Challenges in Understanding Western Economic and Financial Concepts from the Perspective of Young Adults with a Post-Soviet Migration Background in Germany—Findings from a Qualitative Interview Study

Abstract

:1. Introduction

2. Conceptual and Theoretical Background

2.1. Economic Knowledge and Financial Knowledge

- -

- everyday money management (EDM) (includes earning income and buying goods and services, practical example: lemon laws, guarantees, and consumer protection rights),

- -

- banking (hereafter referred to as financial investing, includes saving and using credit, practical example: choosing among different credit options, credit and debit cards, investment options),

- -

- insurance (includes protecting and insuring, practical example: choosing among different kinds of insurances according to personal needs and budget).

- RQ 1: What challenges do young adults who have a post-Soviet MB face in understanding financial and economic concepts?

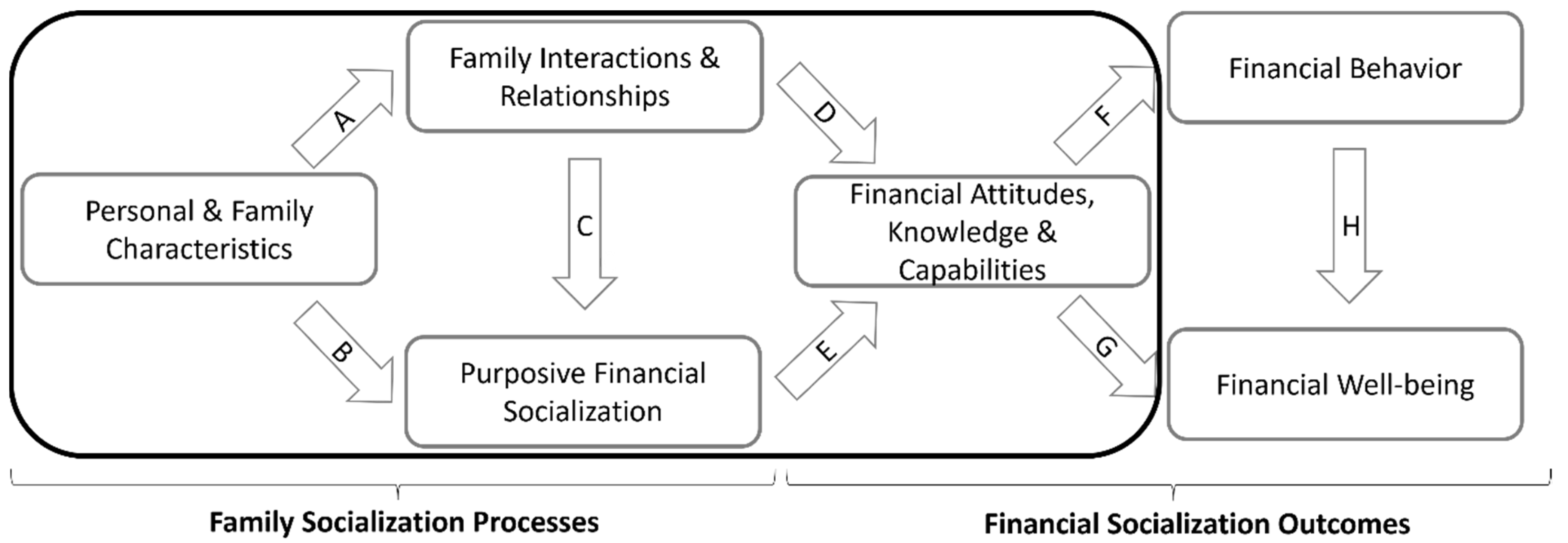

2.2. Family Financial Socialization

- RQ2: How does family financial socialization affect the economic and financial knowledge of young adults who have a post-Soviet MB?

3. Study Design3

- -

- religion and values of respondents and parents (Glorius 2015),

- -

- migration-related issues (Erner et al. 2016; Happ and Förster 2017),

- -

4. Results

4.1. Procedure for Data Analysis

4.2. Descriptive Results

4.3. Qualitative Results

- -

- Category 1 (deductive): Challenging financial terms and concepts

- Subcategory 1 (inductive): Challenges related to country of origin

- Subcategory 2 (inductive): Challenges related to language

- -

- Category 2 (deductive): Challenging economic terms and concepts

- -

- Category 3 (deductive): Influence of family financial socialization

“So the questions with insurances were always the most difficult, because you don’t have so much to do with that in Russia (…) and in Germany, for example, there are these uh compulsory insurances for all of us.”(R1, TAI, Retrospective Part, para. 67)

“So the insurance companies always try or always had as a goal, uh in the case where they have to pay this insurance, they always try not to pay this insurance, to find a reason for it. They say: well it doesn’t apply to the insurance they chose […] okay we promised so and so much money to them, but this is a different case, with the case we have to pay less.”(R1, TAI, Retrospective Part, par. 68–71)

