1. Introduction

Within the area of value-based management (VBM), scholars and practitioners have developed several financial metrics that supposedly predict stock returns. Managers need such metrics in order to set targets that are in line with shareholder interests. Common accounting metrics (e.g., earnings) fall short of this goal, partly because they ignore the different risks of different investments (

Koller et al. 2015;

Stewart 1991). Empirical evidence documents the difficulty of finding internally controllable metrics that approximate stock returns and are robust against noise. Large consulting firms have gone to “

Metric Wars” with each other over which metric is the best proxy for stock returns (

Myers 1996). Results remained mixed even when the debate spread into academic journals. The value relevance of value-based measures remains of interest in current research (

Brück et al. 2022;

Liao et al. 2021;

Mavropulo et al. 2021). In their systematic literature review on this topic,

Toft and Lueg (

2015b) show that some authors provide evidence that sophisticated metrics based on residual income outperform classic accounting metrics in predicting stock returns, while at the same time, a considerable amount of studies negate the superiority of these metrics, especially the most popular one,

economic value added (EVA), developed by the consulting firm Stern Stewart. Despite these ambiguous results, managers need a sense of direction as to which financial goals they should target. This debate remains relevant since alternative multiple-goal performance measurement systems have not proven to be a strong alternative to VBM.

KPMG and Velthuis (

2004) attempted to advance the debate by fundamentally rethinking the approach to residual value. They argue that extant residual-income-based performance metrics such as EVA use an exaggerated capital charge when evaluating managers ex post for their efforts, and that a firm has created shareholder value if its investments have realized a return higher than its risk-free cost of capital. The authors argue that the assumptions of net present value are being violated if realized (i.e., risk-free) profits are ex post benchmarked against expected (i.e., ex ante, risky) profits. Performance management systems built on this fallacy would motivate managers to pick investments with low-variance outcomes, but not those that are expected to create the highest stock returns. As a result, the authors introduce the metric

