Development of the Financial Flow Model for the Sustainable Development of an Industrial Enterprise

Abstract

:1. Introduction

- At the level of macroeconomic systems the category of «economic complexity» is highlighted and evaluated in relation to the environmental impact (Tauseef Hassan et al. 2023); proposed «integrated resource efficiency index», IRE-index, the multiple regression method was used (Koh et al. 2016); the Advanced Human Development Index, determined by the geometric mean method of the four feathers—«Life», «Education», «Income» and «Environment» (Karnitis et al. 2021); the regional sustainable development index (RSDI), calculated also by the geometric mean formula and including 6 indicators—economic growth rates, open unemployment, poverty rate, human development index, Gini index and environmental quality index (Rahma et al. 2019); systematized a wide range of sustainable development assessment techniques, including WDI (world development indicators), Eurostat sustainable development indicators, HDI (human development index), EF (ecological footprint), EPI (environmental performance index), SSI (sustainable society index), EISD (energy indicators for sustainable development), which is reflected in the study (Andriuškevičius et al. 2022); proposed weighting method for energy sustainability analysis of renewable energy production (Tsai 2010).

- At the level of municipalities, 13 private indicators of sustainable development (poverty ratio, physician density, mortality rate, under −5, +15 literacy rate, % total enrolment rate in basic education and others) have been assessed (Salem et al. 2020); other scientists applied the grey entropy method and formed the sustainable urban development system, which covers not 3 classic elements (economic, social and environmental), but 5 (society, the economy, the environment, resources, and technology) (Gong et al. 2019); systematized indicators of sustainable urban development by blocks: environment, transport, economic development, land use, demography, construction, health care, civic engagement (Hassan and Kotval-K 2019). (Awan et al. 2022; Liu et al. 2022b) revealed a U-shaped (nonlinear) relationship between urbanization and the environment (i.e., CO2 emissions).

- At the mesolevel (industry level) an indicator of production reliability at the level of industries was developed, based on the weighting of normalized indicators of economic, social and environmental reliability (Lubnina et al. 2016); an extensive set of key performance indicators (48 social indicators, 30 environmental indicators, and 39 economic indicators) presented in the context of three factors of sustainable industrial development (Contini and Peruzzini 2022); an aggregate indicator of sustainable industrial development based on discriminant analysis and principal component method (Shinkevich et al. 2022) was proposed, etc. Among our own research, we noted the methodology to assess the sustainable development of innovative mesosystems based on a composite indicator ISDI: calculated as a geometric mean of three factors (environmental, economic and social), includes indicators of environmental innovation, the share of enterprises with high pollution levels, the quality index of patent applications, return on assets, the number of researchers in the industry, the index of recycled and subsequently used water in the mesosystem, the share of catchment (Shinkevich et al. 2021b).

- At the microeconomic level, the issue under study through the SAM4SIP method (Self-Assessment Method of capabilities for Sustainability Implementation in the Product innovation process) of assessing an organization’s capacity to implement sustainability (Schulte and Hallstedt 2018) is revealed, the author’s solution is based on empirical research; the formation of Sustainable Development Map of the enterprise (Patalas-Maliszewska and Łosyk 2020); the development of an indicator the maturity of organization in the sustainable development management Leading Sustainability (LeadSUS), which is calculated as the average of six Relevant Domains—General Requirements/Aspects, Resource Management, Sustainable Products and Services, Social Responsibility, Implementation and Operation, Management/Leadership and Strategy (Negulescu et al. 2022), etc.

2. Materials and Methods

- significant strategic role in the development of Russian industry;

- high level of environmental pollution due to the scale and specifics of production;

- a key place in our scientific research (Shinkevich et al. 2021a);

- research on the regularity of the sustainable development the industrial system of PJSC «Nizhnekamskneftekhim»;

- identifying the relationship between financial investments in the industrial system modernization and the level of its sustainable development;

- modeling and optimization of financial flows to ensure the sustainable development of an industrial enterprise.

- In this regard, the study covers several phases.

