1. Introduction

Credence attributes are quality features of a product that cannot readily be ascertained by direct experience [

1] Unlike credence attributes, “search” and “experience” attributes are readily discernible by customers, e.g., by the colour, odour (search attributes) or taste (experience attribute) of, e.g., an apple [

1]. Credence attributes have emerged predominantly in the agricultural food production sector and the fashion industry as part of the marketing of products [

2]. Examples of credence attributes in the agricultural sector include environmental stewardship, animal welfare, fair trade, organic products, listed country of origin, or locally grown goods [

3], while quality in production, including the toxicity of dyes and the durability of materials, is important for fashion garments [

4].

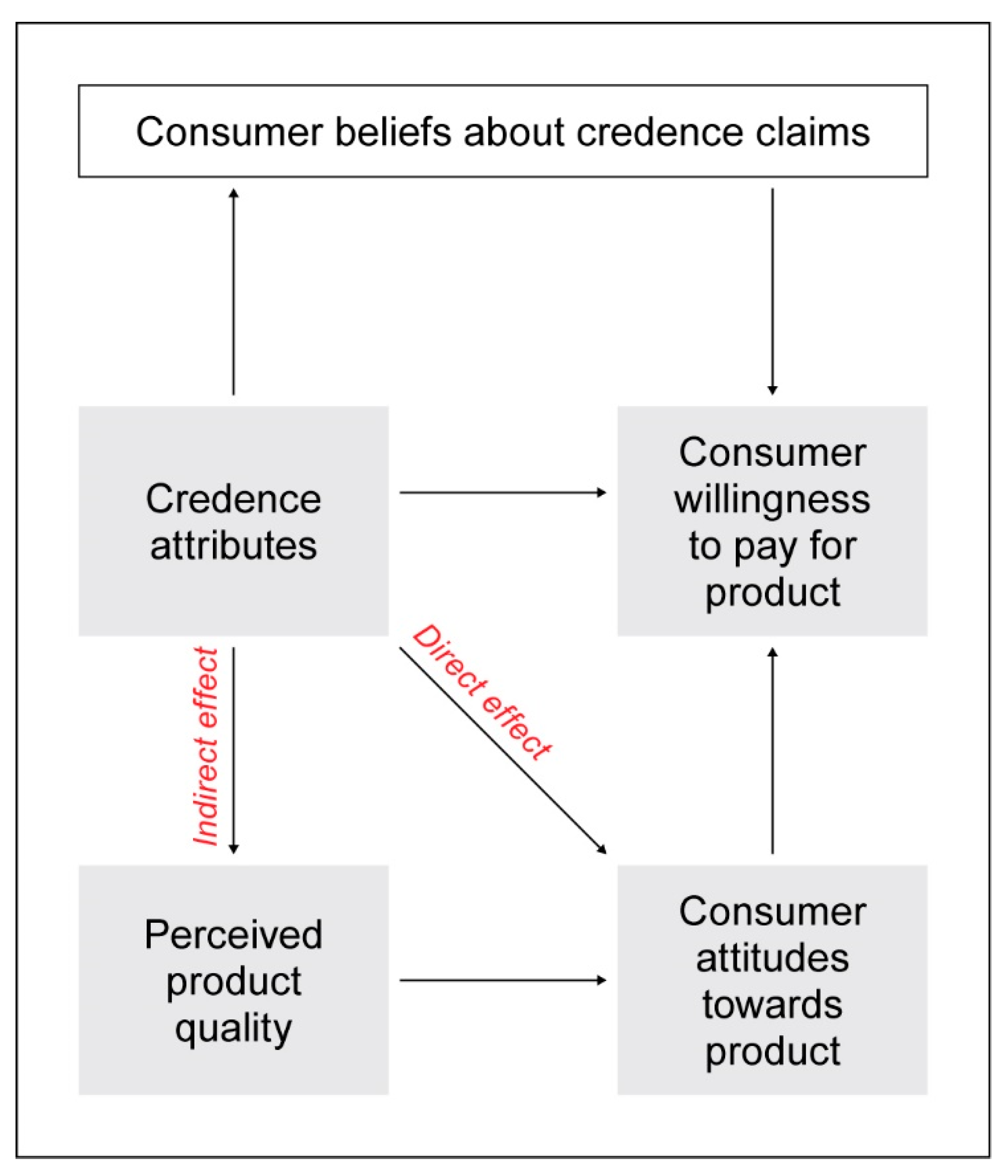

Credence attributes add value to a product and that can result in increased willingness to pay a price premium, or create new market segments (

Figure 1). Sellers typically make claims about credence attributes, which are often expressed by different product labels or certification schemes, or are sometimes reinforced by developing authentic brands and trademarks, which customers will trust [

3]. Therefore, some people are willing to pay more for products carrying a label identifying specific credence features [

5,

6]. If a proper credence system has been clearly established, it was found that consumers would likely pay a premium price for eco-labelled or certified forest products [

7,

8,

9] or even eco-labelled household products [

10].

New Zealand has a large and innovative agricultural sector and therefore focused on understanding the role of credence attributes early on. Several private and public sector initiatives exist in the food and agriculture sectors in New Zealand, which recognise commercial threats and opportunities associated with international consumer attitudes to credence attributes, especially around environmentally sustainable production practices [

3]. Examples of private sector initiatives include sustainable production of wine, dairy, and kiwifruit. Preference of credence attributes in New Zealand’s key markets have been studied [

13] and information on overseas consumer opinions on the value of environmental or social aspects for agricultural products have been collected [

14].