“I have to say I actually don’t think the company pension plan is good because I think we have uh too many, so as our, as our population gets older and older and a lot less people working a lot more people have to cover who just depend on the pension, I think private pension insurance is necessary.”(R2, TAI, item FA20, para. 29)

“You get money from a bank and then you have to pay this money back to the bank and you pay more, precisely because of the interest. That’s more or less the share of the sum that you then pay back over it.”(R7, TAI, Retrospective Part, para. 211)

- -

- Minimum return, deductible, warranty law, overdraft interest rate:

“Gewähr? Is it Gewähr something like guns and stuff?”(R8, TAI, item FA13, paras. 29–44)12

“for example, if I knew what an overdraft interest rate was, I might have thought about answer choice 2.”(R5, TAI, Retrospective Part, para. 150)

“Um, yes, maybe so. And um… here I also have to say about saving for example, […] that the… the Ukrainians as a nation—but I think this is related to the conditions in which people live—they tend to save money rather than spend a larger sum on something right now.”(R4, PCI, para. 153)

“So we kind of didn’t have anything special in the family like: I have to clean the house now or something to get pocket money, no. I just got it from my parents.”.(R4, PCI, paras. 292–95)

“So with my parents, their whole life was about giving me and my sister a financial security and I don’t know, they actually worked their whole life to make sure that now with my sister we have enough money to study here [Germany].”(R7, PCI, paras. 142–43)

“There were times when these investments were actually quite (…) popular (…) among the population and there were a few companies that you could invest in. These were huge funds and unfortunately (…) you could not trust these people, these funds. (…) unfortunately they lost everything they invested. And there was, so to speak, a case that is very well known so with, with MMM14 for example. But there were also other cases and there still are, but by the fact that now people don’t really trust this advertising anymore.”(R4, PCI, para. 325)

“No, so, the [parents] insure me, I’m already insured somehow, but how? So the, so my mom makes insurance for me on everything, (…) in which case I’m guilty or not, but she said if anything happens, you have insurance, actually insured for everything, that’s why it doesn’t matter what happens to me. Yeah and that’s why she didn’t explain anywhere what exactly is what and so, yeah.”(R8, TAI, Retrospective Part, paras. 136–37)

5. Discussion, Limitations, and Outlook

5.1. Discussion

5.2. Limitations and Outlook

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

| Main Category | Subcategory |

|---|---|

| Sociodemographic details (Witzel 2012; Haupt 2022). |

|

| Religion and values of the respondents and their parents (Glorius 2015) |

|

| Migration-related issues (Erner et al. 2016; Happ and Förster 2017). |

|

| Media use (Arnold et al. 2018; Schäfer 2022; Schnell 2017). |

|

| Financial socialization (Danes 1994; Gudmunson and Danes 2011; Cwynar 2022; Glorius 2015). |

|

| Number of the Item | Description |

|---|---|

| Item FA5 (EDM) | This item asks about economic developments affecting increases in construction wages. Responses refer to the effect of an increase in loans issued for residential construction, more graduates seeking employment in the construction industry, an increase in interest rates influencing a downturn in the construction industry, and tougher oversight by building inspectors on new construction projects. |

| Item FA7 (EDM) | The item refers to the concept of income tax and which of the given answers can reduce the amount of taxable income. The selection of answers ranges from speculative gains and interest to costs for food and donations. |

| Item FA20 (Banking) | The question refers to the advantages of a company pension plan compared to a private pension plan. The selection of answers ranges from voluntary payments by the employer, unlimited number of payments by the employer, tax-free pensions, and state-promised minimum returns on occupational pensions. |

| Item FA21 (Banking) | The item asks about the banking priorities of someone who is continually in debt. The answers revolve around the lowest bank account fees, the lowest overdraft interest rate, the shortest payment period for debt repayment, and the lowest fee for a replacement card. |

| Item FA45 (Insurance) | The item asks about measures taken by insurance companies to encourage policyholders to engage in lower-risk behavior. The answers deal with co-payments in the event of a claim, the elimination of premium refunds, insurance policies without deductibles, and low premiums for insurance. |

| Item FA48 (Insurance) | The item asks about the type of insurance that covers self-inflicted damage to one’s car. The selection of answers covers different kinds of insurance. |

| Item EA16 | The item asks about which scenario would lead to an increase in gas sales. Increase in crude oil price or petroleum tax, decrease in car prices or decrease in consumer income. |

| 1 | In this article, a deliberate separation is made between economic knowledge and financial knowledge based on the integrative framework model (Happ 2020). Overlapping statements about the separation of these two concepts sometimes prevail in the literature (Happ 2020; Koh 2016). Similarly, there is inconsistent use of the following terms: education, literacy, knowledge, skills, abilities, and skills (Haupt 2022). In this article focus is on the knowledge components of economic and financial literacy. |

| 2 | The Federal Statistical Office of Germany identify people as having an MB if they or at least one of their parents was born in a country other than Germany (GFSO 2015). |

