1. Introduction

The first cryptocurrency, Bitcoin, was developed in 2009 by a person or group of people operating under the pseudonym Satoshi Nakamoto. The 2008 financial crisis underlined the need for an alternative to the traditional banking system, which served as an inspiration for the development of Bitcoin. Ethereum, introduced in 2015 by Vitalik Buterin, pioneered the concept of smart contracts, allowing for the development of decentralized applications on its blockchain. Thousands of alternative cryptocurrencies have subsequently emerged as a result of the success of Bitcoin and Ethereum (

Hyson and Ancrum 2023;

Marr 2017).

Globally, the phenomenon of cryptocurrency is gaining rapid prominence. A cryptocurrency is defined as “any system of electronic money, used for buying and selling online and without the need for a central bank” (

Oxford Learner’s Dictionary 2023c). According to

CoinMarketCap (

2021), in October 2021, there were 13,260 different cryptocurrencies available in the market, with a total market capitalisation of USD 2.5 trillion, having risen from October 2020 when there were 3440 different cryptocurrencies at a market capitalisation of USD 395 billion; and October 2016 when there were 660 different cryptocurrencies with a market capitalisation of USD 13.5 billion. This is evidence of a substantial increase in the number of different cryptocurrencies available over recent years, as well as the volatility in terms of market capitalisation. In addition, interest in cryptocurrencies is increasing, with more and more entities investing in cryptocurrencies (

Abojeib and Ahmed 2018;

Mlambo 2022;

Nurahma 2023;

Raiborn and Sivitanides 2015;

Sundqvist and Hyytiä 2019).

Given the popularity of investment in cryptocurrencies, coupled with the volatile value of the currency and the lack of literature (

Sundqvist and Hyytiä 2019), it has become increasingly important that the appropriate accounting treatment of investments in cryptocurrencies be identified and consistently applied by investing entities (

AASB 2016;

Ernst and Young 2018;

Sundqvist and Hyytiä 2019;

Yilmaz and Hazar 2018). In addition, assurance and advisory firms are likely to experience a growing demand for auditing and advisory services for crypto investments as cryptocurrencies gain greater traction and relevance in the business market.

In the absence of a specific accounting standard applicable to cryptocurrencies, there has been much deliberation by regulatory bodies, such as the International Accounting Standards Board (IASB), on the appropriate accounting treatment of these investments in recent years (

PricewaterhouseCoopers 2019). In June 2019, the IASB concluded that the International Accounting Standard (IAS) 2

Inventory should be employed for the accounting of investments in cryptocurrencies if the cryptocurrencies are held for trading (

IASB 2019;

Ramassa and Leoni 2021). Otherwise, such investments should be recognised and measured using IAS 38

Intangible Assets (

IASB 2019;

Ramassa and Leoni 2021). Stakeholders have been questioning whether the IASB’s proposed accounting treatment does indeed provide relevant information that faithfully represents the underlying economic phenomenon of cryptocurrencies, resulting in decision-useful information (

Fourie 2018;

IFRS 2019a), and previous studies and stakeholders (

AASB 2016;

Grant Thornton 2018;

Mlambo 2022;

Procházka 2018;

Ramassa and Leoni 2021;

Yatsyk and Shvets 2020) have criticised the IASB’s guidance on accounting for cryptocurrencies.

In the third agenda consultation of the IASB of March 2021 (

IASB 2021), cryptocurrencies were again included as a discussion point. As cryptocurrencies and the holding thereof by entities having to prepare financial statements become more prevalent, the guidance of either applying IAS 2 or IAS 38 will, in all likelihood, have to be revisited. This is due to the very individual nature of cryptocurrencies, which is not necessarily being addressed adequately by the measurement principles in IAS 2 and IAS 38. The Accounting Standards Board of Japan has, for example, concluded that there is currently no category of assets which can satisfactorily be applied to cryptocurrencies. Consequently, the board has decided that such virtual currencies will be treated as a totally separate category of assets (

Yatsyk 2018).

At present, there is uncertainty about the most appropriate accounting treatment of investments in cryptocurrencies based on a lack of concrete existing guidance (

PricewaterhouseCoopers 2019). This could result in different interpretations and applications by various role players and businesses, leading to possible errors, whether inadvertent or intentional, in preparing financial statements (

AASB 2016;

Sundqvist and Hyytiä 2019).

Accounting research cannot be conducted without integrating theory into the study (

Mouton 1996;

Van der Schyf 2008). Existing accounting research omits to include the main element of scholarly activity in accounting, namely accounting theory (

Van der Schyf 2008). In practice, accountants have further been criticised for failing to understand accounting theory and for applying accounting practices without questioning the underlying theory (

Deegan and Unerman 2006). Understanding the structure of accounting theory, from which the accounting techniques are derived, is just as important for accountants as understanding the accounting techniques themselves (

Riahi-Belkaoui 2004). Despite the literature’s emphasis on the value of accounting theory in the process of scholarly accounting activity (

Deegan and Unerman 2006;

Inanga and Schneider 2005;

Van der Schyf 2008), no research addressing the problem of cryptocurrencies using accounting theory could be found. This emphasises the need for the current study.