Finally, credence attributes also play an important role in the primary sector in New Zealand, considering international and national key future trends and challenges that impact land-use change/practice [

15]. The attractiveness of different credence attributes varies in different countries and markets. Consumer surveys undertaken in New Zealand’s main export markets for agricultural products (China, India, Indonesia, Japan, and the UK) show that the most important attribute is food safety, and this always ranks highly. Conversely other attributes considered less important overall (e.g., environmental condition, use of pesticides, traceability of origin, or animal welfare) vary in importance in different countries [

3]. These data suggest that consumers in China, India, and Indonesia are more likely to give greater importance to credence attributes than consumers from Japan and the United Kingdom. At an on-farm level, delivering ‘green’ dairy products in New Zealand can achieve a price premium of 5.3% to 47.5% for environmentally friendly dairy products [

16]. One key factor of credence attributes in the food sector is the ‘country of origin label’, which is even mandatory for some products in New Zealand’s major export countries such as China, Australia, the EU, and the USA [

13]. This label is also sometimes associated with attributes such as quality and food safety [

17,

18].

Unlike agricultural industries, where the primary production is targeted toward food or fashion sectors, the term ‘credence attributes’ is not used frequently within the global forestry sector to date. However, the need to conserve biodiversity, ecosystem services, forest productivity, and the prosperity of forest dependent communities is recognised in most countries, and thus global criteria and indicators to achieve sustainable forest management (SFM) have been agreed to and have existed for a long time [

19]. Given the importance to key markets for recognizing and promoting New Zealand’s agricultural products, this initial study provides the first intentional examination of the application of credence attributes to forest management and forest products marketing. We describe specific credence attributes of forest products and highlight their values and benefits.

Global Synopsis of Forestry & Credence Attributes

Credence attributes are important in food products derived from forests as well. Around 80 percent of the population of the developing world use non-timber/wood forest products (NTFP or NWFP) for health and nutritional needs, and at least 150 NTFP are significant in terms of international trade [

20]. Certification of forest management also includes NTFP [

21,

22,

23], but in principle these products—especially forest food products—could apply for fair trade initiatives, certificates of origin, or even organic certification as well when they are gathered in forests free of chemical treatments [

20]. FSC and PEFC certification are used to promote NTFP; however, the marketing of credence attributes in wood products is much more common [

23,

24].

In addition, wood is widely used as a raw material for the production of food additives and ingredients [

25]. To improve market potential, Stern et al. [

25] suggest that producers of wood-based dietary fibre additives should provide customers with more information and make health claims or introduce communication labels because consumer attitudes towards wood-based food additives are predominantly positive [

25]. This underlines the role that credence attributes of forest products play for customers and producers. The growing use of wood-derived materials in the fashion industry [

26] also indicates a need to account for the credence attributes of forest management and forestry inputs as the raw material supplier into these emergent fashion supply chains (e.g., Tencel cellulosic fibers).

On a forest level, SFM is subject to domestic forest laws but also legality verification, and initiatives such as the EU’s Forest Law Enforcement, Governance, and Trade (FLEGT) apply today and interact with the two main certification schemes PEFC (Programme for the Endorsement of Forest Certification) and FSC (Forest Stewardship Council) [

27].

The development of the first forest certification scheme from the Forest Stewardship Council (FSC) in the 1990s was the result of claims-making and a series of credibility battles and confusion in the marketplace about the sustainability of tropical forest management between growers and producers of forest products and groups advocating environmental protection [

28]. This, unfortunately, resulted in confusion and a lack of reliable mechanisms to improve forest management. However, with environmental groups and a few forest companies both expressing interest in a larger system that could establish the credibility of some claims and discredit others, the certification scheme by a third party was developed [

28].

Certification systems can provide evidence that sustainable forest management has been implemented by forest growers. The most common and widespread certification systems are FSC and PEFC. Today, PEFC is the world’s largest forest certification system with 55 national forest certification systems encompassing more than 300 million hectares of certified forests globally [

29]. In addition, more than 12,500 PEFC chain of custody (CoC) certificates have been issued. FSC was the first certification system, established in 1993. It currently certifies over 228 million hectares worldwide and issued almost 50,000 CoC Certificates [

30]. Both FSC and PEFC have regulations on an international and country-specific scale to ensure sustainable forest management in their area of influence. Globally, FSC uses 10 principles and criteria for forests management [

21]. PEFC’s international ‘Sustainable Forest Management—Requirements’ are outlined in its accepted ‘Sustainability Benchmarks’ [

22]. The benchmark criteria are regularly revised through multi-stakeholder processes to take account of new scientific knowledge, societal change, evolving expectations, and to incorporate the latest best practices. These principles include compliance with national laws, indigenous peoples’ rights, the environmental impact of monitoring and assessing forests, and its management impacts.

Within these schemes, many credence attributes of forest products are covered overall. They have been amalgamated to superordinate categories such as environmental or social aspects. In comparison, credence attributes in the agricultural sector, where specific single attributes are analysed for their respective impacts and value for customers, are only recently beginning to be amalgamated into a ‘sustainable farming’ scheme in New Zealand, named the New Zealand Farm Assurance Programme Plus (NZFAP Plus) [

31]. Surprisingly, there has been little emphasis on understanding the role of specific individual credence attributes in the forestry sector, particularly those that are difficult to certify through certification schemes. This study seeks to address this gap and explores the role of individual credence attributes in forestry and whether it can inform Sustainable Forest Management (SFM), forest certification, the criteria and indicators (C & I) of common forest frameworks such as the Montreal Process, or the environmental, social and governance (ESG) criteria of forest investments.

3. Results and Discussion

Results from our Delphi consultant interviews showed that only eight out of 19 interviewees had heard the term ‘credence attributes’, despite it being a well-known and long-established marketing term, and in growing parlance within the agricultural and food sectors. However, credence attributes, as a concept, were understood by all our participants, but were often caged in different terminology. Our discussions showed that credence attributes in forestry are more often referred to as certification indicators (by commonly used certification schemes such as PEFC or FSC), but are also described with regard to social licence to operate (SLO), corporate social responsibility (CSR), or in regard to ESG criteria (environmental, social, and governance). There is also a tendency to defer to products as deriving from an all-encompassing ‘sustainable forest management’ rather than to identify any specific attribute of a product in terms of how the management of the forest sustainably contributed to the product’s desirability.