| 3 | The ethical commission and data protection officer of Leipzig University were informed and had no objections. |

| 4 | A more in-depth description of the question areas can be found in the Appendix A (Table A1). |

| 5 | Deviating from Lusardi and Mitchell’s (2014) definition of the sensitive financial phase, the lower age limit was raised to 18 in the study. This was accompanied by lower legal requirements than would have been necessary if minors had been interviewed. |

| 6 | The aim of this paper is not to compare groups with and without a migration background, but rather to identify particular barriers and challenges of one specific group. Therefore, no control group was considered at this point, which is usual for explorative studies in social sciences (see e.g., of different fields Davis et al. 2019; Fiedler and Wohlfarth 2018; Jaeger and Haley 2016; Klingler and Marckmann 2016; Lewthwaite 1996; O’Dea and Stern 2022). |

| 7 | The subjects should not have started or completed a commercial/administrative vocational training program, should not have taken the Abitur (A-level) at a business secondary school, and should not have started or completed a business degree program, not even as a minor subject. Vocational training in Germany equips learners with professional competencies, experience, skills, abilities, and knowledge. Vocational training in Germany is organized in various ways. There are school-based training programs and training programs with two learning locations: in school and in a company (dual vocational training). In dual vocational training, trainees alternate between the predominant place of learning in the company and school. Trainees receive a training allowance for the entire training period—regardless of whether they are at school or in the company (Cedefop 2020). Due to the acquisition of knowledge of economic and financial matters within commercial-administrative vocational training programs and the associated formal financial socialization experiences, this was defined as an exclusion criterion. |

| 8 | Two researchers were involved in coding to maintain acceptable intercoder reliability. |

| 9 | The German Federal Statistical Office defines people with a migration background as described in note 2. This definition does not indicate whether the persons themselves have had migration experiences. People’s own migration experiences are significant socialization processes that have a formative influence on their understanding of economic and financial concepts. In order to highlight this distinction in our sample, the criterion migration experience was surveyed and listed in the table. |

| 10 | There were three questions from each area of the TEL and three questions, each from one area of the TFL: everyday money management, banking, insurance. All eight respondents gave correct answers. |

| 11 | The questions were asked in German. These questions are subject to copyright and may not be published. The original TEL and TFL are available in English and can be accessed freely on the Internet. The original American items on the TEL or TFL are referred to in brackets (E for an item of TEL and F for an item of TFL, e.g., (item FA3)). A more detailed description of the items can be found in the Appendix A (Table A2). |

| 12 | In German, the morpheme “Gewähr” in Gewährleistungsrecht is phonetically identical to the German word “Gewehr”—which means pistol. Gewähr is the German translation for warranty, which is a legal regulation designed to protect consumers from deficient products. |

| 13 | The article refers to the understanding of saving in the sense of “not spending money”. The paper and also the statements of the respondents do not take into account whether the money is safe in the bank or in bank accounts. Respondents indicate that saving is an important way to prepare for potential crises. This is not in the sense of safe money in banks. |

| 14 | The MMM cooperative, named after the surnames of its three founders Sergei Mavrodi, Vyacheslav Mavrody, and Olga Melnikova, was an investment fund in Russia in the early 1990s that operated as a Ponzi scheme. A lot of money was collected with the promise of excessive returns and the sale of company shares. The money was stolen by the founders and a large number of people in Russia and former Soviet republics lost their money (Tolstikova 1999). |

| 15 | In this paper, qualitative methods were used to explore barriers to understanding economic and financial concepts among young adults with a post-soviet background in Germany. The knowledge gained can be used to inform pedagogy in many ways, for example to develop learner-oriented educational materials, to design relevant and engaging lessons and assignments, to train teachers effectively, and so on. Although policies and societal implications need to be explored if appropriate changes are to be made to secondary school education, these issues are beyond the scope of this paper and should be addressed in further research. |

References

- Arnett, Jeffrey Jensen. 2001. Conceptions of the Transition to Adulthood: Perspectives from Adolescence Through Midlife. Journal of Adult Development 8: 133–43. [Google Scholar] [CrossRef]

- Arnold, Eva A., Doris Neuberger, Louis Henri Seukwa, and Dirk Ulbricht. 2018. Finanzielle Allgemeinbildung Geflüchteter in Deutschland: Eine qualitative Pilotstudie [Financial Literacy of Refugees in Germany: A Qualitative Pilot Study]. Thünen Series of Applied Economic Theory—Working Paper No. 153. Rostock: University of Rostock. Available online: https://www.econstor.eu/handle/10419/174509 (accessed on 5 September 2022).

