The Study of Utility Valuation of Single-Name Credit Derivatives with the Fast-Scale Stochastic Volatility Correction

Abstract

:1. Introduction

2. Model Setup

2.1. Maximal Expected Utility Problem

2.2. Bond Holder’s Problem and Indifference Price

3. Asymptotic Approximation

3.1. Analysis of the Zero-Strategy Leading Term

3.2. Analysis of the Fast Modification Term

4. Analysis of Fast-Scale Correction under the Exponential Utility Assumption

4.1. Fast-Scale Expansion for Single Name Derivatives

5. Numerical Study of Exponential Utility

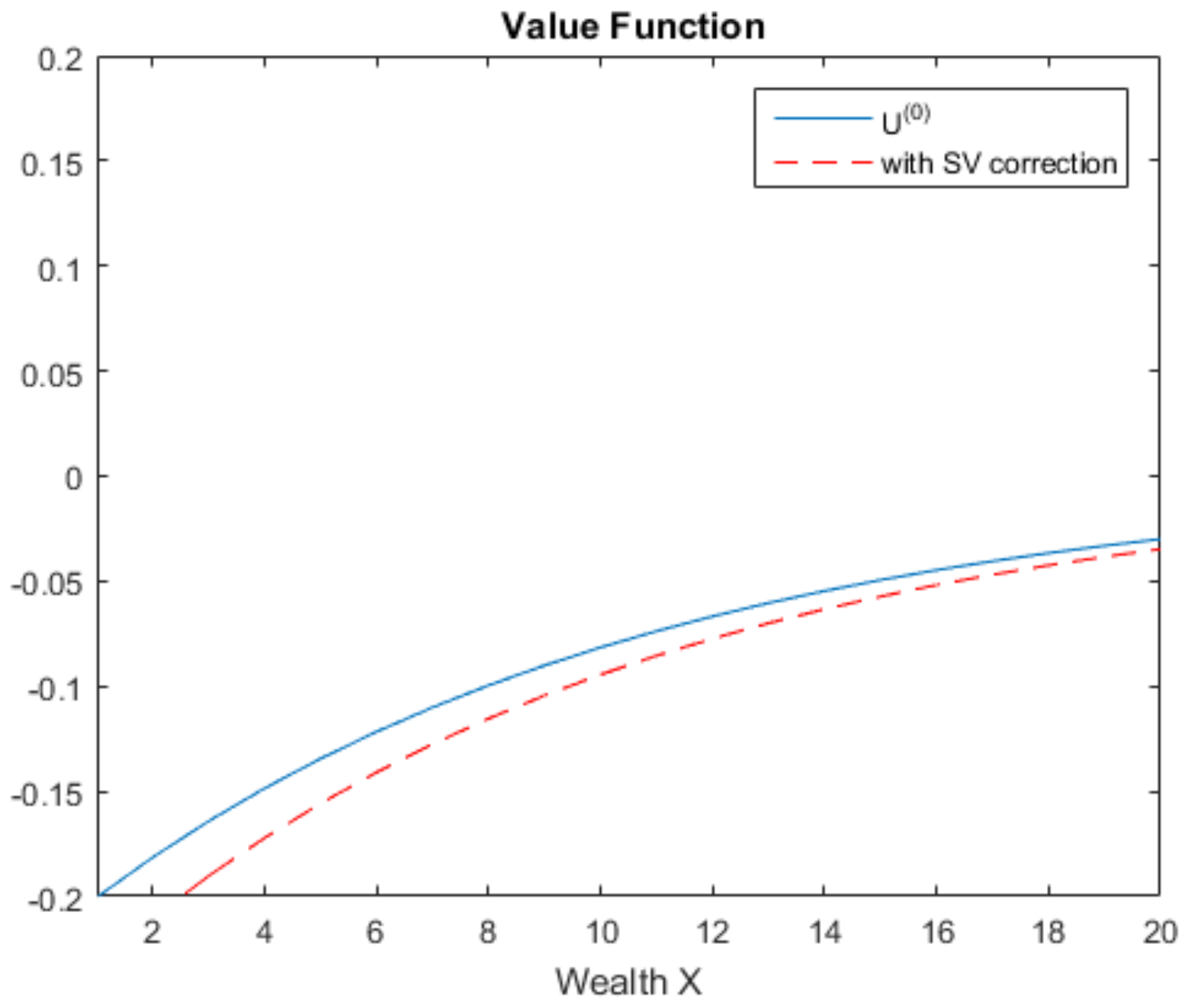

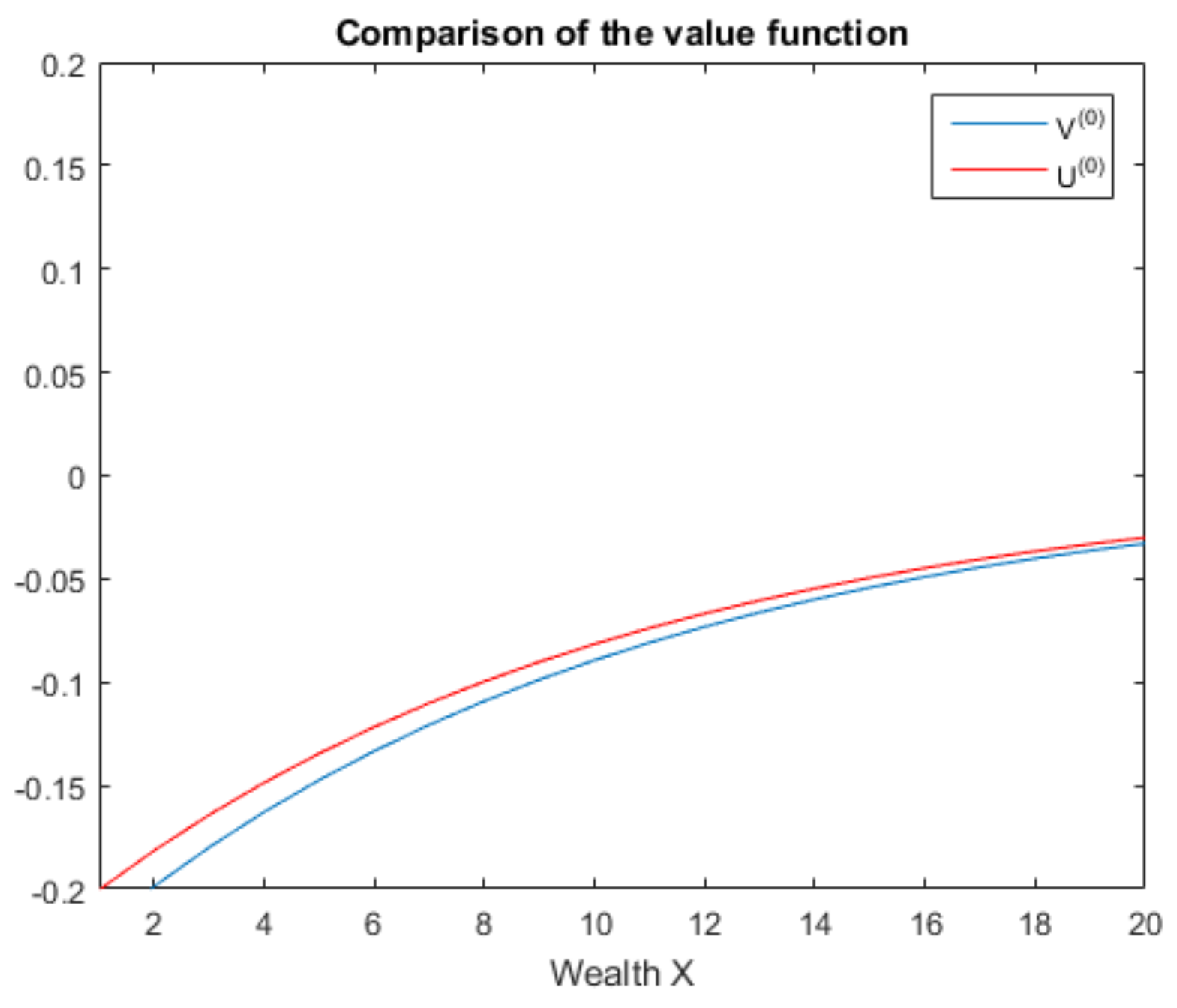

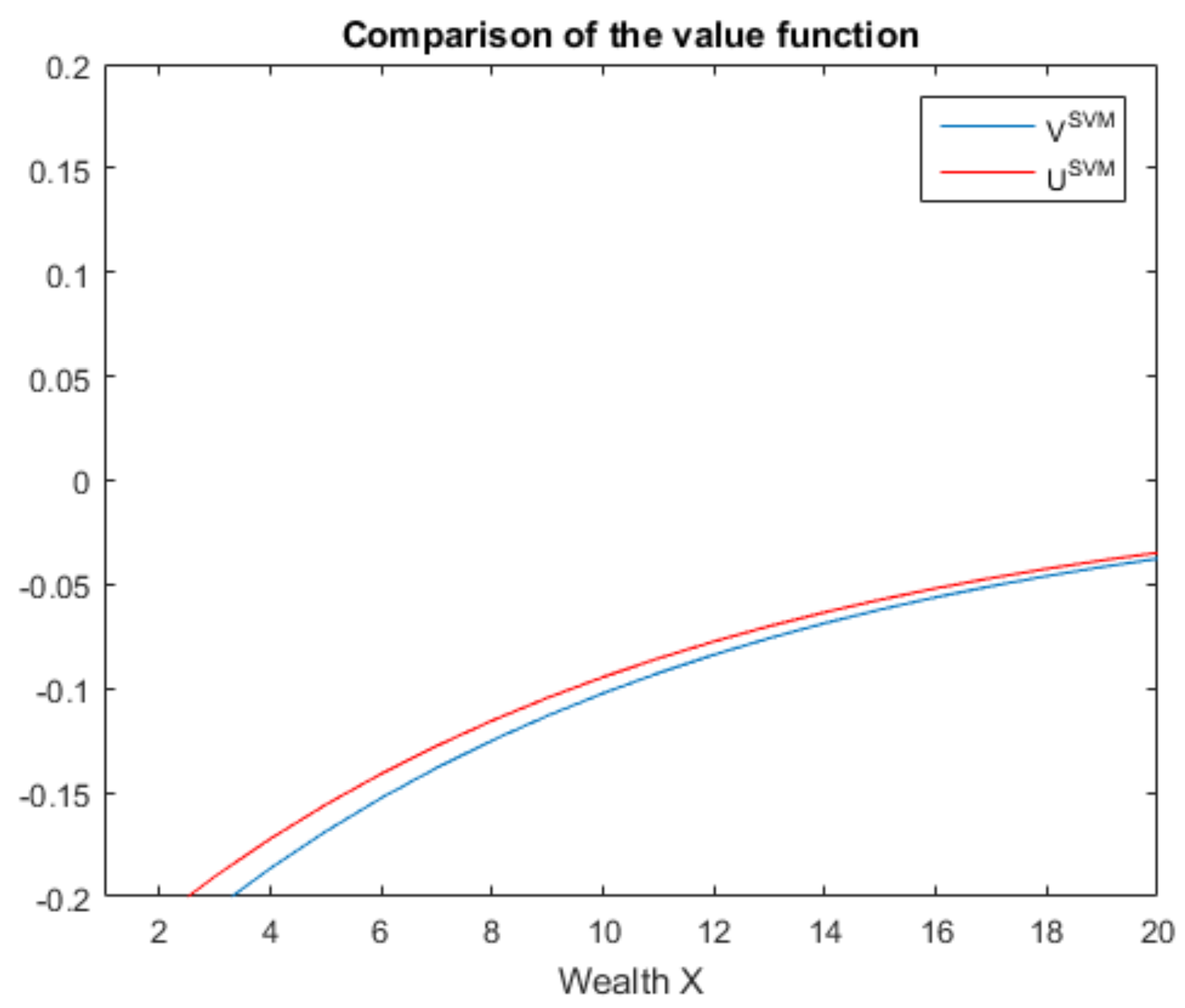

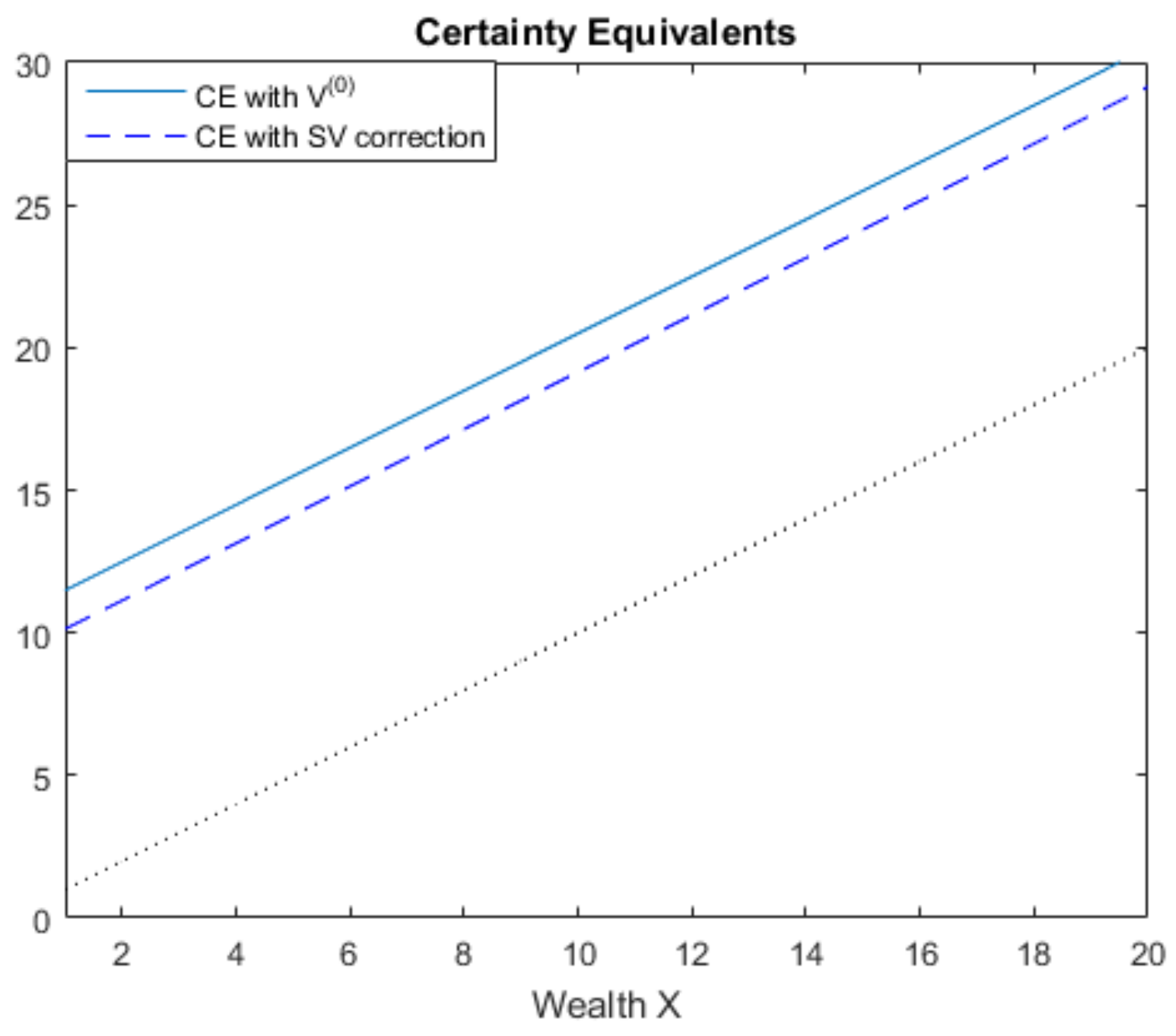

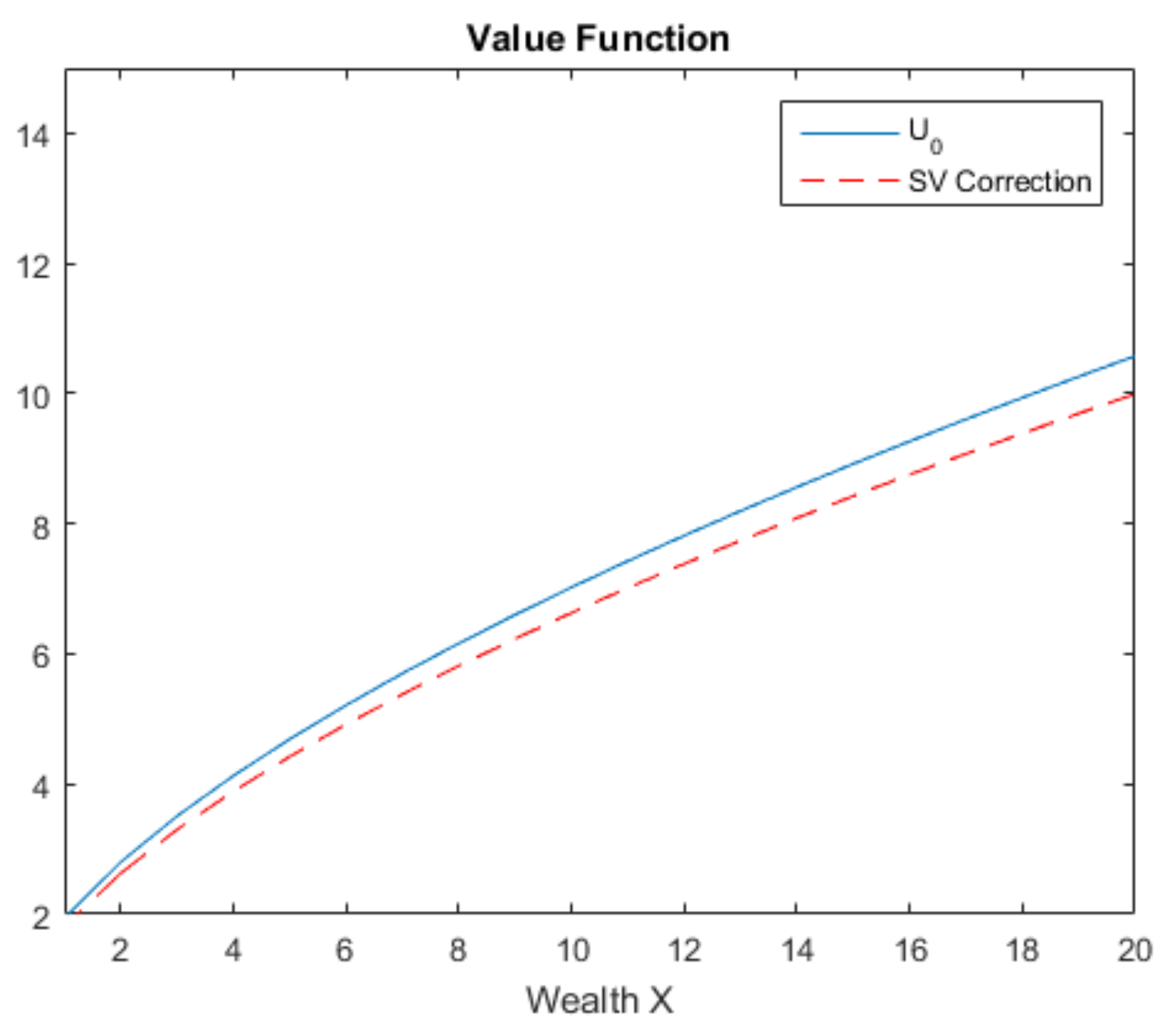

5.1. Analysis of the Value Function

