 229–252. [Google Scholar] [CrossRef]

- Hasbrouck, J. Measuring the information content of stock trades. J. Financ. 1991, 46, 179–207. [Google Scholar] [CrossRef]

- Hasbrouck, J. Trading Costs and Returns for U.S. Equities: Estimating Effective Costs from Daily Data. J. Financ. 2009, 64, 1445–1477. [Google Scholar] [CrossRef] [Green Version]

- Cont, R.; Kukanov, A.; Stoikov, S. The Price Impact of Order Book Events. J. Financ. Econ. 2014, 21, 47–88. [Google Scholar] [CrossRef]

- Fama, E.F.; French, K.R. Multifactor Explanations of Asset Pricing Anomalies. J. Financ. 1996, 51, 55–84. [Google Scholar] [CrossRef]

- Fama, E.F.; French, K.R. A five-factor asset pricing model. J. Financ. Econ. 2015, 116, 1–22. [Google Scholar] [CrossRef] [Green Version]

- Jones, C.M.; Lamont, O.A. Short-sale constraints and stock returns. J. Financ. Econ. 2002, 66, 207–239. [Google Scholar] [CrossRef] [Green Version]

- Nagel, S. Short sales, institutional investors and the cross-section of stock returns. J. Financ. Econ. 2005, 78, 277–309. [Google Scholar] [CrossRef]

- Beber, A.; Pagano, M. Short-Selling Bans Around the World: Evidence from the 2007–09 Crisis. J. Financ. 2013, 68, 343–381. [Google Scholar] [CrossRef]

- Basu, S. The relationship between earnings’ yield, market value and return for NYSE common stocks: Further evidence. J. Financ. Econ. 1983, 12, 129–156. [Google Scholar] [CrossRef]

- Novy-Marx, R. The other side of value: The gross profitability premium. J. Financ. Econ. 2013, 108, 1–28. [Google Scholar] [CrossRef] [Green Version]

- Amihud, Y. Illiquidity and stock returns: cross-section and time-series effects. J. Financ. Mark. 2002, 5, 31–56. [Google Scholar] [CrossRef] [Green Version]

- Bali, T.G.; Cakici, N.; Whitelaw, R.F. Maxing out: Stocks as lotteries and the cross-section of expected returns. J. Financ. Econ. 2011, 99, 427–446. [Google Scholar] [CrossRef] [Green Version]

- Ang, A.; Hodrick, R.J.; Xing, Y.; Zhang, X. The Cross-Section of Volatility and Expected Returns. J. Financ. 2006, 61, 259–299. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Mean | STD | Min | Max | Mean | STD | Min | Max | |

