Stochastic Assessments of Urban Employees’ Pension Plan of China

Abstract

:1. Introduction

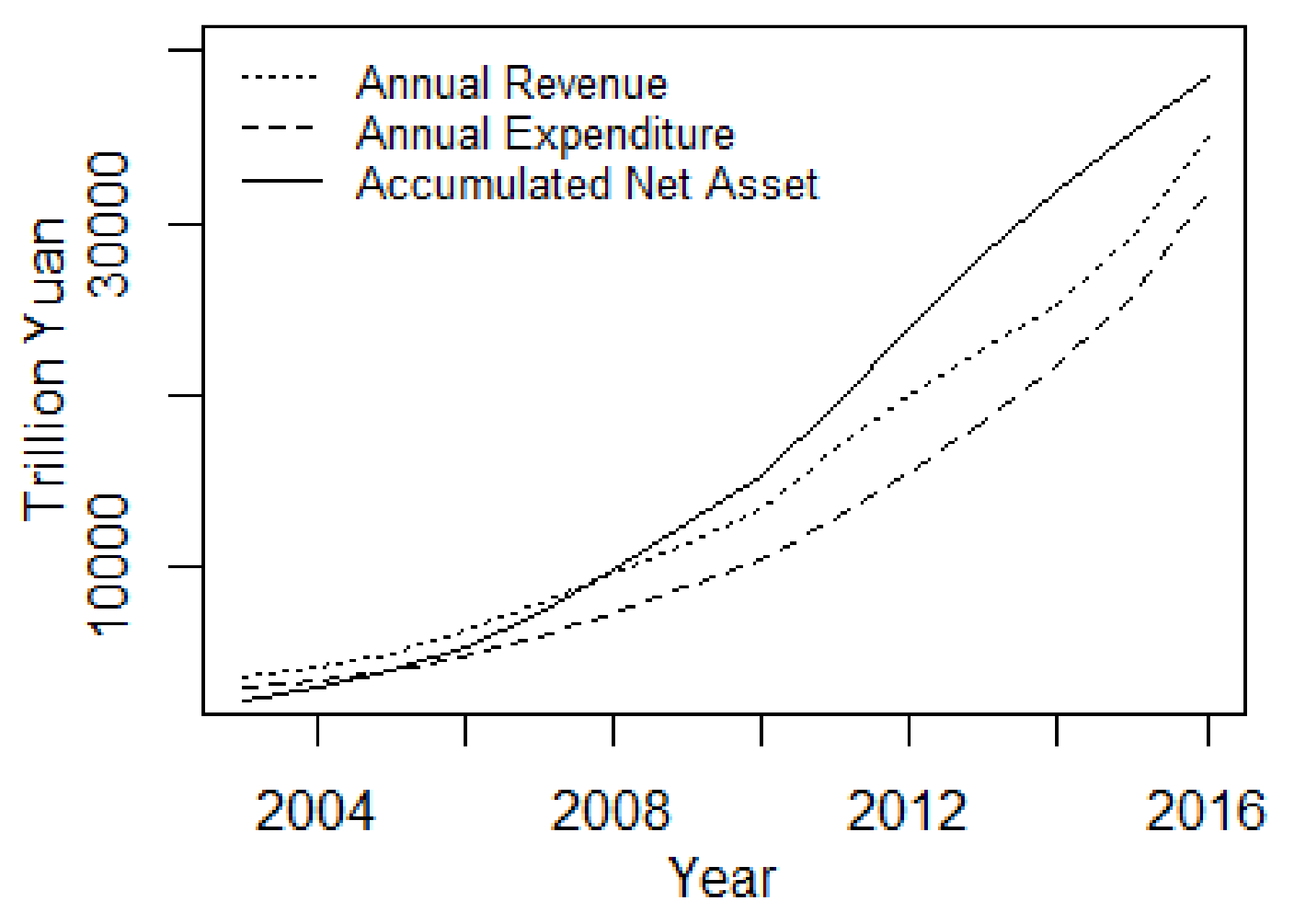

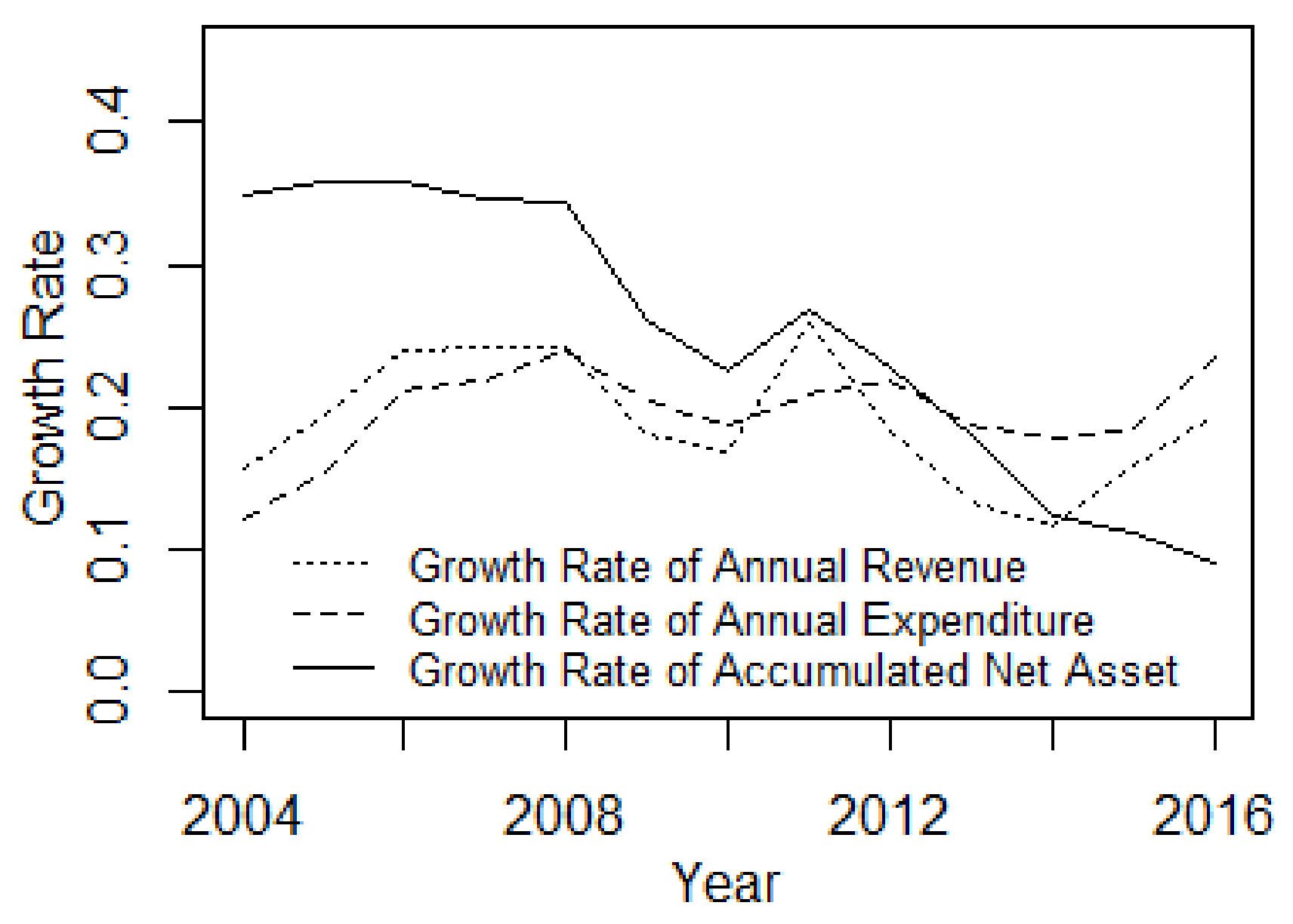

2. The Solvency Situation of Urban Employees’ Public Pension Fund in China

3. Method

3.1. Modelling Demographic Variables

3.1.1. Lee–Carter Approach for Mortality Forecasting

3.1.2. Time-Series Modelling of Age-Specific Fertility

3.2. Matrix Modeling of Population Projection

3.3. Actuarial Indicators of Financial Risk

3.4. Data and Actuarial Assumptions

- (1)

- Initial population: The matrix model of population projection uses age-sex specific population data of 2013 as the initial population vector. The data can be obtained from China population and employment statistics yearbook [23].

- (2)

- Entry age: The legal age of employment in China should be more than 16. Similar to previous study [24], we suppose the entry age for insurance is 20 over the long term.

- (3)

- Normal retirement age: In the current legal provisions, male workers retire at the age of 60, female workers retire at the age of 50, and female staff managers retire at 55 [6,25]. But with the implementation of policy for gradually suspending the retirement age of employees, the retirement age will be delayed. Thus, the retirement age is set to be 60 for men and 55 for women.

- (4)

- Sex ratio at birth: According to the National Population Development Plan (2016–2030), the future objective of gender ratio is set to be 112 at year 2020 and 107 at year 2030 [26]. With the reduction of gender preference, the gender ratio of Chinese urban infants is supposed to be 107 boys to 100 girls.

