Impact of Financial Inclusion on India’s Economic Development under the Moderating Effect of Internet Subscribers

, , and

, , and

Abstract

:1. Introduction

2. Review of Literature

2.1. Financial Inclusion in India

2.2. Government Policy for Financial Inclusion—PMFBY

2.3. Financial Inclusion and Sustainable Growth

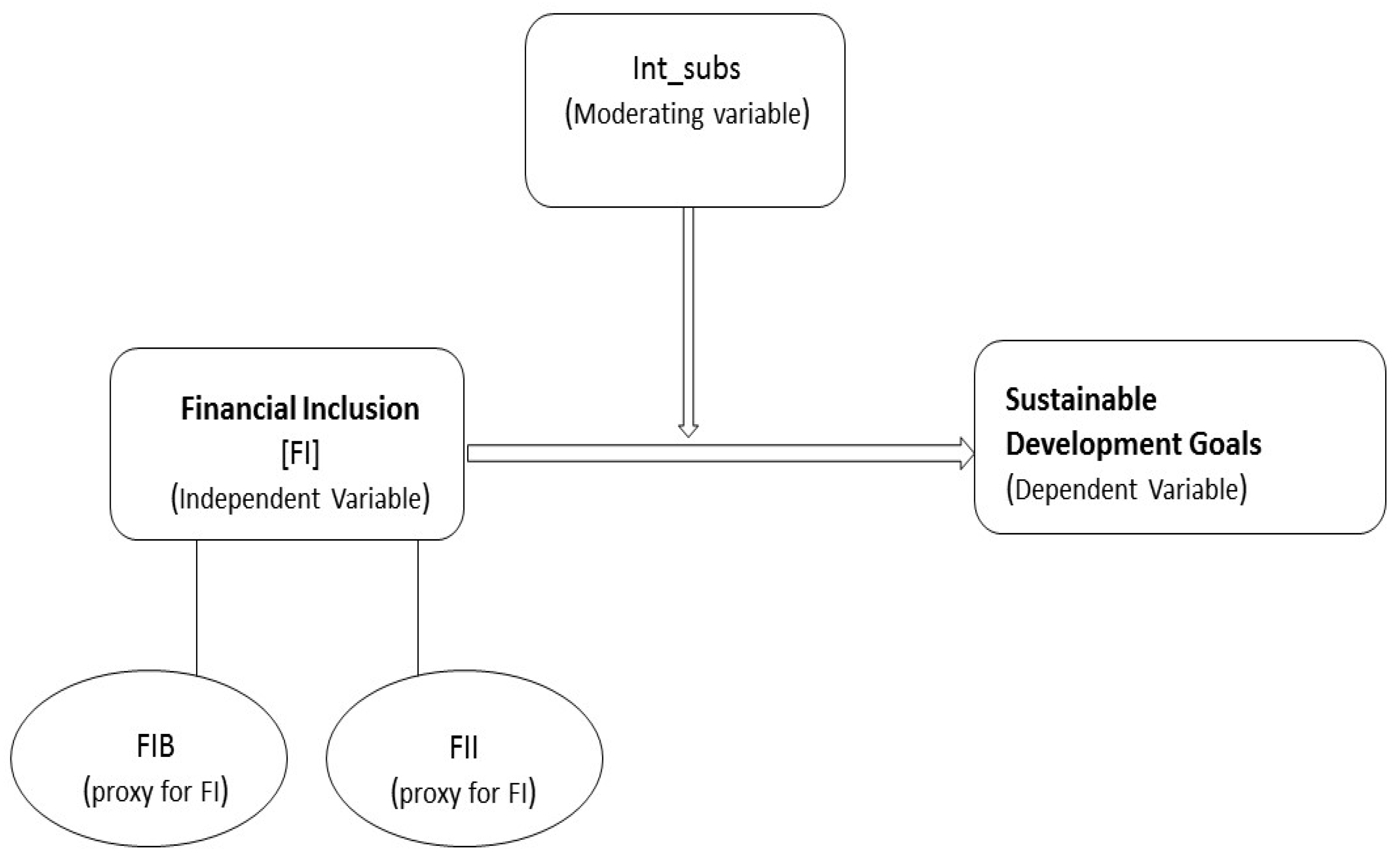

2.4. Theoretical Framework and Hypotheses Development

2.4.1. FI’s Impact on Sustainable Growth

