1. Introduction

Over the last ten years, global carbon dioxide (CO

2) emissions have increased from 25,688 million metric tons in 2003 to 36,310 million metric tons in 2021 [

1]. Simultaneously, non-CO

2 emissions grew by approximately 20% between 2005 and 2020 worldwide, from 10,506 million metric tons of CO

2 equivalent to 12.619 million metric tons of CO

2, respectively, which could remarkably affect the internal equilibrium process of worldwide ecosystems [

2]. In this respect, investments in renewable energy have been made in order to mitigate climate problems [

3]. Thus, an analysis of the impacts of greenhouse gas (GHG) emissions, both CO

2 and non-CO

2, on the share of clean energy investment is of great importance.

GHG emissions have increased continuously because of human activity and non-renewable energy combustion [

2] and have created potential hazards for natural systems [

4]. Extreme weather, for example, caused nearly 80% of the large-scale power blackouts from 2003 to 2012 [

5], ranging from USD 20 to USD 55 billion per year in the United States [

6]. Moreover, disasters induced by GHG emissions influence various areas such as resource management, economic improvement, and population growth [

7]. Some unforeseen risks may also affect environmental quality and energy consumption [

8,

9,

10], the fluctuations and functioning of the energy market [

10,

11,

12,

13,

14,

15,

16,

17,

18,

19], the stock market [

13,

20,

21,

22,

23], the world trade network [

24], and unemployment and recession [

25,

26,

27,

28]. Consequently, policymakers tend to reduce environmental damage through the development of renewable energy [

29].

Potentially 90% of global warming was caused by anthropogenic GHG emissions in 2007, according to the Intergovernmental Panel on Climate Change [

30]. According to the World Bank [

31] and Environmental Protection Agency [

32],

Figure 1 shows the contribution of CO

2 and other GHG emissions in the world in 2021. Two-thirds of the GHG emissions are related to carbon dioxide (CO

2) [

33,

34], the most outstanding gas in the atmosphere [

35]. CO

2 emissions are only emitted from the burning of fossil fuels (i.e., crude oil, coal, natural gas, and petroleum products) [

36]. Meanwhile, among other GHGs, nitrogen oxide (N

2O), methane (CH

4), water vapor (H

2O), and F-gases are the greatest and longest-lasting on earth [

35]. They are released from numerous sources, including the combustion of non-renewable energies, the processing and usage of chemicals, land use modifications, manufacturing processes, and livestock capital [

37]. Both CO

2 and non-CO

2 GHG emissions are legally responsible for climate change policies in many countries around the world. Modelers can make plans to include CO

2 emissions, non-CO

2 emissions, or both in their models. However, non-CO

2 greenhouse gas emissions are rarely considered sufficiently, which may lead to misleading results in implementing the best climate change policies [

38] and differential impacts of policies in some countries depending on how non-CO

2 GHG emissions are taken into consideration [

39]. The effect of wind investment on lowering CO

2 emissions, for example, has not been proven to be positive when excluding non-CO

2 emissions [

40]. Therefore, this paper focuses on the impacts of CO

2 and non-CO

2 GHG emissions on renewable energy investment.

The advantages of clean energy, such as fewer emissions and lower energy input requirements [

41,

42] are reflected in renewable energy investment dramatically all over the world. It is also expected to be the fastest growing energy source between now and 2030 [

43]. Based on a

Bloomberg New Energy Finance report [

44],

Figure 2 exhibits the total clean energy investment between 2004 and 2021 across the globe. From 2008 onward, clean energy investment became more essential, most probably because of climate change and its different levels of environmental losses [

45]. The total investment in clean energy accounted for USD 543 billion in 2010, reaching USD 755 billion in 2021 (almost a 40% increase). Since global trends indicate that the use of solar, wind, and geothermal energy is effective in avoiding GHG emissions [

46], determining the effects of GHG emissions on renewable energy investment has become an important issue. When discussing the impacts of CO

2 and other GHGs on renewable energy investment, GHGs are the reason for global warming. The greater the GHG emissions, the greater the environmental protection awareness internationally, leading to an increase in clean energy consumption [

39].