- (5)

- Contributed rate: According to the State Council (2005) document No. 38, the contributed rate of social pooling fund is set to 20 percent of taxable payroll in the evaluation period [13].

- (6)

- Coverage rate: In the light of development of human resources and social security 13th Five-Year plan, the coverage rate of plan will reach 90 percent. The coverage rate of urban employee’s pension plan is set to increase year by year to 90 percent in the evaluation period.

- (7)

- Urbanization rate: According to the data released by the National Bureau of Statistics, the urbanization rate of the population has increased from 17.92 percent in 1978 to 56.10 percent in 2015. The urban development report of China indicates that the urbanization rate of China will increase to more than 75 percent by 2050. Hence, the urbanization rate is set to increase year by year to reach 75 percent.

- (8)

- Urban employment rate: According to the Statistical Yearbook of China, the ratio of urban employment in the past year has remained at around 85%. Thus, this paper assumes that the future urban employment rate will remain at this level in the prediction interval.

- (9)

- The social pooling replacement rate: According to the State Council (2005) document No. 38, the total replacement rate of an urban employee contributed payroll tax for more than 35 years is set to 59.2 percent of social average wage, and the social pooling replacement rate is set at 35 percent of social average wage [13].

- (10)

- Return rate: Referring to past study [8] and recent changes, we assume that the interest rate under the benchmark scenario is 0.03.