- Development of a universal methodological approach to assessing the sustainable development of an industrial enterprise. At this stage, we have formulated a system of three-way diagnostics of sustainable development. The calculation foundation develops the mesolevel approach for the assessment of the sustainable development of innovative mesosystems based on a comprehensive indicator ISDI (Shinkevich et al. 2021b) proposed earlier. However, in this case we focus on the microeconomic system and propose to expand the list of indicators accounted for the economic, environmental and social aspects. For this we propose to use the geometric average formula to estimate the economic factor of the sustainable development of an industrial enterprise (Iecon), the social factor (Isoc) and the environmental factor (Iecol):where Vi—variable (sub-indices); VRoE—returns on energy, ruble per ruble; VMP—material productivity, ruble per ruble; VRoS—return on sales (coefficient); VSP—social policy and charity expenses per 1 employee, million rubles per person; VRGW—rate of growth of tariff rates/wages, %; VSTR—average staff turnover rate, % (due to its negative nature, the indicator is calculated as the inverse of the average staff turnover rate); VREP—the volume of reduction of emissions of pollutants into the atmospheric air, thousand tons; VRWD—the volume of reduction of wastewater discharges in volume, million cubic meters.

- 2.

- Verification of the proposed methodological approaches by assessing the closeness of the relationship between the calculated values of SDIE (according to the three methods) and the volume of reduction of pollutant emissions VREP and wastewater discharges VRWD. Based on the evaluation results of the pair correlation coefficients, the choice in favor of the best the three methods made. The emphasis on environmental indicators is due to the positive dynamics of the development the indicators, in this regard, this factor chosen as the basis for the verification the methodology.

- 3.

- The construction of an economic-mathematical model of the sustainable development dependence indicator from the industrial enterprise on financial flows:

- acquisition of fixed assets, million rubles (investment activities) (VIA);

- attraction of long-term credits and loans, million rubles (VLTF);

- attraction of short-term credits and loans, million rubles (VSTF).

- 4.

- The emphasis on investments is due to the following: they are aimed at modernization of fixed assets (modern development programs of industries and industrial enterprises), corporate information systems, which contributes to increasing industrial safety, improving working conditions (lean production, 5S), improving the quality of products, saving resources. All of this is a sign of sustainable development.

- 5.

- Determination the optimal values of financial flows that determine, among other things, the sustainable development of the microeconomic system.

3. Results

3.1. Stage 1: Analysis of Individual Aspects of Sustainable Development of an Industrial Enterprise

3.1.1. Diagnostics of the Main Indicators of Economic, Ecological and Social Development of PJSC «Nizhnekamskneftekhim»

3.1.2. Assessment of Sustainable Development Factors of PJSC «Niznekaskneftekhim»

3.2. Stage 2: Three-Way Diagnostics of Sustainable Development of an Industrial Enterprise

3.3. Stage 3: Verification the Proposed Methods for Assessing the Sustainable Development of the Enterprise

3.4. Stage 4: Development of an Economic-Mathematical Model of Financial Flows for Sustainable Development of an Industrial Enterprise

- the coefficient of determination R2 was 0.994 (or 99.4%);

- Fisher’s F-criterion is fulfilled, the hypothesis that the differences between the indicators are non-random and the regression equation is adequate is accepted, because:

- t-Student’s criterion is fulfilled, the significance of the obtained regression coefficients is confirmed, because:

|tcalc| > ttabl. (|−14.79| > 4.3);

|tcalc| > ttabl. (|−10.09| > 4.3).

3.5. Stage 5: Optimization the Financial Flows for Sustainable Development of an Industrial Enterprise

VSTF = 0.257 billion rubles.

4. Discussion

- First, the patterns of enterprise development in the context of individual indicator identified: unbalanced development of economic, environmental and social components; the presence of unrealized potential for sustainable development of the enterprise, despite the high investment activity.

- Secondly, a methodology for assessing the sustainable development of an industrial enterprise based on the calculation the integral index as an aggregator of the three known factors of sustainable development, taking into account key aspects of the enterprise (energy consumption, material consumption, return on sales, per capita social policy costs, staff turnover, reduction of pollutant emissions and wastewater discharges), covering three methods of measurement was developed. The uniqueness of the author’s approach lies in the comparison of the results of the three methods of calculating the integral indicator and the possibility of choosing the most acceptable calculation option.