2.4.2. Internet Subscribers and FI

3. Data and Research Methodology

3.1. Data

3.2. Methodology

4. Result of the Study

4.1. Results of Descriptive Statistics and Correlation Matrix

4.2. Analysis and Results

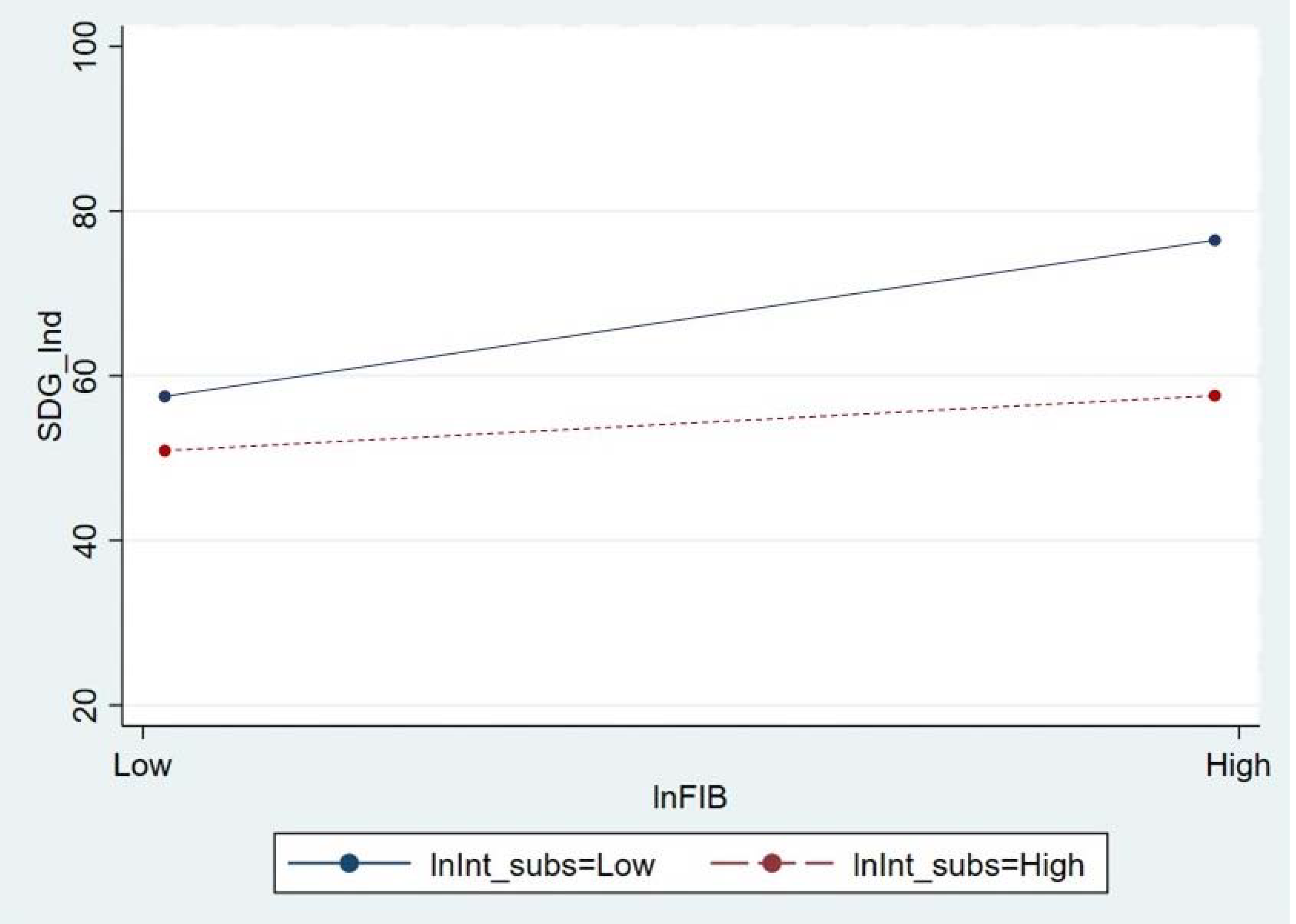

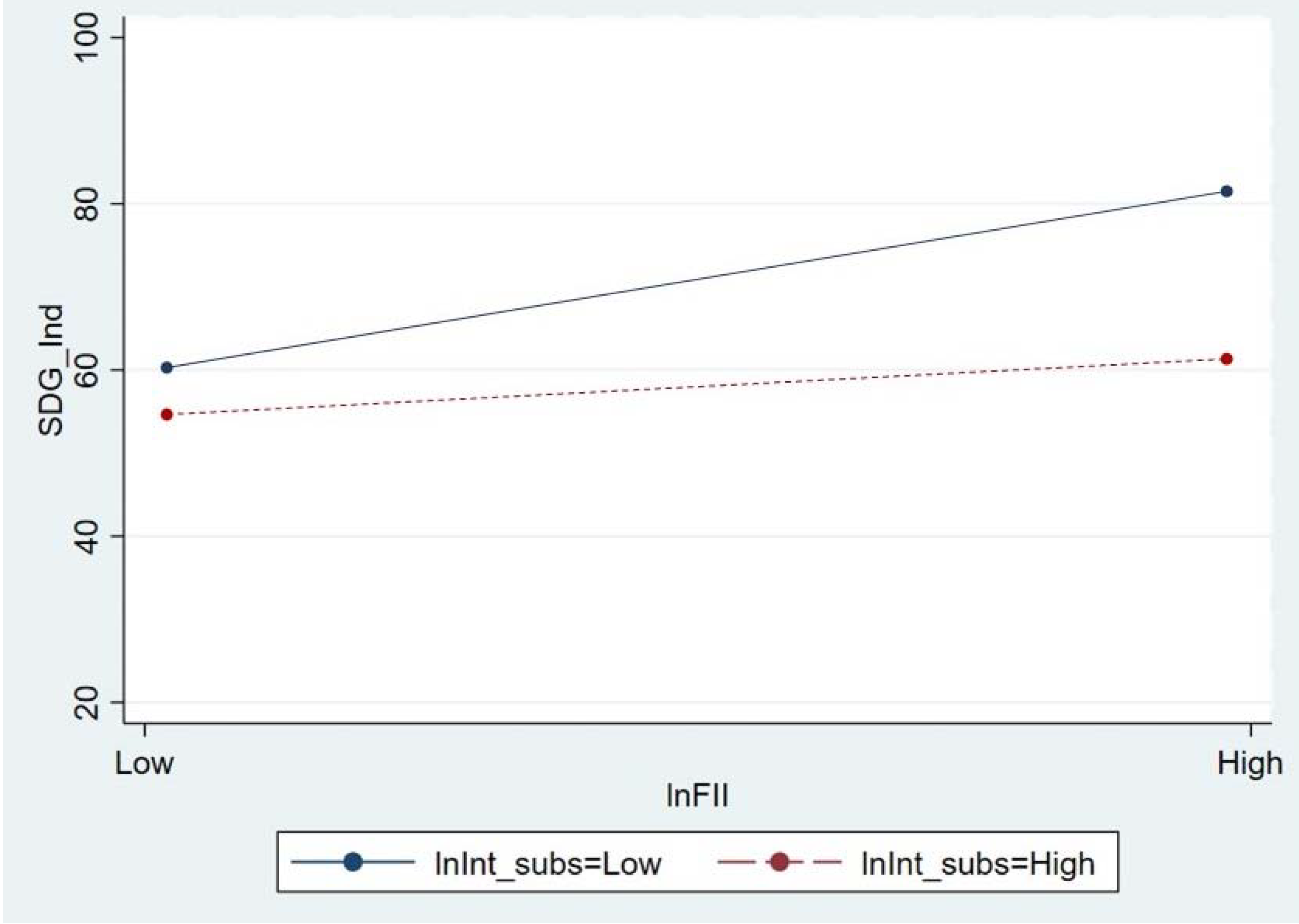

4.3. Marginal Effect of FI on SDG in Models 3 and 4

SDG_Indit = 1.745 + (−0.213)*lnInt_subsit

Where β1 = 1.745, and β3 = −0.213

When lnInt_subsit = 1

Then SDG_Indit = 1.532

When lnInt_subsit = 2

Then SDG_Indit = 1.319

When lnInt_subsit = 3

Then SDG_Indit = 1.106

SDG_Indit = 2.807 + (−0.531)*lnInt_subsit

Where β3 = 2.807 and β4 = −0.531

When lnInt_subsit = 1

Then SDG_Indit = 2.276

When lnInt_subsit = 2

Then SDG_Indit = 1.745

When lnInt_subsit = 3

Then SDG_Indit = 1.214

4.4. Endogeneity and Robustness

5. Discussion

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A. Additional Discussion of Validity of Methodology and the Results’ Consistency

