1. Introduction, Purpose, and Research Questions

Corporate foresight provides an ability to reconfigure the resource base of a firm by including the resources of collaborators and acquisitions. Foresight has a clear and systematic orientation toward the future (

Fergnani 2022, p. 825). However, realizing the value-creating potential of collaborative strategies is very challenging (

Bower 2001;

King et al. 2004;

Schweizer et al. 2022). The resource-based view (RBV) proposes that the accumulation of valuable, rare, inimitable, and organized (VRIO) resources is the basis for adding higher value in comparison with competitors (

Barney and Hesterly 2015). For example, accumulating VRIO resources to enhance economic rent (added value) has become fundamental in academic and managerial strategic thinking (

Lin and Wu 2014). Moreover, research remains rather fragmented regarding the relationship between the building blocks of a synergy-building mechanism joining the VRIO resources of cooperative partners and the foresight of their synergetic implications on the one hand and value-added economic rent on the other.

Schweizer et al. (

2022) argued that most collaborative strategic transactions “do not seem to meet expectations, so scholars and practitioners alike have been calling for a deeper understanding of M&A performance” (

Haleblian et al. 2006;

King et al. 2004;

Schweizer et al. 2022, p. 1). To value collaborative synergies,

Rabier (

2017) recommends quantifying an operating synergy (e.g., revenue growth through new product offerings or cost savings through the economies of scale) that is more likely to result in higher operating profit margins (EBIT/net sales) and financial synergies (e.g., improving free cash flows and optimizing the weighted average cost of capital (WACC)).

Explicit synergies are mainly analyzed by scholars with respect to cost reductions and revenue increases. However, achieving tacit synergy requires creating and developing new competencies that utilize merging partners’ VRIO resources and thus provide “value in development” (

Hao et al. 2020). The implementation of such a tacit synergy or “value in development” requires consideration by scholars and practitioners. This paper aims to develop a conceptual framework that will be useful for scholars and practitioners in developing explicit synergies and valuing tacit synergy in strategic collaborative ventures. Therefore, this paper looks for answers to two research questions: (1) What determines the success or failure of explicit competence-based synergies? (2) How is tacit competence-based synergy measured, with applications for real options?

