Time-Varying Relationship between Crude Oil Price and Exchange Rate in the Context of Structural Breaks

Abstract

:

1. Introduction

2. Methodology and Data

2.1. Model Specification

2.2. Data Selection and Data Pre-Processing

3. Analysis of Time-Varying Characteristics of Crude Oil Price and Exchange Rate Fluctuation

3.1. Parameter Estimation

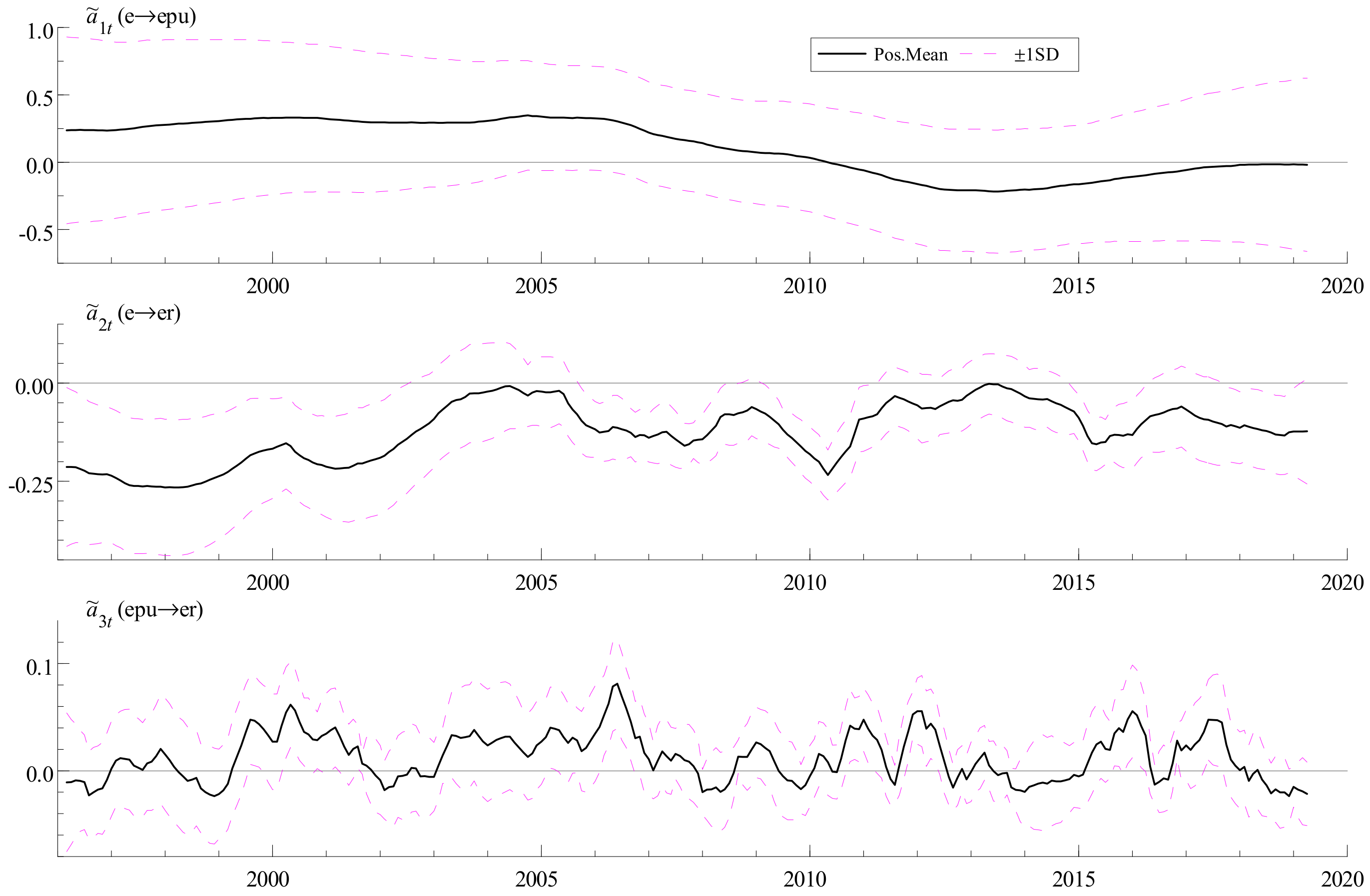

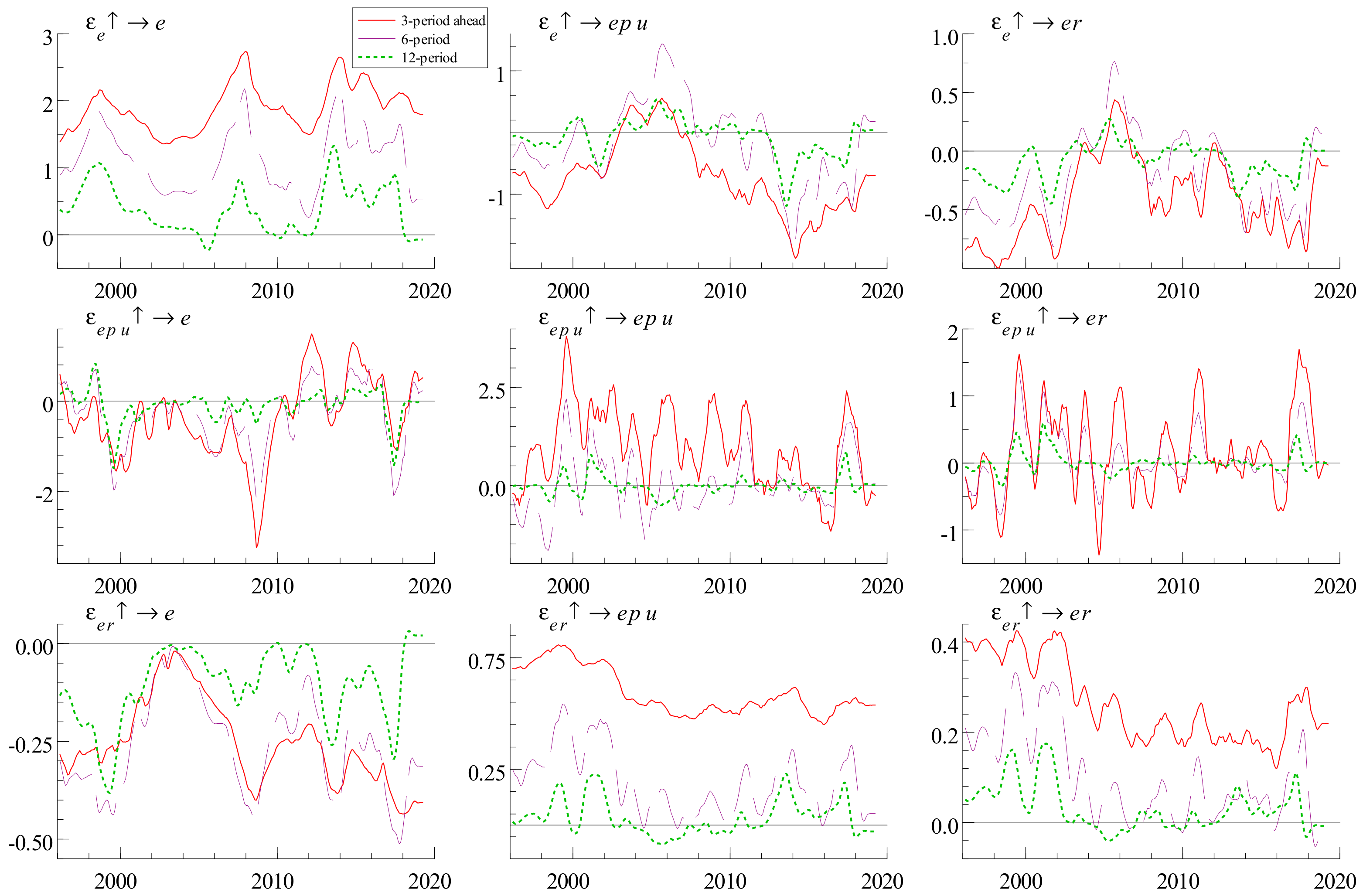

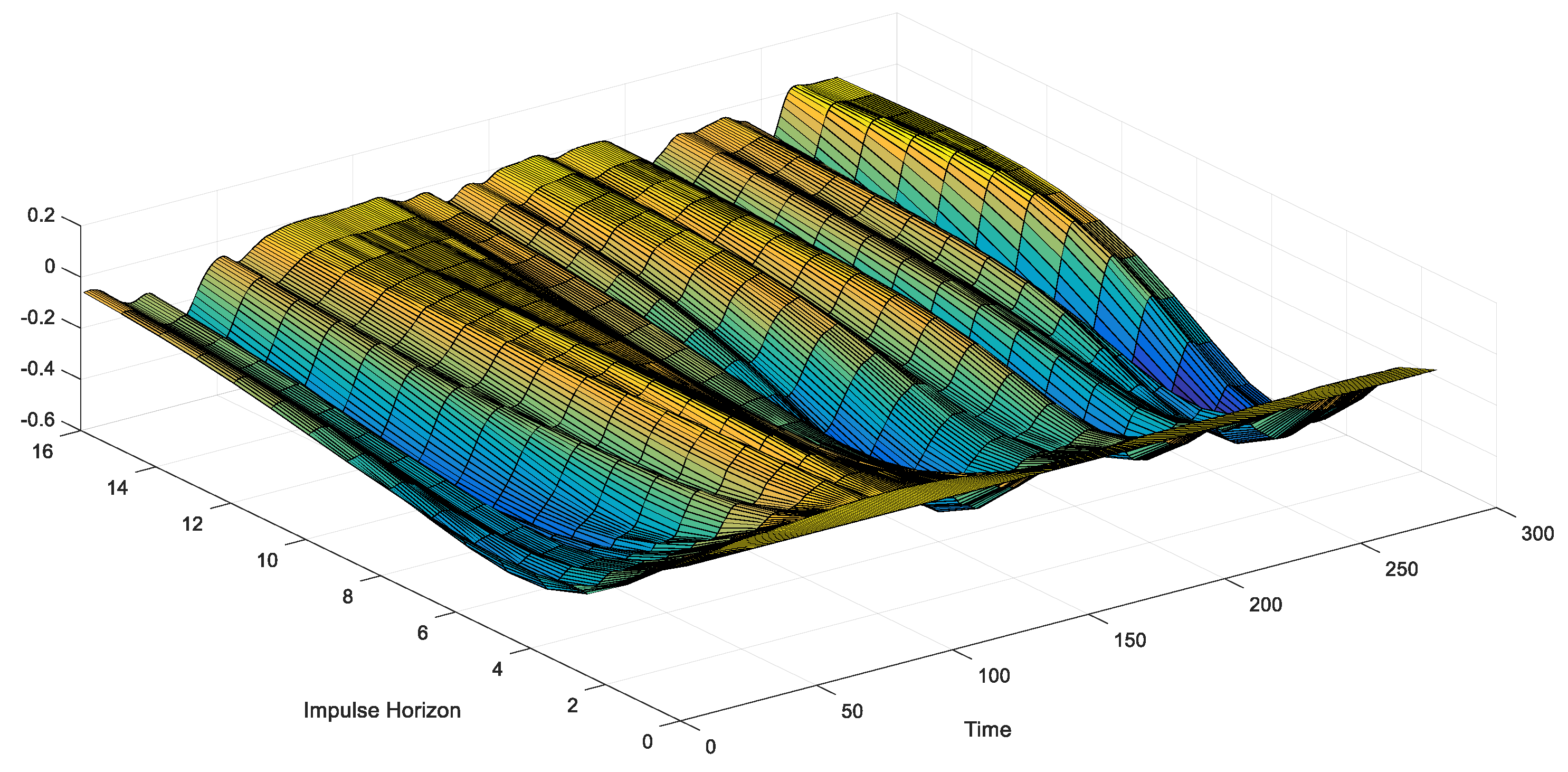

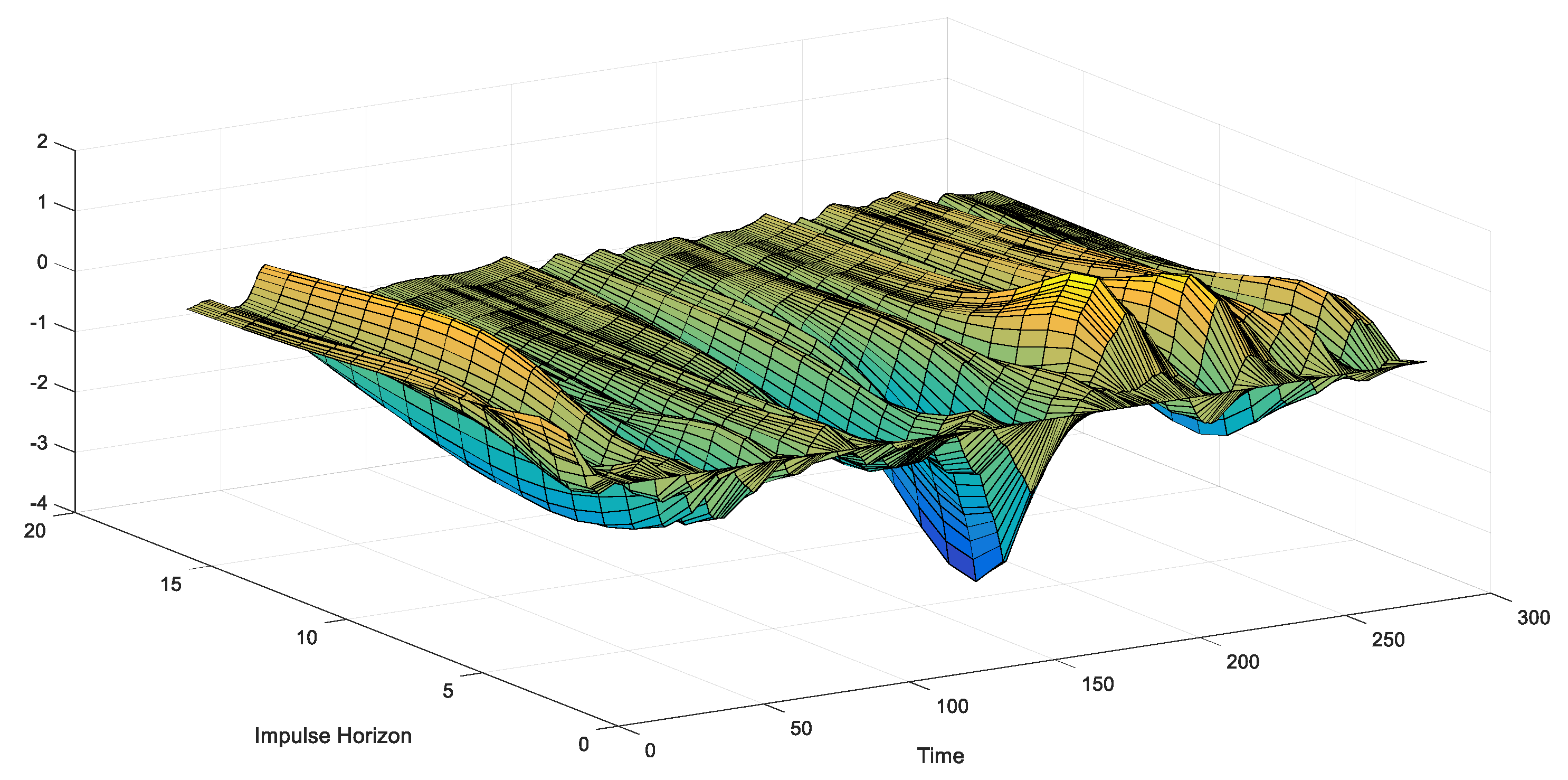

3.2. The Time-Varying Characteristics of the Correlation between Crude Oil Price and Exchange Rate Fluctuations

3.3. Analysis of Time-Varying Characteristics of the Correlation between Crude Oil Price and Exchange Rate Fluctuation with Time-Delay