{kind=link}

{kind=link}

{kind=link}

| DV: SDG_Ind | Base Model 1 (Robust) | Base Model 2 (Robust) | Interaction Model 3 (Robust) | Interaction Model 4 (Robust) | ||||

|---|---|---|---|---|---|---|---|---|

| Coef. | SE. | Coef. | SE. | Coef. | SE. | Coef. | SE. | |

| lnFIB | 2.476 ** | 1.097 | 0.465 | 0.912 | 5.036 *** | 2.781 | 0.395 | 0.629 |

| lnFII | ||||||||

| lnInt_subs | 11.847 *** | 2.421 | 12.237 *** | 2.198 | ||||

| i_lnFIB_lnInt_subs | −1.038 *** | 0.587 | ||||||

| i_lnFII_InInt_subs | −0.001 * | 0.000 | ||||||

| lnAr_Ins | −8.779 *** | .353 | −9.027 *** | 0.714 | −4.553 *** | 1.135 | −4.372 *** | 1.242 |

| lnGr_Pr | 5.991 *** | 1.447 | 8.162 *** | 0.077 | 3.331 *** | 0.725 | 3.787 *** | 0.629 |

| Cons | 43.356 *** | 7.430 | 32.089 *** | 1.828 | 5.650 | 9.063 | 0.736 | 5.748 |

| Hausman Test | 2.70 (0.4410) | 0.65 (0.8855) | 4.50 (0.4800) | 4.75 (0.4474) | ||||

| Wald test for Heteroscedasticity 1 | 1.62 (0.6546) | 3.70 (0.2956) | 14.23 *** (0.0026) | 22.70 *** (0.0000) | ||||

| Wooldridge Autocorrelation Test 2 AR (1) | 61.560 *** (0.0159) | 147.335 *** (0.0067) | 288.030 *** (0.0035) | 154.182 *** (0.0064) | ||||

References

- Agarwal, Tanushree, and Prasant Kumar Panda. 2018. Pattern of Digital Divide and Convergence in Access to ICT Facilities among the Indian States. Journal of Infrastructure Development 10: 37–51. [Google Scholar] [CrossRef]

- Aggarwal, Richa. 2014. Financial Inclusion in India: Challenges and Opportunities. International Journal of Research (IJR) 1: 557–67. [Google Scholar]

- Alam Iqbal, Badar, and Shaista Sami. 2017. Role of banks in financial inclusion in India. Contaduria y Administracion 62: 644–56. [Google Scholar] [CrossRef]

- Andrianaivo, Mihasonirina, and Kangni Kpodar. 2012. Mobile phones, financial inclusion, and growth. Review of Economics and Institutions 3: 30. [Google Scholar] [CrossRef]

- Asongu, Simplice A., and Lieven De Moor. 2015. Recent Advances in Finance for Inclusive Development: A Survey. Available online: https://econpapers.repec.org/paper/abhwpaper/15_2f005.htm (accessed on 12 March 2015).

- Baltagi, Badi Hani, and Badi H. Baltagi. 2008. Econometric Analysis of Panel Data. Chichester: John Wiley & Sons, vol. 4. [Google Scholar]

- Barajas, Adolfo, Ralph Chami, Christian Ebeke, and Sampawende J.-A. Tapsoba. 2012. Workers’ Remittances: An Overlooked Channel of International Business Cycle Transmission? Washington, DC: International Monetary Fund. [Google Scholar]

- Boateng, Kwadwo. 2017. Financial Inclusion for Economic Growth-An Overview of Some Financial Inclusion Policies in India. Available online: www.kaavpublications.org (accessed on 6 February 2017).

- Busenbark, John R., Scott D. Graffin, Robert J. Campbell, and Eric Young Lee. 2022. A marginal effects approach to interpreting main effects and moderation. Organizational Research Methods 25: 147–69. [Google Scholar] [CrossRef]

- Chatterjee, Amrita. 2017. Financial Inclusion, Information and Communication Technology Diffusion and Economic Growth: A Panel Data Analysis. Paper presented at the XXVIIth Annual Conference on Contemporary Issues in Development Economics, Kolkata, India, December 21–22; Available online: https://www.researchgate.net/publication/323218542_Financial_Inclusion_Information_and_Communication_Technology_Diffusion_and_Economic_Growth_A_Panel_Data_Analysis (accessed on 8 March 2020).