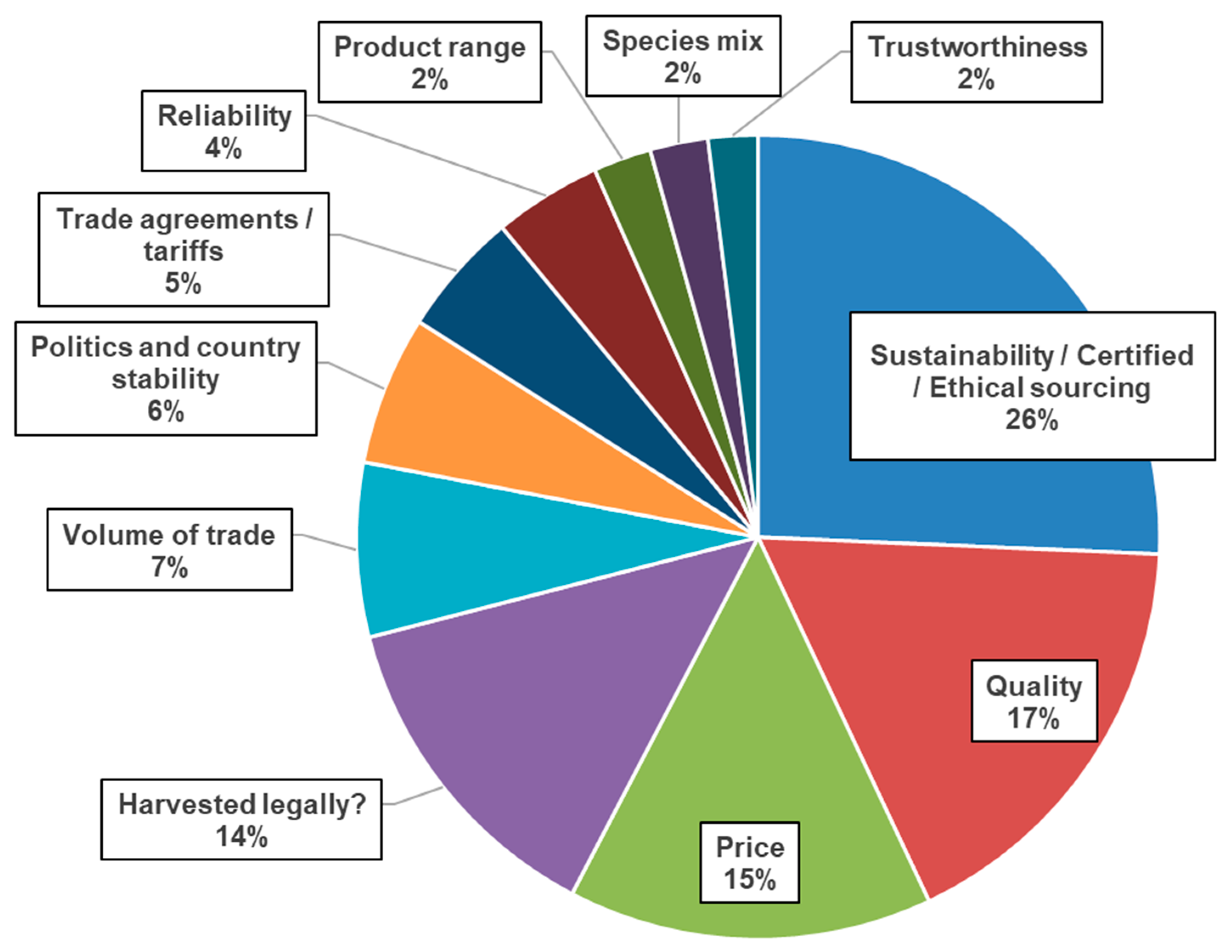

The most noted credence attributes relate to legality of the forest product and highlight the important role of forest certification. Over a quarter of respondents (26%) to our online questionnaire stated certification to be one of the three most important aspects they considered regarding forests products trade (

Figure 2). The survey also showed that PEFC and FSC are the most well-known (86% and 95% respectively) certification schemes, while only 10% were aware of China Environmental Labelling (CEL). Interestingly, the Forest Certification for Ecosystem Services (ForCES), an FSC pilot project to expand and enhance environmental standards, was known to about 14% of survey respondents.

Furthermore, the international experts from our Delphi interviews believe that from a credence perspective, sustainable forest management (SFM) is fundamental and essential in the production of forest products—although what that exactly means was not clearly defined. Trusted supply chains, especially around legality but also on sustainability are a key feature in the trade of forest products.

Most of the experts we interviewed see forest certification in a pivotal role and recommend that it should be developed further. It is seen as an important indicator in global forest trade, particularly the well-known schemes, FSC and PEFC. Certification of the forest as well as the supply chain (chain of custody) currently seems to be the best tool to ensure ecological and social criteria in forestry. However, the expectations on sustainability (economically, ecologically, socially) and multifunctionality (protection of the resource, timber production, job creation, recreation, and biodiversity on the same area) vary substantially between countries as well as certification systems. In addition, while evidence of impacts exists in certain areas and on certain indicators, the impact of forest certification is still hard to quantify and prove on a large scale. Several challenges around the availability of spatially explicit, openly accessible, or standardized data on forest certification make it hard to draw general inferences about whether forest certification is achieving its intended positive social and environmental impacts [

27].

Several of the most desired attributes of forest products from the perspective of our Delphi interviewees in the international market are believed to be “search-” or “experience” attributes. This includes quality features such as special characteristics/specifications dependent on the intended use. Uniformity, for instance, is important for standardised industrial uses, which is of major concern for many importers. On the other hand, versatility is considered as beneficial because timber can be put to a range of different uses.