- Arrondel, Luc, Marlene Haupt, Maria Jesus Mancebón, Gianni Nicolini, Manuel Wälti, and Jasmina Wiersma. 2022. Financial literacy and financial education in Western Europe. In The Routledge Handbook of Financial Literacy. Edited by Gianni Nicolini and Brenda J. Cude. London: Routledge, pp. 363–81. [Google Scholar]

- Asarta, Carlos Jose, Roger B. Butters, and Eric Thompson. 2014. The gender question in economic education: Is it the teacher or the test? Perspectives on Economic Education Research 9: 1–19. [Google Scholar]

- Atkinson, Adele, and Flore-Anne Messy. 2012. Measuring financial literacy: Results of the OECD/International Network on Financial Education (INFE) pilot study. In OECD Working Papers on Finance, Insurance and Private Pension. Paris: OECD. [Google Scholar]

- Bandura, Albert. 1977. Social Learning Theory. Prentice Hall: Englewood Cliffs. [Google Scholar]

- Bosshardt, William, and William B. Walstad. 2014. National Standards for Financial Literacy: Rationale and Content. The Journal of Economic Education 45: 63–70. [Google Scholar] [CrossRef]

- Brau, James C., Andrew L. Holmes, and Craig L. Israelsen. 2019. Financial literacy among college students. Journal of Financial Education 45: 179–205. [Google Scholar]

- Brown, Martin, and Roman Graf. 2013. Financial literacy and retirement planning in Switzerland. Scholar Commons—University of South Carolina 6: 1–23. [Google Scholar] [CrossRef] [Green Version]

- Bucher-Koenen, Tabea, and Bettina Lamla-Dietrich. 2018. The Long Shadow of Socialism: Puzzling Evidence on East-West German Differences in Financial Literacy. Finance and Monetary Economics 47: 413–38. [Google Scholar] [CrossRef]

- Cedefop. 2020. Vocational Education and Training in Germany: Short Description. Luxembourg: Publications Office of the European Union. Available online: http://data.europa.eu/doi/10.2801/329932 (accessed on 3 December 2022).

- CEE (Council for Economic Education). 2010. Voluntary National Content Standards in Economics, 2nd ed. Available online: https://www.councilforeconed.org/wp-content/uploads/2012/03/voluntary-national-content-standards-2010.pdf (accessed on 21 October 2022).

- CEE. 2021. National Standards for Personal Financial Education. Available online: https://www.councilforeconed.org/wp-content/uploads/2021/10/2021-National-Standards-for-Personal-Financial-Education.pdf (accessed on 21 October 2022).

- Cude, Brenda J. 2022. Defining Financial Literacy. In The Routledge Handbook of Financial Literacy. Edited by Gianni Nicolini and Brenda J. Cude. London: Routledge, pp. 5–17. [Google Scholar]

- Cwynar, Andrzej. 2022. Financial literacy and financial education in Eastern Europe. In The Routledge Handbook of Financial Literacy. Edited by Gianni Nicolini and Brenda J. Cude. London: Routledge, pp. 400–19. [Google Scholar]

- Cwynar, Andrzej, Wiktor Cwynar, Monika Baryla-Matejczuk, and Moises Betancort. 2019. Sustainable Debt Behavior and Well-Being of Young Adults: The Role of Parental Financial Socialization Process. Sustainability 11: 7210. [Google Scholar] [CrossRef] [Green Version]

- Danes, Sharon M. 1994. Parental perceptions of children’s financial socialization. Journal of Financial Counseling and Planning 5: 127–49. [Google Scholar]

- Davis, Terry C., Connie L. Arnold, Glenn Mills, and Lucio Miele. 2019. A Qualitative Study Exploring Barriers and Facilitators of Enrolling Underrepresented Populations in Clinical Trials and Biobanking. Frontiers in Cell and Developmental Biology 7: 74. [Google Scholar] [CrossRef] [Green Version]

- Eliason, Scott R., Jeylan T. Mortimer, and Mike Vuolo. 2015. The transition to adulthood: Life course structures and subjective perceptions. Social Psychology Quarterly 78: 205–27. [Google Scholar] [CrossRef] [Green Version]

- Ericsson, K. Anders, and Herbert A. Simon. 1985. Protocol Analysis: Verbal Reports as Data. Cambridge: The MIT Press. [Google Scholar]

- Erner, Carsten, Michael Goedde-Menke, and Michael Oberste. 2016. Financial literacy of high school students: Evidence from Germany. The Journal of Economic Education 47: 95–105. [Google Scholar] [CrossRef]

- Fiedler, Sabine, and Agnes Wohlfarth. 2018. Language choices and practices of migrants in Germany An interview study. Language Problems and Language Planning 42: 267–87. [Google Scholar] [CrossRef]

- Förster, Manuel, and Roland Happ. 2019. The relationship among gender, interest in economic topics, media use, and the economic knowledge of students at vocational schools. Citizenship, Social and Economics Education 18: 143–57. [Google Scholar] [CrossRef]

- Förster, Manuel, Roland Happ, and Andreas Maur. 2018. The Relationship among Gender, Interest in Financial Topics and Understanding of Personal Finance. Empirical Pedagogy 32: 292–308. [Google Scholar]