The aim of this study was twofold. Firstly, the research aimed to determine the most appropriate accounting treatment for investments in cryptocurrencies, based on the IASB’s Conceptual Framework for Financial Reporting (as a form of accounting theory) that results in useful information for users of financial statements for decision-making. Secondly, the research investigated the proposed accounting treatment in terms of International Financial Reporting Standards (IFRS) and sought to determine whether this treatment is aligned with the IASB’s conceptual framework.

This study aimed to make both a theoretical and a practical contribution. The research contributes to the existing theoretical financial reporting body of knowledge by responding to

Van der Schyf’s (

2008) call for the addressing of accounting research problems by making use of accounting theory. The research also makes a practical contribution by assisting stakeholders to understand the theory behind the practice of accounting for cryptocurrencies.

Moreover, by addressing the problem of accounting for cryptocurrencies with the novel reference to accounting theory, this study could reduce uncertainty among entities investing in cryptocurrencies as these entities will have clear guidance on how to faithfully account for and present such investments in their financial statements. With the guidance provided by this study, auditors will be able to assess whether appropriate accounting has been applied to cryptocurrency investments in the financial records of their clients. It will be beneficial for the accounting profession if a consistent accounting treatment is available for cryptocurrency investments, thus ensuring comparable information across entities.

4. The Accounting Treatment Determined Using the IASB’s Conceptual Framework

In terms of IAS 8

Accounting Policies, Changes in Accounting Estimates and Errors, if an IFRS specifically applies to a transaction, other event or condition, the accounting policy or policies applicable to an item must be established by the application of the applicable IFRS (

IASB 1993a). There is, however, currently no IAS or IFRS specifically governing the accounting of cryptocurrencies. IAS 8 further determines that should there be no IFRS specifically applicable to a transaction, other event or condition, the management of the business in question should apply their own judgement to develop and apply an accounting policy that will result in relevant and reliable information for financial statement preparation purposes (

IASB 1993a). In this regard, another established standard might be applicable and include the relevant cryptocurrencies within its scope for the classification, recognition and measurement thereof.

The extract from IAS 8 in the previous paragraph correlates with one of the listed purposes of the IASB’s conceptual framework, i.e., to “assist preparers to develop consistent accounting policies when no Standard applies to a particular transaction or other event, or when a Standard allows a choice of accounting policy” (

IASB 2018). Therefore, in the absence of clear guidance, the conceptual framework can provide the theory (set of principles) to assist preparers in developing consistent accounting policies for accounting for investments in cryptocurrencies (

IASB 2018).

A prescriptive accounting theory describes what financial accounting

should be in terms of recognition and measurement (for example, when considering what items should be classified as assets, liabilities, income and expenses and their corresponding values). The conceptual framework can be reckoned as a prescriptive accounting theory (

Deegan and Unerman 2006;

Vorster 2007) since it seeks to provide a set of principles (

Alexander et al. 2005) that should be applied when accounting for a given phenomenon. The IASB’s conceptual framework will therefore be applied as the appropriate and relevant accounting theory in this study. Other research studies in accounting (

Brink and Steenkamp 2023;

Lamprecht 2016;

Oberholser 2013;

Scheepers 2013) also identified the IASB’s conceptual framework as the relevant accounting theory to apply in addressing an accounting issue. According to

Tan and Low (

2017) and

Ram et al. (

2016), the IASB’s conceptual framework could be used to determine the appropriate accounting treatment of cryptocurrencies.

To determine the accounting treatment of investments in cryptocurrencies based on accounting theory, the definitions, recognition criteria, and measurement bases of the IASB’s conceptual framework should be considered. The conceptual framework defines an asset as “a resource controlled by the entity as a result of past events and from which future economic benefits are expected to flow to the entity” (

IASB 2018). With respect to an entity holding cryptocurrencies, the

past event requirement is met by the fact that the entity bought the cryptocurrencies. The entity can be said to

control the resource, as the entity will hold the power to decide when to sell the digital currency unit. Should the entity subsequently sell the cryptocurrencies, this will result in the

expectation of future economic benefits for the entity (

Venter 2016). This stance was supported by the IFRS discussion group meeting, where a consensus was reached that cryptocurrencies are an asset (

IFRS 2018). The increase or decrease in the price of cryptocurrencies does not place a proviso on the classification of cryptocurrencies as an asset (

Ahmed 2017). Cryptocurrencies, therefore, meet the requirements of the definition of an asset.

The asset can be recognised if it provides information that is useful (relevant and faithful) (

IASB 2018). There is a certainty that the asset exists, and the probability of an inflow of economic benefits is high, meaning that relevant information will be provided by recognising the asset (

IASB 2018). Faithful representation (one of the fundamental qualitative characteristics of useful financial information) is affected by measurement uncertainty (

IASB 2018), but it is not expected that the measurement uncertainty would be so extreme as to prohibit the recognition of the asset.

