Information Jumps, Liquidity Jumps, and Market Efficiency

Abstract

:1. Introduction

2. Market Efficiency in Semimartingale Model

2.1. Semimartingale Model

- is a process for which almost all sample paths are continuous and of finite variation.

- w is a standard Brownian motion.

- The Itô integrand , the spot volatility process, is pathwise strictly positive, cádlág, and locally bounded away from zero.

- is a finite-activity, simple counting process such that, for all , almost surely and is a countable family of non-zero random variables. The i-th jump occurs at stopping time with magnitude . In particular, the time series is adapted to the filtration , where is the -algebra generated by .

- is independent of w.

2.1.1. Large- and Small-Order Flows

2.1.2. Liquidity Jumps and Information Jumps

3. Empirical Methodology

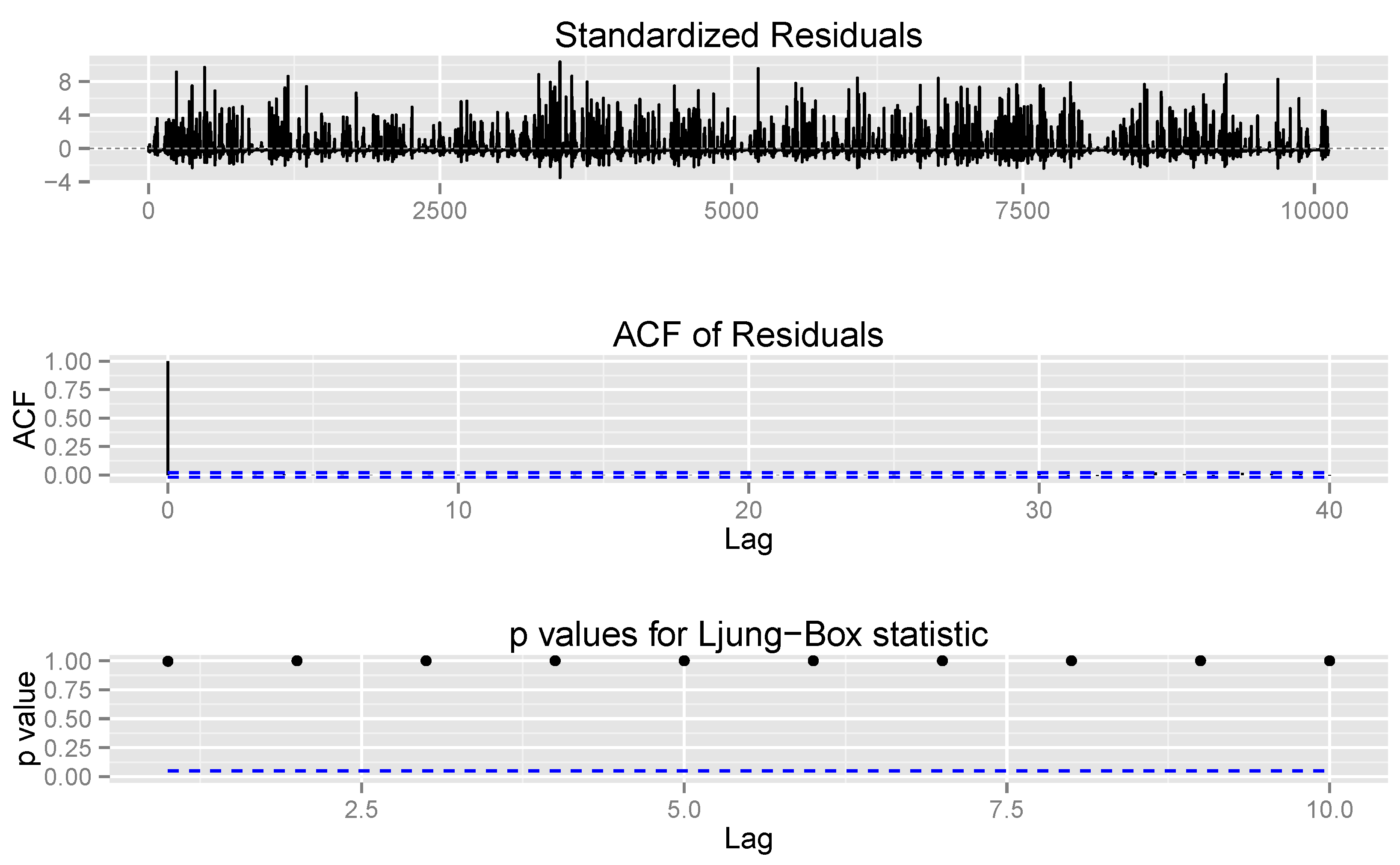

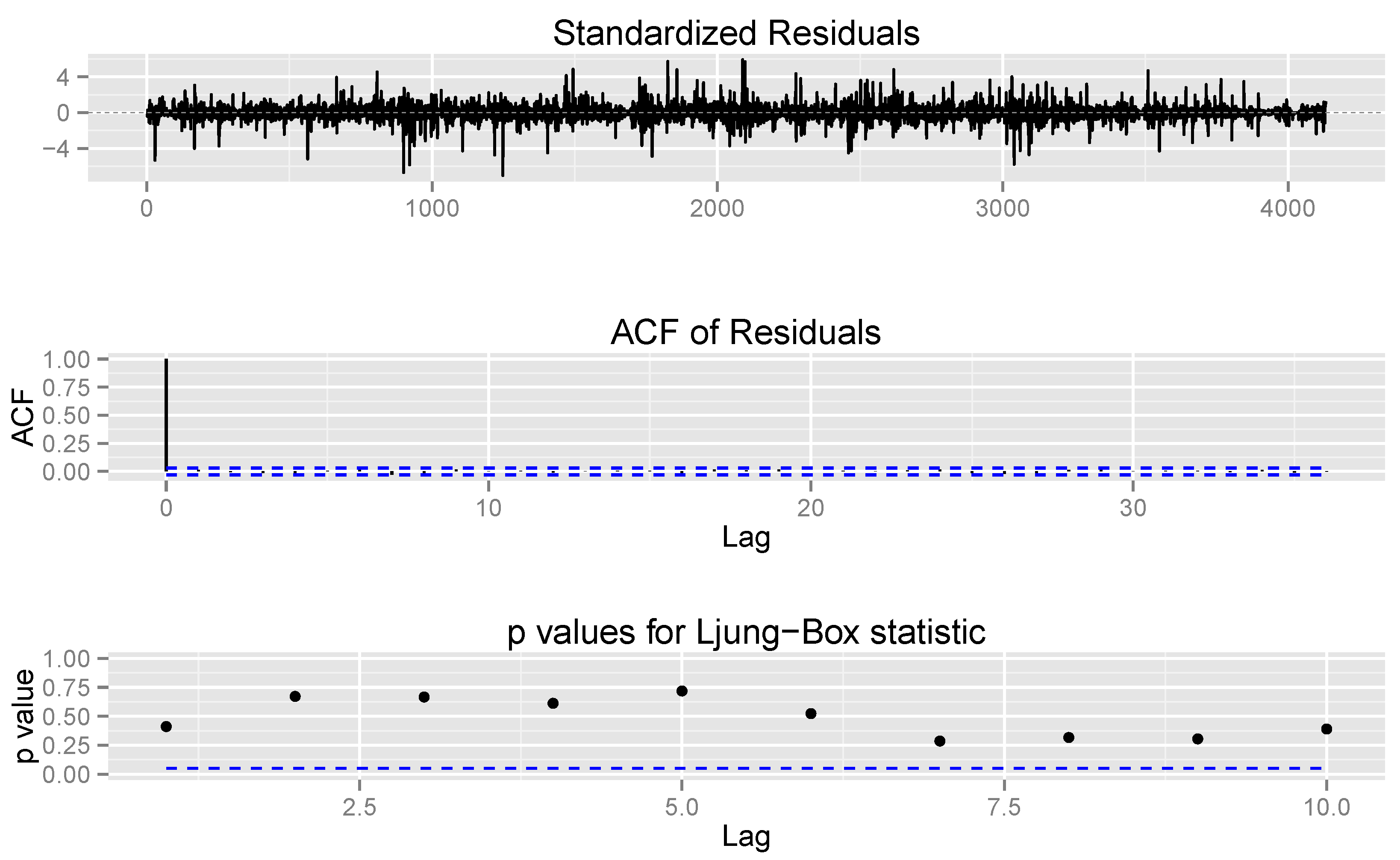

3.1. Estimation of Jumps

3.2. Microstructure Noise

3.3. Test Procedure

- Choose the highest sampling frequency that is free of microstructure noise by computing the quantity given by Equation (4) across different frequencies.