- Consultative Group to Assist the Poor—CGAP. 2011. Global Standard-Setting Bodies and Financial Inclusion for the Poor-Toward Proportionate Standards and Guidance. White Paper. Washington, DC: Global Partnership for Financial Inclusion. [Google Scholar]

- D’souza, Renita. 2018. Examining Mobile Banking as a Tool for FI in India. ORF Issue Brief 265: 1–12. [Google Scholar]

- Dikshit, Smita, and A. C. Pandey. 2021. Role of financial inclusion in realizing sustainable development goals (SDGs). International Journal of Research in Finance and Management 4: 35–39. [Google Scholar] [CrossRef]

- Gautam, Rahul Singh, Shailesh Rastogi, Aashi Rawal, Venkata Mrudula Bhimavarapu, Jagjeevan Kanoujiya, and Samaksh Rastogi. 2022. Financial Technology and Its Impact on Digital Literacy in India: Using Poverty as a Moderating Variable. Journal of Risk and Financial Management 15: 311. [Google Scholar] [CrossRef]

- Ghosh, Saibal. 2016. Does mobile telephony spur growth? Evidence from Indian states. Telecommunications Policy 40: 1020–31. [Google Scholar] [CrossRef]

- Han, Rui, and Martin Melecky. 2013. Financial Inclusion for Stability: Access to Bank Deposits and the Deposit Growth during the Global Financial Crisis Financial Inclusion for Financial Stability. MPRA. Available online: https://mpra.ub.uni-muenchen.de/48339/ (accessed on 16 July 2013).

- Hsiao, Cheng. 2007. Panel data analysis—Advantages and challenges. Test 16: 1–22. [Google Scholar] [CrossRef]

- Inoue, Takeshi, and Shigeyuki Hamori. 2016. Financial access and economic growth: Evidence from Sub-Saharan Africa. Emerging Markets Finance and Trade 52: 743–53. [Google Scholar] [CrossRef]

- Johnson, Susan, and Steven Arnold. 2012. Inclusive financial markets: Is transformation under way in Kenya? Development Policy Review 30: 719–48. [Google Scholar] [CrossRef]

- Kandpal, Vinay. 2020. Reaching sustainable development goals: Bringing financial inclusion to reality in India. Journal of Public Affairs 20: e2277. [Google Scholar] [CrossRef]

- Kim, Jong-Hee. 2016. A study on the effect of financial inclusion on the relationship between income inequality and economic growth. Emerging Markets Finance and Trade 52: 498–512. [Google Scholar] [CrossRef]

- Kim, Minjin, Hanah Zoo, Heejin Lee, and Juhee Kang. 2017. Mobile, Financial Inclusion and Development: A Critical Review of Academic Literature. Available online: https://aisel.aisnet.org/globdev2017/4/ (accessed on 21 October 2022).

- King, Robert, and Ross Levine. 1993. Finance and Growth: Schumpeter Might Be Right. The Quarterly Journal of Economics 108: 717–37. [Google Scholar] [CrossRef]

- Kyereboah-Coleman, Anthony. 2008. Corporate governance and firm performance in Africa: A dynamic panel data analysis. Studies in Economics and Econometrics 32: 1–24. [Google Scholar] [CrossRef]

- Lamba, Vibha. 2021. Descriptive Analysis of Pradhan Mantri Fasal Bima Yojana (Pmfby) From the Year 2016–2020. International Journal of Mechanical Engineering 3: 3971–80. Available online: https://kalaharijournals.com/resources/DEC_593.pdf (accessed on 21 October 2022).

- NITI Aayog. 2020. SDG India Index & Dashboard 2019–20. Available online: http://14.139.60.153/handle/123456789/13652 (accessed on 2 November 2019).