Chapter 6 (Measurement) of the IASB’s conceptual framework covers measurement bases that can be applied when recognising elements in financial statements. This chapter details possible measurement bases to apply and factors to consider when deciding on an appropriate measurement basis. When deciding on the most appropriate measurement basis, the qualitative characteristics of useful financial information, as well as the consideration of any cost constraint, are considered (

IASB 2018). The conceptual framework provides for two alternative measurement bases, historical cost and current value. When applying the historical cost measurement basis, the monetary value of an asset is based on the price of the underlying transaction that gave rise to the asset (

IASB 2018). The consideration paid, plus any related transaction cost to acquire an asset, depicts its historical cost (

IASB 2018). The current value measurement basis reflects any changes in values on the underlying premise that the value presented takes into account conditions on the applicable measurement date (

IASB 2018). Fair value, value in use and current cost are possible measurement bases when the current value is applied to an asset (

IASB 2018). From an asset perspective,

fair value represents the price that would be received when selling an asset (

IASB 2018), whereas

value in use reflects the present value of future economic benefits or cash flows obtained from the continued use of an asset, as well as from its disposal (

IASB 2018). Current cost applies where there is a similar asset in the market, and the current cost will then represent the cost of that particular asset on the measurement date (

IASB 2018).

Certain information about the investment in cryptocurrencies is provided by the measurement basis—either information relating to historical cost or information relating to the current value of the cryptocurrencies. If more than one measurement basis can be used, it needs to be decided which measurement basis offers the most relevant information (predictive and confirmatory relevance) regarding the financial position and performance and ensures the most faithful representation (i.e., information that is complete, neutral and free from measurement error). When selecting a measurement basis for the asset, it is important to consider the economic phenomenon of the transaction, including the characteristics of the asset and the estimated future cash flows (

IASB 2018).

Cryptocurrencies can be bought on an exchange platform. The historical cost is evidenced by the consideration that the holder paid for the cryptocurrency, as well as any related transaction costs. Considering the economic phenomenon under study, the entity’s intention is eventually to sell the cryptocurrency either over the short term in the normal course of business or over the long term where the cryptocurrency is held for capital growth, both resulting in a future cash inflow.

Cryptocurrencies are extremely volatile, with market prices fluctuating daily (

Yatsyk and Shvets 2020), so whether cryptocurrencies are held for short-term or long-term purposes, the historical cost would differ from their current value after initial recognition. The historical cost does not take into account any future changes in the value of the asset held, which is considered to be important information to the users of the financial statements. Moreover, if the historical cost is used, changes in value are only reported when selling the cryptocurrencies. This could be misinterpreted as implying that all the income and expenses recognised at the time of disposing of the cryptocurrencies arose then rather than over the periods during which the cryptocurrencies were held (

IASB 2018). Additionally, because measurement at historical cost does not provide timeous information about changes in value, income and expenses reported on that basis may lack predictive value and confirmatory value by failing to adequately reflect the effect of the entity’s exposure to risk associated with holding the cryptocurrency during the reporting period (

IASB 2018). The conceptual framework also recommends measuring assets that produce cash flows directly, as is the case with cryptocurrencies, at current value. Current value incorporates current estimates of the amount, timing and uncertainty of the future cash flows, resulting in the most relevant information (

IASB 2018).

The current value measurement basis is therefore deemed to be the most appropriate basis to apply when recognising cryptocurrencies (as was also concluded by

Fourie (

2018)). Given the volatile nature of cryptocurrencies, the current value measurement basis will more aptly represent the true value of the cryptocurrencies on the financial reporting (measurement) date, resulting in more relevant information and a faithful representation. It needs to be determined which current value measurement basis will provide the most relevant and faithful representation: the fair value, the value in use, or the current cost?

In terms of fair value, cryptocurrencies will be measured at the value that would be received when the cryptocurrencies are sold in an orderly transaction between market participants (

IASB 2018). The fair value model reflects the perspective of market participants and thus represents an exit price for the entity. The fair value does not take into account the transaction costs involved in disposing of the asset (

IASB 2018), which are negligible when acquiring or disposing of cryptocurrencies (

Fourie 2018;

Francis 2023).

The value-in-use measurement basis is usually applied in scenarios where the asset is used to generate cash flows or other economic benefits (

IASB 2018). Cryptocurrencies are, however, not an asset that will be used by the entity to generate cash flows or other economic benefits—they do not have the ability to generate cash inflows while they are held; for example, no rental or dividend income can be received. Cryptocurrencies are also not an asset that can be used in the production of goods and services. Therefore, the value-in-use measurement basis is not regarded as an appropriate measurement basis for cryptocurrencies. If the current cost basis is applied, cryptocurrencies will be measured at the cost of an equivalent cryptocurrency which includes the amount that would be paid by the entity, including the transaction costs incurred at the measurement date (

IFRS 2018)—thus, representing an entry price as opposed to the fair value which represents an exit price. Current cost provides information about the cost of an asset consumed, and since cryptocurrencies are not an asset consumed by the entity, this might not be an appropriate measurement basis. In addition, selling cryptocurrencies does not involve the use of several economic resources, and measuring the cryptocurrencies at current cost is therefore not recommended (

IASB 2018).

