The Impact of Slumping Oil Price on the Situation of Tanker Shipping along the Maritime Silk Road

Abstract

:1. Introduction

2. Literature Review

3. Data and Methods

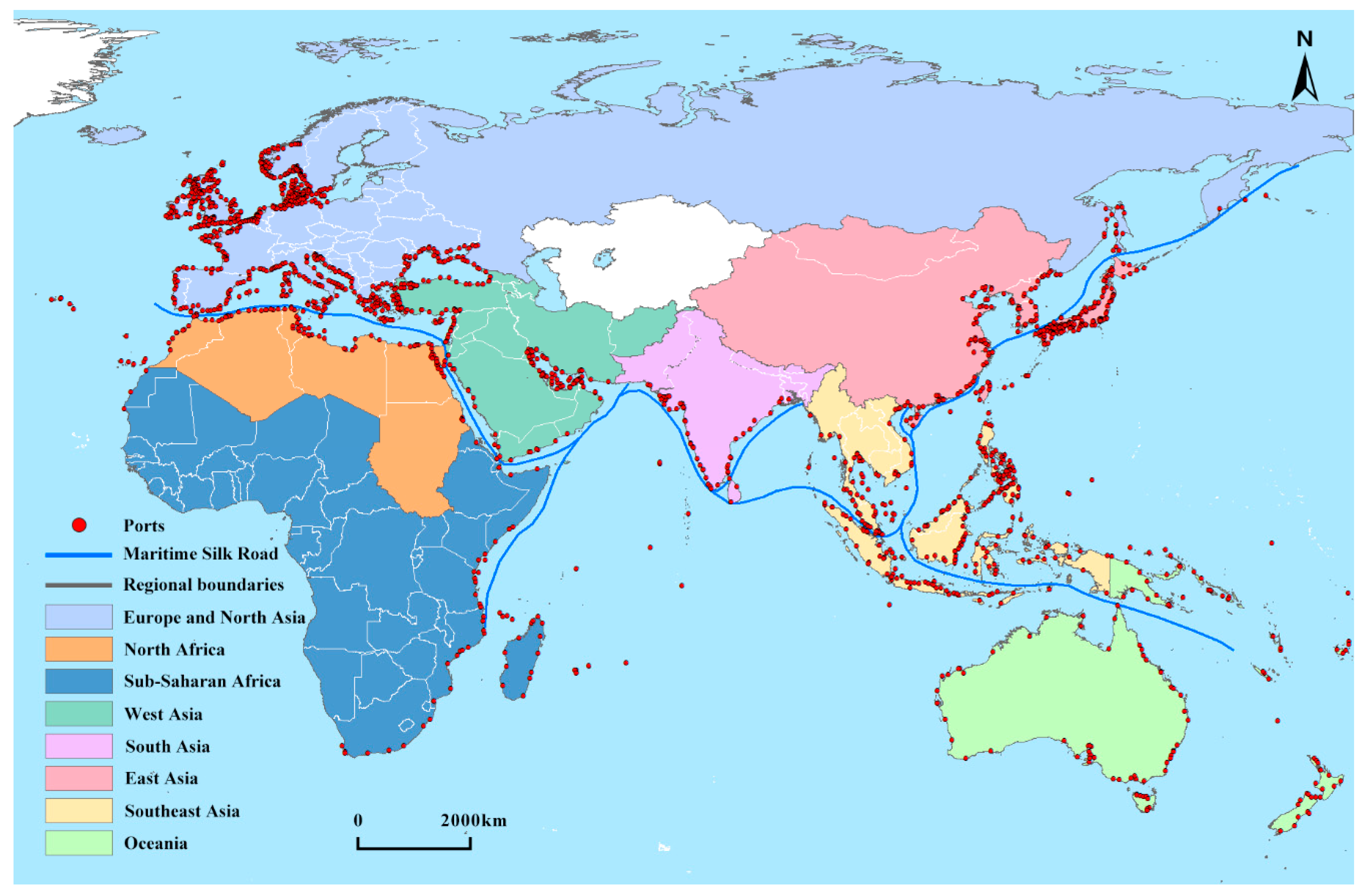

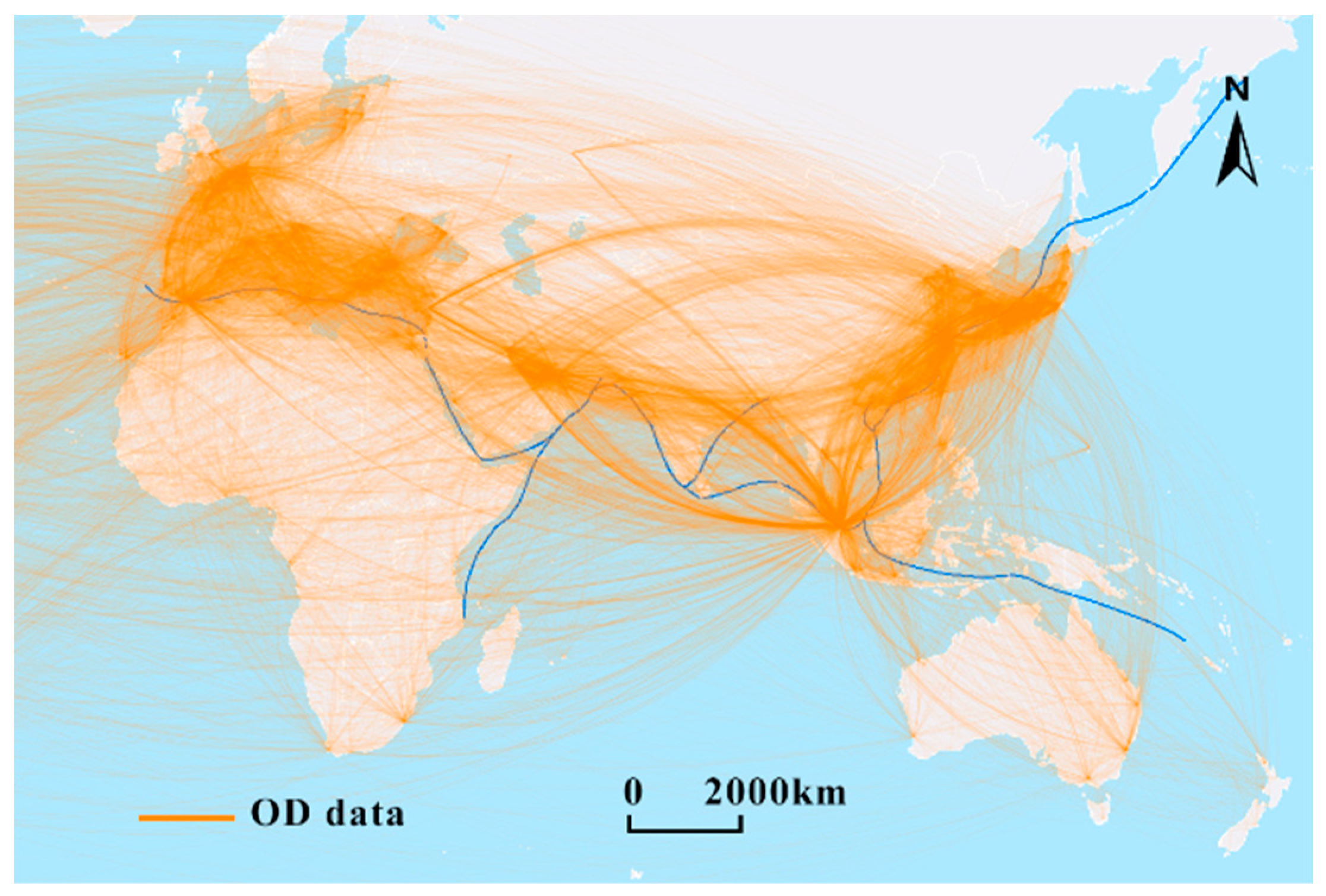

3.1. Study Areas and Data

3.2. Methods

3.2.1. Spearman Rank Correlation Analysis

3.2.2. ARDL Lag Model

4. Empirical Results

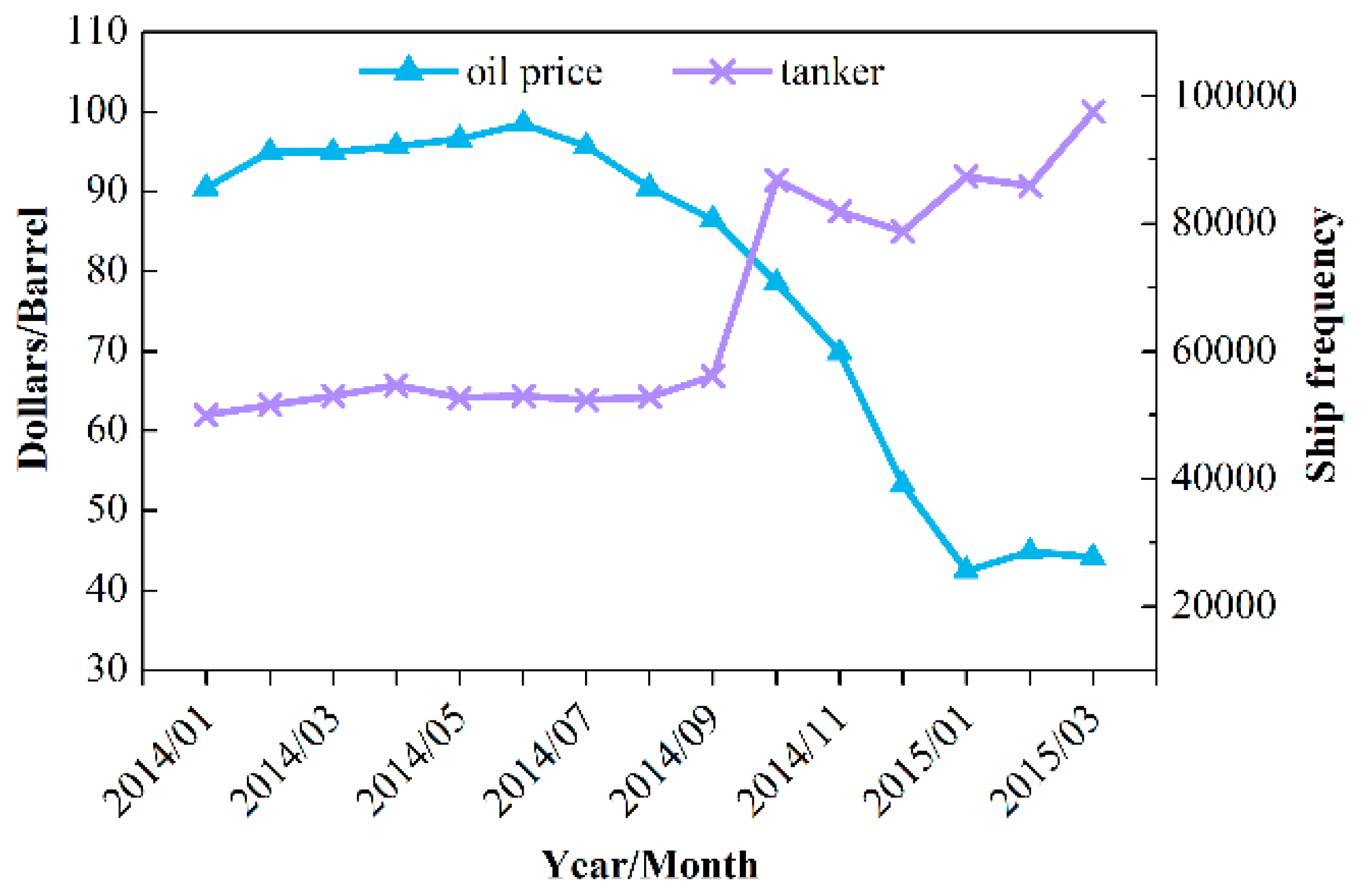

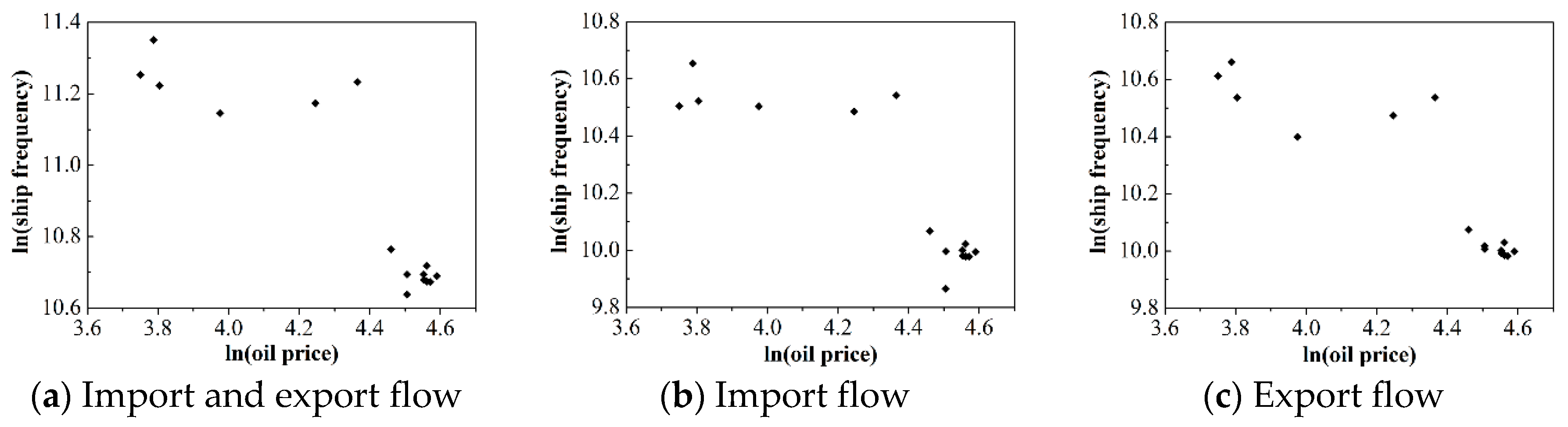

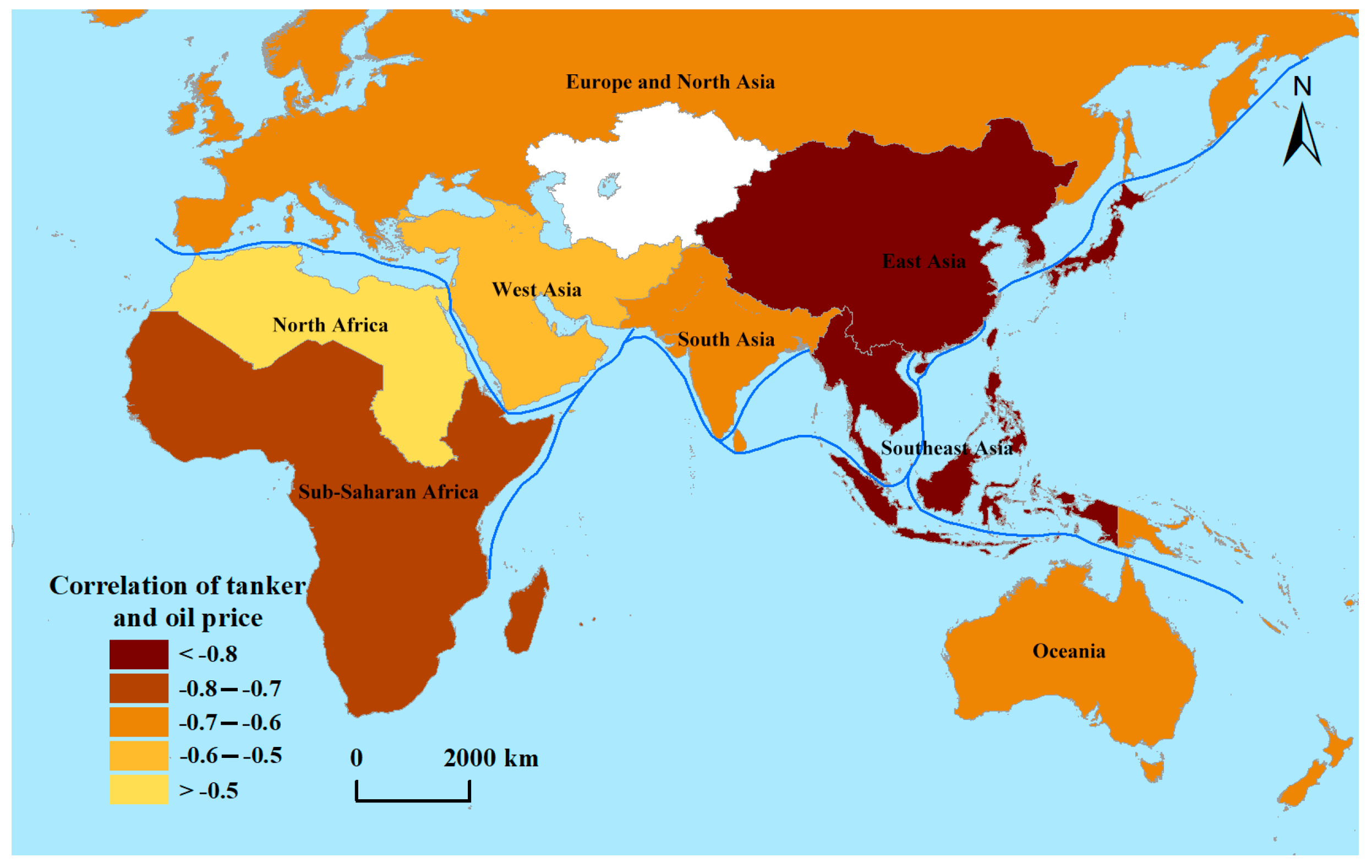

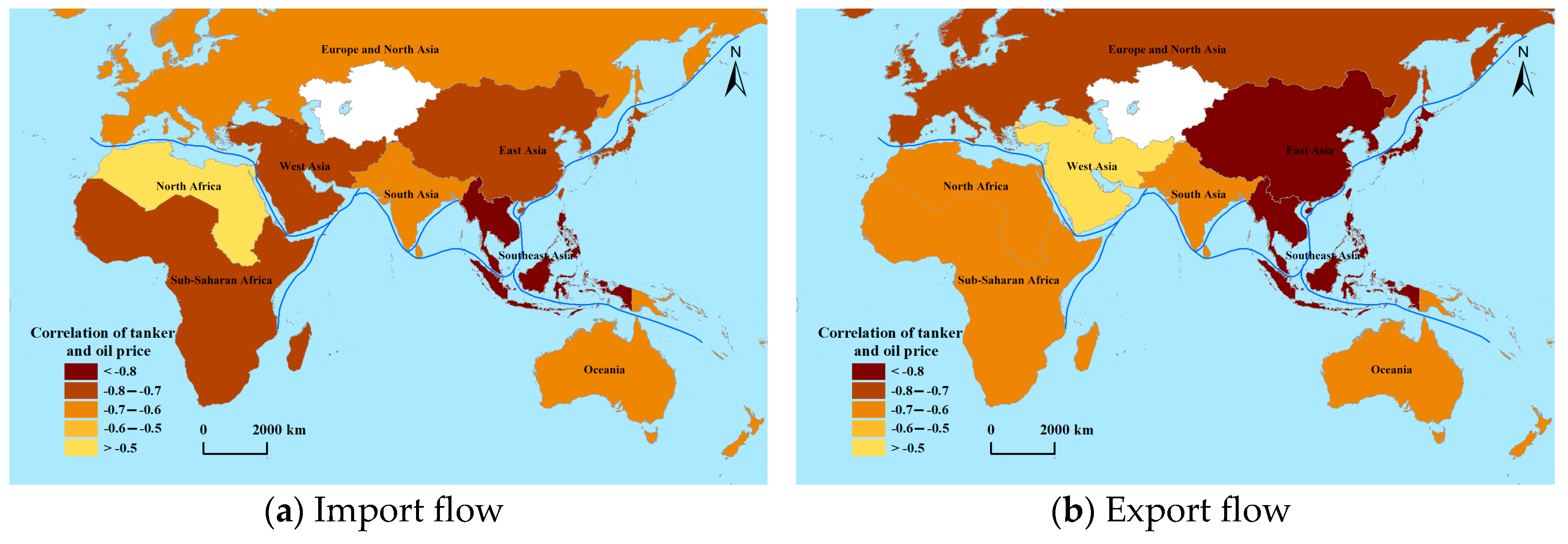

4.1. Nonlinear Correlation

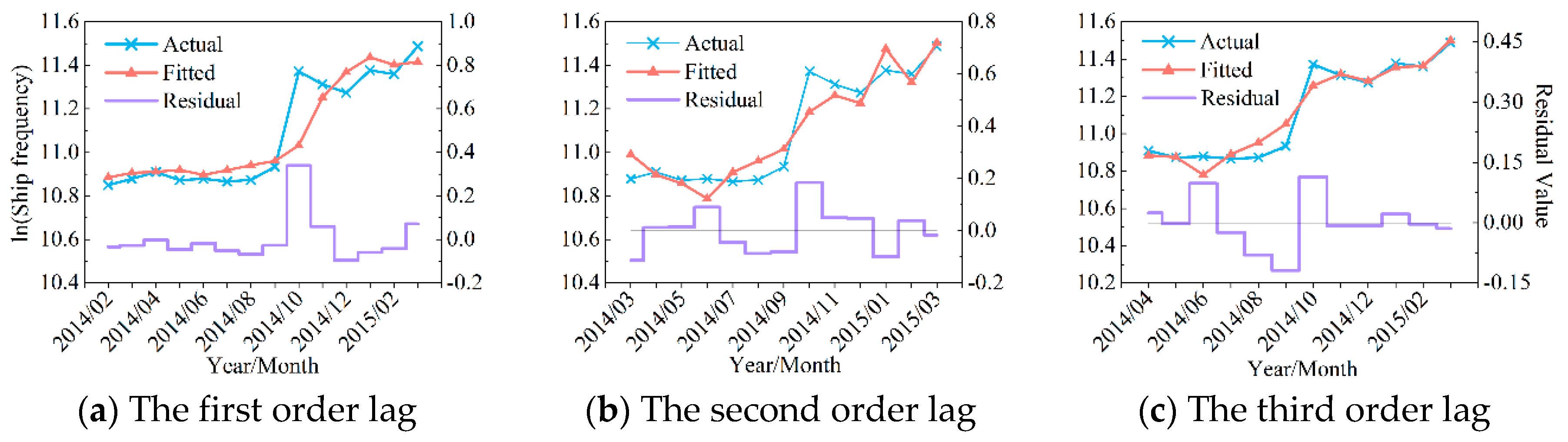

4.2. Lag Analysis

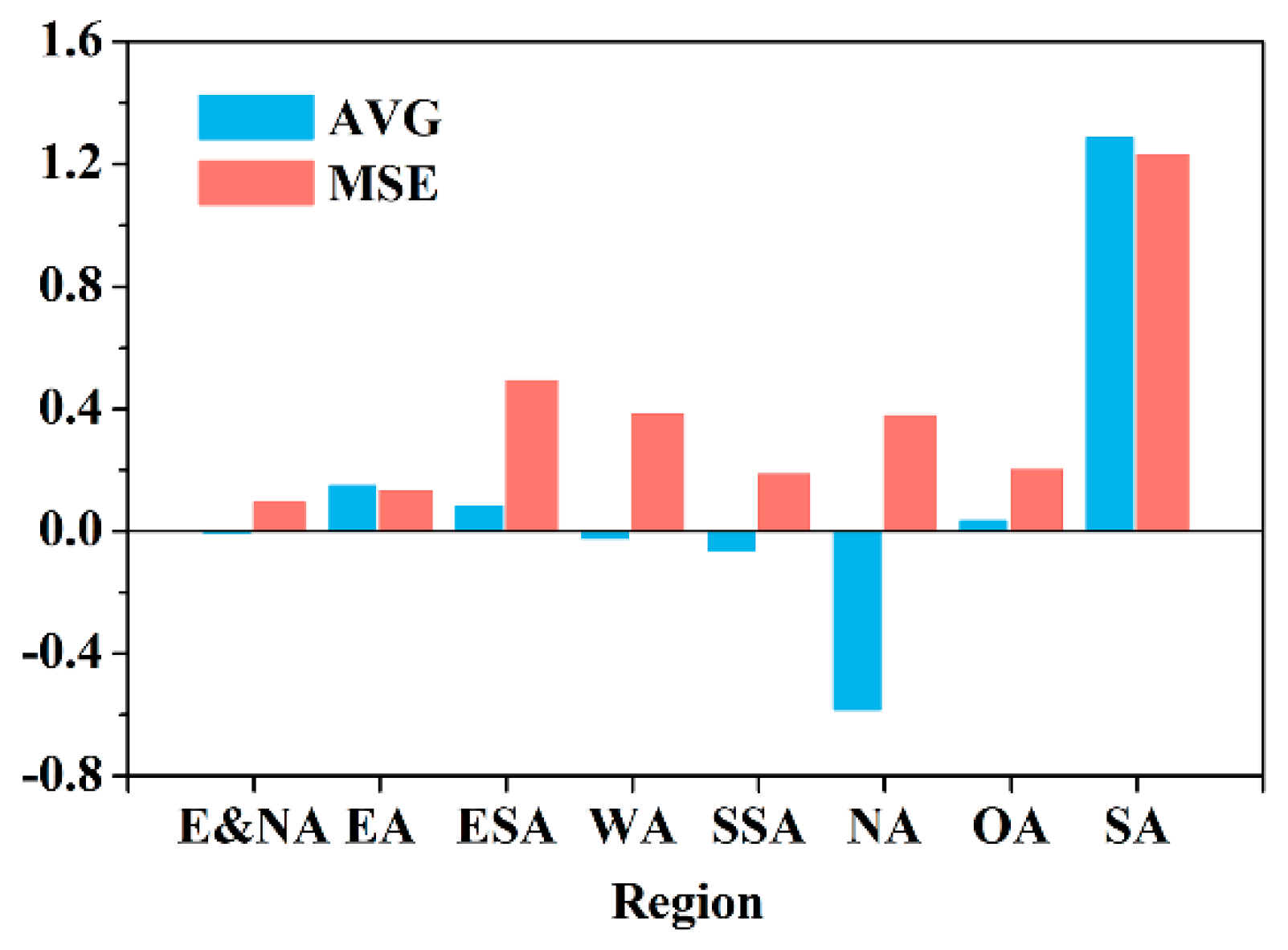