- Onukwugha, Eberechukwu, Jason Bergtold, and Rahul Jain. 2015. A primer on marginal effects—Part I: Theory and formulae. Pharmacoeconomics 33: 25–30. [Google Scholar] [CrossRef]

- Ozili, Peterson K. 2018. Impact of digital finance on financial inclusion and stability. Borsa Istanbul Review 18: 329–40. [Google Scholar] [CrossRef]

- Pandey, Amit, Ravi Kiran, and Rakesh Kumar Sharma. 2022. Investigating the Impact of Financial Inclusion Drivers, Financial Literacy and Financial Initiatives in Fostering Sustainable Growth in North India. Sustainability 14: 11061. [Google Scholar] [CrossRef]

- Park, Cyn-Young, and Rogelio Mercado. 2015. Financial Inclusion, Poverty, and Income Inequality in Developing Asia. Asian Development Bank Economics Working Paper Series; Mandaluyong: ADB, p. 426. [Google Scholar]

- Pearce, Douglas. 2011. Financial Inclusion in the Middle East and North Africa: Analysis and Roadmap Recommendations. World Bank Policy Research Working Paper. Washington, DC: World Bank, p. 5610. [Google Scholar]

- Piper, Alan T. 2014. The Benefits, Challenges and Insights of a Dynamic Panel Assessment of Life Satisfaction. Available online: https://mpra.ub.uni-muenchen.de/59556/ (accessed on 2 January 2014).

- PMFBY—Crop Insurance. n.d. Pradhan Mantri Fasal Bima Yojana—Crop Insurance. Available online: https://pmfby.gov.in/stateWiseDataPage (accessed on 26 September 2022).

- Pradhan, Rudra P., and Pragyan P. Sahoo. 2021. Are there links between financial inclusion, mobile telephony, and economic growth? Evidence from Indian states. Applied Economics Letters 28: 310–14. [Google Scholar] [CrossRef]

- Pradhan, Rudra P., Mak B. Arvin, Neville R. Norman, and John H. Hall. 2014. The dynamics of banking sector and stock market maturity and the performance of Asian economies: Time series evidence. Journal of Economic and Administrative Sciences 30: 16–44. [Google Scholar] [CrossRef]

- Rai, Ruchbah. 2019. Pradhan Mantri Fasal Bima Yojana: An Assessment of India’s Crop Insurance Scheme. ORF Issue Brief 296: 1–16. [Google Scholar]

- Raichoudhury, Ayushi. 2020. Major Determinants of Financial Inclusion: State-Level Evidences from India. Vision 24: 151–59. [Google Scholar] [CrossRef]

- Rasheed, Balach, Siong-Hook Law, Lee Chin, and Muzafar Shah Habibullah. 2016. The role of financial inclusion in financial development: International evidence. Abasyn University Journal of Social Sciences 9: 330–48. [Google Scholar]

- Rastogi, Shailesh, and E. Ragabiruntha. 2018. Financial inclusion and socioeconomic development: Gaps and solution. International Journal of Social Economics 45: 1122–40. [Google Scholar] [CrossRef]

- Rastogi, Shailesh, Arpita Sharma, Chetan Panse, and Venkata Mrudula Bhimavarapu. 2021. Unified Payment Interface (UPI): A digital innovation and its impact on financial inclusion and economic development. Universal Journal of Accounting and Finance 9: 518–30. [Google Scholar] [CrossRef]

- SDG. 2022. THE 17 GOALS Sustainable Development. Available online: https://sdgs.un.org/goals (accessed on 11 October 2022).

- Sethi, Dinabandhu, and Debashis Acharya. 2018. Financial inclusion and economic growth linkage: Some cross country evidence. Journal of Financial Economic Policy 10: 369–85. [Google Scholar] [CrossRef]

- Sharma, Upasana, and Banajit Changkakati. 2022. Dimensions of global financial inclusion and their impact on the achievement of the United Nations Development Goals. Borsa Istanbul Review 22: 1238–50. [Google Scholar] [CrossRef]

- Siddiqui, Taufeeque A., and Kashif I. Siddiqui. 2020. FinTech in India: An analysis on impact of telecommunication on financial inclusion. Strategic Change 29: 321–30. [Google Scholar] [CrossRef]

- Singh, Pankaj, and Gaurav Agrawal. 2020. Development, present status and performance analysis of agriculture insurance schemes in India: Review of evidence. International Journal of Social Economics 47: 461–81. [Google Scholar] [CrossRef]

- Singh, Vinay Kumar, and Sajal Ghosh. 2021. Financial inclusion and economic growth in India amid demonetization: A case study based on panel cointegration and causality. Economic Analysis and Policy 71: 674–93. [Google Scholar] [CrossRef]