4. Stochastic Assessments of Relative Financial Risk Indicators

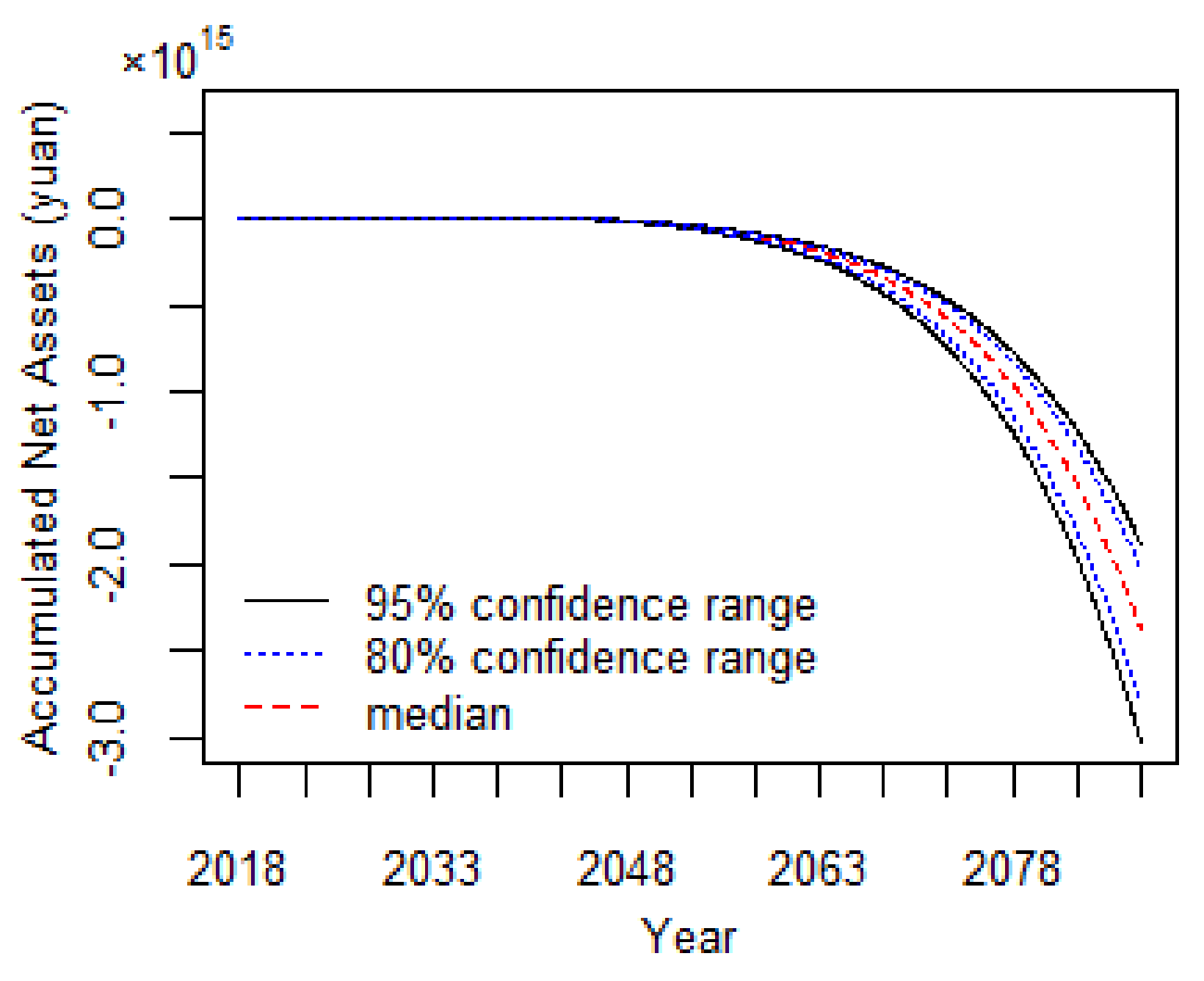

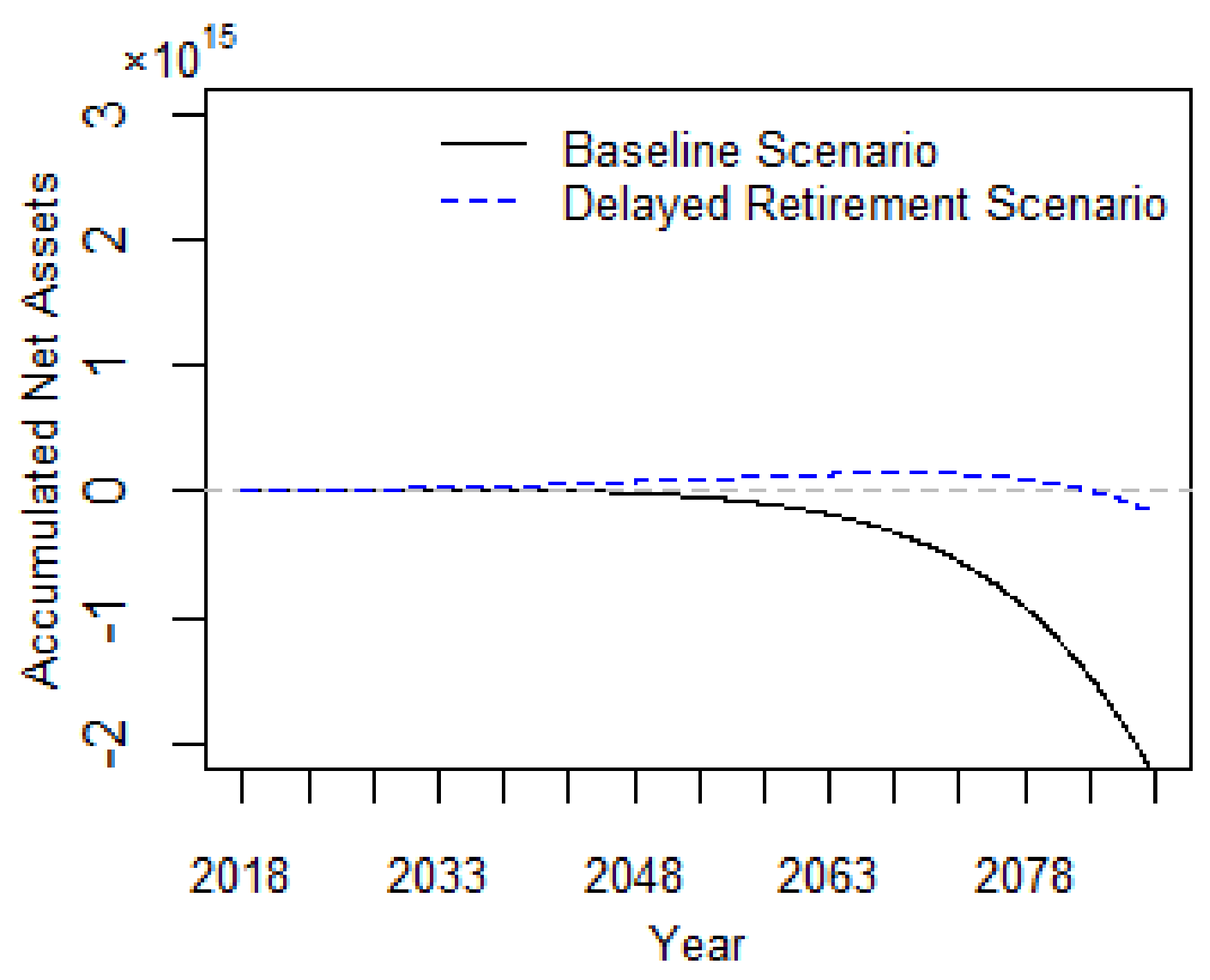

4.1. Stochastic Assessment of Accuulated Net Asset

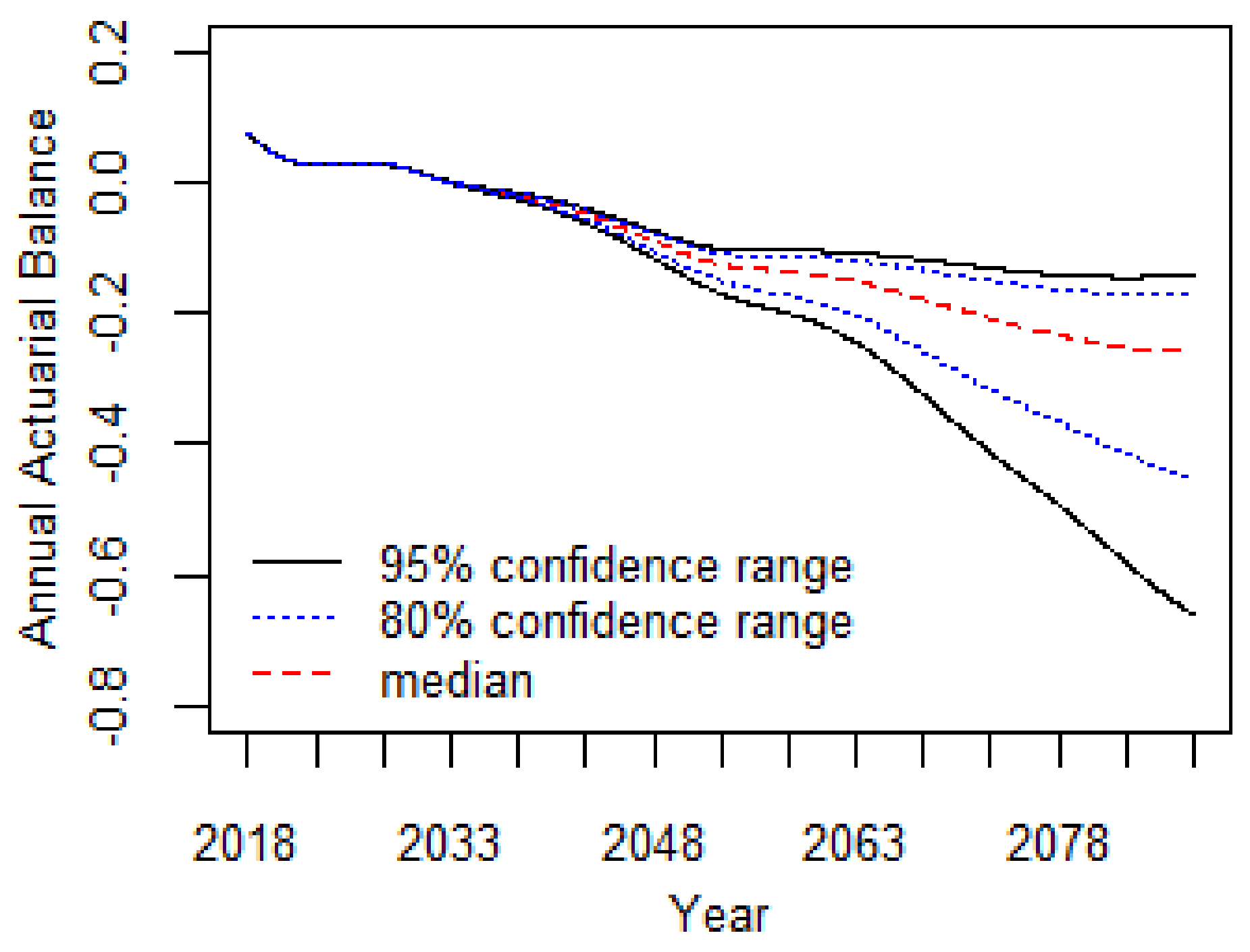

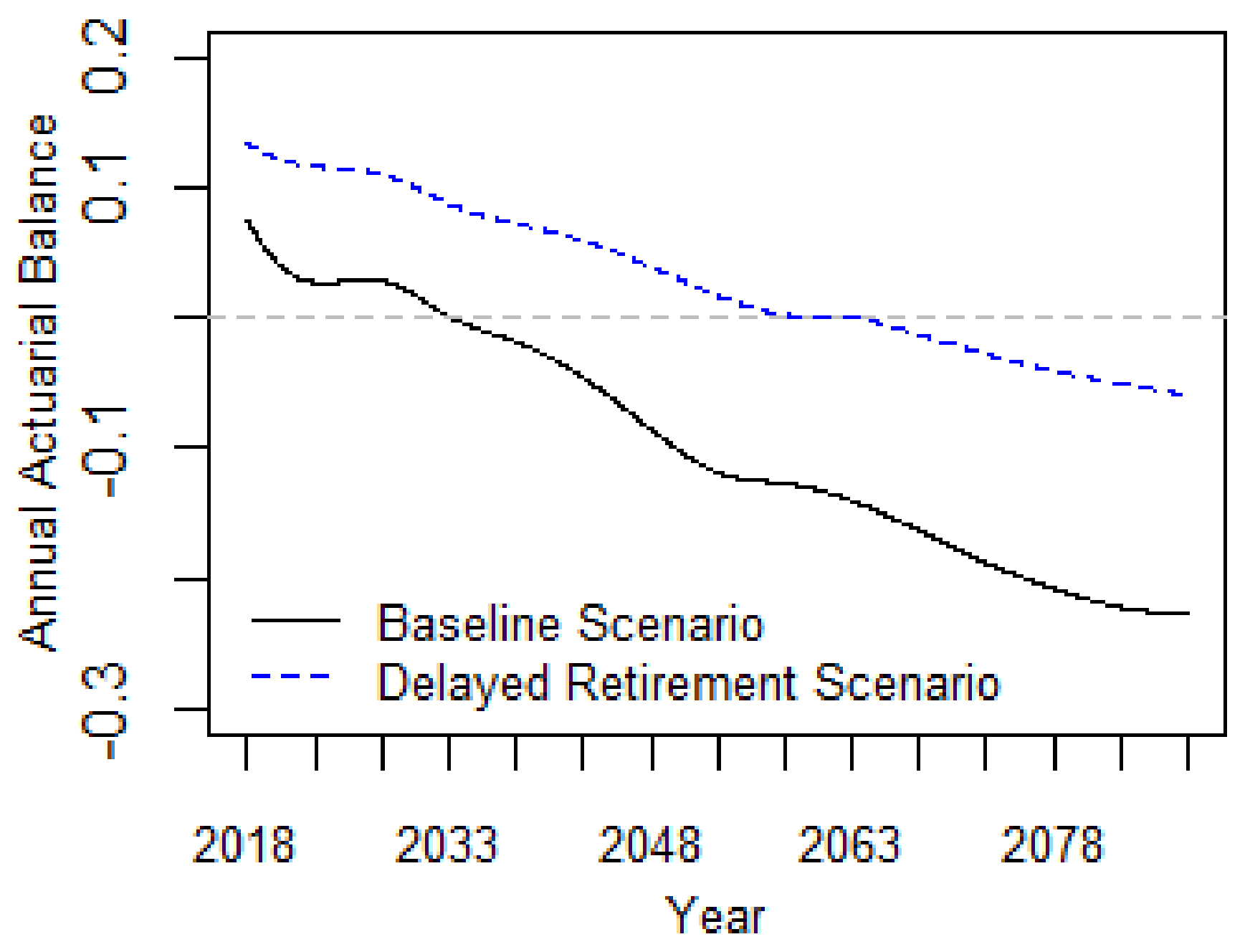

4.2. Stochastic Assessment of Annual Actuarial Balance

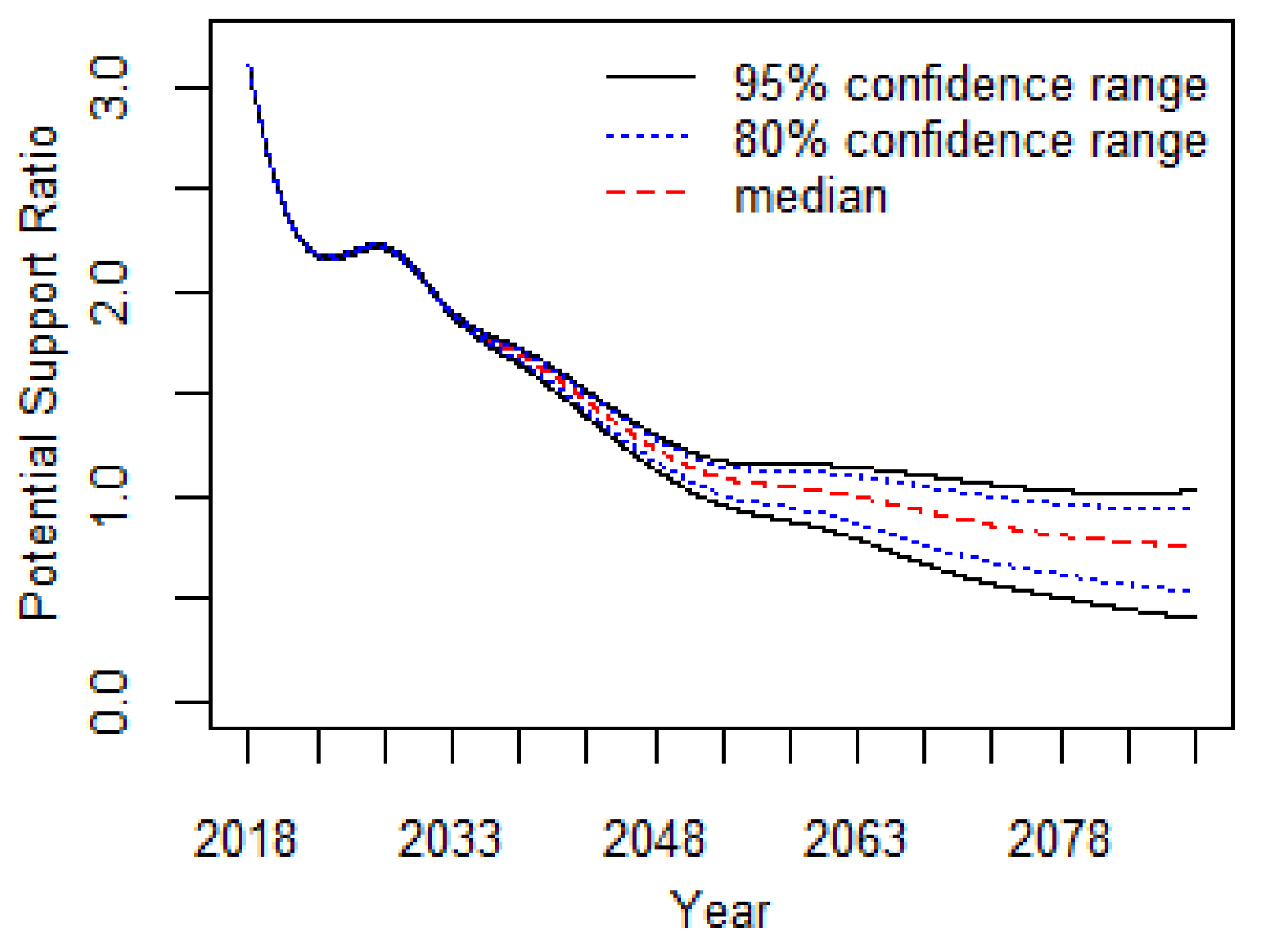

4.3. Stochastic Assessment of Potential Support Ratio

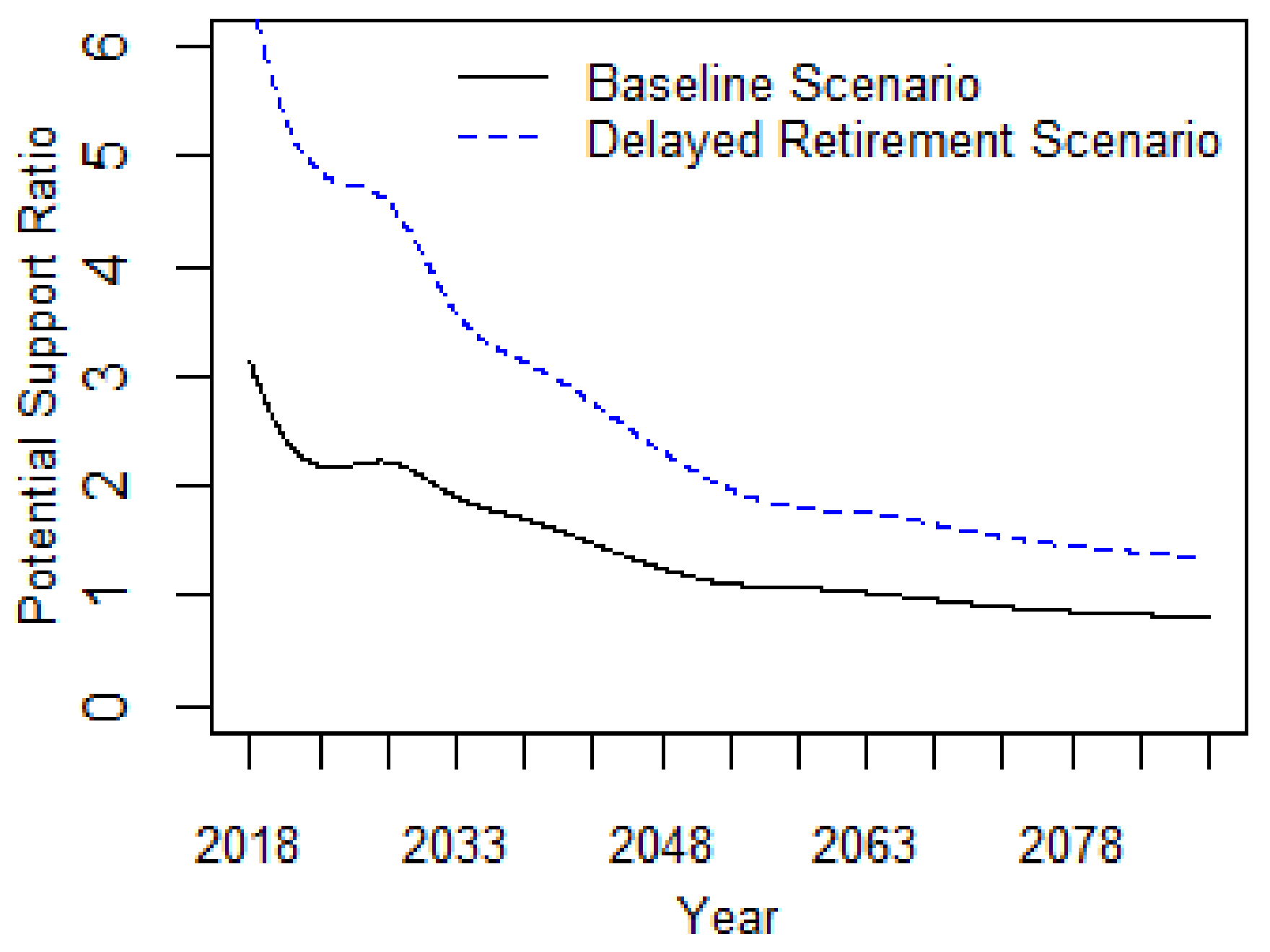

5. Scenario Analysis

6. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- James, E. How can China solve its old age security problem? The interaction between pension, SOE and financial market reform. Comp. Econ. Soc. Syst. 2003, 1, 53–75. [Google Scholar] [CrossRef]

