Corporate Social Responsibility Funding and Its Impact on India’s Sustainable Development: Using the Poverty Score as a Moderator

,

,  , , ,

, , ,

Abstract

:1. Introduction

2. Review of Literature and Hypothesis Development

2.1. CSR and Sustainable Development (SD)

2.2. CSR and Education

2.3. CSR and Environment

3. Data and Research Methodology

3.1. Data

3.2. Methodology

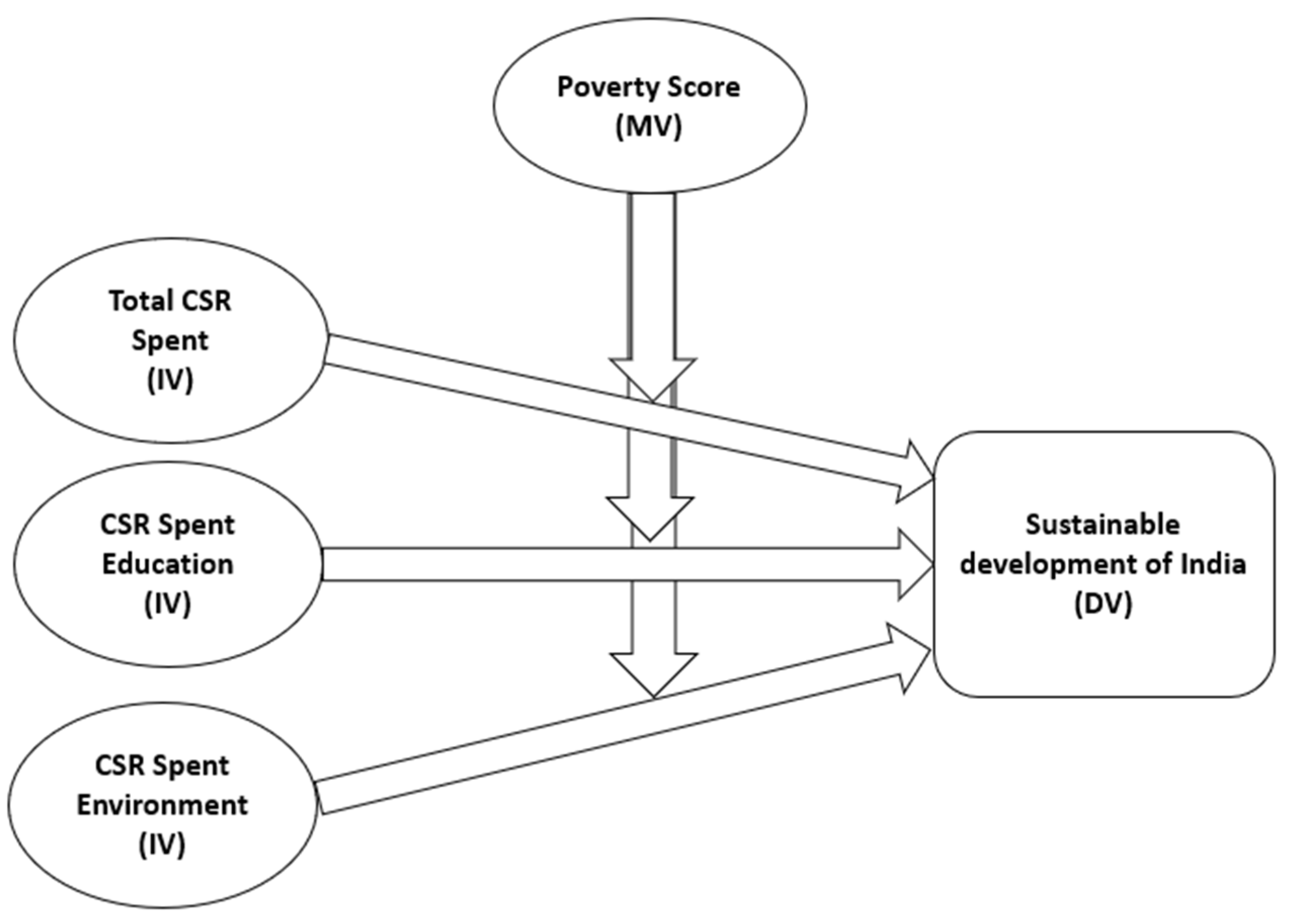

3.3. Variables

4. Results

4.1. Statistics Summary

4.2. Multicollinearity and Endogeneity

4.3. Results of Regression Analysis

4.4. Robustness Check

5. Discussion

5.1. Hypothesis Validation and Comparison with Previous Studies

5.2. Contribution and Implications

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Abbas, Jaffar, Shahid Mahmood, Hashim Ali, Muhammad Ali Raza, Ghaffar Ali, Jaffar Aman, Shaher Bano, and Mohammad Nurunnabi. 2019. The effects of corporate social responsibility practices and environmental factors through a moderating role of social media marketing on sustainable performance of business firms. Sustainability 11: 3434. [Google Scholar] [CrossRef]

- Alvarado-Herrera, Alejandro, Enrique Bigne, Joaquín Aldas-Manzano, and Rafael Curras-Perez. 2017. A scale for measuring consumer perceptions of corporate social responsibility following the sustainable development paradigm. Journal of Business Ethics 140: 243–62. [Google Scholar] [CrossRef]

- Arora, Bimal, and Ravi Puranik. 2004. A review of corporate social responsibility in India. Development 47: 93–100. [Google Scholar] [CrossRef]

- Avotra, Andrianarivo, Andriandafiarisoa Ralison Ny, Chenyun Ye, Yongmin Wu, Lijuan Zhang, and Nawaz Ahsan. 2021. Conceptualising the state of the art of corporate social responsibility (CSR) in green construction and its nexus to sustainable development. Frontiers in Environmental Science 541: 774822. [Google Scholar] [CrossRef]