According to the recent trend in renewable energy investment and GHG emissions, several questions arise from this article:

Are there differences in the effects of CO2 and non-CO2 GHG emissions on clean energy investment between different kinds of clean energy?;

Do floods, which are becoming more frequent in many countries because of climate change, impact solar, wind, and geothermal energy investment similarly?;

Do countries with greater and lesser CO2 and non-CO2 GHG emissions respond similarly to solar, wind, and geothermal investment?

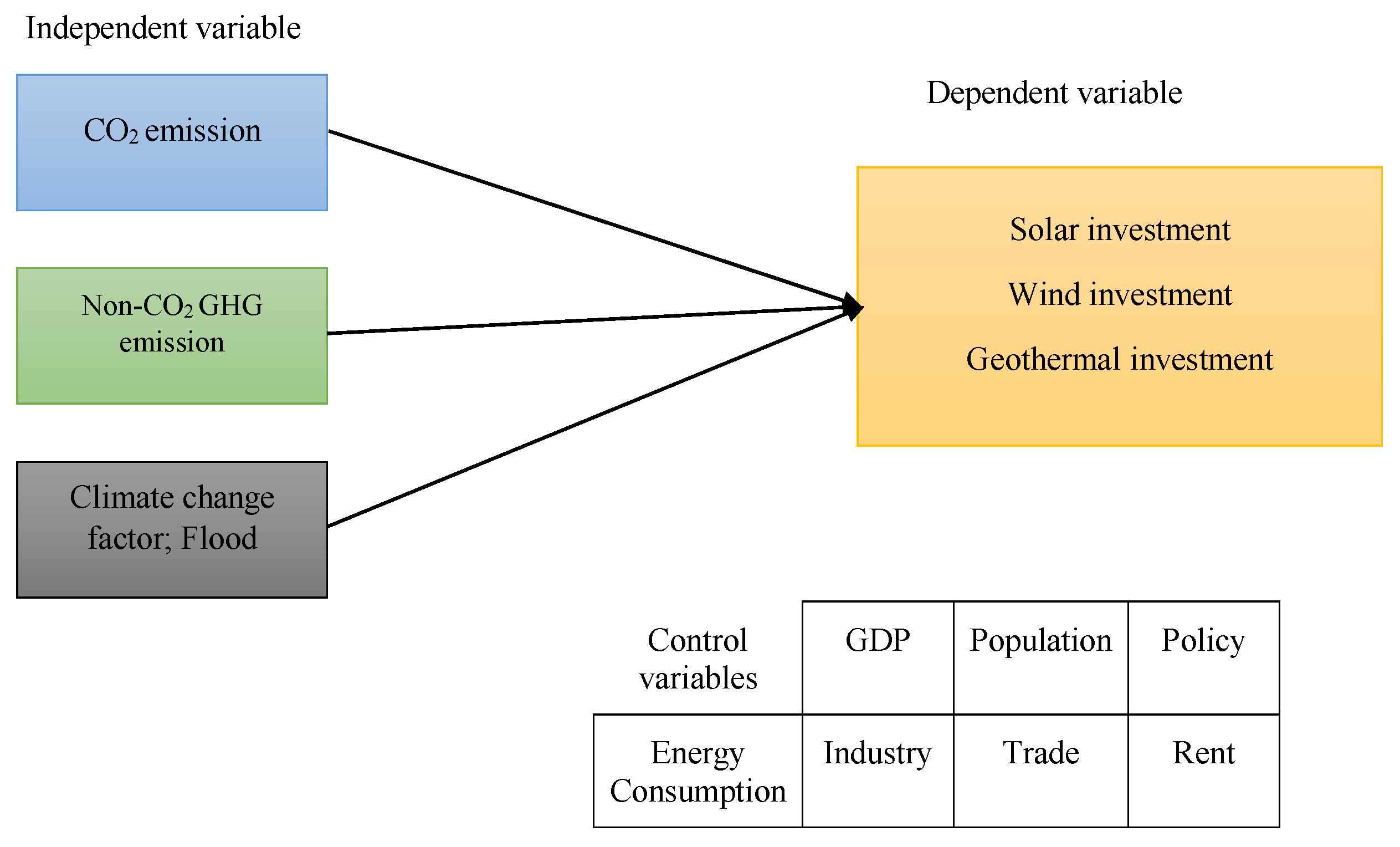

Herein, we utilized the panel data regression model involving 63 countries and using annual data from 1990 to 2021 to provide reliable and reasonable answers to the questions above. The panel regression technique has been commonly used in many fields of energy economics [

47,

48,

49,

50,

51]. The empirical analysis involved the estimation of random effects models, whereas the Hausman test was employed for selecting the appropriate panel model and was found to be significant at

p ≤ 0.10. A collinearity test was applied to examine the linear function of independent variables compared to other variables. A normality test and correlation test are also considered to investigate the relationship between variables. The biggest advantage of the panel data regression approach is that it comes with a panel dataset that includes numerous observations of several individuals over a long period of time [

49,

50], thereby revealing a range of differences in the analysis of CO

2 and non-CO

2 GHG emissions impacts on renewable energy investment. As a result, the use of a panel data regression method is particularly necessary for this paper because the impacts of non-CO

2 and CO

2 GHG emissions on renewable energy investment may differ in different countries and different energy sectors such as wind, solar, and geothermal energies. The existing research shows that many publications have suggested that only CO

2 emissions should be considered when studying the impact of greenhouse gas (GHG) emissions on renewable energy investment. However, this study considers both CO

2 and non-CO

2 GHG emissions and demonstrates that the results vary significantly when non-CO

2 emissions are included. Therefore, this paper addresses the gap in knowledge regarding the influence of different types of GHG emissions on a clean energy investment.

This paper is structured as follows:

Section 2 briefly summarizes the related literature and the trends of CO