Changes in the fair value of an asset reflect changes in the expectations of market participants and changes in their risk preferences (

IASB 2018). When an entity plans to sell an asset, measurement at fair value is appropriate as the information reflects those changes providing predictive value or confirmatory value to users of financial statements. Fair value will provide the users of the financial statements with insight into the current expectations of market participants about the amount, timing, and uncertainty of future cash flows of the underlying item resulting in relevant information (

IASB 2018). The fair value of cryptocurrencies will be determinable because an active market exists for most of the major cryptocurrencies, such as Bitcoin (

Grant Thornton 2018;

Procházka 2018). However, for some lessor-known cryptocurrencies, an active market might not exist (

Grant Thornton 2018;

Procházka 2018), and the fair value must be estimated. When a measure cannot be determined directly and must instead be estimated, measurement uncertainty arises that, in turn, affects faithful representation (

IASB 2018). However, if a measurement basis offers relevant information, which is the case when using the fair value basis, measurement uncertainty does not preclude the use of that measurement basis (

IASB 2018). Moreover, this uncertainty can be mitigated through proper disclosure of the estimation technique applied in the annual financial statements. It can therefore be concluded that the fair value measurement basis will provide a faithful representation of the cryptocurrency transaction. Thus, the fair value measurement basis can be selected as the most appropriate measurement basis for measuring the investment in cryptocurrencies for both intentions (namely, either to sell the cryptocurrencies over the short term, where cryptocurrencies are held for trading, or to sell the cryptocurrencies over the long term, where the cryptocurrencies are held for capital growth) of the entity.

Fourie (

2018) also recommended using the fair value measurement basis of the conceptual framework to measure investments in cryptocurrencies.

In addition to being relevant and faithfully presented, the information should be, as far as possible, comparable, verifiable, timely and understandable (

IASB 2018). Fair value is not determined from an entity-specific perspective but rather from the perspective of market participants and is independent of when the asset was acquired. Cryptocurrencies measured at fair value are measured at the same amount by entities that have access to the same markets. This can improve comparability both from period to period for a reporting entity and in a single period across entities (

IASB 2018). If the fair value of an asset can be determined directly by observing prices in an active market, as would be the case for most cryptocurrencies, the process of fair value measurement is low-cost, simple and easy to understand, and the fair value can be verified through direct observation. At initial recognition, the cost of cryptocurrencies acquired is, in most cases, equal to their fair value at that date (for cryptocurrencies in an active market). The conceptual framework determines that if a current value measurement basis is used for subsequent measurement, it is also normally appropriate for initial recognition (

IASB 2018). The fair value measurement basis can therefore be applied for initial and subsequent measurement.

5. Comparing the IASB’s Proposed Accounting Treatment under IFRS with the Conceptual Framework

The accounting treatment based on the IASB’s conceptual framework provides a strong foundation against which different suggested IFRS accounting treatments for cryptocurrencies can be evaluated. This section starts by explaining the IASB’s proposed accounting treatment in terms of IFRS. The accounting treatments as inventory (IAS 2) and intangible asset (IAS 38) are discussed separately. Thereafter, the IASB’s proposed accounting treatment is compared with the accounting treatment determined in the previous section, when only the conceptual framework was considered.

5.1. Inventory

IAS 2 defines inventory as “assets: (a) held for sale in the ordinary course of business; (b) in the process of production for such sale; or (c) in the form of materials or supplies to be consumed in the production process or in the rendering of services” (

IASB 1993b). IAS 38 specifically excludes “intangible assets held by an entity for sale in the ordinary course of business”. Such assets should be treated in accordance with the requirements as appropriate in terms of IAS 2 (

IASB 1998a).

As cryptocurrencies are not objects that are produced or used as material or supplies for a production process, they must be held for sale in the ordinary course of business to be able to classify as inventory. Should an entity, therefore, purchase cryptocurrencies with the pure intention of selling them as part of their ordinary business proceedings, they meet the definition of inventory, and IAS 2 would apply.

According to IAS 2, inventory should be measured at the lower of cost or net realisable value (the estimated selling price less costs to sell) (

IASB 1998a). In applying IAS 2 with reference to the IASB’s conceptual framework, cryptocurrencies should be measured at whichever is the lower value between historical cost and fair value (taking into account that transaction costs are negligible). Therefore, if the fair value exceeds the historical cost, such an adjustment will not be accounted for. As the market prices of cryptocurrencies are extremely volatile, this raises the concern as to whether the application of the measurement in terms of IAS 2 will result in useful information for users for decision-making (

Fourie 2018;

Mlambo 2022;

Williamson 2018;

Yatsyk and Shvets 2020). The alternative is to measure the cryptocurrencies at fair value, less costs to sell in terms of IAS 2 (

Morozova et al. 2020).

IAS 2 par. 3(b) determines that the stipulations of the standard do “not apply to the measurement of inventories held by commodity broker-traders who measure their inventories at fair value less costs to sell”.

IASB (

1993b) further indicates that:

(b)roker-traders are those who buy or sell commodities for others or on their own account … (Such inventories) are principally acquired with the purpose of selling in the near future and generating a profit from fluctuations in price or broker-traders’ margin. When these inventories are measured at fair value less costs to sell, they are excluded from only the measurement requirements of this Standard.

