The Blue Bond Market: A Catalyst for Ocean and Water Financing

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

2. Sustainable Bonds

2.1. Bonds as a Financial Instrument

2.2. Sustainable Bonds as an Emerging Debt Category

3. Blue Bonds: A New Type of Sustainable Bonds

3.1. Definition

3.2. The Case for Ocean Financing

3.2.1. Interlinkages between the Ocean, Climate Change, and Sustainability

3.2.2. Lack of Funding

3.2.3. Economic Potential of the Oceans

3.3. Freshwater Conservation and the Connection between Blue Bonds and Water Bonds

3.4. Blue Bonds for Ocean and Freshwater Financing: Current State of the Literature

3.4.1. Need for Clarity on Definition and Use of Proceeds

3.4.2. Impact Metrics as an Enabler for Sustainable Ocean Development

3.4.3. Blue Bond Issuance Size and Participants

3.4.4. Blue Bond Yields and Coupon Rates

4. Methodology

4.1. Scope of Research

4.2. Research Methodology

4.3. Research Contribution

5. The State of Blue Bonds

5.1. Use of Proceeds

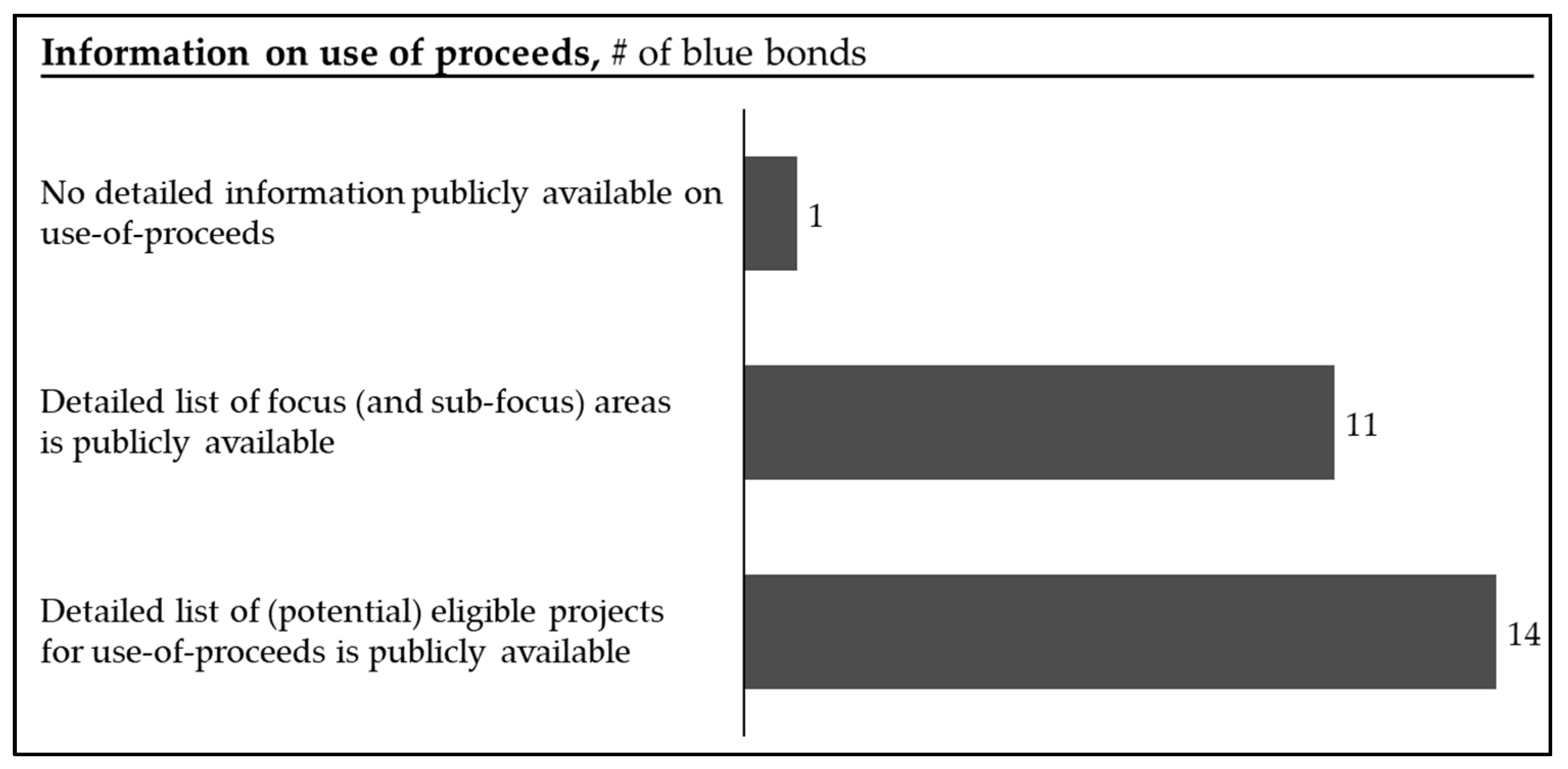

5.1.1. Use of Proceeds Data Availability

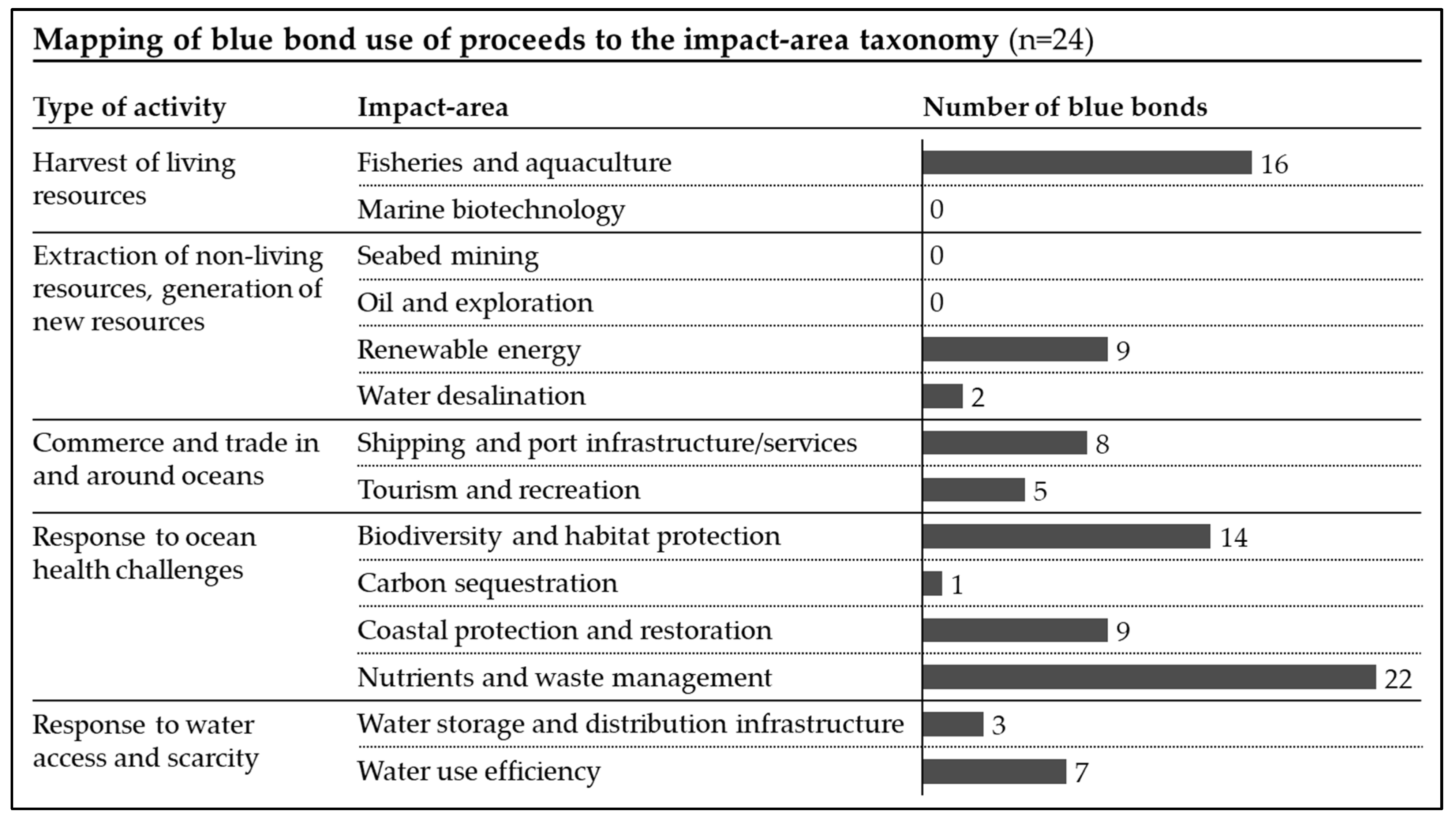

