1. Introduction

With the rapid development of economy, China overtook the US as the world’s biggest energy consumer and greenhouse gas (GHG) emitter. About 1.6–2.0 billion m

2 of buildings are constructed every year in China [

1], accounting for about 40% of the world’s total new buildings [

2]. A large amount of GHG will be emitted during the life cycle of buildings, especially in construction and operation stages. In order to achieve the sustainable development of construction, there is a great need to clearly know both the costs and the environment costs of buildings.

At present, there is no common understanding of the concept of environmental cost in the academic circle, and there are still some differences among different research fields. According to United States Environmental Protection Agency (USEPA) [

3], how environmental costs are defined depends on how the information is used. Whether a cost can be defined as environmental cost is not absolute but needs to be considered according to specific research purpose. The definition of environmental costs is more representative in the System of Integrated Environmental and Economic Accounting (SEEA) published by the United Nations Statistics Division (UNSD) in 1993 [

4]. According to the definition, environmental costs consist of two levels: (1) the use and loss value of natural resources in output and final consumption; (2) the impact value of pollution generated by output and consumption activities on environment. In addition, the United States Council on Environmental Quality divides environmental costs into four parts: environmental loss costs, environmental protection costs, environmental affairs costs and environmental pollution elimination costs.

In China, the Research Group on Integrated Environmental and Economic Accounting (Green GDP) proposed in its technical guidance that environmental costs are composed of pollution control costs and environmental degradation costs, among which pollution control costs can be divided into actual pollution control costs and virtual pollution control costs. Based on the definition, the Research Group has conducted a study on China’s green national economic accounts and published a number of studies on China’s environmental economic accounts [

5,

6,

7].

The relationship between environmental performance and economic performance is critical for environmental cost analysis. Several methodologies have been proposed to reveal the relationship, such as life cycle cost analysis (LCCA), whole life cost, eco-cost and eco-efficiency. Usually, the LCCA term implies that environmental costs are not included, as is the case in the similar whole life cost. Eco-efficiency has been proposed as one of the main tools to facilitate the transformation from unsustainable developments to sustainable developments [

8]. It is based on the concept of increasing productivity and reducing economic and environmental performance at the same time [

9,

10]. Eco-efficiency refers to the ratio between the added value of a product (e.g., GDP) and the environmental impacts of the product or service (e.g., SO

2 emissions) [

9,

11]. It has significant implications for environmental management accounting (EMA) system as well as environmental accounting [

10,

12].

Additionally, the environmental costs or eco-cost indicators are used to assess the environmental costs. Eco-costs are a measure to prevent the burden of products by expressing the amount of environmental burden. Vogtländer et al. [

13] used “eco-costs 2007”, an indicator for assessing ecosystem deterioration and human health problems, to compare the environmental impact of bamboo materials with commonly used materials such as timber. Baeza-Brotons et al. [

14] applied eco-costs to evaluate the environmental impacts of cement with and without addition of sewage sludge ash. Kravanja and Čuček [

11] presented a novel indicator called eco-profit, which was defined as the sum of eco-benefit (positive impact of environmental unburdens) and eco-cost (negative impact of environmental burdens).

For the application of environmental cost in civil engineering, only handful of studies can be found. Kendall et al. [

15] proposed an integrated life cycle assessment (LCA) and LCCA model to assess and compare traditional concrete bridges with cement-based composite bridges. The LCCA they calculated includes construction, consumer and environmental costs, reflecting the loss caused by air pollution. Chen [

16] established a life cycle environmental impact cost analysis index system of bridges based on LCCA, calculating life cycle environmental costs of bridges at different stages. The results show that, among all stages, the environmental cost of the material production stage is higher than that of any other stages. A method translating the environmental impact into monetary units was composed by Carreras et al. [

17]. The approach used eco-cost indicators to quantify the cost to prevent a given amount of environmental burden. However, the eco-costs only considered the material consumption and energy consumption. Chou and Yeh [

18] developed a CO

2 emissions evaluation system and an environmental cost calculation method to compare the difference of environmental performance between fully prefabricated and cast-in-situ construction. In their study, CO

2 emissions were simply converted into environmental costs by referencing the profit-seeking enterprise income tax in Taiwan, and the progressive tax rate was used to transform the simulated total CO

2 emissions into environmental cost.

Through literature review, studies of building environmental costs, especially the life cycle environmental costs, are still quite insufficient. At present, several existing issues could complicate these efforts in research on environmental cost in civil engineering. For instance, environmental costs are always underestimated. Additionally, lack of adequate measuring and managing systems of environmental costs is another obstacle [

19]. To overcome this gap, a calculating model for environmental costs of a building throughout life cycle is presented in this paper to obtain total energy consumption and pollutant emission costs of buildings.