2 and non-CO

2 GHG emissions, as well as solar, wind, and geothermal investments, which are especially discussed. Data sources and variables are interpreted, and the details of the econometric methodology are provided in

Section 3. In

Section 4, the empirical results are explained. Finally, the paper is concluded in

Section 5 and provides corresponding policy implications.

2. Literature Review

After the 1980s, which coincided with industrial development, CO

2 emissions have been accelerated, and non-CO

2 GHG emissions continue to grow in both developing and developed countries [

52].

Figure 3 compares the average CO

2 and non-CO

2 emissions between 1990 and 2021, according to the World Bank [

31]. As can be seen from the figure, countries with a large population (e.g., India and China) have greater CO

2 emissions, whereas countries such as Brazil, Indonesia, Australia, Qatar, the Philippines, Bangladesh, Mexico, and Vietnam reported a share of 40–90% non-CO

2 emissions in 2021. This indicates that non-CO

2 GHG emissions have risen, probably because of less coal usage and higher renewable energy investment [

53]. As large amounts of greenhouse gas emissions have influenced economic [

2,

13,

54,

55], energy [

56,

57], and environmental issues [

58,

59], modelers can develop plans for different climate change policies [

39], depending on which types of GHG emissions are used.

A large number of studies addressed only CO

2 emissions, such as [

60,

61,

62,

63]. However, overlooking non-CO

2 GHG emissions may result in misleading impacts and false results. Studies from China, for instance, focus on CO

2 emission levels, and data are published with different selection processes. For example, the authors of [

38] showed that the impacts of climate change policy differ with and without non-CO

2 GHG emissions. They discovered that, without non-CO

2 GHG emissions, China experiences a large volume reduction in real GDP. Other previous studies [

64,

65,

66,

67] also estimated that cost savings, for example, can reach up to 70% when additional gases are included. Some studies only examined various gases, such as CO

2, CH

4, and N

2O in [

66] and CO

2 and CH

4 in [

65,

68]. Many reviewed all GHG emissions, including [

38,

64,

68,

69,

70,

71,

72]. This paper focused on both CO

2 and non-CO

2 GHG emissions to provide more accurate impacts of GHG emissions. The main objective of this paper is to examine how CO

2 emissions and other GHG emissions impact renewable energy investment.