5.1.2. Overview of Use of Proceeds in Blue Bond Database

5.1.3. Discussion on Use of Proceeds

5.2. Impact-Metric Assessment

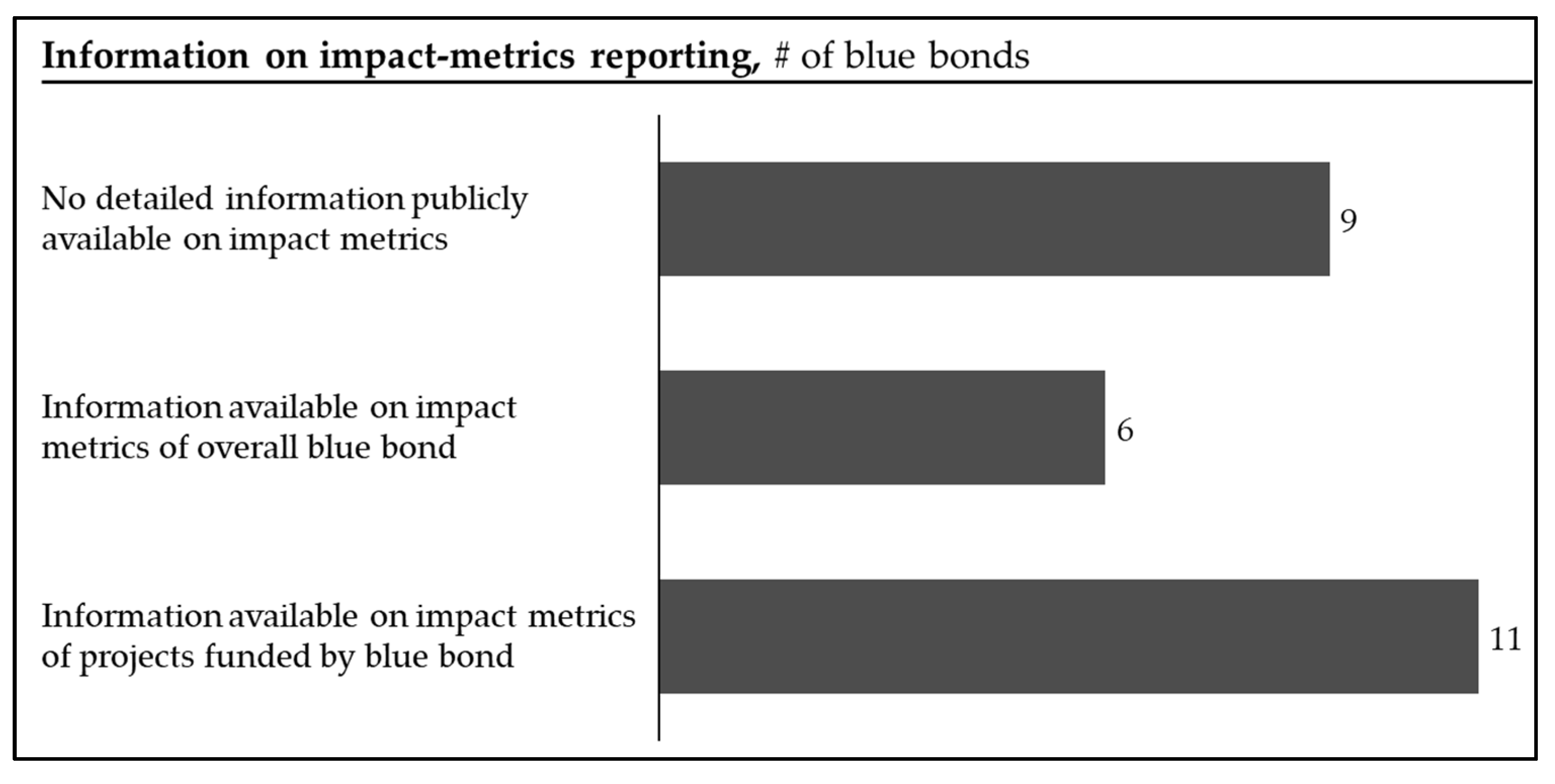

5.2.1. Impact-Metric Data Availability

5.2.2. Overview of Impact Metrics Used in Blue Bond Database

5.2.3. Discussion

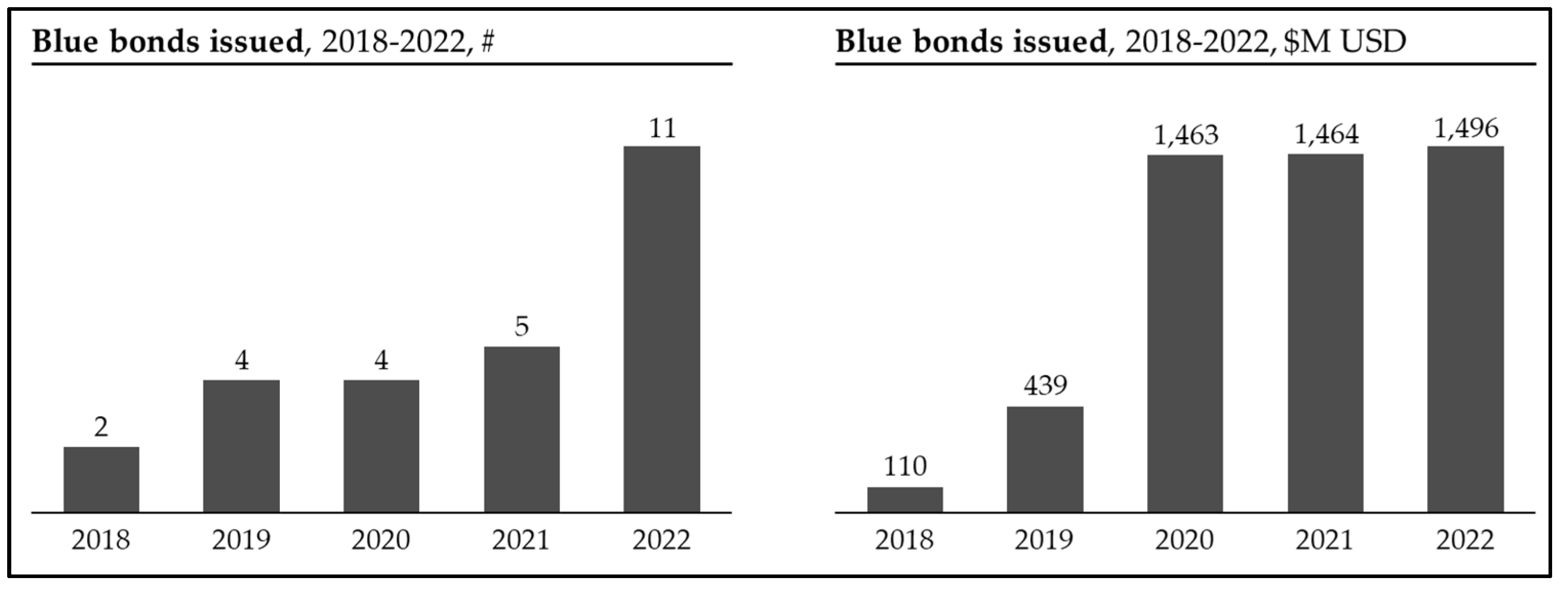

5.3. Overview of the Blue Bond Market between 2018–2022

5.3.1. Total Size of the Market

5.3.2. Average Size of Blue Bonds

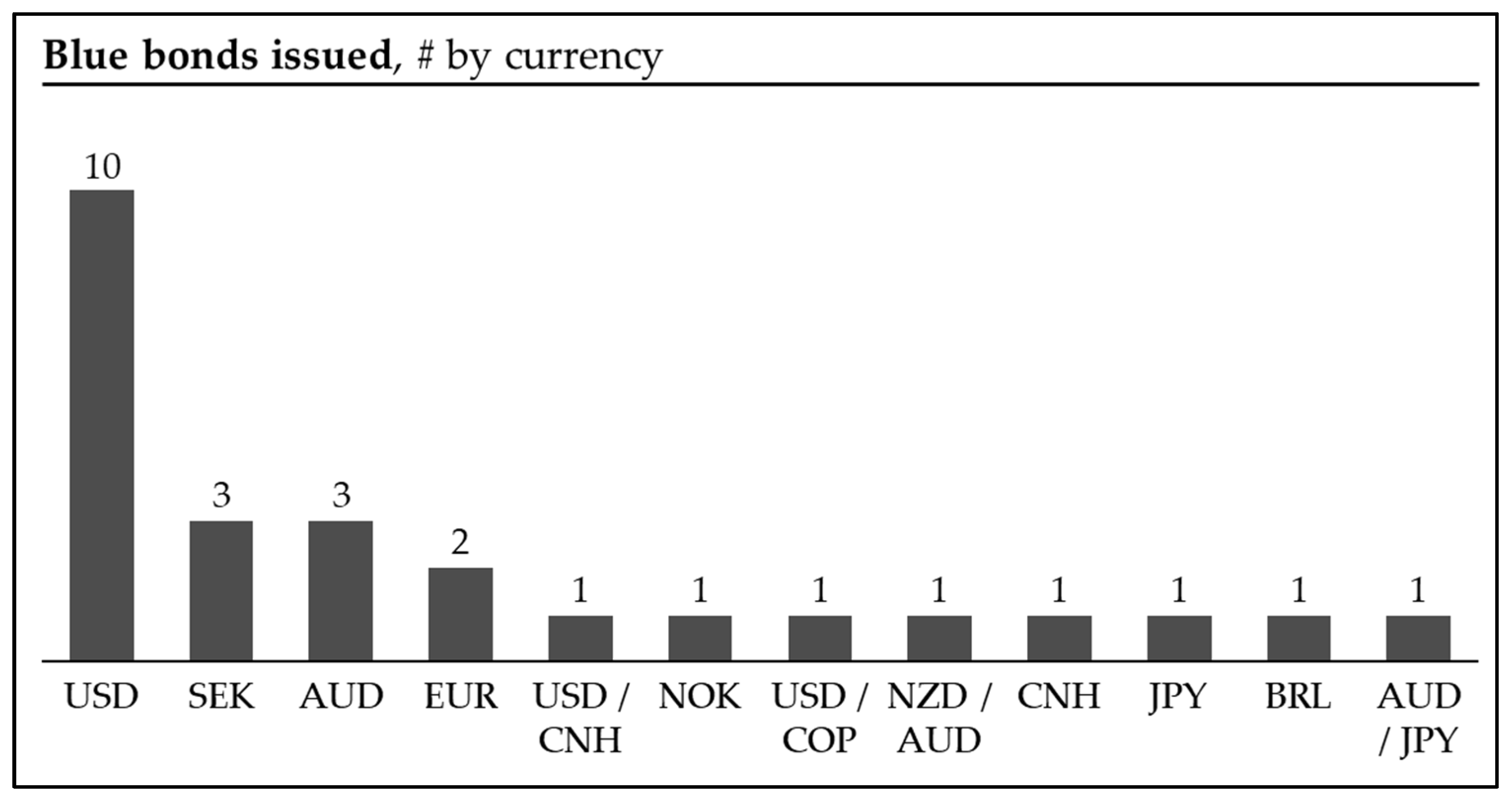

5.3.3. Currency of Blue Bond Issuances

5.3.4. Maturity of Blue Bonds

5.3.5. Coupon Interest Rates of Blue Bonds

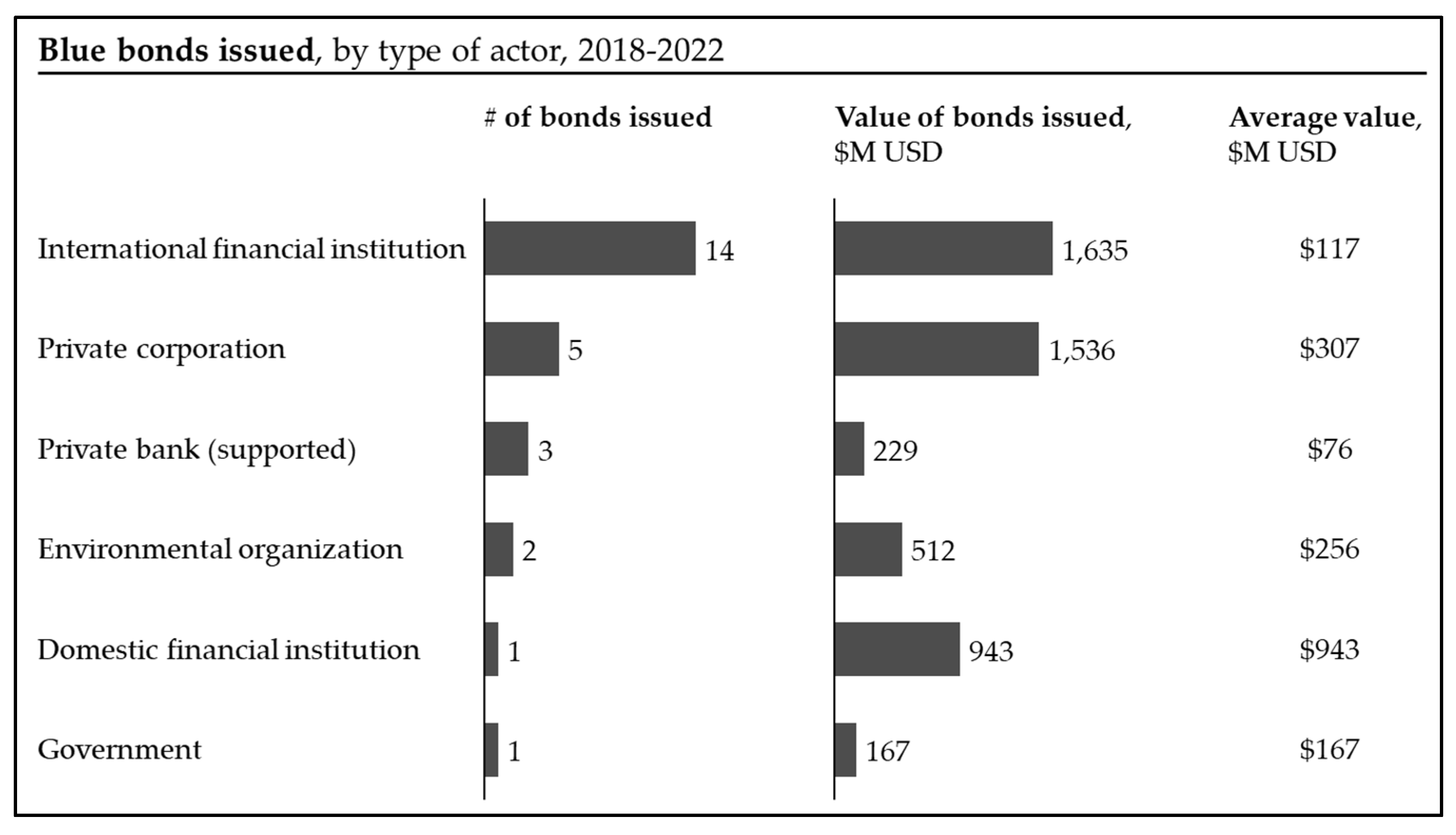

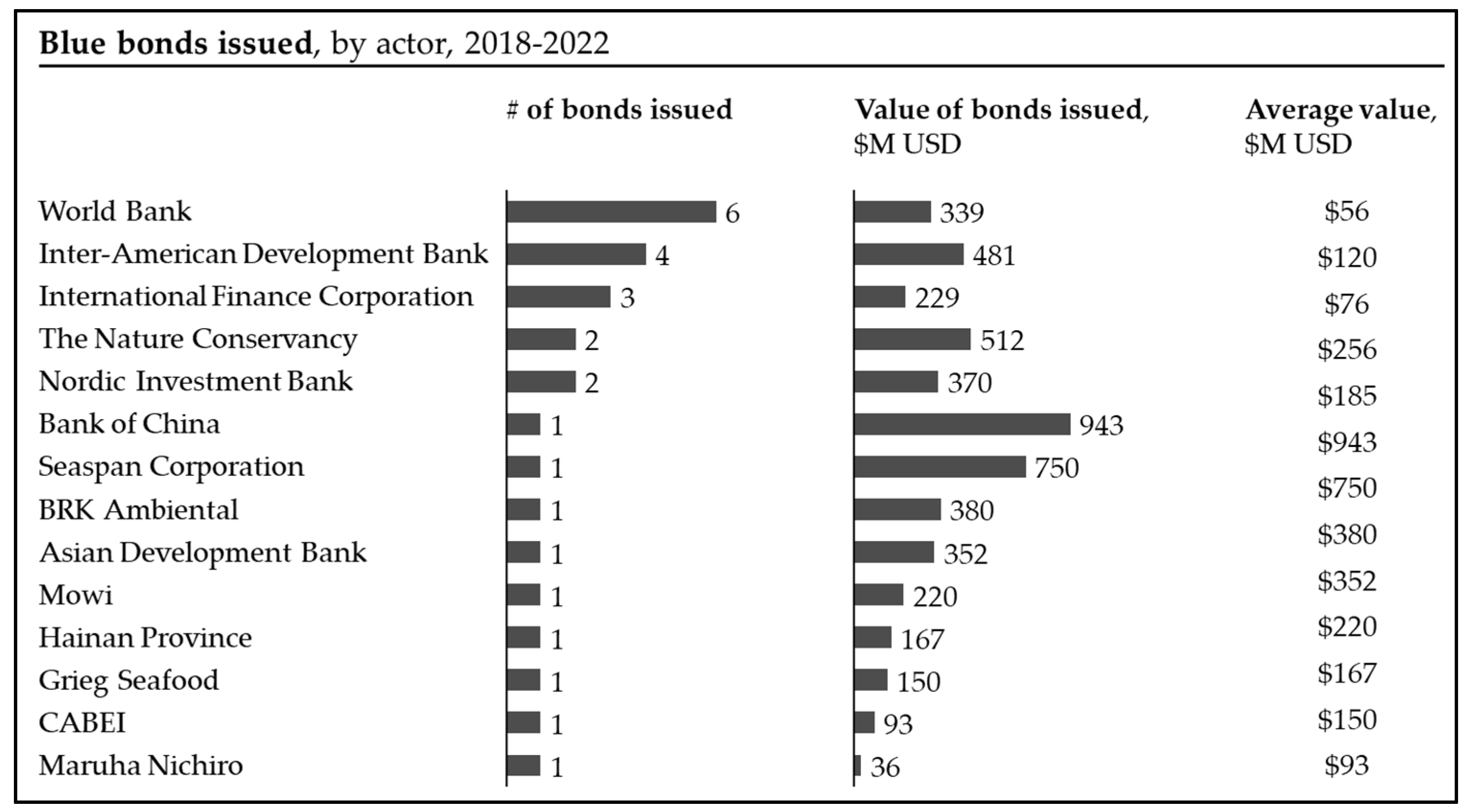

5.4. Blue Bond Market Actors

- -

- The World Bank has issued five blue bonds for a total of USD 324M, in line with its PROBLUE program established in 2018 to support the implementation of SDG14 and the “sustainable and integrated development of oceanic sectors in healthy oceans” (World Bank 2022b). The World Bank also supported the Seychelles with a partial guarantee in its USD 15M blue bond (World Bank 2018a).