- Thirdly, the economic-mathematical model of sustainable development management of industrial enterprise developed, which allows identifying the best proportions of attracting credit resources, contributing to the increase in the integral indicator of sustainable development the industrial enterprise. The peculiarity of the approach lies in the flexibility of modeling provided by the choice of the method for calculating the aggregate indicator of sustainable development.

5. Conclusions

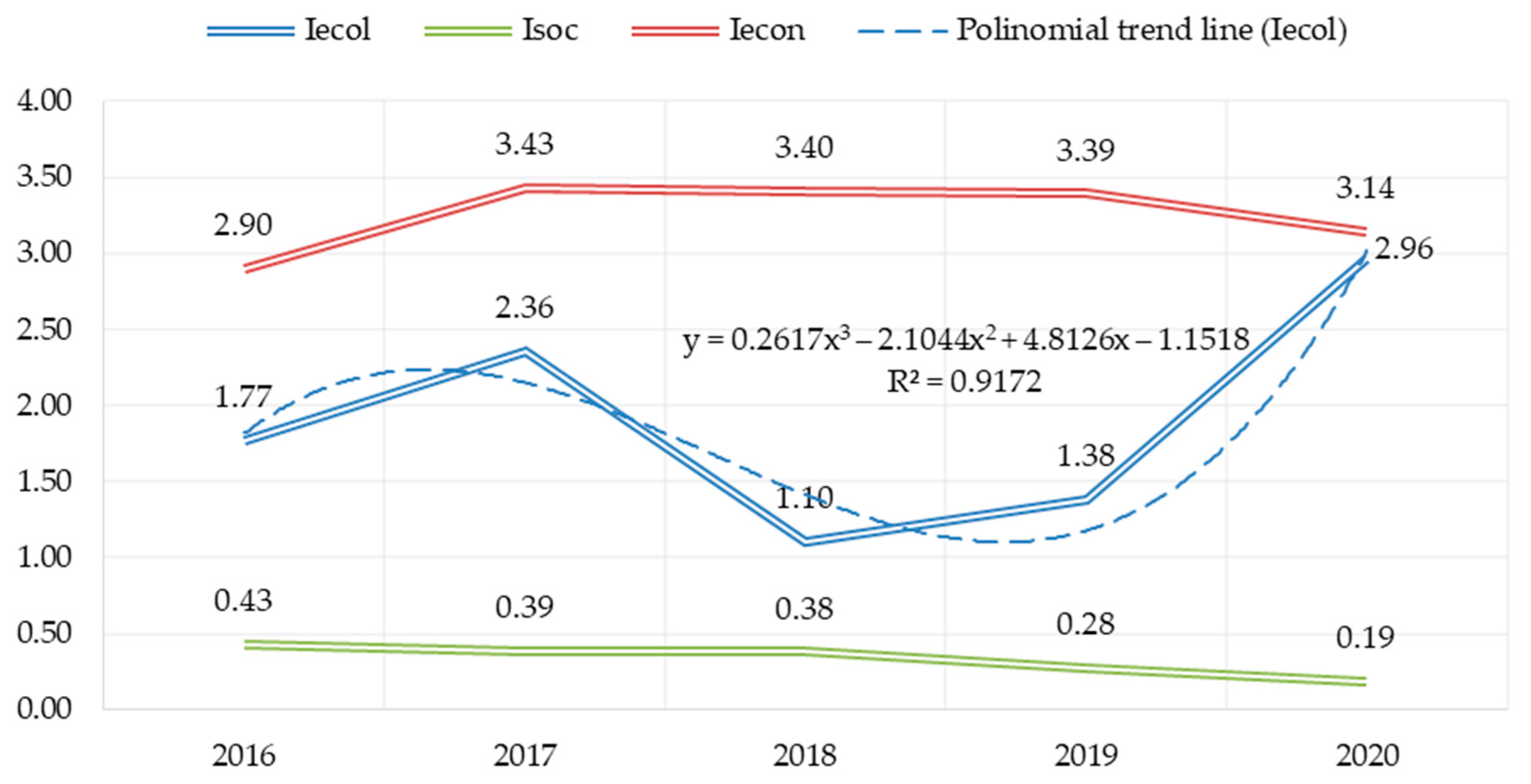

- the coronavirus pandemic of 2020 had an impact on the company’s activities (both economic and social indicators);

- the sustainable development of the enterprise is characterized by an imbalance, as evidenced by the multidirectional trends of changes in the factors Iecon, Isoc, Iecol;

- the investment flow management system of the enterprise requires optimization, restructuring of financing sources, which will help to ensure sustainable development and improve the overall picture of the enterprise development.