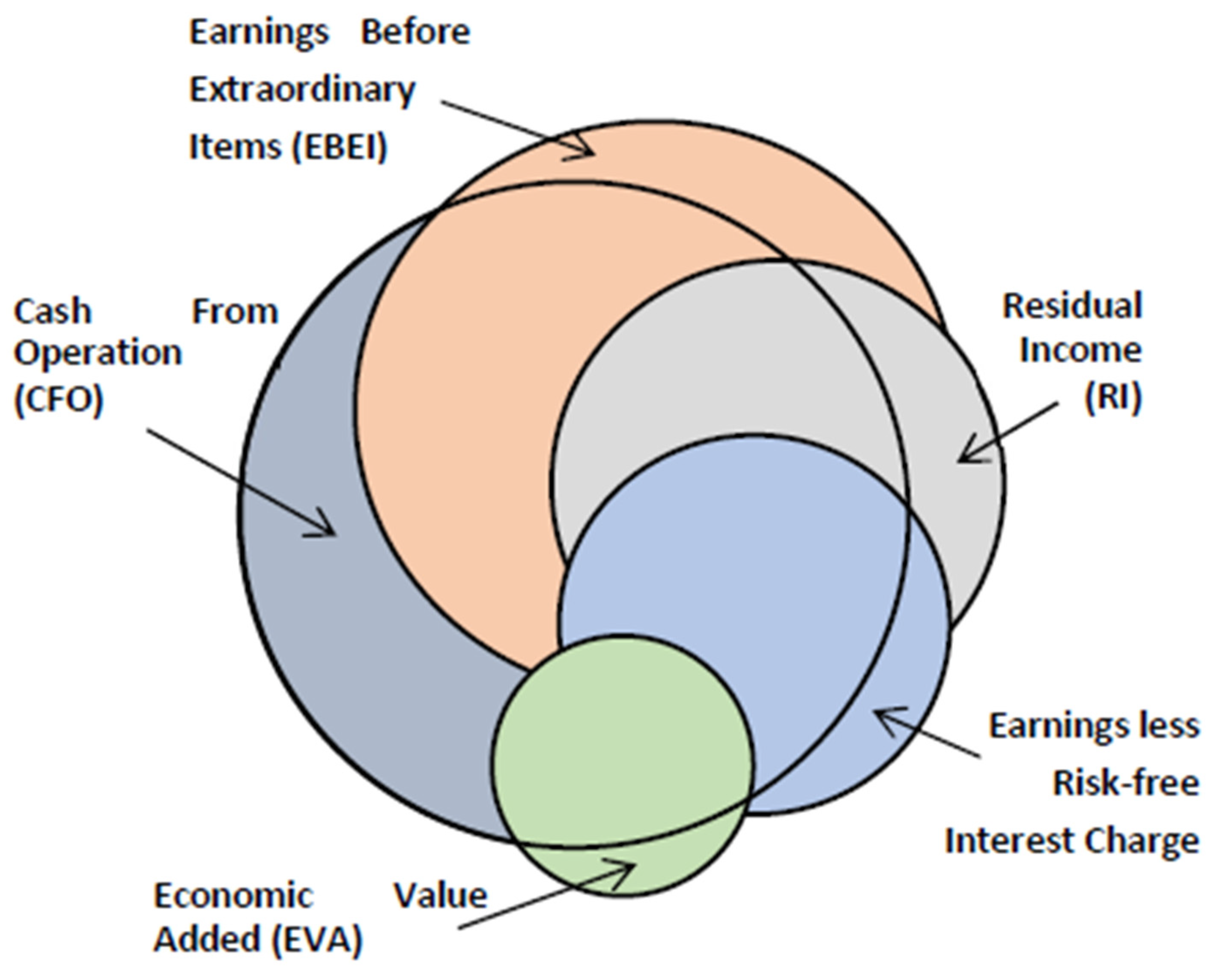

earnings less risk-free interest charge (ERIC). ERIC benchmarks managerial performance in terms of

realized (risk-free) profits against the investment’s risk-free cost of capital.

As yet, no study has provided empirical evidence to show if ERIC constitutes a superior metric of shareholder value creation (

Velthuis and Wesner 2005). Such an investigation is warranted because KPMG, a Big 4 audit firm, is an influential source of management practices. In addition, a simultaneous check regarding the performance of EVA may settle conflicting results and confirm the ongoing validity of previous findings (e.g., on EVA by

Biddle et al. 1997). Hence, it is the goal of this study to

evaluate the relative and incremental information content of ERIC in predicting stock returns. Relative information content examines if ERIC has a greater association with stock returns than other proxies. For this, we compare ERIC to previously investigated stock return proxies, i.e., cash flow from operations (CFO), earnings before extraordinary items (EBEI), residual income (RI), and EVA. Incremental information content assesses whether any one component of ERIC adds incremental information content beyond that which is contained in its other components. The components of ERIC are CFO, accrual, extraordinary items (ExtraOrd), after-tax interest expenses (ATInt), certainty equivalent adjustments (CEQAdj), and capital charge (CapChg).

To ensure comparability with previous studies, we follow the established methodology in this field (

Biddle et al. 1997;

Easton and Harris 1991). Our dataset contains information on 214 S&P500 companies from annual reports and the U.S. stock market over a 10-year period ranging from 2003 to 2012. We present two major findings. First, we find that accounting-based performance metrics exhibit the strongest association with stock returns in the short and long term. Residual income prevails in the intermediate term. Second, as a novelty in this field, we can document that ERIC clearly outperforms EVA in predicting stock returns. This might spark new debates on controversial VBM metrics such as EVA. As to incremental information content, five of ERIC’s six components add incremental information content in the short term (the exception being extraordinary items). Overall, we find that ERIC is not a predictor of transient and myopic 1-year stock returns. Rather, we provide evidence that ERIC is a valid predictor of long-term stock returns. On this basis, we debate how using ERIC can benefit practicing managers in target setting and managing firm value.

The remainder of the study is organized as follows:

Section 2 describes the components of ERIC, the hypothesis, and the statistical tests.

Section 3 describes the data, the variables, and the descriptive statistics.

Section 4 and

Section 5 provide the analyses and sensitivity analyses, respectively. Finally,

Section 6 discusses the results, and

Section 7 sums up the study.