- Baltagi, Badi Hani, and Badi H. Baltagi. 2008. Econometric Analysis of Panel Data. Chichester: John Wiley & Sons, vol. 4. [Google Scholar]

- Bhagwat, Pranjali. 2011. Corporate social responsibility and sustainable development. Paper presented at Conference on Inclusive & Sustainable Growth, Nagpur, India, July 15–16. [Google Scholar]

- Bhimavarapu, Venkata M., Shailesh Rastogi, and Jagieevan Kanoujiya. 2022. Ownership concentration and its influence on transparency and disclosures of banks in India. Corporate Governance: The International Journal of Business in Society, ahead-of-print. [Google Scholar]

- Chatterjee, Bhaskar, and Nayan Mitra. 2017. CSR should contribute to the national agenda in emerging economies-the ‘Chatterjee Model’. International Journal of Corporate Social Responsibility 2: 1–11. [Google Scholar] [CrossRef]

- Chopra, Abha, and Shruti Marriya. 2013. Corporate social responsibility and education in India. Issues and Ideas in Education 1: 13–22. [Google Scholar] [CrossRef]

- Cordeiro, James J., A. Ambra Galeazzo, Tara Shankar Shaw, Rajaram Veliyath, and M. K. Nandakumar. 2018. Ownership influences on corporate social responsibility in the Indian context. Asia Pacific Journal of Management 35: 1107–36. [Google Scholar] [CrossRef]

- Douglas, Alex, John Doris, and Brian Johnson. 2004. Corporate social reporting in Irish financial institutions. The TQM Magazine 16: 387–95. [Google Scholar] [CrossRef]

- Ebner, Daniela, and Rupert J. Baumgartner. 2006. The relationship between sustainable development and corporate social responsibility. In Corporate Responsibility Research Conference. Belfast Dublin: Queens University, vol. 4, No. 5.9. p. 2006. [Google Scholar]

- ElAlfy, Amr, Nicholas Palaschuk, Dina El-Bassiouny, Jeffrey Wilson, and Olaf Weber. 2020. Scoping the evolution of corporate social responsibility (CSR) research in the sustainable development goals (SDGs) era. Sustainability 12: 5544. [Google Scholar] [CrossRef]