Demanded physical properties include strength, storage capability, long fibres, colour/aesthetic value, or durability, but demands and grades differ by countries and intended uses. Some very important desired attributes of forest products gather around availability and reliability (consistency) of the supply of the product as well as—of course—price. While price was a strong consideration in whether to trade in international forest products by fifteen per cent of the online survey respondents, it was not the most important factor. When prompted to provide factors in order of importance, quality, sustainability, and legality were commonly listed, whereas price was not ranked by any of the 37 respondents as the prominent factor (

Figure 3). One reason for that might be that pricing mechanisms in forestry are strongly influenced by supply and demand and also views on relative qualities and substitution, e.g., between Douglas fir and radiata pine or between pruned and A-grade logs. In addition, the ability for forest growers to hold stock in the forest warehouse and continue to add value makes a point of differentiation compared to seasonal sectors such as agri-food and horticulture. Arguably, in an inflexible seasonal context, credence attributes might even offer greater value.

Our low survey response rate (12%) may reflect the level of unfamiliarity with the term ‘credence attributes’ among the forestry community. Selected credence attributes are still nascent and emerging within this sector in comparison to the agriculture or food sector. Although several experts in forest products marketing were consulted as part of the Delphi discussions, only a few seemed conversant with the term. Because of this, it may have hindered potential experts in this field from responding to the online survey, or more likely from our results, it is apparent that the field is just emerging within the forest products sector, so very few experts exist. Alternatively, the low response rate may reflect that web-based surveys provide lower responses than other modes [

34], while still providing accurate and representative results with high validity [

35].

Search and experience attributes are not the only factors considered within international wood products markets; credence attributes currently play an important role and this role is also expected to increase in the future. No matter how superior quality the forest product is, the ultimate condition expressed by online survey respondents are that products are acquired by legal means and illegal logging is excluded. Assurances of legality are therefore an important social licence attribute and agreed to be a key feature and part of the exclusion criteria for illegal traders.

Another very important attribute is ‘without deforestation’ (and without virgin forest destruction). Forest regeneration after harvest and not clearing natives was also of high concern and importance from the expert’s view. ‘Without clear-cuts’ was also mentioned several times during our Delphi interviews as being an important aspect. However, most Delphi experts used the general terms ‘environmental protection/management/aspects’ when interviewed, which included protection of ecosystem services such as biodiversity, soil (erosion control), water conservation, and protected species. These items were also collectively categorised and described as sustainability or sustainable forest management (SFM) as a summary of credence attributes in our interview discussions. Origin is believed to be a crucial factor in the interviewed experts’ view when it comes to trust, legality and sustainability. However, origin can also play a role regarding fibre miles and carbon footprint.

Experts we interviewed reported concerns about soil disturbance, tropical timber harvesting, or palm oil conversion in South East Asian countries (e.g., Indonesia or Malaysia) or about concerns about the legality of timber as a reoccurring issue, for example in Romania and Russia. Those are issues even with certification because environmental labels (e.g., FSC) have the same international standards but different national interpretations, as these regulations often refer to respective country’s laws and also have country-specific indicators and verifiers, and therefore diverge in different countries. With these reoccurring problems, experts perceive a trend to promote regionality of timber in some countries in Europe.

Fibre miles or carbon footprint refers to the transport distances from the forest to the customer. The Delphi interviewees believed that fibre miles were important in some countries of the EU and Asia; however, most countries currently seem to have lesser concerns around transport distances for wood products, which contrasts with high concern for food miles from New Zealand.

Generally, the environmental credence attributes were regarded as more important than the social credence attributes by most Delphi experts we interviewed. In addition, they were also considered more important in natural forest and less in plantation forests. This contrasts with results from the online survey, which gave high ranking to social and ethical aspects (e.g., lack of child labour, professionalism, social licence, and community engagement) alongside aspects of trust and legality (e.g., certification and political stability), while environmental attributes (e.g., biodiversity, waste, and fibre miles) were lower ranked (

Table 1).

Results from the online survey show the three highest rated credence attributes as being ‘without child labour’ (3.4), ‘place of origin’ (3.3), and ‘deforestation-free’ (3.2) (

Table 1). Amongst the three attributes, ‘place of origin’ had the least ranking variability or coefficient of variation (0.2), indicating that our online respondents consistently regarded this attribute as very important. Ranked 4th and 5th were the credence attributes of the forest company being certified by PEFC and FSC, respectively. Surprisingly, community engagement and biodiversity ranked only 10th and 11th, respectively. The three least rated attributes were ‘packaging waste’ (2.2), ‘fibre miles’ (1.9), and ‘pesticide free’—indicating that those three were of the least concern. The lowest ranking for ‘pesticide free’ might imply that using pesticides in forestry may be a lesser issue than using them in growing food products. In addition, survey participants might have focused on timber products in their reply and not considered the option of food production with NTFP. The last three attributes also have higher coefficient of variation than other higher ranked attributes, suggesting that while some respondents rated them the lowest, others rated them higher.

In the production of forest products that are imported by your country, which of the following claims about how the product was grown and processed are most important?

While some Delphi experts and other researchers believe that forest products with certain credence attributes or labels achieve price premiums in the market [

9,

36,

37,

38,

39,

40,

41,

42], other experts don’t see much concrete evidence from an international market perspective. They report that the regulatory requirements to comply to certain additional standards have not yet been translated into higher prices for some suppliers but have put an extra cost burden on them, and that premiums are also dependent on the product line. However, for some products it is sometimes no longer about getting price premiums, but it increasingly becomes a matter of continued market access, especially in big box stores that demand certified forest products [

43]. This development was anticipated several years ago [

44]. However, whether customers buy from big box stores and pay a price premium for ‘certified’ products, or only buy at these shops due to reliability and predictability, availability of supply cannot be ascertained. Hence, certification was seen by some experts we interviewed as a ‘seal of approval’, which is required for market access into the big box stores or for meeting ESG standards of institutional capital.