- Soumen, Sarkar, and Kumar Paul Sujit. 2021. A Study on the Significant Approaches towards Financial Inclusion in India. The Journal of Oriental Research Madras, 73–87. [Google Scholar]

- Sujlana, Paramjit, and Chhavi Kiran. 2018. A Study on Status of Financial Inclusion in India. International Journal of Management Studies 5: 96. [Google Scholar] [CrossRef]

- Swamy, Vighneswara. 2014. Financial Inclusion, Gender Dimension, and Economic Impact on Poor Households. World Development 56: 1–15. [Google Scholar] [CrossRef]

- Telecom Regulatory Authority of India. 2022. Performance Indicators Reports | Telecom Regulatory Authority of India; August 7, Telecom Regulatory Authority of India. Available online: https://www.trai.gov.in/release-publication/reports/performance-indicators-reports (accessed on 11 October 2022).

- Tiwari, Rajesh, Khem Chand, and Bimal Anjum. 2020. Crop Insurance in India: A Review of Pradhan Mantri Fasal Bima Yojana (PMFBY). FIIB Business Review 9: 249–55. [Google Scholar] [CrossRef]

- Van de Meerendonk, Tim. 2020. Claiming crisis: Narratives of tension and insurance in rural India. Contemporary South Asia 28: 362–73. [Google Scholar] [CrossRef] [PubMed]

- Van, Loan Thi-Hong, Anh The Vo, Nhan Thien Nguyen, and Duc Hong Vo. 2021. Financial inclusion and economic growth: An international evidence. Emerging Markets Finance and Trade 57: 239–63. [Google Scholar] [CrossRef]

- Wooldridge, Jeffrey M. 2015. Introductory Econometrics: A Modern Approach. Boston: Cengage Learning. [Google Scholar]

| SN | Variable | Type | Definition | Citations |

|---|---|---|---|---|

| 1 | SDG_Ind | DV | The SDG India Index aims to present a comprehensive picture of the nation’s social, economic, and environmental situation and its States and UTs. | NITI Aayog (2020). |

| 2 | lnFIB | IV | Farmers Application Benefited comes under PMFBY (in lakh) and is used as a proxy of FI. PMFBY is concerned with crop insurance for farmers in India. The natural log value is utilized. | PMFBY—Crop Insurance (n.d.); Lamba (2021). |

| 3 | lnFII | IV | Farmers Application Insured comes under PMFBY (in lakh) and is used as a proxy of FI. The natural log value is utilized. | PMFBY—Crop Insurance (n.d.); Lamba (2021). |

| 4 | lnInt_subs | IV | The total number of internet subscribers per 100 in India has been taken from TRAI, and this variable is used as a proxy of digitalization. The natural log value is utilized. | Performance Indicators Reports, Telecom Regulatory Authority of India (2022, August 7). |

| 5 | lnAr_Ins | CV | Under PMFBY, Area Insured (lakh hectares) is used as a control variable in this study. The natural log value is utilized. | PMFBY—Crop Insurance (n.d.); Lamba (2021). |

| 6 | lnGr_Pr | CV | Under PMFBY, Gross Premium (INR in crore) is used as a control variable in this study. The natural log value is utilized. | PMFBY—Crop Insurance (n.d.); Lamba (2021). |

| Variables | Mean | SD | Min | Max |

|---|---|---|---|---|

| SDG_Ind | 64.05882 | 6.833482 | 50 | 75 |

| lnFIB | 1.571513 | 1.841450 | −3.816713 | 4.476143 |

| lnFII | 2.789169 | 1.613935 | −0.592397 | 4.999527 |

| lnInt_subs | 3.983403 | 0.315029 | 3.230014 | 4.487737 |

| lnAr_Ins | 2.191722 | 1.856352 | −0.988861 | 4.862151 |

| lnGr_Pr | 5.714827 | 2.829563 | 0 | 8.756804 |

| Variables | lnFIB | lnFII | lnInt_subs | i_lnFIB_lnInt_subs | i_lnFII_InInt_subs | lnAr_Ins | lnGr_Pr |