- Elkington, John. 1998. Cannibals with Forks: The Triple Bottom Line of 21st Century Business. Stony Creek: New Society Publishers. [Google Scholar]

- Fallah Shayan, Niloufar, Nasrin Mohabbati-Kalejahi, Sepideh Alavi, and Mohammad Ali Zahed. 2022. Sustainable development goals (SDGs) as a framework for corporate social responsibility (CSR). Sustainability 14: 1222. [Google Scholar] [CrossRef]

- Fatma, Mobin, and Zillur Rahman. 2016. The CSR’s influence on customer responses in Indian banking sector. Journal of Retailing and Consumer Services 29: 49–57. [Google Scholar] [CrossRef]

- Ghanbarpour, Tohid, and Anders Gustafsson. 2022. How do corporate social responsibility (CSR) and innovativeness increase financial gains? A customer perspective analysis. Journal of Business Research 140: 471–81. [Google Scholar] [CrossRef]

- Gigauri, Iza. 2022. Corporate Social Responsibility and COVID-19 Pandemic Crisis: Evidence from Georgia. In Research Anthology on Developing Socially Responsible Businesses. Hershey: IGI Global, pp. 1668–87. [Google Scholar]

- Grover, Purva, Arpan Kumar Kar, and P. Vigneswara Ilavarasan. 2019. Impact of corporate social responsibility on reputation—Insights from tweets on sustainable development goals by CEOs. International Journal of Information Management 48: 39–52. [Google Scholar] [CrossRef]

- Hamann, Ralph. 2003. Mining companies’ role in sustainable development: The’why’and’how’of corporate social responsibility from a business perspective. Development Southern Africa 20: 237–54. [Google Scholar] [CrossRef]

- Herrmann, Kristina K. 2004. Corporate Social Responsibility and Sustainable Development: The European Union Initiative as a Case Study. Indiana Journal of Global Legal Studies 11: 205–32. Available online: https://www.repository.law.indiana.edu/ijgls/vol11/iss2/6 (accessed on 31 July 2021). [CrossRef]

- Hsiao, Cheng. 2007. Panel data analysis—Advantages and challenges. Test 16: 1–22. [Google Scholar] [CrossRef]

- Huk, Katarzyna, and Mateusz Kurowski. 2021. The environmental aspect in the concept of corporate social responsibility in the energy industry and sustainable development of the economy. Energies 14: 5993. [Google Scholar] [CrossRef]

- Ibidunni, Olanrewaju Samson. 2013. Corporate social responsibility in higher education institutions in the development of communities and society in Nigeria. In Corporate Social Responsibility. Berlin/Heidelberg: Springer, pp. 235–64. [Google Scholar]

- İyigün, N. Öykü. 2015. What could entrepreneurship do for sustainable development? A corporate social responsibility-based approach. Procedia-Social and Behavioral Sciences 195: 1226–31. [Google Scholar] [CrossRef]

- Kanji, Repaul, and Rajat Agrawal. 2020. Exploring the use of corporate social responsibility in building disaster resilience through sustainable development in India: An interpretive structural modelling approach. Progress in Disaster Science 6: 100089. [Google Scholar] [CrossRef]

- Kanoujiya, Jagjeevan, Shailesh Rastogi, and Venkata Mrudula Bhimavarapu. 2022. Competition and distress in banks in India: An application of panel data. Cogent Economics & Finance 10: 2122177. [Google Scholar]

- Kolk, Ans, and Rob Van Tulder. 2010. International business, corporate social responsibility and sustainable development. International Business Review 19: 119–25. [Google Scholar] [CrossRef] [Green Version]

- Li, Xiao, Gang Liu, Qinghua Fu, Abdul Aziz Abdul Rahman, Abdelrhman Meero, and Muhammad Safdar Sial. 2022. Does Corporate Social Responsibility Impact on Corporate Risk-Taking? Evidence from Emerging Economy. Sustainability 14: 531. [Google Scholar] [CrossRef]

- Manohar, E. 2019. Essential alignment: Corporate social responsibility and social impact assessment for sustainable development—An empirical study. Journal of Management 6. Available online: http://www.iaeme.com/jom/issues.asp?JType=JOM&VType=6&IType=3 (accessed on 30 September 2022). [CrossRef]