- Förster, Manuel, Roland Happ, and Dimitar Molerov. 2017. Using the U.S. Test of Financial Literacy in Germany—Adaptation and Validation. Journal of Economic Education 48: 123–35. [Google Scholar] [CrossRef]

- German Federal Statistical Office [GFSO] [Statistisches Bundesamt]. 2015. Bevölkerung und Erwerbstätigkeit Bevölkerung mit Migrationshintergrund—Ergebnisse des Mikrozensus 2014 (Fachserie 1, Reihe 2.2) [Population and Employment. Population with a Migration Background—Results of the Microcensus 2014 (Fachserie 1, Reihe 2.2)]. Wiesbaden: Federal Statistical Office. [Google Scholar]

- German Federal Statistical Office [GFSO] [Statistisches Bundesamt]. 2022. Bevölkerung und Erwerbstätigkeit Bevölkerung mit Migrationshintergrund—Ergebnisse des Mikrozensus 2021—Fachserie 1 Reihe 2.2 [Population and Employment. Population with a Migration Background—Results of the Microcensus 2021—Fachserie 1, Reihe 2.2]. Available online: https://www.destatis.de/DE/Themen/Gesellschaft-Umwelt/Bevoelkerung/Wanderungen/_inhalt.html (accessed on 12 December 2022).

- Glorius, Birgit. 2015. Familie in Mittel- und Osteuropa [Family in Central and Eastern Europe]. In Handbuch Familiensoziologie [Handbook of Family Sociology]. Edited by Paul B. Hill and Johannes Kopp. Berlin/Heidelberg: Springer, pp. 55–90. [Google Scholar] [CrossRef]

- Gramatki, Iulian. 2016. A comparison of financial literacy between native and immigrant school students. Education Economics 25: 304–22. [Google Scholar] [CrossRef]

- Gudmunson, Clinton G., and Sharon M. Danes. 2011. Family financial socialization: Theory and critical review. Journal of Family and Economic Issues 32: 644–67. [Google Scholar] [CrossRef]

- Happ, Roland. 2020. Der Einfluss des Migrationshintergrundes auf unterschiedliche Facetten des ökonomischen Wissens—Implikationen für die Wirtschaftsdidaktik (Habilitationsschrift) [The Influence of Migration Background on Different Facets of Economic Knowledge—Implications for the Didactics of Economics (habilitation thesis)]. Mainz: Johannes Gutenberg-University Mainz. [Google Scholar]

- Happ, Roland, and Manuel Förster. 2017. The importance of controlling for socioeconomic factors when determining how vocational training and a secondary school economics class influence the financial knowledge of young adults in Germany. Zeitschrift für ökonomische Bildung 6: 121–46. [Google Scholar]

- Happ, Roland, and Manuel Förster. 2019. The relationship between migration background and knowledge and understanding of personal finance of young adults in Germany. International Review of Economics Education 30: 1–14. [Google Scholar] [CrossRef]

- Happ, Roland, Manuel Nagel, Olga Zlatkin-Troitschanskaia, and Susanne Schmidt. 2019. How migration background affects master degree students’ knowledge of business and economics. Studies in Higher Education 46: 457–72. [Google Scholar] [CrossRef]

- Happ, Roland, Manuel Förster, Olga Zlatkin-Troitschanskaia, and Vivian Carstensen. 2016. Assessing the previous economic knowledge of beginning students in Germany: Implications for teaching economics in basic courses. Citizenship, Social and Economics Education 15: 45–57. [Google Scholar] [CrossRef]

- Haupt, Marlene. 2022. Measuring financial literacy: The role of knowledge, skills and attitudes. In The Routledge Handbook of Financial Literacy. Edited by Gianni Nicolini and Brenda J. Cude. London: Routledge, pp. 79–95. [Google Scholar]

- Hurrelmann, Klaus. 2015. Sozialisation [Socialization]. In Handbuch der Erziehungswissenschaft [Handbook of Educational Science]. Edited by Gerhard Mertens, Winfried Böhm, Ursula Frost and Volker Ladenthin. Leiden: Ferdinand Schöningh, pp. 313–57. [Google Scholar]

- Hurrelmann, Klaus, Matthias Grundmann, and Sabine Walper. 2015. Theoretische und methodische Grundlagen [Theoretical and methodological foundations]. In Handbuch Sozialisationsforschung [Handbook Socialization Research]. 7. Auflage. Edited by Klaus Hurrelmann, Matthias Grundmann and Sabine Walper. Weinheim: Beltz, pp. 14–31. [Google Scholar]

- Huston, Sandra J. 2010. Measuring financial literacy. The Journal of Consumer Affairs 44: 296–316. [Google Scholar] [CrossRef]

- Jacobsen, Jens, and Lorena Meyer. 2022. Praxisbuch Usability and UX: Was Alle Wissen Sollten, die Websites und Apps Entwickeln (3., aktualisierte und erweiterte Auflage) [Practice book Usability and UX: What Everyone Who Develops Websites And apps Should Know (3rd, updated and expanded edition)]. Bonn: Rheinwerk Verlag GmbH. [Google Scholar]