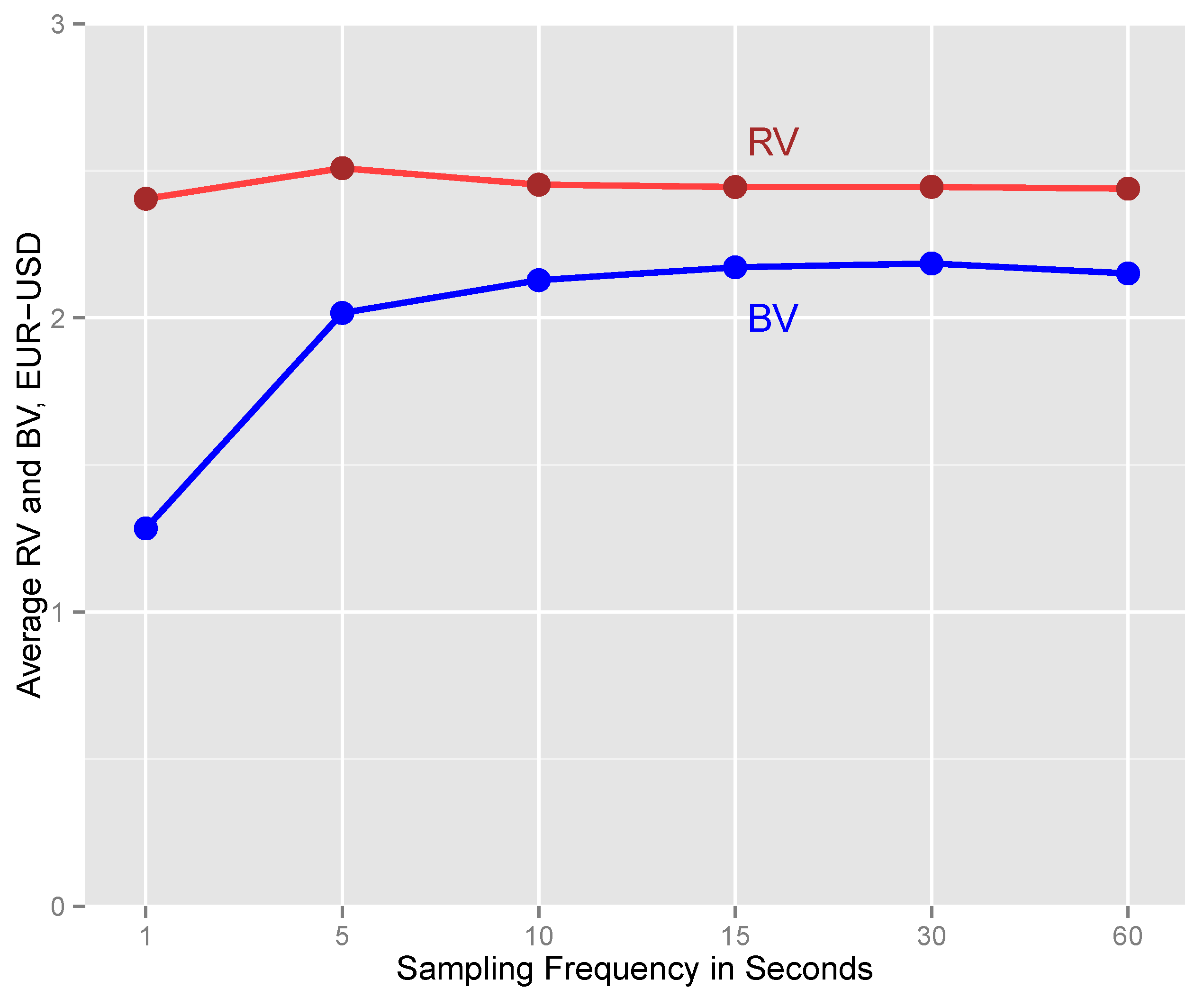

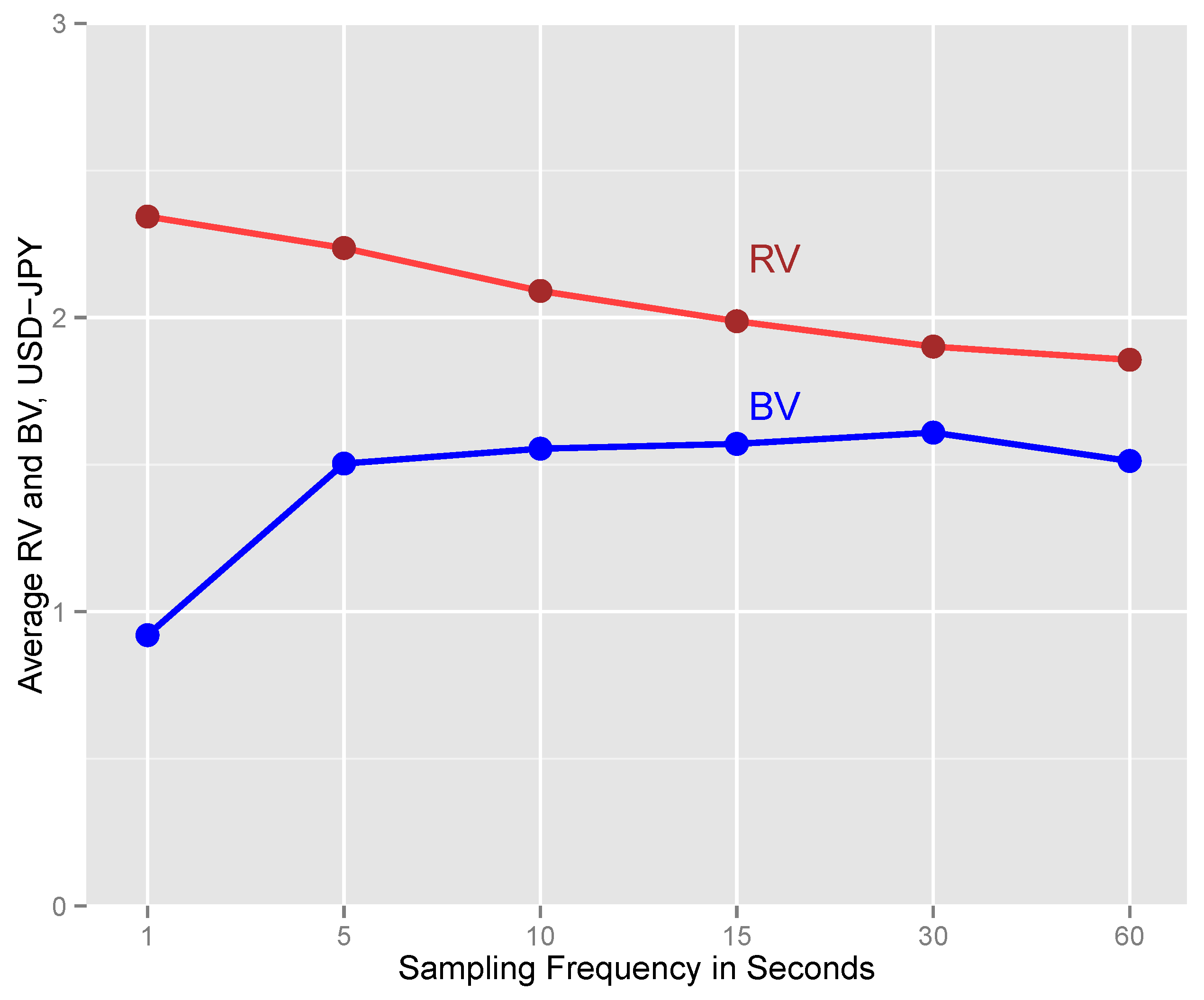

- At the chosen frequency, estimate the jumps using the statistic of Equation (3).

- Test the martingale null hypothesis on the time series of estimated jumps.

