1. Introduction

As a significant indicator of globalization, foreign direct investment (FDI) has become a pivotal stimulant to boost domestic investment and growth (

Ndikumana and Verick 2008). The inward and outward FDI flows help to enhance people’s income, investments/assets, and overall development (

Sylwester 2005). Theoretically, the inward FDI substitutes domestic investment if the external firms finance similar enterprises and the local firms discontinue their businesses. This occurs because foreign firms are more contesting and are equipped with up-to-date technology (

Chen et al. 2017). In addition, if foreign companies finance their enterprises from the host economy’s capital markets, it decreases the financial liquidity of the native investors. As a result, capital borrowing becomes more costly for the domestic investors to finance their firms (

Serrasqueiro 2017). Therefore, if foreign firms utilize local input factors in order to manufacture their complementary goods, it brings positive spillover effects and increases the domestic investment (

Ali et al. 2018).

The FDI outflow allows firms/companies to penetrate new markets, to import intermediary goods from foreign countries at lower costs, and to access overseas technology. Thus, the outward FDI benefits the domestic economy. In addition, the growing competition among investing companies carries production spillovers to the local firms (

Herzer 2010). However, considering the consequences of the outward FDI on domestic investment, the outward FDI decreases the likelihood of domestic investment as foreign investors transfer the scarce domestic financial resources to foreign investment (

Al-sadiq 2013). As a result, fewer funds remain for the local firms to invest.

On the other hand, by employing their investments, multinational enterprises (MNEs) benefit the host country by guaranteeing access to sophisticated overseas technologies and valuable input factors in manufacturing finished goods at lower costs (

Herzer 2010). Moreover, in some cases, the outward FDI substitutes foreign or regional productivity when firms move parts of their production mechanisms and industries to foreign countries. Therefore, external investment inexorably diminishes the domestic investment, the employment opportunities, the production, and, thus, the economic output. Moreover, the host economy’s development portfolio depends on rearward and forward connections with the MNEs (

Ali and Wang 2018).

Bangladesh has become one of the major forces in the world economy by effectively pursuing its trade liberalization policy since the 1980s (

Bashar and Khan 2007). This policy has brought massive opportunities for both inner and outer investors. More importantly, the government of Bangladesh has created various economic zones across the country to implement its policies, such as export processing zones (EPZs), special economic zones (SEZs), etc. In addition, the government has seen a substantial increase in FDI inflow due to several investments in power production and labor-intensive industries, such as readymade garments. As a result, Bangladesh witnessed a significant rise in FDI influx in 2018 and maintained its top place in South Asia by receiving a total of USD 3.61 billion (

UNCTAD 2018).

In 2019, Bangladesh’s FDI inflow fell by 56 percent (USD 1.6 billion), compared to USD 3.6 billion in 2018. In Bangladesh, the export-based apparel sector is still a significant FDI recipient, and the principal investor countries in this sector include China, Hong Kong, and South Korea. The total FDI stocks of the country were USD 16.4 billion in 2019. However, Bangladesh mainly receives FDI from China, South Korea, India, Egypt, the United Kingdom, the United Arab Emirates, and Malaysia (

UNCTAD 2019). Moreover, major developed Asian economies outsource the production from their factories, especially that of apparel products, to Bangladesh. As a result, Bangladesh ranks 168th out of 190 countries (

World Bank 2020). Apart from FDI inflows, Bangladeshi corporations and multinational corporations have invested worldwide. The FDI of Bangladesh to other nations increased more than thrice based on this country’s outbound FDI accounted for USD 170 million in 2017 (

UNCTAD 2018). More importantly, Bangladesh has been importing more raw materials and capital goods by utilizing the outbound FDI for the last two decades. Overall, the inward FDI flows witnessed an upward trend after the democratic era started in 1996, and it continued up until 2018, with noticeable fluctuations. However, the FDI outflows show an increasing trend from 2006 to 2018, with substantial changes that were similar to the FDI inflows.

Figure 1 documents the FDI inflow and outflow as a percentage of GDP ranging from 1990 to 2019 in Bangladesh.

