Predicting Explicit and Valuing Tacit Synergies of High-Tech Based Transactions: Amazon.com’s Acquisition of Dubai-Based Souq.com

Abstract

:1. Introduction

2. Measuring Explicit Collaborative Synergy of Corporate Integrative Strategies

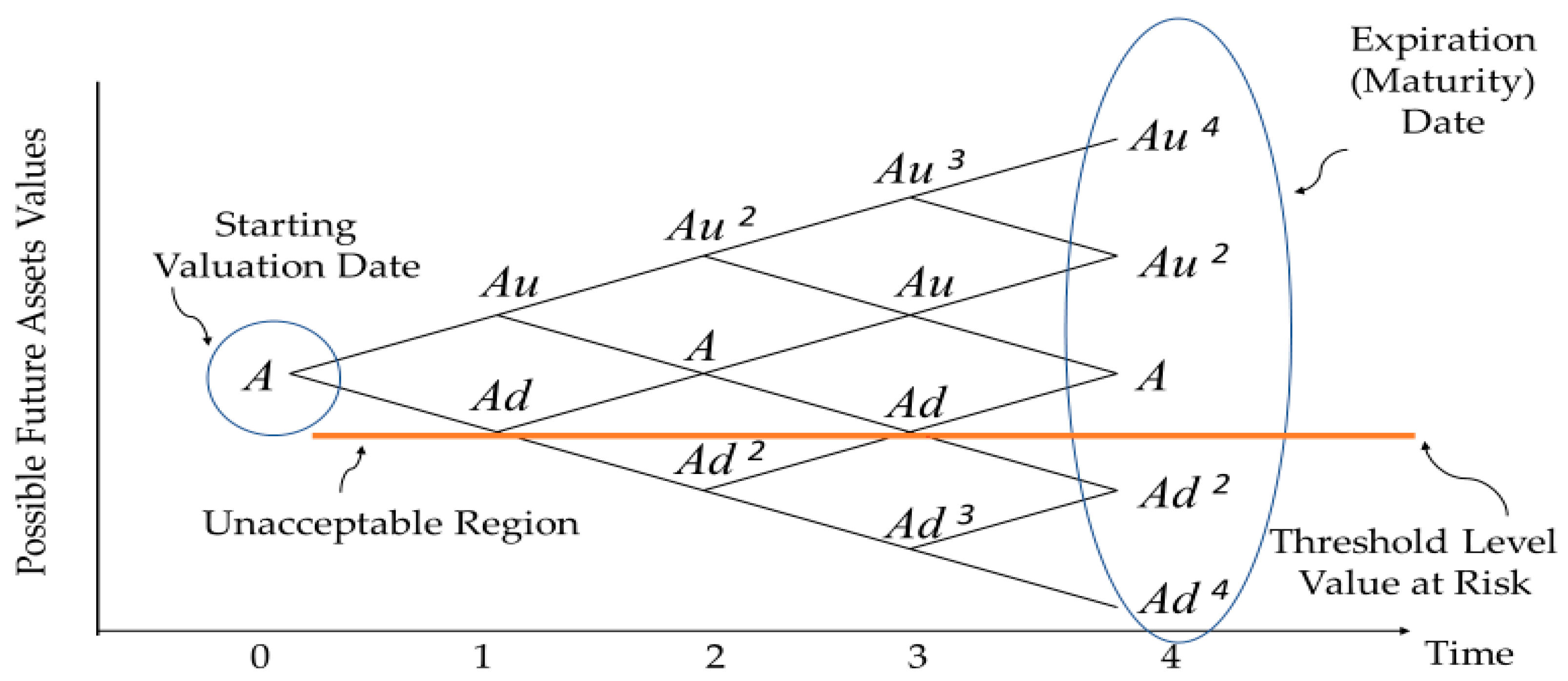

3. Valuing Tacit Collaborative Synergies

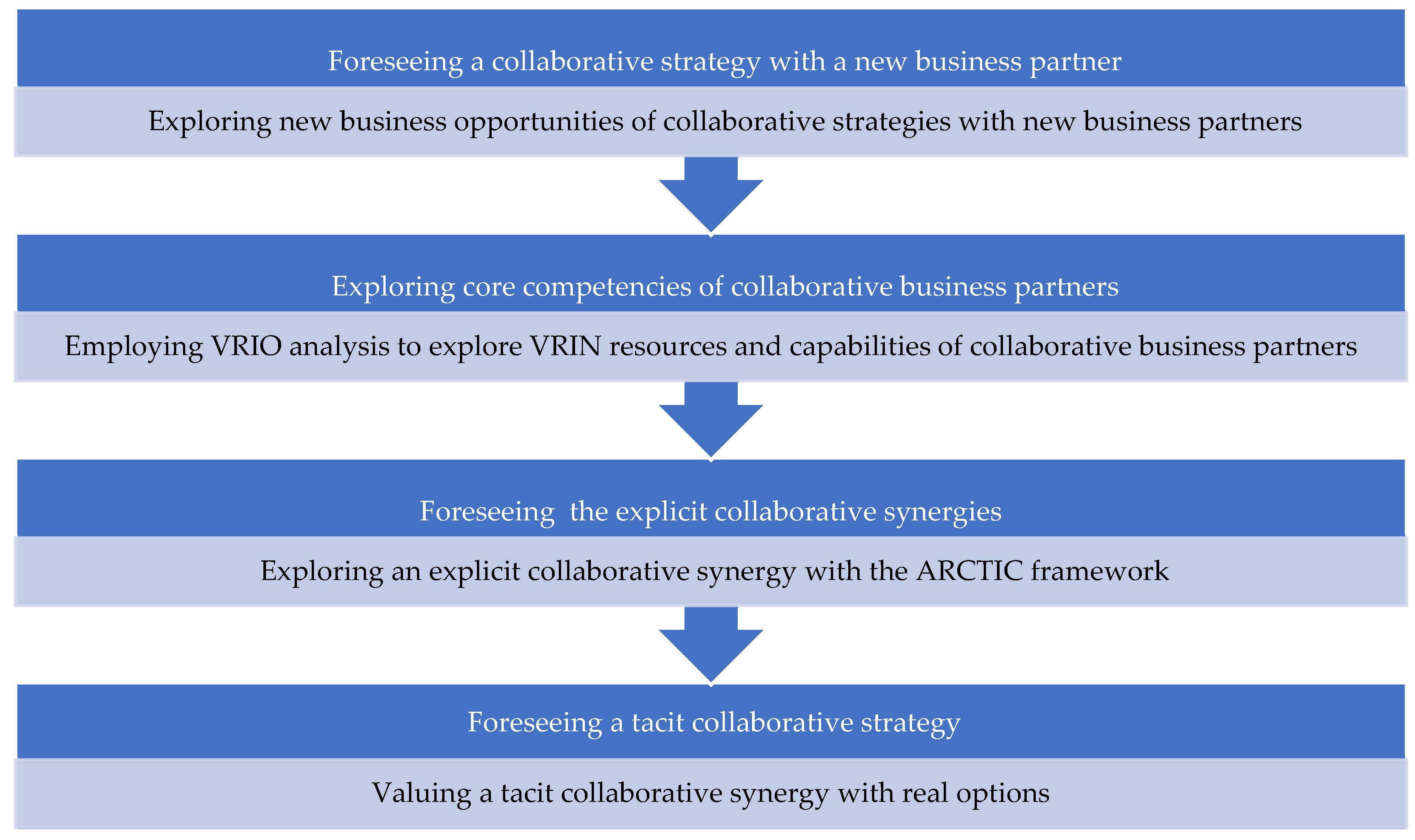

4. Method

5. Case Study Amazon.com Acquisition of Souq.com. Data Analysis and Interpretation of Results

5.1. Rationales behind Entering the Acquisition of Souq.com by Amazon.com and the Impact of Core Competencies on Explicit Collaborative Synergies

5.2. Predicting an Explicit Collaborative Synergy in Amazon.com’s Acquisition of Souq.com

“… With this deal, Amazon expected to extend its resources and infrastructure to Souq’s operation and Souq was to benefit in terms of both delivery capabilities and customer selection. At the time, Amazon would have access to the largest online customer base of the region thus enabling potential cross-selling synergies, it would also be able to leverage Souq.com infrastructure to store and deliver products”.