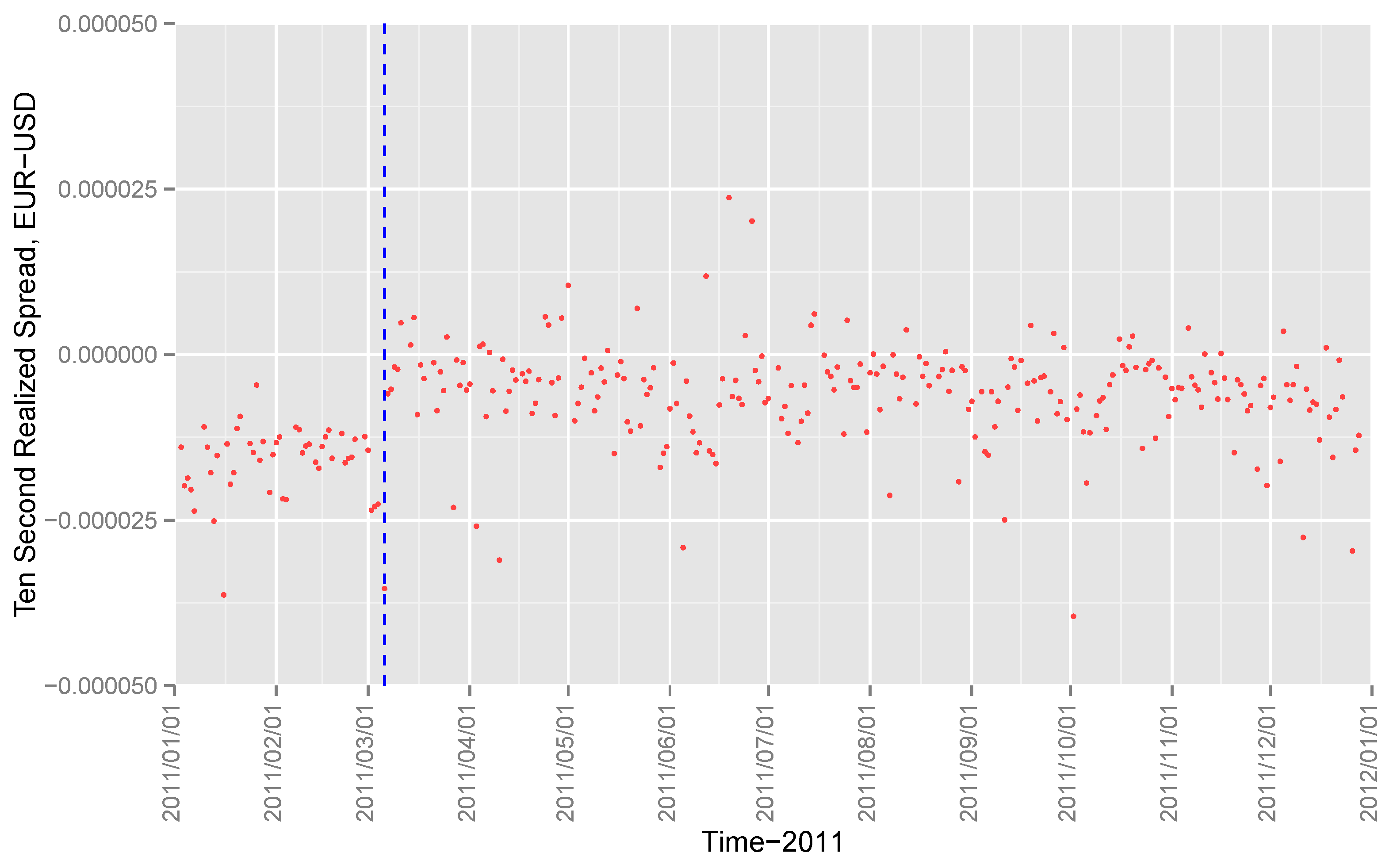

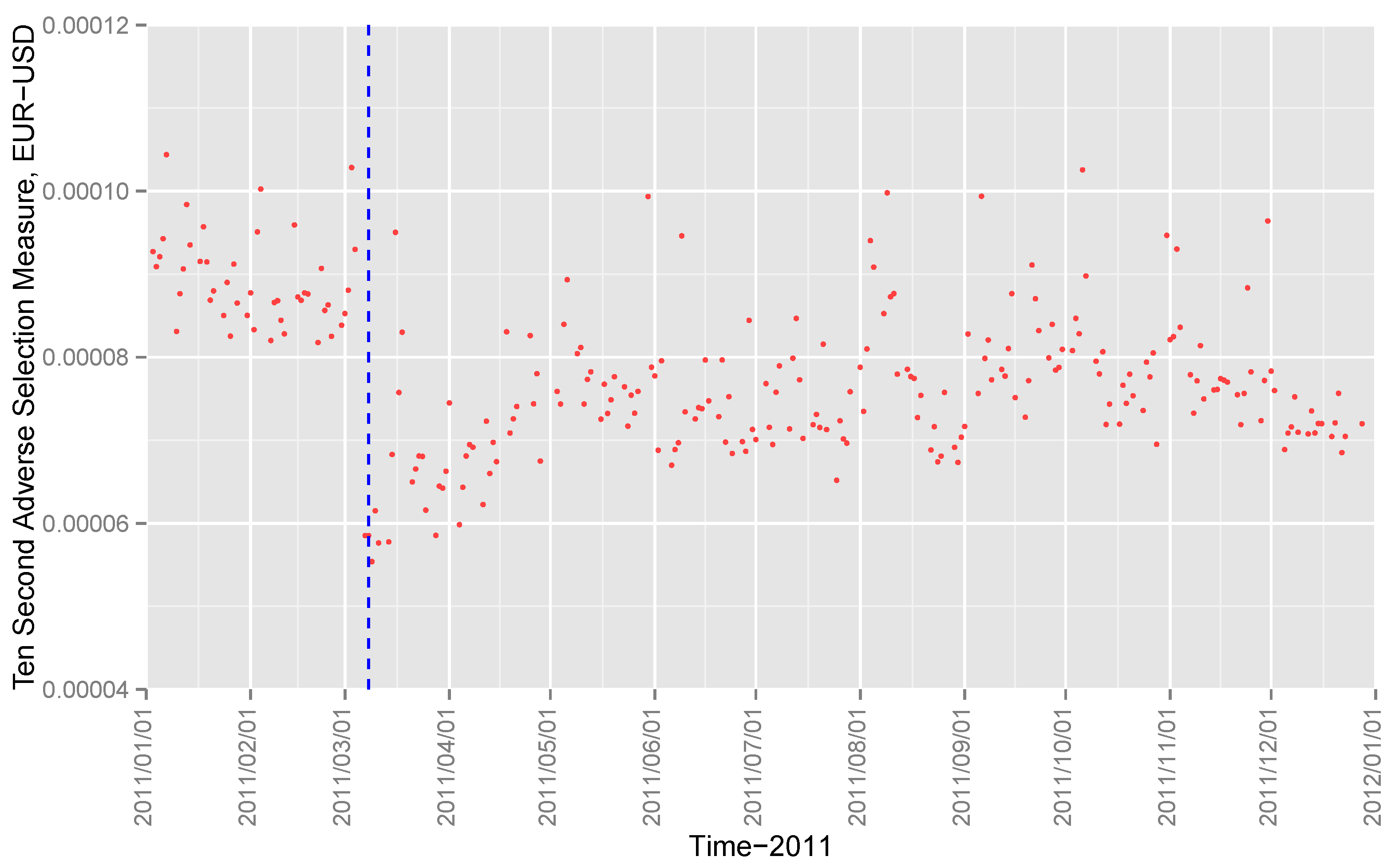

4. Application to FX Market

4.1. Martket Setting and Data

4.1.1. Interdealer FX Spot Market and EBS Platform

4.1.2. Data

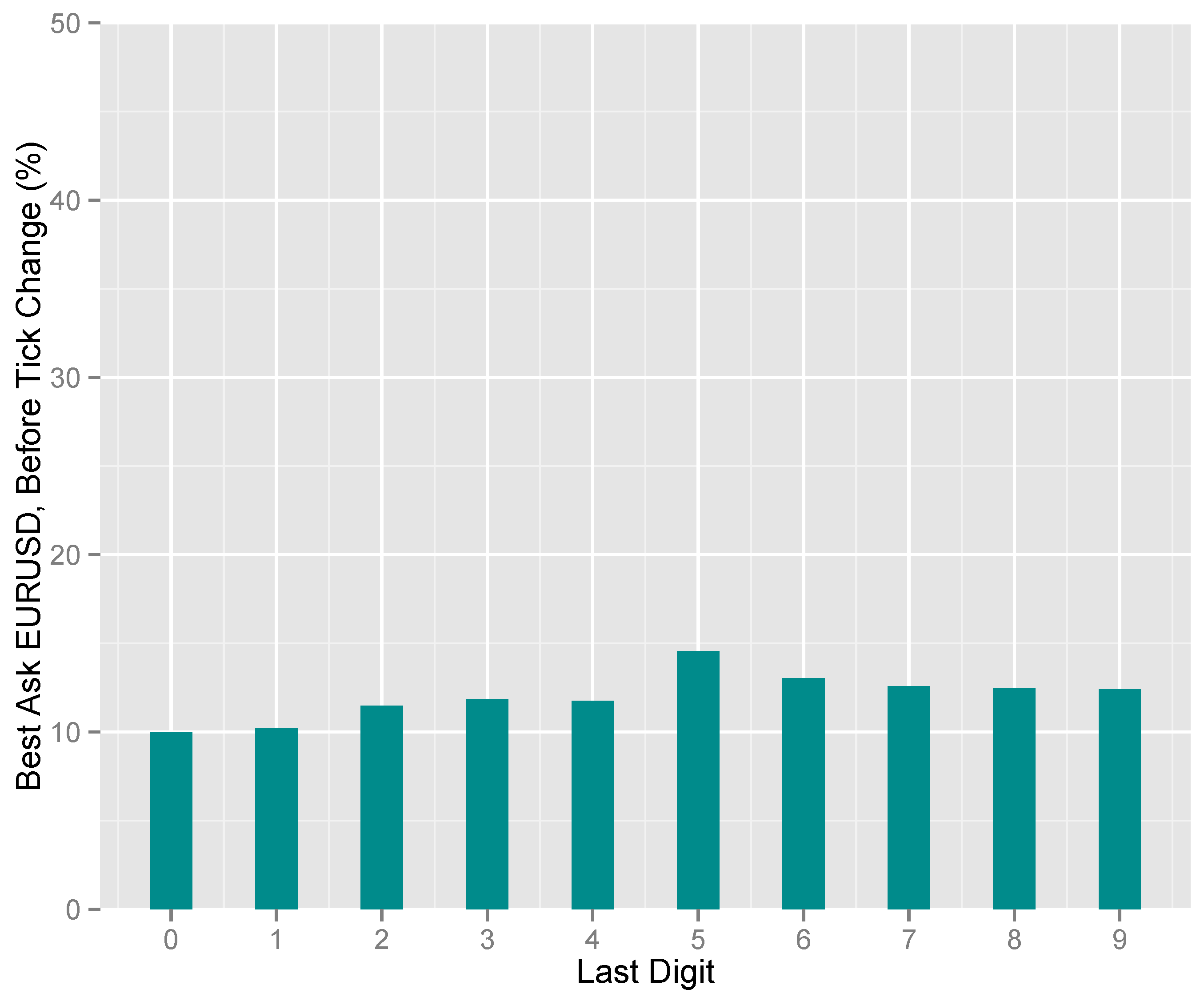

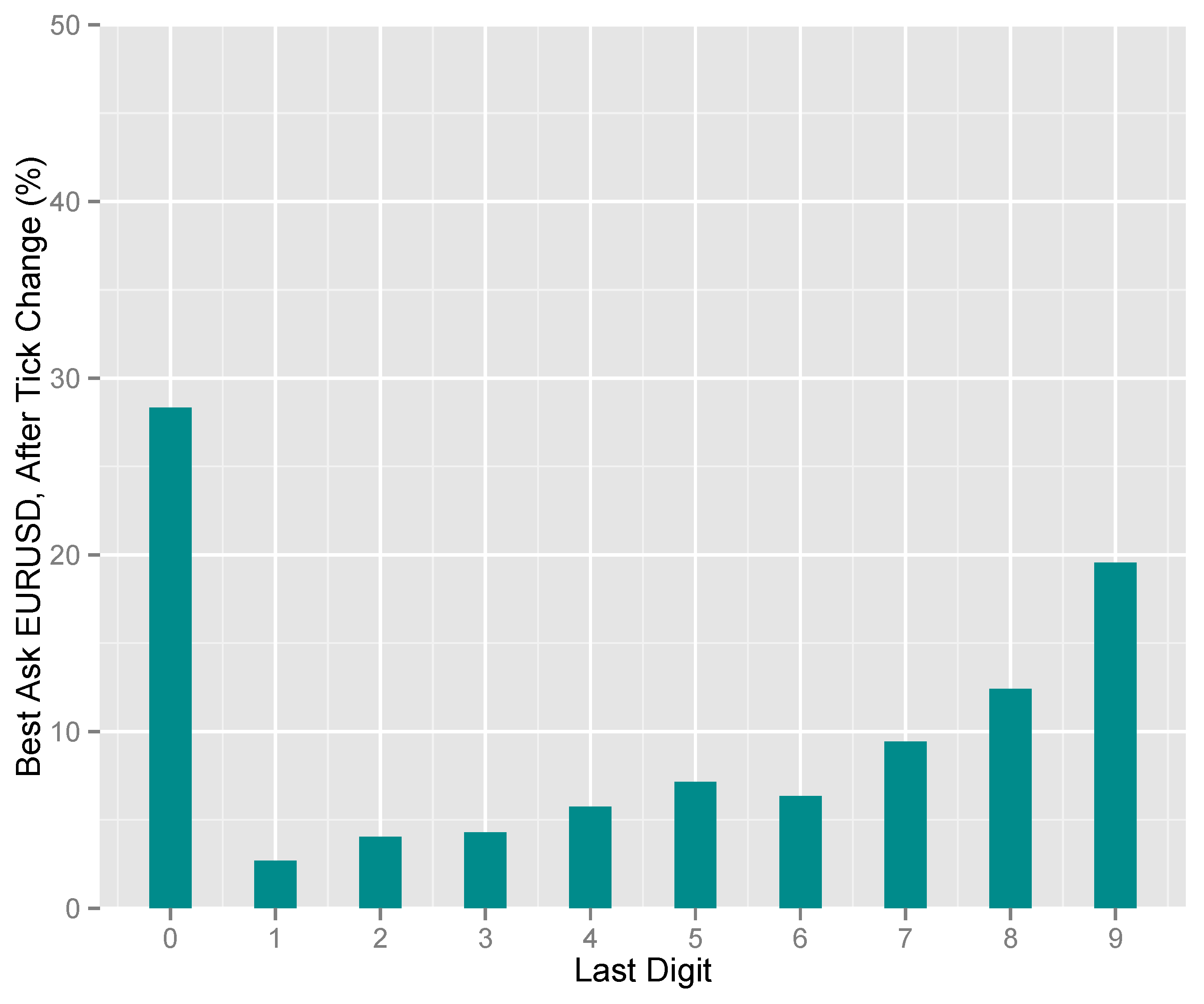