Since renewable energy usage is considered an efficient plan to overcome GHG emission problems [

73,

74,

75], many researchers have accomplished research on their relationships. For instance, [

45,

76,

77,

78] emphasize that CO

2 emissions positively contribute to the consumption of renewable energy. Another study [

79] came to a similar conclusion through the implementation of solar energy to minimize SO

2, NOx, and CO

2 GHG emissions. Meanwhile, some scientists [

40,

42] thought that the effects of GHG emissions on wind investment were ambiguous. One possible reason is that they considered only CO

2 emissions in their calculations. In comparison, others discovered a positive relationship between wind investment and CO

2 emissions [

80]. According to [

37,

81,

82,

83], GHG emissions also responded positively to geothermal energy investment and other variable energy. Therefore, in the analysis of how CO

2 and non-CO

2 GHG emissions impact clean energy investment, the main idea is that GHG effects and climate change consequences such as flooding are conducive to such investment [

84].

Investment in renewable energy has been followed in many countries, including Australia [

71], South Korea [

38], the European Union [

85], New Zealand [

86], China [

87], Croatia [

88], Poland [

89], and other regions [

90]. Based on IEA reports [

43],

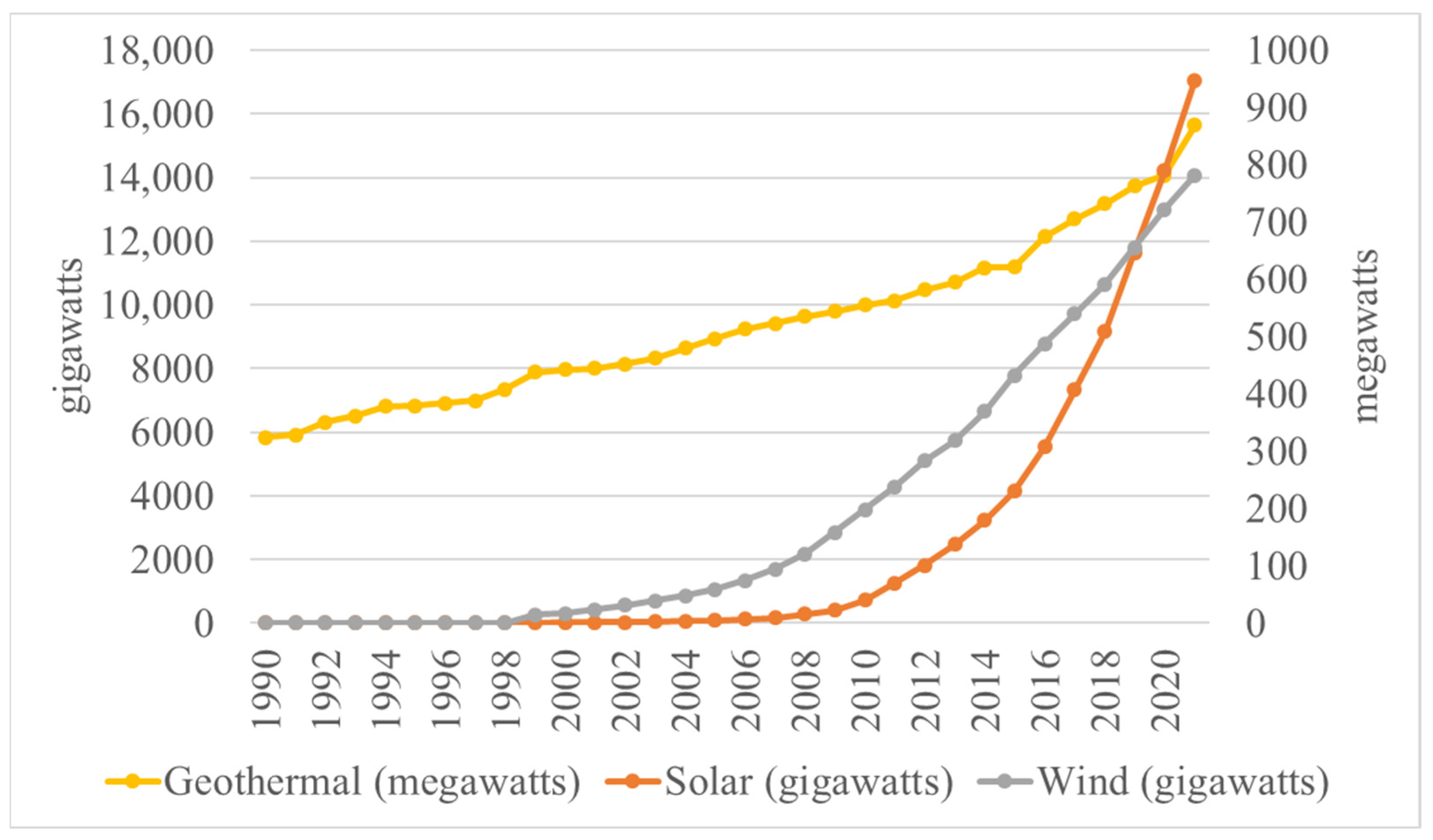

Figure 4 illustrates the installed capacities of wind, solar, and geothermal energy between 1990 and 2021 on a globe scale. According to International Energy Agency reports, renewable energy investment has increased dramatically and is expected to be the fastest growing energy resource from now until 2030. From the datapoint in REN21 [

91], a record value of USD 71 billion was invested in solar photovoltaic and wind power, where the share of geothermal and other renewable energy was 4.8% in the United States, 6% in France, 3.2% in Japan, and 16%, 6.5%, 1.7%, and 5.6%, respectively, in Canada, Italy, the United Kingdom, and Germany. By that time, nearly 500 GW had been invested in solar and wind, whereas the installed capacities for geothermal energy were lower at about 15 GW globally in 2018.

The mitigation of CO

2 emissions through renewable energy investment is well accepted by some researchers. For instance, in some previous studies [

75,

92,

93,

94,

95], it was assumed that the share of clean energy could play an important role in making good decisions in energy policy. Meanwhile, [

53], consistent with [