- -

- The Inter-American Development Bank has issued three blue bonds worth USD 96M under its Sustainable Debt Framework (IDB 2020), and provided a USD 200M policy-based guarantee in the Government of The Bahamas (2022)’s USD 385M blue bond.

- -

- The International Finance Corporation released its “Guidelines for Blue Finance” in 2022 (IFC 2022c) and supported three financial corporations to issue blue bonds and develop their own blue bond framework. Banks were supported in Thailand, the Philippines, and Ecuador for issuances of USD 50M, USD 100M, and USD 79M, respectively.

- -

- -

- The Nordic Investment Bank has issued two blue bonds worth USD 370M with a focus “only on investments within water management and protection category”. The bonds aim to attract “investors that are conscious of the challenges facing the region’s water resources, especially those affecting the Baltic Sea”, such as eutrophication and water infrastructure depletion (NIB 2019a, n.d.b).

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A. List of Blue Bonds Issuances

| # | Release | Issuer | Amount (USD M) | Currency | Redemption | Sources |

| 1 | Aug 18 | World Bank (IBRD) | 95 | SEK | 7 years | (Rosane 2018; World Bank 2018d, 2018e) |

| 2 | Oct 18 | Government of Seychelles | 15 | USD | 10 years | (World Bank 2018a, 2018b, 2018c) |

| 3 | Jan 19 | Nordic Investment Bank | 220 | SEK | 5 years | (NIB 2019b, 2019c, 2021; NIB and SEB 2019) |

| 4 | Apr 19 | World Bank (IBRD) | 10 | USD | 3 years | (Morgan Stanley 2019; World Bank 2019c) |

| 5 | May 19 | World Bank (IBRD) | 180 | EUR | 20 years | (Rosane 2018; World Bank 2018d, 2019b) |

| 6 | Nov 19 | World Bank (IBRD) | 29 | USD | 5 years | (World Bank 2019a) |

| 7 | Jan 20 | Mowi ASA | 220 | EUR | 5 years | (Mowi 2020a, 2020b, 2020c, 2022) |

| 8 | Oct 20 | Nordic Investment Bank | 150 | SEK | 5 years | (NIB 2020; NIB et al. 2020) |

| 9 | Nov 20 | Grieg Seafood–Jun 2020 Grieg Seafood–Nov 2020 | 100 50 | USD | 5 years 5 years | (CICERO 2020; Grieg Seafood 2020a, 2020b, 2020c, 2020d, 2022) |

| 10 | Nov 20 | Bank of China–CNH tranche Bank of China–USD tranche | 443 500 | CNH, USD | 2 years 3 years | (BOC 2020a, 2020b, 2020c; Davis 2020; Ernst & Young 2020, 2022) |

| 11 | May 21 | World Bank (IBRD) | 10 | USD, COP | 5 years | (World Bank 2021a, 2021b, 2021c, 2021d) |

| 12 | Jul 21 | Seaspan Corp | 750 | USD | 8 years | (Seaspan 2021a, 2021b; Sustainalytics 2021) |

| 13 | Sep 21 | Asian Development Bank–AUD Asian Development Bank–NZD | 151 151 | AUD, NZD | 15 years 10 years | (Asian Development Bank 2021a, 2021b, 2022a) |

| 14 | Nov 21 | IDB Invest | 37 | AUD | 10 years | (IDB 2020, 2021a, 2021b) |

| 15 | Nov 21 | Government of Belize | 365 | USD | 20 years | (Credit Suisse 2021; TNC 2021a, 2021b) |

| 16 | May 22 | TMBThanachart Bank | 50 | USD | 5 years | (IFC 2022e; TMBThanachart 2022a, 2022b, 2022c) |

| 17 | Jun 22 | The Commonwealth of the Bahamas | 385 | USD | 7–14 years | (Government of The Bahamas 2022; IDB 2022a; West 2022) |

| 18 | Jun 22 | BDO Unibank Philippines | 100 | USD | 7 years | (BDO 2022a, 2022b; IFC 2022b) |

| 19 | Oct 22 | Government of Barbardos | 147 | USD | 15 years | (Government of Barbados 2022a, 2022b; TNC 2022) |

| 20 | Oct 22 | IDB Invest | 25 | AUD | 15 years | (IDB 2020, 2022d) |

| 21 | Nov 22 | People’s Government of Hainan Province | 167 | CNH | 2 years | (Credit Agricole 2022; HKSAR Government 2022; Linklaters 2022) |

| 22 | Nov 22 | Maruha Nichiro Corporation | 36 | JPY | 5 years | (Maruha Nichiro Corporation 2022a, 2022b, 2022c) |

| 23 | Nov 22 | IDB Invest | 34 | AUD | 20 years | (IDB 2020, 2022c) |

| 24 | Nov 22 | Banco Internacional | 79 | USD | 4 years | (Banco Internacional 2022; IFC 2022a, 2022d) |

| 25 | Nov 22 | BRK Ambiental | 380 | BRL | 20 years | (BRK Ambiental 2022a, 2022b; Environmental Finance 2022; Sustainalytics 2022b) |

| 26 | Dec 22 | CABEI–AUD CABEI–JPY | 21 72 | AUD, JPY | 5 years 5 years | (CABEI 2022a, 2022b; Sustainalytics 2022a) |

Appendix B. Mapping of the Blue Bonds

| 2018 | 2019 | 2020 | 2021 | 2022 | |||||||||||||||||||||||

| Type of Activity | Impact Area | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 | 19 | 20 | 21 | 22 | 23 | 24 | 25 | 26 |

| Harvest of living resources | Fisheries and aquaculture | X | X | X | X | X | X | X | X | X | X | X | X | X | X | X | X | ||||||||||

| Marine biotechnology | |||||||||||||||||||||||||||

| Extraction of non-living resources, generation of new resources | Seabed mining | ||||||||||||||||||||||||||

| Oil and exploration | |||||||||||||||||||||||||||

| Renewable energy | X | X | X | X | X | X | X | X | X | ||||||||||||||||||

| Water desalination | X | X | |||||||||||||||||||||||||

| Commerce and trade in and around oceans | Shipping and port infrastructure/services | X | X | X | X | X | X | X | X | ||||||||||||||||||

| Tourism and recreation | X | X | X | X | X | ||||||||||||||||||||||

| Response to ocean health challenges | Biodiversity and habitat protection | X | X | X | X | X | X | X | X | X | X | X | X | X | X | ||||||||||||

| Carbon sequestration | X | ||||||||||||||||||||||||||

| Coastal protection and restoration | X | X | X | X | X | X | X | X | X | ||||||||||||||||||

| Nutrients and waste management | X | X | X | X | X | X | X | X | X | X | X | X | X | X | X | X | X | X | X | X | X | X | |||||

| Response to water access and scarcity | Water storage and distribution infrastructure | X | X | X | |||||||||||||||||||||||

| Water use efficiency | X | X | X | X | X | X | X | ||||||||||||||||||||

Appendix C. Details per Blue Bond

| AUGUST 2018: WORLD BANK SUSTAINABLE DEVELOPMENT BOND | |

| Issuer | World Bank |

| Amount ($) | 95M USD |

| Currency | SEK (1 billion) |

| Redemption | 7 years |

| Coupon | 0.625% (issue price 99.172%) |

| Investors | AP1, SEB Företagsobligationsfond, SPP Storebrand, Swedbank Robur Fonder AB |

| Concessionary financing | Unspecified |

| Other actors | SEB (Lead manager) |

| Use-of-proceeds | “- Sustainable use of water in order to increase access to safe and reliable water sources - Sustainable use of ocean resources and marine life” The sustainable development bond is part of an initiative to highlight the critical role of water and ocean resources and mentions a focus on “conservation and sustainable use of fresh and salt water resources”, “sustainable water management to ensure access to safe water and water security” and “sustainable use of ocean and marine resources”, “strong governance of marine and coastal resources to support sustainable fisheries and aquaculture”, more resilient coastlines, “[…] coastal and marine protected areas, and reduce[d] pollution” |

| Geography | Unspecified |

| Impact metrics | Unspecified |

| Notes | |

| Sources | (Rosane 2018; World Bank 2018d, 2018e) |

| OCTOBER 2018: SEYCHELLES BLUE BOND | |

| Issuer | Government of Seychelles |

| Amount ($) | 15M USD |

| Currency | US dollar |

| Redemption | 10 years |

| Coupon | 6.50% |

| Investors | Prudential, Calvert Impact Capital, Nuveen |

| Concessionary financing | The World Bank (partial guarantor), Global Environment Facility (concessional loan) |

| Other actors | BNY Mellon (trustee), Standard Chartered Bank (placement agent), Rockefeller Foundation (donor), Seychelles Conservation and Climate Adaptation Trust (grant manager), Development Bank of Seychelles (loan fund manager) |

| Use-of-proceeds | “Expansion of sustainable-use marine protected areas, improved governance of priority fisheries, project management and coordination, promotion of sustainable practices, fisheries management planning, education awareness programs, stock rebuilding, refitting fishing vessels, aquaculture development” |

| Geography | Seychelles |

| Impact metrics | Increase the sustainable-use marine protected areas to 30% by 2020 |

| Notes | The Rockefeller Foundation granted 425,000 USD to assist with the transaction costs for the Bond (e.g., the legal fees). Projects are funded through the Blue Grant Fund, which provides grants (up to 70K USD) to fund early-stage innovations to de-risk business ideas as well as the Blue Investment Fund, which provides loans of 50K to 3M USD to projects at an interest rate of 4%. |

| Sources | (World Bank 2018a, 2018b, 2018c) |

| JANUARY 2019: NORDIC-BALTIC BLUE BOND | |

| Issuer | Nordic Investment Bank (NIB) |

| Amount ($) | 220M USD |

| Currency | SEK (2 billion) |

| Redemption | 5 years |

| Coupon | 0.375% |

| Investors | 89% investors are based in Sweden, 11% elsewhere. 48% of investors are pension funds or institutional investors, 40% asset managers or funds, 12% banks, and <1% are retail or private investors. Investors included AMF, AP3, Captor, Cliens Kapitalförvaltning, Handelsbanken, LF Jönköping, LF Treasury, SEB Investment Management, WWF, Öhman Fonder, Swedbank Robur. |

| Concessionary financing | None mentioned |

| Other actors | SEB (lead manager) |

| Use-of-proceeds | “- Wastewater treatment and water pollution prevention: with the aim of reducing discharges into water (mainly phosphorus, nitrogen, organic matter, heavy metals, plastics and pharmaceuticals) - Stormwater systems and flood protection: with the aim of supporting pollution prevention and the development of climate change resilient infrastructure - Protection of water resources: with the aim of minimising groundwater extraction and contamination, and improving the replenishment of aquifers - Protection and restoration of water and marine ecosystems: projects aimed at the extension of protected areas, protection and restoration of water and marine ecosystems, and biodiversity (such as wetlands, rivers and lakes, coastal areas and open sea zones)” In line with NIB’s Environmental Bond Framework in the category “Water management and protection” |

| Geography | Denmark, Estonia, Finland, Iceland, Latvia, Lithuania, Norway, Sweden |

| Impact metrics | Added/upgraded WWTP capacity/connections (997,170 PE up until 12/31/2021 across two NIB blue bonds) Nitrogen discharge (-300 t/a up until 12/31/2021 across two NIB blue bonds) NIB also mentions avoided overflow of untreated wastewater (m³/a), BOD discharge (t/a), Phosphorus discharge (t/a), Energy recovery from wastewater sludge (MWh/a) and GHG emissions (t/a), without impact up until 12/31/2021. |

| Notes | NIB details the financing on a project-by-project basis, linked to their Blue Bond projects. This includes details on the loans granted and their respective impact. |

| Sources | (NIB 2019b, 2019c, 2021; NIB and SEB 2019) |

| APRIL 2019: WORLD BANK & MORGAN STANLEY SUSTAINABILITY BOND | |

| Issuer | World Bank |

| Amount ($) | 10M USD |

| Currency | U.S. dollar |

| Redemption | 3 years |

| Coupon | 2.35% (Year 1), 2.70% (Year 2), 3.15% (Year 3) |

| Investors | Unspecified |

| Concessionary financing | n/a |

| Other actors | Morgan Stanley (lead manager) |

| Use-of-proceeds | “Plastic waste reduction efforts in oceans Promotion of the sustainable use of marine resources in developing countries including scientific research, policy and regulatory reform and cross-sector collaboration.” The bond is issued in line with the World Bank’s Sustainable Development Bond Framework which mentions the “twin goals of eliminating extreme poverty and promoting shared prosperity”. |