3. Sample Selection, Variable Definitions, and Descriptive Statistics

In order to ensure comparability with previous studies in this field, we align our methodology as much as possible with Biddle et al.’s (1997) seminal study. The data used in this study refer to the firms of the Standard & Poor’s 500 Index, and are collected from Compustat, the Center for Research in Security Prices (CRSP), and Bloomberg. We cover a 10-year period beginning on 1 January 2003 and ending on 31 December 2012. Some of our calculated metrics require information for the fiscal year 2002, which gives a total of 11 years. A total of 269 firms were removed, either because their fiscal year ended during the year or due to data unavailability. A total of 17 firms were removed due to extreme outliers that would substantially distort the linear equation for the majority of the sample (

Hair et al. 2018). For the same reason, 103 firm-year observations were winsorized within four standard deviations (

Wooldridge 2017). That is, variables are assigned a value equal to the median minus (plus) four standard deviations. The final data set encompasses 214 firms for the period 2002–2012.

3.1. Dependent Variable

MktAdjRets is the dependent variable. It comprises the 12-month compound stock return of a firm (January–December), less a 12-month compound return on the S&P500 stock market index (April–March). The comparison to the market return detects the over-/underperformance of a firm. We subtract a 3-month-lagged stock return since market participants need some time to incorporate all information contained in the annual report into stock prices (

K. Lueg et al. 2019;

Lueg 2022;

Lueg and Pesheva 2021;

Muheki et al. 2014). Data are obtained from CRSP.

3.2. Independent Variables and Descriptive Data: Relative Information Content Tests

This study deals with the same independent variables as

Biddle et al. (

1997), but with one additional variable, ERIC.

CFO: Cash flow from operation, acquired through Compustat data item D308 and item name “Operating Activities Net Cash Flow”. The definition from Compustat is “change in cash from all items classified in the Operating Activities section on a Statement of Cash flow”.

EBEI: Earnings before extraordinary items, obtained from Compustat data item D18 and item name “Income before Extraordinary Items”.

RI: Calculated using EBEI plus ATInt less WACC, obtained from Bloomberg using the mnemonic “WACC” multiplied by the CE using

KPMG and Velthuis’ (

2004) definition.

EVA:

Economic value added is calculated using the same information as RI, but with adjustments defined by

Young (

1999) and

Ray (

2012).

ERIC:

Earnings less risk-free interest charge is calculated using the certainty equivalents of PAT (

) and risk-free interest charge of capital (

), calculated as per

KPMG and Velthuis (

2004). See

Section 3.2 for a more detailed data description.

All independent variables are deflated by the MVE three months after the beginning of the fiscal year (MVE

t−1) to reduce heteroscedasticity.

Table 1 shows the pooled descriptive data. Like

Biddle et al. (

1997), this study of the descriptive statistics finds the lowest standard deviation for EBEI and higher values for the mean and median for CFO.