4. Time-Varying Characteristics of Crude Oil Price and Exchange Rate Based on Structural Breaks

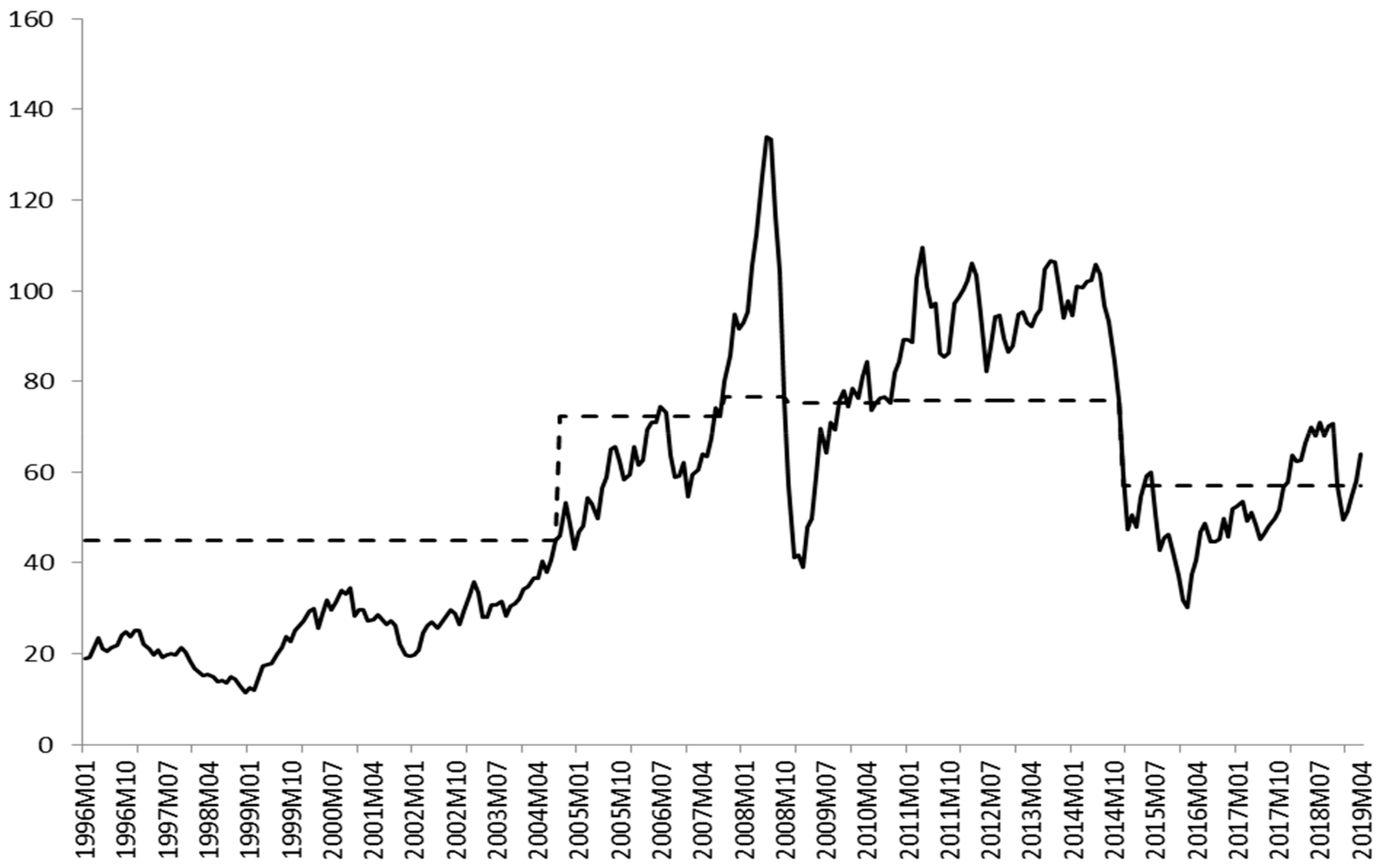

4.1. Unit Root Test in the Presence of Structural Breaks

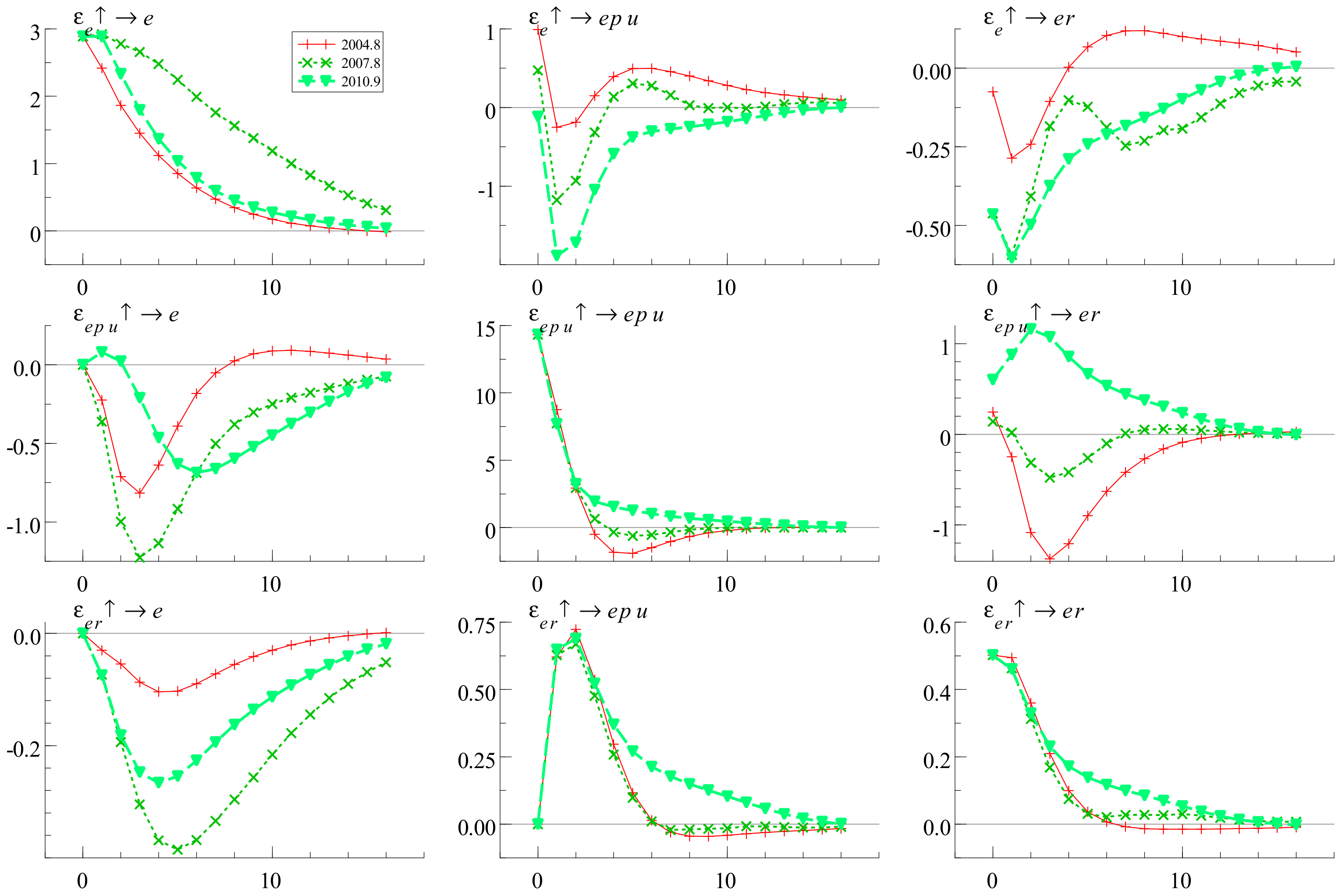

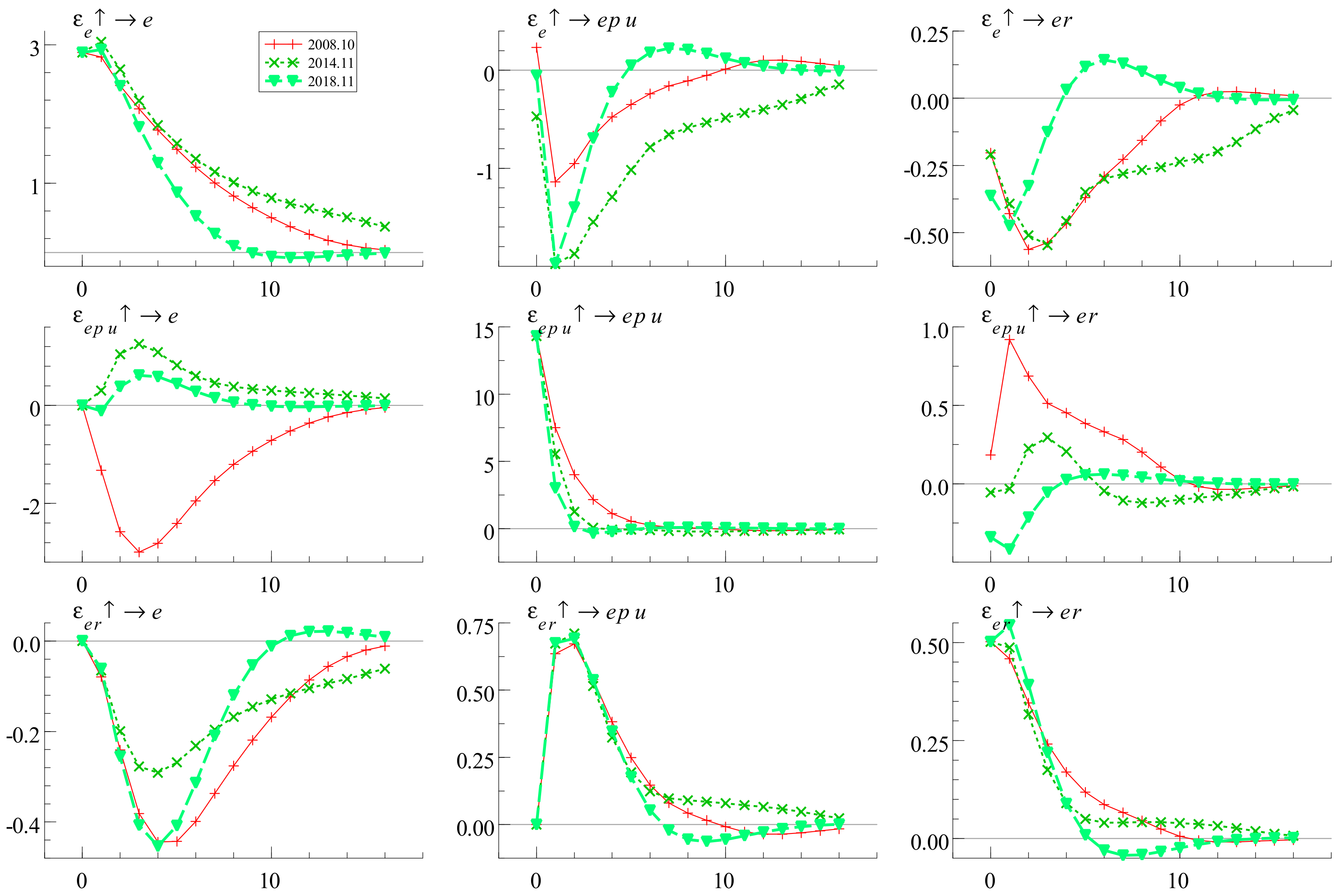

4.2. Estimation of Impulse Response Function Based on Structural Breaks

4.3. Time-Varying Characteristics Based on Structural Breaks

5. Conclusions and Policy Implications

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Wen, F.H.; Xu, L.H.; Ouyang, G.D.; Kou, G. Retail investor attention and stock price crash risk: Evidence from China. Int. Rev. Financ. Anal. 2019, 65, 15. [Google Scholar] [CrossRef]

- Chen, H.T.; Liu, L.; Wang, Y.D.; Zhu, Y.M. Oil price shocks and US dollar exchange rates. Energy 2016, 112, 1036–1048. [Google Scholar] [CrossRef] [Green Version]

- Chang, H.F.; Huang, L.C.; Chin, M.C. Interactive relationships between crude oil prices, gold prices, and the NT-US dollar exchange rate-a Taiwan study. Energy Policy 2013, 63, 441–448. [Google Scholar] [CrossRef]

- Hussain, M.; Zebende, G.F.; Bashir, U.; Ding, D.H. Oil price and exchange rate co-movements in Asian countries: Detrended cross-correlation approach. Phys. A 2017, 465, 338–346. [Google Scholar] [CrossRef]