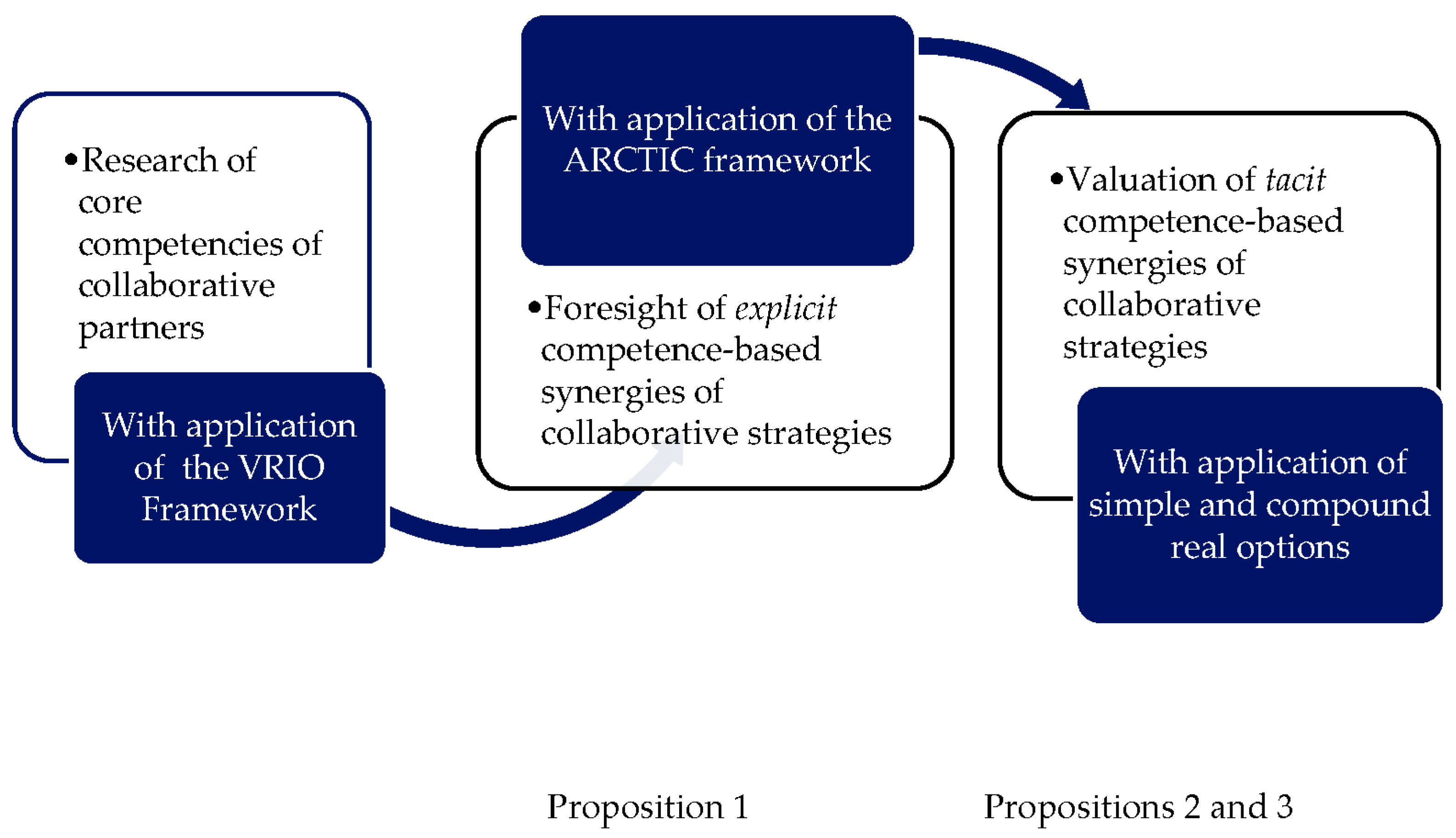

This study answers those research questions empirically by exploring the prerequisites of explicit competence-based synergies via the ARCTIC framework and measuring tacit synergy by considering the successful merger of Ahold and Delhaize in 2016, investigating the reasons for the termination of Tesco and Carrefour’s international alliance (2018–2021), and valuing their unrealized synergies by way of sequential compound real (call-on-call) options. After carrying out two illustrative (deductive) case studies, the paper provides three theoretical propositions and explores explicit competence-based synergies in international alliances and mergers and acquisitions within global supermarkets through the RBV theoretical lens in general and the ARCTIC framework in particular. The paper measures tacit synergies or values in development with a simple and sequential compound real option application.

The remainder of the paper is organized as follows. Based on an in-depth literature review, the ARCTIC framework is developed and extended as a building block for competence-based synergies. Next, explicit and tacit synergies between allied firms and merging partners’ firms are discussed. This section supplements the ARCTIC framework with the foresight of explicit synergies and combines the application of real options with a measurement of tacit synergies. Then, the paper discusses in detail the value of tacit collaborative synergies with complex or exotic real options (

Hull 2022, p. 592). Three theoretical propositions are derived from the literature review. Then, illustrative case studies on the 2016 merger of Ahold and Delhaize and the international purchasing alliance between Tesco and Carrefour from 2018–2021 are conducted empirically to justify the developed propositions. Finally, the empirical results, the theoretical and empirical contributions, the limitations of the research, and future directions are discussed.

3. Design, Methodology, and Approach

Having analyzed a case study of the Ahold and Delhaize merger in 2016 and the strategic alliance between Tesco and Carrefour during the period of 2018–2021 and the potential collaboration after the alliance, the paper has explored the probable challenges in the global supermarkets’ alliances through two contemporary theoretical lenses: the resource-based view and real options theory. To find the causes of the success or failure of explicit competence-based synergies related to the international contexts of the Ahold and Delhaize merger and the Tesco and Carrefour alliance, the author has employed the ARCTIC framework.

The research confirmed that synergies in strategic collaborative ventures are a function of strategic compatibility, complementarities, and transferability of core competencies that are fostered by the internal advantages (A) and external relevance (R) of core competencies of partnership companies and are underpinned by open and interactive communication and absorption capacities (C), mutual trust, commitment, and integration promptness (T), the ability to deal with the impact of an institutional dimension and implement a robust implementation plan (I), and cultural compliance of business partners (C).

As shown in

Table 2, the author has adopted the recommendation of

Dunis and Klein (

2005) on real options variables to calculate the tacit competence-based synergies as the real options premium value of the merger of Ahold and Delhaize in 2016 by applying a simple option using the Black–Scholes option pricing model according to Formula (1) and to measure the collaborative synergies of the international alliance between Tesco and Carrefour and assess the potential synergies in the case of their future merger by applying sequential compound options according to Formula (2).