4.1.3. Tick Size Change

4.2. Information Efficiency Hypothesis

4.2.1. Microstructure Noise Threshold

4.2.2. Information Efficiency and Tick Size Change

4.3. Further Evidence

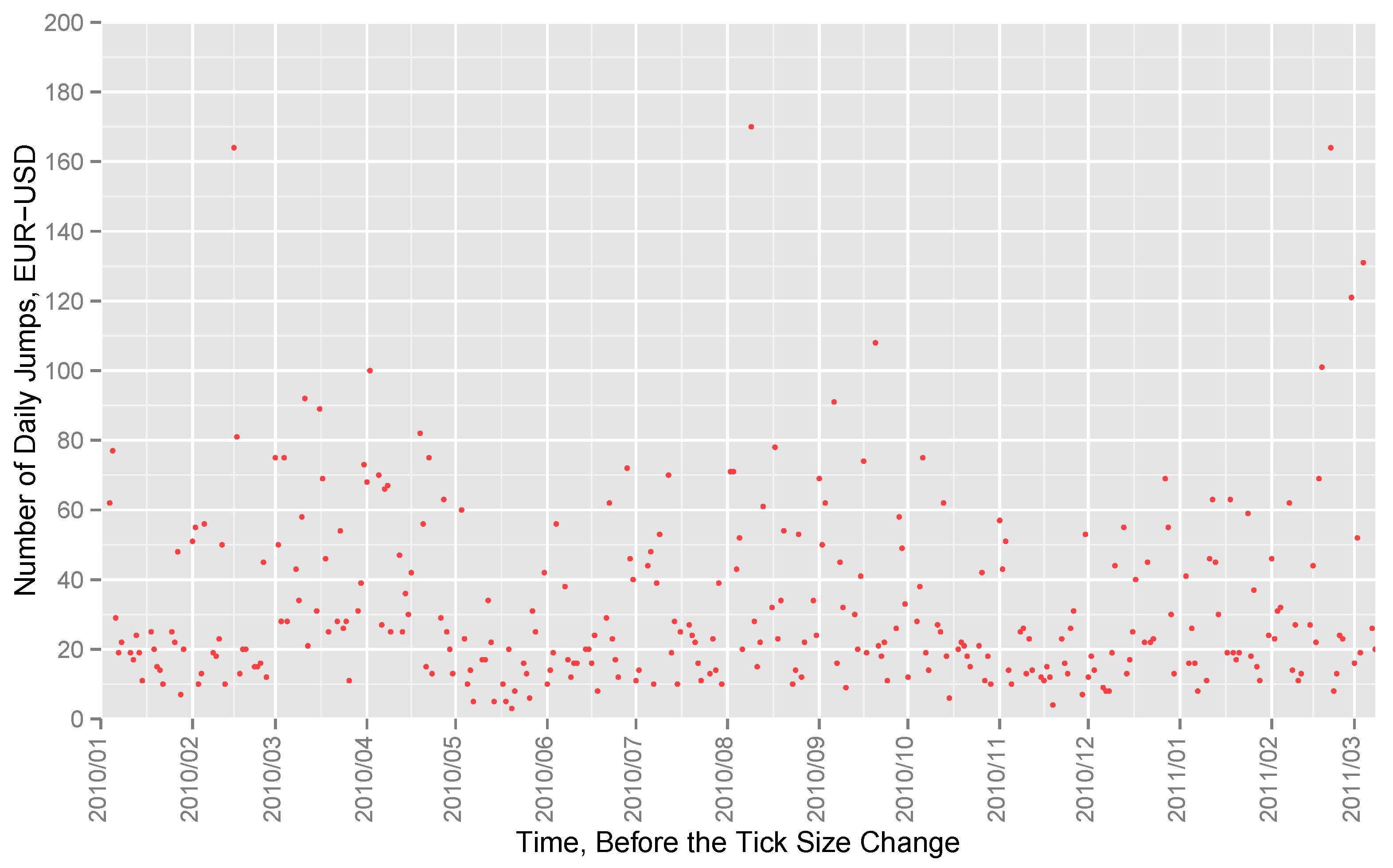

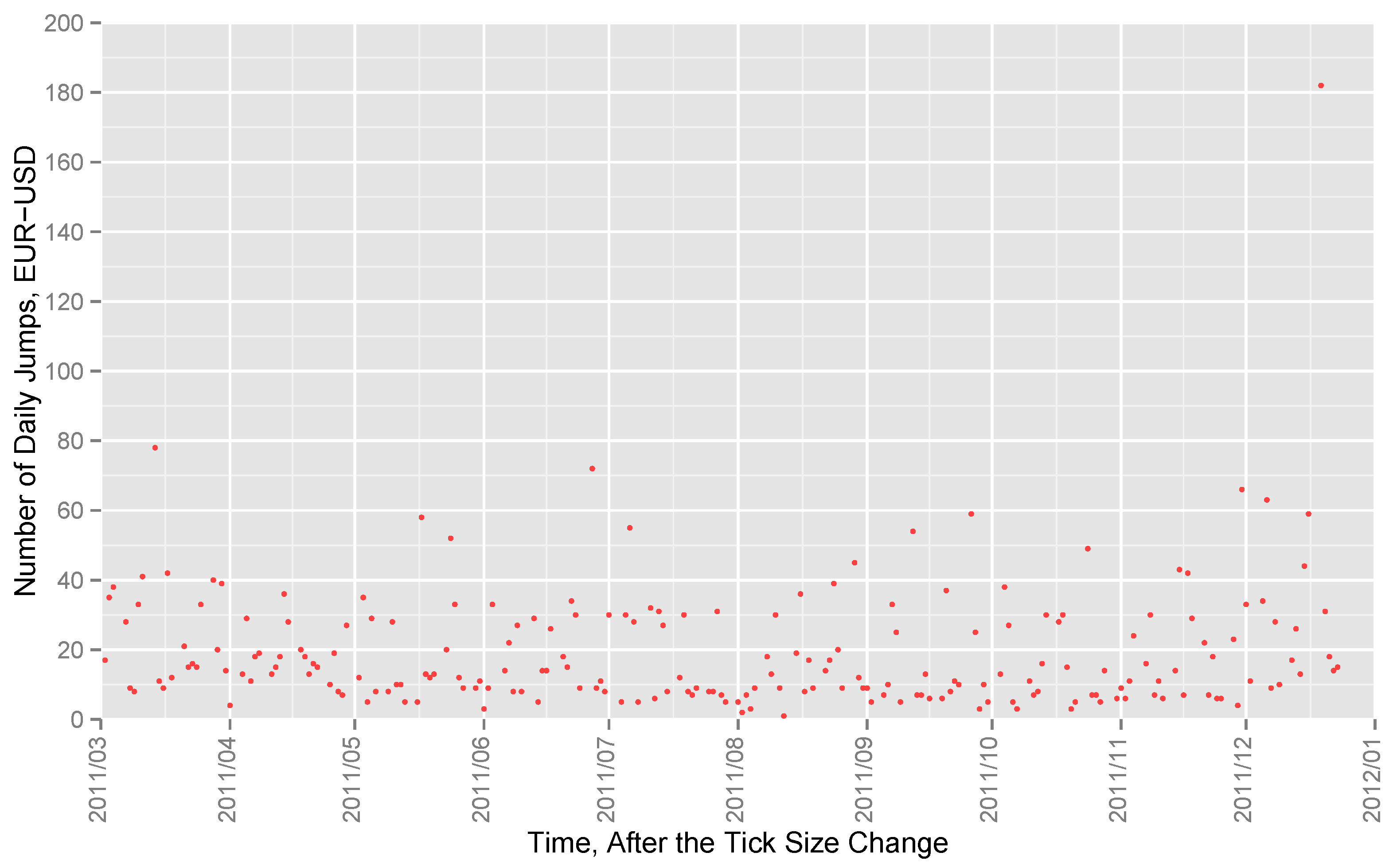