To be able to meet the abovementioned scope exclusion, cryptocurrencies must, therefore, first be included as a

commodity. The

Oxford Learner’s Dictionary (

2023b) defines a commodity as “a product or a raw material that can be bought and sold”. According to

Prentis (

2015), cryptocurrencies are seen as functioning for a user as a means of obtaining something that the user wants to acquire. Within such a scope of users, cryptocurrencies, therefore, perform the role of money, and consequently, cryptocurrencies should be seen as a commodity (

Deloitte 2018;

Prentis 2015). In 2015, the Commodities Futures Trading Commission in America designated Bitcoin as a commodity (

Hussey 2020), it being a commodity in terms of the Commodity Exchange Act (

United States Commodity Futures Trading Commission 2019). Given their extreme price volatility, cryptocurrencies further lend themselves to futures trading, akin to commodities. This, therefore, supports the perception of cryptocurrencies as a commodity.

Procházka (

2018) further concluded that cryptocurrencies should be treated as commodities held by broker-traders.

If cryptocurrencies are held for trading purposes, they fall under the scope of IAS 2 in terms of the recognition of the cryptocurrencies. However, as cryptocurrencies are perceived as a commodity, the entity holding the cryptocurrencies for trading purposes is a broker-trader, and IAS 2 par. 5 is applicable, henceforth excluding the cryptocurrencies from the measurement principles, as stipulated in IAS 2. Under the broker-trader caveat, the cryptocurrencies are measured at fair value less costs to sell, with any changes in the fair value accounted for in profit or loss. This eliminates the foreseen impracticality of applying IAS 2 par. 9 (measuring at the lower of cost and net realisable value).

The

recognition of cryptocurrencies as an asset under IAS 2 aligns with the application of the IASB’s conceptual framework. The

measurement of cryptocurrencies under IAS 2 at fair value less costs to sell also aligns with the application of the conceptual framework measuring the asset at fair value since little to no transaction costs are related to selling cryptocurrencies (

Fourie 2018;

Francis 2023).

Should an entity, however, hold cryptocurrencies for another purpose, such as capital appreciation, the scope of IAS 2 is not applicable, as cryptocurrencies do not meet the definition of an inventory item. In such instances, cryptocurrencies are accounted for in terms of IAS 38.

5.2. Intangible Asset

In terms of IAS 38, an intangible asset is “an identifiable non-monetary asset without physical substance” (

IASB 1998a).

IASB (

1998a) further states that:

An asset is identifiable if it either: (a) is separable, i.e., is capable of being separated or divided from the entity and sold, transferred, licensed, rented or exchanged, either individually or together with a related contract, identifiable asset or liability, regardless of whether the entity intends to do so; or (b) arises from contractual or other legal rights, regardless of whether those rights are transferable or separable from the entity or from other rights and obligations.

IAS 32 Financial Instruments: Presentation par. 13 states that contractual refers to:

An agreement between two or more parties that has clear economic consequences that the parties have little, if any, discretion to avoid, usually because the agreement is enforceable by law. Contracts, and thus financial instruments, may take a variety of forms and need not be in writing.

Irrespective of the purpose for which cryptocurrencies are held, this does not give the entity holding them a contractual right “to receive cash or another financial asset; or to exchange financial assets or financial liabilities with another entity under conditions that are potentially favourable to the entity” (

IASB 1995). Cryptocurrencies can be seen as analogous to gold bullion as per the IFRS 9

Financial Instruments Guidance on Implementing, which states that irrespective of the fact that gold bullion is highly liquid, it does not represent a contractual right to receive cash or another financial asset inherent in the gold bullion (

IASB 2014).

As discussed in the previous paragraph, cryptocurrencies do not result in a contractual right for an entity and, therefore, to meet the

identifiable condition, the asset must be separable from the entity. Cryptocurrencies enable the entity to trade the cryptocurrencies on a relevant exchange (

Grant Thornton 2018). It can therefore be concluded that the cryptocurrencies are separable from the entity and consequently meet the first proviso of the intangible asset definition, which is that it must be

identifiable.

A monetary asset is defined as “money held and assets to be received in fixed or determinable amounts of money” (

IASB 1998a). Cryptocurrencies do not meet the definition of money (

Procházka 2018) as cryptocurrencies are not currently regulated by any government or legal entity and are not widely accepted as a medium of exchange (

Abojeib and Ahmed 2018;

Fourie 2018;

Smith et al. 2019). The IFRS Interpretations Committee also maintains that a holding in cryptocurrencies is non-monetary (

IASB 2019). This is based on the fact that the holding does not entitle the holder to receive a fixed or determinable number of units of currency. Furthermore, the supply and demand in the market within which the cryptocurrencies trade will dictate the price thereof (

Luno 2017). Since the value of cryptocurrencies fluctuates constantly and is very volatile, the value is not fixed or determinable. By the exclusion of cryptocurrencies from the scope of a monetary asset, cryptocurrencies are a non-monetary asset. This is further supported by IAS 21

The Effects of Changes in Foreign Exchange Rates par. 16, which states that “the essential feature of a monetary item is a right to receive (or an obligation to deliver) a fixed or determinable number of units of currency” (

IASB 2003).