| Geography | Developing countries, unspecified |

| Impact metrics | Project-level reporting can be found on the World Bank’s website. Project impact reports include detailed information on project name, country, lifetime, target results, and capital. The individual mapping between the sustainability bond issuance and the projects is not publicly available. |

| Notes | Even though originally described as a “sustainability bond”, this transaction has been frequently referred to as a “blue bond” after given its focus on ocean plastic waste. |

| Sources | (Morgan Stanley 2019; World Bank 2019c) |

| MAY 2019: WORLD BANK SUSTAINABLE DEVELOPMENT BOND | |

| Issuer | World Bank (International Bank for Reconstruction and Development, IBRD) |

| Amount ($) | 180M USD |

| Currency | EUR (200 million) |

| Redemption | 20 years |

| Coupon | CMS10y10y—1.274% |

| Concessionary financing | n/a |

| Other actors | HSBC (lead manager) |

| Use-of-proceeds | Raise awareness for the critical role that water and ocean resources play in development around the world “- Sustainable use of water in order to increase access to safe and reliable water sources - Sustainable use of ocean resources and marine life” The sustainable development bond is part of an initiative to highlight the critical role of water and ocean resources and mentions a focus on “conservation and sustainable use of fresh and salt water resources”, “sustainable water management to ensure access to safe water and water security” and “sustainable use of ocean and marine resources”, “strong governance of marine and coastal resources to support sustainable fisheries and aquaculture”, more resilient coastlines, “[…] coastal and marine protected areas, and reduce[d] pollution” |

| Geography | Global |

| Impact metrics | Unspecified |

| Sources | (Rosane 2018; World Bank 2018d, 2019b) |

| NOVEMBER 2019: WORLD BANK & CREDIT SUISSE SUSTAINABLE DEVELOPMENT BOND | |

| Issuer | World Bank |

| Amount ($) | 28.6M USD |

| Currency | U.S. dollar |

| Redemption | 5 years |

| Coupon | Unspecified |

| Investors | Credit Suisse private wealth management clients (through Credit Suisse’s Low Carbon Blue Economy Note) |

| Concessionary financing | n/a |

| Other actors | Credit Suisse (sole manager) |

| Use-of-proceeds | “Raise awareness for the vital role fresh and saltwater resources play for people, livelihoods, and the planet Promote strong governance of marine and coastal resources to support sustainable fisheries and aquaculture Make coastlines more resilient Establish coastal and marine protected areas Improve solid waste management to reduce pollution in waterways and oceans Sustainable fisheries Ocean waste upcycling” The bond is issued in line with the World Bank’s Sustainable Development Bond Framework which mentions the “twin goals of eliminating extreme poverty and promoting shared prosperity”. |

| Geography | Unspecified |

| Impact metrics | Project-level reporting can be found on the World Bank’s website. Project impact reports include detailed information on project name, country, lifetime, target results, and capital. The individual mapping between the sustainability bond issuance and the projects is not publicly available. |

| Notes | Even though originally described as a “sustainability bond”, this transaction has been frequently referred to as a “blue bond”. |

| Sources | (World Bank 2019a) |

| JANUARY 2020: MOWI GREEN BOND | |

| Issuer | Mowi ASA FRN |

| Amount ($) | $220M USD |

| Currency | Euro (200 million) |

| Redemption | 5 years |

| Coupon | EURIBOR + 1.60% |

| Investors | Unspecified |

| Concessionary financing | n/a |

| Other actors | Danske Bank (global coordinator), DNB markets (green bond advisor), Nordea (joint lead manager), ABN Amro (joint lead manager), Rabobank (joint lead manager), SEB (joint lead manager), CICERO (SPO) |

| Use-of-proceeds |

|

| Geography | Scotland, Norway, Chile, Canada, Faroes |

| Impact metrics | Mowi mentions many KPIs in its Green Bond Framework, including related to the SDG targets:

|

| Sources | (Mowi 2020a, 2020b, 2020c, 2022) |

| OCTOBER 2020: NIB BALTIC SEA BLUE BOND | |

| Issuer | Nordic Investment Bank (NIB) |

| Amount ($) | 150M USD |

| Currency | SEK (1.5 billion) |

| Redemption | 5 years |

| Coupon | 0.10% |

| Investors | Investors were 95% Swedish, 4% Finnish, 1% other European. 69% were fund managers, 30% pension and insurance funds, and 1% retail. Investors included “Folksam Group, Svenska Handelsbanken Asset Management, Nordea Asset Management, Robur Asset Management, Skandia Liv, Storebrand Asset Management” |

| Concessionary financing | Unspecified |

| Other actors | Danske Bank, Swedbank (joint lead managers) |

| Use-of-proceeds | See above (January 2019 Nordic-Baltic Blue Bond) |

| Geography | Denmark, Estonia, Finland, Iceland, Latvia, Lithuania, Norway, Sweden |

| Impact metrics | See above (January 2019 Nordic-Baltic Blue Bond) |

| Notes | See above (January 2019 Nordic-Baltic Blue Bond) |

| Sources | (NIB 2020; NIB et al. 2020) |

| NOVEMBER 2020: GRIEG SEAFOOD GREEN BOND | |

| Issuer | Grieg Seafood |

| Amount ($) | 150M USD (tranche 1 of 100M USD in June 2020; tranche 2 of 50M USD in November 2020) |

| Currency | NOK |

| Redemption | 5 years |

| Coupon | 3m NIBOR + 340 bps |

| Investors | Unspecified |

| Concessionary financing | Unspecified |

| Other actors | DNB markets and Nordea (joint lead managers and green bond advisors) |

| Use-of-proceeds | “Post-smolt production and investments in Newfoundland are the key focus areas.” Proceeds can be invested across four categories:

|

| Geography | Norway, Canada, UK |

| Impact metrics | Impact metrics include: “Sustainable feed

Sustainable farming

Pollution prevention and control

Water and wastewater management

Waste management

|

| Notes | |

| Sources | (CICERO 2020; Grieg Seafood 2020a, 2020b, 2020c, 2020d, 2022) |

| NOVEMBER 2020: BANK OF CHINA’S BLUE BOND | |

| Issuer | Bank of China, Macau Branch and Paris Branch |

| Amount ($) | 942.5M USD |

| Currency | CNH (3 billion), U.S. dollar (500 million) |

| Redemption | 2 years (CNH), 3 years (U.S. dollar) |

| Coupon | 3.15% at par (CNH), 0.95% at 99.694 (U.S. dollar) |

| Investors | CNH: 96% sold in Asia, 3% in US, 1% in Europe. 46% to banks and financial institutions, 27% to asset managers, 19% to private banks and 8% to insurers and others. USD: 59% sold in Asia, 41% in EMEA. 42% to banks, 18% to central banks and sovereign wealth funds, 17% to fund managers and asset managers, 10% to corporations, 8% to private banks and others, 5% to insurers. |

| Concessionary financing | n/a |

| Other actors | CNH: BOC, Credit Agricole, BNP Paribas, Agricultural Bank of China Hong Kong, Citi, DBS, KGI Asia, Mizuho and Scotiabank (global coordinators) USD: BOC, Credit Agricole, BNP Paribas, Natixis, Société General (global coordinators) ABC Hong Kong, CCB International, China International Capital Corp (lead managers, bookrunners) Ernst & Young (independent external review provider) |

| Use-of-proceeds | “Renewable energy: including the production and transmission of renewable energy, and the manufacturing of renewable energy appliances and products; renewable energy includes solar energy, onshore and offshore wind energy and biomass energy Sustainable water and wastewater management: including sustainable infrastructure for clean and/or drinking water, wastewater treatment, sustainable urban drainage systems and river training and other forms of flooding mitigation” The Appendix Report on Pre-Issuance of BOC’s 2020 Blue Bonds includes 25 nominated projects for a total of 7.1B RMB. 58% of this amount relates to sustainable water and wastewater management (e.g., marine related sewage treatment project), and 42% relate to offshore wind projects. At the end of 2021, Ernst and Young stated that the full 6.3B RMB (100% of the proceeds) had been disbursed. 79% of this had been allocated to renewable energy, and 21% to sustainable water and wastewater management. |

| Geography | The Appendix report states the following regions for funding of the nominated projects: 30% Eastern China, 3% Northern China, 54% Southern China, 6% United Kingdom, 7% France. Ernst & Young’s statement on the disbursement of proceeds does not mention the real geographical allocation. |

| Impact metrics | Incremental sewage treatment capacity of 6,176,161 m3/day. Increase of 2987 MW installed capacity for offshore wind power project. GHG emission reductions. No impact figures are reported in Ernst & Young’s statement on the disbursement of proceeds. |

| Notes | BOC is the first commercial bank to issue a blue bond |

| Sources | (BOC 2020a, 2020b, 2020c; Davis 2020; Ernst & Young 2020, 2022) |

| MAY 2021: WORLD BANK & JP MORGAN SUSTAINABLE DEVELOPMENT BOND | |

| Issuer | World Bank |

| Amount ($) | 10M USD |

| Currency | Payable in U.S. dollar, but issued in Colombian pesos (37.275 billion) |

| Redemption | 5 years |

| Coupon | 4.75% |

| Investors | Fiera Capital (sole investor) |

| Concessionary financing | n/a |

| Other actors | JP Morgan Securities (lead manager) |

| Use-of-proceeds | Access to clean water and the sustainable use of ocean and marine resources (SDG 6 and SDG 14). No specific projects specified. The bond is issued in line with the World Bank’s Sustainable Development Bond Framework which mentions the “twin goals of eliminating extreme poverty and promoting shared prosperity”. |

| Geography | IBRD’s member countries |

| Impact metrics | Project-level reporting can be found on the World Bank’s website. Project impact reports include detailed information on project name, country, lifetime, target results, and capital. The individual mapping between the sustainability bond issuance and the projects is not publicly available. |

| Sources | (World Bank 2021a, 2021b, 2021c, 2021d) |

| JULY 2021: SEASPAN CORP BLUE TRANSITION BOND | |

| Issuer | Seaspan Corporation |

| Amount ($) | 750M USD |

| Currency | U.S. dollar |

| Redemption | 8 years |

| Coupon | 5.50% |

| Investors | Unspecified |

| Concessionary financing | Unspecified |

| Other actors | Sustainalytics (SPO) |

| Use-of-proceeds | Eligible Projects under Seaspan’s Blue Transition Bond issuance include:

Eligible containership newbuild projects will feature:

|

| Geography | Unspecified |

| Impact metrics | Reduce GHG emissions by 50% by 2050 compared to 2008, in line with the International Marine Organization’s (IMO) goal Sustainalytics (in their SPO) notes that this is not in line with a two-degree climate scenario. |

| Notes | Seaspan’s blue bond is issued in connection with its “Blue Transition Bond Framework”, which his aligned with ICMA’s Green Bond Principles and the “Climate Transition Finance Handbook 2020”. |

| Sources | (Seaspan 2021a, 2021b; Sustainalytics 2021) |

| SEPTEMBER 2021: ADB BLUE BOND FOR OCEAN INVESTMENTS | |

| Issuer | Asian Development Bank (ADB) |

| Amount ($) | 352M USD |

| Currency | AUD (208 million), NZD (217 million) |

| Redemption | 15 years (AUD), 10 years (NZD) |

| Coupon | 1.8% (AUD), 2.1525% (NZD) |

| Investors | The Dai-chi Life Insurance Company (AUD), Meiji Yasuda Life Insurance Company (NZD) |

| Concessionary financing | Unspecified |

| Other actors | Citigroup Global Markets (arranger, AUD), Credit Agricole CIB (arranger, NZD) CICERO Shades of Green (Second Party Opinion) |

| Use-of-proceeds | Reduce waste flow to ocean, reduce greenhouse gas emissions, reduce “non-point source pollution to the marine environment from ‘source to sea’ by supporting green farming and controlling pesticide and fertilizer use” ADB’s Blue Bond Framework includes the following projects as eligible to be funded by blue bond proceeds:

|

| Geography | Asia and the Pacific (e.g., Maldives, China) |

| Impact metrics | Unspecified |

| Notes | The Blue Bond is part of ADB’s “Action Plan for Healthy Oceans and Sustainable Blue Economies launched in 2019, which aims to catalyze sustainable investments in Asia and the Pacific by committing to invest and provide technical assistance of at least $5 billion by 2024”. |

| Sources | (Asian Development Bank 2021a, 2021b, 2022a) |

| NOVEMBER 2021: IDB INVEST BLUE BOND | |

| Issuer | Inter-American Investment Corporation (IDB Invest) |

| Amount ($) | 37M USD |

| Currency | AUD (50 million) |

| Redemption | 10 years |

| Coupon | 2.2% |

| Investors | Unspecified |

| Concessionary financing | Unspecified |

| Other actors | TD Securities (Lead manager) |

| Use-of-proceeds | Projects contributing to the “UN Sustainable Development Goal 6, expanding clean water and sanitation to people in the region” The bond is issued in line with IDB Invest’s “Sustainable Debt Framework”. The Framework does not explicitly mention blue bonds but does mention “climate change adaptation and climate resilience” and “sustainable water and wastewater management” in its Green Bond categories. |

| Geography | Caribbean and Latin America |

| Impact metrics | Unspecified |

| Notes | The bond is the first blue bond in Latin America and the Caribbean, and “lays the groundwork for future blue bonds that finance projects in other industries, such as low-carbon and resilient ports, the circular economy and sustainable tourism.” IDB Invest released its report “Accelerating Blue Bonds Issuances” together with the UN Global Compact and describes a list of blue projects based on “multi-stakeholder collaboration [which] has contributed to an increasing convergence around what constitutes blue”. It mentions the following categories:

