3.1. Assessment of Capabilities of Development of the Iraqi Oil and Gas Industry

The current state of the Iraqi gas industry is characterized by the following trends [

5,

17,

18]:

Iraq consumes 93,344 million cubic feet of natural gas per year, as of 2017.

Iraq ranks 92nd in the world in natural gas consumption, accounting for about 0.1% of the total world consumption of 132,290,211 million cubic feet.

Iraq consumes 2486 cubic feet of natural gas per capita per year (with a population of 37,552,781 in 2017), or 7 cubic feet per capita per day.

Iraq produces 885,029.22 million cubic feet of natural gas per year (as of 2015), ranking 33rd in the world.

Iraq does not export natural gas.

According to analytical forecasts, over the next decade, commercial gas production in Iraq will increase to about 50 billion m

3 [

18]. Considering that Iraqi-associated gas is rich in ethane, progress in its exploration and production could also contribute to a significant increase in petrochemical production. The methods Iraq uses to extract and use its gas will determine the overall process of reform and modernization.

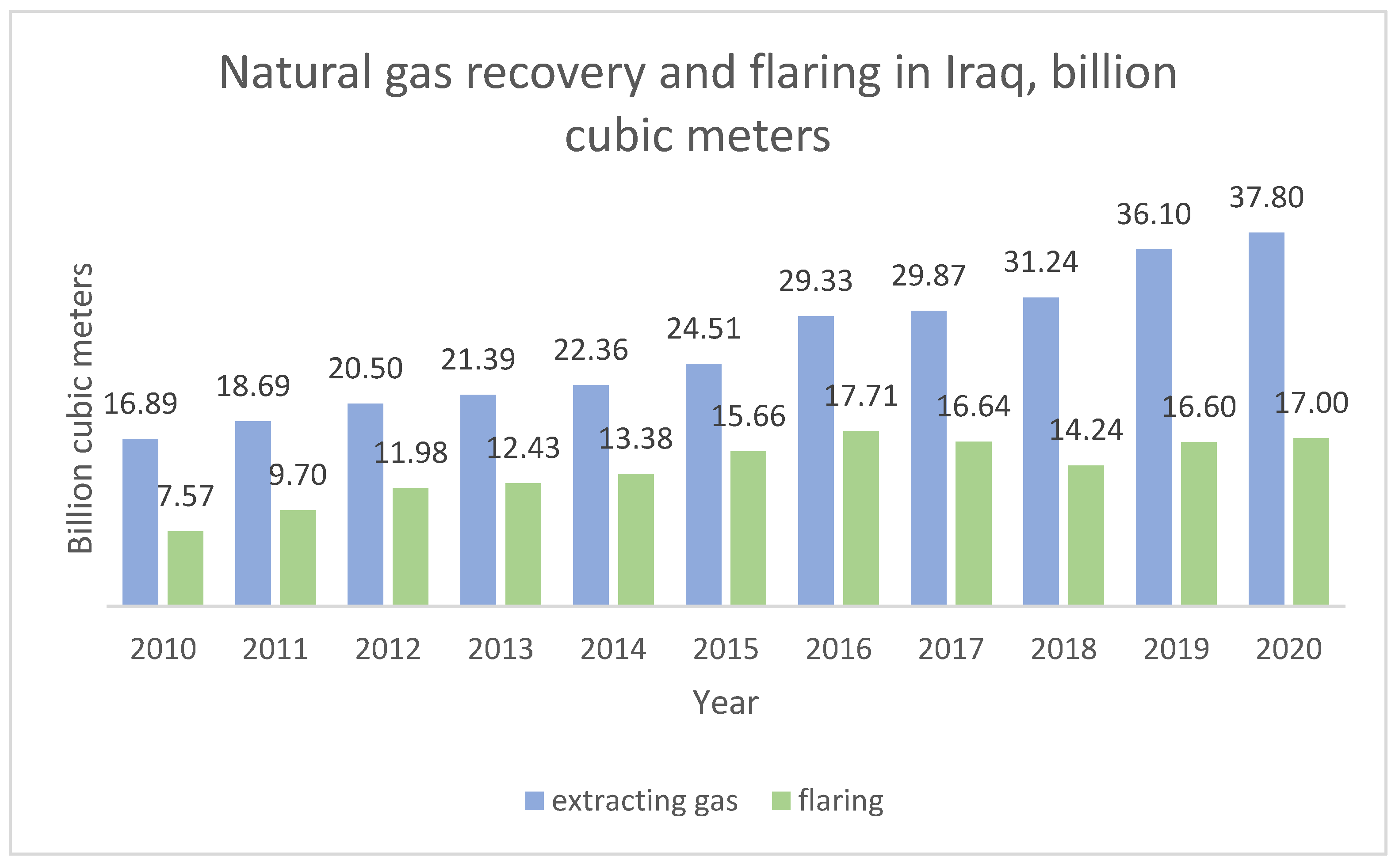

About three quarters of Iraq’s natural gas reserves are associated with oil. Most of this associated natural gas is concentrated in supergiant fields in the south of the country [

19]. In 2019, Iraq produced 378 billion cubic feet of dry natural gas.

In 2019, Iraq consumed 636 billion cubic feet of dry natural gas, most of which was used by the electricity sector. According to the World Bank, Iraq flared 632 billion cubic feet of natural gas in 2019 [

19], ranking second in the world in natural gas flaring, after Russia. Natural gas is flared due to insufficient pipeline capacity and other medium-flow infrastructure used to transport natural gas from production areas.

Figure 2 presents data on the extraction and flaring of natural gas in Iraq.

Until recently, the full development of gas reserves has been hampered by conflicts, sanctions and underinvestment. Conflicts resulted in damage to key energy facilities, which have been not fully recovered [

22]. Subsequent political reforms must follow a coherent policy of economic and social development, which will benefit all Iraqis and be based on a fair distribution of wealth and equality between generations [

23]. The country has not benefited from unsustainable profits, inefficient state-owned enterprises, and commitment to short-term consumption in a bloated public sector. As a result, Iraq’s macro-economy remains very fragile and urgently needs to be addressed, as a sound fiscal and monetary system is critical to the country’s stability.

