1. Introduction

In the last twenty years, the impact of family ownership on performance of listed firms has attracted the efforts of worldwide scholars (

Poutziouris et al. 2015;

Villalonga and Amit 2020). A large part of the available research (

Poutziouris et al. 2015) focuses on performance metrics related to financial ratios, and balance sheet items. However, the evidence on the stock market performance of these firms is very limited, (

Eugster and Isakov 2019). A question still deserving a conclusive answer is whether there exists a

Family factor able to impact on stock performances, and whether this feature can be a guideline to obtain superior portfolio allocation rules. The first objective of this paper is to fill the literature gap, by proposing a detailed analysis of the stock returns of family-owned firms, compared to the rest of the market, in the last decade. Secondly, this paper aims to assess the impact of family ownership on stock performances, from an investor’s point of view. Using a comprehensive sample of non-financial firms, and an accurate definition of family-owned firm, evidence has been found that family ownership has a beneficial effect, and these firms consistently outperform counterparts and the entire Italian stock market. The detected abnormal return is impressive—(about) 7% per year. The obtained results may be a useful guide for investors and fund managers interested in stock selection criteria. The focus on the Italian market is, as far as we know, the first attempt to provide an extensive study concerning this country. The Italian case may be interesting due to the large number of family-owned firms.

Family ownership is the most common ownership in listed companies around the world (

La Porta et al. 1999;

Villalonga and Amit 2020). In the U.S., Anderson and Reeb

Anderson and Reeb (

2003) show the frequency of family ownership, concerning around 35% of the listed companies in the S&P 500. In Western Europe as well, the presence of family ownership is predominant: around 44% of the listed companies (

Faccio and Lang 2002). In Italy, the portion of family ownership is 60%, above the European average, although it reduces to 20% in the largest 20 listed firms (

Barontini and Caprio 2006). In the reported studies, the definition of family property requires that at least 20% of voting rights be handled by a family.

These findings on the dominance of family as ownership structure have prompted researchers to shed light on its impact on firm performance.

Poutziouris et al. (

2015) reported that the relationship between family ownership and profitability is mostly investigated, through the analysis of two financial ratios: ROA, return on assets, and Tobin’s Q. The impact of the family factor has been also evaluated through cross-sectional or panel data regressions, where the regressors include key quantitative and qualitative characteristics of firms. Although it could be relevant for investors attempting to pick stocks successfully, there are few studies investigating the impact of the family factor on stock returns (e.g., see

Eugster and Isakov 2019).

Anderson and Reeb (

2003) and

Poutziouris et al. (

2015) find that, in the Anglo-Saxon stock markets, family ownership has generally a beneficial effect, however, they identify a reversed-U-shape relation between ownership level and performance. When family shareholding overcomes a certain threshold, it is likely that firm performance begins to decline.

Eugster and Isakov (

2019), using the investor’s point of view, find that the

Founding family property has a positive impact on stock returns in the Swiss stock market, with an annual outperformance of 4% to 7%, compared to counterparts.

Barontini and Caprio (

2006) find that family firms in continental Europe have higher market valuations compared to non-family ones. This is also true after the founding stage, although families heavily use control-enhancing devices. The best results come from firms where a family has an active role, alongside a hired-hand executive.

The authors claiming better performance of family firms agree on the fact that some additional conditions are involved, especially a strong minority shareholder protection. In contrast,

Villalonga and Amit (

2006) find that the outperformance of American family firms fades when founders’ descendants follow. In the same context,

Miller et al. (

2007) suggest that the outperformance detected in the previous works could be due to an excessively broad definition of family. In fact, in firms with multiple family members, the potential value of far-sighted family guidance may likely be weakened by possible internal family conflicts.

Filatotchev et al. (

2005) find that firms listed in the Taiwan stock market whose dominant shareholder is an institutional investor have better performance than any other family counterparts, and the independence of the board from family ownership has a positive impact.

In short, for these scholars, the governance role of family members and their heirs appears to play a significant role, even though it can be negative. In addition, the separation between control and ownership in contexts of weak minority shareholder protection (see

Claessens et al. 2002;

Cronqvist and Nilsson 2003) seems to impact firm performances negatively. Notwithstanding, all of that reinforces the argument that in contexts of sound minority shareholders’ protection, the family firms have higher market valuations, regardless of family management involvement. In fact, in a cross-national study at the European level,

Maury (

2006) finds that family firms have superior profitability, reflected in higher market valuations, when the protection of minority shareholders is strong enough.

Isakov and Weisskopf (

2014) reach the same conclusion for the Swiss stock market.

