Term Premia in Norwegian Interest Rate Swaps

Abstract

:1. Introduction

2. Literature Review

3. Materials and Methods

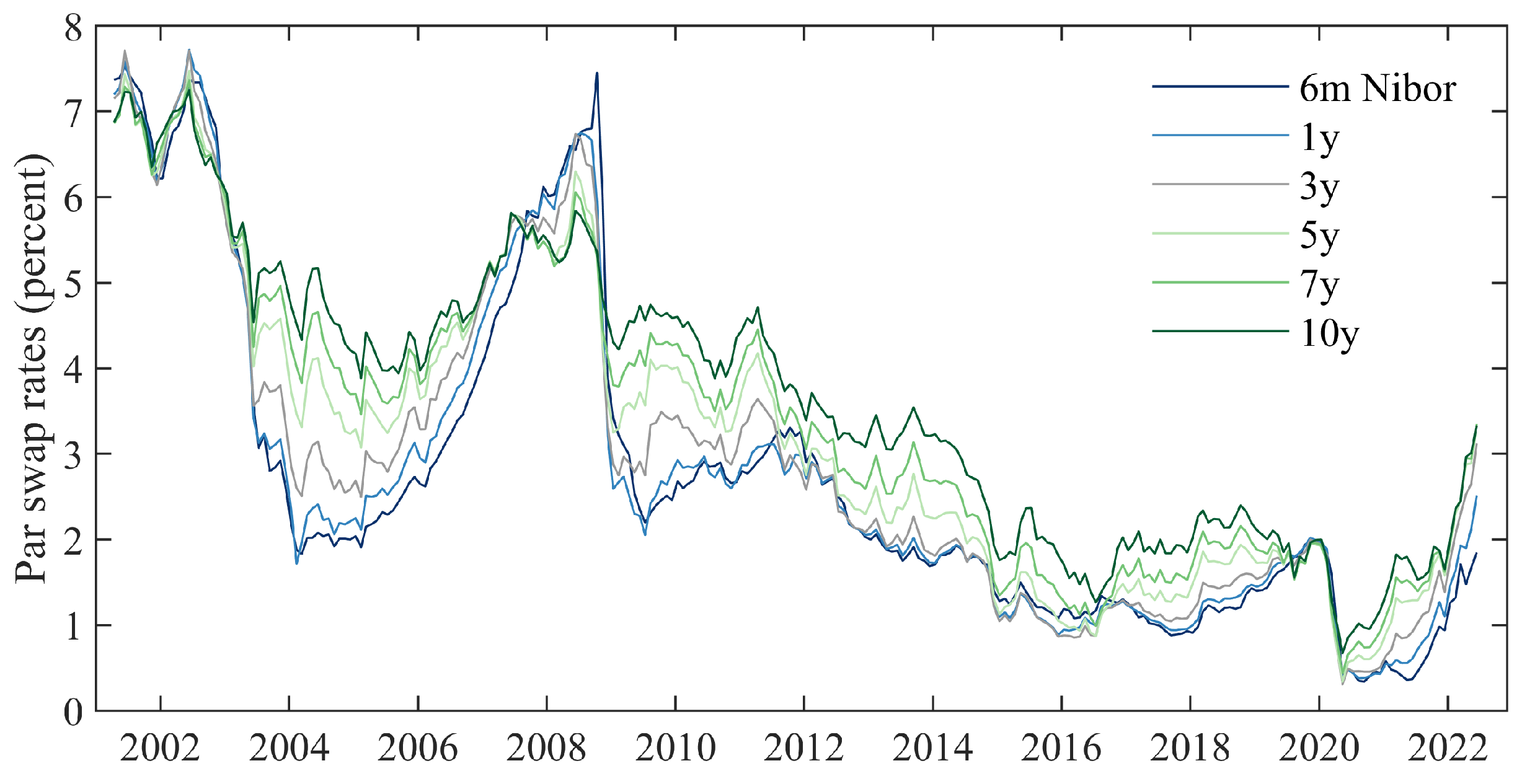

3.1. Data

3.2. Methodology

3.2.1. Affine Term Structure Models

3.2.2. Econometric Framework

3.2.3. Estimation Strategy

4. Results and Discussion

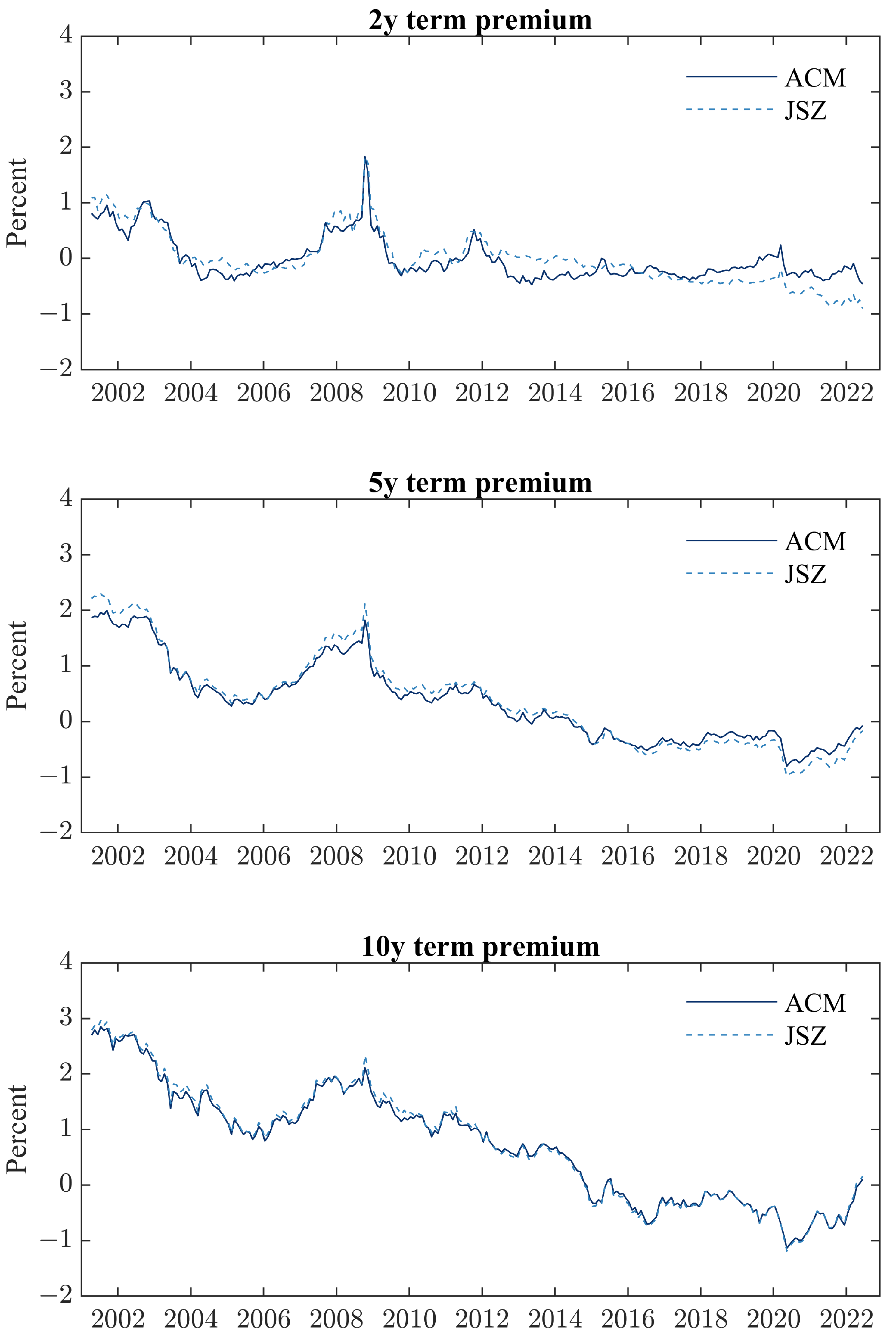

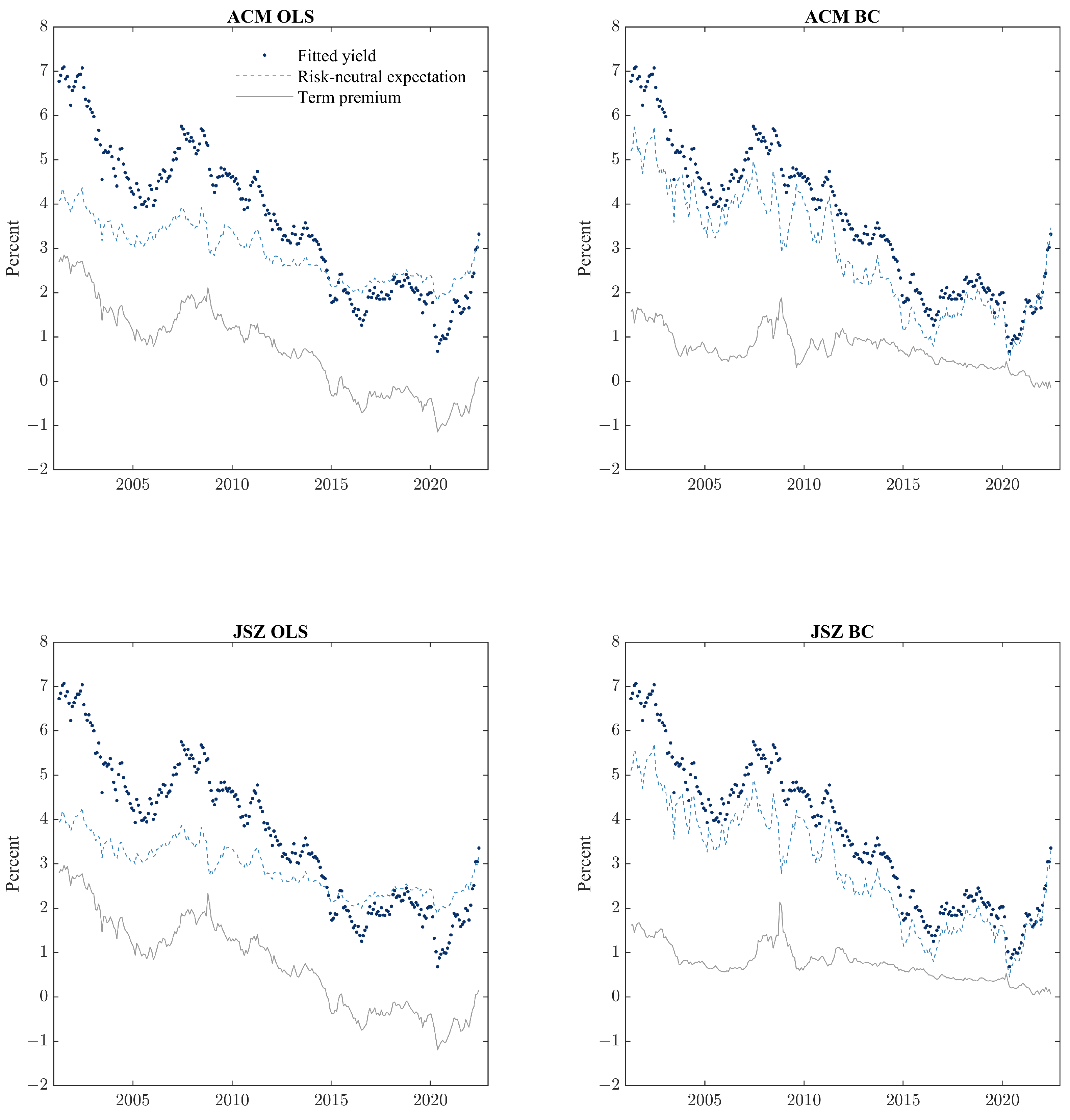

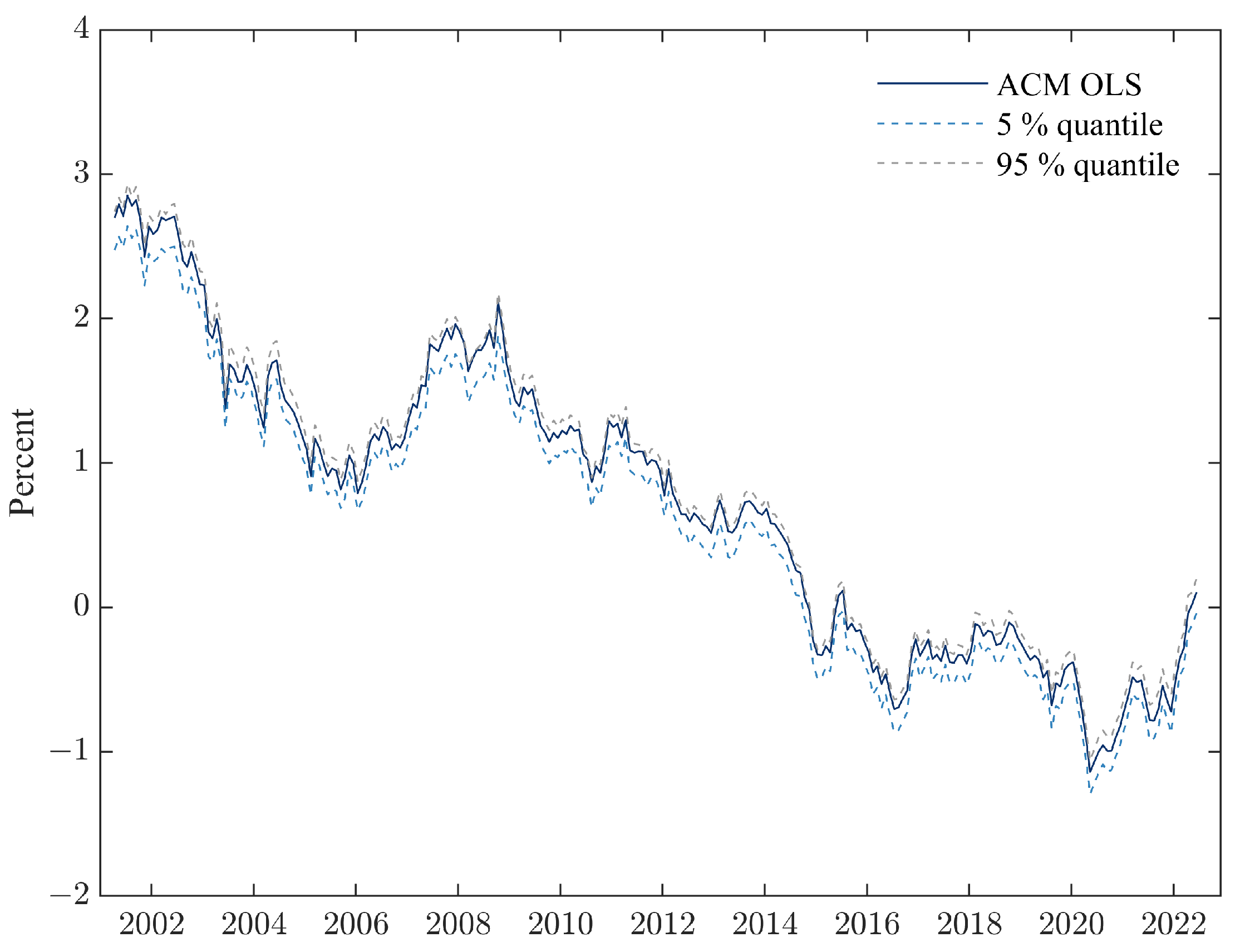

4.1. Term Premium Estimates

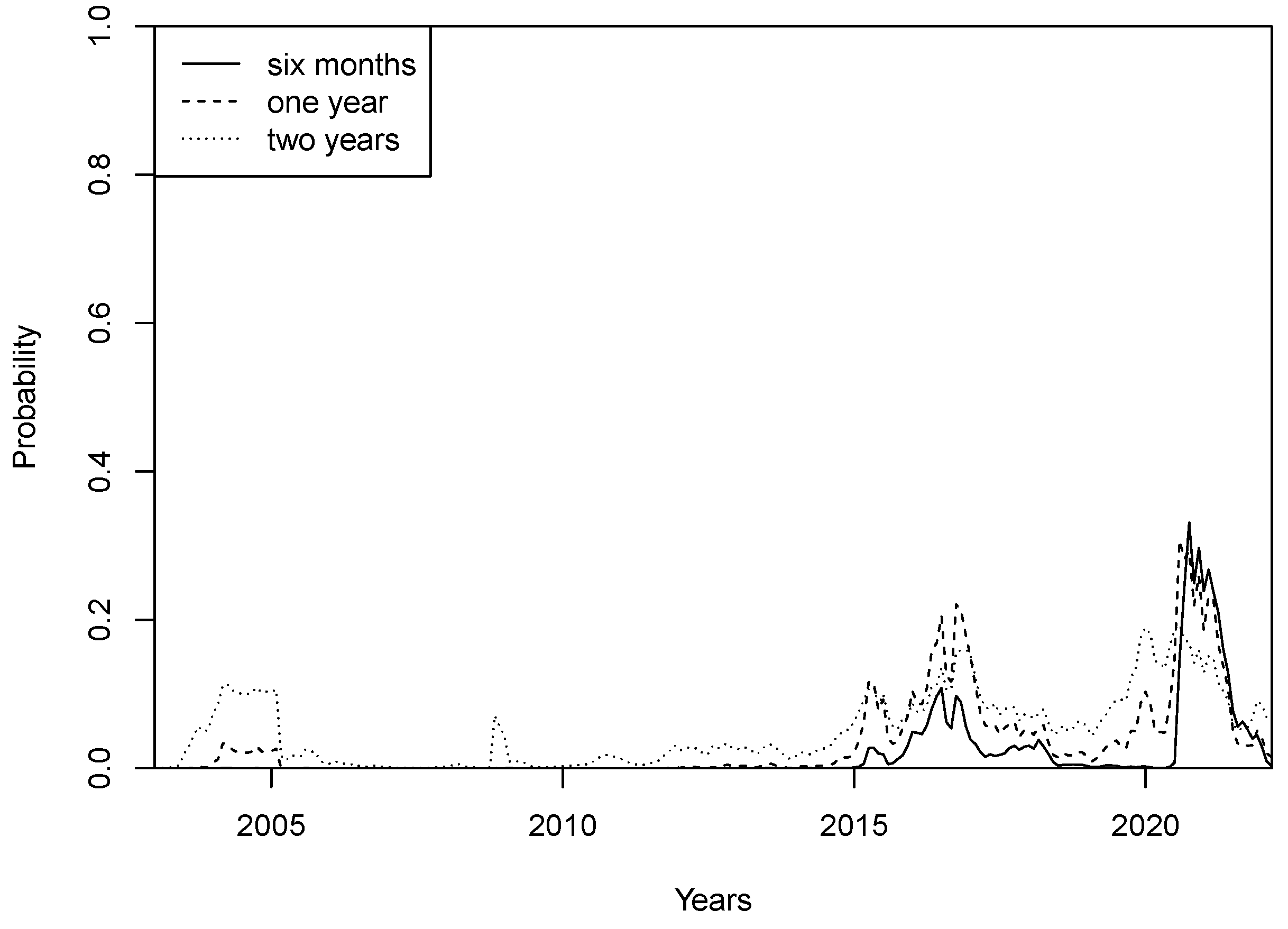

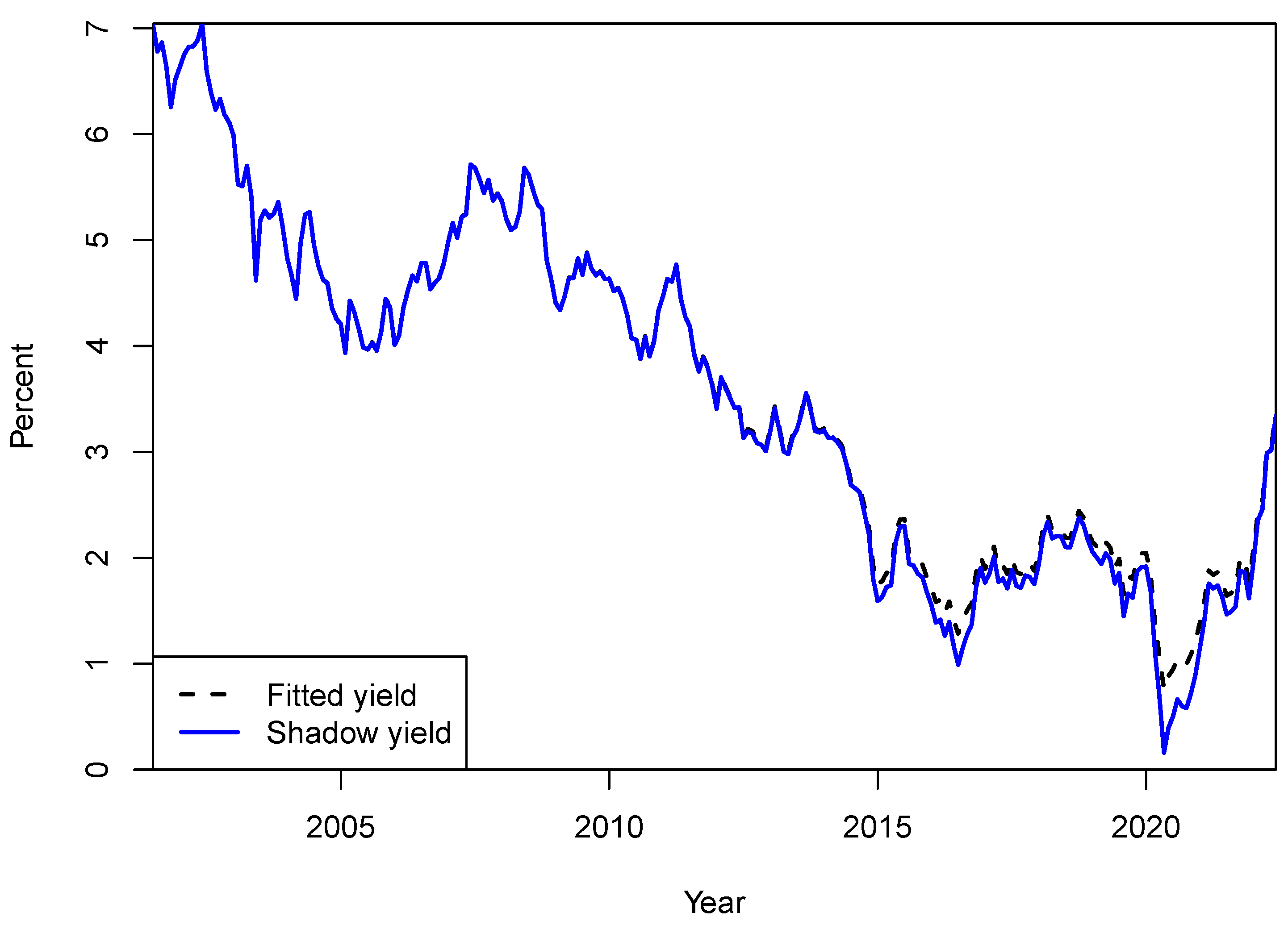

4.2. Impact of the Zero Lower Bound

4.3. Impact of Small Sample Bias

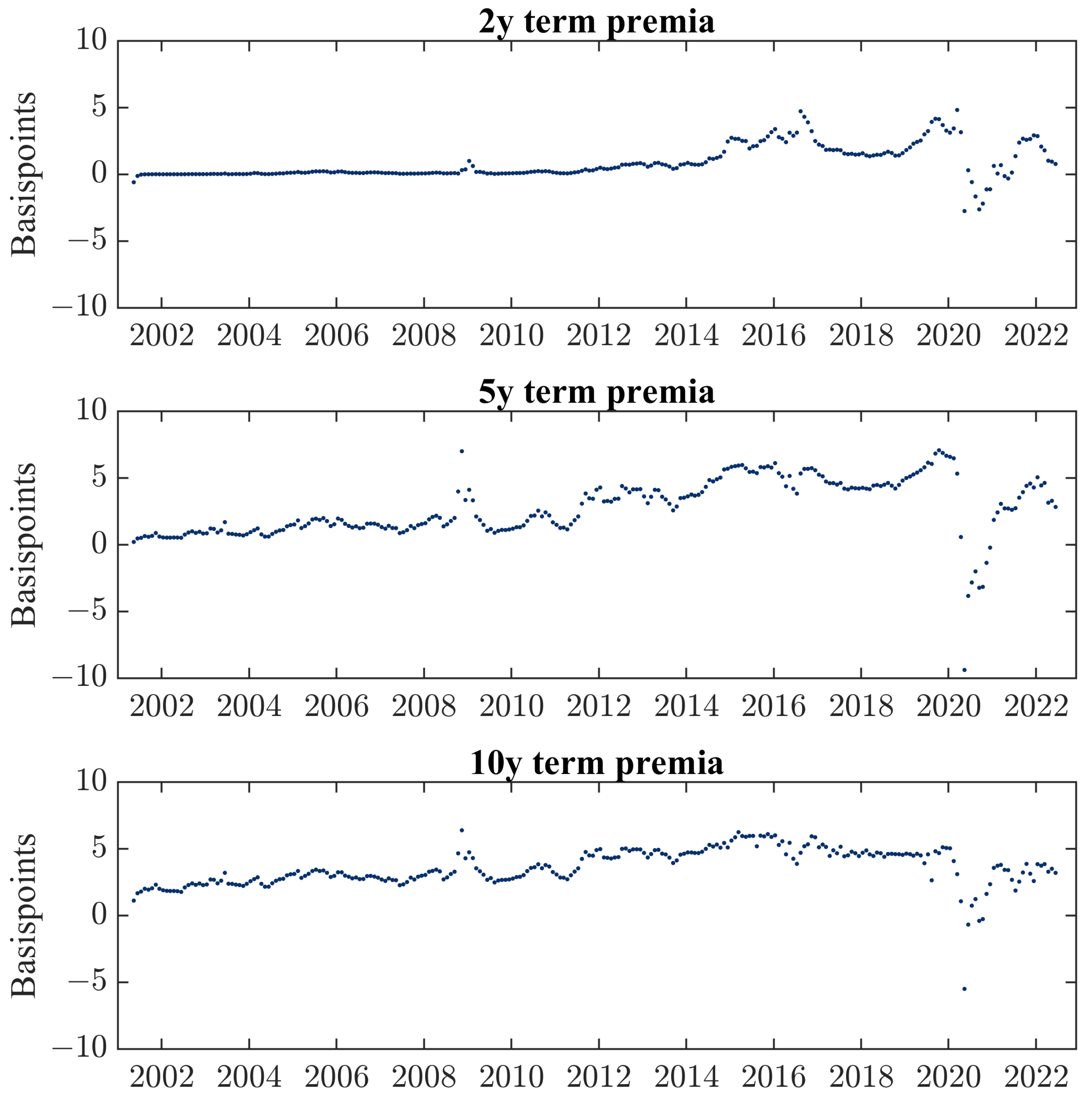

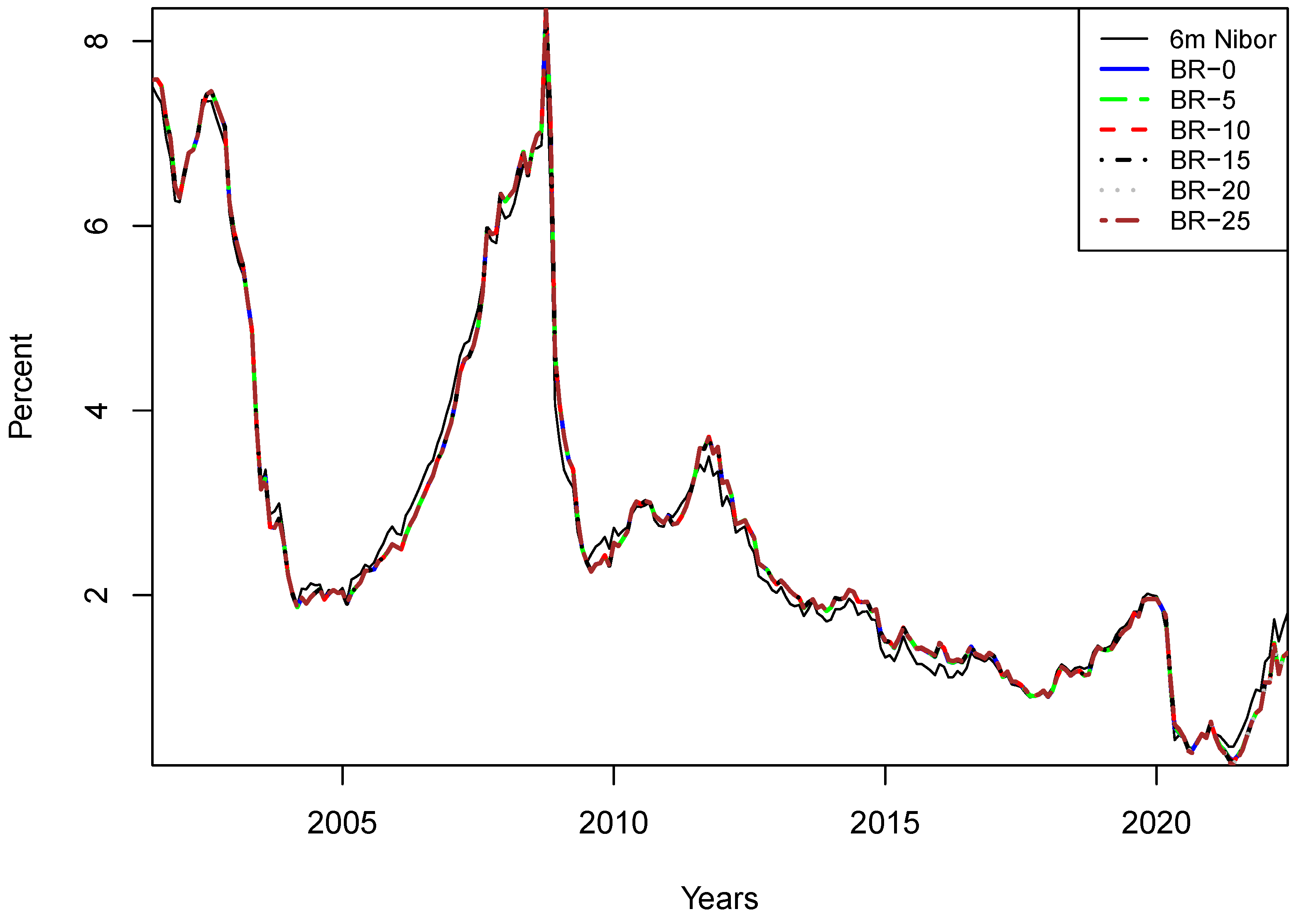

4.4. Impact of Measurement Error

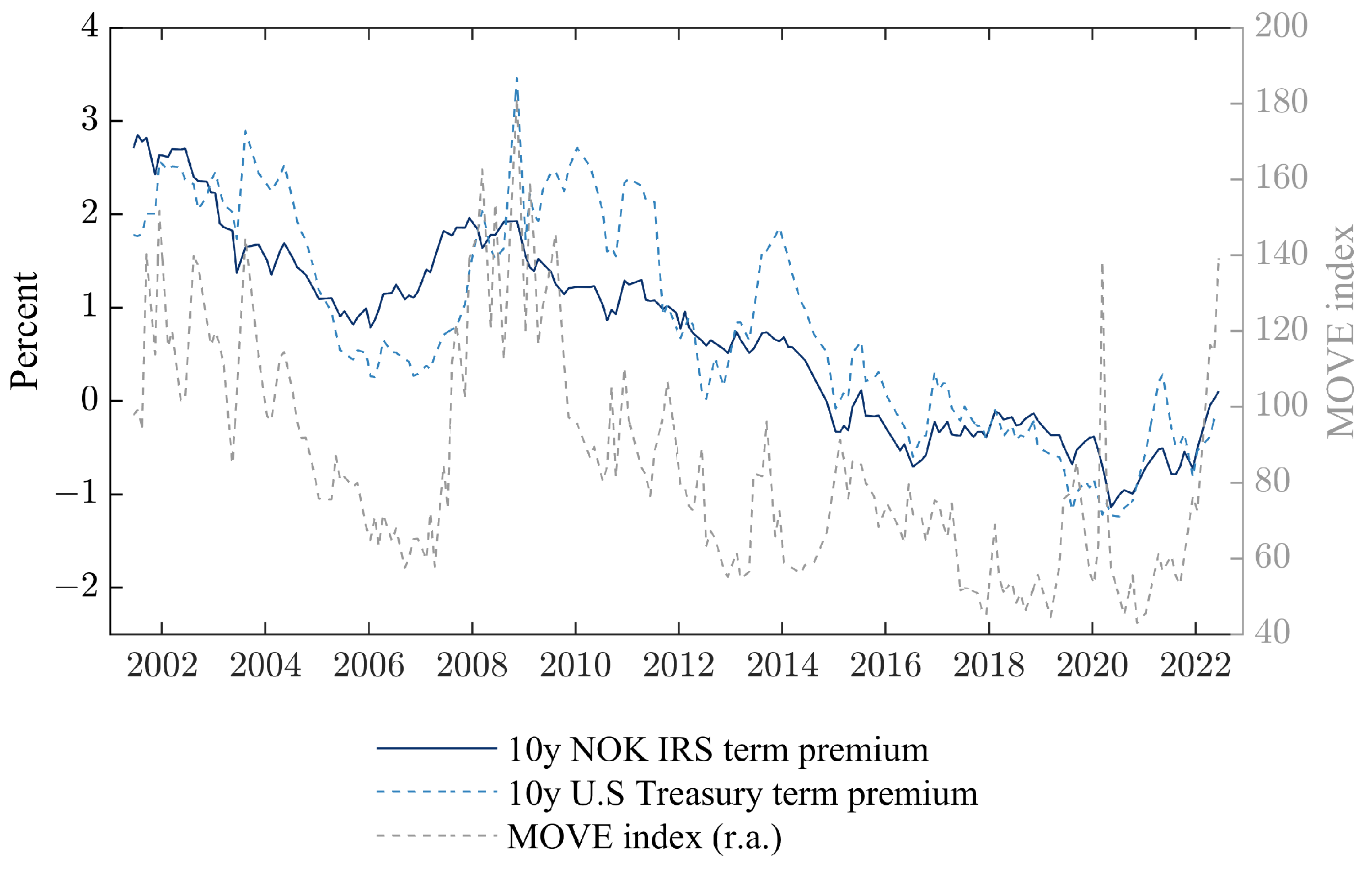

4.5. Correlation of Term Premia Estimates to Fundamental Risk Factors

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| ACM | The dynamic term structure model proposed by Adrian et al. (2013) |