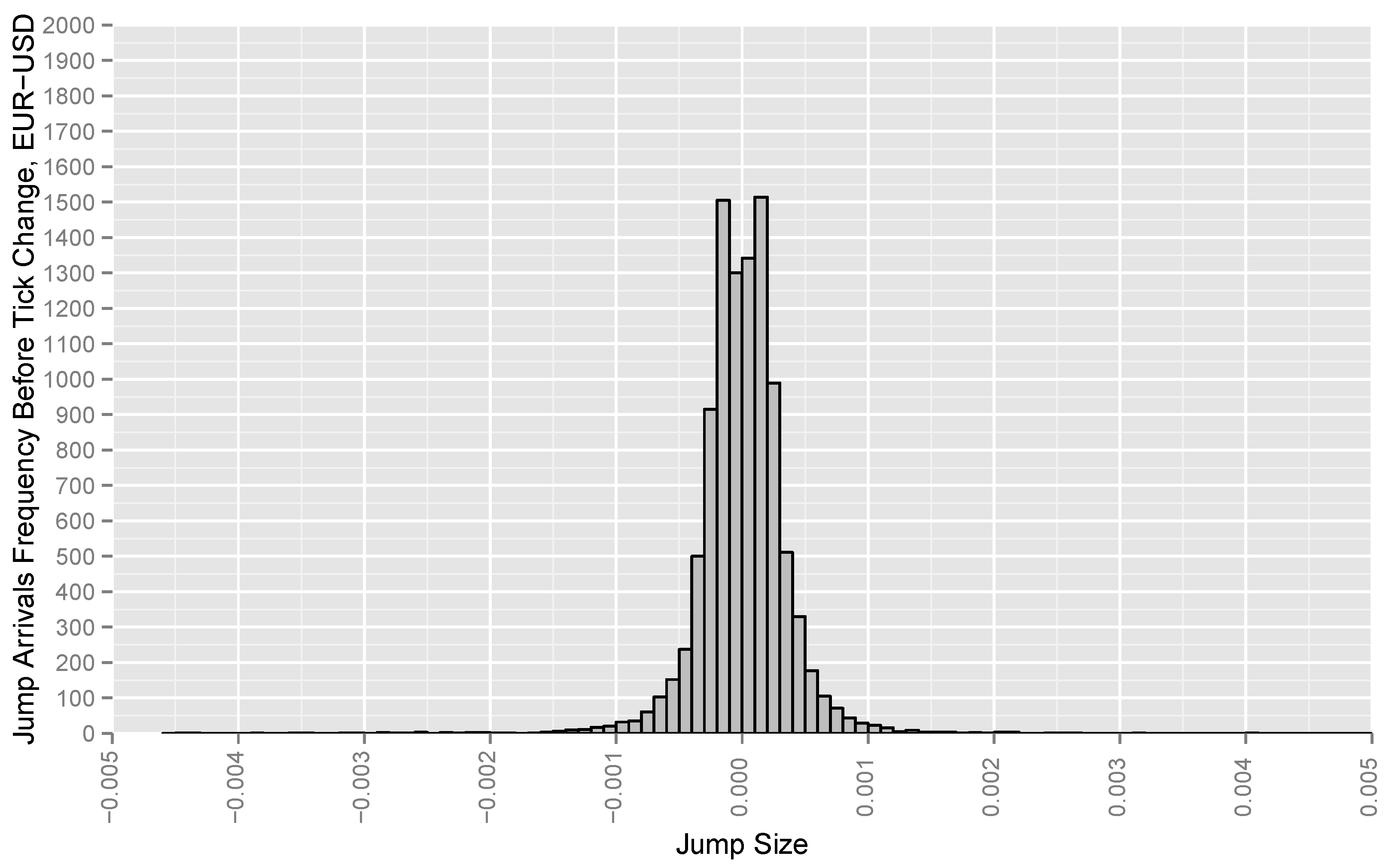

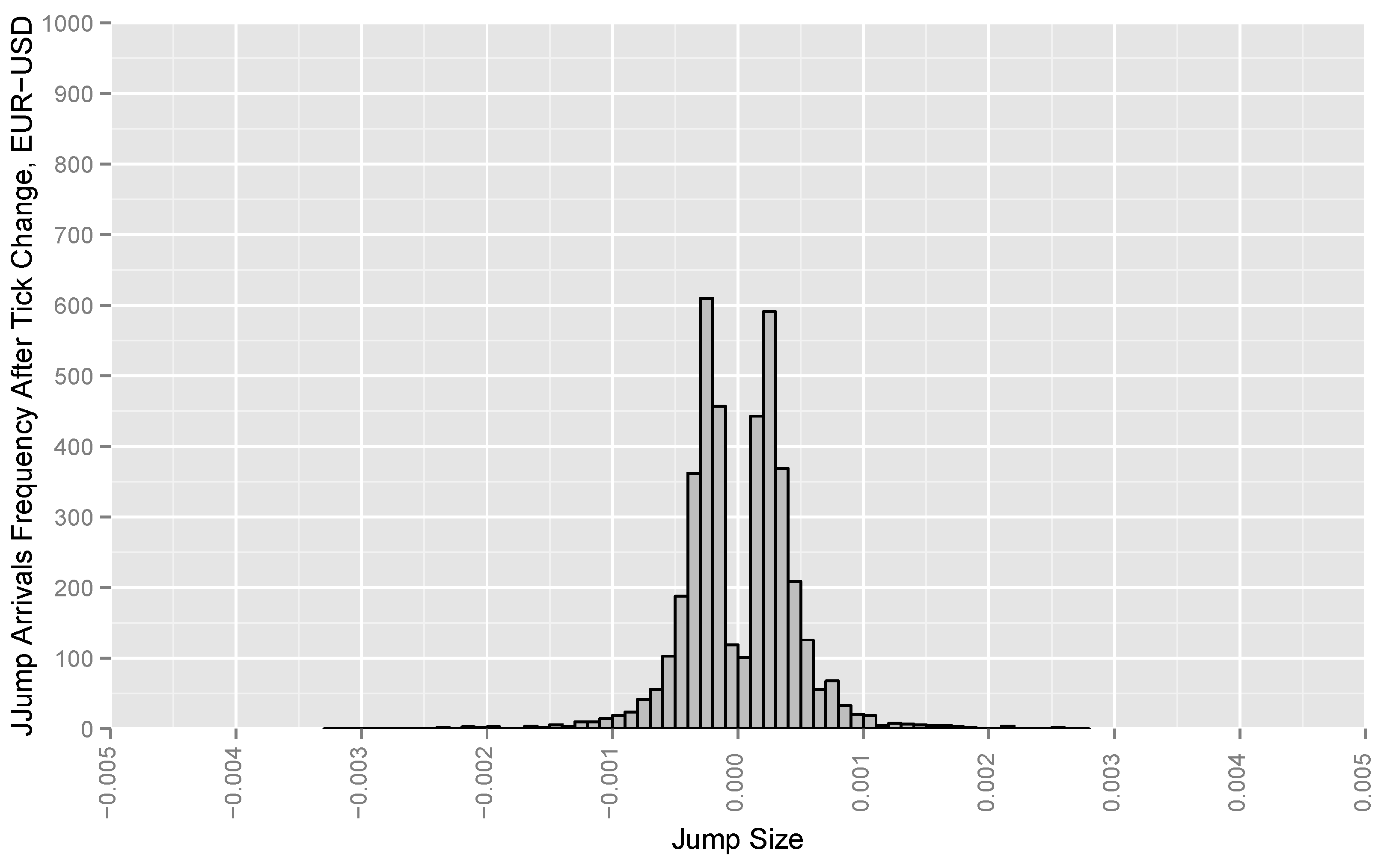

4.3.1. Jump Magnitudes

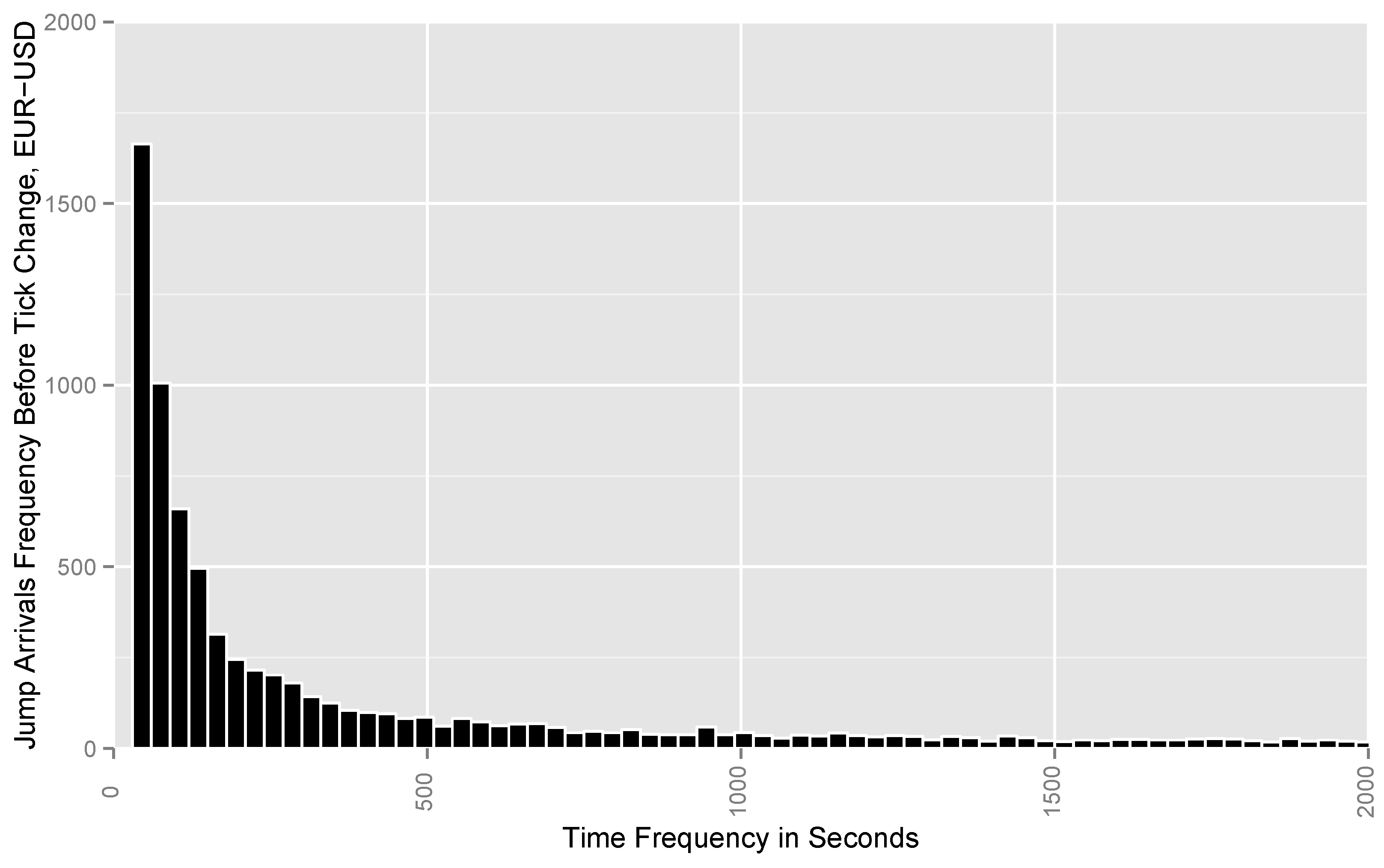

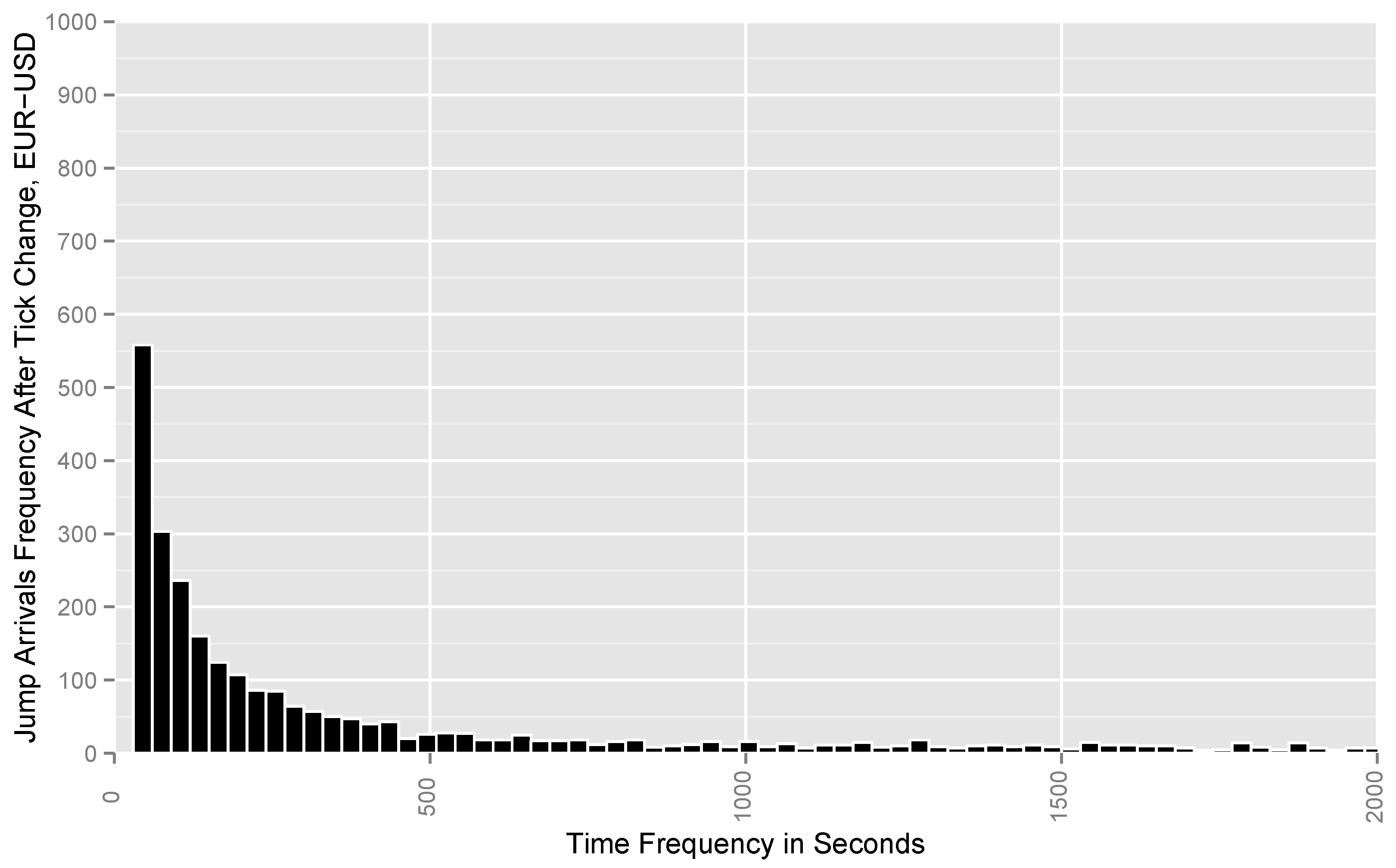

4.3.2. Jump Inter-Arrival Times

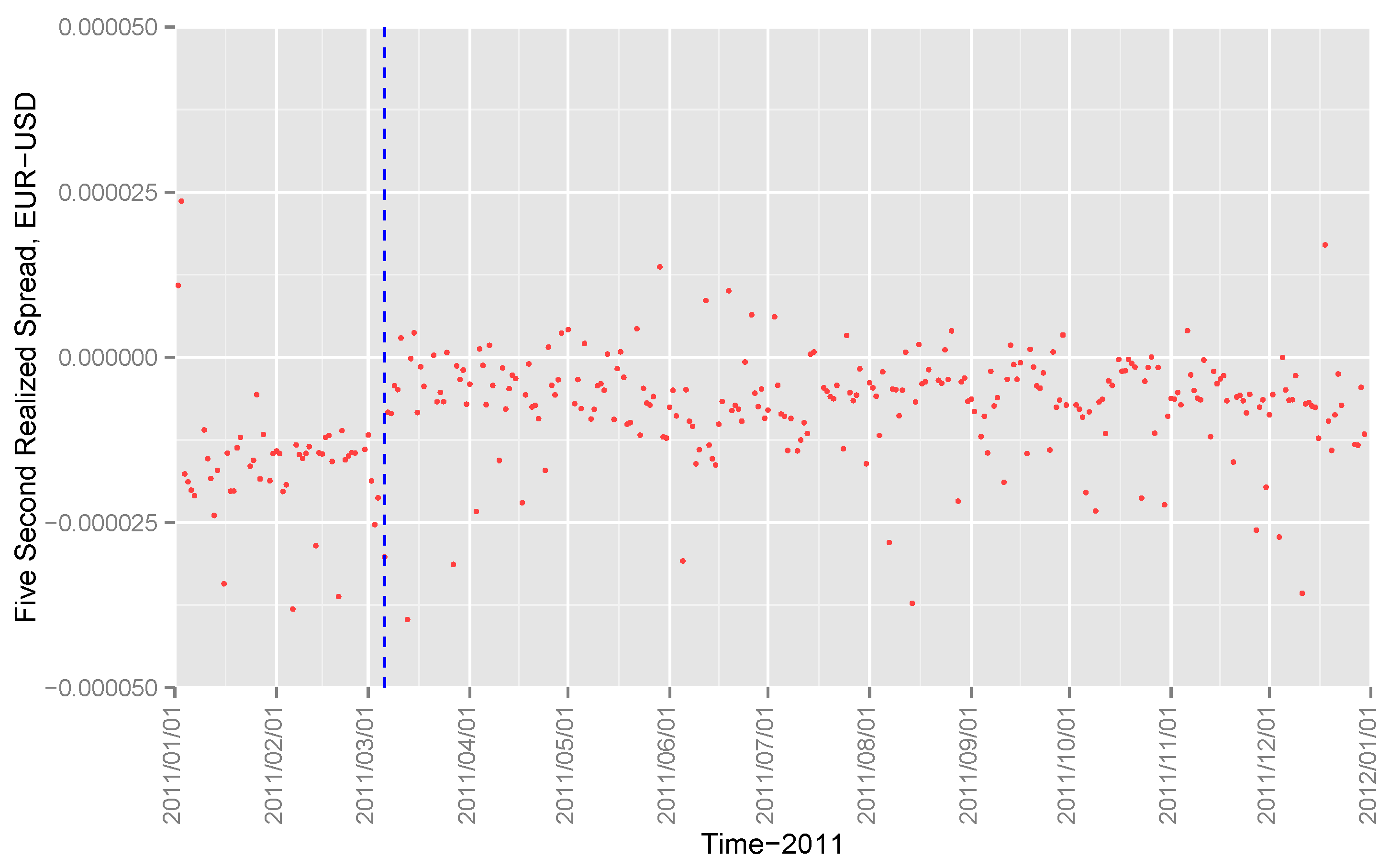