|

| Sources | (IDB 2020, 2021a, 2021b) |

| NOVEMBER 2021: TNC BLUE BONDS FOR CONSERVATION – BELIZE’S BLUE BOND | |

| Issuer | Government of Belize |

| Amount ($) | 365M USD |

| Currency | U.S. dollar |

| Redemption | 20 years |

| Coupon | TBC |

| Investors | The Nature Conservancy |

| Concessionary financing | U.S. International Development Finance Corporation (political risk insurance) |

| Other actors | The Nature Conservancy (initiative taker), Credit Suisse (sole structurer and arranger), |

| Use-of-proceeds | Marine protection, sustainable economic development and addressing climate change |

| Geography | Belize |

| Impact metrics | “Key commitments are as follows:

|

| Notes | The financial transaction is set up as a debt-for-nature swap. The proceeds will be used by Belize to repurchase some of its bonds to “reduce debt service costs” by 12% of its GDP. 23.5M USD will be placed into an endowment “that will set aside funding for marine conservation accessible from 2041”. In addition, “approximately USD 4 mn annually, paid in Belize dollars, over the next 20 years will flow to a new, independent conservation fund for Belize, which will disburse funds to marine and coastal conservation projects.” Belize’s Blue Bond is the inaugural transaction part of TNC’s “Blue Bonds for Conservation” project which was launched in 2019 and committed 40.5M to refinance 1.6B in debt. |

| Sources | (Credit Suisse 2021; TNC 2021a, 2021b) |

| OCTOBER 2022: TMBTHANACHART BANK BLUE BOND | |

| Issuer | TMBThanachart Bank |

| Amount ($) | 50M USD |

| Currency | U.S. dollar |

| Redemption | 5 years |

| Coupon | 6 months term SOFR + 1.15% |

| Investors | International Finance Corporation |

| Concessionary financing | Unspecified |

| Other actors | S&P Global (SPO) |

| Use-of-proceeds | Renewable energy, based on following criteria:

Sustainable water and wastewater management:

Pollution prevention and waste management:

Sustainable management of natural resources:

|

| Geography | Unspecified |

| Impact metrics | TMBThanachart maps its “Green and Blue Bond Framework” to the SDG targets:

|

| Sources | (IFC 2022e; TMBThanachart 2022a, 2022b, 2022c) |

| JUNE 2022: BAHAMAS BLUE BLOND | |

| Issuer | The Commonwealth of The Bahamas |

| Amount ($) | 385M USD (consisting of 135M USD in Series A notes and 250M USD in Series B notes) |

| Currency | U.S. dollar |

| Redemption | 14 years (Series A notes) and 7 years (Series B notes) |

| Coupon | 3.850% (Series A notes), 9.000% (Series B notes) |

| Investors | Unspecified |

| Concessionary financing | Inter-American Development Bank ($200M policy-based guarantee) |

| Other actors | Goldman Sachs, Oppenheimer & Co (leads) |

| Use-of-proceeds | Support the blue economy |

| Geography | Bahamas |

| Impact metrics | Unspecified |

| Sources | (Government of The Bahamas 2022; IDB 2022a; West 2022) |

| JUNE 2022: BDO BLUE BOND | |

| Issuer | BDO Unibank |

| Amount ($) | 100M USD |

| Currency | U.S. dollar |

| Redemption | 7 years |

| Coupon | Unspecified |

| Investors | International Finance Corporation |

| Concessionary financing | Unspecified |

| Other actors | Unspecified |

| Use-of-proceeds | “Address the depletion of the blue economy and the scarcity of clean water resources, including activities aimed at combating marine plastics, improving ocean projection, and sustainable water management” “Expand financing for projects that help prevent marine pollution and preserve clean water resources, while supporting the country’s climate goals” |

| Geography | Philippines |

| Impact metrics | Unspecified |

| Notes | Blue bond adheres to ICMA’s Green Bond Principles and IFC’s Blue Finance Guidelines IFC will help BDO expand its Sustainable Finance Framework and “launch a framework for blue bond issuance that will help support further issuances in this space” |

| Sources | (BDO 2022a, 2022b; IFC 2022b) |

| OCTOBER 2022: BARBADOS BLUE BOND | |

| Issuer | Government of Barbados |

| Amount ($) | 146.5M USD |

| Currency | U.S. dollar, local currency |

| Redemption | 15 years |

| Coupon | Unspecified The debt conversion allowed the Government of Barbados to repurchase a $77.6M 6.500% note due 2029 and a $72.9M “Series E 8% bonds due 2043”. |

| Investors | Unspecified |

| Concessionary financing | TNC, 50M USD guarantee Inter-American Development Bank (IDB), 100M USD guarantee |

| Other actors | Credit Suisse (Global Lead Arranger), CIBC FirstCaribbean (Domestic Lead Arranger) |

| Use-of-proceeds | Ocean economy, water management |

| Geography | Barbados |

| Impact metrics | Expand Barbados’ marine protected areas to 30%, “including coral reefs, mangroves, fish spawning sites and other important ocean habitats and species as determined from the completion of a holistic, participatory marine spatial planning process that uses the best available science for decision making” Improve marine water management in Barbados |

| Notes | The debt conversion will free up $50 million “to support environmental and sustainable development actions in Barbados over the next 15 years, making both the country and the livelihoods of its people more resilient in the face of climate change” |

| Sources | (Government of Barbados 2022a, 2022b; TNC 2022) |

| OCTOBER 2022: IDB INVEST BLUE BOND (II) | |

| Issuer | Inter-American Investment Corporation (IDB Invest) |

| Amount ($) | 25M USD |

| Currency | AUD (38 million) |

| Redemption | 15 years |

| Coupon | 4.55% |

| Investors | Taiju Life Insurance Company (sole investor) |

| Concessionary financing | Unspecified |

| Other actors | Citibank (lead manager) |

| Use-of-proceeds | “Finance private sector projects that contribute to the UN Sustainable Development Goal 6, Clean Water and Sanitation, and will promote the sustainable use of water resources for economic growth, improved livelihoods, and jobs, as well as ocean conservancy” |

| Geography | Latin America and the Caribbean |

| Impact metrics | Unspecified |

| Notes | The bond is IDB’s second blue bond issued in line with its “Sustainable Debt Framework”. |

| Sources | (IDB 2020, 2022d) |

| OCTOBER 2022: HAINAN BLUE BOND | |

| Issuer | People’s Government of Hainan Province |

| Amount ($) | 167M USD |

| Currency | CNH (1.2 billion) |

| Redemption | 2 years |

| Coupon | 2.42% |

| Investors | “International investors, including major international banks, asset management companies and funds” |

| Concessionary financing | Unspecified |

| Other actors | Credit Agricole CIB (Joint Lead Manager, Joint Bookrunner), Linklaters, Allen & Overy (legal advisors) |

| Use-of-proceeds | “Maritime economy and marine protection projects” “Water sanitation, sustainable shipping and port logistics, fisheries and seafood value chain, and marine ecosystem restoration” |

| Geography | Hainan, China |

| Impact metrics | Unspecified |

| Notes | Blue bond was issued in alignment with ICMA and IFC’s principles as well as the UN Global Compact |

| Sources | (Credit Agricole 2022; HKSAR Government 2022; Linklaters 2022) |

| NOVEMBER 2022: MARUHA NICHIRO CORPORATION’S BLUE BOND | |

| Issuer | Maruha Nichiro Corporation |

| Amount ($) | 36M USD |

| Currency | JPY (5 billion) |

| Redemption | 5 years |

| Coupon | 0.55% |

| Investors | Range of mostly Japanese asset managers, and institutional investors |

| Concessionary financing | Unspecified |

| Other actors | Mizuho Securities (lead managing company, financial agent), Mitsubishi UFJ (lead managing company), Morgan Stanley Securities (structuring agent) |

| Use-of-proceeds | “Environmentally sustainable fisheries and aquaculture operations” Example: “Land-based salmon aquaculture project” Project category:

|

| Geography | Unspecified |

| Impact metrics | Maruha Nichiro mentions SDGs 2, 3, 5, 7, 8, 9, 12, 13, 14 and 15 in its Blue Finance Framework. As an overall company, it has set KPIs to create “Environmental Value”. Two relevant areas are: “Action for Marine Pollution by marine plastics: practice zero discharge of plastics into the ocean by the company & supply chain.” KPIs are:

|

| Sources | (Maruha Nichiro Corporation 2022a, 2022b, 2022c) |

| NOVEMBER 2022: IDB INVEST BLUE BOND (III) | |

| Issuer | Inter-American Investment Corporation (IDB Invest) |

| Amount ($) | 34M USD |

| Currency | AUD (50 million) |

| Redemption | 20 years |

| Coupon | 4.90% |

| Investors | T&D Financial Life Insurance (sole investor) |

| Concessionary financing | Unspecified |

| Other actors | Nomura (lead manager) |

| Use-of-proceeds | “Finance private sector projects that contribute to the UN Sustainable Development Goal 6, Clean Water and Sanitation, and will promote the sustainable use of water resources for economic growth, improved livelihoods, and jobs, as well as ocean conservancy” |

| Geography | Latin American and the Caribbean |

| Impact metrics | Unspecified |

| Notes | The bond is IDB’s third blue bond issued in line with its “Sustainable Debt Framework”. |

| Sources | (IDB 2020, 2022c) |

| NOVEMBER 2022: BANCO INTERNACIONAL BLUE BOND | |

| Issuer | Banco Internacional |

| Amount ($) | 79M USD |

| Currency | U.S. dollar |

| Redemption | 4 years |

| Coupon | TBD |

| Investors | Other international investors, mobilized by the IFC |

| Concessionary financing | IFC (40 million) |

| Other actors | Picaval Casa de Valores (stock brocker), Bondholder Represenatative, Lexvalor (legal advisor) |

| Use-of-proceeds | “Provide long-term loans and support projects that contribute to a sustainable blue economy and the preservation of clean water resources, including sustainable aquaculture, fishing, and seafood value chain management” “The proceeds of the blue bond will be on-lent exclusively to sub-clients eligible under the IFC’s Blue Finance Guidelines. Eligible projects broadly include activities such as sustainable fishing and aquatic farming, water supply and treatment, chemicals and plastics treatment, water and waste management in vessels and shipping yards, licensed sustainable tourism operators, and the manufacturing of ocean-friendly products and offshore renewable energy” |

| Geography | Ecuador |

| Impact metrics | Unspecified |

| Notes | The bond adheres to “ICMA’s Green Bond Principles and IFC’s Blue Finance Guidelines”. IFC will support Banco Internacional in developing its blue finance framework. |

| Sources | (Banco Internacional 2022; IFC 2022a, 2022d) |

| NOVEMBER 2022: BRK AMBIENTAL | |

| Issuer | BRK Ambiental |

| Amount ($) | 380M USD |

| Currency | Brazilian Real (1.95 billion) |

| Redemption | 20 years |

| Coupon | Ceiling rate: the maximum of (i) the “Titulo Publico Tesouro IPCA+” + 1.95% and (ii) 7.65% annually Floor rate: the maximum of (i) the “Titulo Publico Tesouro IPCA+” + 1.75% and (ii) 7.45% annually |

| Investors | Unspecified |

| Concessionary financing | Unspecified |

| Other actors | Banco BTG Pactual SA (lead coordinator), Banco Itau BBA, Banco Bradesco BBI, Banco Safra, Santander, UBS BB, XP Investimentos (coordinators) |

| Use-of-proceeds | “Sustainable Water and Wastewater Management

Affordable Basic Infrastructure

|

| Geography | Brazil, Metropolitana de Maceio |

| Impact metrics | “Volume of wastewater treated; benefited population; population served, average percentage of the population of the municipalities served; number of families served, efficiency of sewage treatment, percentage of water loss, percentage of municipalities with infant mortality rates above the national average, average hospitalization rate due diarrhea in the municipalities (per 1000 inhabitants), average percentage of population with income up to ½ minimum wage; average monthly salary of formal workers (per minimum wage), added treatment volume (sewage: m3/h, water: L/s), increase in average percentage of population served.” “The use of proceeds are expected to provide 90% of the population in the region of Maceió in the state of Alagoas in Brazil with sanitation services until 2037 and reduce water waste to up to 25% over 20 years, impacting 1.5 million people.” |

| Notes | |

| Sources | (BRK Ambiental 2022a, 2022b; Environmental Finance 2022; Sustainalytics 2022b) |

| DECEMBER 2022: CENTRAL AMERICAN BANK FOR ECONOMIC INTEGRATION (CABEI) | |

| Issuer | CABEI |

| Amount ($) | 93M USD |

| Currency | Tranche AUD: 30 million AUD (21M USD) Tranche JPY: 10 billion JPY (72M USD) |

| Redemption | 5 years |

| Coupon | AUD: 4.40% JPY: 0.562% |

| Investors | Unspecified |

| Concessionary financing | Unspecified |

| Other actors | Daiwa Capital Markets America (arranger) |

| Use-of-proceeds | “Water resources protection”

“Sustainable water management”

“Renewable energy”

“Blue economy”

“Nature protection”

|

| Geography | Central America |

| Impact metrics | Examples of impact indicators include: “Water resources protection

Sustainable water management

Renewable energy

Blue economy

Nature protection

|

| Notes | |

| Sources | (CABEI 2022a, 2022b; Sustainalytics 2022a) |

References

- Althalet, Fareis, Tira Siya Fajar Rahayu, Hera Hera, Ayu Fil Akhirati, Pingki Pingki, Nirwana Nura, and Angelika Gita Andreana. 2021. Incorporating Blue Bonds as a funding alternative for a sustainable development project. International Journal of Research in Business and Social Science (2147–4478) 10: 129–34. [Google Scholar] [CrossRef]

- Asian Development Bank. 2021a. ADB Issues First Blue Bond for Ocean Investments. Available online: https://www.adb.org/news/adb-issues-first-blue-bond-ocean-investments (accessed on 28 November 2022).