| BR | The dynamic term structure model proposed by Bauer and Rudebusch (2016) |

| JSZ | The dynamic term structure model proposed by Joslin et al. (2011) |

| NOK | Norwegian Krone |

| IRS | Interest Rate Swap |

| 1 | More recently, the Norwegian Overnight Weighted Average (NOWA) rate has been proposed as an alternative to Nibor, following international reference rate reforms. So far, NOWA transaction volumes have been limited and market participants are reluctant to adopt NOWA. Furthermore, Nibor has been assessed and recognized by the European Commission as a critical benchmark. Hence, we expect Nibor to remain the primary benchmark rate in Norwegian Krone in the foreseeable future. |

| 2 | Strictly speaking, yields contain an additional convexity term—which relates to Jensen’s inequality; see Rebonato (2018). However, unless yield volatility is very high or for very long maturities, the convexity effect is typically small. In line with the literature, we ignore it for the purpose of this paper. |

| 3 | Risk neutral in this context refers to yields that would exist under the pure expectation hypothesis. That is, yields with a market price of interest rate risk equal to zero and thus no term premium. |

| 4 | To enhance the practical application of research presented in this paper, we maintain updated NOK IRS term premia estimates https://github.com/MortenRisstad/NOKIRSTP here. (6 March 2023). |

| 5 | Libor: London Interbank Offered Rate. OIS: Overnight Index Swap. |

| 6 | Maturities beyond 10 years are also quoted but significantly less liquid, and the related quotes are consequently less reliable. |

| 7 | See, for instance, Hevia and Sola (2018). |

| 8 | For instance, in Germany, short-term bond yields have been negative since mid-2014. Similarly, long-term yields were below zero from early 2019 until the end of 2021. |