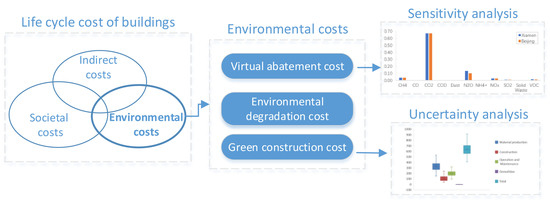

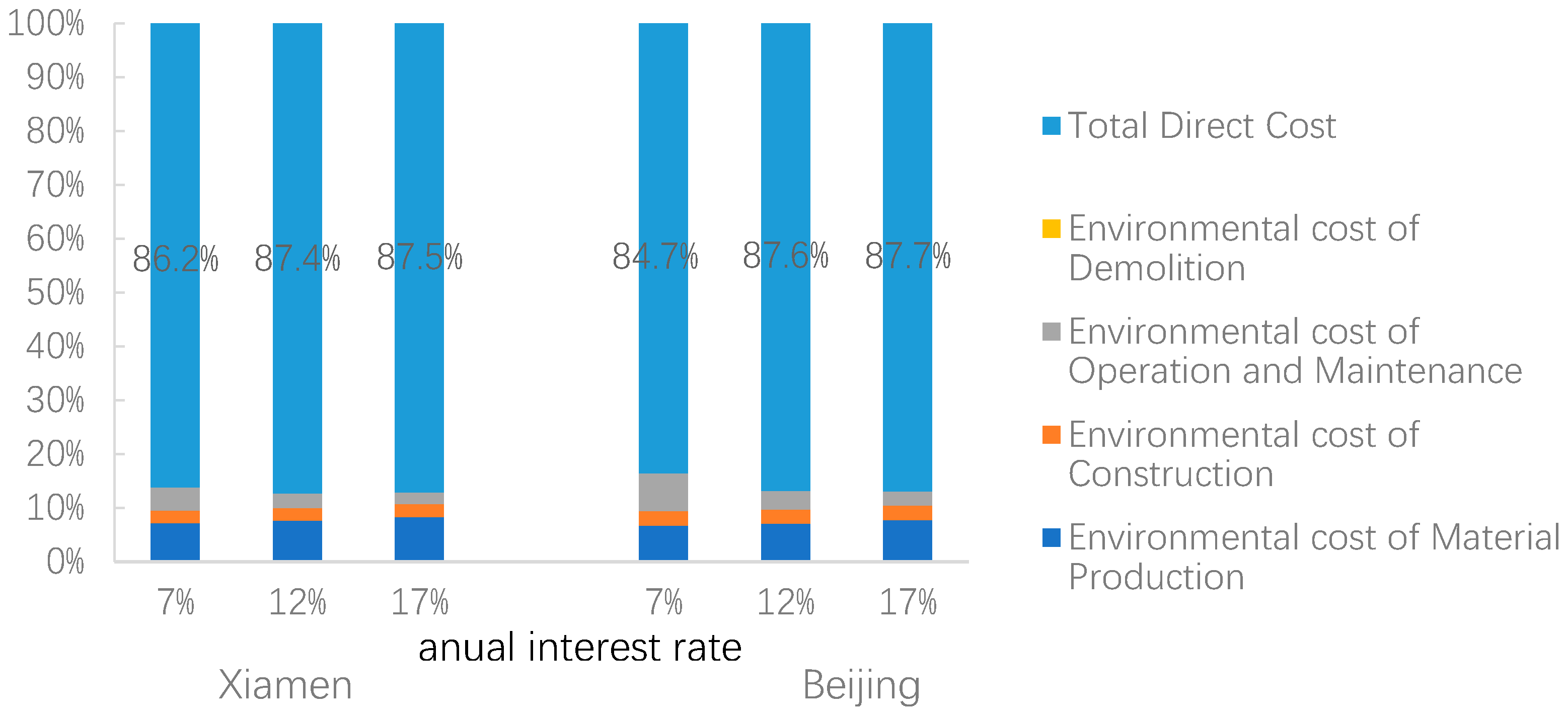

The aim of this paper is to establish a single-objective optimization model by converting environmental impact into environmental cost, with the same unit of direct cost. The following investigations are conducted: (1) Firstly, this study builds an LCA model with all processes; (2) A virtual abatement cost of pollutants and environmental degradation cost according to macroscopic data of environmental economic accounting in China is calculated; (3) The green construction measures fee is incorporated into the environmental cost for the characteristics of building construction; (4) In order to analyze the differences in northern and southern parts of China, two residential buildings, one located in Beijing and the other in Xiamen, China, are taken as case studies; (5) Uncertainty analysis is carried out, including model and data uncertainties to evaluate how these sources of uncertainty may affect the environmental cost results; (6) Finally, sensitivity analysis of the environmental costs is conducted to identify major input variables, including the discount rate and the unit virtual abatement costs of pollutants.