- Matten, Drik, and Jeremy Moon. 2004. Corporate social responsibility. Journal of Business Ethics 54: 323–37. [Google Scholar] [CrossRef]

- Mishra, Lokanath. 2021. Corporate social responsibility and sustainable development goals: A study of Indian companies. Journal of Public Affairs 21: e2147. [Google Scholar] [CrossRef]

- Moon, Jeremy. 2007. The contribution of corporate social responsibility to sustainable development. Sustainable Development 15: 296–306. [Google Scholar] [CrossRef]

- Nagaich, Sangeeta, and Preeti Sharma. 2014. Is literacy a cause of an increase in women work participation in Punjab (India): A regional analysis? International Journal of Research in Applied, Natural and Social Sciences 2: 3–8. [Google Scholar]

- Narwal, Mahabir, and Tejinde Sharma. 2008. Perceptions of corporate social responsibility in India: An empirical study. Journal of Knowledge Globalization 1: 61–79. [Google Scholar]

- NITI Aayog. 2018. SDG India Index|NITI Aayog. Available online: https://www.niti.gov.in/sdg-india-index#:~:text=The%20SDG%20India%20Index%20is,society%20and%20the%20general%20public (accessed on 8 August 2022).

- Revathy, B. 2012. Corporate social responsibility—An implementation guide for business. Far East Journal of Psychology and Business 6: 15–31. [Google Scholar]

- Rural Population; n.d. Rural Population. Available online: https://ejalshakti.gov.in/IMISReports/Reports/BasicInformation/rpt_RWS_RuralPopulation_S.aspx?Rep=0 (accessed on 10 September 2022).

- Sengupta, Meeta. 2017. Impact of CSR on education sector. In Corporate Social Responsibility in India. Cham: Springer, pp. 33–50. [Google Scholar]

- Shah, Krishna Kumar. 2012. Corporate social responsibility in Nepal. Academic Voices: A Multidisciplinary Journal 2: 33–37. [Google Scholar] [CrossRef]

- Sharma, Seema G. 2009. Corporate social responsibility in India: An overview. Int’l Law 43: 1515. [Google Scholar]

- Sharma, Seema. 2011. Corporate social responsibility in India. Indian Journal of Industrial Relations 46: 637–49. [Google Scholar]

- Singh, B. J. R., and Preetinder Kaur. 2016. Corporate social responsibility in India. International Journal of Higher Education Research & Development 1: 51–96. [Google Scholar]

- Singh, Seema. 2016. Integrating social responsibility of university and corporate sector for inclusive growth in India. Higher Education for the Future 3: 183–96. [Google Scholar] [CrossRef]

- SOUTHTRIPURA DISTRICT. 2006. Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA). Available online: https://southtripura.nic.in/scheme/mahatma-gandhi-national-rural-employment-guarantee-act-mgnrega/ (accessed on 30 September 2020).

- Verma, Sanjeev, and Rohit Chauhan. 2007. Role of Corporate Social Responsibility in Developing Economies. Available online: http://hdl.handle.net/2259/657 (accessed on 31 July 2021).

- Wooldridge, Jeffrey M. 2015. Introductory Econometrics: A Modern Approach. Boston: Cengage Learning. [Google Scholar]

- Xia, Bo, Ayokunle Olanipekun, Qing Chen, Lin-lin Xie, and Yong Liu. 2018. Conceptualising the state of the art of corporate social responsibility (CSR) in the construction industry and its nexus to sustainable development. Journal of Cleaner Production 195: 340–53. [Google Scholar] [CrossRef]

- Yadav, Hemant. 2018. Depress Poverty and Impress Rural Development through MNREG. Journal of Commerce 13: 52–60. Available online: http://jctindia.org/images/articles/15542117721.pdf (accessed on 31 July 2021).