“… By becoming part of the Amazon family, we’ll be able to vastly expand our delivery capabilities and customer selection much faster, as well as continue Amazon’s great track record of empowering sellers”.

“… We are working to quickly integrate Souq.com and Amazon capabilities, in terms of both customer experience and fulfillment, to provide an ever-improving shopping experience for customers in the Middle East”.

“… It is an exhilarating time for the e-commerce industry in the region. Integration of Amazon’s technology and global resources with our local expertise will help us to offer a great service to our loyal customers”.

“… Amazon is a great fit for us. We have a lot of common values, and it is all about innovation, technology, and the type of customer experience and thinking that Amazon has”.

5.3. Valuing a Tacit Collaborative Synergy of Amazon.com’s Acquisition of Souq.com with Binominal Option Pricing Model

“Today marks a proud day for Souq and Amazon, a day that we have been working towards since the two companies came together in 2017. Amazon. ae brings together Souq’s local know-how and Amazon’s global expertise, something we believe will be of significant benefit to UAE customers”.

6. Findings and Discussion

7. Conclusions, Limitations, and Future Work

Funding

Data Availability Statement

Conflicts of Interest

References

- Amazon. 2019. Souq Becomes Amazon.ae in the UAE. Press Center. Available online: https://press.aboutamazon.com/2019/5/souq-becomes-amazon-ae-in-the-uae (accessed on 22 December 2022).

- Amram, Martha, and Nalin Kulatilaka. 1999. Real Options: Managing Strategic Investment in an Uncertain World, 1st ed. Boston: Harvard Business School Press. 246p. [Google Scholar]

- Banerjee, Arindam. 2021. Amazon’s Acquisition of Souq.com: Synergies in the GCC Region. Journal of International Business Education 16: 1–8. [Google Scholar]

- Barney, Jay B. 1996. Gaining and Sustaining Competitive Advantage. Boston: Addison-Wesley. [Google Scholar]

- Barney, Jay B., and William S. Hesterly. 2018. Strategic Management and Competitive Advantage: Concepts and Cases, 6th ed. Global Edition. London: Pearson. [Google Scholar]

- Bower, Joseph L. 2001. Not all M&As are alike—And that matters. Harvard Business Review 79: 92–101. [Google Scholar] [PubMed]

- BSIC. 2017. Bocconi Students’ Investment Club. Amazon of Arabia: Jeff Bezos’ Giant Buys Souq in a Move to Enter the Middle East Market. Available online: https://bsic.it/amazon-arabia-jeff-bezos-giant-buys-souq-move-enter-middle-east-market/ (accessed on 17 December 2022).

- Chi, Tailan, Jing Li, Lenos G. Trigeorgis, and Andrianos E. Tsekrekos. 2019. Real options theory in international business. Journal of International Business Studies 50: 525–53. [Google Scholar] [CrossRef]

- Čirjevskis, Andrejs. 2021. Exploring Critical Success Factors of Competence-Based Synergy in Strategic Alliances: The Renault–Nissan–Mitsubishi Strategic Alliance. Journal of Risk and Financial Management 14: 385. [Google Scholar] [CrossRef]

- Čirjevskis, Andrejs. 2023a. Measuring dynamic capabilities-based synergies using real options in M&A deals. International Journal of Applied Management Science, 1–13, in press. [Google Scholar]

- Čirjevskis, Andrejs. 2023b. Managing competence-based synergy in acquisition processes: Empirical evidence from the ICT and global cosmetic industries. Knowledge Management Research & Practice 21: 41–50. [Google Scholar]