Higher prices are, however, believed to be realistic for some niche markets for products with credence attributes. This could be some special use or specific, very high quality/certified products, e.g., in the tropical wood sector.

A new and emerging market concerns the health aspects of forest products. According to some experts, this credence attribute is trending and thus rapidly becoming more important, especially in the Asian market, but also partly in the USA. Some consumers want products that are not only free of harmful effects but also had positive health benefits in terms of physical health and wellbeing. For this purpose, forest products should minimize harmful chemical substances in the production process. This could include restrictions on the use of herbicides or pesticides for establishment, pest control, or the impact of the processing of wood and paper used in NTFP packaging. Environmental concerns in some countries led to a prohibition or at least complications of herbicide application for site preparation and release work several years ago (e.g., in Quebec [

45] or parts of Europe). In this context, mechanical release was conducted on high-competition sites and larger stock types were successfully used for establishment [

46]. Health concerns can have strong market effects, as the recent rejection and disposal of manuka honey in Japan shows. Early this year, Japan rejected NZ honey in response to concerns about glyphosate levels, which impacted trade (worth

$71 million NZD in 2019) [

47].

On the other hand, special eco-labels could potentially become a powerful marketing channel for some products in a niche market—sectors whose products are close to people and their health or where special ingredients or substances from wood are particularly desired. Examples mentioned include wood fibre for clothing or the avoidance of treated pine materials in the living areas of people. Furthermore, purposeful organic cultivation in forest environments could become part of food production (NTFP) or be managed differently through an agroforestry system where trees and other plants such as ginseng grow together. Thus, food harvested from forests could be organically grown, which might be a new type of value-added forest product. Such a brand story is a growth opportunity for premiums in specialised and niche forest products. However, it is key that descriptions on how the product was superiorly grown and managed, along with social benefits for the community and labour force are required for the full brand story to resonate with customers.

The rating for this credence attribute (‘pesticide-free’) in the survey was rather low. This indicates that not much attention is given on this detail in the broad market, and this topic is rather believed to be important only for a niche market by the survey participants.

Furthermore, credence attributes play an important role in manufactured products and their promotion. The specific marketing is dependent on industry, sector, and product and various labels exist. Carbon footprint, chemical-free production, renewable packaging, or renewable materials were most frequently mentioned by the experts we interviewed. Renewable materials are observed to be very important for packaging. Many packaging companies promote that their packaging products are recycled or renewable, especially in e-commerce markets. It has become common to see FSC, PEFC, or other logos (e.g., Rainforest Alliance’s frog) on packaging in all of Asia, Europe, and the US. In addition, carbon footprint is considered important in that area and is expected to increase in prominence.

Generally, a lot of momentum is currently perceived on developing renewable bio-products, sustainable innovation and circular (bio)-economy. Companies such as Stora Enso or Lenzing are perceived as leading global providers of renewable solutions in biomaterials and packaging or in the production of cellulose fibres for producing textiles or medical applications respectively.

3.1. Claims of Credence Attributes of Forest Products—Promotional Opportunity or Simply Meeting Requirements?

Claims about credence attributes are quite common for forest products. According to the Delphi experts we interviewed, these range from environmental (e.g., biodiversity, water footprint, ecosystem services provision, sustainably managed, etc.) to social (access for recreation, gathering food, community engagement, harvesting safely, etc.) and legal aspects (forest legality, certification). Promotion adjectives around forest products include terms such as ‘certified’, ‘sustainable’, ‘renewable’, or ‘natural’. However, in contrast to many agricultural products, the claims made are not always product-specific and sometimes rather about the forest company or industry, its values, and that they adhere to certain principles. Certification was believed to be a very important factor for claims on environmental, social, and legal aspects of how the product is grown in the forest. Apart from the certification bodies and single companies, there is also evidence of forest-sector marketing using credence claims. The American Wood Council or the Softwood Lumber Board try to improve the market share of wood in construction by highlighting the ESG benefits of the forest growing cycle. Similar interest groups are known in Europe as well.

However, some experts we interviewed argued that making credence-based claims, e.g., about certification, is less promotional than rather about meeting standards regarding ESG or for continued market access of timber products, e.g., for big box stores.

For institutional investors, such as pension plans, superannuation funds, but also insurance companies, listed companies (Weyerhaeuser, Rayonier) or other timber investment management corporations (TIMOs), there is rising pressure to demonstrate sustainable management and good stewardship of their assets. These aspects are also expected to become more important to forest investors. The websites, reports, and declarations of many companies inform about their ESG activities.

3.2. Environmental Aspects

The claims around environmental attributes are generally about sustainable management and production as well as water conservation. Most companies use the ESG criteria for reporting on these aspects (see

Table 2). Energy consumption is a very recent feature to report on, in addition to the more ‘standard’ attributes and benefits of forests. In particular, the pulp and paper sector emphasises its environmental measures in many countries.

The feature of chemical-free production, which some companies in Asia promote their products with, can be related to environmental as well as social aspects. However, the health feature of this production aspect obviously dominates the concerns over the environmental considerations. The environmental certification and chemical-free pressures for wood products came primarily from EU and Japan, over the past 25–30 years, but our study found a greater emphasis from the Delphi consultants on the importance of chemical-free products now coming from the Americas, whereas health was mentioned mostly by EU nations and particularly Asian respondents.

The origin of the wood is sometimes promoted. Where on the one hand the tendency to promote around ‘local’ is evident (USA, Austria, Germany), others associate a country with high standards in general as a positive attribute regarding the origin.