2. Methods

According to the Guideline for Chinese Environmental and Economic Accounting [

5] and the characteristics of construction engineering, the environmental costs of buildings are divided into three parts: (1) green construction measures cost, which refers to the practical costs of protecting the environment during construction stage; (2) virtual abatement costs, which are used to control the emissions of pollutants in the life cycle of buildings, including water pollutants, air pollutants and solid waste pollutants, and where

Cva1,

Cva2 and

Cva3 are the virtual abatement costs of air pollution, water pollution and solid waste pollution, respectively; (3) environmental degradation cost, which is the environmental loss cost caused by the emission and pollution of buildings, where

Ced1,

Ced2 and

Ced3 are the environmental degradation costs of air pollution, water pollution and solid waste pollution, respectively.

The flowchart of the model is demonstrated in

Figure 1. Based on the collected project inventory, three types of environmental pollution including air, water and solid waste pollution will be quantified. Based on the quantified results and the methods proposed in this paper, the virtual abatement costs and environmental degradation costs of the three types of environmental pollution can be obtained. Finally, the total environmental costs of a building will be obtained by adding green construction measures costs of subengineering fees including construction, decoration and erection works.

2.1. Green Construction Measures Cost

The Chinese government has proposed to levy green construction measures costs to improve the energy efficiency of construction. Green construction measures cost (

Cgc) refers to environmental protection fees, which are used to reduce the negative impact of construction and consumption of resources under the condition of ensuring engineering quality and safety. The ratio of green construction measure costs to subengineering fees of an actual engineering project is shown in

Table 1.

2.2. Virtual Abatement Costs

The virtual abatement cost represents the cost of curbing untreated environmental pollutants. Three pollutants categories are included: water pollutants (including COD and ammonia), air pollutants (including SO2, dust, fine particulate matter and NOx) and solid waste pollutants (including household waste in operation stage and building material waste in demolition stage). The virtual abatement cost is calculated based on the quantity of pollutant emissions, i.e., the results of life cycle inventory, and virtual abatement costs of per unit pollutant, which is in accordance with the Guideline for Chinese Environmental and Economic Accounting.

2.2.1. Life Cycle Inventory

The framework selected in this study is in the light of the standards of ISO [

20] and the Society of Environmental Toxicology and Chemistry (SETAC) [

21]. The functional unit is considered as floor area (m

2). The cut-off principle of this study is in reference to previous research [

22]: sorting all the building materials according to their mass, with the cumulative quality accounting for more than 80% of the building materials being taken into consideration.

As the two case studies are located in China, a local LCI database, Chinese Life Cycle Database (CLCD), is preferred. Although the life cycle inventory (LCI) has achieved remarkable process since last decade, the local LCI database is not able to cover all the material. Therefore, the Europe Life Cycle Database (ELCD) [

23] is used to complete the case studies (see

Table 2).

● Material production stage

Pollutant emissions produced in this stage can be calculated based on the bill of material quantities and the life cycle inventory. A proper material loss rate has been considered in the bill of quantities, which references the Quota of Beijing Construction Project [

24].

● Construction stage

The two main sources of pollutant emissions produced in this stage are construction machines and material transportation. Gasoline, diesel and electricity consumed by construction machines are calculated based on National Unified Construction Machinery Quota [

25]. In the light of 2013 Statistical Yearbook of China, the average transportation distance is 181 km [

2]. It is assumed that building materials are transported by trucks. The average fuel consumption level is about 101.78 L/(kt·km) [

13]. The diesel consumption can be calculated as follows:

where

Q is the diesel consumption;

mi is the mass of

-th material;

Li is the transportation distance of

-th material, assumed to be 181 km;

qmi is the average fuel consumption for transporting per unit material, assumed to be 101.78 L/(kt·km).

● Operation stage

Energy consumption during this stage implicates the energy and resources, including electricity, natural gas and water consumption. Since the two case buildings just completed construction, there are no actual maintenance monitoring data. Consequently, the water consumption, electricity consumption and domestic waste production for each person can only be estimated based on the local statistical yearbook [

26,

27], assuming that each family consists of three people. The number of apartments in the two case study buildings is 78 for Xiamen and 100 for Beijing.