The heavy dependence on electricity and gas imported from Iran to supply local power plants is another problem for the Iraqi economy. Iraq is experiencing a deep energy crisis with power shortages that have persisted for decades due to blockades and successive wars. For example, Iraq produces 19,000 megawatts of electricity, while representatives of the electricity sector argue that the real need is over 30,000 megawatts. The unstable relations between the countries for many years have resulted in frequent power cuts, especially in summer, when temperatures sometimes exceed 50 degrees Celsius. The Iraqi authorities are continuing negotiations with the countries of the Persian Gulf, led by Saudi Arabia, regarding the import of electricity through the connection between its energy system and the system of the Persian Gulf [

24].

In addition, the country faces the challenge of creating jobs for a rapidly growing number of young people. The development of the gas industry provides an opportunity to diversify the economy, but this structural change will take many years, and immediate action is needed to integrate the rapidly increasing young labor force into the labor market. The public sector can no longer provide this labor force with jobs, as it could during the period of high oil prices, so it is important to develop a robust private sector and attract foreign direct investment, which is destined to become a powerful engine of growth and job creation [

25].

The most challenging obstacles to the development of the gas industry in Iraq are as follows [

2,

3,

6]:

The need to conduct a variety of administrative proceedings to obtain the necessary permits, approvals and opinions;

Complex and lengthy administrative and legal procedures;

Division of competencies within the above administrative and legal procedures between various state authorities and local self-government;

Vague provisions and doubts regarding their interpretation, as well as excessively frequent changes in legal status;

The issue of accessing energy enterprises for the real properties to be invested in;

Lengthy legal proceedings.

3.2. Development of the Contract System

As we can see, one of the obstacles in the industry is state regulation. Thus, in 2017–2018, the Council of Ministers resolutions (No. 423 and No. 50) were adopted regarding the market regulation for natural, associated and liquefied gas, as well as the conversion of gas into electricity. The resolutions envisage the establishment of a gas pipeline company, holding of tenders to implement contracts for gas production and processing, the development of infrastructure facilities for gas processing, etc. Investors buy gas from the Ministry of Oil at agreed prices, sell it to companies that convert gas into electricity, and export gas. However, there is still no law in Iraq that lays the foundations for subsoil use, since the political groups in the country fail to agree on the legal boundaries of foreign companies in Iraq and the distribution of oil revenues. Each investment contract is considered on an individual basis. This leads to reduced competition, monopolization of the industry and corruption in contract procedures.