4.3. Regional Comparison and Analysis Along the MSR

4.3.1. Lag Affects Regional Differences

4.3.2. Comparison of Cargo Flow before and after Oil Price Slumped

5. Discussion

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Wang, L.H.; Zhu, Y.; Ducruet, C.; Bunel, M.; Lau, Y.Y. From hierarchy to networking: The evolution of the “twenty-first-century Maritime Silk Road” container shipping system. Trans. Rev. 2018, 6, 1–20. [Google Scholar] [CrossRef]

- Chen, Y.F.; Chao, Z.D. Transmission mechanism and dynamic effect of International oil price shocks on China’s terms of trade. J. Int. Trade 2013, 5, 3–18. [Google Scholar]

- Wen, P.X. Analysis of the impact of global oil price decline on the tanker market. China Water Trans. 2015, 15, 108–110. [Google Scholar]

- Oladosu, G.A.; Leiby, P.N.; Bowman, D.C.; Uría-Martínez, R.; Johnson, M.M. Impacts of oil price shocks on the United States economy: A meta-analysis of the oil price elasticity of GDP for net oil-importing economies ☆. Energy Policy 2018, 115, 523–544. [Google Scholar] [CrossRef]

- Chai, J.; Cao, P.J.; Zhou, X.Y.; Lai, K.K.; Chen, X.F.; Su, S. The Conductive and Predictive Effect of Oil Price Fluctuations on China’s Industry Development Based on Mixed-Frequency Data. Energies 2018, 11, 1372. [Google Scholar] [CrossRef]