|---|---|---|---|---|---|---|---|

| lnFIB | 1.0000 | ||||||

| lnFII | 0.9116 * | 1.0000 | |||||

| lnInt_subs | 0.1568 | −0.1129 | 1.0000 | ||||

| i_lnFIB_lnInt_subs | 0.9957 * | 0.9015 * | 0.1984 | 1.0000 | |||

| i_lnFII_InInt_subs | 0.9246 * | 0.9898 * | 0.0033 | 0.9258 * | 1.0000 | ||

| lnAr_Ins | 0.6563 * | 0.7039 * | −0.1523 | 0.6395 * | 0.6812 * | 1.0000 | |

| lnGr_Pr | 0.7173 * | 0.7342 * | 0.0838 | 0.7318 * | 0.7653 * | 0.7674 * | 1.0000 |

| DV: SDG_Ind | Model 1 (Base_Model 1) | Model 2 (Base_Model 2) | Model 3 (Interaction_Model 1) | Model 4 (Interaction_Model 2) | ||||

|---|---|---|---|---|---|---|---|---|

| Coeff. | SE. | Coeff. | SE. | Coeff. | SE. | Coeff. | SE. | |

| SDG_Ind log 1 | −0.085 | 0.096 | 0.041 | 0.171 | 0.116 * | 0.045 | 0.168 *** | 0.050 |

| lnFIB | 3.209 *** | 0.754 | 1.745 * | 0.971 | ||||

| lnFII | 0.741 * | 0.567 | 2.807 | 2.005 | ||||

| lnInt_subs | 12.993 * | 1.491 | 15.878 *** | 1.564 | ||||

| i_lnFIB_lnInt_subs | −0.213 * | 0.200 | ||||||

| i_lnFII_InInt_subs | −0.531 * | 0.412 | ||||||

| lnAr_Ins | −8.037 *** | 1.212 | −9.535 *** | 2.541 | −5.630 *** | 1.151 | −5.897 *** | 1.465 |

| lnGr_Pr | 4.412 *** | 0.713 | 8.302 *** | 2.535 | 4.627 *** | 0.900 | 5.241 *** | 1.243 |

| Cons. | 56.032 *** | 7.610 | 28.600 | 21.515 | −12.632 | 7.060 * | −31.466 *** | 12.007 |

| Sargan Test | 34.5127 (0.1845) | 31.50035 (0.2953) | 26.17405 (0.4536) | 25.28593 (0.5028) | ||||

| AR (1) | −0.68492 * (0.0934) | −1.4732 ** (0.0407) | −1.3898 * (0.0646) | −1.4432 ** (0.0490) | ||||

| AR (2) | −1.0764 (0.2818) | −1.1104 (0.2668) | −1.0864 (0.2773) | −1.0817 (0.2794) | ||||

| SDG India Index: SDG_ind | ||||

|---|---|---|---|---|

| lnFIB | lnFII | i_lnFIB_lnInt_subs | i_lnFII_lnInt_subs | |

| Durbin Chi-2 | 0.133011 | 0.394987 | 0.43016 | 0.144275 |

| (0.7153) | (0.5297) | (0.5119) | (0.7041) | |

| Wu-Hausman Test | 0.111337 | 0.335555 | 0.334586 | 0.112219 |

| (0.7414) | (0.5674) | (0.5686) | (0.7405) | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Pushp, A.; Gautam, R.S.; Tripathi, V.; Kanoujiya, J.; Rastogi, S.; Bhimavarapu, V.M.; Parashar, N. Impact of Financial Inclusion on India’s Economic Development under the Moderating Effect of Internet Subscribers. J. Risk Financial Manag. 2023, 16, 262. https://doi.org/10.3390/jrfm16050262

Pushp A, Gautam RS, Tripathi V, Kanoujiya J, Rastogi S, Bhimavarapu VM, Parashar N. Impact of Financial Inclusion on India’s Economic Development under the Moderating Effect of Internet Subscribers. Journal of Risk and Financial Management. 2023; 16(5):262. https://doi.org/10.3390/jrfm16050262

Chicago/Turabian StylePushp, Aman, Rahul Singh Gautam, Vikas Tripathi, Jagjeevan Kanoujiya, Shailesh Rastogi, Venkata Mrudula Bhimavarapu, and Neha Parashar. 2023. "Impact of Financial Inclusion on India’s Economic Development under the Moderating Effect of Internet Subscribers" Journal of Risk and Financial Management 16, no. 5: 262. https://doi.org/10.3390/jrfm16050262