Oil and gas contracts represent relationships between oil- and gas-producing countries and international companies operating in the exploration and production of oil or gas. Such contracts are used if the owner of the subsoil lacks financial or material and technological resources.

The following types of oil and gas contracts exist:

- -

Term Service Contracts (TSC);

- -

Production Sharing Contracts (PSC);

- -

Franchising contracts;

- -

Hybrid contracts.

Franchising and hybrid contracts are used less often.

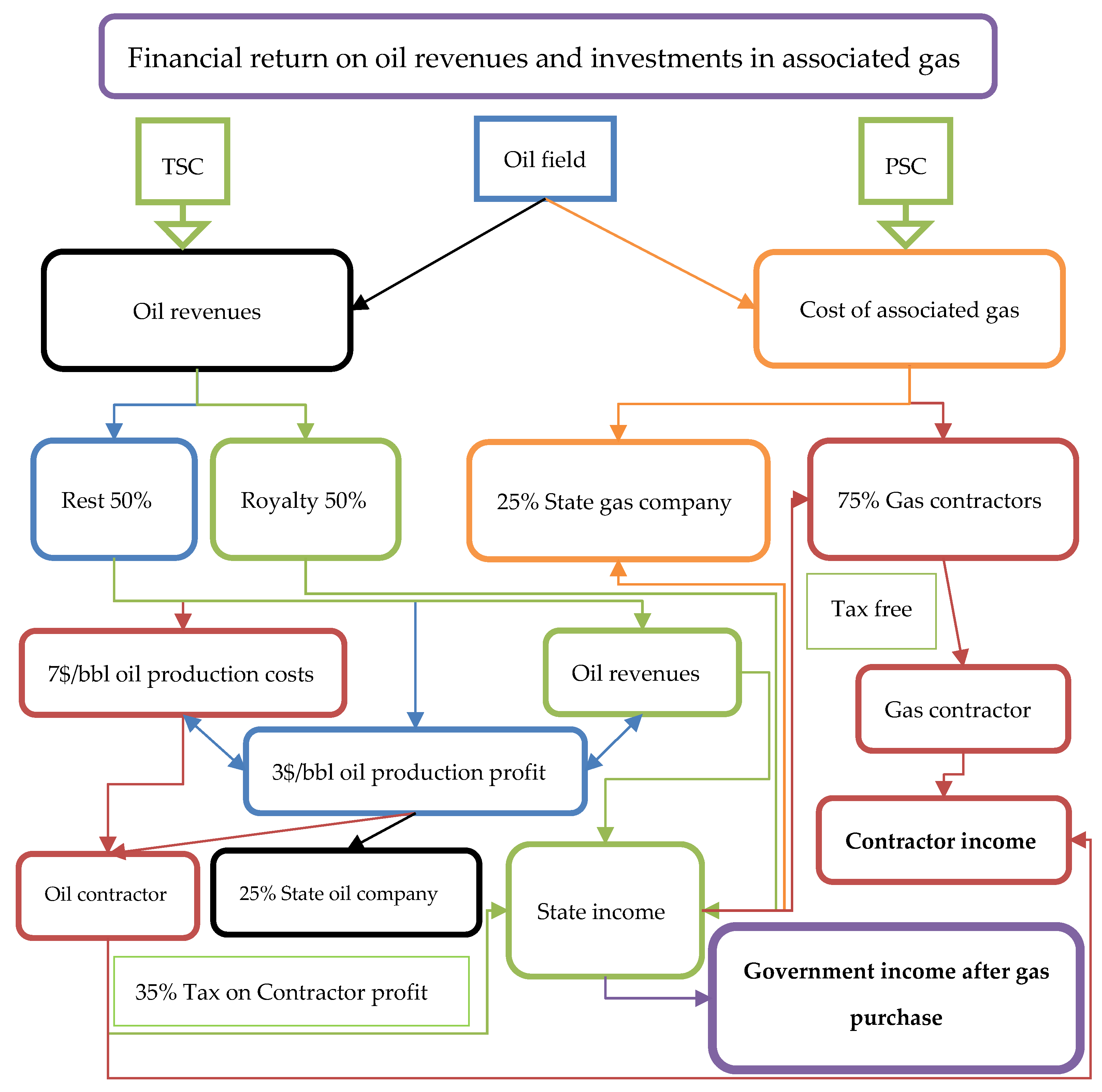

A feasibility study of investments in the use of associated gas and production of free gas is discussed below. A diagram of financial transactions that occur when investing in associated gas, and the income from oil and associated gas, are shown in

Figure 3 and

Figure 4. In

Figure 5, a situation with associated gas flaring is shown. The diagrams were compiled using Reference [

26].