- Jaeger, Audrey J., and Karen J. Haley. 2016. My Story, my identity: Doctoral students of color at a research university. Qualitative Research in Education 5: 276–308. [Google Scholar] [CrossRef]

- Jorgensen, Bryce L., and Jyoti Savla. 2010. Financial Literacy of Young Adults: The Importance of Parental Socialization. Family Relations Interdisciplinary Journal of Applied Family Science 59: 465–78. [Google Scholar] [CrossRef]

- Jorgensen, Bryce L., Damon L. Rappleyea, John T. Schweichler, Xiangming Fang, and Mary E. Moran. 2017. The financial behavior of emerging adults: A family financial socialization approach. Journal of Family and Economic Issues 38: 57–69. [Google Scholar] [CrossRef]

- Jüttler, Andreas, and Stephan Schumann. 2016. Effects of Students Sociocultural Background on Economic Competencies in Upper Secondary Education. In Economic Competence and Financial Literacy of Young Adults: Status and Challenges, 1st ed. Edited by Eveline Wuttke, Jürgen Seifried and Stephan Schumann. The Hague: Barbara Budrich Publishers, vol. 3, pp. 121–48. [Google Scholar] [CrossRef]

- Klingler, Corinna, and Georg Marckmann. 2016. Difficulties experienced by migrant physicians working in German hospitals: A qualitative interview study. Human Resources for Health 14: 1–13. [Google Scholar] [CrossRef] [Green Version]

- Koh, Noi Keng. 2016. Approaches to teaching financial literacy: Evidence-Based Practices in Singapore Schools. In International Handbook of Financial Literacy. Edited by Carmela Aprea, Eveline Wuttke, Klaus Breuer, Noi Keng Koh, Peter Davies, Bettina Greimel-Fuhrmann and Jane S. Lopus. Berlin/Heidelberg: Springer, pp. 499–514. [Google Scholar]

- Kowal, Sabine, and Daniel C. O’Connell. 2005. The transcription of conversations. In A Companion to Qualitative Research. Edited by Uwe Flick, Ernst von Kardorff and Ines Steinke. London: Sage, pp. 248–52. [Google Scholar]

- Krohne, Heinz-Walter, and Michael Hock. 2015. Psychologische Diagnostik. Grundlagen und Anwendungsfelder (2., überarbeitete und aktualisierte Auflage) [Psychological Diagnostics. Fundamentals and Fields of Application (2nd, Revised and Updated Edition)]. Stuttgart: Kohlhammer. [Google Scholar]

- Kuckartz, Udo. 2014. Qualitative Text Analysis. London: Sage. [Google Scholar]

- Lapan, Stephen D., Marylynn T. Quartaroli, and Frances J. Riemer. 2012. Qualitative Research: An Introduction to Methods and Designs, 1st ed. Hoboken: Jossey-Bass. [Google Scholar]

- Leighton, Jacqueline P. 2017. Using Think-Aloud Interviews and Cognitive Labs in Educational Research. Oxford: Oxford University Press. [Google Scholar]

- Lewthwaite, Malcolm. 1996. A study of international students’ perspectives on cross-cultural adaptation. International Journal for the Advancement of Counselling 19: 167–85. [Google Scholar] [CrossRef]

- Lokhande, Mohini. 2016. Doppelt benachteiligt? Kinder und Jugendliche mit Migrationshintergrund im deutschen Bildungssystem [Doubly Disadvantaged? Children and Youth with a Migration Background in the German Education System]. Berlin: Sachverständigenrat deutscher Stiftungen für Integration und Migration. [Google Scholar]

- Lusardi, Annamaria, and Olivia S. Mitchell. 2011. Financial literacy around the world: An overview. Journal of Pension Economics and Finance 10: 497–508. [Google Scholar] [CrossRef] [Green Version]

- Lusardi, Annamaria, and Olivia S. Mitchell. 2014. The Economic Importance of Financial Literacy: Theory and Evidence. Journal of Economic Literature 52: 5–44. [Google Scholar] [CrossRef] [Green Version]

- Lusardi, Annamaria, Olivia S. Mitchell, and Vilsa Curto. 2010. Financial literacy among the young. The Journal of Consumer Affairs 44: 358–80. [Google Scholar] [CrossRef]

- Mandell, Lewis. 2008. The Financial Literacy of Young American Adults. Results of the 2008 National Jump$tart Coalition Survey of High School Seniors and College Students. Jump$tart Coalition for Personal Financial Literacy. Available online: http://views.smgww.org/assets/pdf/2008%20JumpStart%20Financial%20Literacy%20Survey.pdf (accessed on 21 November 2022).

- McAuliffe, Marie, and Binod Khadria, eds. 2020. World Migration Report 2020. International Organization for Migration. Available online: https://publications.iom.int/system/files/pdf/wmr_2020.pdf (accessed on 14 September 2022).