- CBO’s Long-Term Modeling Group. Uncertainty in Social Security’s Long-Term Finances: A Stochastic Analysis; Congressional Budget Office, Congress of the United States: Washington, DC, USA, 2001.

- Lee, R.D.; Anderson, M.W. Tuljapurkar, S. Stochastic forecasts of the social security trust fund. SSRN Electron. J. 2003. [Google Scholar] [CrossRef]

- Cheng, A.W.; Miller, M.L.; Morris, M.; Schultz, J.P.; Skirvin, J.P.; Walder, D.P. A stochastic Model of the Long-Range Financial Status of the Oasdi Program; Office of the Chief Actuary, U.S. Social Security Administration: Baltimore, MD, USA, 2004.

- Liu, X.; Zhang, Y.; Fang, L.; Li, Y.; Pan, W. Reforming China’s pension scheme for urban workers: Liquidity gap and policies’ effects forecasting. Sustainability 2015, 7, 10876–10894. [Google Scholar] [CrossRef]

- Tian, Y.; Zhao, X. Stochastic forecast of the financial sustainability of basic pension in China. Sustainability 2016, 8, 46. [Google Scholar] [CrossRef]

- Alho, J.M.; Spencer, B.D. Uncertain population forecasting. J. Am. Stat. Assoc. 1985, 80, 306–314. [Google Scholar] [CrossRef] [PubMed]

- Carter, L.R.; Lee, R.D. Modeling and forecasting U.S. sex differentials in mortality. Int. J. Forecast. 1992, 8. [Google Scholar] [CrossRef]

- Lee, R.; Tuljapurkar, S. Uncertain demographic futures and social security finances. Am. Econ. Rev. 1998, 88, 237–241. [Google Scholar]

- Alho, J.M.; Jensen, S.E.H.; Lassila, J. Uncertain Demographics and Fiscal Sustainability; Cambridge University Press: Cambridge, UK, 2008; pp. 224–315. [Google Scholar]

- Lassila, J.; Valkonen, T. Uncertain demographics and pension policy. Rev. Écon. 2008, 59, 913–926. [Google Scholar] [CrossRef]

- Auerbach, A.J.; Lee, R. Welfare and generational equity in sustainable unfunded pension systems. J. Public Econ. 2011, 95, 16–27. [Google Scholar] [CrossRef] [PubMed]

- The State Council of China. Available online: http://www.gov.cn/zhuanti/2015-06/13/content_2878967.htm (accessed on 30 March 2018).