- Yadav, Sopan Vikrant. 2020. Sustainable Development and Corporate Social Responsibility in India: A Critique. International Journal of Advanced Research 8: 121–24. [Google Scholar] [CrossRef] [PubMed]

- Zahid, R. Ammar, Muhammad Kaleem Khan, Waseem Anwar, and Umer Sahil Maqsood. 2022a. The role of audit quality in the ESG-corporate financial performance nexus: Empirical evidence from Western European companies. Borsa Istanbul Review, in press. [Google Scholar] [CrossRef]

- Zahid, R. Ammar, Muzammil Khurshid, and Wajid Khan. 2022b. Do chief executives matter in corporate financial and social responsibility performance nexus? A dynamic model analysis of Chinese firms. Frontiers in Psychology 13: 897444. [Google Scholar] [CrossRef]

- Zaman, Rashid, Tanusree Jain, Georges Samara, and Dima Jamali. 2022. Corporate governance meets corporate social responsibility: Mapping the interface. Business & Society 61: 690–752. [Google Scholar]

{kind=link}

| SN | Variable | Type | Definition | Source |

|---|---|---|---|---|

| 1 | SDG_Ind | DV | The Sustainable Development Goals (SDG India) aims to thoroughly evaluate the nation’s social, economic, and environmental problems, as well as those of its states and union territories (UTs). | NITI Aayog (2018) |

| 2 | T_CSR | IV | According to the CSR policy, each company that must follow CSR standards must invest 2% of its average net earnings over the preceding three years. This CSR effort will assist India in achieving its sustainable development goals through public–private partnerships. This study uses the overall CSR amount spent on sustainable development as an explanatory variable. | (Mishra 2021; Moon 2007). |

| 3 | CSR_edu | IV | CSR amount spent on education is used as an explanatory variable. | (Mishra 2021; Moon 2007). |

| 4 | CSR_Env | IV | CSR spent on the environment is used as an explanatory variable. | (Mishra 2021; Moon 2007). |

| 5 | IND_PS | MV | In this study, the India poverty score is employed as a moderator. | (SOUTHTRIPURA DISTRICT 2006; Yadav 2018). |

| 6 | RP | CV | Numbers of rural populations in Indian states are used in this study as a control variable. | Rural Population (n.d.) |

| Variables | Mean | SD | Min | Max |

|---|---|---|---|---|

| SDG_Ind | 64.30645 | 6.173797 | 50 | 75 |

| T_CSR | 385.4104 | 610.6643 | 0.11 | 3336.14 |

| CSR_edu | 167.272 | 291.4414 | 0 | 1611.6 |

| CSR_Env | 31.56145 | 49.97927 | 0 | 283.11 |

| IND_PS | 48.6504 | 20.66298 | 0.71 | 76 |

| RP | 3.0207 | 3.6007 | 252,204 | 1.7008 |

| Variables | T_CSR | CSR_edu | CSR_Env | dT_CSR | dCSR_edu | dCSR_Env | dIND_PS | i_dCSR_dIND_PS | i_dCSR_edu_dIND_PS | i_dT_CSR_Env_dIND_PS | ln_RP |

|---|---|---|---|---|---|---|---|---|---|---|---|

| T_CSR | 1.0000 | ||||||||||

| CSR_edu | 0.9889 * | 1.0000 | |||||||||

| CSR_Env | 0.8193 * | 0.7946 * | 1.0000 | ||||||||

| dT_CSR | 1.0000 * | 0.9889 * | 0.8193 * | 1.0000 | |||||||

| dCSR_edu | 0.9889 * | 1.0000 * | 0.7946 * | 0.9889 * | 1.0000 | ||||||

| dCSR_Env | 0.8193 * | 0.7946 * | 1.0000 * | 0.8193 * | 0.7946 * | 1.0000 | |||||

| dIND_PS | −0.0492 | −0.0287 | −0.0234 | −0.0492 | −0.0287 | −0.0287 | 1.0000 | ||||

| i_dT_CSR_dIND_PS | −0.1404 | −0.1423 | −0.0447 | −0.1404 | −0.1423 | −0.0447 | 0.0170 | 1.0000 | |||

| i_dCSR_edu_dIND_PS | −0.1461 | −0.1518 | −0.0357 | −0.1461 | −0.1518 | −0.0357 | −0.0051 | 0.9887 * | 1.0000 | ||