- Boldanov, R.; Degiannakis, S.; Filis, G. Time-varying correlation between oil and stock market volatilities: Evidence from oil-importing and oil-exporting countries. Int. Rev. Financ. Anal. 2016, 48, 209–220. [Google Scholar] [CrossRef] [Green Version]

- Wang, M.G.; Tian, L.X.; Du, R.J. Research on the interaction patterns among the global crude oil import dependency countries: A complex network approach. Appl. Energy 2016, 180, 779–791. [Google Scholar] [CrossRef]

- Ronen, D. The effect of oil price on containership speed and fleet size. J. Oper. Res. Soc. 2011, 62, 211–216. [Google Scholar] [CrossRef]

- De, A.; Choudhary, A.; Turkay, M.; Tiwari, M.K. Bunkering Policies for a Fuel Bunker Management Problem for Liner Shipping Networks. Eur. J. Oper. Res. 2019, 1–13. [Google Scholar] [CrossRef]

- De, A.; Wang, J.; Tiwari, M.K. Hybridizing Basic Variable Neighborhood Search With Particle Swarm Optimization for Solving Sustainable Ship Routing and Bunker Management Problem. IEEE Trans. Intell. Transp. Syst. 2019, 1–12. [Google Scholar] [CrossRef]

- Pal, D.; Mitra, S.K. Asymmetric oil product pricing in India: Evidence from a multiple threshold nonlinear ARDL model. Econ. Model. 2016, 59, 314–328. [Google Scholar] [CrossRef]

- Kolodzeij, M.; Kaufmann, R.K. Oil demand shocks reconsidered: A cointegrated vector autoregression. Energy Econ. 2014, 41, 33–40. [Google Scholar] [CrossRef]

- He, Y.; Wang, S.; Lai, K.K. Global economic activity and crude oil prices: A cointegration analysis. Energy Econ. 2010, 32, 868–876. [Google Scholar] [CrossRef]

- Nusair, S.A. The effects of oil price shocks on the economies of the Gulf Co-operation Council countries: Nonlinear analysis. Energy Policy 2016, 91, 256–267. [Google Scholar] [CrossRef]

- Zhu, H.; Su, X.; Guo, Y.; Ren, Y. The Asymmetric Effects of Oil Price Shocks on the Chinese Stock Market: Evidence from a Quantile Impulse Response Perspective. Sustainability 2016, 8, 766. [Google Scholar] [CrossRef]