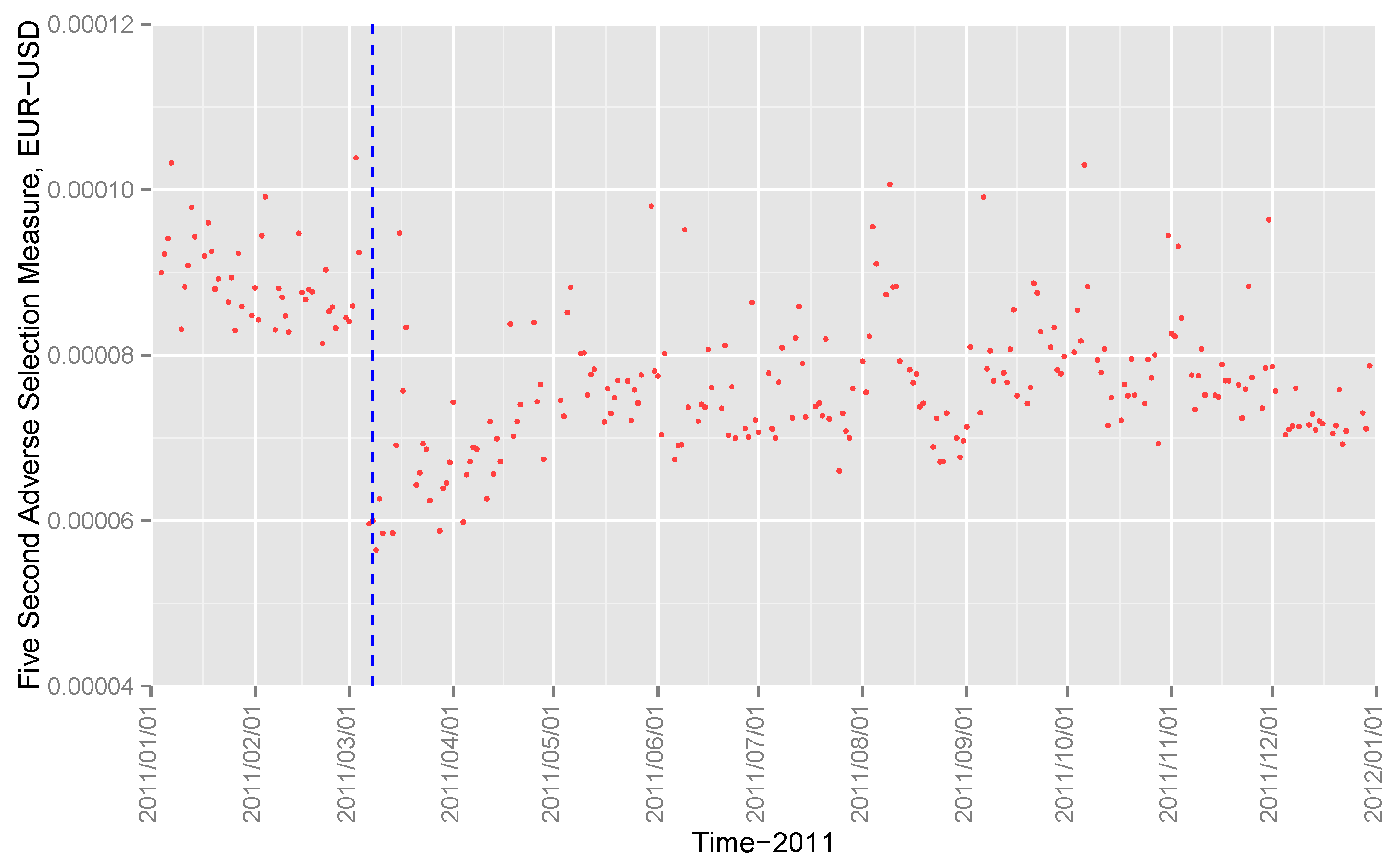

4.3.3. Realized and Effective Spreads

5. Discussion

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

| 1 | See Harrison and Kreps (1979) for the seminal discussion and Delbaen and Schachermayer (1994) for a contemporary treatment. |