Let us calculate the losses of the Iraqi economy in the absence of investment in the area.

For the calculation, let us assume that Iraqi oil production per day amounts to 50 thousand barrels per day. The APG produced will amount to 850 thousand m

3; the selling price will be 75 USD/bbl; the cost of associated gas production will be 56 USD/thousand cubic meters; the price of imported gas will be 280 USD per thousand m

3 of natural gas. The production of 50 thousand barrels of oil under standard conditions will yield about 850 thousand m

3 of natural gas [

26].

The calculations economically substantiate the expediency of investing in gas and using gas associated with oil operations, instead of importing natural gas from abroad. It should be noted that Iraq relies on oil to fund more than 95% of its budget [

26].

Oil revenues account for 95% of the Iraqi budget. Accordingly,

$

Costs of importing gas from abroad = 238,000 $

Costs of associated gas production = 47,600

$

The difference between the cost of gas production and imported gas = 190,400 $.

Percentage of losses for the Iraqi economy in the absence of investments in associated gas.

Thus, Iraq will lose 6% of its total national revenue if it does not invest in associated gas and depends on gas that is imported from abroad; however, if Iraq invests in associated gas, this will provide 5% of state revenue, which reduces losses from 6% to 1%. It is worth noting that Iraq produces more than 4 million barrels of oil per day and flares more than 55% of the associated petroleum gas. The economic feasibility of developing investments in associated gas can also be confirmed on the basis of the following analytical data. Iraq imports natural gas from abroad (to generate electricity) at a price of 245–350 US dollars per thousand m3, while obtaining natural gas from APG costs the Iraqi government 35–105 US dollars per thousand m3. The conclusions from the studies and calculations are as follows:

It is necessary to continue and expand oil exploration to increase oil reserves, increase the oil production limit and increase associated gas production within the OPEC oil-production limits, as well as increasing oil reserves through the development of fields in all regions of Iraq.

It is necessary to continue joint projects with major international gas companies to increase the exploration and development of free gas to meet the local demand and export opportunities for gas, as well as the possibility of developing natural gas in the western region of Iraq.

Increasing the production of gas and its derivatives will promote the development of relevant industries that intensively use clean energy, with a preference for investment in the private and joint sectors.

The natural gas system, the pricing of household gas and the gas used for transportation should be properly developed, and the number of filling stations, which is dependent on the supply of natural gas, should be increased, as this is environmentally friendly.

Petrochemical plants should mainly develop to meet local needs and other export-oriented industries; export-oriented industries, such as petrochemicals, omust be located in the same area, close to Basra, due to ports, geographic location and infrastructure size.

The natural gas service sector, including local and international companies, should be encouraged through investment contracts that are acceptable to all investors, namely through profit-sharing in service contracts and production-sharing contracts, so that more international companies are present in Iraq.

A typical formula for calculating economic rent (

ER), as a starting point for evaluating a particular section of an oil or gas field, may look like this:

where:

ER: Economic rent.

n: Time horizon.

t: Year.

Po: Expected price of oil and gas, USD per barrel.

Pr: Expected oil and gas production, barrel/year.

rt: Royalty, %.

Lt: Expected income tax, USD/year.

Jt: Expected production costs, USD/year.

w: Expected well-drilling costs, USD.

I: Discount rate.

Studies show the need to base the calculation of the cost of production reductions in the oil and gas fields, within the framework of technical service contracts. Then, we can find the production reduction factor using the following mathematical formula:

where “

” is a production reduction factor.

The formula for cash income from oil and gas technical service contracts might look like this:

where:

ГД—state share (SS);

ПД—contractor share (CS);

GP—state partner;

Po—expected price of oil and gas;

Pr—expected production of oil and gas;

Lt—expected profit tax;

P—profit;

RF (R-Factor)—recovery factor = (Total income)/(Total costs) × 100%

PF (P-Factor)—production factor = (Actual production)/(Planned production) × 100%

ReF (Re-Factor)—production reduction factor = (Actual production)/(Reduced production) × 100%

C—costs of oil and gas production.