| i_dCSR_Env_dIND_PS | −0.0478 | −0.0371 | 0.0304 | −0.0478 | −0.0371 | 0.0304 | 0.0029 | 0.8785 * | 0.8357 * | 1.0000 | |

| ln_RP | 0.4896 * | 0.4509 * | 0.4864 * | 0.4896 * | 0.4509 * | 0.4864 * | −0.0239 | −0.0057 | 0.0045 | 0.0146 | 1.0000 |

| .DV: SDG_Ind | ||||||

|---|---|---|---|---|---|---|

| T_CSR | CSR_edu | CSR_Env | i_dCSR_dIND_PS | i_dCSR_edu_dIND_PS | i_dT_CSR_Env_dIND_PS | |

| Durbin Chi-2 | 8.08514 * | 6.30402 * | 5.45476 * | 0.835575 | 0.709013 | 0.306135 |

| (0.0045) | (0.0120) | (0.0195) | (0.3607) | (0.3998) | (0.5801) | |

| Wu-Hausman Test | 8.40299 * | 6.44144 * | 5.52924 * | 0.796756 | 0.675306 | 0.290529 |

| (0.0045) | (0.0126) | (0.0205) | (0.3741) | (0.4131) | (0.5910) | |

| DV: SDG_Ind | Model 1 (Base_Model_1) | Model 2 (Base_Model_2) | Model 3 (Base_Model_3) | Model 4 (Interaction_1) | Model 5 (Interaction_2) | Model 6 (Interaction_3) |

|---|---|---|---|---|---|---|

| Coeff. | Coeff. | Coeff. | Coeff. | Coeff. | Coeff. | |

| SDG_Ind log 1 | 0.132 * | 0.136 * | 0.206 * | 0.167 * | 0.173 * | 0.236 * |

| T_CSR | 0.003 * | |||||

| CSR_edu | 0.007 * | |||||

| CSR_Env | 0.058 * | |||||

| dT_CSR | 0.004 * | |||||

| dCSR_edu | 0.007 * | |||||

| dCSR_Env | 0.059 * | |||||

| dIND_PS | 0.108 * | 0.112 *** | 0.112 *** | |||

| i_dCSR_dIND_PS | 0.000 *** | |||||

| i_dCSR_edu_dIND_PS | 0.000 * | |||||

| i_dCSR_Env_dIND_PS | 0.083 | |||||

| ln_RP | −1.433 * | −1.303 * | −1.630 * | −1.436 * | −1.318 * | −1.611 * |

| Cons. | 77.669 * | 75.597 * | 75.744 * | 77.002 * | 74.649 * | 75.384 * |

| Sragan Test | 121.1437 | 120.5826 | 109.3801 | 120.2162 | 0.0508 | 109.1444 |

| AR (1) | −1.7949 | −1.7962 | −1.8336 | −1.868 | −1.8716 | −1.843 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gautam, R.S.; Bhimavarapu, V.M.; Rastogi, S.; Kappal, J.M.; Patole, H.; Pushp, A. Corporate Social Responsibility Funding and Its Impact on India’s Sustainable Development: Using the Poverty Score as a Moderator. J. Risk Financial Manag. 2023, 16, 90. https://doi.org/10.3390/jrfm16020090

Gautam RS, Bhimavarapu VM, Rastogi S, Kappal JM, Patole H, Pushp A. Corporate Social Responsibility Funding and Its Impact on India’s Sustainable Development: Using the Poverty Score as a Moderator. Journal of Risk and Financial Management. 2023; 16(2):90. https://doi.org/10.3390/jrfm16020090

Chicago/Turabian StyleGautam, Rahul Singh, Venkata Mrudula Bhimavarapu, Shailesh Rastogi, Jyoti Mehndiratta Kappal, Hitesh Patole, and Aman Pushp. 2023. "Corporate Social Responsibility Funding and Its Impact on India’s Sustainable Development: Using the Poverty Score as a Moderator" Journal of Risk and Financial Management 16, no. 2: 90. https://doi.org/10.3390/jrfm16020090