3.3. Social Aspects

Most of the actions on social aspects mentioned by the Delphi experts we interviewed were around the support of rural or indigenous or local communities. In general, forest owners are also typically promoting the recreational access/access to nature and the public benefit they provide, rather than a product-specific focus.

Another central feature perceived by the experts is the employment of people along the value chain (and in rural areas). Some countries with a strong focus on the primary sector also have a close connection of forestry to agriculture, and hence forestry is linked to food supply, as many farmers also manage some forests. Worker safety and employment rights are also covered by CSR reporting. In addition, some experts observed companies promoting social benefits created for their own staff and workers.

3.4. Legal Aspects

Legal aspects are mostly regarded as standard business practice, and they are less able to be used as a marketing instrument. Timber legality is today taken for granted in many trade markets, and promotion on that would seem odd and suspicious to some experts. However, marketing of ‘legal’ timber is common in the DIY sector, but these promotions mostly refer to certification schemes (PEFC, FSC, SFI (Sustainable Forest Initiative), ATFS (American Tree Farm System), COC-certification) as ‘certified’ wood from legal sources.

3.5. Credence Attributes Compared to Criteria and Indicators of Sustainable Forest Management

Initiatives to ensure and promote sustainable forest management exist on different levels and from different perspectives. Frameworks such as the Montreal Process describe, monitor, assess, and report on national forest trends and progress toward sustainable forest management [

48]. The criteria and indicators of such a framework reflect a holistic approach to forests as ecosystems and address a range of forest values. These frameworks can reflect quantitative and qualitative changes over time and thus give an indication of the sustainability of forest management. Some of the requirements cannot be applied to individual forest stands and shall rather be considered on a larger scale. An important dimension of SFM is the scale at which it is applied—from global or national, to landscape level, or even to forest management unit. While different scales exist, they still can depend on and inform each other. The perspectives on SFM also differ between buyers of forest products and markets, forest companies, or investors.

Table 3 compares how far credence attributes mentioned in this paper are already covered in the criteria and indicators (C & I) of sustainable forest management frameworks, as well as in the principles (FSC) and standards (PEFC) of the main certification schemes. The C & I of the Montreal Process [

48], Forest Europe [

49], and the International Tropical Timber Organisation [

50] were searched for the respective topics of the credence indicators. In addition, the standards and principles from PEFC [

22] and FSC [

21] have also been checked for these credence attributes. The respective numbers of the C & I, principles and standards have been included in the table if a relation to the respective credence attributes could be found.

While there is a different perspective between forest products versus forest management, credence attributes can still give some indications and inform forest management about present or potentially future market expectations. On the one hand, most of the credence attributes in relation to social and environmental aspects are covered by all or some of the C & I of the frameworks and certification schemes—albeit on different scales. On the other hand, several of the more trade related credence attributes are not covered by the frameworks and schemes or just to a very limited extent. The ‘pesticide free/health of forest products’ credence attribute, for example, is best covered by PEFC, which has requirements for PEFC—accredited companies on the use, documentation, pesticide classes, bans, and instructions of pesticides [

22]. Some of the credence attributes, such as health attributes or fibre miles, extend beyond the standards of SFM but will add additional value for trading forest products.

Furthermore,

Table 3 highlights the supply versus demand tension that comes through in the differences in the word cloud, where quality, price, and legality are most important; while ESGs are working constraints to operate and access markets, encapsulated by legality.

3.6. Forest Sector Reporting of CSR and ESG

There is a growing consumer expectation and demand for information and transparency provisions in relation to production processes and practices [

51,

52]. Thus, most of our experts believe that reporting on credence attributes is important and will further increase in the future. This kind of reporting is sometimes described as corporate social responsibility or a ‘CSR report’, ‘responsibility report’, or more frequently as ‘sustainability’ or ‘environmental and social goals’, or an ‘ESG report’, depending on emphasis, period, and ‘fashion’. The trend and development of reporting has changed over the years. Currently, some experts see a trend that businesses are renaming their annual report as a sustainability report or transitioning to ‘green’ reporting. Reporting on natural and social capital aims to create attention and better interaction with nature and to a better prosperity and well-being of people, compared to the view of capital as just a monetary aspect [

53,

54].

These standards of reporting have grown in importance over the years, especially regarding forest investment. They are key for plantation forestry enterprises as their institutional investors want to ensure good stewardship of their assets and credence in their management.

Initiatives such as the Natural Capital Protocol or the Social & Human Capital Protocol are designed to help generate trusted and credible information to support better decision-making of companies, including how they interact with nature and social and human aspects [

53,

54]. The advantage of using such tools is that they can provide a standardized framework. The difficulty of finding measurable indicators for non-monetary value is mitigated by this approach which was one concern of our experts.

Our interviewed experts expect that reporting will increase in regard to climate change (carbon sequestration/carbon sinks, use of forest products to replace fossil fuels), ecosystem services (drinking water, wildlife conservation), and environmentally friendly practices such as green supply chains, but also towards social responsibility for society (e.g., job creation (in rural areas), safety, wages, welfare of employees, more inclusive forest management practices on a landscape level). Reporting is established almost everywhere in the world and is mandatory in many countries for certain companies. It is also considered important for maintaining social licence to operate, which means an ongoing acceptance or approval of operations by local community stakeholders, consumers, and the general population who are affected.

Experience from our experts shows that reporting is common for TIMOs (timber investment management operations) or REITs (real estate investment trusts) but also applies to timber associations (forest owners), third-party certification agencies, and other forestry companies/forest managers elsewhere. The general trend and willingness to join, especially in green initiatives, is perceived by many experts.