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

| Conditional Designation | Content |

| SDIE | integral indicator of sustainable development of the enterprise, coefficient |

| Iecon | the economic factor of sustainable development of the enterprise, coefficient |

| Isoc | social factor of sustainable development of the enterprise, coefficient |

| Iecol | environmental factor of sustainable development of the enterprise, coefficient |

| VRoE | returns on energy, rubles per rubles |

| VMP | material productivity, rubles per rubles |

| VRoS | return on sales, coefficient |

| VSP | social policy and charity expenses per 1 employee, million rubles per person |

| VRGW | rate of growth of tariff rates/wages, % |

| VSTR | average staff turnover rate, % |

| VREP | the volume of reduction of emissions of pollutants into the atmospheric air, thousand tons |

| VRWD | the volume of reduction of wastewater discharges in volume, million cubic meters |

| VIA | acquisition of fixed assets, million rubles |

| VLTF | attraction of long-term loans and borrowings, million rubles |

| VSTF | attraction of short-term loans and borrowings, million rubles |

References

- Ahmad, Munir, Irfan Khan, Muhammad Qaiser Shahzad Khan, Gul Jabeen, Hafiza Samra Jabeen, and Cem Işık. 2023. Households’ perception-based factors influencing biogas adoption: Innovation diffusion framework. Energy 263: 126155. [Google Scholar] [CrossRef]

- Ali, Shahid, Qingyou Yan, Asif Razzaq, Irfan Khan, and Muhammad Irfan. 2022. Modeling factors of biogas technology adoption: A roadmap towards environmental sustainability and green revolution. Environmental Science and Pollution Research 30: 11838–60. [Google Scholar] [CrossRef]

- Andriuškevičius, Karolis, Dalia Štreimikienė, and Irena Alebaitė. 2022. Convergence between Indicators for Measuring Sustainable Development and M&A Performance in the Energy Sector. Sustainability 14: 10360. [Google Scholar] [CrossRef]

- Awan, Ashar, Muhammad Sadiq, Syed Tauseef Hassan, Irfan Khan, and Noor Hashim Khan. 2022. Combined nonlinear effects of urbanization and economic growth on CO2 emissions in Malaysia. An application of QARDL and KRLS. Urban Climate 46: 101342. [Google Scholar] [CrossRef]

- Azam, Waseem, Irfan Khan, and Ali Syed Ahtsham. 2023. Alternative energy and natural resources in determining environmental sustainability: A look at the role of government final consumption expenditures in France. Environmental Science and Pollution Research 30: 1949–65. [Google Scholar] [CrossRef]

- Chen, Toly. 2017. Competitive and sustainable manufacturing in the age of globalization. Sustainability 9: 26. [Google Scholar] [CrossRef] [Green Version]

- Contini, Giuditta, and Margherita Peruzzini. 2022. Sustainability and Industry 4.0: Definition of a Set of Key Performance Indicators for Manufacturing Companies. Sustainability 14: 11004. [Google Scholar] [CrossRef]

- Dyrdonova, Alena N., and Tatiana S. Lin’kova. 2019. Principles of petrochemical cluster’ sustainability assessment based on its members’ energy efficiency performance. E3S Web of Conferences 124: 04013. [Google Scholar] [CrossRef]

- Esposito, Paolo, and Spiridione Lucio Dicorato. 2020. Sustainable Development, Governance and Performance Measurement in Public Private Partnerships (PPPs): A Methodological Proposal. Sustainability 12: 5696. [Google Scholar] [CrossRef]

- Gong, Qunxi, Min Chen, Xianli Zhao, and Zhigeng Ji. 2019. Sustainable Urban Development System Measurement Based on Dissipative Structure Theory, the Grey Entropy Method and Coupling Theory: A Case Study in Chengdu, China. Sustainability 11: 293. [Google Scholar] [CrossRef] [Green Version]