The final requirement to meet the definition of an intangible asset is that the cryptocurrencies must have no physical substance. Cryptocurrencies are not physical coins but rather a “unique chain of digital signatures that are stored in a digital wallet installed on the user’s computer” (

Bjerg 2016). As cryptocurrencies are digital currencies in a virtual network, they have no physical substance. Cryptocurrencies, therefore, meet the definition of an intangible asset—as also concluded by

Abojeib and Ahmed (

2018) and

Fourie (

2018).

Even though, from a technical perspective, cryptocurrencies meet the definition of an intangible asset, as discussed in the previous paragraphs, they do not possess the nature and underlying economic characteristics of intangible assets (

Procházka 2018). Conventional items falling within the ambit of IAS 38 are computer software, patents and licences, to name but a few (

IASB 1998a). The manner of utilisation of these items is vastly different from that of cryptocurrencies and raises the question of whether such classification and consequent application of the implied measurement principles will satisfactorily meet the purpose of financial statements, especially when cryptocurrencies become more prevalent and are a material holding for entities. According to

Retief (

2018), the main purpose of intangible assets is to generate economic benefits in the ordinary course of an entity’s business. In a general context, cryptocurrencies are, however, held for investment purposes (when applying IAS 38) with the intent of capital appreciation, and consequently, the intended use can be argued as being vastly different.

If IAS 38 is applied to cryptocurrencies as recommended by the IASB, after initial recognition at cost price, the entity will have to determine an accounting policy of either the cost model or the revaluation model (

IASB 1998a). In terms of the cost model, the cryptocurrencies will be accounted for at their cost less any accumulated amortisation and any accumulated impairment losses (

IASB 1998a).

Keeping in mind that the reason for classification in terms of IAS 38 is that the purpose of holding cryptocurrencies is for capital appreciation purposes, the value and practicality of using the cost model as accounting policy is questionable. Accounting for cryptocurrencies in accordance with the cost model, any growth will not be evident from viewing the financial statements because—irrespective of the escalation of the value of the asset—the cryptocurrencies will merely be stated and reflected at their cost. This is not practical for the users of financial statements who would ultimately view the statements to obtain an understanding of the current financial position of the entity. The financial position would not be evident if the value of the cryptocurrencies showed significant growth and especially if cryptocurrencies constituted a crucial proportion of the entity’s assets. This results in concerns as to whether accounting for investment in cryptocurrencies as intangible assets, in terms of the cost model, would result in useful information to users of financial statements for decision-making.

The alternative accounting policy option under IAS 38 is the revaluation model. Under this model, cryptocurrencies must be accounted for at their fair value on the determined date of revaluation, less any subsequent accumulated amortisation and any subsequent accumulated impairment losses (

IASB 1998a). Under both the cost and the revaluation model, this immediately begs the consideration of an applicable amortisation period for the cryptocurrencies. Generally, the nature and characteristics of cryptocurrencies are such that they do not have an expiry date and there is no curtailment on the extent to which they can be used (

Sterley 2019). Cryptocurrencies will therefore be represented best in the financial statements as having an indefinite useful life (

Abojeib and Ahmed 2018;

Procházka 2018). Intangible assets with indefinite useful lives are not amortised but must be tested for impairment if there is an indication of impairment or annually, irrespective of whether there is any such indication (

IASB 1998a). Such impairment tests are done in terms of IAS 36

Impairment of Assets and any resulting impairment loss will be recognised in profit or loss (

IASB 1998b).

An impairment will be recognised if the carrying amount exceeds the recoverable amount, being the highest amount between the fair value minus costs to sell and the value in use (i.e., the present value of the future cash flows expected to be derived from the asset) (

IASB 1998b). In the case of cryptocurrencies initially measured at historical cost (which equals the fair value) and subsequently measured at fair value, an impairment loss would only be recognised if the recoverable amount is less than the fair value (carrying amount). The fair value (carrying amount) and the fair value minus the costs to sell (taken into account for determining the recoverable amount) would be very similar since transaction costs are negligible (

Fourie 2018;

Francis 2023). If the value in use exceeds the fair value minus the costs to sell, the fair value (carrying amount) would not exceed the recoverable amount, and there would be no impairment loss. An impairment loss would, therefore, only be recognised for cryptocurrencies if there is a decrease in fair value minus the costs to sell, and the cryptocurrencies would either be measured at fair value or fair value minus the costs to sell.

If the entity’s accounting policy choice is the revaluation model, the fair value of the cryptocurrencies must be determined in accordance with IFRS 13

Fair Value Measurement. IFRS 13 par. 9 defines fair value as “the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date” (

IASB 2011). An active market should therefore be prevalent for this accounting policy choice to be viable. Appendix A of IFRS 13 defines an active market as one “in which transactions for the asset or liability take place with sufficient frequency and volume to provide pricing information on an ongoing basis” (

IASB 2011). Generally, intangible assets will not have an active market, but IAS 38 par. 78 cites examples such as production quotas or transferable licences for which an active market may exist. Beyond the definition, no other guidance is provided in terms of what would satisfactorily constitute an active market, and therefore each entity should apply its own judgement in the accounting policy choice and determination of the existence of an active market based on the cryptocurrencies held by them (

Grant Thornton 2018).