- O’Dea, Xianghan, and Julian Stern. 2022. Cross-Cultural Integration through the Lens of Loneliness: A Study of Chinese Direct Entry Students in the United Kingdom. Qualitative Research in Education 11: 203–29. [Google Scholar] [CrossRef]

- OECD. 2016. OECD/INFE International Survey of Adult Financial Literacy Competencies. OECD. Available online: www.oecd.org/finance/OECD-INFE-International-Survey-of-Adult-Financial-Literacy-Competencies.pdf (accessed on 1 September 2022).

- OECD. 2019. Financial Literacy Needs of Migrants and their Families in the Commonwealth of Independent States (CIS). Available online: www.oecd.org/daf/fin/financial-education/financial-education.htm (accessed on 8 September 2022).

- Panagiotidis, Jannis. 2021. Postsowjetische Migration in Deutschland: Eine Einführung (Sonderausgabe für die Bundeszentrale für politische Bildung) [Post-Soviet Migration in Germany: An Introduction (Special Edition for the Federal Agency for Civic Education)]. Bonn: Bundeszentrale für Politische Bildung. [Google Scholar]

- Pang, Ming Fai. 2010. Boosting financial literacy: Benefits from learning study. Instructional Science 38: 659–77. [Google Scholar] [CrossRef]

- Saunders, Benjamin, Julius Sim, Tom Kingstone, Shula Baker, Jackie Waterfield, Bernadette Bartlam, Heather Burroughs, and Clare Jinks. 2018. Saturation in qualitative research: Exploring its conceptualization and operationalization. Quality and Quantity International Journal of Methodology 52: 1893–907. [Google Scholar] [CrossRef] [PubMed]

- Schäfer, Svenja. 2022. Mediennutzung und metakognitive Urteile: Die Rolle digitaler Nachrichten für die Wahrnehmung von Wissen (Dissertation) [Media use and metacognitive judgments: The role of digital news in the perception of knowledge. (phd thesis)]. Berlin. [Google Scholar] [CrossRef]

- Schmid, Kurt. 2006. Kenntnisse zum Themenkomplex internationaler Wirtschaft [Knowledge of the subject complex of international economics]. Ibw-Mitteilungen 4: 1–13. [Google Scholar]

- Schnell, Christina. 2017. Hat der Migrationshintergrund einen Einfluss auf die Schülerleistung im Fach Wirtschaft? Ergebnisse einer Studie in Niedersachsen [Does migration background influence student performance in economics? Results of a Study in Lower Saxony]. Journal of Economic Education 6: 98–120. [Google Scholar]

- Seeber, Günther, and Thomas Retzmann. 2017. Financial Literacy—Finanzielle (Grund-)Bildung—Ökonomische Bildung [Financial Literacy—Financial (Basic) Education—Economic Education]. Vierteljahrshefte zur Wirtschaftsforschung 86: 69–80. [Google Scholar] [CrossRef] [Green Version]

- Serido, Joyce. 2022. Financial literacy among young adults. In The Routledge Handbook of Financial Literacy. Edited by Gianni Nicolini and Brenda J. Cude. London: Routledge, pp. 31–46. [Google Scholar]

- Shim, Soyeon, Jing J. Xiao, Bonnie L. Barber, and Angela C. Lyons. 2009. Pathways to life success: A conceptual model of financial well-being for young adults. Journal of Applied Developmental Psychology 30: 708–23. [Google Scholar] [CrossRef]

- Solga, Heike, and Rosine Dombrowski. 2009. Soziale Ungleichheiten in schulischer und außerschulischer Bildung Stand der Forschung und Forschungsbedarf [Social Inequalities in School and Out-of-School Education. State of Research and Research Needs]. Working Paper 171. Düsseldorf: Hans Böckler Foundation. [Google Scholar]

- Sweller, John. 2011. Cognitive Load Theory, 1st ed. Berlin/Heidelberg: Springer. [Google Scholar]

- Tolstikova, Natasha. 1999. MMM As a Phenomenon of the Russian Consumer Culture. In European Advances in Consumer Research. Edited by Bernard Dubois, Tina M. Lowrey, L. J. Shrum and Marc Vanhuele. Seattle: Association for Consumer Research, vol. 4, pp. 208–15. [Google Scholar]

- Van Someren, Maarten W., Yvonne F. Barnard, and Jacobijn. A. C. Sandberg. 1994. The Think aloud Method: A Practical Guide to Modeling Cognitive Processes. Cambridge: Academic Press. [Google Scholar]

- Walstad, William. B. 1998. Why it’s Important to Understand Economics. The Region, 22–26. Available online: https://www.minneapolisfed.org/article/1998/why-its-important-to-understand-economics (accessed on 12 November 2022).