- Cong, R.G.; Wei, Y.M.; Jiao, J.L.; Fan, Y. Relationships between oil price shocks and stock market: An empirical analysis from China. Energy Policy 2008, 36, 3544–3553. [Google Scholar] [CrossRef]

- Jawadi, F.; Louhichi, W.; Ben Ameur, H.; Cheffou, A.I. On oil-us exchange rate volatility relationships: An intraday analysis. Econ. Model. 2016, 59, 329–334. [Google Scholar] [CrossRef]

- Volkov, N.I.; Yuhn, K.H. Oil price shocks and exchange rate movements. Glob. Financ. J. 2016, 31, 18–30. [Google Scholar] [CrossRef]

- Turhan, M.I.; Sensoy, A.; Hacihasanoglu, E. A comparative analysis of the dynamic relationship between oil prices and exchange rates. J. Int. Financ. Mark. Inst. Money 2014, 32, 397–414. [Google Scholar] [CrossRef]

- Mensah, L.; Obi, P.; Bopkin, G. Cointegration test of oil price and us dollar exchange rates for some oil dependent economies. Res. Int. Bus. Financ. 2017, 42, 304–311. [Google Scholar] [CrossRef]

- Sun, X.; Lu, X.; Yue, G.; Li, J. Cross-correlations between the US monetary policy, US dollar index and crude oil market. Phys. A Stat. Mech. Its Appl. 2017, 467, 326–344. [Google Scholar] [CrossRef]

- Coudert, V.; Mignon, V. Reassessing the empirical relationship between the oil price and the dollar. Energy Policy 2016, 95, 147–157. [Google Scholar] [CrossRef] [Green Version]

- Kumar, S. Asymmetric impact of oil prices on exchange rate and stock prices. Q. Rev. Econ. Financ. 2019, 72, 41–51. [Google Scholar] [CrossRef]

- Bahmani-Oskooee, M.; Saha, S. On the effects of policy uncertainty on stock prices: An asymmetric analysis. Quant. Financ. Econ. 2019, 3, 412–424. [Google Scholar] [CrossRef]

- Basher, S.A.; Haug, A.A.; Sadorsky, P. Oil prices, exchange rates and emerging stock markets. Energy Econ. 2012, 34, 227–240. [Google Scholar] [CrossRef] [Green Version]

- Bildirici, M.E.; Badur, M.M. The effects of oil prices on confidence and stock return in China, India and Russia. Quant. Financ. Econ. 2018, 2, 884–903. [Google Scholar] [CrossRef]

- Jones, C.M.; Kaul, G. Oil and the stock markets. J. Financ. 1996, 51, 463–491. [Google Scholar] [CrossRef]

- Sornette, D.; Cauwels, P.; Smilyanov, G. Can we use volatility to diagnose financial bubbles? Lessons from 40 historical bubbles. Quant. Financ. Econ. 2018, 2, 1–105. [Google Scholar] [CrossRef]

- McLeod, R.C.D.; Haughton, A.Y. The value of the US dollar and its impact on oil prices: Evidence from a non-linear asymmetric cointegration approach. Energy Econ. 2018, 70, 61–69. [Google Scholar] [CrossRef]

- Anoruo, E. Testing for Linear and Nonlinear Causality between Crude Oil Price Changes and Stock Market Returns. Int. J. Econ. Sci. Appl. Res. 2012, 4, 75–92. [Google Scholar]

- De Vita, G.; Trachanas, E. ‘Nonlinear causality between crude oil price and exchange rate: A comparative study of China and India’—A failed replication (negative type 1 and type 2). Energy Econ. 2016, 56, 150–160. [Google Scholar] [CrossRef]

- Ewing, B.T.; Malik, F. Modelling asymmetric volatility in oil prices under structural breaks. Energy Econ. 2017, 63, 227–233. [Google Scholar] [CrossRef]

- Chen, L.; Du, Z.; Hu, Z. Impact of economic policy uncertainty on exchange rate volatility of China. Financ. Res. Lett. 2020, 32, 101266. [Google Scholar] [CrossRef]

- Yang, L.; Cai, X.J.; Hamori, S. Does the crude oil price influence the exchange rates of oil-importing and oil-exporting countries differently? A wavelet coherence analysis. Int. Rev. Econ. Financ. 2017, 49, 536–547. [Google Scholar] [CrossRef]

- Tiwari, A.K.; Albulescu, C.T. Oil price and exchange rate in India: Fresh evidence from continuous wavelet approach and asymmetric, multi-horizon Granger-causality tests. Appl. Energy 2016, 179, 272–283. [Google Scholar] [CrossRef]

- Bartsch, Z. Economic policy uncertainty and dollar-pound exchange rate return volatility. J. Int. Money Finan. 2019, 98, 17. [Google Scholar] [CrossRef]

- Li, Z.; Zhong, J. Impact of economic policy uncertainty shocks on China’s financial conditions. Financ. Res. Lett. 2019, 101303. [Google Scholar] [CrossRef]

- Li, Z.H.; Dong, H.; Huang, Z.H.; Failler, P. Asymmetric effects on risks of virtual financial assets (VFAs) in different regimes: A case of bitcoin. Quant. Financ. Econ. 2018, 2, 860–883. [Google Scholar] [CrossRef]

- Apergis, N.; Miller, S.M. Do structural oil-market shocks affect stock prices? Energy Econ. 2009, 31, 569–575. [Google Scholar] [CrossRef] [Green Version]

- Salisu, A.A.; Fasanya, I.O. Modelling oil price volatility with structural breaks. Energy Policy 2013, 52, 554–562. [Google Scholar] [CrossRef]

- Sadorsky, P. Modelling and forecasting petroleum futures volatility. Energy Econ. 2006, 28, 467–488. [Google Scholar] [CrossRef]

- Kang, S.; Yoon, S. Forecasting Volatility of Crude Oil Markets. Energy Econ. 2009, 31, 119–125. [Google Scholar] [CrossRef]