- Dunis, Christian L., and Til Klein. 2005. Analyzing mergers and acquisitions in European financial services: An application of real options. European Journal of Finance 11: 339–55. [Google Scholar] [CrossRef]

- Eisenhardt, Kathleen M., and Melissa E. Graebner. 2007. Theory building from cases: Opportunities and challenges. Academy of Management Journal 50: 25–32. [Google Scholar] [CrossRef] [Green Version]

- Fahy, Michael. 2017. Amazon Completes Souq.com Deal. NBusiness. July 3. Available online: https://www.thenationalnews.com/business/amazon-completes-souq-com-deal-1.91570 (accessed on 17 December 2022).

- Fergnani, Alessandro. 2022. Corporate foresight: A new frontier for strategy and management. Academy of Management Perspectives 36: 820–44. [Google Scholar] [CrossRef]

- Fiss, Peer C. 2009. Case studies and the configurational analysis of organizational phenomena. In The SAGE Handbook of Case-Based Methods. Edited by David Byrne and Charles C. Ragin. London and Thousand Oaks: Sage, pp. 424–40. [Google Scholar]

- Ghemawat, Pankaj. 2007. Managing differences: The central challenge of global strategy. Harvard Business Review 85: 58–68. [Google Scholar] [PubMed]

- Hannah, Douglas P., Ron Tidhar, and Kathleen M. Eisenhardt. 2021. Analytic models in strategy, organizations, and management research: A guide for consumers. Strategic Management Journal 42: 329–60. [Google Scholar] [CrossRef]

- Hao, Bin, Jiangfeng Ye, Yanan Feng, and Ziming Cai. 2020. Explicit and tacit synergies between alliance firms and radical innovation: The moderating roles of interfirm technological diversity and environmental technological dynamism. R&D Management 50: 432–46. [Google Scholar]

- King, Major David R., Dan R. Dalton, Catherine M. Daily, and Jeffrey G. Covin. 2004. Meta-analyses of post-acquisition performance: Indications of unidentified moderators. Strategic Management Journal 25: 187–200. [Google Scholar] [CrossRef] [Green Version]

- Kogut, Bruce. 1985. Designing global strategies: Comparative and competitive value-added chains. Sloan Management Review 26: 15–28. [Google Scholar]

- Kogut, Bruce. 1991. Joint ventures and the option to expand and acquire. Management Science 37: 19–33. [Google Scholar] [CrossRef]

- Kyläheiko, Kalevi, Jaana Sandström, and Virpi Virkkunen. 2002. Dynamic capability view in terms of real options. International Journal of Production Economics 80: 65–83. [Google Scholar] [CrossRef]

- Lambrecht, Bart M. 2017. Real Option in finance. Journal of Banking and Finance 81: 166–71. [Google Scholar] [CrossRef]

- MAGNiTT. 2017. A Different Story from the Middle East: Entrepreneurs Building an Arab Tech Economy. Available online: https://magnitt.com/news/different-story-middle-east-entrepreneurs-building-arab-tech-economy-20010 (accessed on 12 January 2023).

- Macrotrend. 2022. Amazon EBITDA 2010–2022. Available online: https://www.macrotrends.net/stocks/charts/AMZN/amazon/ebitda (accessed on 22 December 2022).

- Mun, Johnatan. 2016. Real Options Analysis: Tools and Techniques for Valuing Strategic Investments and Decisions with Integrated Risk Management and Advanced Quantitative Decision Analytics, 3rd ed. Hoboken: Wiley, John & Sons, Inc. 695p. [Google Scholar]

- Prahalad, Coimbatore K., and Gary Hamel. 1990. The Core Competence of the Corporation. Harvard Business Review 68: 79–91. [Google Scholar]

- Reuter. 2017. Amazon Clinches Deal to Buy Middle East Online Retailer Souq.com. Available online: https://www.reuters.com/article/souqcom-ma-amazoncom-idUSL5N1H51ZB (accessed on 18 December 2022).