| 2 | |

| 3 | Extending the martingale framework to incorporate information sharing via the social network is an interesting question and remains to be explored in future research. |

| 4 | Adaptedness with respect to an underlying filtration is assumed throughout. Similarly, stopping times are defined with respect to the underlying filtration. |

| 5 | For the dataset analyzed in Section 4.2, the minimum and average time-between-trades are 1 and s, respectively. See Lee and Hannig (2010) for a jump test that allows for infinite activity, with small Lèvy jumps. |

| 6 | |

| 7 | |

| 8 | This is also true for the FX data analyzed in Section 4.2. |

| 9 | By Itô isometry, . |

| 10 | In our specific case, we chose to sample at regular time intervals. Therefore, the stopping times are, in fact, deterministic. |

| 11 | Boudt et al. (2011) shows that the bipower variation estimator of Equation (2) can be made robust with respect to periodicity by filtering the computed returns using Weighted Standard Deviation (WSD) or Truncated Maximum Likelihood (TML). For the WSD filter, the weights depend on the value of the standardized return divided by the periodicity estimate. For the Truncated Maximum Likelihood (TML) estimator, introduced by Marazzi and Yohai (2004), zero weight is given to observations that are outliers according to the value of the ML loss function. In our empirical application, this periodicity-robust improvement leads to no material difference being detected in the estimated jumps. This is because, in the semimartingale model of Equation (1), the periodicity enters into the finite-variation, or drift, component . In our ultra-high-frequency setting, the drift component is negligible. Peridocity bias were observed at a lower frequency (e.g., the five-minute frequency of Boudt et al. (2011)) was not observed in our setting. |

| 12 | See, for example, the BIS report: http://www.bis.org/publ/rpfx10.pdf (accessed on 15 December 2021). |

| 13 | FX market customarily lists base currency first. For example, EUR/USD is read as “US dollar per Euro”. |

| 14 | The spot market makes up 37% of the global FX market daily turnover of 1.5 trillion USD, and 35% of this volume are interdealer trades. See the report by the Bank for International Settlements (BIS): http://www.bis.org/publ/rpfx13fx.pdf (accessed on 15 December 2021). |

| 15 | Results on the other major currency pairs do not qualitatively differ from EUR/USD and are available upon request. |

| 16 | “Pip“ is abbreviation for Price Increment Point. |

| 17 | The hourly averages of realized volatility and bipower variation were computed over our two-year sample. |

| 18 | Non-serial correlation is weaker than the martingale property. Therefore, a rejection of the no-serial correlation null hypothesis is a rejection of the martingale hypothesis. |

| 19 | While the customary choice of lag s of realized spread is 5 min (e.g., Hendershott et al. (2011)), this was not appropriate in our high-frequency setting. According to our analysis in Section 4.2, the microstructure effect ceased to be present at frequencies lower than 30 s. Our computation shows that the realized spread exhibited the same behavior across tick size changes at all frequencies higher than 30 s, that is, under different degrees of microstructure effect. The same remarks apply to the effective spread and adverse selection proxy. |

| 20 | See http://www.ebs.com/access-methods/ebs-workstation.aspx (accessed on 15 December 2021) for details on EBS workstations provided to Manual Traders. |

| 21 | See http://www.ebs.com/access-methods/ebs-ai.aspx (accessed on 15 December 2021) for details on EBS interface technology for automated trading. EBS estimates that around 30%-35% of the volume on its trading platform is driven by high-frequency market makers. |

| 22 | |

| 23 | Considerations of the full limit order book include, for example, translating the bid-ask spread price impact regression Huang and Stoll (1997) to the semi-martingale setting. This would for allow the analysis of the price impact of small orders, complementing the analysis of large orders presented in this paper. |

References

- Aït-Sahalia, Yacine, and Jean Jacod. 2009. Estimating the degree of activity of jumps in high frequency data. Annals of Statistics 37: 2202–44. [Google Scholar] [CrossRef] [Green Version]

- Amihud, Yakov. 2002. Illiquidity and stock returns: Cross-section and time-series effects. Journal of Financial Markets 5: 31–56. [Google Scholar] [CrossRef] [Green Version]

- Andersen, Torben G., Tim Bollerslev, and Dobrislav Dobrev. 2007a. No-arbitrage semi-martingale restrictions for continuous-time volatility models subject to leverage effects, jumps and i.i.d. noise: Theory and testable distributional implications. Journal of Econometrics 138: 125–80. [Google Scholar] [CrossRef] [Green Version]

- Andersen, Torben G., Tim Bollerslev, and Francis X. Diebold. 2007b. Roughing it up: Including jump components in the measurement, modeling, and forecasting of return volatility. Review of Economics and Statistics 89: 701–20. [Google Scholar] [CrossRef]

- Andersen, Torben G., Tim Bollerslev, Per Frederiksen, and Morten Ørregaard Nielsen. 2010. Continuous-time models, realized volatilities, and testable distributional implications for daily stock returns. Journal of Applied Econometrics 25: 233–61. [Google Scholar] [CrossRef] [Green Version]

- Barndorff-Nielsen, Ole E., and Neil Shephard. 2004. Power and bipower variation with stochastic volatility and jumps. Journal of Financial Econometrics 2: 1–37. [Google Scholar] [CrossRef] [Green Version]

- Barndorff-Nielsen, Ole E., and Neil Shephard. 2006. Econometrics of testing for jumps in financial economics using bipower variation. Journal of Financial Econometrics 4: 1–30. [Google Scholar] [CrossRef]

- Boudt, Kris, Christophe Croux, and Sébastien Laurent. 2011. Robust estimation of intraweek periodicity in volatility and jump detection. Journal of Empirical Finance 18: 353–67. [Google Scholar] [CrossRef]

- Brogaard, Jonathan, Terrence Hendershott, and Ryan Riordan. 2014. High-frequency trading and price discovery. Review of Financial Studies 27: 2267–306. [Google Scholar] [CrossRef] [Green Version]

- Cai, Jie, Ralph A. Walkling, and Ke Yang. 2016. The price of street friends: Social networks, informed trading, and shareholder costs. Journal of Financial and Quantitative Analysis 51: 801–37. [Google Scholar] [CrossRef] [Green Version]

- Chaboud, Alain, Benjamin Chiquoine, Erik Hjalmarsson, and Clara Vega. 2014. Rise of the machines: Algorithmic trading in the foreign exchange market. Journal of Finance 69: 2045–84. [Google Scholar] [CrossRef] [Green Version]

- Delbaen, Freddy, and Walter Schachermayer. 1994. A general version of the fundamental theorem of asset pricing. Mathematische Annalen 300: 463–520. [Google Scholar] [CrossRef]

- Durlauf, Steven N. 1991. Spectral based testing of the martingale hypothesis. Journal of Econometrics 50: 355–76. [Google Scholar] [CrossRef] [Green Version]

- Fama, Eugene F. 1970. Efficient market hypothesis: A review of theory and empirical work. Journal of Finance 25: 28–30. [Google Scholar] [CrossRef]

- Fama, Eugene F. 1991. Efficient markets: Ii. fiftieth anniversary invited paper. Journal of Finance 46: 1575–617. [Google Scholar] [CrossRef]

- Gu, Chen, and Alexander Kurov. 2020. Informational role of social media: Evidence from twitter sentiment. Journal of Banking and Finance. [Google Scholar] [CrossRef]

- Gwilym, Owain, Andrew Clare, and Stephen Thomas. 1998. Extreme price clustering in the London equity index futures and options markets. Journal of Banking & Finance 22: 1193–206. [Google Scholar]

- Harrison, J. Michael, and David M Kreps. 1979. Martingales and arbitrage in multiperiod securities markets. Journal of Economic Theory 20: 381–408. [Google Scholar] [CrossRef]

- Hasbrouck, Joel, and Gideon Saar. 2013. Low-latency trading. Journal of Financial Markets 16: 646–79. [Google Scholar] [CrossRef]

- Hendershott, Terrence, Charles M. Jones, and Albert J. Menkveld. 2011. Does algorithmic trading improve liquidity? Journal of Finance 66: 1–33. [Google Scholar] [CrossRef] [Green Version]

- Huang, Roger D., and Hans R. Stoll. 1997. The components of the bid-ask spread: A general approach. Review of Financial Studies 10: 995–1034. [Google Scholar] [CrossRef]

- Huang, Roger D., and Hans R. Stoll. 2001. Tick size, bid-ask spreads, and market structure. The Journal of Financial and Quantitative Analysis 36: 503–22. [Google Scholar] [CrossRef] [Green Version]

- Jing, Wei, and Xueyong Zhang. 2021. Online social networks and corporate investment similarity. Journal of Corporate Finance 68: 101921. [Google Scholar] [CrossRef]

- Kyle, Albert S. 1985. Continuous auctions and insider trading. Econometrica 53: 1315–35. [Google Scholar] [CrossRef] [Green Version]

- Lawrence, Harris. 1991. Stock price clustering and discreteness. Review of Financial Studies 4: 389–415. [Google Scholar]

- Lee, Suzanne S., and Jan Hannig. 2010. Detecting jumps from lévy jump diffusion processes. Journal of Financial Economics 96: 271–90. [Google Scholar] [CrossRef] [Green Version]

- Lee, Suzanne S., and Per A. Mykland. 2008. Jumps in financial markets: A new nonparametric test and jump dynamics. Review of Financial Studies 21: 2535–63. [Google Scholar] [CrossRef]

- Marazzi, Alfio, and Victor J Yohai. 2004. Adaptively truncated maximum likelihood regression with asymmetric errors. Journal of Statistical Planning and Inference 122: 271–91. [Google Scholar] [CrossRef]

- O’Hara, Maureen. 2015. High frequency market microstructure. Journal of Financial Economics 116: 257–70. [Google Scholar] [CrossRef]

- Ohta, Wataru. 2006. An analysis of intraday patterns in price clustering on the Tokyo Stock Exchange. Journal of Banking & Finance 30: 1023–39. [Google Scholar]

- Schmidt, Anatoly B. 2012. Ecology of the Modern Institutional Spot FX: The EBS Market in 2011. SSRN. Available online: http://ssrn.com/abstract=1984070 (accessed on 15 December 2021).