- Jian, J.; Gu, R. Asymmetrical long-run dependence between oil price and US dollar exchange rate—Based on structural oil shocks. Phys. A Stat. Mech. Its Appl. 2016, 456, 75–89. [Google Scholar] [CrossRef]

- Bai, D.P.; Rath, B.N. Nonlinear causality between crude oil price and exchange rate: A comparative study of China and India. Energy Econ. 2015, 51, 149–156. [Google Scholar] [CrossRef]

- Mollick, A.V.; Sakaki, H. Exchange rates, oil prices and world stock returns. Resour. Policy 2019, 61, 585–602. [Google Scholar] [CrossRef]

- Jain, A.; Biswal, P.C. Dynamic linkages among oil price, gold price, exchange rate, and stock market in India. Resour. Policy 2016, 49, 179–185. [Google Scholar] [CrossRef]

- Reboredo, J.C. Modelling oil price and exchange rate co-movements. J. Policy Model. 2012, 34, 419–440. [Google Scholar] [CrossRef]

- Ji, Q.; Shahzad, S.J.H.; Bouri, E.; Suleman, M.T. Dynamic Structural Impacts of Oil Shocks on Exchange Rates: Lessons to Learn; Springer: Berlin/Heidelberg, Germany, 2020; Volume 9. [Google Scholar] [CrossRef] [Green Version]

- Brémond, V.; Hache, E.; Razafindrabe, T. On the link between oil price and exchange rate: A time-varying VAR parameter approach. Work. Pap. 2015. [Google Scholar] [CrossRef]

- Wen, F.; Xiao, J.; Huang, C.; Xia, X. Interaction between oil and US dollar exchange rate: Nonlinear causality, time-varying influence and structural breaks in volatility. Appl. Econ. 2018, 50. [Google Scholar] [CrossRef]

- Castro, C.; Jiménez-Rodríguez, R. Time-Varying Relationship between Oil Price and Exchange Rate. MPRA Paper. 2018. Available online: https://mpra.ub.uni-muenchen.de/87879/ (accessed on 9 October 2019).

- Primiceri, G.E. Time varying structural vector autoregressions and monetary policy. Rev. Econ. Stud. 2005, 72, 821–852. [Google Scholar] [CrossRef]

- Jebabli, I.; Arouri, M.; Teulon, F. On the effects of world stock market and oil price shocks on food prices: An empirical investigation based on tvp-var models with stochastic volatility. Energy Econ. 2014, 45, 66–98. [Google Scholar] [CrossRef]

- Liao, G.K.; Li, Z.H.; Du, Z.Q.; Liu, Y. The heterogeneous interconnections between supply or demand side and oil risks. Energies 2019, 12, 17. [Google Scholar] [CrossRef] [Green Version]

- Xu, Y.; Han, L.; Wan, L.; Yin, L. Dynamic link between oil prices and exchange rates: A non-linear approach. Energy Econ. 2019, 84. [Google Scholar] [CrossRef]

- Balcilar, M.; Gupta, R.; Kyei, C.; Wohar, M.E. Does economic policy uncertainty predict exchange rate returns and volatility? Evidence from a nonparametric causality-in-quantiles test. Open Econ. Rev. 2016, 27, 229–250. [Google Scholar] [CrossRef] [Green Version]

- You, W.; Guo, Y.; Zhu, H.; Tang, Y. Oil price shocks, economic policy uncertainty and industry stock returns in China: Asymmetric effects with quantile regression. Energy Econ. 2017, 68, 1–18. [Google Scholar] [CrossRef]

- Dong, H.; Liu, Y.; Chang, J. The heterogeneous linkage of economic policy uncertainty and oil return risks. Green Financ. 2019, 1, 46–66. [Google Scholar] [CrossRef]

- Beckmann, J.; Czudaj, R.L.; Arora, V. The relationship between oil prices and exchange rates: Revisiting theory and evidence. Energy Econ. 2020. [Google Scholar] [CrossRef]

- Baker, S.R.; Bloom, N.; Davis, S.J. Measuring Economic Policy Uncertainty. Chicago Booth Research Paper No. 13-02; SSRN. 2013. Available online: https://ssrn.com/abstract=2198490 (accessed on 9 October 2019). [CrossRef] [Green Version]

- Baker, S.R.; Bloom, N.; Davis, S.J. Measuring economic policy uncertainty. Q. J. Econ. 2016, 131, 1593–1636. [Google Scholar] [CrossRef]

- Jarque, C.M.; Bera, A.K. Efficient tests for normality, homoscedasticity and serial independence of regression residuals. Econ. Lett. 1980, 6, 255–259. [Google Scholar] [CrossRef]

- Hodrick, R.J.; Prescott, E.C. Postwar US business cycles: An empirical investigation. J. Money Credit Bank. 1997, 24, 1–16. [Google Scholar] [CrossRef]

- Nakajima, J. Time-Varying Parameter VAR Model with Stochastic Volatility: An Overview of Methodology and Empirical Applications. Available online: https://www.imes.boj.or.jp/research/papers/english/11-E-09.pdf (accessed on 9 October 2019).