- Ministry of Human Resources and Social Security of the People’s Republic of China. Available online: http://www.mohrss.gov.cn/SYrlzyhshbzb/zwgk/szrs/tjgb/ (accessed on 19 February 2018).

- The State Council of China. Available online: http://www.gov.cn/zhengce/content/2015-08/23/content_10115.htm (accessed on 22 February 2018).

- Fedotenkov, I.; Meijdam, L. Crisis and pension system design in the EU: International spillover effects via factor mobility and trade. Economist 2013, 161, 175–197. [Google Scholar] [CrossRef]

- Schmertmann, C.; Zagheni, E.; Goldstein, J.R.; Myrskylä, M. Bayesian forecasting of cohort fertility. J. Am. Stat. Assoc. 2014, 109, 500–513. [Google Scholar] [CrossRef]

- CBO’s Long-Term Modeling Group. Quantifying Uncertainty in the Analysis of Long-Term Social Security Projections; Congressional Budget Office, Congress of the United States: Washington, DC, USA, 2005.

- Thomas, J.R.; Clark, S.J. More on the cohort-component model of population projection in the context of HIV/AIDS: A Leslie matrix representation and new estimates. Demogr. Res. 2011, 25, 39–101. [Google Scholar] [CrossRef] [PubMed]

- Tian, F. Demographic probabilistic forecast method and its application. Northwest Popul. J. 2011, 5, 9–13. [Google Scholar]

- Pânzaru, C. On the sustainability of the Romanian pension system in the light of population declining. Procedia Soc. Behav. 2015, 183, 77–84. [Google Scholar] [CrossRef]

- Zhao, Y.; Bai, M.; Liu, Y.; Hao, J. Quantitative analyses of transition pension liabilities and solvency sustainability in China. Sustainability 2017, 9, 2252. [Google Scholar] [CrossRef]

- National Bureau of Statistics of the People’s Republic of China. Available online: http://www.stats.gov.cn/tjsj/ndsj/2014/indexch.htm (accessed on 12 September 2017).

- Wang, X.; Mi, H. Pension deficit: Scope, methodology and measurement. J. Quant. Tech. Econ. 2013, 10, 49–62. [Google Scholar]

- Yang, D.U.; Wang, M. Demographic ageing and employment in China; ILO Employment Working Paper; No. 57; Employment Sector, International Labor Office: Geneva, Switzerland, 2010. [Google Scholar]

- The State Council of China. Available online: http://www.gov.cn/zhengce/content/2017-01/25/content_5163309.htm (accessed on 19 October 2017).

- Curtis, C.C.; Lugauer, S.; Mark, N.C. Demographics and aggregate household saving in Japan, China, and India. J. Macroecon. 2017, 51, 175–191. [Google Scholar] [CrossRef]

- Curtis, C.C.; Lugauer, S.; Mark, N.C. Demographic Patterns and Household Saving in China. AEJ Macroecon. 2015, 7, 58–94. [Google Scholar] [CrossRef]

- Song, Z.M.; Storesletten, K.; Wang, Y.; Zilibotti, F. Sharing high growth across generations: Pensions and demographic transition in China. AEJ Macroecon. 2015, 7, 1–39. [Google Scholar] [CrossRef] [Green Version]

- Lugauer, S.; Mark, N.C. The role of household saving in the economic rise of China. SSRN Electron. J. 2013. [Google Scholar] [CrossRef]

- Wei, S.-J.; Zhang, X.B. The competitive saving motive: Evidence from rising sex ratios and savings rates in China. J. Political Econ. 2011, 119, 511–564. [Google Scholar] [CrossRef]

- Imrohoroglu, A.; Zhao, K. The Chinese saving rate: Long-term care risks, family insurance, and demographics. J. Monet. Econ. 2018. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Age Range | Estimates of Fertility Time-Series Equations | σ (Residual) |

|---|---|---|

| 15–19 | 2.23 | |

| 20–24 | 16.11 | |

| 25–29 | 20.91 | |

| 30–34 | 7.63 | |

| 35–39 | 3.64 | |

| 40–44 | 1.73 | |

| 45–49 | 0.96 |

| Year | 95% Confidence Range | 80% Confidence Range | Median | Mean | s.d. | ||

|---|---|---|---|---|---|---|---|

| 2018 | 4.43 | 4.44 | 4.43 | 4.43 | 4.43 | 4.43 | 1.62 × 10−3 |

| 2023 | 6.07 | 6.12 | 6.08 | 6.11 | 6.09 | 6.09 | 1.56 × 10−2 |

| 2028 | 8.41 | 8.56 | 8.44 | 8.54 | 8.49 | 8.49 | 4.39 × 10−2 |

| 2033 | 9.73 | 10.10 | 9.79 | 10.03 | 9.91 | 9.91 | 0.109 |

| 2038 | 8.88 | 10.36 | 9.15 | 10.12 | 9.63 | 9.63 | 0.434 |

| 2043 | 2.25 | 7.27 | 3.13 | 6.38 | 4.79 | 4.77 | 1.46 |

| 2048 | −17.01 | −4.09 | −14.87 | −6.44 | −10.64 | −10.63 | 3.76 |

| 2053 | −57.41 | −28.23 | −52.32 | −33.38 | −42.88 | −42.88 | 8.47 |

| 2058 | −126.09 | −65.39 | −115.21 | −76.10 | −95.66 | −95.79 | 17.6 |

| 2063 | −240.58 | −122.18 | −220.77 | −142.31 | −182.01 | −181.94 | 34.6 |

| 2068 | −436.28 | −206.73 | −398.79 | −249.04 | −325.03 | −324.34 | 66.7 |

| 2073 | −752.24 | −341.79 | −689.22 | −417.79 | −557.68 | −554.43 | 1.20 × 102 |