|---|---|---|---|---|---|---|---|---|

| Panel A: Momentum | ||||||||

| PRET(10,0)/1/3 | 1.90 | 0.44 | 1.49 | 2.72 | 6.72 | 14.14 | 0.04 | 210.83 |

| PRET(10,0)/1/6 | 1.90 | 0.43 | 1.49 | 2.72 | 6.46 | 12.94 | 0.04 | 197.91 |

| PRET(10,5)/1/3 | 2.01 | 0.48 | 1.49 | 2.72 | 7.07 | 14.70 | 0.04 | 310.83 |

| PRET(10,5)/1/6 | 2.00 | 0.47 | 1.49 | 2.72 | 6.89 | 14.07 | 0.04 | 307.07 |

| Panel B: Value | ||||||||

| BM/1/3 | 2.16 | 0.42 | 1.49 | 2.72 | 5.35 | 15.61 | 0.07 | 174.52 |

| BM/1/6 | 2.16 | 0.42 | 1.49 | 2.72 | 5.31 | 15.62 | 0.07 | 174.52 |

| EP/1/3 | 2.14 | 0.45 | 1.49 | 2.72 | 6.84 | 18.41 | 0.08 | 197.91 |

| EP/1/6 | 2.14 | 0.45 | 1.49 | 2.72 | 6.82 | 18.44 | 0.08 | 197.91 |

| Panel C: Profitability | ||||||||

| GPA/1/3 | 2.07 | 0.49 | 1.49 | 2.72 | 6.56 | 11.37 | 0.00 | 84.87 |

| GPA/1/6 | 2.07 | 0.49 | 1.49 | 2.72 | 6.54 | 11.40 | 0.00 | 84.87 |

| Panel D: Friction | ||||||||

| ILLIQ 1/1/3 | 2.50 | 0.22 | 1.49 | 2.72 | 2.09 | 3.80 | 0.03 | 70.97 |

| ILLIQ 1/1/6 | 2.50 | 0.23 | 1.49 | 2.72 | 2.08 | 3.71 | 0.03 | 70.97 |

| Panel E: Lottery-Like | ||||||||

| MAX 1/1/3 | 2.27 | 0.45 | 1.49 | 2.72 | 7.68 | 19.00 | 0.00 | 228.11 |

| MAX 1/1/6 | 2.27 | 0.45 | 1.49 | 2.72 | 7.52 | 18.50 | 0.00 | 228.11 |

| SKEW 1/1/3 | 2.11 | 0.48 | 1.49 | 2.72 | 6.76 | 14.54 | 0.06 | 219.12 |

| SKEW 1/1/6 | 2.11 | 0.47 | 1.49 | 2.72 | 6.96 | 15.56 | 0.07 | 219.12 |

| Panel F: Defensive | ||||||||

| IVOL 12/1/3 | 2.22 | 0.47 | 1.49 | 2.72 | 12.18 | 27.89 | 0.11 | 219.12 |

| IVOL 12/1/6 | 2.22 | 0.47 | 1.49 | 2.72 | 12.18 | 27.96 | 0.11 | 219.12 |

| 12/1/3 | 2.41 | 0.39 | 1.49 | 2.72 | 4.65 | 11.27 | 0.04 | 228.11 |

| 12/1/6 | 2.41 | 0.39 | 1.49 | 2.72 | 4.62 | 11.99 | 0.04 | 228.11 |

| lue-Weighted | Equal-Weighted | |||

|---|---|---|---|---|

| Return w/o Impact | Return w/o Impact | |||

| Panel A: Momentum | ||||

| PRET(10,0)/1/3 | 1.56 | 3213 | 1.94 | 1346 |

| PRET(10,0)/1/6 | 1.40 | 3371 | 2.96 | 2279 |

| PRET(10,5)/1/3 | 1.54 | 1463 | 1.87 | 757 |

| PRET(10,5)/1/6 | 0.98 | 1466 | 2.69 | 1040 |

| Panel B: Value | ||||

| BM/1/3 | 1.50 | 1863 | 2.26 | 4154 |

| BM/1/6 | 1.57 | 2273 | 2.86 | 5538 |

| EP/1/3 | 1.21 | 1575 | 1.21 | 1522 |

| EP/1/6 | 1.26 | 2033 | 1.66 | 2186 |

| Panel C: Profitability | ||||

| GPA/1/3 | 0.55 | 14,479 | 1.31 | 5228 |

| GPA/1/6 | 0.61 | 17,589 | 1.41 | 6731 |

| Panel D: Friction | ||||

| ILLIQ 1/1/3 | 0.84 | 807 | 1.94 | 1574 |

| ILLIQ 1/1/6 | 0.91 | 1416 | 1.95 | 2727 |

| Panel E: Lottery-Like | ||||

| MAX 1/1/3 | 1.06 | 374 | 1.02 | 150 |

| MAX 1/1/6 | 0.29 | 262 | 1.10 | 1058 |

| SKEW 1/1/3 | 0.77 | 266 | 1.17 | 330 |

| SKEW 1/1/6 | 0.91 | 835 | 1.20 | 864 |

| Panel F: Defensive | ||||

| IVOL 12/1/3 | 0.82 | 4771 | 1.48 | 3055 |

| IVOL 12/1/6 | 0.84 | 11,654 | 1.59 | 4017 |

| 12/1/3 | 0.68 | 389 | 0.93 | 182 |

| 12/1/6 | 0.37 | 335 | 0.90 | 1077 |

| Value-Weighted | Equal-Weighted | |||

|---|---|---|---|---|

| Max Profit | Max Profit | |||

| Panel A: Momentum | ||||

| PRET(10,0)/1/3 | 1250 | 5.41 | 500 | 2.35 |

| PRET(10,0)/1/6 | 1300 | 5.54 | 850 | 3.87 |

| PRET(10,5)/1/3 | 550 | 2.46 | 300 | 1.31 |

| PRET(10,5)/1/6 | 600 | 2.10 | 400 | 1.78 |

| Panel B: Value | ||||

| BM/1/3 | 700 | 3.09 | 1550 | 7.47 |

| BM/1/6 | 850 | 3.81 | 2050 | 9.97 |

| EP/1/3 | 600 | 2.47 | 600 | 2.45 |

| EP/1/6 | 800 | 3.23 | 850 | 3.61 |

| Panel C: Profitability | ||||

| GPA/1/3 | 6300 | 14.67 | 2000 | 8.88 |

| GPA/1/6 | 7550 | 19.05 | 2550 | 11.67 |

| Panel D: Friction | ||||

| ILLIQ(1)/1/3 | 350 | 1.08 | 600 | 2.78 |

| ILLIQ(1)/1/6 | 600 | 1.98 | 1000 | 4.82 |

| Panel E: Lottery-Like | ||||

| MAX(1)/1/3 | 150 | 0.53 | 50 | 0.24 |

| MAX(1)/1/6 | 100 | 0.16 | 400 | 1.62 |

| SKEW(1)/1/3 | 100 | 0.33 | 150 | 0.52 |

| SKEW(1)/1/6 | 350 | 1.16 | 350 | 1.36 |

| Panel F: Defensive | ||||

| IVOL(12)/1/3 | 2000 | 6.20 | 1150 | 5.16 |

| IVOL(12)/1/6 | 4850 | 15.46 | 1500 | 6.90 |

| (12)/1/3 | 150 | 0.45 | 50 | 0.26 |

| (12)/1/6 | 150 | 0.26 | 450 | 1.50 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kim, J.; Park, Y.J. Is Factor Investing Sustainable after Price Impact Costs? The Capacity of Factor Investing in Korea. Sustainability 2019, 11, 4797. https://doi.org/10.3390/su11174797

Kim J, Park YJ. Is Factor Investing Sustainable after Price Impact Costs? The Capacity of Factor Investing in Korea. Sustainability. 2019; 11(17):4797. https://doi.org/10.3390/su11174797

Chicago/Turabian StyleKim, Jungmu, and Yuen Jung Park. 2019. "Is Factor Investing Sustainable after Price Impact Costs? The Capacity of Factor Investing in Korea" Sustainability 11, no. 17: 4797. https://doi.org/10.3390/su11174797