- Hassan, Azad, and Zeenat Kotval-K. 2019. A Framework for Measuring Urban Sustainability in an Emerging Region: The City of Duhok as a Case Study. Sustainability 11: 5402. [Google Scholar] [CrossRef] [Green Version]

- Holden, Erling, Kristin Linnerud, and David Banister. 2014. Sustainable development: Our Common Future revisited. Global Environmental Change 26: 130–39. [Google Scholar] [CrossRef] [Green Version]

- Hou, Peng, Mengting Zhou, Jiaqi Xu, and Yue Liu. 2021. Financialization, Government Subsidies, and Manufacturing R&D Investment: Evidence from Listed Companies in China. Sustainability 13: 12633. [Google Scholar] [CrossRef]

- Karnitis, Edvins, Janis Bicevskis, and Girts Karnitis. 2021. Measuring the Implementation of the Agenda 2030 Vision in Its Comprehensive Sense: Methodology and Tool. Energies 14: 856. [Google Scholar] [CrossRef]

- Khan, Irfan, Abdulrasheed Zakari, Vishal Dagar, and Sanjeet Singh. 2022. World energy trilemma and transformative energy developments as determinants of economic growth amid environmental sustainability. Energy Economics 108: 105884. [Google Scholar] [CrossRef]

- Koh, Lenny S. C., Jonathan Morris, Seyed M. Ebrahimi, and Raymond Obayi. 2016. Integrated Resource Efficiency: Measurement and Management. International Journal of Operations & Production Management 36: 1576–600. [Google Scholar] [CrossRef]

- Liczmańska-Kopcewicz, Katarzyna, Paula Pypłacz, and Agnieszka Wiśniewska. 2020. Resonance of Investments in Renewable Energy Sources in Industrial Enterprises in the Food Industry. Energies 13: 4285. [Google Scholar] [CrossRef]

- Linnerud, Kristin, Erling Holden, and Morten Simonsen. 2021. Closing the sustainable development gap: A global study of goal interactions. Sustainable Development 29: 738–53. [Google Scholar] [CrossRef]

- Liu, Haiying, Irfan Khan, Abdulrasheed Zakari, and Majed Alharthi. 2022a. Roles of trilemma in the world energy sector and transition towards sustainable energy: A study of economic growth and the environment. Energy Policy 170: 113238. [Google Scholar] [CrossRef]

- Liu, Haiying, Majed Alharthi, Ahmed Atil, Muhammad Wasif Zafar, and Irfan Khan. 2022b. A non-linear analysis of the impacts of natural resources and education on environmental quality: Green energy and its role in the future. Resources Policy 79: 102940. [Google Scholar] [CrossRef]

- Lubnina, Alsu A., Alexander N. Melnik, and Marina V. Smolyagina. 2016. On modelling of different sectors of economy in terms of sustainable development. International Business Management 10: 5592–95. [Google Scholar]

- Lyeonov, Serhiy, Tetyana Pimonenko, Yuriy Bilan, Dalia Štreimikienė, and Grzegorz Mentel. 2019. Assessment of Green Investments’ Impact on Sustainable Development: Linking Gross Domestic Product Per Capita, Greenhouse Gas Emissions and Renewable Energy. Energies 12: 3891. [Google Scholar] [CrossRef] [Green Version]

- Negulescu, Oriana Helena, Anca Draghici, and Gabriela Fistis. 2022. A Proposed Approach to Monitor and Control Sustainable Development Strategy Implementation. Sustainability 14: 11066. [Google Scholar] [CrossRef]

- Osipov, Vladimir S., Yuriy A. Krupnov, Galina N. Semenova, and Maria V. Tkacheva. 2022. Ecologically Responsible Entrepreneurship and Its Contribution to the Green Economy’s Sustainable Development: Financial Risk Management Prospects. Risks 10: 44. [Google Scholar] [CrossRef]

- Patalas-Maliszewska, Justyna, and Hanna Łosyk. 2020. An Approach to Assessing Sustainability in the Development of a Manufacturing Company. Sustainability 12: 8787. [Google Scholar] [CrossRef]