Certain cryptocurrencies, for example Bitcoin, see considerable daily trading, therefore, an active market is evident. There, however, are other lesser-known cryptocurrencies that might not satisfy “providing pricing information on an ongoing basis” as stipulated by the definition of an active market (

Deloitte 2018). In such cases, the fair value of the cryptocurrencies needs to be estimated. Given the extensive volatility in the price of cryptocurrencies, the revaluation will most likely have to take place annually for the fair value to not materially differ from the carrying amount at the reporting date, as required by IAS 38 par. 79. Any fair value adjustment as a result of the revaluation must be recognised in other comprehensive income (

IASB 1998a).

The

recognition of cryptocurrencies as an asset under IAS 38 aligns with the application of the IASB’s conceptual framework. In terms of IAS 38, revaluation model cryptocurrencies are measured at fair value less accumulated impairment losses

1. An impairment loss is only recognised for the difference between the fair value and the fair value less costs to sell. Cryptocurrencies are, therefore, subsequently measured at fair value less costs to sell. The

measurement of cryptocurrencies under IAS 38 at fair value less costs to sell aligns with the application of the IASB’s conceptual framework measuring the asset at fair value since little to no transaction costs are related to selling cryptocurrencies (

Fourie 2018;

Francis 2023).

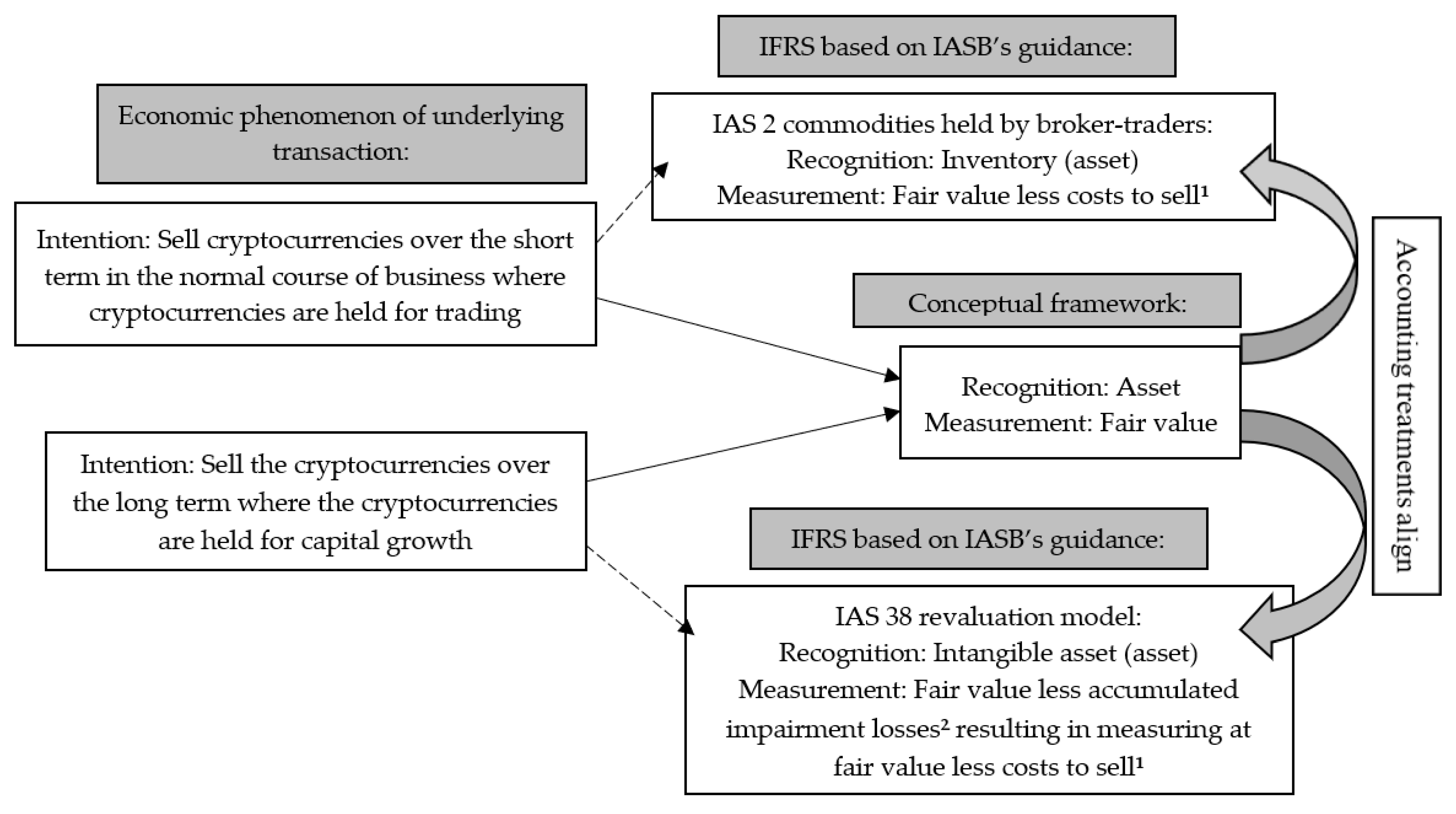

Figure 1 summarises the comparison of the accounting treatments as per the conceptual framework and the guidance provided by the IASB for the economic phenomenon of the underlying transaction.