- Ridder, Hans-Gerd. 2016. Case Study Research. Approaches, Methods, Contribution to Theory. Sozialwissenschaftliche Forschungsmethoden. Munchen and Mering: Rainer Hampp Verlag, vol. 12. [Google Scholar]

- Sayegh, Hadeel Al, and Alexander Cornwell. 2017. Amazon Clinches Deal to Buy Middle East Online Retailer Souq.com. Reuter. Available online: https://www.reuters.com/article/us-souq-com-m-a-amazon-com-idUSKBN16Z0Q1 (accessed on 27 November 2022).

- Schweizer, Lars, Le Wang, Eva Koscher, and Bjorn Michaelis. 2022. Experiential learning, M&A performance, and post-acquisition integration strategy: A meta-analysis. Long Range Planning, in press. [Google Scholar]

- Strategic Management Society. 2020. Strategy Practice IG. What Do We Do? Available online: https://www.strategicmanagement.net/ig-strategy-practice/overview (accessed on 27 March 2020).

- Teece, David J., Garry Pisano, and Amy Shuen. 1997. Dynamic capabilities and strategic management. Strategic Management Journal 18: 509–33. [Google Scholar] [CrossRef]

- Teoh, Chin Chuen, and Gerald B. Sheblè. 2007. Lattice Method of Real Options Analysis—Solving the Curse of Dimensionality and Strategic Planning. Available online: https://www.researchgate.net/publication/4341635_Lattice_Method_of_Real_Option_Analysis_-_Solving_the_Curse_of_Dimensionality_and_Strategic_Planning (accessed on 8 February 2023).

- Tong, Tony W., and Jeffrey J. Reuer. 2007. Real Options in Strategic Management. Advances in Strategic Management 24: 3–24. [Google Scholar]

- VLab. 2022. Amazon.com Inc. GARCH Volatility Analysis. Available online: https://vlab.stern.nyu.edu/volatility/VOL.AMZN%3AUS-R.GARCH (accessed on 21 December 2022).

- YChart. 2022a. Amazon.com Inc. (AMZN). Available online: https://ycharts.com/companies/AMZN/market_cap (accessed on 21 December 2022).

- YChart. 2022b. Amazon.com Inc. (AMZN). Available online: https://ycharts.com/companies/AMZN/valuation (accessed on 21 December 2022).

- YChart. 2022c. Amazon.com Inc. (AMZN). Available online: https://ycharts.com/indicators/10_year_treasury_rate (accessed on 21 December 2022).

- Yin, Robert K. 2018. Case Study Research and Applications. Design and Methods, 6th ed. London and Thousand Oaks: SAGE Publications, Inc. 352p. [Google Scholar]

{kind=link}

{kind=link}

| Financial Options Variables | Real Option Variables | Sources of Data |

|---|---|---|

| Share price | The cumulated market value of collaborative business partners before the announced deal terms, excluding the week of an announcement (four-week average) | https://ycharts.com/ (accessed on 12 February 2023). https://www.reuters.com/ (accessed on 12 February 2023). https://www.google.com/finance (accessed on 12 February 2023). |

| Strike price | The hypothetical future market value of the separated entities forecast by the DCF or EV-based multiples | www.helgilibrary.com (accessed on 12 February 2023). www.marcotrends.net (accessed on 12 February 2023). Own calculation |

| Standard deviation | The annualized standard deviation of stock within one week after the announcement | https://vlab.stern.nyu.edu/docs/volatility/GARCH (accessed on 12 February 2023). Own calculation |

| Risk-free rate | Domestic three-month rate to the leading collaborated partner | https://ycharts.com (accessed on 12 February 2023). https://www.statista.com/ (accessed on 12 February 2023). |

| Time to maturity | One year or by the expectation of management on getting collaborative synergy | The synergy life cycle. |