- Bai, S.; Koong, K.S. Oil prices, stock returns, and exchange rates: Empirical evidence from China and the United States. N. Am. J. Econ. Financ. 2018, 44, 12–33. [Google Scholar] [CrossRef]

- Kim Karlsson, H.; Li, Y.; Shukur, G. The Causal Nexus between Oil Prices, Interest Rates, and Unemployment in Norway Using Wavelet Methods. Sustainability 2018, 10, 2792. [Google Scholar] [CrossRef]

- Zhang, C.; Liu, F.; Yu, D. Dynamic jumps in global oil price and its impacts on China’s bulk commodities. Energy Econ. 2018, 70, 297–306. [Google Scholar] [CrossRef]

- Ahmadi, M.; Bashiri, B.N.; Manera, M. How is volatility in commodity markets linked to oil price shocks? Energy Econ. 2016, 59, 11–23. [Google Scholar] [CrossRef]

- Nwoko, I.C.; Aye, G.C.; Asogwa, B.C. Oil price and food price volatility dynamics: The case of Nigeria. Cogent Food Agric. 2016, 2, 1142413. [Google Scholar] [CrossRef]

- Sun, Y.Y.; Zhang, X.; Hong, Y.M.; Wang, S.Y. Asymmetric pass-through of oil prices to gasoline prices with interval time series modelling. Energy Econ. 2019, 78, 165–173. [Google Scholar] [CrossRef]

- Cansado-Bravo, P.; Rodríguez-Monroy, C. Persistence of Oil Prices in Gas Import Prices and the Resilience of the Oil-Indexation Mechanism. The Case of Spanish Gas Import Prices. Energies 2018, 11, 3486. [Google Scholar] [CrossRef]

- Shi, W.M.; Yang, Z.Z.; Li, K.X. The impact of crude oil price on the tanker market. Marit. Policy Manag. 2013, 40, 309–322. [Google Scholar] [CrossRef]

- Yi, Z. Investigating dependencies among oil price and tanker market variables by copula-based multivariate models. Energy 2018, 161, 435–446. [Google Scholar]

- Ruan, Q.S.; Wang, Y.; Lu, X.S.; Qin, J. Cross-correlations between Baltic Dry Index and crude oil prices. Phys. A Stat. Mech. Its Appl. 2016, 453, 278–289. [Google Scholar] [CrossRef]

- Chen, H.; Cullinane, K.; Liu, N. Developing a model for measuring the resilience of a port-hinterland container transportation network. Transp. Res. Part E Logist. Transp. Rev. 2017, 97, 282–301. [Google Scholar] [CrossRef]

- De, A.; Pratap, S.; Kumar, A.; Tiwari, M.K. A hybrid dynamic berth allocation planning problem with fuel costs considerations for container terminal port using chemical reaction optimization approach. Ann. Oper. Res. 2018, 1–29. [Google Scholar] [CrossRef]

- Duru, O.; Clott, C.; Mileski, J.P. U.S. tanker transport: Current structure and economic analysis. Res. Transp. Bus. Manag. 2017, 25, 39–50. [Google Scholar] [CrossRef]

- Li, T.Y.; Xue, L.Y.; Chen, Y.; Chen, F.; Miao, Y.Q.; Shao, X.Z.; Zhang, C.Y. Insights from multifractality analysis of tanker freight market volatility with common external factor of crude oil price. Phys. A Stat. Mech. Its Appl. 2018, 505, 374–384. [Google Scholar] [CrossRef]

- Grote, M.; Mazurek, N.; Gräbsch, C.; Zeilinger, J.; Floch, S.L.; Wahrendorf, D.S.; Höfer, T. Dry bulk cargo shipping—An overlooked threat to the marine environment? Mar. Pollut. Bull. 2016, 110, 511–519. [Google Scholar] [CrossRef]

- Guo, Y.F.; Wen, X.Q.; Wu, Y.R.; Guo, X.M. How is China’s coke price related with the world oil price? The role of extreme movements. Econ. Model. 2016, 58, 22–33. [Google Scholar] [CrossRef]

- Yu, H.; Fang, Z.; Peng, G.; Feng, M. Revealing the Linkage Network Dynamic Structures of Chinese Maritime Ports through Automatic Information System Data. Sustainability 2017, 9, 1913. [Google Scholar] [CrossRef]

- Guan, Q.; An, H.Z.; Gao, X.Y.; Huang, S.P.; Li, H.J. Estimating potential trade links in the international crude oil trade: A link prediction approach. Energy 2016, 102, 406–415. [Google Scholar] [CrossRef]

- Ducruet, C. Multilayer dynamics of complex spatial networks: The case of global maritime flows (1977–2008). J. Transp. Geogr. 2017, 60, 47–58. [Google Scholar] [CrossRef]

- Mou, N.; Liu, C.; Zhang, L.; Fu, X.; Xie, Y.; Li, Y.; Peng, P. Spatial Pattern and Regional Relevance Analysis of the Maritime Silk Road Shipping Network. Sustainability 2018, 10, 977. [Google Scholar] [CrossRef]