We believe that it is necessary to introduce changes to the legislation, and to consolidate the transformation of existing oil and gas agreements into service contract. This is the key challenge in the development of the Iraqi gas industry. A service contract will allow the investor some discretion: under previous contracts, profits were distributed on the basis of the declared discrete value, and the use of service contracts implies the use of ad valorem rates (i.e., rates per cent) of the initial values. This approach seems more economically feasible, since its use to conclude contracts for the development of oil and gas fields will ensure higher revenues while reducing production costs.

The details of this approach are provided in

Figure 6.

When selling a given volume of commercial gas for a certain period of time, the company receives 100% of the sales revenue. According to the terms of the applicable service contract, 50% of the received revenue is paid to the government as royalties. The balance of the revenue is divided into reimbursements of the production costs incurred by the contractor when developing the asset, and profits.

We shall now calculate the practical application of this technique. We will consider this approach by using an example (

Figure 7).

It has been revealed that the provisions offered by Iraqi legislation when regulating the construction process are not in line with the specifics of the implementation of linear investments. Linear facilities, such as gas infrastructure, are largely located in regional areas. Subsequently, such investments are associated with the need to carry out administrative procedures with the state authorities and local governments, which often not only do not cooperate with each other to efficiently obtain the appropriate permits, but compete with each other, leading to conflicting goals. This situation is largely due to the fragmentation of individual competencies between bodies that solve highly specialized tasks, and the lack of a single decision-making center that plays a decisive role in the investment process for linear investments.

It should be noted that public administration authorities are aware of the problems associated with the administrative and legal barriers that impede the implementation of linear investments. One measure to improve the energy security of the country could be legislative measures, aiming to remove investment barriers, particularly in the area of major investments in infrastructure (warehouses, CNG infrastructure, gas compressor stations, etc.).

Furthermore, attempts should be made to introduce legislative solutions that would contribute to the expansion of the energy infrastructure. These form main stages of the administrative and legal procedures that are necessary to invest in infrastructure. As part of the investment process, there are several main stages of the administrative and legal procedures that a company will face when planning to develop a linear infrastructure. First of all, they must determine in which facility they will invest. This calls for agreement with local governments and their inclusion in local plans (local territorial development plans). The foreseen infrastructure, as a rule, will only partly pass through areas that are covered by local plans, while other areas will remain uncovered. This necessitates a separate decision on the facilities in which to invest.

Additional infrastructure facilities for the distribution of gas in Iraq will be needed to connect regions with new gas sources, or gas-supply sources, to areas where production is expected to increase. Not all areas will need an extensive transmission network; connecting new investments to the existing network may be enough. As mentioned earlier, each new infrastructure investment will largely depend on the economic viability of the project. Therefore, it is not surprising that long-term contracts will ensure greater predictability and allow for long-term planning.

It should be mentioned that a foreign company will not want to build a new transmission infrastructure unless provided with two important elements. First of all, the reliability of the supply of raw materials is worth noting; this can only be guaranteed by a long-term sales contract. In addition, this allows for companies to begin the process of raising funds, and manage portfolios of investments. Secondly, the sale of purchased and shipped raw materials should be ensured. In this case, the best option is to search for major customers, which could be a large industrial (chemical) plant or a power plant equipped with gas units. In this context, a long-term gas purchase agreement should also be considered to ensure economic viability and full utilization of infrastructure facilities [

4]. It is necessary to apply advanced methods of managing oil and gas companies [

27,

28]. It is also necessary to monitor the problems of taxation [

29], the employment of efficient technologies [

30,

31,

32], and the application of modern geophysical methods [

33].

In addition, market competition for unconventional gas production (the issue of exploration concessions to many entities) should contribute to greater diversification of supplies and, as a result, the possibility of Iraq being engaged as a supplier by, for example, EU countries. The search for new sources of natural gas supplies, in response to the forecasted growth in the consumption of this raw material, will entail the need to expand another important element of the gas infrastructure, viz. underground gas storage facilities. The country’s energy security in the field of gas is associated with the availability of sufficient gas reserves that could be employed in crisis situations (in of sudden interruptions in gas supplies from abroad, an unexpected increase in demand caused by weather conditions, etc.). Thus, the predicted growth in gas consumption requires a proportional increase in storage capacity.