| The Core Competencies of Souq.com and Amazon.com | (A?) | (R?) | (C?) | (T?) | (I?) | (C?) |

|---|---|---|---|---|---|---|

| “Souq.com has the largest online retailer and marketplace platform in the Arab world, offering more than 400.000 products across 31 categories” (BSIC 2017) | Yes | Yes | Yes | Yes | Yes | Yes |

| “Souq.com presents in several markets of the region including Egypt, Saudi Arabia, Kuwait, Qatar, and Oman”. (BSIC 2017) | Yes | Yes | Yes | Yes | Yes | Yes |

| “Souq.com develops a logistic infrastructure by creating its delivery system (partnering with local logistic companies)” (BSIC 2017) | Yes | Yes | Yes | Yes | Yes | Yes |

| “Souq creates a prepaid card purchasable in brick-and-mortar stores, as well as developing its payment gateway, Payfort” (BSIC 2017) | Yes | Yes | Yes | Yes | Yes | Yes |

| “Amazon is the world’s largest online shopping retailer, operating in 189 countries and employing more than 341.000 people across 5 continents” (BSIC 2017) | Yes | Yes | Yes | Yes | Yes | Yes |

| “Amazon.com delivers innovation across its multiple businesses, ranging from drone delivery systems to the manufacturing of electronic devices” (BSIC 2017) | Yes | Yes | Yes | Yes | Yes | Yes |

| “Amazon.com has a continuous focus on external growth, running more than 50 acquisitions in the last ten years” (BSIC 2017) | Yes | Yes | Yes | Yes | Yes | Yes |

| Financial Call Options | Option Variables | Real Options Data |

|---|---|---|

| Stock price (in USD billion) | S | 409.57 |

| The strike price (in USD billion) | K | 446.71 |

| Time to expiration (in number of years) | T | 2.0 |

| The standard deviation of stock returns within one week before the acquisition announcement | σ | 23.0% |

| Risk-free rate | rf | 2.42% |

| 0 | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| 847.62 | |||||

| 732.87 | |||||

| 633.65 | 633.65 | ||||

| 547.87 | 547.87 | ||||

| 473.70 | 473.70 | 473.70 | |||

| 409.57 | 409.57 | 409.57 | |||

| 354.12 | 354.12 | 354.12 | |||

| 306.18 | 306.18 | ||||

| 264.73 | 264.73 | ||||

| 228.89 | |||||

| 197.90 |

| Parameters of the binominal tree | Equations | Numbers |

| Time increment (years) | 0.40 | |

| Up factor (u) | 1.157 | |

| Down factor (d) | 0.865 | |

| Risk-neutral probability (p) | 0.497 |

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| 400.91 | |||||

| 290.46 | |||||

| 195.50 | 186.94 | ||||

| 125.39 | 105.46 | ||||

| 77.69 | 58.53 | 26.99 | |||

| 46.90 | 32.07 | 13.28 | |||

| 17.39 € | 6.54 | 0.00 | |||

| 3.22 | 0.00 | ||||

| 0.00 | 0.00 | ||||

| 0.00 | |||||

| 0.00 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Čirjevskis, A. Predicting Explicit and Valuing Tacit Synergies of High-Tech Based Transactions: Amazon.com’s Acquisition of Dubai-Based Souq.com. J. Risk Financial Manag. 2023, 16, 123. https://doi.org/10.3390/jrfm16020123

Čirjevskis A. Predicting Explicit and Valuing Tacit Synergies of High-Tech Based Transactions: Amazon.com’s Acquisition of Dubai-Based Souq.com. Journal of Risk and Financial Management. 2023; 16(2):123. https://doi.org/10.3390/jrfm16020123

Chicago/Turabian StyleČirjevskis, Andrejs. 2023. "Predicting Explicit and Valuing Tacit Synergies of High-Tech Based Transactions: Amazon.com’s Acquisition of Dubai-Based Souq.com" Journal of Risk and Financial Management 16, no. 2: 123. https://doi.org/10.3390/jrfm16020123