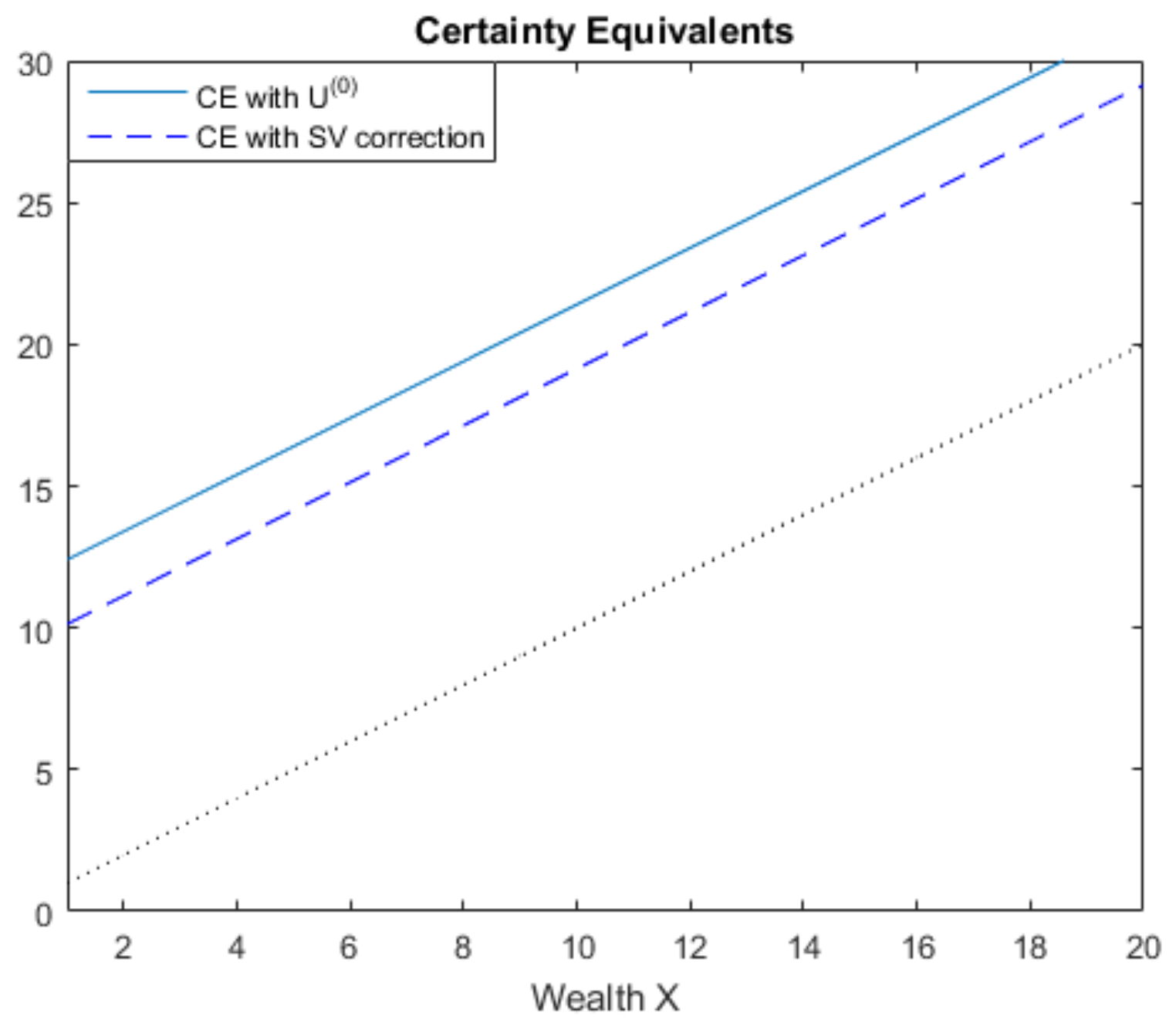

5.2. The Effect of Volatility Correction

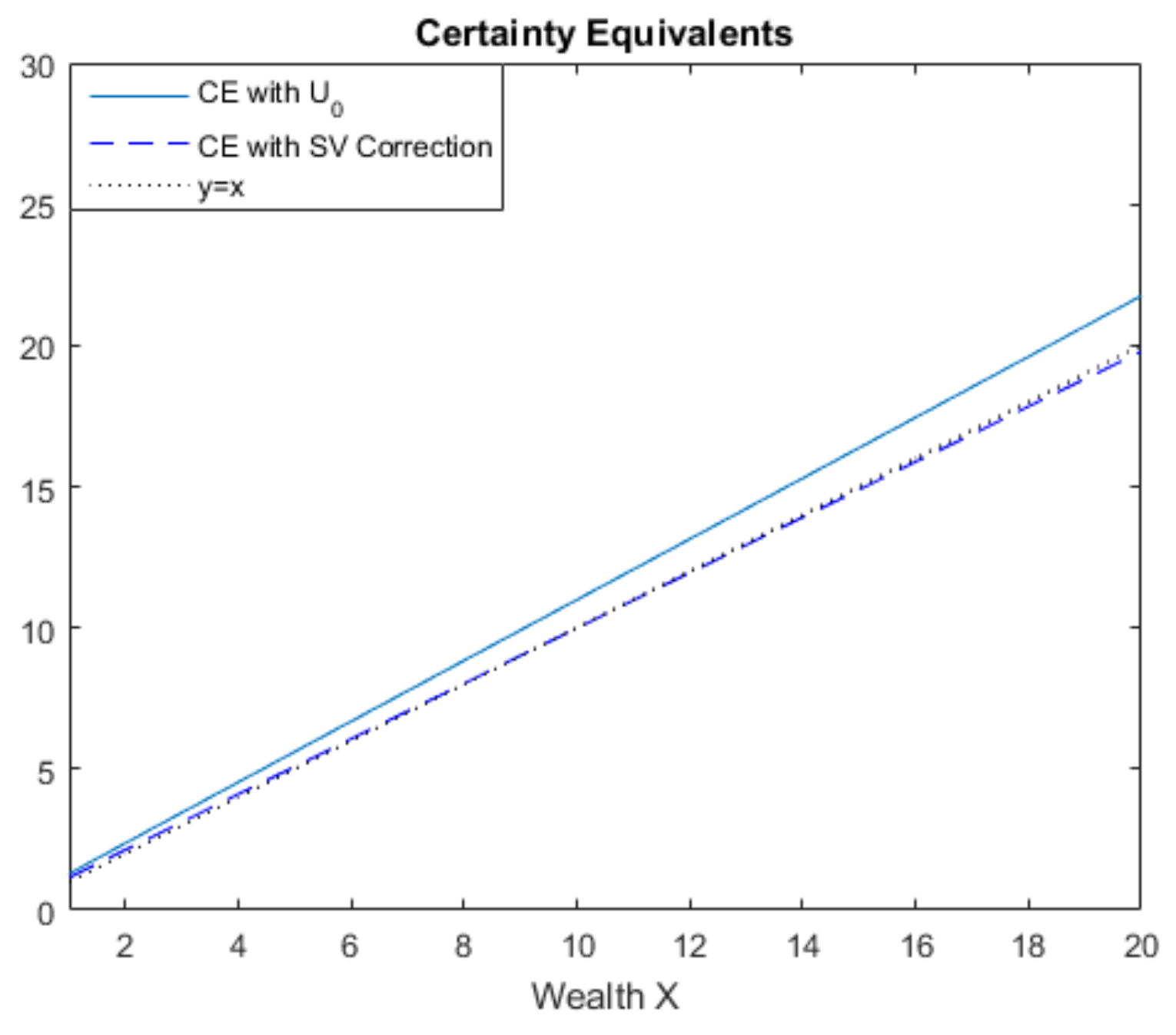

5.3. Analysis of Yield Spread

6. Numerical Study of CRRA Utility

7. Conclusions and Future Work

Acknowledgments

Author Contributions

Conflicts of Interest

Appendix A

References

- Tan, Y.; Floros, C. Risk, capital and efficiency in Chinese banking. J. Int. Financ. Mark. Inst. Money 2013, 26, 378–393. [Google Scholar] [CrossRef] [Green Version]

- Tan, Y. The impacts of risk and competition on bank profitability in China. J. Int. Financ. Mark. Inst. Money 2016, 40, 85–110. [Google Scholar] [CrossRef]

- Madan, D.B.; Unal, H. Pricing the risks of default. Rev. Deriv. Res. 1998, 2, 121–160. [Google Scholar] [CrossRef]

- Jarrow, R.A.; Turnbull, S.M. Pricing derivatives on financial securities subject to credit risk. J. Financ. 1995, 50, 53–85. [Google Scholar] [CrossRef]

- Lando, D. On Cox processes and credit risky securities. Rev. Deriv. Res. 1998, 2, 99–120. [Google Scholar] [CrossRef]