The conducted analysis identified the factors that influence the development of the oil and gas industry’s infrastructure in Iraq. Unfortunately, most factors on which the development of gas infrastructure depends are unknown (uncertain). These are variables, which may manifest themselves in the future; today, we can only predict their possible impact. Therefore, the factors that affect the development of the Iraqi gas industry can be divided into two groups.

Determinants of infrastructure development, which have significant impact on the market:

Growth/decrease in GDP, which, in an era of economy based on the energy produced from natural resources, is crucial to the reported demand for energy, and, therefore, for natural gas; the growing demand for natural gas requires an expansion of the infrastructure that supplies raw materials to end consumers;

The priorities of the state’s energy policy, which determines strategic energy sectors and has a decisive influence on the distribution of the investment funds required for new infrastructure; the decision to build a nuclear power plant may decrease the inflow of funds to investments in gas infrastructure (the reverse trend is observed in Germany, with natural gas becoming an alternative to the foreseen closure of nuclear power plants);

An increase in electricity demand associated with economic growth; the construction of gas-fired power units can not only meet the increased demand for electricity, but also allow for a flexible coverage of short-term electricity shortages, for example, in summer (gas can be turned on and off very quickly);

The industrial exploitation of unconventional gas resources could significantly change the energy mix in Iraq; connecting new gas sources to the transport network would be a huge investment project, and the possible consequences associated with falling natural gas prices could lead to the creation of new gas-based power units; in the long term, if natural gas resources turn out to be extremely large, it will be possible to export gas (in the traditional form or as CNG);

National legislation, including mineral tax provisions that may determine the profitability of exploiting energy resources, in addition, restrictions related to international climate obligations (Kyoto Protocol) or plans to reduce greenhouse gas emissions into the atmosphere. It is also necessary to take into account the existing methods of regulating the markets of natural monopolies [

34].

Other considerations that may have a lesser impact on the development of the Iraqi gas industry in the future:

Development of the potentially vast market for cars and trucks fueled by compressed natural gas (CNG), which, however, requires the developed infrastructure (many filling stations to accommodate CNG filling), due to low prices for this type of gas, this infrastructure is currently being developed quite intensively, e.g., in the United States;

Population growth, which, although not a direct cause of the development of the gas market and infrastructure, nevertheless contributes to its increased economic activity, which has a direct impact on GDP growth (potentially increasing gas consumption);

Growth in industrial output, which can contribute, albeit to a lesser extent than GDP growth, to the expansion of infrastructure (although it should be noted that, in developed countries, less energy-intensive services dominate the formation of GDP);

High prices for crude oil or coal, which may affect the decisions of individual and commercial consumers regarding their heating method (switching to gas heating);

Ambient temperature, and its possible increase with climate change (regardless of the causative factors), as well as population decline, will also have an indirect impact on infrastructure development, affecting the GDP trend (although, as mentioned earlier, it may have a minor impact on the decrease in demand for gas for heating purposes);

An increase in gas production costs associated, on the one hand, with the previously mentioned, more restrictive regulation of hydraulic fracturing technologies, and, on the other hand, with the possible exploitation of increasingly less-accessible fields, which will lead to the need to search for alternative energy sources;

Exploitation of unconventional crude oil resources (oil sands or oil shale), which, paradoxically, can jeopardize investment in gas infrastructure by causing oil prices to fall worldwide (the same mechanism that led to the shale gas boom in the US is employed);

Technologies that increase energy efficiency and lead to more pro-environmental consumer behavior; in extreme cases, such measures can hinder the development of the gas industry, as they contribute to the more efficient use of raw materials. In the long-term, a technological revolution can be envisaged, resulting in the search for an alternative source of energy (fossil fuel) and independence from the current fossil-fuel infrastructure.

3.3. Choice of the Development Strategy for the Iraq Gas Industry

The following is a step-by-step calculation scheme for choosing a strategy to develop of the Iraqi gas industry:

At stage 1, the influence of different factors on the functioning and development of the gas industry should be determined. After working through the problem in terms of a hierarchy, it is necessary to evaluate the criteria and the alternatives. Using an analysis of hierarchies, elements should be compared in pairs, and their impact on the overall characteristics of the process should also be collated. We consider paired comparisons in matrix form [

15].