- Asian Development Bank. 2021b. Green and Blue Bond Framework. Available online: https://www.adb.org/sites/default/files/publication/731026/adb-green-blue-bond-framework.pdf (accessed on 28 November 2022).

- Asian Development Bank. 2022a. Investor Presentation—Investing in a Prosperous, Inclusive, Resilient, and Sustainable Asia and the Pacific. Available online: https://www.adb.org/sites/default/files/institutional-document/191221/investor-presentation-202210.pdf (accessed on 28 November 2022).

- Asian Development Bank. 2022b. Ocean Finance Framework. Available online: https://www.adb.org/sites/default/files/publication/777461/adb-ocean-finance-framework.pdf (accessed on 28 November 2022).

- Banca Transilvania. 2022. The First Blue Funding Supported by IFC Supports the Sustainable Use of Water in Romania. €100 million for Banca Transilvania. Available online: https://en.bancatransilvania.ro/bt-social-media-newsroom/stiri/prima-finantare-blue-sustinuta-de-ifc-sprijina-folosirea-sustenabila-a-apei-in-romania-100-de-milioane-de-euro-pentru-banca-transilvania/ (accessed on 30 November 2022).

- Banco Internacional. 2022. Resolution No. SCVS-IRQ-DRMV-2022-00007936. Available online: https://www-bancointernacional-com-ec.translate.goog/storage/2020/11/Resolucio%CC%81n-de-autorizacio%CC%81n-expedida-por-la-SUPERCIAS-Bono-Azul.pdf?_x_tr_sl=es&_x_tr_tl=en&_x_tr_hl=nl&_x_tr_pto=wapp (accessed on 30 November 2022).

- Banga, Josué. 2019. The green bond market: A potential source of climate finance for developing countries. Journal of Sustainable Finance & Investment 9: 17–32. [Google Scholar]

- BBVA. 2023. BBVA Assisted Desarrollos Hidráulicos de Cancún in the Issuance of the First Blue Bond in Mexico and the First of Its Kind for the Bank. Available online: https://www.bbvacib.com/insights/news/bbva-assisted-desarrollos-hidraulicos-de-cancun-in-the-issuance-of-the-first-blue-bond-in-mexico-and-the-first-of-its-kind-for-the-bank/ (accessed on 2 February 2023).

- BDO. 2022a. BDO issues first Blue Bond for US$100 Million. Available online: https://www.bdo.com.ph/news-and-articles/BDO-Unibank-Blue-Bond-USD-100-million-first-private-sector-issuance-southeast-asia-IFC-marine-pollution-prevention-clear-water-climate-goals-sustainability (accessed on 29 November 2022).

- BDO. 2022b. IFC’s Investment in BDO’s Blue Bond Helps Tackle Marine Pollution. Available online: https://www.bdo.com.ph/news-and-articles/BDO-Unibank-IFC-Blue-Bond-investment-100-million-USD-marine-pollution-prevention-clear-water-climate-goals-sustainability (accessed on 29 November 2022).

- Berggren, Jens, and Birgitta Liss Lymer. 2016. Source to Sea—Linkages in the 2030 Agenda for Sustainable Development. Available online: https://siwi.org/wp-content/uploads/2017/12/Berggren-and-Liss-Lymer-2016-S2S-linkages-in-the-2030-agenda.pdf (accessed on 30 January 2023).

- Bhutta, Umair Saeed, Adeel Tariq, Muhammad Farrukh, Ali Raza, and Muhammad Khalid Iqbal. 2022. Green bonds for sustainable development: Review of literature on development and impact of green bonds. Technological Forecasting and Social Change 175: 121378. [Google Scholar] [CrossRef]

- Bloomberg New Energy Finance. 2021. Sustainable Debt Issuance Breezed Past $1.6 Trillion in 2021. Available online: https://about.bnef.com/blog/sustainable-debt-issuance-breezed-past-1-6-trillion-in-2021/ (accessed on 27 November 2022).

- BOC. 2020a. Bank of China Limited Sustainability Series Bonds Management Statement. Available online: https://pic.bankofchina.com/bocappd/report/201805/P020180530287666583473.pdf (accessed on 28 November 2022).

- BOC. 2020b. BOC’s 2020 Blue Bonds External Review Form. Available online: https://pic.bankofchina.com/bocappd/report/202009/P020200913763660583185.pdf (accessed on 28 November 2022).

- BOC. 2020c. BOC’s 2020 Blue Bonds Information Template. Available online: https://pic.bankofchina.com/bocappd/report/202009/P020200913763659336260.pdf (accessed on 28 November 2022).

- Borio, Claudio, Stijn Claessens, and Nikola Tarashev. 2022. Finance and Climate Change Risk: Managing Expectations. Available online: https://cepr.org/voxeu/columns/finance-and-climate-change-risk-managing-expectations (accessed on 27 February 2023).

- BRK Ambiental. 2022a. BRK anuncia a primeira emissão de debênture azul do setor privado no Brasi. Available online: https://www.brkambiental.com.br/brk-anuncia-a-primeira-emissao-de-debenture-azul-do-setor-privado-no-brasil (accessed on 7 February 2023).

- BRK Ambiental. 2022b. Prospecto preliminar da oferta pública de distribuição de debêntures simples, não Conversíveis em ações, em série única, da espécie quirografária, a ser convolada em Espécie com garantia real, com garantia fidejussória adicional, da 2ª emissão da. Available online: https://api.mziq.com/mzfilemanager/v2/d/9ffe3afc-e8e3-4e62-9f49-04166095f065/1b930f11-592b-6732-d0c9-ec74dc60acdd?origin=2 (accessed on 7 February 2023).

- CABEI. 2022a. Green and Blue Bond Framework. Available online: https://www.bcie.org/fileadmin/bcie/espanol/archivos/novedades/publicaciones/institucionales/NINT_-_CABEIs_Green_and_Blue_Bond_Framework_20221201_FINAL.pdf (accessed on 2 February 2023).

- CABEI. 2022b. Only a Week after Releasing Its Green and Blue Bond Framework CABEI Issues Its First ever Blue Bond. Available online: https://www.bcie.org/en/news-and-media/news/article/a-solo-una-semana-del-lanzamiento-de-su-marco-de-bonos-verdes-y-azules-el-bcie-emite-su-primer-bono-azul (accessed on 2 February 2023).

- CABEI. 2023. CABEI Issues Its Second Blue Bond less than a Month after Publishing Its Blue Taxonomy. Available online: https://www.bcie.org/en/news-and-media/news/article/el-bcie-emite-su-segundo-bono-azul-a-menos-de-un-mes-de-publicar-su-taxonomia-azul (accessed on 2 February 2023).

- Caramichael, John, and Andreas Rapp. 2022. The Green Corporate Bond Issuance Premium. International Finance Discussion Papers, 1346. [Google Scholar] [CrossRef]

- CICERO. 2020. Grieg Seafood ASA Green Bond Second Opinion. Available online: https://cdn.sanity.io/files/1gakia31/production/cb88bc229eaf9bed5d3afa3a7ee714bf22a2e953.pdf (accessed on 7 February 2023).

- Claes, Julien, Duko Hopman, Gualtiero Jaeger, and Matt Rogers. 2022. Blue Carbon: The Potential of Coastal and Oceanic Climate Action. Available online: https://www.mckinsey.com/capabilities/sustainability/our-insights/blue-carbon-the-potential-of-coastal-and-oceanic-climate-action (accessed on 3 December 2022).

- Climate Bonds Initiative. 2021. Water Infrastructure Criteria under the Climate Bonds Standard. Available online: https://www.climatebonds.net/files/files/Water%20Criteria%20Document%20Final_17Jan21.pdf (accessed on 30 January 2023).

- Climate Bonds Initiative. 2022a. Climate Bonds Interactive Data Platform. Available online: https://www.climatebonds.net/market/data/ (accessed on 2 December 2022).

- Climate Bonds Initiative. 2022b. Water Infrastructure Criteria under the Climate Bonds Standard. Criteria Document Version 3.2. Available online: https://www.climatebonds.net/files/files/Water%20Criteria%20Document%20Final_100822.pdf (accessed on 8 February 2023).

- Credit Agricole. 2022. China Launches the First Local Government Blue and Sustainability Dim Sum Bonds. Available online: https://www.ca-cib.com/pressroom/news/china-launches-first-local-government-blue-and-sustainability-dim-sum-bonds (accessed on 29 November 2022).

- Credit Suisse, and Responsible Investor Research. 2020. Investors and the Blue Economy. Available online: https://d16yj43vx3i1f6.cloudfront.net/uploads/research/BlueEconomy_report_Final.pdf (accessed on 3 December 2022).

- Credit Suisse. 2021. Credit Suisse Finances The Nature Conservancy’s Blue Bond for Marine Conservation for Belize. Available online: https://www.credit-suisse.com/about-us-news/en/articles/media-releases/credit-suisse-finances-the-nature-conservancys-blue-bond-for-marine-conservation-for-belize-202111.html (accessed on 28 November 2022).

- Davis, Morgan. 2020. BOC makes waves with first blue bond. GlobalCapitalAsia. Available online: https://www.globalcapital.com/asia/article/28mubssrshvmtp29bqlts/asia-fig-senior-debt/boc-makes-waves-with-first-blue-bond (accessed on 28 November 2022).

- de Mariz, Frederic. 2022. The Promise of Sustainable Finance: Lessons From Brazil. Georgetown Journal of International Affairs 23: 185–90. [Google Scholar] [CrossRef]

- Dealogic, and ICMA. 2022. Value of Deals on International Debt Capital Markets in the 2nd Quarter of 2022, by Currency. Available online: https://www.statista.com/statistics/247300/transaction-volume-on-the-global-bond-market-by-currency/ (accessed on 2 December 2022).

- Dembele, Faty, Timothy Randall, David Vilalta, and Vanessa Bangun. 2022. Blended Finance Funds and Facilities. Available online: https://doi.org/10.1787/fb282f7e-en (accessed on 3 December 2022).

- Deschryver, Pauline, and Frederic de Mariz. 2020. What future for the green bond market? How can policymakers, companies, and investors unlock the potential of the green bond market? Journal of risk and Financial Management 13: 61. [Google Scholar] [CrossRef] [Green Version]

- Díaz, Sandra, Josef Settele, Eduardo Brondízio, Hien Ngo, Maximilien Guèze, John Agard, Almut Arneth, Patricia Balvanera, Kate Brauman, and Stuart Butchart. 2019. Summary for Policymakers of the Global Assessment report on Biodiversity and Ecosystem Services of the Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services. Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services. Available online: https://doi.org/10.5281/zenodo.3553579 (accessed on 28 November 2022).

- Ehlers, Torsten, and Frank Packer. 2017. Green bond finance and certification. BIS Quarterly Review. Available online: https://www.bis.org/publ/qtrpdf/r_qt1709h.pdf (accessed on 2 December 2022).

- Environmental Finance. 2022. Impact initiative of the year—Latin America and Caribbean: BRK’s Blue Bond. Available online: https://www.environmental-finance.com/content/awards/impact-awards-2022/winners/impact-initiative-of-the-year-latin-america-and-caribbean-brks-blue-bond.html (accessed on 7 February 2023).

- Ernst & Young. 2020. Attestation Report on Pre-issuance of BOC’s 2020 Blue Bonds -Appendix. Available online: https://pic.bankofchina.com/bocappd/report/202009/P020200913763657935921.pdf (accessed on 28 November 2022).

- Ernst & Young. 2022. Assurance Report on Use of Proceeds from Blue Bonds Issuance of Bank of China Limited. Available online: https://pic.bankofchina.com/bocappd/report/202203/P020220324757232257630.pdf (accessed on 28 November 2022).

- European Investment Bank. n.d. Climate Awareness Bonds. Available online: https://www.eib.org/en/investor-relations/cab/index.htm (accessed on 27 November 2022).

- Flammer, Caroline. 2021. Corporate Green Bonds. Journal of Financial Economics 142: 499–16. [Google Scholar] [CrossRef]

- Fredston-Hermann, Alexa, Christopher Brown, Simon Albert, Carissa Klein, Sangeeta Mangubhai, Joanna Nelson, Lida Teneva, Amelia Wenger, Steven Gaines, and Benjamin Halpern. 2016. Where Does River Runoff Matter for Coastal Marine Conservation? [Hypothesis and Theory]. Frontiers in Marine Science 3: 273. [Google Scholar] [CrossRef] [Green Version]

- Galaz, Victor, Johan Gars, Fredrik Moberg, Bjorn Nykvist, and Cecilia Repinski. 2015. Why ecologists should care about financial markets. Trends in Ecology & Evolution 30: 571–80. [Google Scholar]

- Gambetta, Gina. 2021. Japanese Insurers Buy ADB’s First Blue Bonds. Responsible Investor. Available online: https://www.responsible-investor.com/japanese-insurers-buy-adb-s-first-blue-bonds/ (accessed on 3 December 2022).