- Hao, C.; Zhang, B.; Carling, K.; Alam, M.M. Review of the Literature on Credit Risk Modeling: Development of the Recent 10 Years; Business Perspectives: Sumy, Ukraine, 2009. [Google Scholar]

- Black, F.; Scholes, M. The pricing of options and corporate liabilities. J. Political Econ. 1973, 81, 637–654. [Google Scholar] [CrossRef]

- Sircar, R.; Zariphopoulou, T. Utility valuation of credit derivatives: Single and two-name cases. Adv. Math. Financ. 2007, 279–301. [Google Scholar] [CrossRef]

- Papageorgiou, E.; Sircar, R. Multiscale intensity models for single name credit derivatives. Appl. Math. Financ. 2008, 15, 73–105. [Google Scholar] [CrossRef]

- Merton, R.C. Optimum consumption and portfolio rules in a continuous-time model. J. Econ. Theory 1971, 3, 373–413. [Google Scholar] [CrossRef]

- Heston, S.L. A closed-form solution for options with stochastic volatility with applications to bond and currency options. Rev. Financ. Stud. 1993, 6, 327–343. [Google Scholar] [CrossRef]

- Longstaff, F.A.; Schwartz, E.S. A simple approach to valuing risky fixed and floating rate debt. J. Financ. 1995, 50, 789–819. [Google Scholar] [CrossRef]

- Fouque, J.P.; Papanicolaou, G.; Sircar, R.; Solna, K. Multiscale stochastic volatility asymptotics. Multiscale Model. Simul. 2003, 2, 22–42. [Google Scholar] [CrossRef]

- Fouque, J.P.; Sircar, R.; Zariphopoulou, T. Portfolio optimization and stochastic volatility asymptotics. Math. Financ. 2017, 27, 704–745. [Google Scholar] [CrossRef]

- Hodges, S.D.; Neuberger, A. Optimal Replication of Contingent Claims under Transaction Costs. Rev. Futures Mark. 1989, 8, 222–239. [Google Scholar]

- Davis, M.; Yoshikawa, D. An equilibrium approach to indifference pricing. Adv. Financ. Eng. 2012, 29–56. [Google Scholar] [CrossRef]

- Fouque, J.P.; Papanicolaou, G.; Sircar, R.; Solna, K. Multiscale Stochastic Volatility for Equity, Interest Rate, and Credit Derivatives; Cambridge University Press: Cambridge, UK, 2011. [Google Scholar]

- Duffie, D.; Zariphopoulou, T. Optimal investment with undiversifiable income risk. Math. Financ. 1993, 3, 135–148. [Google Scholar] [CrossRef]

- Sircar, R.; Zariphopoulou, T. Utility valuation of multi-name credit derivatives and application to CDOs. Quant. Financ. 2010, 10, 195–208. [Google Scholar] [CrossRef]

- Brémand, P. Point Processes and Queues; Springer: New York, NY, USA, 1981. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Name | Value | Sensitivity |

|---|---|---|

| 0.11 | 3.65% | |

| v | 0.25 | 1.80% |

| 0.5 | 1.32% | |

| 0.5 | −19.61% |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, S.; Zhou, Y.; Wiwatanapataphee, B.; Wu, Y.; Ge, X. The Study of Utility Valuation of Single-Name Credit Derivatives with the Fast-Scale Stochastic Volatility Correction. Sustainability 2018, 10, 1027. https://doi.org/10.3390/su10041027

Liu S, Zhou Y, Wiwatanapataphee B, Wu Y, Ge X. The Study of Utility Valuation of Single-Name Credit Derivatives with the Fast-Scale Stochastic Volatility Correction. Sustainability. 2018; 10(4):1027. https://doi.org/10.3390/su10041027

Chicago/Turabian StyleLiu, Shican, Yanli Zhou, Benchawan Wiwatanapataphee, Yonghong Wu, and Xiangyu Ge. 2018. "The Study of Utility Valuation of Single-Name Credit Derivatives with the Fast-Scale Stochastic Volatility Correction" Sustainability 10, no. 4: 1027. https://doi.org/10.3390/su10041027