To justify its propositions, the paper further discusses and interprets the research findings of the Ahold and Delhaize merger and Tesco and Carrefour purchasing alliance case studies.

4. Illustrative (Deductive) Case Study of the Ahold and Delhaize Merger

In 2015, Dutch grocer Ahold announced the acquisition of Belgian food retailer Delhaize for USD 28 billion, and the deal was completed in 2016. The two merging corporations are now known as the Ahold Delhaize group and have become number four among the largest US-based grocers. The Ahold–Delhaize merger “adds scale, allows us [to invest more] in innovation, and provides opportunities to develop our store formats in a highly competitive market,” said Ahold Chief Executive Dick Boer. (

Walker and Gasparro 2015, p. 1).

According to analysts, the companies had relatively little geographic overlap in the US and could leverage their scale to lower transportation and warehousing costs, as well as garner more purchasing power with food suppliers (

Walker and Gasparro 2015). To explore the explicit and tacit competence-based synergies that had been generated within the Ahold and Delhaize merger process, the ARCTIC framework and simple real call option valuation were applied.

4.1. Justification of the First Proposition. Exploration of the Prerequisite of Explicit Competence-Based Synergies in the Ahold and Delhaize Merger with the ARCTIC Framework

Employing the VRIO framework, the two sets of core competencies of collaborative partners were explored by asking four questions regarding resources and capabilities: Are they valuable? Rare? Costly and/or time-consuming to imitate? Efficiently and effectively organized? Then, employing the ARCTIC framework, complementarity (factors A and R), compatibility (the first C factor), and transferability (factors T, I, and second C) of the core competencies were analyzed.

The results of the VRIO and, as an extension, the ARCTIC analyses show that both grocers have compatible, transferable, and mutually complementary core competencies. Practically, by employing the VRIO framework, the core competencies as a source of competitive advantage of each collaborative partner must be explored. Then, by applying the ARCTIC framework, the core competencies of the first collaborative partner (Ahold) should be explored regarding their complementarity (factors A and R), compatibility (the first C factor), and transferability (factors T, I, and second C) to the second partner (Delhaize) by answering “Yes” or “No”; thus, opportunities to create explicit collaborative competence-based synergies can be foreseen.

In the same manner, the second collaborative partner, namely, Delhaize, should explore the core competencies of Ahold in terms of the correspondence to the ARCTIC framework so that it can also foresee explicit collaborative competence-based synergies. Finally, in the case of six “Yes” answers, the foreseen explicit synergies in the M&A deal can be valued by employing a simple real options application involving the Black–Scholes option pricing model (BSOPM) and sequential compound real options in the case of an alliance to a merger and acquisition strategy.

Regarding the complementarity core competencies (factors A and R) of Ahold and Delhaize, one of them is geographic complementarity in terms of locations in the US market. Ahold was more active in urban zones of the USA, whereas the US-based Food Lion grocery chain of Delhaize is more active in rural areas. This core competence gave them a significant competitive advantage by engaging almost all types of customers in the USA.

Regarding the compatibility of core competencies (the first C factor ), the similar business model that fit each market should be mentioned as well. Ahold and Delhaize acquired local grocers rather than promoting their brand in acquired supermarkets. Both grocers began as family-based businesses. Therefore, their business models and corporate cultures are compatible.

When it comes to the transferability of core competencies (factors T, I, and second C), digitalization of grocery retailing, which has a strong impact on the retail customer, should be mentioned as well. Ahold had a well-developed digital undertaking (click and collect) in Europe and the US thanks to Bol.com subsidiaries, and Delhaize could benefit from it. Transferability of core competencies and their effective integration provided an explicit competence-based synergy that could be foreseen by employing the ARCTIC framework as shown in

Table 3.

Having employed the ARCTIC framework to foresee prerequisites of explicit synergies of the Ahold Delhaize merger, it became quite evident that complementarity (A, R), compatibilities (first C), and transferability (T, I, and second C) of core competencies of Ahold Delhaize helped the partners to reciprocally benefit each other. To put it simply, several featured reasons drive explicit competence-based synergies as follows. Having integrated two sets of core competencies, the Ahold Delhaize group now provides exhaustive product mix options to their customers and caters to various customers in terms of geographic segments in the retail (grocery) industry. The Ahold Delhaize group has extensive dealer networks and associates’ networks that help in managing competitive advantages (cost reduction and differentiation) in the retail (grocery) industry. Even though most off-line players in the grocery industry strive to innovate, the Ahold Delhaize group has already advanced a successful record in consumer-driven digital innovations (e.g.,

Čirjevskis 2020).