Additionally, the pollutant emissions also include household waste, which can be estimated based on household waste of similar commercial buildings per unit time. For residential buildings, the energy consumption and household waste amount are influenced by per capita consumption and living habits, which can be estimated in the light of the statistical yearbook. For regions in northern China, the environmental costs caused by the consumption of coal for heating cannot be ignored.

● Demolition stage

The data about energy consumption of China’s construction in the demolition stage are very scarce. The percentages of landfill, incineration and recycling in this paper are based on the data provided by Fabre [

28], Zeng [

29] and Lei et al. [

30], who collected the current inventory data of construction waste recycle and landfill, mainly considering the resource consumption during recycle and landfill. The inventory data of construction waste is shown in

Table 3.

2.2.2. Virtual Abatement Costs of Pollutants

The virtual abatement costs (

Cva) generated by the air and water pollution generated during the building life cycle can be quantified based on the bill of quantities and life cycle inventory. The formula is as follows:

where

Q1 is the amount of air pollutants, based on LCI;

Q2 is the amount of water pollutants, based on LCI;

cva1 is the unit virtual abatement costs of air pollution (see

Table 4);

cva2 is the unit virtual abatement costs of water pollution (see

Table 5).

2.2.3. Virtual Abatement Costs of Solid Waste

The solid waste produced in the building life cycle is composed of building solid waste and household waste.

● Building solid waste

The recycle rate of building material in China is considerable low. Most of building solid waste is simply treated by depositing or burying in the suburb, which will cause severe environmental pollution during transportation and deposition [

31]. The abatement costs of building solid waste can be calculated as follows:

where

Cva31 is the virtual abatement costs of building solid waste;

Q31 is the total amount of building solid waste;

cva31 is the virtual abatement cost per unit building solid waste. According to the results of pollution loss survey data and System of Integrated Environmental and Economic Accounting (SEEA) of pilot provinces, the general industrial solid waste per unit virtual management cost is 22 CNY/t [

5].

● Household waste

With the development of China’s urbanization, most of household waste is disposed after harmless treatment, instead of directly drained off into the natural environment. The definition of harmless disposal is when advanced technology and scientific technology are used in the treatment of municipal solid waste to reduce the environmental impact of solid waste [

32]. There are mainly three kinds of garbage harmless treatments: landfill, compost and incineration.

With the promotion of household waste treatment technology, some cities have achieved 100% harmless treatment. In this study, it is assumed that no harm will be caused by household waste after harmless treatment, and the environmental degradation costs can be ignored. The virtual abatement costs of household waste can be calculated as:

where

Cva32 is the virtual abatement costs of household waste;

Q32 is the total amount of household waste;

cva32 is the transportation costs of household waste;

Qk is the amount of household waste treated by different technologies;

cvak is the unit virtual abatement costs of each treatment (shown in

Table 6).