- Gattuso, Jean-Pierre, Alexandre Magnan, Laurent Bopp, William Cheung, Carlos Duarte, Jochen Hinkel, Elizabeth Mcleod, Fiorenza Micheli, Andreas Oschlies, and Phillip Williamson. 2018. Ocean solutions to address climate change and its effects on marine ecosystems. Frontiers in Marine Science 5: 337. [Google Scholar] [CrossRef] [Green Version]

- Gonzalez-Ruiz, Juan David, Alejandro Arboleda, Sergio Botero, and Javier Rojo. 2019. Investment valuation model for sustainable infrastructure systems: Mezzanine debt for water projects. Engineering, Construction and Architectural Management 26: 850–84. [Google Scholar] [CrossRef]

- Gottschalk, Ricardo, and Daniel Poon. 2020. Scaling up Finance for the Sustainable Development Goals. In Southern-Led Development Finance: Solutions from the Global South, 1st ed. Edited by Diana Barrowclough, Kevin Gallagher and Richard Kozul-Wright. London: Routledge. [Google Scholar]

- Government of Barbados. 2022a. Barbados Announces Successful Closing of Landmark Debt Conversion That Will Support Marine Conservation for Generations. Available online: https://www.prnewswire.com/news-releases/barbados-announces-successful-closing-of-landmark-debt-conversion-that-will-support-marine-conservation-for-generations-301629490.html (accessed on 29 November 2022).

- Government of Barbados. 2022b. The Government of Barbados Announces the Final Results of Its Offer to Purchase for Cash Its Notes Listed Below. Available online: https://www.prnewswire.com/news-releases/the-government-of-barbados-announces-the-final-results-of-its-offer-to-purchase-for-cash-its-notes-listed-below-301626665.html (accessed on 29 November 2022).

- Government of The Bahamas. 2022. The Commonwealth of The Bahamas Successfully Prices US$385 Million Notes. Available online: https://www.bahamas.gov.bs/wps/portal/public/gov/government/news/the%20commonwealth%20of%20the%20bahamas%20successfully%20prices%20us385%20million%20notes (accessed on 29 November 2022).

- Government of the Republic of Fiji. 2022. Fijian Sustainable Bond Framework 2022. Available online: https://fijiclimatechangeportal.gov.fj/wp-content/uploads/2022/11/Fijian-Sustainable-Bond-Framework.pdf (accessed on 1 December 2022).

- Grieg Seafood. 2020a. Base Prospectus Final Terms for ISIN NO0010885007. Available online: https://cdn.sanity.io/files/1gakia31/production/86a7f4280b289b9b32b3be161bd2e9b82893a9df.pdf (accessed on 7 February 2023).

- Grieg Seafood. 2020b. Base Prospectus Final Terms for ISIN NO0010908858 (Temporary Bonds to be Converted into ISIN: NO0010885007). Available online: https://cdn.sanity.io/files/1gakia31/production/5621992770a6a320d3addaa83b7830993ef90434.pdf (accessed on 7 February 2023).

- Grieg Seafood. 2020c. Bond Investor Presentation November 2020. Available online: https://cdn.sanity.io/files/1gakia31/production/c8fca2986b9b89ff64655f039b3a6356de693fb0.pdf (accessed on 7 February 2023).

- Grieg Seafood. 2020d. Green Bond Framework. Available online: https://cdn.sanity.io/files/1gakia31/production/92d0d3e7903ee90e2a409a1f02f963be1a389787.pdf (accessed on 7 February 2023).

- Grieg Seafood. 2021. Green Bond Report 2020. Available online: https://cdn.sanity.io/files/1gakia31/production/f2c7a53d07dd3303d9cb11a06753aae707705e0a.pdf (accessed on 7 February 2023).

- Grieg Seafood. 2022. Green Bond Report 2021. Available online: https://cdn.sanity.io/files/1gakia31/production/a7547e0e396deef64fae497700e8763fcd78f153.pdf (accessed on 7 February 2023).

- HKSAR Government. 2022. HKSAR Government Welcomes Issuance of Bonds in Hong Kong by Hainan Provincial Government and Shenzhen Municipal Government. Available online: https://www.info.gov.hk/gia/general/202210/24/P2022102400500.htm (accessed on 29 November 2022).

- Hoegh-Guldberg, Ove, Catherine Lovelock, Ken Caldeira, Jennifer Howard, Thierry Chopin, and Steve Gaines. 2019. The Ocean as a Solution to Climate Change: Five Opportunities for Action. Available online: https://oceanpanel.org/wp-content/uploads/2022/06/HLP_Report_Ocean_Solution_Climate_Change_final.pdf (accessed on 28 February 2023).

- ICMA. 2020. Sustainability-Linked Bond Principles. Available online: https://www.icmagroup.org/assets/documents/Regulatory/Green-Bonds/June-2020/Sustainability-Linked-Bond-Principles-June-2020-171120.pdf (accessed on 27 November 2022).

- ICMA. 2021. The Principles, Guidelines and Handbooks. Available online: https://www.icmagroup.org/sustainable-finance/the-principles-guidelines-and-handbooks/ (accessed on 27 November 2022).

- IDB. 2020. Sustainable Debt Framework. Available online: https://www.idbinvest.org/en/download/12265 (accessed on 30 November 2022).

- IDB. 2021a. Accelerating Blue Bonds Issuances in Latin America and the Caribbean. Available online: https://idbinvest.org/en/download/13319 (accessed on 30 November 2022).

- IDB. 2021b. IDB Invest Issues First Blue Bond in Latin America and the Caribbean. Available online: https://www.idbinvest.org/en/news-media/idb-invest-issues-first-blue-bond-latin-america-and-caribbean (accessed on 30 November 2022).

- IDB. 2022a. The Bahamas Advances Creation of Social and Inclusive Blue Economy using IDB Guarantee. Available online: https://www.iadb.org/en/news/bahamas-advances-creation-social-and-inclusive-blue-economy-using-idb-guarantee (accessed on 30 November 2022).

- IDB. 2022b. Banco Bolivariano Blue Bond. Available online: https://idbinvest.org/en/projects/banco-bolivariano-blue-bond (accessed on 30 November 2022).

- IDB. 2022c. IDB Invest Issues Blue Bond to Finance Water Projects in Latin America and the Caribbean (November 2022). Available online: https://idbinvest.org/en/news-media/idb-invest-issues-blue-bond-finance-water-projects-latin-america-and-caribbean-0 (accessed on 30 November 2022).

- IDB. 2022d. IDB Invest Issues Blue Bond to Finance Water Projects in Latin America and the Caribbean (October 2022). Available online: https://www.idbinvest.org/en/news-media/idb-invest-issues-blue-bond-finance-water-projects-latin-america-and-caribbean (accessed on 30 November 2022).

- IFC. 2022a. Banco Internacional Blue Bond. Available online: https://disclosures.ifc.org/project-detail/SII/46190/banco-internacional-blue-bond (accessed on 29 November 2022).

- IFC. 2022b. DCM BDO Blue Bond. Available online: https://disclosures.ifc.org/project-detail/SII/46151/dcm-bdo-blue-bond (accessed on 29 November 2022).

- IFC. 2022c. Guidelines for Blue Finance. Available online: https://www.ifc.org/wps/wcm/connect/4a61d420-82b2-41e9-b2fd-b7fb0af38bba/IFC-Guidelines-for-Blue-Finance.pdf?MOD=AJPERES&CVID=ogvh-4f (accessed on 29 November 2022).

- IFC. 2022d. IFC Announces $40 million Agreement with Banco Internacional to Support First Private Sector Blue Bond in Ecuador and Latin America. Available online: https://pressroom.ifc.org/all/pages/PressDetail.aspx?ID=27216 (accessed on 29 November 2022).

- IFC. 2022e. IFC to Support Thailand’s Blue Economy through First Blue Bond Issued by TMBThanachart Bank. Available online: https://pressroom.ifc.org/all/pages/PressDetail.aspx?ID=26967 (accessed on 29 November 2022).

- IFC. 2022f. IFC, ICMA, UNGC, UNEP FI, and ADB Announce Coalition to Support the Blue Economy. Available online: https://pressroom.ifc.org/all/pages/PressDetail.aspx?ID=27050 (accessed on 29 November 2022).

- Johansen, Despina, and Rolf Vestvik. 2020. The cost of saving our ocean—Estimating the funding gap of sustainable development goal 14. Marine Policy 112: 103783. [Google Scholar] [CrossRef]

- Jouffray, Jean-Baptiste, Beatrice Crona, Emmy Wassénius, Jan Bebbington, and Bert Scholtens. 2019. Leverage points in the financial sector for seafood sustainability. Science Advances 5: eaax3324. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Jouffray, Jean-Baptiste, Robert Blasiak, Magnus Nyström, Henrik Österblom, Kanae Tokunaga, Colette Wabnitz, and Albert Norström. 2021. Blue Acceleration: An ocean of risks and opportunities. Ocean Risk and Resilience Action Alliance (ORRAA) Report 42: 1–42. [Google Scholar]

- Konar, Manaswita, and Helen Ding. 2022. A Sustainable Ocean Economy for 2050. Available online: https://oceanpanel.org/wp-content/uploads/2022/05/Ocean-Panel_Economic-Analysis_FINAL.pdf (accessed on 3 December 2022).

- Lagoarde-Segot, Thomas. 2020. Financing the sustainable development goals. Sustainability 12: 2775. [Google Scholar] [CrossRef] [Green Version]

- LAO. 2000. Parks and Water Bonds: Implementation Issues. Available online: https://lao.ca.gov/2000/052500_parkwater_bonds/052500_parkwater_bonds.html (accessed on 2 March 2023).

- Le Blanc, David, Clovis Freire, and Marjo Vierros. 2017. Mapping the Linkages between Oceans and Other Sustainable Development Goals: A Preliminary Exploration. UN Department of Economic and Social Affairs (DESA) Working Papers 149: 1–34. [Google Scholar] [CrossRef]

- Li, Wai Chin, Hung Fat Tse, and Lincoln Fok. 2016. Plastic waste in the marine environment: A review of sources, occurrence and effects. Science of The Total Environment 566–567: 333–49. [Google Scholar] [CrossRef]

- Linklaters. 2022. Linklaters Advises People’s Government of Hainan Province of the People’s Republic of China on Its First Offshore Bond Issuance. Available online: https://www.linklaters.com/en/about-us/news-and-deals/deals/2022/october/we-advise-peoples-government-of-hainan-province-of-the-prc-on-its-first-offshore-bond-issuance (accessed on 29 November 2022).

- Maltais, Aaron, and Bjorn Nykvist. 2020. Understanding the role of green bonds in advancing sustainability. Journal of Sustainable Finance & Investment 11: 233–52. [Google Scholar]

- March, Antaya, Pierre Failler, and Michael Bennett. 2023. Challenges when designing blue bond financing for Small Island Developing States. ICES Journal of Marine Science fsac238. [Google Scholar] [CrossRef]

- Maruha Nichiro Corporation. 2022a. Blue Finance Framework. Available online: https://www.maruha-nichiro.com/media/files/en_blue_finance_framework.pdf (accessed on 29 November 2022).

- Maruha Nichiro Corporation. 2022b. Notice Regarding Determination of Terms and Conditions for Issuance of Blue Bonds. Available online: https://www.maruha-nichiro.com/media/files/20221027_en_blue_bond.pdf (accessed on 29 November 2022).

- Maruha Nichiro Corporation. 2022c. Notice Regarding Issuance of Japan’s First “Blue Bond”. Available online: https://www.maruha-nichiro.com/media/files/20220929_03_bluebond_issuance.en.pdf (accessed on 29 November 2022).

- Mathew, Joywin, and Claire Robertson. 2021. Shades of blue in financing: Transforming the ocean economy with blue bonds. Journal of Investment Compliance 22: 243–47. [Google Scholar] [CrossRef]

- Mathew, Joywin, and Claire Robertson. 2022. The Blue Bond Guidance to Finance the Sustainable Blue Economy. Available online: https://www.dlapiper.com/en-us/insights/publications/2022/09/the-blue-bond-guidance-to-finance-the-sustainable-blue-economy (accessed on 29 November 2022).

- Mocanu, Mihaela, Laura-Gabriela Constantin, and Bogdan Cernat-Gruici. 2021. Sustainability bonds. an international event study. Journal of Business Economics and Management 22: 1551–76. [Google Scholar] [CrossRef]

- Morgan Stanley. 2019. Blue Bonds: The Next Wave of Sustainable Bonds. Available online: https://www.morganstanley.com/content/dam/msdotcom/ideas/blue-bonds/2583076-FINAL-MS_GSF_Blue_Bonds.pdf (accessed on 27 November 2022).

- Mowi. 2020a. Base Prospectus NO0010874050. Available online: https://mowi.com/wp-content/uploads/2020/06/Bond-Prospectus-Mowi-ASA-NO0010874050.pdf (accessed on 29 November 2022).

- Mowi. 2020b. First Ever Green Bond Issue from a Seafood Company. Available online: https://mowi.com/blog/first-ever-green-bond-issue-from-a-seafood-company/ (accessed on 29 November 2022).

- Mowi. 2020c. Mowi ASA Green Bond Framework. Available online: https://corpsite.azureedge.net/corpsite/wp-content/uploads/2020/01/GBF_Mowi_Jan2020.pdf (accessed on 29 November 2022).

- Mowi. 2022. Green Bond Impact Report 2021. Available online: https://corpsite.azureedge.net/corpsite/wp-content/uploads/2022/03/Mowi-Green-Bond-Impact-Report-2021.pdf (accessed on 29 November 2022).