Sraer and Thesmar (

2007), in a similar institutional context, find family outperformance in descendants’ management rather than founders’. It is evident that the difference in some conclusions could be attributed to multifaceted factors across the countries such as minority shareholder protection, control-enhancing devices, family generation, and cultural background

Isakov and Weisskopf (

2014).

The results presented above may seem in contrast to market efficiency (

Fama 1970). In fact, the type of ownership, as public information, should be already incorporated in the stock market price. Therefore, there should be no reason to believe that picking stocks based on this information might lead to superior portfolios. However, the fact that some information is in the public domain does not ensure it is properly assessed, especially if it is qualitative.

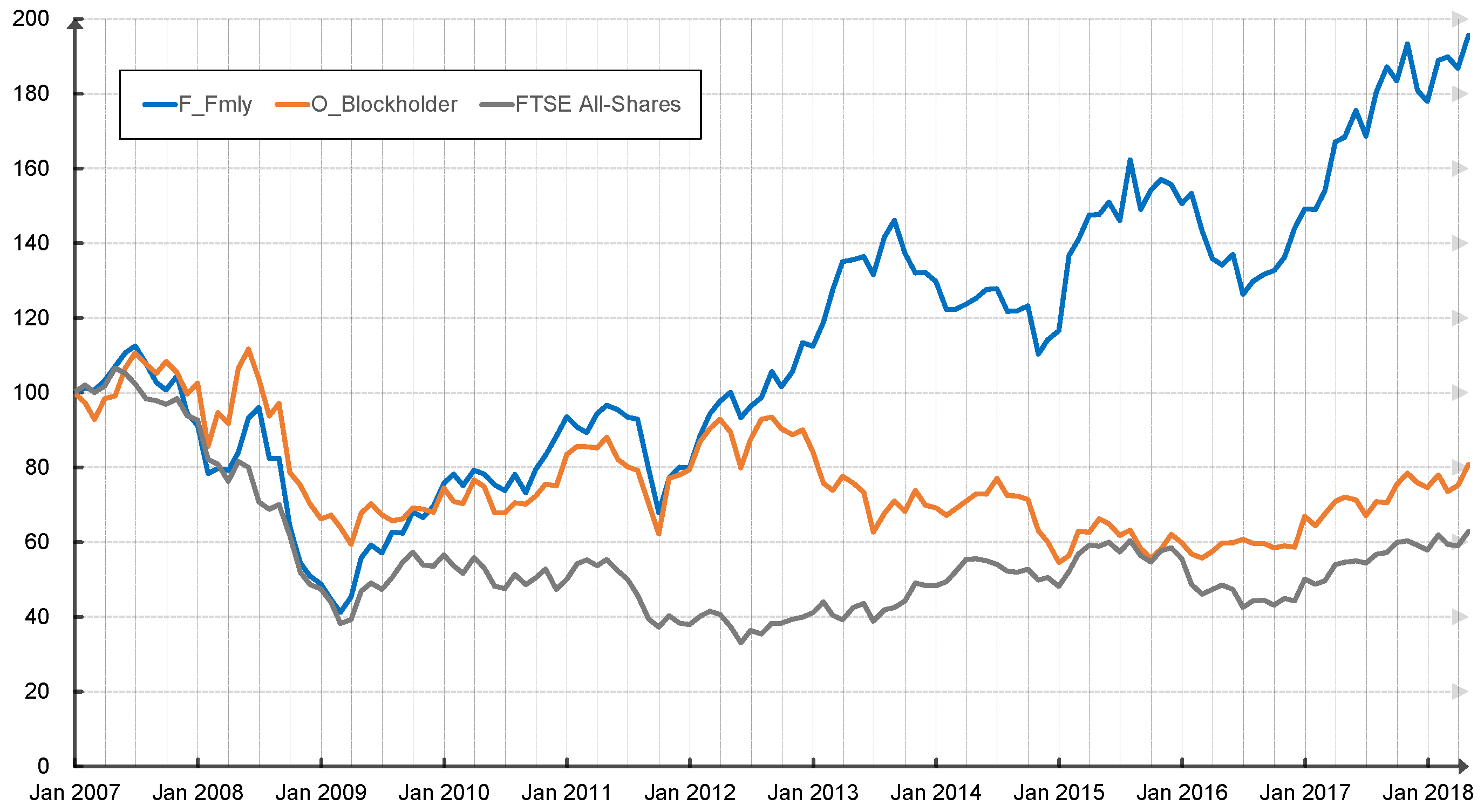

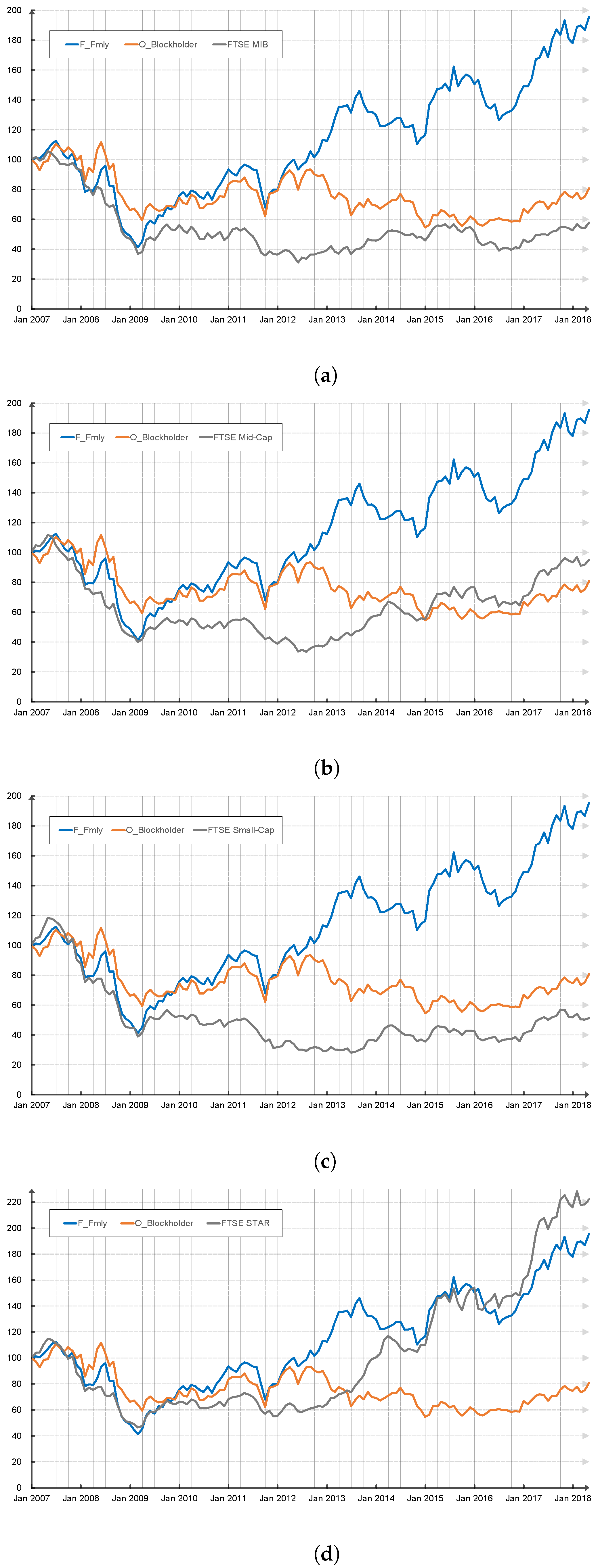

This paper proposes an empirical analysis of panel data, from January 2007 to April 2018, for a sample of 116 firms listed on the FTSE Italia All-Shares index. Although the Italian stock market is relatively small compared to its US or UK peers, Italy is still one of the most important economies in the world. In addition, Italian companies are characterized by high ownership concentration, the presence of many families, and a sound minority shareholder protection. Therefore, it may appear interesting for investigating the family property impact on stock performance.

The impact of ownership identity on stock returns is addressed through different methods. Initially, a specific definition of