- Peng, P.; Yang, Y.; Cheng, S.; Lu, F.; Yuan, Z.M. Hub-and-spoke structure: Characterizing the global crude oil transport network with mass vessel trajectories. Energy 2019, 168, 966–974. [Google Scholar] [CrossRef]

- Hao, X.Q.; An, H.Z.; Qi, H.; Gao, X.Y. Evolution of the exergy flow network embodied in the global fossil energy trade: Based on complex network. Appl. Energy 2016, 162, 1515–1522. [Google Scholar] [CrossRef]

- Li, M.X. The impact of international oil price fluctuations on China-Australian iron ore shipping. Shipp. Manag. 2016, 38, 16–18. [Google Scholar]

- Chen, J.F.; Chen, L. Analysis of the impact of international oil price fluctuation on China’s shipping industry. China Water Trans. 2011, 11, 41–42. [Google Scholar]

- Chen, F.; Miao, Y.Q.; Tian, K.; Ding, X.X.; Li, T.Y. Multifractal cross-correlations between crude oil and tanker freight rate. Phys. A Stat. Mech. Its Appl. 2017, 474, 344–354. [Google Scholar] [CrossRef]

- Altinay, G. Short-run and long-run elasticities of import demand for crude oil in Turkey. Energy Policy 2007, 35, 5829–5835. [Google Scholar] [CrossRef]

- Yu, H.C.; Fang, Z.X.; Lu, F.; Murray, A.T.; Zhang, H.C.; Peng, P.; Mei, Q.; Chen, J.H. Impact of oil price fluctuations on tanker maritime network structure and traffic flow changes. Appl. Energy 2019, 237, 390–403. [Google Scholar] [CrossRef]

- Gong, P.P.; Song, Z.Y.; Liu, W.D. Commodity structure of trade between China and countries in the Belt and Road Initiative area. Prog. Geogr. 2015, 34, 571–580. [Google Scholar]

- Gautheir, T.D. Detecting Trends Using Spearman’s Rank Correlation Coefficient. Environ. Forensics 2001, 2, 359–362. [Google Scholar] [CrossRef]

- Sek, S.K. Impact of oil price changes on domestic price inflation at disaggregated levels: Evidence from linear and nonlinear ARDL modeling. Energy 2017, 130, 204–217. [Google Scholar] [CrossRef]

- Odhiambo, N.M. Energy consumption and economic growth nexus in Tanzania: An ARDL bounds testing approach. Energy Policy 2009, 37, 617–622. [Google Scholar] [CrossRef]

- Ozturk, I.; Acaravci, A. The causal relationship between energy consumption and GDP in Albania, Bulgaria, Hungary and Romania: Evidence from ARDL bound testing approach. Appl. Energy 2010, 87, 1938–1943. [Google Scholar] [CrossRef]

- Pesaran, M.H.; Shin, Y.; Smith, R.P. Pooled Mean Group Estimation of Dynamic Heterogeneous Panels. J. Am. Stat. Assoc. 1999, 94, 621–634. [Google Scholar] [CrossRef]

- De, A.; Wang, J.; Tiwari, M.K. Fuel Bunker Management Strategies within Sustainable Container Shipping Operation Considering Disruption and Recovery Policies. IEEE Trans. Eng. Manag. 2019, 1–23. [Google Scholar] [CrossRef]

- Yang, R.; Mou, N.X.; Peng, P.; Liu, X.L.; Zhang, H.C.; Lu, F. Evaluation on competitiveness of important ports along 21st-Century Maritime Silk Road. J. Geo-Inf. Sci. 2018, 20, 623–631. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Type | Correlation Coefficient | Significance Test |

|---|---|---|

| Import and export flow | −0.807143 ** | 0.000275 |

| Import flow | −0.782143 ** | 0.00057 |

| Export flow | −0.889286 ** | 0.000009 |

| Lag Period | Adjusted-R2 | F Statistical Quantity | AIC | SC |

|---|---|---|---|---|

| 1 | 0.762521 | 14.91392 | −1.122056 | −0.939469 |

| 2 | 0.822817 | 12.14529 | −1.342967 | −1.088221 |

| 3 | 0.824597 | 8.387541 | −1.412639 | −1.089367 |

| 3 * | 0.870976 | 15.85104 | −1.647591 | −1.405138 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mou, N.; Xie, Y.; Yang, T.; Zhang, H.; Kim, Y.R. The Impact of Slumping Oil Price on the Situation of Tanker Shipping along the Maritime Silk Road. Sustainability 2019, 11, 4796. https://doi.org/10.3390/su11174796

Mou N, Xie Y, Yang T, Zhang H, Kim YR. The Impact of Slumping Oil Price on the Situation of Tanker Shipping along the Maritime Silk Road. Sustainability. 2019; 11(17):4796. https://doi.org/10.3390/su11174796

Chicago/Turabian StyleMou, Naixia, Yanxin Xie, Tengfei Yang, Hengcai Zhang, and Yoo Ri Kim. 2019. "The Impact of Slumping Oil Price on the Situation of Tanker Shipping along the Maritime Silk Road" Sustainability 11, no. 17: 4796. https://doi.org/10.3390/su11174796