A set of local priorities is formed based on a group of paired comparison matrices, expressing the set’s influence on the unit element of the adjacent level from above, for which the set of vectors is calculated. Then, the result is to be normalized to one, thus obtaining a priority vector. One matrix of pair-changes describes the second level as a matrix of dominance. The factors are compared pairwise, assessing their impact on the innovative development of the region. Once the criteria (alternative factors) have been determined, the consistency of the local criteria should be assessed. The consistency index provides information about the degree of change in numerical and ordinal consistency. If the deviation exceeds the established limits, the calculations in the matrix should be rechecked.

Calculations are based on the fact that, when selling a given volume of commercial gas for a certain period of time, the company will receive 100% of the sales revenue. Based on the terms of the applicable service contract, 50% of the received revenue is paid to the government in the form of royalties. The rest of the proceeds are divided into two directions: reimbursement of the production costs incurred by the contractor in the process of developing the asset, and profits. The production costs depend on the individual characteristics of the field and are regulated by a number of factors, which include, among other things, the regional factor, the complexity of field development, and hazardous working conditions. However, this value cannot exceed 40% of the revenue, since further increases will mean that participation in this project is economically unjustified. According to the terms of the contract, 75% of the profits will be deducted by the Iraqi Oil Ministry, and the remaining 25% will be sold as follows: 25% of the balance (i.e., from 25%) falls to the state partner company, and 75% of the balance is received by the contractor. The contractor’s profit is subject to income tax at the level of 35%.

In the hierarchy analysis method, elements are compared in pairs, and their impact on the overall process characteristics is also compared.

Table 1 presents the results of an assessment of these factors’ impact on the development of the Iraqi gas industry. Let us consider pairwise comparisons as a matrix.

Let us consider the sequence used to obtain the calculation results presented in

Table 1. This technique was also used to obtain results at other stages; please review auxiliary

Table 2.

To make a pairwise comparison of the factors’ influence on the development of the Iraqi gas industry, the following scale was used: 1—equal significance; 3—moderate superiority of one factor over another; 5—significant superiority; 9—very strong superiority; 2, 4, 6, 8—intermediate judgments.

The first line was obtained as follows. The influence of political and social factors were compared: political factors predominated over social ones (the number 5). The reciprocal value (1/5) was entered in the symmetrical position of the matrix. For Iraq, political factors were less strong than economic ones. The estimate was 1/3; the inverse number were entered into the symmetrical position of the matrix, that is, 3. The estimates were obtained by qualified experts in the field, with scientific doctorates. Other factors were assessed in a similar way. To ensure the reliability of the expert survey, indicators of the consistency index (ИC) and the consistency ratio (OC) were calculated. The consistency index provides information about the degree of violation of numerical and ordinal consistency. Lack of consistency was a limiting factor. The value of the consistency ratio should not exceed 20%.

Calculation in columnar form “Eigen Vector”

Political: (1 + 5 + 0.333 + 3 + 3):5 = 2.47

Social: (0.2 + 1 + 0.333 + 0.333 + 0.333):5 = 0.44

Political: (3 + 3 + 1 + 4 + 3):5 = 2.8

Environmental: (0.333 + 3 + 0.25 + 1 + 0.5):5 = 1.017

Technical and process: (0.333 + 3 + 0.333 + 2 + 1):5 = 1.333

Calculation in columnar form “Normalized Priority Vector Estimates”

Economic: 2.47:8.06 = 0.306

Social: 0.44:8.06 = 0.055

Political: 2.8:8.06 = 0.348

Environmental: 1.017:8.06 = 0.126

Technical and process: 1.333:8.06 = 0.165

The consistency index is calculated as follows. First, each column of judgments is summed, then the sum of the first column is multiplied by the value of the first component of the normalized priority vector. The sum of the second column is multiplied by the second component, and so on. Then, the resulting numbers are summed. Thus, one can obtain the value denoted as

:

For an inversely symmetric matrix ≥ is always followed.

The consistency index can be found using the formula:

, where

is the number of compared components.

A table of average consistency for random matrices of different orders is given below, as

Table 3.

To obtain the consistency ratio (

OC), let us divide the

ИC by a number corresponding to the random consistency of the matrix of the same order:

The final calculations by factors are presented in

Table 1.