96], surveyed the correlation between carbon dioxide emissions and clean energy use and suggested that clean energy is productive in dealing with GHG emissions. However, there has been no study in the literature on whether the effect of non-CO

2 GHG emissions on clean energy investment is influenced by clean energy development.

From the existing literature, we found that many recent publications advocated only CO2 emission levels to study how GHG emissions affect renewable energy investment. Here, the present study focuses on both CO2 and non-CO2 GHG emissions, with the results diverging when non-CO2 emission levels were included. In this context, this paper fills the gap on how different types of GHG emissions influence clean energy investment separately.

5. Conclusions and Policy Suggestions

5.1. Conclusions

This study examined the effect of CO2 and non-CO2 emissions on clean energy investments using the panel data regression technique with random effects across 63 countries from 1990 to 2021. This paper also studied whether countries with greater and lower renewable energy investments respond similarly to GHG emission effects. Therefore, the panel data model was applied to the parameter results for countries with large and low carbon dioxide emissions. We investigated the influence of CO2 and non-CO2 GHG emissions on three types of energy (mainly solar, wind, and geothermal). In this study, we also tried to answer some questions as follows: (1) do countries with greater and lesser CO2 and non-CO2 GHG emissions respond similarly to clean energy investments? (2) are there differences in the effects of CO2 and other GHG emissions on clean energy investments between different kinds of clean energy? (3) do the effects of CO2 and non-CO2 emissions on clean energy investments exhibit heterogeneity between different regions? and (4) does Flood as a representative of climate change that shows extreme temperatures, have a positive impact on renewable energy investment? To provide reasonable answers to these questions, the panel data regression model with random effects was used. According to the empirical results, we arrived at various main conclusions. We found that CO2 emissions have a positive effect on solar, wind, and geothermal investments in all countries. In fact, the amount of CO2 emissions is considered a pattern for investing in three types of energy across the globe. The reason may be that the CO2 emission dataset is released directly by official sources, while for choosing the best policy to reduce GHG emissions, non-CO2 emissions are of great significance, as excluding non-CO2 GHG emissions may lead to misleading results.