Transparency is therefore deemed a key feature in reporting. However, the ability to report on certain criteria can sometimes be difficult and the question remains as to what data companies use and how reliable it is. Features that can easily be measured, such as harvested timber, can be shown in a report without difficulty. The quantification or metrification of social impacts, for instance, is more complicated sometimes and it is likely to stay on an abstract level with positive examples. This involves an inherent risk that CSR reporting is tending towards a “greenwashing” track with lots of promotion and positive PR including SDG, ESG, or other desired goals, but with less facts behind the surface. The system is currently perceived to be driven that way. Therefore, some of our experts believe that it is even more paramount to ensure credibility in the whole system and criteria based on hard facts and audits from certification bodies. Practical implementation as well as long-term sustainability and credibility are key for the credibility of companies or certification bodies.

Last, a different level of reporting is anticipated in the future by our experts. For example, the cradle-to-cradle is comprehensive across the value chain. It is believed that this is best implemented at the holistic level, especially in carbon reporting. Producers are deemed to have little influence here compared to the rest of the value chain. Marketing the story of long-term stored carbon (e.g., in buildings) is believed to be crucial.

3.7. Importance of Credence Attributes through the Lens of ESG

Many countries decided to follow a strong pathway with reduced carbon emissions and a more sustainable development, particularly after the outbreak of COVID-19. To date, 137 countries have committed to carbon neutrality confirmed by pledges to the Carbon Neutrality Coalition and recent policy statements by governments, and six of them have passed their carbon neutral targets into law (Sweden, Denmark, France, Hungary, New Zealand, and the UK) [

55]. The majority of the countries’ zero-carbon goals are set to the year 2050, including the EU, USA, the UK, and New Zealand [

55,

56,

57]. Carbon neutrality can thus be considered as one of the key future trends, which was confirmed by our experts’ opinion. Therefore, sustainable investing is gathering momentum across the investment universe.

Currently, the EU plans to introduce a system for classifying green investments, which is particularly relevant for asset management firms [

57]. In addition, Brussels will introduce an eco-label for retail financial products to allow consumers to easily see whether products marketed to them as green are sustainable. This label is very likely to include—among others—forestry products as well [

57]. This development is expected to increase the allocation of assets to ESG further and thus increase the importance of credence attributes. Considering the growing demand of wood for a clean and low carbon future forestry will be a prosperous asset to a diversified investment portfolio [

57].

The environmental values of planted forests will have an increasingly important influence on opportunities to access value-added markets and the ability to attract investment from the global financial sector [

58]. Several studies show that forest management should include a stronger emphasis on other sustainability values around ecosystem services and social issues to optimise forest values [

59,

60,

61], and credence attributes can be used to highlight these.

3.8. ESG Criteria, Credence Attributes, and Environmental Labelling in the Investment Space

The financial sector is integrating climate into its business models and demands climate-related information. Thus, ESG criteria have received greater attention in the investment space over recent years and ESG factors have become an important investment criterion for shareholders and investment firms [

62]. While several years ago sustainable investing was considered a small niche and with limitations on financial performance there is now continuing prevalence of sustainable investment across the global investment industry, with assets under management reaching USD 35.3 trillion and a growth of 15% in two years [

63]. The most common sustainable investment strategy outlined in this report is the integration of ESG. KPMG has reported on the rise of ESG in the hedge fund industry and the rise of sustainable investing [

64]. They described that the biggest drivers of ESG investing are institutional investors. The UK pension plan, for example, requires companies to use the reporting framework of the Task Force on Climate-related Financial Disclosures, with a strong focus on carbon footprint and the actions taken to reduce it—credence attributes that are expected to grow in prominence by our experts.

Today, people who like to invest and at the same time have a good feeling about their investments (dubbed alternative ESG investors) have a great choice of options, and almost all big investment companies or big distributers of Exchange Traded Funds (ETF) such as Black Rock (iShares), UBS, Vanguard, Amundi, Fidelity, etc., offer funds that include ESG criteria. Even direct investments in the global forestry sector are possible with special sector ETFs, such as the Global Timber and Forestry ETF [

65], or alternatively with direct investments in listed forest companies such as Weyerhaeuser, Manulife, or Stora Enso.

On top of that, the next step of responsible money investment is called “impact investing”. People following this strategy invest their money explicitly with the aim to have a demonstrable positive impact on environment and society [

66,

67]. Many opportunities exist for impact investment options and even pension plans such as the New Zealand Kiwisaver offer an impact investment option with “hand-picked investments in businesses that are actively building a better future for the world” [

68]. This clearly shows the potential value of credence attributes.

Performance of companies with credence values have also been discussed in the investment space for a long time. An exhaustive review of more than 2200 primary studies shows that the relation between ESG criteria and corporate financial performance (CFP) is positive [

69]. Outperformance opportunities of ESG investments exist in many areas of the market and the positive ESG impact on CFP appears stable over time. Friede et al. [

69] conclude that the orientation toward long-term responsible investing should be important for all kinds of rational investors in order to fulfil their fiduciary duties and may better align investors’ interests with the broader objectives of society.

In addition, certain labels or certification schemes signal environmental and health information on products throughout their life cycle to consumers and other stakeholders, but it can also have a significant impact on a companies’ performance in general. For example, manufacturing firms significantly increased their financial performance and productivity after obtaining environmental labelling certifications [

70]. These positive effects from the empirical evidence from China are attributed to both the labelling effect and the technical factor. The better performance was mainly a result of price premiums rather than increased market share.

Credence is an extremely critical value in the investment area. Shareholders invest in a company based on the belief that they will run their operations responsibly and effectively over the long term. If investors lose confidence, this usually has dramatic effects for the company and can lead to severe loss of market value (i.e., share price) or even to bankruptcy. However, quantification of the environmental benefits, credence attributes, or ESG aspects is not without its problems. While commodities require standardized measures, ecosystem service commodities are at best described by indicators of their complex ecological functions [

71]. That results in vague definitions in the ESG criteria and can lead to doubts on the sustainable background of claims or greenwashing allegations, which recently sparked fears across the wider investment industry [

72]. The analysis of single credence attributes can help understand and define these criteria better and improve authenticity and transparency. In addition, the rising demand for sustainable investment products has created a variety of products, and thus comparability is believed to be an even greater problem than greenwashing [

73]. Understanding of credence attributes, comparability, and standardization need to be improved to facilitate more efficient capital allocation in ESG funds [

73].