Table 4 shows the results of an assessment of the importance of the actors’ goals. For the Council of Ministers of Iraq, the most important goal when building a strategy for the development of the gas industry is the construction of infrastructure for the gas industry—the value of the normalized priority vector estimate is 0.478. The total estimates of the goals are 1 (0.350 + 0.478 + 0.172 = 1). The results of the assessment of the objectives of the Iraqi Ministry of Oil, the Ministry of Energy, and the state gas and oil companies, both public–private and private oil and gas enterprises, are interpreted in a similar way.

At stage 2, it is necessary to determine actors’ degree of influence on factors. At stage 3, the importance of all seven goals of the actors should be determined. These are compared in pairs. The result is priority vectors that reflect the ordering of weights and goals. The results of the actors’ assessment are summarized in

Table 4.

At stage 4, a synthesis of priorities should be determined, starting from the second level. The local priorities are multiplied by the priority of the top-level criterion and summed for each element of the impact criterion.

Let us determine the degree of actors’ influence on factors by multiplying the matrix of vectors of the third level of actors’ priorities by the vector of priorities from the second level in

Table 5.

The calculation is based on the fact that, when selling one barrel of oil at a price of 75 USD/bbl., the sales revenues will be 75 USD. Half of the proceeds (37.5 USD) are paid to the government in the form of royalties. The second half is distributed as follows: production costs in this field are 8 USD/bbl, with the retained earnings of 29.5 USD.

According to the terms of the contract, 75% of the retained earnings (22,125 USD) fell on the Iraqi Ministry of Oil, and the remainder was distributed between the state partner company and the contractor in the following ratio: 25% of the balance (≈1844 USD) fell on the state partner, and 75% of the balance (≈5.531 US dollars) on the contractor. The contractor’s profits were subject to a 35% income tax (≈1936 USD). As a result, the income distribution looks like this:

The state—61.561 USD (37.5 + 22.125 + 1.936);

Government partner—1.844 USD;

Contractor—11.595 USD (8 + 3.595).

Let us consider the results of the analysis:

- (1)

For the Council of Ministers of Iraq, the main goal is to form the infrastructure of the gas industry as a prerequisite for the effective development of the national economy;

- (2)

For the Oil Ministry, the main goal is ensuring the sustainable functioning and development of the oil and gas industry;

- (3)

For the Ministry of Energy, the main goal is to increase the economic efficiency of the production, transmission and distribution of electricity;

- (4)

For national gas companies, the main goal is the development of an infrastructure for the utilization of free and associated gas;

- (5)

For national oil companies, the main goal is the use of associated gas;

- (6)

For public–private oil and gas companies, the main goal is the exploration of oil and associated gas fields;

- (7)

For private oil and gas companies, the main goal is to increase the utilization of oil and gas reserves.

The normalized vector is then applied to obtain weights for the development strategies for the Iraqi gas industry. By normalizing the weights of the goals with maximum values, we obtain the resulting vector of the goal weights. At stage 5, the development strategies’ degree of influence on the actors’ goals should be determined. Let us consider five contract investment strategies within the hierarchical model for the development of the Iraqi gas industry:

Investing in associated gas, stopping the use of oil to generate energy and electricity.

Investing in associated gas, fully meeting the needs of the industry regarding this type of resource, and refusing to import gas from abroad.

Investing in free gas and stopping the import of electricity from abroad.

Free basic investments and operations, and investments in petrochemical projects.

Investing in natural gas (both associated and free), making arrangements for the exportation of operations with natural gas. The weights of the strategies were formed in the dominance matrices using goals; the results of paired comparisons are presented in

Table 6.

Stage 6 is the determination of the necessary strategy for the development of the Iraqi gas industry. When multiplying the matrix by the vector of goal weights, the remarkable thing is that the largest share is accounted for by the second strategy, i.e., investing in associated gas, independently meeting the needs of the Iraqi industry regarding this type of resource, and refusing to import gas from abroad.

Thus, in summary:

Iraq possesses large natural gas resources, which can be used to increase clean energy use via greater investments in free gas fields and associated gas processing.

A promising investment image should be developed to attract foreign investment by reducing bureaucracy and increasing the share of profits, so that the return relationship between owner and investor is straight. This would mean that profits increase together, instead of without the other party.

The investment strategies for natural gas production in Iraq are as follows: the first step is to invest in the processing of associated gas in oil fields; the second step is to invest in free gas fields, since the investment costs of associated gas are lower because it directly depends on the infrastructure of oil fields.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}