- Rahma, Hania, Akhmad Fauzi, Bambang Juanda, and Bambang Widjojanto. 2019. Development of a Composite Measure of Regional Sustainable Development in Indonesia. Sustainability 11: 5861. [Google Scholar] [CrossRef] [Green Version]

- Sachs, Jeffrey, Christian Kroll, Guillaume Lafortune, Grayson Fuller, and Finn Woelm. 2021. The Decade of Action for the Sustainable Development Goals: Sustainable Development Report 2021. Cambridge: Cambridge University Press. [Google Scholar]

- Salem, Muhammad, Naoki Tsurusaki, Prasanna Divigalpitiya, and Emad Kenawy. 2020. An Effective Framework for Monitoring and Measuring the Progress towards Sustainable Development in the Peri-Urban Areas of the Greater Cairo Region, Egypt. World 1: 1–19. [Google Scholar] [CrossRef]

- Samarina, Vera P., Tatiana P. Skufina, and Diana Yu Savon. 2021a. Comprehensive assessment of sustainable development of mining and metallurgical holdings: Problems and mechanisms of their resolution. Ugol 7: 20–24. [Google Scholar] [CrossRef]

- Samarina, Vera P., Tatiana P. Skufina, Diana Yu Savon, and Alexey I. Shinkevich. 2021b. Management of Externalities in the Context of Sustainable Development of the Russian Arctic Zone. Sustainability 13: 7749. [Google Scholar] [CrossRef]

- Schulte, Jesko, and Sophie Isaksson Hallstedt. 2018. Self-Assessment Method for Sustainability Implementation in Product Innovation. Sustainability 10: 4336. [Google Scholar] [CrossRef] [Green Version]

- Schulte, Jesko, Carolina Villamil, and Sophie I. Hallstedt. 2020. Strategic Sustainability Risk Management in Product Development Companies: Key Aspects and Conceptual Approach. Sustainability 12: 10531. [Google Scholar] [CrossRef]

- Shen, Yang, and Xiuwu Zhang. 2022. Study on the Impact of Environmental Tax on Industrial Green Transformation. International Journal of Environmental Research and Public Health 19: 16749. [Google Scholar] [CrossRef] [PubMed]

- Shinkevich, Alexey I. 2020. Sustainable development of territories in the zone of industrial facilities. IOP Conference Series: Materials Science and Engineering 890: 012190. [Google Scholar] [CrossRef]

- Shinkevich, Marina V., Alexey I. Shinkevich, Liudmila A. Ponkratova, Natalya V. Klimova, Guzel F. Yusupova, Irina V. Lushchik, and Tatiana A. Zhuravleva. 2015. Models and Technologies to Manage the Institutionalization of Sustainable Innovative Development of Meso-Systems. Mediterranean Journal of Social Sciences 6: 32–39. [Google Scholar] [CrossRef]

- Shinkevich, Alexey I., Farida F. Galimulina, Yulia S. Polozhentseva, Alla A. Yarlychenko, and Naira V. Barsegyan. 2021a. Computer Analysis of Energy and Resource Efficiency in the Context of Transformation of Petrochemical Supply Chains. International Journal of Energy Economics and Policy 11: 529–36. [Google Scholar] [CrossRef]

- Shinkevich, Alexey I., Irina G. Ershova, and Farida F. Galimulina. 2021b. Innovative Mesosystems Algorithm for Sustainable Development Priority Areas Identification in Industry Based on Decision Trees Construction. Mathematics 9: 3055. [Google Scholar] [CrossRef]

- Shinkevich, Aleksey I., Alsu R. Akhmetshina, and Ruslan R. Khalilov. 2022. Development of a Methodology for Forecasting the Sustainable Development of Industry in Russia Based on the Tools of Factor and Discriminant Analysis. Mathematics 10: 859. [Google Scholar] [CrossRef]

- Tauseef Hassan, Syed, Ping Wang, Irfan Khan, and Bangzhu Zhu. 2023. The impact of economic complexity, technology advancements, and nuclear energy consumption on the ecological footprint of the USA: Towards circular economy initiatives. Gondwana Research 113: 237–46. [Google Scholar] [CrossRef]

- The National Credit Ratings Website. n.d. Available online: https://ratings.ru/analytics/corps/investment-efficiency-240821/ (accessed on 21 December 2022).