- White, Halbert. 2014. Asymptotic Theory for Econometricians. Cambridge: Academic Press. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Jump Time Series | Before | After |

| Durlauf Test | ||

| Box-Ljung Test | ||

| Box-Pierce Test | ||

| Durbin-Watson Test | ||

| Inter-Arrival Times | Before | After |

| Daily average number of jumps | 33 | 20 |

| Arrival intensity (exponential fit) | ||

| Autoregressive order | 27 | 2 |

| Jump Sizes | Before | After |

| Mean | ||

| Standard deviation | ||

| Skewness | ||

| Kurtosis | ||

| Mira symmetry Test |

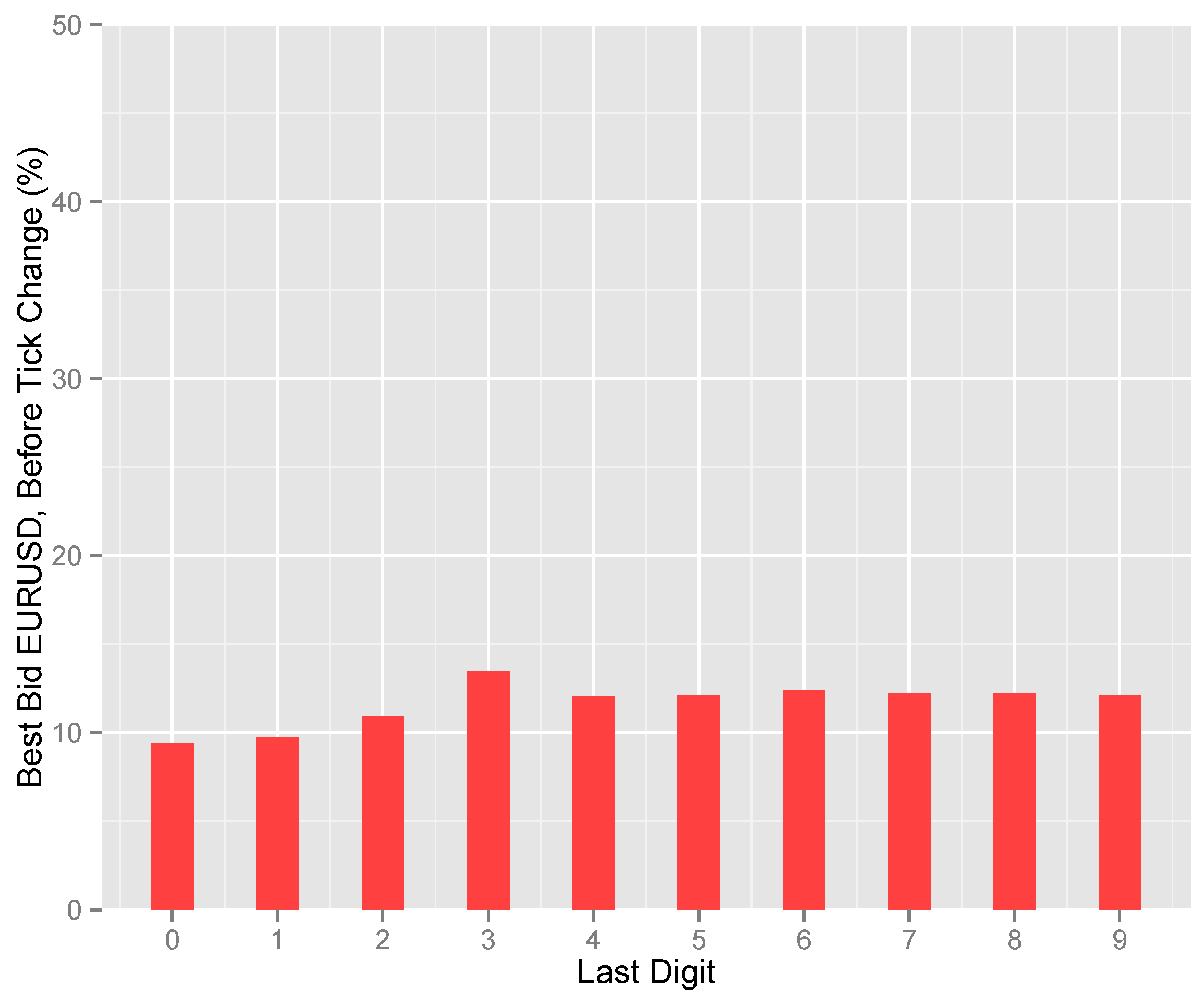

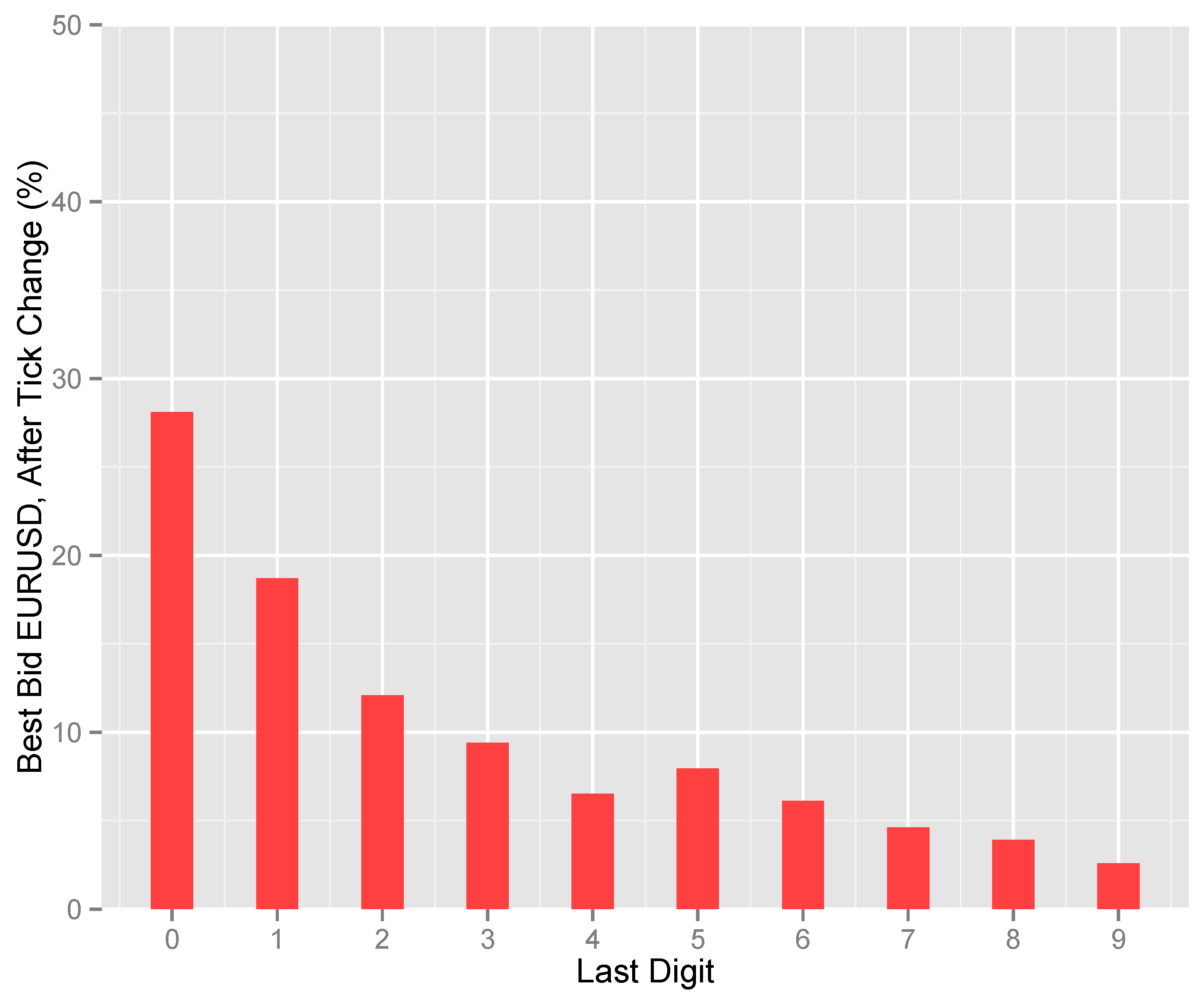

| Last digit of quoted price | 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

| Before tick size change | 1.59 | 1.43 | 1.57 | 1.52 | 1.54 | 1.61 | 1.54 | 1.60 | 1.50 | 1.41 |

| After tick size change | 2.12 | 1.06 | 1.05 | 1.08 | 1.08 | 1.58 | 1.05 | 1.01 | 1.07 | 1.10 |

| Last digit of quoted price | 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

| Before tick size change | 1.53 | 1.32 | 1.62 | 1.59 | 1.45 | 1.54 | 1.53 | 1.54 | 1.43 | 1.48 |

| After tick size change | 2.19 | 1.03 | 1.02 | 1.10 | 1.09 | 1.32 | 1.06 | 1.04 | 1.07 | 1.09 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tseng, M.C.; Mahmoodzadeh, S. Information Jumps, Liquidity Jumps, and Market Efficiency. J. Risk Financial Manag. 2022, 15, 97. https://doi.org/10.3390/jrfm15030097

Tseng MC, Mahmoodzadeh S. Information Jumps, Liquidity Jumps, and Market Efficiency. Journal of Risk and Financial Management. 2022; 15(3):97. https://doi.org/10.3390/jrfm15030097

Chicago/Turabian StyleTseng, Michael C., and Soheil Mahmoodzadeh. 2022. "Information Jumps, Liquidity Jumps, and Market Efficiency" Journal of Risk and Financial Management 15, no. 3: 97. https://doi.org/10.3390/jrfm15030097