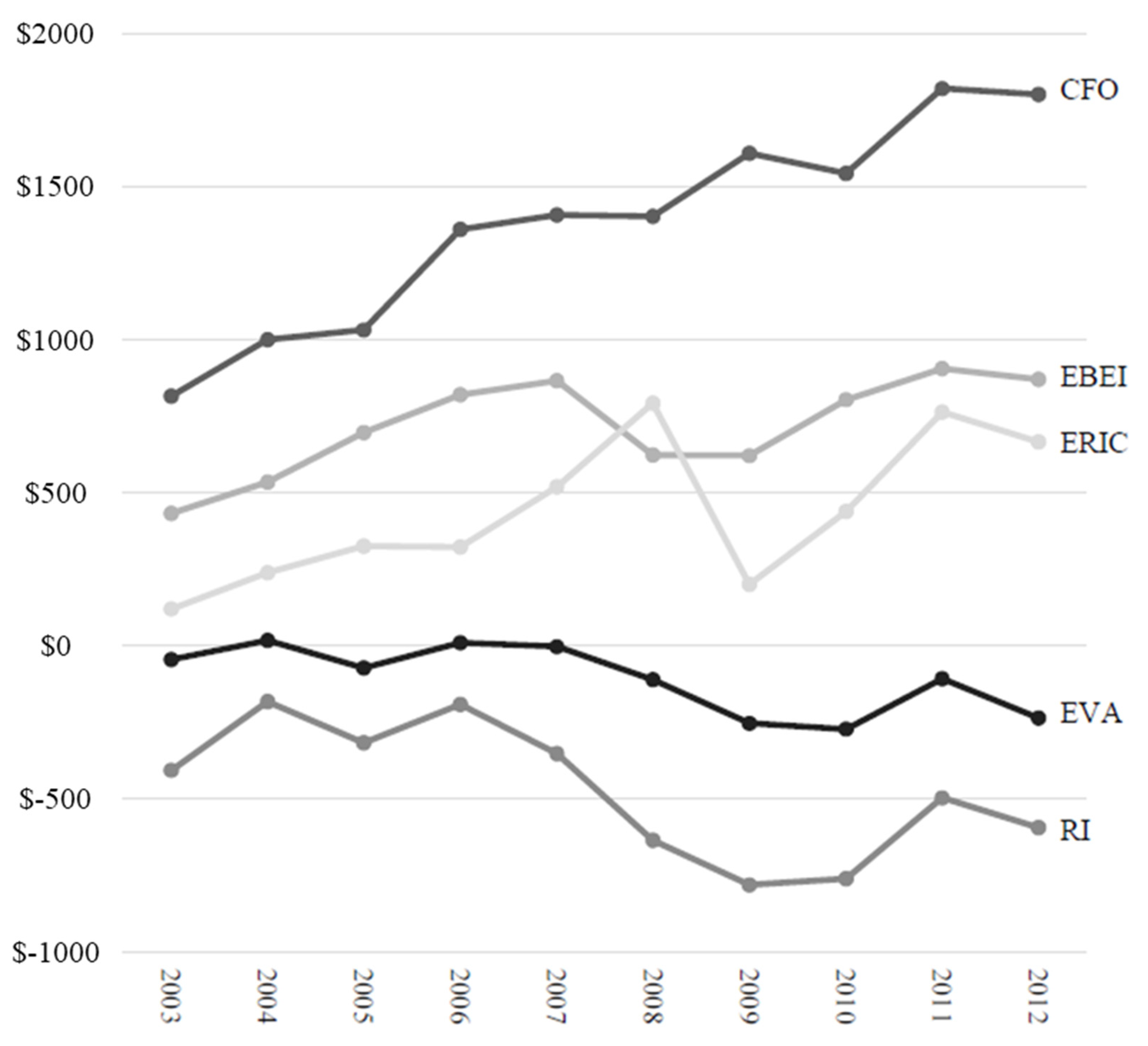

Figure 1 illustrates the non-deflated median values from each performance metric. EVA is negative for 8 out of 10 years, and RI is negative for 5 out of 10 years. CFO, EBEI, and ERIC are positive every year. The negative values of EVA and RI could indicate the difficulties of earning above the capital costs in a competitive market (

Chen and Dodd 2001). It could likewise indicate the use of overly high levels of cost of capital, making it difficult for companies to create shareholder value, as claimed by

KPMG and Velthuis (

2004). To investigate the level of the performance metrics,

Bacidore et al. (

1997) argue that a performance metric must have a natural level, which must be zero, meaning that if a particular performance metric is positive, then one should expect a positive reaction in the stock price, and the opposite if negative. CFO has the same sign as stock returns in 1186 of 2140 firm years (55.4%), which is higher than EBEI, ERIC, EVA, and RI with 55.3%, 52.9%, 51.6% and 51.4%, respectively. This analysis does not take into account the level above or below the performance metric and stock returns, respectively, but only if the sign of the performance metric is the same as the stock return, which could indicate that performance metrics have a natural level for shareholder value creation.

Unlike

Biddle et al. (

1997), who found EBEI to be most correlated with MktAdjRets, but consistent with

Clinton and Chen (

1998), this study indicates that CFO is most correlated with MktAdjRets; CFO is followed by RI, ERIC, EVA, and EBEI. RI, ERIC, and EVA are surprisingly negatively correlated with MktAdjRets; this is also consistent with

Clinton and Chen (

1998), who found EVA to be negatively correlated with stock returns and RI to be insignificant. According to

Clinton and Chen (

1998), the reason might be that the market is not as efficient as assumed, or the cost of capital information might not be incorporated into the stock prices. RI seems to be highly correlated with EBEI, EVA, and ERIC, but EBEI is also highly correlated with ERIC.