- Walstad, William B., Ken Rebeck, and Roger B. Butters. 2013. The Test of Economic Literacy. Examiners Manual, 4th ed. New York: Council for Economic Education. [Google Scholar]

- Walstad, William B., and Ken Rebeck. 2016. The Test of Financial Literacy Examiners Manual. New York: Council for Economic Education. [Google Scholar]

- Witzel, Andreas. 2012. The Problem-Centered Interview: Principles and Practice. London: Sage. [Google Scholar]

- World Health Organization (WHO). 2021. Health Systems in Action Kyrgyzstan. Geneva: WHO. [Google Scholar]

- Worthington, Andrew C., and Ainulashkin Marzuki. 2022. Financial literacy, financial education, and Islamic finance. In The Routledge Handbook of Financial Literacy. Edited by Gianni Nicolini and Brenda J. Cude. London: Routledge, pp. 470–85. [Google Scholar]

- Wuttke, Eveline, and Carmela Aprea. 2018. A situational judgment approach for measuring young adults’ financial literacy. Empirical Pedagogy 32: 272–92. [Google Scholar]

- Zuhair, Segu, Guneratne Wickremasinghe, and Riccardo Natoli. 2015. Migrants and self-reported financial literacy. Insights from a case study of newly arrived CALD migrants. International Journal of Social Economics 42: 368–86. [Google Scholar] [CrossRef]

| Respondent (R#) | Mother | Father | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Country of Birth | In Germany Since | Mother Tongue | Age | Country of Birth | In Germany Since | Mother Tongue | Country of Birth | In Germany Since | Mother Tongue | |

| 1 | Russia | 2019 | Russian | 22 | Russia | - | Russian | Russia | - | Russian |

| 2 | Germany | birth | German | 21 | Belarus | 1999 | Russian | Russia | around 1990 | Russian |

| 3 | Germany | birth | German | 18 | Kazakhstan | 1995 | Russian | Russia | 1995 | Russian |

| 4 | Ukraine | 2014 | Ukrainian | 24 | Ukraine | - | Ukrainian | Ukraine | - | Ukrainian |

| 5 | Russia | 2004 | German | 21 | Kazakhstan | 2004 | Russian | Kazakhstan | 2004 | Russian |

| 6 | Germany | birth | Azerbaijani | 20 | Azerbaijan | 2000 | Azerbaijani | Azerbaijan | before 2000 | Azerbaijani |

| 7 | Kyrgyzstan | 2017 | Russian | 21 | Kyrgyzstan | - | Russian | Kyrgyzstan | - | Russian |

| 8 | Latvia | 2016 | Latvian | 24 | Latvia | - | Russian | Latvia | - | Russian |

| TEL/TFL Area | Correct Answers (8 Resp.) | Rate in % | Male (4 Resp.) | Rate in % | Female (4 Resp.) | Rate in % | With ME (4 Resp.) | Rate in % | Without ME (4 Resp.) | Rate in % |

|---|---|---|---|---|---|---|---|---|---|---|

| TEL | 20 | 83.33 | 11 | 91.67 | 9 | 75.00 | 11 | 91.67 | 9 | 75.00 |

| TFL EDM | 14 | 58.33 | 7 | 58.33 | 7 | 58.33 | 7 | 58.33 | 7 | 58.33 |

| TFL banking | 14 | 58.33 | 8 | 66.67 | 6 | 50.00 | 8 | 66.67 | 6 | 50.00 |

| TFL insurance | 14 | 58.33 | 7 | 58.33 | 7 | 58.33 | 9 | 75.00 | 5 | 41.67 |

| Challenging Financial Terms and Concepts | |

|---|---|

| Content | Financial terms and concepts unknown or unfamiliar to respondents, as they cannot explain them adequately. |

| Reason | Cultural- or country-specific differences, lack of equivalent terms or concepts, or language challenges may be reasons for finding the terms and concepts challenging. |

| Example of response | “Uh I don’t know exactly what warranty uh right is, but um yeah with that I kind of can’t quite answer the question either” (R2, TAI, para. 23). |

| Delimitation | Statements about economic concepts such as competitive market, functions of money or the labor market are assigned to category 2. |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Heidel, S.; Happ, R. Challenges in Understanding Western Economic and Financial Concepts from the Perspective of Young Adults with a Post-Soviet Migration Background in Germany—Findings from a Qualitative Interview Study. J. Risk Financial Manag. 2023, 16, 165. https://doi.org/10.3390/jrfm16030165

Heidel S, Happ R. Challenges in Understanding Western Economic and Financial Concepts from the Perspective of Young Adults with a Post-Soviet Migration Background in Germany—Findings from a Qualitative Interview Study. Journal of Risk and Financial Management. 2023; 16(3):165. https://doi.org/10.3390/jrfm16030165

Chicago/Turabian StyleHeidel, Sebastian, and Roland Happ. 2023. "Challenges in Understanding Western Economic and Financial Concepts from the Perspective of Young Adults with a Post-Soviet Migration Background in Germany—Findings from a Qualitative Interview Study" Journal of Risk and Financial Management 16, no. 3: 165. https://doi.org/10.3390/jrfm16030165