- The Smart-lab Website. n.d. NKNH—Financial Reports, Annual Reports, Presentations. Available online: https://smart-lab.ru/q/NKNC/f/l/ (accessed on 21 December 2022).

- The Sustainability Monitoring Russia Website. n.d. Energy Transition Readiness Rating. Available online: https://monitoring-esg.com/ratings/energy-transition-rating/ (accessed on 21 December 2022).

- The World Bank Website. n.d. Available online: https://www.worldbank.org/en/home (accessed on 21 December 2022).

- Tobisova, Alica, Andrea Senova, Gabriela Izarikova, and Ivana Krutakova. 2022. Proposal of a Methodology for Assessing Financial Risks and Investment Development for Sustainability of Enterprises in Slovakia. Sustainability 14: 5068. [Google Scholar] [CrossRef]

- Tsai, Wen-Tien. 2010. Energy sustainability from analysis of sustainable development indicators: A case study in Taiwan. Renewable and Sustainable Energy Reviews 14: 2131–38. [Google Scholar] [CrossRef]

- Waas, Tom, Jean Hugé, Aviel Verbruggen, and Tarah Wright. 2011. Sustainable Development: A Bird’s Eye View. Sustainability 3: 1637–61. [Google Scholar] [CrossRef] [Green Version]

- Yang, Liu, Han Qin, Quanxin Gan, and Jiafu Su. 2020. Internal Control Quality, Enterprise Environmental Protection Investment and Finance Performance: An Empirical Study of China’s A-Share Heavy Pollution Industry. International Journal of Environmental Research and Public Health 17: 6082. [Google Scholar] [CrossRef] [PubMed]

- Zhuravlyov, Vladimir, Tatyana Khudyakova, Natalia Varkova, Sergei Aliukov, and Svetlana Shmidt. 2019. Improving the Strategic Management of Investment Activities of Industrial Enterprises as a Factor for Sustainable Development in a Crisis. Sustainability 11: 6667. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Method | 2016 | 2017 | 2018 | 2019 | 2020 | Growth Rate |

|---|---|---|---|---|---|---|

| Method 1 | 1.301 | 1.465 | 1.125 | 1.090 | 1.208 | −7.17% |

| Method 2 | 1.709 | 1.922 | 2.067 | 1.982 | 1.713 | 0.24% |

| Method 3 | 1.861 | 1.877 | 1.792 | 1.814 | 1.857 | −0.25% |

| Meтoд | The Volume of Reduction of Emissions of Pollutants into the Atmospheric Air, Thousand Tons | The Volume of Reduction of Wastewater Discharges in Volume, Million Cubic Meters |

|---|---|---|

| SDIE (1) | 0.174 | 0.737 |

| SDIE (2) | −0.781 | 0.082 |

| SDIE (3) | 0.54 | 0.608 |

| SDIE (1) | VIA | VLTF | VSTF | |

|---|---|---|---|---|

| SDIE (1) | 1 | |||

| VIA | −0.701 | 1 | ||

| VLTF | −0.825 | 0.845 | 1 | |

| VSTF | −0.566 | −0.053 | 0.007 | 1 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Galimulina, F.F.; Shinkevich, M.V.; Barsegyan, N.V. Development of the Financial Flow Model for the Sustainable Development of an Industrial Enterprise. J. Risk Financial Manag. 2023, 16, 128. https://doi.org/10.3390/jrfm16020128

Galimulina FF, Shinkevich MV, Barsegyan NV. Development of the Financial Flow Model for the Sustainable Development of an Industrial Enterprise. Journal of Risk and Financial Management. 2023; 16(2):128. https://doi.org/10.3390/jrfm16020128

Chicago/Turabian StyleGalimulina, Farida F., Marina V. Shinkevich, and Naira V. Barsegyan. 2023. "Development of the Financial Flow Model for the Sustainable Development of an Industrial Enterprise" Journal of Risk and Financial Management 16, no. 2: 128. https://doi.org/10.3390/jrfm16020128