| 2078 | −1234.01 | −552.10 | −1133.82 | −680.81 | −920.21 | −910.92 | 2.00 × 102 |

| 2083 | −1963.06 | −870.33 | −1807.37 | −1076.94 | −1470.01 | −1450.61 | 3.21 × 102 |

| 2088 | −3025.56 | −1305.51 | −2790.65 | −1649.59 | −2270.59 | −2234.26 | 5.04 × 102 |

| Year | 95% Confidence Range | 80% Confidence Range | Median | Mean | s.d. | ||

|---|---|---|---|---|---|---|---|

| 2018 | 0.075383 | 0.075688 | 0.075433 | 0.075632 | 0.07553 | 0.075531 | 7.76 × 10−5 |

| 2023 | 0.026665 | 0.028059 | 0.026915 | 0.027809 | 0.02735 | 0.027356 | 0.000354 |

| 2028 | 0.027938 | 0.029892 | 0.028263 | 0.029523 | 0.028875 | 0.028893 | 0.000494 |

| 2033 | −0.00047 | 0.002568 | 2.19 × 10−5 | 0.001989 | 0.000991 | 0.001006 | 0.000777 |

| 2038 | −0.02614 | −0.0117 | −0.02324 | −0.01396 | −0.01851 | −0.01859 | 0.003659 |

| 2043 | −0.06197 | −0.03145 | −0.05633 | −0.03627 | −0.04582 | −0.0461 | 0.007786 |

| 2048 | −0.1156 | −0.06014 | −0.10462 | −0.06866 | −0.0854 | −0.08619 | 0.014085 |

| 2053 | −0.17023 | −0.07985 | −0.15091 | −0.09237 | −0.11883 | −0.12069 | 0.022888 |

| 2058 | −0.20048 | −0.07562 | −0.17301 | −0.09173 | −0.1275 | −0.13058 | 0.032021 |

| 2063 | −0.24456 | −0.07072 | −0.20317 | −0.09172 | −0.14067 | −0.14499 | 0.044723 |

| 2068 | −0.32493 | −0.0695 | −0.25824 | −0.09612 | −0.1637 | −0.17181 | 0.065755 |

| 2073 | −0.41357 | −0.07195 | −0.31719 | −0.10434 | −0.18857 | −0.2025 | 0.089838 |

| 2078 | −0.49315 | −0.07495 | −0.36625 | −0.11045 | −0.20807 | −0.22794 | 0.112879 |

| 2083 | −0.58198 | −0.07198 | −0.41439 | −0.11056 | −0.22254 | −0.25016 | 0.143976 |

| 2088 | −0.66239 | −0.06359 | −0.44998 | −0.10496 | −0.22578 | −0.26092 | 0.176715 |

| Year | 95% Confidence Range | 80% Confidence Range | Median | Mean | s.d. | ||

|---|---|---|---|---|---|---|---|

| 2018 | 3.10945 | 3.118086 | 3.110851 | 3.116494 | 3.113611 | 3.113644 | 0.002204 |

| 2023 | 2.172967 | 2.192129 | 2.176384 | 2.188667 | 2.182335 | 2.182424 | 0.004854 |

| 2028 | 2.207609 | 2.235412 | 2.21218 | 2.230084 | 2.220849 | 2.221124 | 0.007035 |

| 2033 | 1.882788 | 1.914331 | 1.887838 | 1.908253 | 1.897854 | 1.898029 | 0.008064 |

| 2038 | 1.642543 | 1.755201 | 1.663965 | 1.736208 | 1.699935 | 1.699841 | 0.028576 |

| 2043 | 1.385562 | 1.568494 | 1.416325 | 1.536583 | 1.476993 | 1.476635 | 0.046629 |

| 2048 | 1.131954 | 1.373179 | 1.172689 | 1.329793 | 1.251899 | 1.251366 | 0.061287 |

| 2053 | 0.956134 | 1.264857 | 1.008603 | 1.210517 | 1.11018 | 1.10929 | 0.078235 |

| 2058 | 0.879054 | 1.277324 | 0.943726 | 1.206746 | 1.074957 | 1.074686 | 0.101637 |

| 2063 | 0.78928 | 1.296217 | 0.870382 | 1.202888 | 1.030029 | 1.033604 | 0.129188 |

| 2068 | 0.667377 | 1.299924 | 0.764521 | 1.183047 | 0.96324 | 0.969851 | 0.1614 |

| 2073 | 0.570588 | 1.287346 | 0.676906 | 1.150322 | 0.900967 | 0.908694 | 0.183949 |

| 2078 | 0.504966 | 1.273002 | 0.618137 | 1.127438 | 0.85774 | 0.866228 | 0.19812 |

| 2083 | 0.447586 | 1.286874 | 0.569677 | 1.126997 | 0.828336 | 0.838052 | 0.215241 |

| 2088 | 0.405848 | 1.327825 | 0.538482 | 1.147676 | 0.822016 | 0.8345 | 0.236383 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhao, Y.; Bai, M.; Feng, P.; Zhu, M. Stochastic Assessments of Urban Employees’ Pension Plan of China. Sustainability 2018, 10, 1028. https://doi.org/10.3390/su10041028

Zhao Y, Bai M, Feng P, Zhu M. Stochastic Assessments of Urban Employees’ Pension Plan of China. Sustainability. 2018; 10(4):1028. https://doi.org/10.3390/su10041028

Chicago/Turabian StyleZhao, Yueqiang, Manying Bai, Peng Feng, and Mengyuan Zhu. 2018. "Stochastic Assessments of Urban Employees’ Pension Plan of China" Sustainability 10, no. 4: 1028. https://doi.org/10.3390/su10041028