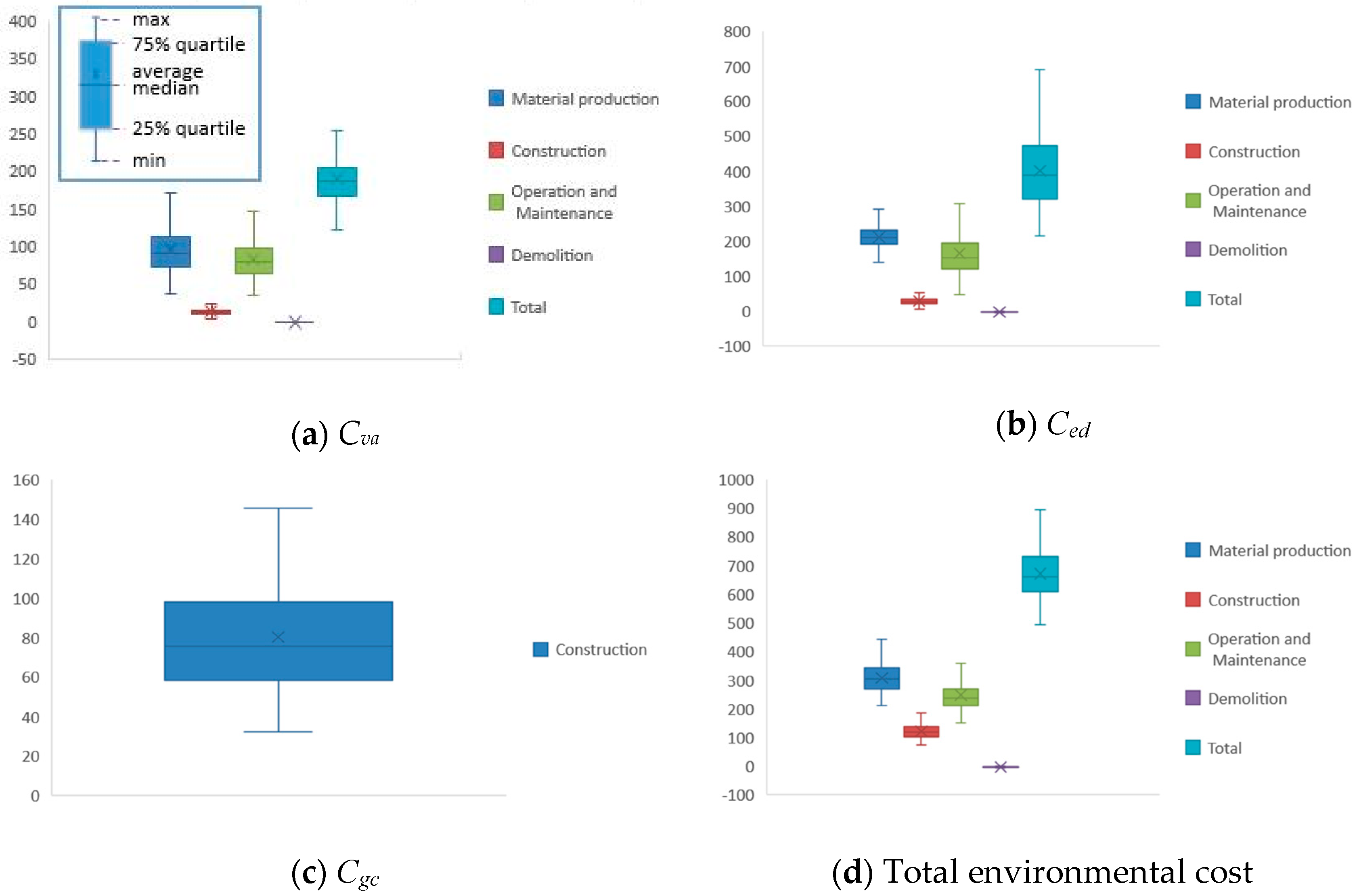

By summing up

Cva1,

Cva2 and

Cva3, the total virtual abatement costs of building can be calculated as follows:

2.3. Environmental Degradation Costs

Environmental degradation cost (Ced) indicates the economic value loss caused by the degradation of environmental functions. The environmental degradation cost is calculated by the pollution loss cost method. The pollution loss cost method requires a specific technical approach to conduct a special survey of pollution losses to determine the monetary value of the impact of pollution emissions on local environmental quality. After quantifying these influences, the environmental degradation costs caused by pollution can be determined.

The Chinese government published the Chinese Environmental and Economic Accounting Report 2004 [

6]. As some local governments firmly opposed publishing the report, after 2008, there are no updated data that can be used to estimate environmental degradation costs.

In order to estimate the environmental degradation costs, a formula was established in the light of the ratio of environmental degradation costs to virtual abatement costs, shown as:

where

Ced is the total environmental degradation costs;

Cvai is the virtual abatement costs of air pollution if

i = 1, or water pollution if

i = 2, or solid waste pollution if

i = 3;

ri is the average ratio of environmental degradation costs to virtual abatement costs, according to the Chinese Environmental and Economic Accounting Report 2004 (see

Table 7),

r1 = 2.25,

r2 = 1.32,

r3 = 0.31.

Based the discussion above, the total life cycle environmental costs can be calculated as:

where

Ce is the total life cycle environmental costs;

Cgc is the green construction measures costs;

Cva is the virtual abatement costs;

Ced is the environmental degradation costs.

Since the time value of money concerns the effect of time and interest rate on monetary amounts, this effect must be given primary consideration in environmental cost [

33]. Present value, also known as present discounted value, is the value of an expected income stream determined at the valuation date. The present value is always less than or equal to the future value due to the potential of interest-earning, which referred to as the time value of money. The most commonly applied model of present valuation uses compound interest.

The present value of the total environmental costs of a building can be expressed as:

where

Cepv is the present value of the total environmental costs;

Cep is the environmental cost of the material production stage;

Cec is the environmental cost of the construction stage;

Ceo is the environmental cost of the operation stage;

Cedem is the environmental cost of the demolition stage;

t1 is the number of annual interest periods during construction stage, assumed to be 2 years;

t2 is the number of annual interest periods during operation stage, assumed to be 50 years;

r is the discount rate, assumed to be 7%;

A is the equal annual payment; (

P|

A,

r,

ti) is the equal-payment-series present-worth factor at time

ti, calculated as

.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}