4.2. Justification of the Second Proposition. Valuation of Tacit Competence-Based Synergies with a Simple Real (Call) Options Application

To value tacit competence-based synergies or “value in development” of the Ahold and Delhaize collaborative venture as a simple real call option, the Black–Scholes simple option pricing model (

Black and Sholes 1973) was employed, namely: C (S, t) = S0 ∗ N(d1) − K ∗ e

−rT ∗ N(d2), where N(d1) and N(d2) are the cumulative distribution functions of the standard normal distribution; C (S, t) is the call option price (a tacit synergy value) at time t; S0 is the price of the underlying asset at time 0; K is the exercise price at time t; T is time in years; r is a risk-free rate; e is a mathematical constant approximately equal to 2.71828, the base of the natural logarithm; σ is expected volatility of an underlying asset’s value. To value the tacit synergy or a value in development synergy with a real options application, the author used the data shown in

Table 4.

The real option variables of the Black–Scholes option pricing model to value the tacit competence-based synergies of the Ahold and Delhaize collaborative venture were calculated employing a Microsoft Excel spreadsheet in Office 2010 and are given in

Table 5.

The value of tacit synergies confirms the proposition given and provides evidence that Ahold Delhaize maximized market value added according to the estimated simple real (call) option value that equaled 3.5 EUR bn. To conclude, the application of simple real options provided for the estimation of a tacit synergy or value in the development of mergers and acquisitions deals.

5. Illustrative (Deductive) Case Study of the Tesco–Carrefour Purchasing Alliance

5.1. Rationales behind Entering an Alliance and the Impact of Institutional Context

A central rationale for entering an alliance for both Tesco and Carrefour (2018–2021) was firstly developing sales of their own product brands and, secondly, eliminating the middlemen in the face of suppliers. If the government did not intervene in the process, then the alliance would work perfectly for both companies. It was found that, being a very profitable form of collaboration for both Tesco and Carrefour, the alliance impacted the fairness of the market in the following aspects: decreasing the market power of supplies and decreasing suppliers’ involvement in innovations. As an outcome of the problems found, the French Competition Authority decided to adjust the cooperation terms for five years by (1) excluding several product families from the scope of the alliance, (2) limiting volumes for eight product categories, (3) and re-establishing the possibility for small suppliers to respond to calls for tenders (

Gauthier 2020).

By imposing strict restrictions on the Tesco–Carrefour alliance, French authorities supported suppliers in the market (especially small ones) and limited the partners’ operations with their own product brands, which was the highest priority for the alliance. Moreover, an influential role was played by the COVID-19 pandemic that started in 2019. Firstly, the UK and French governments introduced several restrictions on gatherings, mobility, and collaboration for safety purposes. Thus, customers started to visit offline grocery stores less often and for shorter periods. A big portion of customers moved towards online shopping. Secondly, the general purchasing power of consumers decreased due to increased unemployment. Moreover, the Brexit event in the life of the UK had some serious consequences for the Tesco–Carrefour alliance.

First, with the complication of paperwork (legal environment), it became much more difficult for both countries to perform logistics between countries and interact in general. Second, many immigrants living in the UK left the country due to the complicated process of receiving residence permits (

Butcher and Schraer 2018). Thus, with Brexit, Tesco and Carrefour faced regulatory problems which they could not predict and which, finally, slowed down the development of their own product brands.

5.2. Justification of the First Proposition. Exploration of the Prerequisite of Explicit Competence-Based Synergies in Tesco and Carrefour’s International Alliance using the ARCTIC Framework

When analyzing the core competencies of the collaborative partners, it can be concluded that Tesco and Carrefour were both successful in maintaining their leadership status within the highly unpredictable retail sector, where the companies followed cost leadership strategies and differentiation. Tesco and Carrefour were successful in obtaining both with the support of precise and smart management of the supply chain. The strategic use of geographical presence and customer loyalty also played a vital role in their success. Both companies made sure to align their internal core competencies with the market environment. However, the insufficient institutional strategies and somewhat neglected integration plan for core competencies highlighted a negative scenario for competence-based synergy in the future of this alliance, as shown in

Table 6.