| 9 | The difference equations for ACM contain one additional minor component compared with JSZ and BR. This is due to the ACM assumption of serially uncorrelated excess return pricing errors, as opposed to serially uncorrelated yield pricing errors (see Section 2.4 of Adrian et al. (2013)). |

| 10 | See Van Dijk et al. (2018) for a thorough discussion of joint modeling of risk factors in the physical () and risk-neutral () measures. |

| 11 | PCA has, since the seminal contribution of Ang and Piazzesi (2003), been the primary building blocks of modern term structure models. See Oprea (2022) for a recent application. |

| 12 | A canonical Gaussian DTSM is one that is maximally flexible in its parameterization of both the physical and risk-neutral distributions of , subject only to normalizations that ensure econometric identification. |

| 13 | See, for instance, Adrian et al. (2013); Bauer and Rudebusch (2016); Diebold and Li (2006); Malik and Meldrum (2016) and Jennison (2017), who report comparable fitting errors. |

| 14 | Comments from Fed officials led the market to expect an imminent removal of monetary accommodation. |

| 15 | Simulation results for other maturities and DTSMs are available from the corresponding author upon request. |

References

- Adrian, Tobias, Richard K. Crump, and Emanuel Moench. 2013. Pricing the term structure with linear regressions. Journal of Financial Economics 110: 110–38. [Google Scholar] [CrossRef] [Green Version]

- Ang, Andrew, and Monika Piazzesi. 2003. A no-arbitrage vector autoregression of term structure dynamics with macroeconomic and latent variables. Journal of Monetary Economics 50: 745–87. [Google Scholar] [CrossRef]

- Aydin, Halil İbrahim, and Ozgur Ozel. 2019. Term Premium in Turkish Lira Interest Rates. Ankara: Central Bank of the Republic of Turkey. [Google Scholar]

- Bauer, Michael D., and Glenn D. Rudebusch. 2016. Monetary policy expectations at the zero lower bound. Journal of Money, Credit and Banking 48: 1439–65. [Google Scholar] [CrossRef] [Green Version]

- Bauer, Michael D., and Glenn D. Rudebusch. 2020. Interest rates under falling stars. American Economic Review 110: 1316–54. [Google Scholar] [CrossRef]

- Bauer, Michael D., Glenn D. Rudebusch, and Jing Cynthia Wu. 2012. Correcting estimation bias in dynamic term structure models. Journal of Business & Economic Statistics 30: 454–67. [Google Scholar]

- Bekaert, Geert, Eric C. Engstrom, and Nancy R. Xu. 2019. The time variation in risk appetite and uncertainty (no. w25673). Management Science 68: 3975–4004. [Google Scholar] [CrossRef]

- Berardi, Andrea, and Alberto Plazzi. 2022. Dissecting the yield curve: The international evidence. Journal of Banking & Finance 134: 106286. [Google Scholar]

- Bernanke, Ben. 2013. Long-Term Interest Rates: A Speech at the Annual Monetary/Macroeconomics Conference; Technical Report. Washington, DC: Board of Governors of the Federal Reserve System (US).