- Brahmasrene, T.; Huang, J.C.; Sissoko, Y. Crude oil prices and exchange rates: Causality, variance decomposition and impulse response. Energy Econ. 2014, 44, 407–412. [Google Scholar] [CrossRef]

- Kido, Y. On the link between the US economic policy uncertainty and exchange rates. Econ. Lett. 2016, 144, 49–52. [Google Scholar] [CrossRef]

- Troster, V.; Shahbaz, M.; Uddin, G.S. Renewable energy, oil prices, and economic activity: A Granger-causality in quantiles analysis. Energy Econ. 2018, 70, 440–452. [Google Scholar] [CrossRef] [Green Version]

- Huang, Z.H.; Liao, G.K.; Li, Z.H. Loaning scale and government subsidy for promoting green innovation. Technol. Forecast. Soc. Chang. 2019, 144, 148–156. [Google Scholar] [CrossRef]

- Li, Z.H.; Liao, G.K.; Wang, Z.Z.; Huang, Z.H. Green loan and subsidy for promoting clean production innovation. J. Clean Prod. 2018, 187, 421–431. [Google Scholar] [CrossRef]

- Nusair, S.A.; Olson, D. The effects of oil price shocks on Asian exchange rates: Evidence from quantile regression analysis. Energy Econ. 2019, 78, 44–63. [Google Scholar] [CrossRef]

- Bai, J.S.; Perron, P. Estimating and testing linear models with multiple structural changes. Econometrica 1998, 66, 47–78. [Google Scholar] [CrossRef]

- Bai, J.; Perron, P. Computation and analysis of multiple structural change models. J. Appl. Econom. 2003, 18, 1–22. [Google Scholar] [CrossRef] [Green Version]

- Andrews, D.W.K.; Monahan, J.C. An improved heteroskedasticity and autocorrelation consistent Covariance-matrix estimator. Econometrica 1992, 60, 953–966. [Google Scholar] [CrossRef]

- Li, Z.; Liao, G.; Albitar, K. Does corporate environmental responsibility engagement affect firm value? The mediating role of corporate innovation. Bus. Strateg. Environ. 2019. [Google Scholar] [CrossRef]

- Golub, S.S. Oil prices and exchange-rates. Econ. J. 1983, 93, 576–593. [Google Scholar] [CrossRef]

- Yousefi, A.; Wirjanto, T.S. Exchange rate of the US dollar and the j curve: The case of oil exporting countries. Energy Econ. 2003, 25, 741–765. [Google Scholar] [CrossRef]

- Coudert, V.; Couharde, C.; Mignon, V. Does Euro or dollar pegging impact the real exchange rate? The case of oil and commodity currencies. World Econ. 2011, 34, 1557–1592. [Google Scholar] [CrossRef]

- Wen, F.H.; Zhao, Y.P.; Zhang, M.Z.; Hu, C.Y. Forecasting realized volatility of crude oil futures with equity market uncertainty. Appl. Econ. 2019, 51, 6411–6427. [Google Scholar] [CrossRef]

- Kang, W.S.; Ratti, R.A. Oil shocks, policy uncertainty and stock market return. J. Int. Financ. Mark. Inst. Money 2013, 26, 305–318. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Mean | Std.Dev | Skewness | Kurtosis | JB | ADF | |

|---|---|---|---|---|---|---|

| Variable (Level) | ||||||

| Oil_price | 54.585 | 29.131 | 0.456 | 2.149 | 17.307 | −2.307 |

| US_REER | 109.885 | 9.551 | 0.063 | 1.772 | 17.769 | −1.528 |

| Policy_uncertainty | 108.414 | 35.372 | 0.962 | 3.410 | 45.162 | −3.037 ** |

| Variable (volatility term after de-trending by using the Wavelet analysis method) | ||||||

| Oil_price | 0 | 10.605 | 0.410 | 6.284 | 133.670 | −6.013 *** |

| US_REER | 0 | 2.923 | 0.117 | 3.345 | 2.0245 | −5.694 *** |

| Policy_uncertainty | 0 | 21.051 | 1.222 | 4.999 | 116.349 | 10.055 *** |

| Parameter | Mean | Std.Dev | 95% L 1 | 95% U 2 | Geweke 3 | Inef. 4 |

|---|---|---|---|---|---|---|

| 0.0224 | 0.0025 | 0.0182 | 0.0278 | 0.419 | 12.13 | |

| 0.0218 | 0.0024 | 0.0177 | 0.0271 | 0.938 | 15.74 | |

| 0.0741 | 0.0249 | 0.0414 | 0.1371 | 0.806 | 99.22 | |

| 0.0436 | 0.0079 | 0.0311 | 0.0619 | 0.109 | 36.37 | |

| 0.3372 | 0.0812 | 0.2002 | 0.5162 | 0.589 | 68.95 | |

| 0.4130 | 0.0823 | 0.2668 | 0.5880 | 0.780 | 54.50 |

| Specifications | ||||||

|---|---|---|---|---|---|---|

| Tests 1 | ||||||

| 1.313 | 2.336 | 4.524 | 19.578 | 50.672 | 60.303 | 60.303 |

| 3.783 | 1.773 | 3.459 | 3.458 | 0.663 | 60.303 | |

| Number of breaks selected 2 | ||||||

| Sequential | BIC | LWZ | ||||

| 5 | 5 | 4 | ||||

| Estimates with Five Breaks 3 | ||||||

| 1.606 (0.565) | 1.443 (0.620) | 1.841 (1.396) | 1.701 (3.551) | 1.572 (1.066) | 1.496 (1.346) | |

2004M8  | 2007M8 | 2008M10  | 2010M9 | 2014M11 | ||

| (03M11-05M7) | (07M6-08M4) | (06M12-09M3) | (10M7-13M2) | (13M11-15M1) | ||

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, Y.; Failler, P.; Peng, J.; Zheng, Y. Time-Varying Relationship between Crude Oil Price and Exchange Rate in the Context of Structural Breaks. Energies 2020, 13, 2395. https://doi.org/10.3390/en13092395

Liu Y, Failler P, Peng J, Zheng Y. Time-Varying Relationship between Crude Oil Price and Exchange Rate in the Context of Structural Breaks. Energies. 2020; 13(9):2395. https://doi.org/10.3390/en13092395

Chicago/Turabian StyleLiu, Yue, Pierre Failler, Jiaying Peng, and Yuhang Zheng. 2020. "Time-Varying Relationship between Crude Oil Price and Exchange Rate in the Context of Structural Breaks" Energies 13, no. 9: 2395. https://doi.org/10.3390/en13092395