When assessing the prerequisites of the competence-based synergy of the international alliance between Tesco and Carrefour by applying the ARCTIC framework application, it is clear that the complementarity and compatibility (factors A, R, C, T) of the core competencies of Tesco and Carrefour were not enough to deelop their further growth and generate competence-based synergies due to insufficient dynamic political capabilities and planning of integration of core competencies (factor I). Recently,

Oliver (

2016) found that the UK and France differ concerning Hofstede’s six dimensions of national culture.

There are significant differences in the dimensions “uncertainty avoidance”, or the attempt to make life predictable and controllable (France’s index is 86 and the UK index is 35), and “power distance”, or accepting the hierarchy of power and authority (France’s index is 68 and the UK index is 35) (

Hofstede et al. 2010). In this vein, cultural differences (the second C factor) between the collaborative partners could have also become insurmountable obstacles to creating a competence-based synergy. As a result, after the alliance formation, the partners did not benefit from each other’s competencies as shown in

Table 1.

Even though competence-based synergy potential can be found in global purchasing power, reducing the cost of goods according to customers’ needs, acquiring more and more customers, selling their own product brands, and sharing market profitability, their inability to cope with institutional context (factor “I”) was central to the failure of collaborative synergies of this international alliance. Although the partners did not demonstrate strong dynamic political capabilities, what could they have done differently anyway?

What is next for these companies and why is a possible future merger of Tesco and Carrefour not out of the question? Looking at the successful digitalization strategy of the Ahold Delhaize group, Carrefour and Tesco could accelerate their focus on innovation and create a seamless online and offline experience for their customers. Recent research on the success of the Ahold and Delhaize (AD) merger (

Čirjevskis 2020) confirms the argument that “enterprise digitalization is a way for companies to make their processes more efficient” (

Eremina et al. 2019, p. 1).

As an example of innovation, the Ahold Delhaize group has created automated checkout, self-scanning technology, and digital price labelling on the shelf. It turned out that the digitalization challenge in the grocery business, changing customer demand, and the fierce competition in the grocery market were the main rationales behind the merger of Ahold Delhaize and could be the next step in close collaboration between Tesco and Carrefour. To what extent is this possible?

5.3. Justification of the Third Proposition. Valuation of Tacit Competence-Based Synergies by applying Sequential Compound Real Options

Having discussed the rationales behind the alliance’s termination, the sequential compound option is applied to value tacit competence-based synergies provided by the alliance (as a first growth option) and tacit synergies of a hypothetical future merger (as the second growth option). The European type of compound option is exercisable only at expiration, where the duration of an option (T1 and T2) is the expectation of management of gaining collaborative synergy. Previous studies on the periods of gaining synergies in M&A deals of stock-listed companies have recommended using a 10-year period (T) for achieving synergies (

Damodaran 2005, p. 14), three years after the merger (

Vergos 2003), or even up to one year (

Dunis and Klein 2005, p. 7). The duration of gaining collaborative tacit synergy in an alliance formation (T1) is three years or the duration of the alliance lifecycle.

Because the merger could have been started, hypothetically, on 1 January 2022, for the valuation of the second call option (merger and acquisition), the assumption was made that the duration of gaining synergy would be three years till the end of 2024. Similarly, when Dutch grocer Ahold acquired Belgian food retailer Delhaize for USD 28 billion in 2015, it was reported that three years were needed to gain synergy (

Board Report Ahold 2015). The sequential compound option parameters have been calculated by applying the file extension XLSM that is assigned to spreadsheets created by Microsoft Excel 2007 and later versions, employing the function: @CallonCall(StockPrice; Strike1; Strike2; Expiry1; Expiry2; RiskFreeRate; Dividend; Volatility) where dividends equal zero (see

Table 7).

Having applied a combined sequential compound real option to value Tesco and Carrefour collaboration synergies, the option valuation result (tacit synergies) was estimated at EUR 2.17 bn, evidencing that a possible merger of the two global grocery retailers might not be excluded in the future.

6. Conclusions, Contributions, Research Limitations, and Future Work

This paper constitutes a novel theoretical and empirical contribution to foreseeing an explicit competence-based synergy in international collaborative ventures from the resource-based view and values a tacit competence-based synergy by applying real options. This is the main theoretical contribution of this paper. Moreover, the paper makes several theoretical and empirical contributions to the strategic management, international business, and corporate finance disciplines.