3.9. Credence Attributes Deemed of High Importance for the Future by Our Experts

Considering the growing importance of credence attributes over the globe, the question of which attributes will particularly increase in prominence in the forestry sector in the future is emerging. The outlook on credence attributes from our experts’ view provides estimates around which credence attributes might grow most in prominence. Environmental factors were generally regarded to increase in relevance the most. Most important in many of the experts’ views was the attribute of ‘deforestation-free/zero deforestation’ assurance that wood products are not responsible for forest losses in different countries.

In addition, the topic of climate change was frequently mentioned, as well as how forests are managed to mitigate the effects of climate change. Closely connected to this aspect was carbon sequestration and climate neutrality. Our experts believe that the public awareness of the environment and green consumption is increasing due to global warming. Because of increasing pressure from consumers to respond to climate change, governments and, by extension, industries are expected to meet targets under the Paris Agreement. Forests make excellent carbon sinks, and especially high-quality timber products that store carbon for much longer than low-quality products that end up being burned after use. This will encourage carbon-friendly product claims and possibly increased local sourcing or at least stating a known origin of the wood products’ sourcing.

Traceability and transparency of forest products were other important factors identified by the experts—this relates to the beforementioned ESG challenges of greenwashing and comparability. This is not only important from a local sourcing perspective (fibre miles and CO2-footprint), but also from the legal side about wood source legitimacy and environmental requirements from different countries (general commitment to sustainability). Being able to show where trees grew, and who was involved in the harvesting, milling, and transportation would put a human touch to the value chain. This could be a possible advantage for isolated countries such as Australia or NZ, as they can quite easily ascertain the origin of the wood product (at least from the country perspective) compared to Europe with a lot of countries and small scales, where diverse product flows are much more difficult to trace (timber, seeds, etc.).

Ecosystem services (ES) in general and particularly around water quality, nitrogen release/reduction, soil (erosion control), biodiversity, and conservation of native species are also expected to increase in importance over the next five to ten years.

Finally, forest management standards and credibility, often represented by certification of SFM are expected to grow. However, additionally, ‘brand names’ of sustainably produced forest products are expected to become more important.

A connection between environmental aspects and social attributes is the use of pesticides or chemical application in forest management. On the one hand, this is seen as an impact on the environment; on the other hand, it is also related to people’s health. Both the intact environment and healthy forest products are related to the human desire towards a healthy (and better) life. Therefore, many customers, especially in the Asian countries, prefer healthy products in their built environment.

Other social aspects, such as social justice, or employment issues, such as quality of work or safety at work, might become more important in some countries. This includes cultural aspects around forest management, as well as Indigenous people and the traditional use of wood species.

4. Conclusions

Credence attributes, although not widely recognised in this terminology in the forestry sector, already play an important role in the forestry sector for timber forest products as well as for NTFP. Many are bundled into certification scheme aspects, or encompassed within a wider ‘SFM’ claim.

Some credence attributes, such as the legality of forest products, form the basis of trade and certification and are almost taken for granted in the business environment. Other attributes, such as fibre miles or carbon footprint, are of varying importance in different parts of the world, but carbon footprint is believed to increase in prominence in manufactured forest products.

This study revealed the potential value of some less frequently focused-on attributes, including the health aspects of forest products. These are of growing interest for NTFP as well as for timber products in the built environment, as they are related to the human desire to live a healthy lifestyle individually, and at the same time caring about nature and acting in an environmentally-friendly way. Promoting this attribute of a forest pro-duct can result in additional value of the product and furthermore establish or enlarge a potential market. Given the rise of middle-class households in several countries including the Asian market, which can afford to buy ‘healthy’ products, and the high awareness of health aspects, this could develop into a promising niche market for some forest products. Producers of forest products could change or improve some business practices to diversify their potential market, get access to new markets, or potentially get paid price premiums.

Our research highlights areas where present SFM frameworks are currently disclosing some credence aspects, such as country of origin labelling, verification of chemical potency claims, and amount of packaging waste created, but only to a limited extent for customers and the market.

Through understanding the strengths and importance to key markets of these credence attributes in relation to SFM, sustainable forest management frameworks and certification schemes can be improved to more pertinently address and validate claims made by forest producers. Schemes can also then quickly provide a line of sight to customers seeking verification concerning more pertinent individual attributes than an overarching certification stamp or SFM assurance. This study suggests that there is scope for improvement in relation to legal, political, and trade-related certification and monitoring frameworks within the forest sector, to better account for individual credence attributes of growing importance to international markets.

At the same time, consumer demand for information and transparency provisions in relation to production processes and practices is growing. Associated with this, it is expected that ESG and credence attributes will grow in prominence over the next years. This is an increasingly important factor for companies and in the investment space. Credence factors also could be incorporated into the ESG and Green Index metrics that are offered by various international investment advisory firms. Since several big forest companies act on behalf of international investors, such as in pension plans, or are listed companies, the forestry sector will be affected by this increased demand for sustainable, ecological, and social management and reporting. This would be particularly important for TIMOs and in continued investment for plantation forest management. In addition to financial capital, nature capital as well as social and human capital will play an increasingly important role for companies, and understanding the role of credence attributes can help to manage these more effectively.

This study explored the role of credence attributes in forestry in general and identified the most relevant credence attributes and their importance to forest and trade experts. This information can be used to inform work on forest frameworks, especially on C & I and on the standards and principles of certification schemes. The understanding of these attributes can be used to prepare for current and future market expectations and to facilitate the further development of SFM.

{kind=link}

{kind=link}

{kind=link}