3.3. Independent Variables and Descriptive Data: Incremental Information Content Tests

ERIC is composed of five components: CFO (defined above), accrual, ATInt, ExtraOrd, CEQAdj, and CapChg.

Accrual: Like

Biddle et al. (

1997), accrual is calculated as

. It is expected to be negative due to non-cash items, which is the case according to panel B of

Table 1.

ATInt: After-tax interest expenses are obtained from Bloomberg.

ExtraOrd: Extraordinary Items are included to make ERIC match more with existing theory.

CEQAdj: Certainty equivalent adjustment is an adjustment to earnings before interest after taxes (EBIAT). CEQAdj is calculated using the Capital Asset Pricing Model (CAPM) and the risk-free interest charge.

CapChg: Capital charge is calculated using the definition of CE by

Pfeiffer and Velthuis (

2009) and the risk-free interest rate used in the calculation of CEQAdj.

Like

Biddle et al. (

1997), panel B in

Table 1 shows that the accrual median and mean are negative, meaning that, on average, CFO is larger than EBEI, and that the firm in the income statement is burdened by non-cash items such as depreciation, amortization, change in non-cash current assets and current liabilities, and so forth. Accrual and CFO are highly negatively correlated, consistent with

Biddle et al. (

1997). CapChg is only statistically significantly correlated at a 0.05 level with MktAdjRets, which is inconsistent with the theoretical argument of the superiority of performance metrics including CapChg over those excluding CapChg. All other components are mutually statistically significant at a level of 0.01. The ERIC-specific components ExtraOrd and CEQAdj are not statistically significant with MrkAdjRets (panel B in

Table 1). All other components are correlated at a level of 0.01 except CapChg and CEQAdj, which are correlated at a level of 0.05. CEQAdj and CapChg are not statistically significantly correlated with ExtraOrd.

5. Sensitivity Analyses and Extensions

We test the sensitivity of the results in

Table 2 and

Table 3. This section tests the same performance metrics in several different ways by using four different tests: partitioning of annual observations into five non-overlapping two-year periods (

Section 5.1); adopters of EVA/ERIC-like metrics (

Section 5.2); long-term association with stock returns (five-year) (

Section 5.3); and changing returns from contemporaneous (one-year) to contemporaneous plus one-year ahead (two-year) returns (

Section 5.4).

5.1. Differences across Subperiods

This section divides the dataset into five two-year subperiods from 2003 to 2004, 2005 to 2006, 2007 to 2008, 2009 to 2010, and 2011 to 2012 (results are not separately tabulated but summarized later in Table 7). In the period from 2003 to 2004, CFO had the highest R2 (6.3%). From 2005 to 2006, RI (14.9%) was most associated with MktAdjRets. From 2007 to 2008, EBEI was the strongest predictor of stock returns (12.4%). During the period of the financial crisis from 2009 to 2010, ERIC was most associated with MktAdjRets and explained 11.9% of the annual returns. In the period from 2011 to 2012, EBEI again had the highest R2 (16.2%). ERIC outperformed EVA in all periods, except from 2003 to 2004, but the greater R2 in that period was not statistically significant.

In incremental information content tests, 13 (12) of 30 ERIC components (6 over 5 periods) are significant at a level of p < 0.05 (p < 0.01). None of the components are statistically significant at conventional levels (p < 0.05) in any period. For the two-year periods, CFO adds the most incremental information content beyond that contained in the other components.