- Bianchetti, Marco, and Massimo Morini. 2013. Interest Rate Modelling after the Financial Crisis. Edited by Massimo Morini and Marco Bianchetti. London: Risk Books, Incisive Media, vol. 11. [Google Scholar]

- Black, Fischer. 1995. Interest rates as options. The Journal of Finance 50: 1371–76. [Google Scholar] [CrossRef]

- Bollerslev, Tim, Benjamin Hood, John Huss, and Lasse Heje Pedersen. 2018. Risk everywhere: Modeling and managing volatility. The Review of Financial Studies 31: 2729–73. [Google Scholar] [CrossRef]

- Brooks, Robert, Brandon N. Cline, and Walter Enders. 2015. A comparison of the information in the libor and cmt term structures of interest rates. Journal of Banking & Finance 54: 239–53. [Google Scholar]

- Byrne, Joseph P., Shuo Cao, and Dimitris Korobilis. 2019. Decomposing global yield curve co-movement. Journal of Banking & Finance 106: 500–13. [Google Scholar]

- Callaghan, Michael. 2019. Expectations and the Term Premium in New Zealand Long-Term Interest Rates. Reserve Bank of New Zealand Analytical Note, AN2019/02. Wellington: Reserve Bank of New Zealand. [Google Scholar]

- Campbell, John Y., and Robert J. Shiller. 1988. The dividend-price ratio and expectations of future dividends and discount factors. The Review of Financial Studies 1: 195–228. [Google Scholar] [CrossRef] [Green Version]

- Cochrane, John H., and Monika Piazzesi. 2005. Bond risk premia. American Economic Review 95: 138–60. [Google Scholar] [CrossRef]

- Cohen, Benjamin H., Peter Hördahl, and Fan Dora Xia. 2018. Term premia: Models and some stylised facts. BIS Quarterly Review September 1: 79–90. [Google Scholar]

- Collin-Dufresne, Pierre, and Bruno Solnik. 2001. On the term structure of default premia in the swap and libor markets. The Journal of Finance 56: 1095–15. [Google Scholar] [CrossRef]

- Dahlquist, Magnus, and Henrik Hasseltoft. 2013. International bond risk premia. Journal of International Economics 90: 17–32. [Google Scholar] [CrossRef] [Green Version]

- Dai, Qiang, and Kenneth J. Singleton. 2000. Specification analysis of affine term structure models. The Journal of Finance 55: 1943–78. [Google Scholar] [CrossRef] [Green Version]

- Dai, Qiang, and Kenneth Singleton. 2003. Term structure dynamics in theory and reality. The Review of Financial Studies 16: 631–78. [Google Scholar] [CrossRef]

- D’Amico, Stefania, Canlin Li, J. Sears, and M. Cahill. 2014. The Term-Premium Effect of the Federal Reserve’s Asset Purchase Announcements. Technical Report. Chicago: Federal Reserve Bank of Chicago. [Google Scholar]

- d’Amico, Stefania, Don H. Kim, and Min Wei. 2018. Tips from TIPS: The informational content of Treasury Inflation-Protected Security prices. Journal of Financial and Quantitative Analysis 53: 395–436. [Google Scholar] [CrossRef] [Green Version]

- de Lange, Petter Eilif, Morten Risstad, and Sjur Westgaard. 2022. Term Premia in Norwegian Government Bond Yields. Beta 36: 1–21. [Google Scholar] [CrossRef]

- de los Rios, Antonio Diez, and Maral Shamloo. 2017. Quantitative Easing and Long-Term Yields in Small Open Economies. Paris: International Monetary Fund. [Google Scholar]

- Diebold, Francis X., and Canlin Li. 2006. Forecasting the term structure of government bond yields. Journal of Econometrics 130: 337–64. [Google Scholar] [CrossRef] [Green Version]

- Duffee, Gregory R. 2002. Term premia and interest rate forecasts in affine models. The Journal of Finance 57: 405–43. [Google Scholar] [CrossRef] [Green Version]

- Duffie, Darrell, and Rui Kan. 1996. A yield-factor model of interest rates. Mathematical Finance 6: 379–406. [Google Scholar] [CrossRef] [Green Version]

- Fama, Eugene F., and Robert R. Bliss. 1987. The information in long-maturity forward rates. The American Economic Review 77: 680–92. [Google Scholar]

- Filipović, Damir, and Anders B. Trolle. 2013. The term structure of interbank risk. Journal of Financial Economics 109: 707–33. [Google Scholar] [CrossRef] [Green Version]

- Gallitschke, Janek, Stefanie Seifried, and Frank Thomas Seifried. 2017. Interbank interest rates: Funding liquidity risk and xibor basis spreads. Journal of Banking & Finance 78: 142–52. [Google Scholar]

- Gräb, Johannes, and Thomas Kostka. 2018. Predicting Risk Premia in Short-Term Interest Rates and Exchange Rates. ECB Working Paper Series No 2131; Frankfurt: European Central Bank. [Google Scholar]

- Guimarães, Rodrigo. 2014. Expectations, Risk Premia and Information Spanning in Dynamic Term Structure Model Estimation. Technical Report. London: Bank of England. [Google Scholar]

- Harvey, Campbell R. 1986. Recovering Expectations of Consumption Growth from an Equilibrium Model of the Term Structure of Interest Rates. Ph.D. thesis, University of Chicago, Graduate School of Business, Chicago, IL, USA. [Google Scholar]

- Hevia, Constantino, and Martin Sola. 2018. Bond risk premia and restrictions on risk prices. Journal of Risk and Financial Management 11: 60. [Google Scholar] [CrossRef] [Green Version]

- Hui, Cho-Hoi, Chi-Fai Lo, and Chin-To Fung. 2017. Dynamics of Market Anomalies and Measurement Errors of Risk-Free Interest Rates. HKIMR Working Paper. Hong Kong: Hong Kong Institute for Monetary Research. [Google Scholar]

- Hunzinger, Chadd B., and Coenraad C. A. Labuschagne. 2015. Pricing a collateralized derivative trade with a funding value adjustment. Journal of Risk and Financial Management 8: 17–42. [Google Scholar] [CrossRef] [Green Version]

- Jennison, Fraser. 2017. Estimation of the Term Premium within Australian Treasury Bonds; Working Paper. Canberra: Australian Office of Financial Management, pp. 18–83.