In this paper, two research questions have been answered empirically. By employing deductive logic, the case studies represent important critical success factors that impact explicit synergy and provide a tacit competence-based synergy in M&A deals and international strategic alliances. Having analyzed the acquisition of Delhaize by Ahold Delhaize in 2015 and the creation of the Ahold Delhaize group in 2016, the case study has confirmed that the ARCTIC framework helps foresee explicit competence-based synergies in M&A processes (first proposition). What is more, a tacit synergy can be valued with a simple real option (second proposition). This is the paper’s important theoretical and practical contribution to global M&A issues.

Regarding the contribution to the strategic management discipline, the application of the ARCTIC framework goes beyond the application of VRIO resources to operations of an individual corporation in individual foreign countries (

Kogut 1985;

Ghemawat 2007) and thus contributes to a resource-based view on strategy (

Barney 1991) in the international and institutional contexts of collaborative ventures. The research has confirmed the six success factors of the ARCTIC framework that enable one to foresee explicit competence-based synergies of collaborative ventures (

first proposition). The research has also confirmed that, even though the Tesco and Carrefour purchasing alliance mainly generated strengths for the groups (factors A, R, C, and T), there were nevertheless some significant weaknesses (factors I and second C) that led to the alliance’s termination.

Moreover, the ARCTIC framework helped to foresee prerequisites of explicit synergies of the Ahold Delhaize merger, making it quite evident that complementarity (A, R), compatibilities (first C), and transferability (T, I, and second C) of core competencies of Ahold Delhaize helped the group to create a collaborative synergy. The application of simple real options valued the tacit synergy of this collaborative deal and confirmed the second proposition.

In contributing to the real options theory,

Kogut (

1991) argued that “when a firm initiates an alliance, the firm obtains an option to expand or acquire in response to future market developments while retaining the option to defer complete commitment” (

Tong and Reuer 2007, p. 38). In this vein, initiating an international alliance between Tesco and Carrefour has been considered as exercising the initial option to generate alliance-based synergies, which in turn would have led to the creation of other real options, such as the option to acquire or the option to abandon (

Li et al. 2007). Therefore, the paper contributes to the intersection between corporate finance and strategic management by demonstrating that tacit competence-based synergies of collaboration strategy from alliance to merger can be valued by sequential compound real options (

third proposition).

Within most salient future research opportunities on corporate foresight, Fergnani recommends two-stage mediation as follows: corporate foresight > new business opportunities > resource-based changes > performance (

Fergnani 2022, p. 836). This paper contributed to this scientific recommendation by demonstrating the following discourse on mediation stages of foresight:

corporate foresight (collaborative strategies) >> new business opportunities (identification of VRIO resources of potential collaborative partners) >> resource-based changes (exploration with the ARCTIC framework) >> performance (real options valuation of competence-based synergies as added market value) as given in

Figure 1.

Having empirically answered the two research questions of the paper, the relationship among the developed propositions and the conceptual model of foresight of explicit synergies and valuation of tacit competence-based synergies comprises the theoretical and managerial contributions of the research and can be employed by practitioners for decision-making and scholars for similar future research as shown in

Figure 1.

Figure 1 illustrates the likely relationships among the main constructs presented in the paper, with the ARCTIC framework shown as a building block of explicit synergism of collaborative ventures and the application of real options valuations to quantitatively measure tacit competence-based synergies.

What lesson can be distilled from the case studies conducted that should be considered in future research? When it comes to the limitation of real options application to measure competence-based synergies,

Ragozzino et al. (

2016) argued that “… If some attributes of real options are not observable and are, moreover, dependent on the unique assets held by heterogeneous firms and the synergies and complementarities that such investments can generate, then the analytical exercise surrounding the study of real options becomes complex as well as qualitative and subjective” (

Ragozzino et al. 2016, p. 433). In this vein, more interviews with industry practitioners are needed, to obtain their expert opinions, as is further quantitative research.

The evaluation of competence-based synergies was made based on the assumption that all six factors of the ARCTIC framework have the same weight of significance. However, the case study results confirm that institutional context and dynamic political capabilities could be a key to the creation of competence-based synergies in an international alliance. Therefore, the weighting of each factor of the ARCTIC framework for each strategic context, particularly for the global grocery industry and, for instance, the global ICT industry, comprises a promising future research arena. Moreover, future research could further explore the role of the six factors of the ARCTIC framework as a driver of dynamic capabilities that underpins explicit and tacit competencies-based synergies in collaborative strategies.

{kind=link}