5.2. Do adopters of VBM Metrics React More Strongly?

Firms that adopt VBM metrics are, obviously, more likely to manage them and

aim for their maximization (

Toft and Lueg 2015b). Accordingly, VBM adopters should

eventually show greater association with MktAdjRets than non-adopters (

Biddle et al. 1997;

Palliam 2006). To distinguish between (sophisticated) adopters and non-adopters, we examined annual reports and proxy statements for 2140 firm years from 2003 to 2012. We searched for the terms

ERIC, EVA, economic value added, economic profit, residual income, abnormal earnings, excess earnings, excess income, excess realizable profit, and

super-profits. None of the firms used ERIC. We created two categories of adopters:

VBM adoption was used as a dummy variable metric if firms mentioned one of our search terms. A total of 146 of the 214 firms used these VBM-related terms in their annual reports or proxy statements (68.2%). The second,

VBM compensation, was used if firms mentioned that the metric was used in this specific year for compensation purposes. Of the possible 2140 firm years, 1170 firm years (54.7%) were found to contain such metrics in relation to the top executive compensation in that given year. We re-ran our regression from above, expecting that the importance of RI, EVA, and ERIC would increase.

Table 4 depicts our results for the relative information content. Compared with our original investigation (

Table 2),

all explanatory power of the metrics decreased. We would have expected this decrease for CFO and EBEI, as VBM adopters (both

VBM adoption and

VBM compensation) should focus more on RI, EVA, and ERIC. However, the predictive power of VBM metrics also decreased. Overall, CFO and EBEI are still better predictors of stock returns than VBM metrics. In this test, among VBM adopters, ERIC does not significantly outperform EVA anymore. This is probably because none of the firms mentioned ERIC, so none of them have attempted to manage ERIC.

Table 5 depicts our results for the incremental information content. Both

VBM adoption and

VBM compensation show greater R

2 (15.50% and 18.50%) than the model used in

Table 3 (12.70%). This suggests that firms using VBM metrics have a greater association with one-year MktAdjRets. CFO and accrual are once more the two components with the greatest information content. However, they add less incremental value among VBM adopters, as shown by the lower F-statistics compared to

Table 3. Further components of ERIC add less incremental value to explaining stock returns, and yet, they are higher among VBM adopters (

Table 5) than among the whole sample (

Table 3). Unlike in

Table 3, the ExtraOrd items are significant.

5.3. Five-Year Returns as the Dependent Variable

Stewart (

1994) reports the strongest results for EVA over a five-year period. This test will take the stock return from 31 March 2008 to 31 March 2013 and the five different performance metrics from 1 January 2008 to 31 December 2012 (2008–2012) as the non-lagged (X

t) performance metric, and from 1 January 2003 to 31 December 2007 (2003–2007) as the lagged (X

t−1) performance metrics. Because of the data used in this regression, only one test is performed. This test is the single most important test of our study, clarifying the ability of the performance metrics to gauge long-term shareholder value (

Copeland et al. 2004;

Holler 2008, pp. 16–18;

KPMG and Velthuis 2004;

Venanzi 2012, p. 9). In this test, depicted in

Table 6, EBEI (7.5%) outperforms all other performance metrics, yet its relative value of R

2 is lower compared with

Biddle et al. (

1997). ERIC is now a much better performance metric in the long term than EVA, predicting 3.7% of 5-year stock returns. Contrary to our previous 1-year return analyses, CFO contributes the least relevant information in the long term.

5.4. Two-Year (Contemporaneous and One-Year Ahead) Returns as the Dependent Variable

This test allows for the possibility that the stock market takes longer than one year to incorporate performance metrics into stock prices (not tabulated, later summarized in

Table 7). We take the contemporaneous year and the next year’s stock returns as the dependent variable. This test finds RI to be better associated with two-year stock returns (4.3%) than CFO, ERIC, EBEI, and EVA (3.7%, 1.5%, 1.5%, and 1.3%, respectively). ERIC once again significantly outperforms EVA, and all pairwise combinations of performance metrics are statistically significant at a level of

p < 0.01. From the incremental information content test, all F-statistics are statistically significant at a level of 0.01 except CEQAdj, which is statically significant at a level of

p < 0.05. ExtraOrd is not statistically significant. The R

2 for the components of ERIC is 6.6%, suggesting that ERIC’s components add information content beyond those of CFO. The ERIC-specific components are statistically significant, and the F-statistics suggests that the capital charge component is important to ERIC and only slightly less important than CFO.

{kind=link}

{kind=link}