- Nash, Kirsty, Jessica Blythe, Christopher Cvitanovic, Elizabeth Fulton, Benjamin Halpern, EJ Milner-Gulland, Prue Addison, Gretta Pecl, Reg Watson, and Julia Blanchard. 2020. To achieve a sustainable blue future, progress assessments must include interdependencies between the sustainable development goals. One Earth 2: 161–73. [Google Scholar] [CrossRef] [Green Version]

- National Oceanography Centre. 2018. Rising Sea Levels Could Cost the World $14 Trillion a Year by 2100. Available online: https://noc.ac.uk/news/rising-sea-levels-could-cost-world-14-trillion-year-2100 (accessed on 3 December 2022).

- NIB, and SEB. 2019. Nordic Investment Bank (NIB) Launches an Inaugural 5-Year SEK 2 Billion Nordic–Baltic Blue Bond. Available online: https://www.nib.int/files/7bb314a4d17f64324262d6fb884d2f90398009ea/9207-2019-nib-seb-joint-press-release.pdf (accessed on 2 December 2022).

- NIB, Danske Bank, and Swedbank. 2020. NIB SEK 1.5 billion 5-Year Nordic-Baltic Blue Bond. Available online: https://www.nib.int/files/03c2a48e4c0d142117199687ccf1fee4cca6d8f5/10464-2020-joint-press-release-nib-nordic-baltic-blue-bond-6-october-2020.pdf (accessed on 2 December 2022).

- NIB. 2019a. Clean Seas in the Nordic–Baltic Region. Available online: https://www.nib.int/cases/clean-seas-in-the-nordic-baltic-region (accessed on 2 December 2022).

- NIB. 2019b. NIB Environmental Bond Framework. Available online: https://www.nib.int/files/f5bde5526b8d812aead65dd8e3e182d55d347842/10460-neb-framework-oct-2019.pdf (accessed on 2 December 2022).

- NIB. 2019c. NIB Issues First Nordic–Baltic Blue Bond. Available online: https://www.nib.int/releases/nib-issues-first-nordic-baltic-blue-bond (accessed on 2 December 2022).

- NIB. 2020. NIB Launches Five-Year SEK 1.5 Billion Nordic–Baltic Blue Bond. Available online: https://www.nib.int/releases/nib-launches-five-year-sek-1-5-billion-nordic-baltic-blue-bond (accessed on 2 December 2022).

- NIB. 2021. Projects Financed by NIB Environmental Bonds. Available online: https://www.nib.int/investors/environmental-bonds/neb-financed-projects?category=Blue%20Bond%20project (accessed on 2 December 2022).

- NIB. n.d.a About: Member Countries, Governing Bodies and Capital. Available online: https://www.nib.int/who-we-are/about/member-countries-governing-bodies-and-capital (accessed on 2 December 2022).

- NIB. n.d.b NIB Environmental Bonds. Available online: https://www.nib.int/investors/environmental-bonds (accessed on 2 December 2022).

- Nikkei. 2022. New “Label” for ESG Bonds—Maruha Nichiro’s Blue Bond Attracts High Levels of Investor Attention. Nikkei Japan. Available online: https://www.nikkei.co.jp/nikkeiinfo/en/global_services/quick/new-label-for-esg-bonds---maruha-nichiros-blue-bond-attracts-high-levels-of-investor-attention.html (accessed on 4 December 2022).

- NWB Bank. 2021. Water Bond Report: Using Financial Instruments for the Benefit of People and Planet. Available online: https://nwbbank.com/application/files/7916/5545/2094/NWB_Bank_Newsletter_Waterbonds_2021.pdf (accessed on 30 November 2022).

- OECD. 2016. The Ocean Economy in 2030. Paris: OECD Publishing. [Google Scholar] [CrossRef]

- OECD. 2019. The SDG Financing Lab. Available online: https://sdg-financing-lab.oecd.org/explore (accessed on 3 December 2022).

- OECD. 2022. Financing a Water Secure Future. Paris: OECD Publishing. [Google Scholar] [CrossRef]

- Park, Stephen. 2018. Social Bonds for Sustainable Development: A Human Rights Perspective on Impact Investing. Business and Human Rights Journal 3: 233–55. [Google Scholar] [CrossRef] [Green Version]

- Plastic Bank. 2022. Plastic Bank’s Partnership with Lombard Odier. Available online: https://plasticbank.com/client/Lombard-odier/ (accessed on 28 November 2022).

- Redondo Alamillos, Rocio, and Frederic de Mariz. 2022. How Can European Regulation on ESG Impact Business Globally? Journal of risk and Financial Management 15: 291. [Google Scholar] [CrossRef]

- Requicha Ferreira, Manuel. 2022. The New ESG Bond Markets. Berlin and Heidelberg: Springer International Publishing, pp. 149–65. [Google Scholar] [CrossRef]

- Rosane, Olivia. 2018. World Bank Launches Bond Series to Raise Awareness about Water and Ocean Resources. Available online: https://www.ecowatch.com/world-bank-water-bonds-2601968581.html (accessed on 7 February 2023).

- Rosser, Annabelle, and Caitrin Chappelle. 2021. How Water Bonds Plug Spending Holes. Available online: https://www.ppic.org/blog/how-water-bonds-plug-spending-holes/ (accessed on 30 January 2023).

- Roth, Nathalie, Torsten Thiele, and Moritz Von Unger. 2019. Blue bonds: Financing resilience of coastal ecosystems. Key Points for Enhancing Finance Action. Blue Natural Capital Financing Facility: Technical Guideline Prepared for IUCN GMPP. Available online: https://www.4climate.com/dev/wp-content/uploads/2019/04/Blue-Bonds_final.pdf (accessed on 1 March 2023).

- Schatz, Roland. 2017. SDG Commitment Report 100: Tracking Companies’ Efforts to Contribute to the Sustainable Development Goals. Available online: https://www.cbd.int/financial/2017docs/un2017-scr100.pdf (accessed on 28 February 2023).

- Seaspan. 2021a. Blue Transition Bond Framework. Available online: https://www.seaspancorp.com/wp-content/uploads/2021/06/20210623-Blue-Transition-Bond-Framework.pdf (accessed on 30 November 2022).

- Seaspan. 2021b. Seaspan Completes Significantly Upsized $750 Million Offering Of Blue Transition Bonds. Available online: https://www.seaspancorp.com/press_release/seaspan-completes-significantly-upsized-750-million-offering-of-blue-transition-bonds/ (accessed on 30 November 2022).

- SEC. n.d. Bonds. Available online: https://www.investor.gov/introduction-investing/investing-basics/investment-products/bonds-or-fixed-income-products/bonds (accessed on 27 November 2022).

- Shiiba, Nagisa, Hsing Hao Wu, Michael Huang, and Hajime Tanaka. 2022. How blue financing can sustain ocean conservation and development: A proposed conceptual framework for blue financing mechanism. Marine Policy 139: 104575. [Google Scholar] [CrossRef]

- Smith, Lisa. 2022. Why Companies Issue Bonds. Available online: https://www.investopedia.com/articles/investing/062813/why-companies-issue-bonds.asp (accessed on 27 November 2022).

- Sumaila, Ussid Rashid, Melissa Walsh, Kelly Hoareau, Anthony Cox, Louise Teh, Patricia Abdallah, Wisdom Akpalu, Zuzy Anna, Dominique Benzaken, Beatrice Crona, and et al. 2021. Financing a sustainable ocean economy. Nature Communications 12: 3259. [Google Scholar] [CrossRef] [PubMed]

- Sustainalytics. 2021. Second-Party Opinion: Seaspan Blue Transition Bond Framework. Available online: https://www.sustainalytics.com/corporate-solutions/sustainable-finance-and-lending/published-projects/project/seaspan-corporation/seaspan-blue-transition-bond-framework-second-party-opinion-(2021)/seaspan-blue-transition-bond-framework-second-party-opinion-(2021) (accessed on 27 November 2022).

- Sustainalytics. 2022a. Second-Party Opinion CABEI Green and Blue Bond Framework. Available online: https://mstar-sustops-cdn-mainwebsite-s3.s3.amazonaws.com/docs/default-source/spos/cabei_green-and-blue-bond_second-party-opinion_dec-2022.pdf (accessed on 7 February 2023).

- Sustainalytics. 2022b. Second-Party Opinion. BRK Ambiental Sustainable Financing Framework. Available online: https://api.mziq.com/mzfilemanager/v2/d/9ffe3afc-e8e3-4e62-9f49-04166095f065/5f60181c-772c-70b7-8564-9bcc0f300924?origin=1 (accessed on 7 February 2023).

- Thiele, Torsten, and Leah Gerber. 2017. Innovative financing for the high seas. Aquatic Conservation: Marine and Freshwater Ecosystems 27: 89–99. [Google Scholar] [CrossRef]

- Thompson, Benjamin. 2022. Blue bonds for marine conservation and a sustainable ocean economy: Status, trends, and insights from green bonds. Marine Policy 144: 105219. [Google Scholar] [CrossRef]

- Tirumala, Raghu, and Piyush Tiwari. 2022. Innovative financing mechanism for blue economy projects. Marine Policy 139: 104194. [Google Scholar] [CrossRef]

- TMBThanachart. 2022a. Condensed Interim Financial Statements for the Three-Month and Nine-Month Periodsended 30 September 2022 and Independent Auditor’s Review Report. Available online: https://media.ttbbank.com/5005/ir_fininfo_quar/6715-en.pdf (accessed on 29 November 2022).

- TMBThanachart. 2022b. TTB Green and Blue Bond. Available online: https://www.ttbbank.com/en/ir/credit-rating-and-debenture/green-blue-bond (accessed on 29 November 2022).

- TMBThanachart. 2022c. ttb Green and Blue Bond Framework. Available online: https://media.ttbbank.com/1/ir/green-blue-bond/ttb-green-blue-bond-framework-en.pdf (accessed on 29 November 2022).

- TNC. 2021a. Blue Bonds: An Audacious Plan to Save the World’s Ocean. Available online: https://www.nature.org/en-us/what-we-do/our-insights/perspectives/an-audacious-plan-to-save-the-worlds-oceans/ (accessed on 28 November 2022).

- TNC. 2021b. TNC Statement on Belize Conservation Commitments. Available online: https://www.nature.org/en-us/about-us/where-we-work/latin-america/belize/belize-blue-bond/ (accessed on 28 November 2022).

- TNC. 2022. The Nature Conservancy Announces Its Third Global Debt Conversion in Barbados. Available online: https://www.nature.org/en-us/newsroom/tnc-announces-barbados-blue-bonds-debt-conversion/ (accessed on 28 November 2022).

- UN Global Compact. 2019. 5 Tipping Points for a Healthy and Ocean Productive Ocean by 2030. Available online: https://unglobalcompact.org/library/5726 (accessed on 28 February 2023).

- UN Global Compact. 2020a. Blue Bonds. Reference Paper for Investments Accelerating Sustainable Ocean Business. Available online: https://ungc-communications-assets.s3.amazonaws.com/docs/publications/Blue-Bonds-Reference-Paper-for-Sustainable-Ocean-Investments.pdf (accessed on 28 November 2022).

- UN Global Compact. 2020b. Practical Guidance to Issue a Blue Bond. Available online: https://ungc-communications-assets.s3.amazonaws.com/docs/publications/Practical-Guidance-to-Issue-a-Blue-Bond.pdf (accessed on 28 November 2022).

- UNDP. 2022. Indonesia Unveils a Plan to Launch Blue Bond at UN Ocean Conference 2022. Available online: https://www.undp.org/indonesia/press-releases/indonesia-unveils-plan-launch-blue-bond-un-ocean-conference-2022#:~:text=The%20Blue%20Bond%20will%20be,Blue%20Principle%E2%80%9D%2C%20said%20Mr (accessed on 28 November 2022).

- UNEPFI. 2021a. Recommended Exclusions for Financing a Sustainable Blue Economy. Available online: https://www.unepfi.org/wordpress/wp-content/uploads/2021/06/Recommended-Exclusions-for-Sustainable-Blue-Economy-Financing_UNEP-FI.pdf (accessed on 28 November 2022).

- UNEPFI. 2021b. Turning the Tide: How to Finance a Sustainable Ocean Recovery. Available online: https://www.unepfi.org/publications/turning-the-tide/ (accessed on 30 January 2023).

- United Nations. n.d. SDG6. Ensure Availability and Sustainable Management of Water and Sanitation for All. Targets and Indicators. Available online: https://sdgs.un.org/goals/goal6 (accessed on 8 February 2023).

- Verlaine, Julia-Ambra. 2021. Green Investing Looks to Clean Up the Maritime Industry. Wall Street Journal. Available online: https://www.wsj.com/articles/green-investing-looks-to-clean-up-the-maritime-industry-11634549402 (accessed on 4 December 2022).

- Wabnitz, Colette, and Robert Blasiak. 2019. The rapidly changing world of ocean finance. Marine Policy 107: 103526. [Google Scholar] [CrossRef]

- West, Oliver. 2022. Bahamas eyes blue bond with IADB guarantee. Global Capital. Available online: https://www.globalcapital.com/article/2a75ucaze1qwvve5d8f7k/emerging-markets/em-latam/bahamas-eyes-blue-bond-with-iadb-guarantee (accessed on 29 November 2022).

- Winpenny, James. 2015. Water: Fit to Finance? World Water Council, OECD. Available online: https://www.worldwatercouncil.org/en/publications/water-fit-finance (accessed on 30 January 2023).