In concluding the findings of this study: It was found that cryptocurrencies meet the definition and recognition criteria of an asset in terms of the conceptual framework. The economic phenomenon of the transaction indicates that an entity holding an investment in cryptocurrencies can have one of two intentions, namely either to sell the cryptocurrencies over the short term, where cryptocurrencies are held for trading, or to sell the cryptocurrencies over the long term where the cryptocurrencies are held for capital growth. Given the volatile nature of cryptocurrencies, the current value measurement basis will best represent the true value of the cryptocurrencies on the measurement date, whether the cryptocurrencies are held for trading or for capital growth. More specifically, the fair value measurement basis, which is based on market participant assumptions, was regarded to be the most appropriate measurement basis for cryptocurrencies resulting in the most relevant information and ensuring the most faithful representation.

Comparing the IASB’s guidance to account for cryptocurrencies in terms of IAS 2 if the cryptocurrencies are held for trading or in terms of IAS 38 if cryptocurrencies are held for capital growth with the conceptual framework, the following was found. The

recognition of cryptocurrencies as an asset under IAS 2 and IAS 38 aligns with the application of the conceptual framework. In terms of IAS 2 commodities held by broker-traders, cryptocurrencies will be measured at fair value less costs to sell. In terms of the IAS 38 revaluation model, cryptocurrencies will be measured at fair value less accumulated impairment losses.

2 An impairment loss would only be recognised for the difference between the fair value and the fair value less costs to sell. Cryptocurrencies would therefore be measured at fair value, less costs to sell. The

measurement of cryptocurrencies at fair value less costs to sell under IAS 2 and IAS 38 also aligns with the application of the conceptual framework measuring the asset at fair value since little to no transaction costs are related to selling cryptocurrencies. However, when cryptocurrencies are not accounted for under the IAS 2 measurement scope exclusion (therefore measuring at the lower of cost or net realisable value) and when the IAS 38 cost model is applied, the accounting treatment will not align with the conceptual framework.

6. Conclusions

Currently, there is uncertainty about the most appropriate accounting treatment for investments in cryptocurrencies owing to a lack of concrete, existing guidance. Even though the literature has emphasised the importance of considering accounting theory in the process of scholarly activity in accounting, accounting theory has not been considered in addressing the research problem of accounting for cryptocurrencies prior to this study. The aim of this research was, therefore, to determine the most appropriate accounting treatment for cryptocurrencies based on the IASB’s Conceptual Framework for Financial Reporting (as a form of accounting theory) that produces useful information for users of financial statements for decision-making. The research also investigated the proposed accounting treatment in terms of IFRS and sought to determine whether this treatment is aligned with the IASB’s conceptual framework.

When uncertainty about an accounting treatment persists even after the IASB has issued guidance, one must question whether the guidance is in line with the concepts that underlie the preparation and presentation of financial statements (i.e., the IASB’s conceptual framework). In terms of the IASB’s conceptual framework, an investment in cryptocurrencies (held for trading or for capital growth purposes) should be accounted for as an asset measured at fair value. This accounting treatment aligns with the accounting treatment suggested by the IASB, but only in specific scenarios, namely under IAS 2, when accounted for as commodities held by broker-traders, and under IAS 38 applying the revaluation model. The reason uncertainty persisted might be due to the guidance provided by the IASB being vague, limited and with no clear link to the concepts that underlie the preparation and presentation of financial statements.

The scope of this study excluded the accounting of cryptocurrencies by miners of cryptocurrencies. As an area for future research, accounting theory can be applied to determine an appropriate accounting treatment for mentioned cryptocurrencies. In addition, it is recommended that the accounting treatment of other digital assets, for example, crypto tokens that operate on existing blockchains, be investigated.

This study strove to make both a theoretical and a practical contribution. The researchers responded to a call to address accounting research problems by applying accounting theory, leading to the theoretical proposition contained in this article. This study also offers practical assistance to stakeholders in understanding the theory behind the practice of accounting for cryptocurrencies which are considered very important according to the literature. In addition, the novel proposal of addressing the problem of accounting for cryptocurrencies through the lens of accounting theory could reduce uncertainty among entities holding investments in cryptocurrencies. For the first time, entities holding investments in cryptocurrencies have clear guidance on how to faithfully account for and present such investments in their financial statements. This study has indicated the circumstances under which the guidance proposed by the IASB will result in decision-useful information based on the IASB’s conceptual framework. The guidance developed could also be utilised by future researchers to evaluate the accounting treatment of cryptocurrencies in practice. Auditors could apply the guidance in assessing the appropriateness of accounting for cryptocurrencies.

{kind=link}