Non-CO2 GHG emissions had negative impacts on solar and geothermal energy investments. The effects of these emissions on wind energy differed across countries. The average CO2 emissions are accounted for to divide countries into two groups. The first group included countries with low carbon dioxide emissions, and the second group comprised regions with huge amounts of carbon emissions. The estimation results indicated that non-CO2 GHG emissions did not impact solar, wind, and geothermal investments in more polluted countries compared with those in less polluted regions. Meanwhile, the relationship between wind energy and geothermal investments and non-CO2 GHG emissions was positive in the second group of countries. The reason may be that non-CO2 emissions were the cause of pollutants in these types of countries.

Regarding the climate change variable Flood, there was uncertainty about how it could increase renewable energy investments. The relationship between Flood and solar, and geothermal energy was negative, but positive for wind investments. A review of the related literature also approved the same results. When it comes to controlling variables, Energy consumption, Industry level, and Policy all had positive impacts on the three types of clean energy.

We also found that for countries that experience high levels of environmental pollution or CO2 emission levels, Flood and CO2 emission levels are the most important factors in deciding whether to invest in solar, wind, or geothermal energy. Development growth is an effective way to increase wind power investment, which is supported by the literature. Trade was also investigated as an effective method of increasing solar and geothermal investments in less polluted countries.

5.2. Policy Suggestions

According to the empirical results of this study, some policy recommendations and suggestions to improve environmental quality through clean energy investments can be drawn as follows.

First, the results show that non-CO2 GHG emissions have a significant positive correlation with decreasing solar energy investments in less polluted countries. This suggest that such regions should focus more on clean energy, given that the main source of pollution in these countries is comprised of non-CO2 GHG emissions. As policy has a positive effect on renewable energy investment, authorities can apply effective energy policies, such as subsidies, to encourage countries to invest in renewable energy investments.

Moreover, non-CO2 emissions had positive effects on wind and geothermal investments in less polluted countries. Thus, governments should continue to implement policies on clean energy and encourage investors to conduct differentiated clean energy plans based on the different environments of countries.

Furthermore, from an economic perspective, a higher portion of economic growth is deemed beneficial for lowering CO2 emissions in less polluted countries through greater investments in wind power. Hence, developed nations should expand clean energy equipment to achieve CO2 emission reductions.

Finally, all countries should pay more attention to the positive relationship between CO2 emissions and clean energy investment and the negative relationship between non-CO2 GHG emissions and clean energy. Although CO2 emissions are considered agents determining the amounts of investments in renewable energy, we found that non-CO2 emissions are of great importance. The least polluted nations may enjoy lower carbon emissions by reducing the scale of import trades, whereas the most polluted nations should expand their energy policies. This may aid policymakers in achieving more environmentally friendly economic decisions. It seems that reaching the substantial investment levels needed to successfully manage the transition into a renewable energy future in less polluted regions is a topic worthy of discussion. In this respect, energy policies can help them reach greenhouse gas emission reduction goals.

The research only focused on the influence of CO2 and non-CO2 emissions on three specific forms of clean energy, namely solar, wind, and geothermal. It did not take other types of clean energy, like hydropower and bioenergy, into account. In upcoming studies, the effects of emissions from these other types of clean energy could be explored. Additionally, the study did not examine how technological advancements impact investments in clean energy. Future research could investigate this relationship. Additionally, socio-economic factors such as education, income, and population growth were not considered in the study. Including these factors in future research could provide a more comprehensive analysis of the factors that determine investments in clean energy. In forthcoming studies, we intend to employ advanced machine learning techniques to examine the intricate relationship between climate change variables and the progress towards renewable energy adoption.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}