Founding family is formulated. Afterwards, two market-value portfolios are built, representing the investment strategies based on the ownership identity. Then, the portfolio returns are analyzed in a framework including a four-factor model of

Carhart (

1997) and

Fama and French (

1992,

1993), to control for abnormal returns, taking into account exposure to various risk factors. To provide more robust assessment, the single stock returns are also analyzed by taking into account industry and firm characteristics, by using a control model.

The main results are that (i) a portfolio strategy based on founding families greatly outperforms the benchmark index and the alternative portfolio strategy; (ii) that is not explained by exposure to risk factors; and (iii) the single stock return benefits from the Founding family property, with other things being equal. Overall, the emerging evidence is for a positive impact of Founding family ownership, which is rewarded by the stock market returns.

This research contributes to the existing literature in two ways. First, this work is, to our knowledge, the first one to analyze the impact of family ownership on the Italian stock market. Second, it is one of the few papers that evaluate the firm performance from an investor’s point of view, which is too often neglected, even though it represents the most severe evaluation for a firm.

The paper is organized as follows:

Section 2.1 describes the data and variables used in the analysis, with a focus on the family factor definition.

Section 2.1.4 presents some descriptive statistics and insights of the sample.

Section 2.2 presents the methodology.

Section 3 presents the results.

Section 4 concludes.

{kind=link}

{kind=link}