- Joslin, Scott, Kenneth J. Singleton, and Haoxiang Zhu. 2011. A new perspective on Gaussian dynamic term structure models. The Review of Financial Studies 24: 926–70. [Google Scholar] [CrossRef]

- Jotikasthira, Chotibhak, Anh Le, and Christian Lundblad. 2015. Why do term structures in different currencies co-move? Journal of Financial Economics 115: 18–83. [Google Scholar] [CrossRef]

- Kilian, Lutz. 1998. Small-sample confidence intervals for impulse response functions. Review of Economics and Statistics 80: 218–30. [Google Scholar] [CrossRef]

- Krippner, Leo. 2015. Zero Lower Bound Term Structure Modeling: A Practitioner’s Guide. Berlin: Springer. [Google Scholar]

- Kumar, Ronald Ravinesh, Peter Josef Stauvermann, and Hang Thi Thu Vu. 2021. The relationship between yield curve and economic activity: An analysis of g7 countries. Journal of Risk and Financial Management 14: 62. [Google Scholar] [CrossRef]

- Liu, Jun, Francis A. Longstaff, and Ravit E. Mandell. 2006. The market price of risk in interest rate swaps: The roles of default and liquidity risks. The Journal of Business 79: 2337–59. [Google Scholar] [CrossRef] [Green Version]

- Malik, Sheheryar, and Andrew Meldrum. 2016. Evaluating the robustness of UK term structure decompositions using linear regression methods. Journal of Banking & Finance 67: 85–102. [Google Scholar]

- McCoy, Eric. 2019. A Calibration of the Term Premia to the Euro Area. Technical Report. Brussels: Directorate General Economic and Financial Affairs (DG ECFIN). [Google Scholar]

- Moessner, Richhild. 2018. Effects of asset purchases and financial stability measures on term premia in the Euro area. Applied Economics 50: 4617–31. [Google Scholar] [CrossRef]

- Mönch, Emanuel. 2019. The term structures of global yields. BIS Papers 102: 3–15. [Google Scholar]

- Oprea, Andreea. 2022. The use of principal component analysis (pca) in building yield curve scenarios and identifying relative-value trading opportunities on the romanian government bond market. Journal of Risk and Financial Management 15: 247. [Google Scholar] [CrossRef]

- Pope, Alun Lloyd. 1990. Biases of estimators in multivariate non-gaussian autoregressions. Journal of Time Series Analysis 11: 249–58. [Google Scholar] [CrossRef]

- Priebsch, Marcel. 2013. Computing arbitrage-free yields in multi-factor Gaussian shadow-rate term structure models. FEDS Working Paper 63: 1–35. [Google Scholar]

- Rebonato, Riccardo. 2018. Bond Pricing and Yield Curve Modeling: A Structural Approach. Cambridge: Cambridge University Press. [Google Scholar]

- Rudebusch, Glenn D., Brian P. Sack, and Eric T. Swanson. 2006. Macroeconomic implications of changes in the term premium. FRB of San Francisco Working Paper 89: 241–69. [Google Scholar]

- Sekkel, Rodrigo. 2011. International evidence on bond risk premia. Journal of Banking & Finance 35: 174–81. [Google Scholar]

- Van Dijk, Marcel T. P., Cornelis S. L. De Graaf, and Cornelis W. Oosterlee. 2018. Between and : The measure for pricing in asset liability management. Journal of Risk and Financial Management 11: 67. [Google Scholar] [CrossRef] [Green Version]

- Wright, Jonathan H. 2011. Term premia and inflation uncertainty: Empirical evidence from an international panel dataset. American Economic Review 101: 4514–34. [Google Scholar] [CrossRef] [Green Version]

- Wright, Jonathan H. 2014. Term premia and inflation uncertainty: Empirical evidence from an international panel dataset: Reply. American Economic Review 104: 138–41. [Google Scholar] [CrossRef]

- Wu, Jing Cynthia, and Fan Dora Xia. 2016. Measuring the macroeconomic impact of monetary policy at the zero lower bound. Journal of Money, Credit and Banking 48: 253–91. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Tenor | Mean | Std. dev | Min | Max | 1 | 2 |

|---|---|---|---|---|---|---|

| 6m | 2.79 | 1.94 | 0.34 | 7.87 | 0.98 | 0.60 |

| 1y | 2.76 | 1.87 | 0.36 | 7.58 | 0.98 | 0.62 |

| 2y | 2.92 | 1.82 | 0.31 | 7.57 | 0.98 | 0.68 |

| 3y | 3.05 | 1.77 | 0.31 | 7.43 | 0.98 | 0.73 |

| 5y | 3.27 | 1.70 | 0.38 | 7.24 | 0.98 | 0.77 |

| 7y | 3.46 | 1.66 | 0.50 | 7.14 | 0.98 | 0.79 |

| 10y | 3.65 | 1.62 | 0.68 | 7.08 | 0.99 | 0.80 |

| Model | 1y | 2y | 3y | 5y | 7y | 10y |

|---|---|---|---|---|---|---|

| ACM | 2.79 | 1.94 | 0.34 | 7.87 | 0.98 | 0.6 |

| JSZ | 2.76 | 1.87 | 0.36 | 7.58 | 0.98 | 0.62 |

| Tenor | Model | EU | RA | MOVE | OBX IV |

|---|---|---|---|---|---|

| 2y | ACM | 0.59 | 0.56 | 0.67 | 0.75 |

| JSZ | 0.60 | 0.47 | 0.63 | 0.66 | |

| 5y | ACM | 0.33 | 0.27 | 0.63 | 0.60 |

| JSZ | 0.33 | 0.26 | 0.62 | 0.59 | |

| 10y | ACM | 0.29 | 0.22 | 0.58 | 0.54 |

| JSZ | 0.29 | 0.24 | 0.59 | 0.56 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

de Lange, P.E.; Risstad, M.; Semmen, K.; Westgaard, S. Term Premia in Norwegian Interest Rate Swaps. J. Risk Financial Manag. 2023, 16, 188. https://doi.org/10.3390/jrfm16030188

de Lange PE, Risstad M, Semmen K, Westgaard S. Term Premia in Norwegian Interest Rate Swaps. Journal of Risk and Financial Management. 2023; 16(3):188. https://doi.org/10.3390/jrfm16030188

Chicago/Turabian Stylede Lange, Petter Eilif, Morten Risstad, Kristian Semmen, and Sjur Westgaard. 2023. "Term Premia in Norwegian Interest Rate Swaps" Journal of Risk and Financial Management 16, no. 3: 188. https://doi.org/10.3390/jrfm16030188