The FDI inflows of Bangladesh mainly suffer from an abysmal and underdeveloped state affair, natural disasters, and socio-economic and political volatilities. Besides, the country faces some other barriers to attracting FDI, including a weak infrastructure, corruption, a lack of transparency, bureaucratic inefficiency and corruption, a vulnerable financial sector, a lack of export diversification and market orientation, and a hefty reliance on the garment sector (

UNCTAD 2019). Despite this, a strategically important location has been a considerable advantage for external investors to invest in Bangladesh. Potential domestic consumption and natural resources have also been important factors in attracting foreign investors. Moreover, the country’s government strengthens the private sector-based growth, which helps to preserve the foreign currency that is earned mainly from the remittance flows. Therefore, the central bank’s attempt is appropriate, as it ensures foreign currency transferability. It is also true that an open and diversified economic nature, a low-waged labor force, a strategic and competitive position in the global value chain, and a favorable economic and legislative environment for business are instrumental to enhancing the FDI inflows in Bangladesh (

Business France 2019).

The measures of different governments are favorable to increasing the FDI in Bangladesh. The country’s policymakers eagerly seek to attract FDI in the energy and infrastructure sectors. Many incentive programs, such as a trade policy framework, a growth strategy via exports, and a public–private partnership (PPP) scheme, have already been in place since 2009 (

Mengistu and Adhikary 2011). They also attempt to develop agro-based industrial products, leather-based footwear and related goods, software and ICT commodities, light engineering, pharmaceuticals, and shipbuilding by using internal processes and external potentials of diverse companies in order to reduce the heavy dependence on the textile-based industrial production. In addition, the economy has taken on several mega projects in order to provide infrastructure for foreign companies, such as a rail bridge and road over the Padma River and the Dhaka metro rail project (

Islam et al. 2022). Moreover, Bangladesh has signed 30 bilateral investment accords with different countries in order to create a favorable business climate for both internal and external investors (

UNCTAD 2019). However, such initiatives of the policymakers call for an empirical investigation in order to justify the efficiency of the FDI flows on the domestic investment and economic growth in Bangladesh.

Studies on the association between FDI and domestic investment have drawn much attention from policymakers concerning the growth in different economies (

Agosin and Machado 2005;

Prasanna 2010;

Wang 2010;

Tan et al. 2016;

Onaran et al. 2013;

Hanousek et al. 2021; and

Ndikumana and Verick 2008). However, the existing literature mainly highlights the effects of FDI on the domestic investment in the host economy, but there are very few studies on the nexus between the outward FDI and the domestic investment for the source economy (

Herzer and Schrooten 2008;

Goedegebuure 2006;

Tan et al. 2016). Similarly, most of the economic literature on Bangladesh depicts the positive, or somewhat ineffective, contribution of the inward FDI to the economic growth and the negative role of the outward FDI in the economic growth. Besides, no study has previously examined the effects of the decomposed measures of FDI, including the inward and outward FDI, on the domestic investment in Bangladesh.

This study contributes to the existing argument on the association between the FDI inflows (IDI) and the FDI outflows (ODI), and the domestic investment (DI), by utilizing annual time series data for Bangladesh over the period of 1976–2019. In addition, this study incorporates some control variables, such as per capita GDP growth, real interest rate, and institutional quality, which is measured by the level of the violation of political rights (VPR). More specifically, Bangladesh’s spectacular growth rate (of more than 6%) over the last two decades deserves the inclusion of the per capita GDP growth variable in this study’s model. Besides, in the case of Bangladesh, investors are somewhat reluctant to take out loans from the banks, despite the lower rate of real interest, as the volatile political circumstance impedes the investment process. Therefore, this situation requires examining the contribution of the real interest rates to the capital formation, i.e., the domestic investment flows. Finally, the bad governance emanates from the incumbents and some separate groups, making the state-circumstance antagonistic for business and investment. Therefore, this study considers the political terror scale as the proxy of the institutional quality in the estimation procedure. However, in the past, these variables have hardly been used by any other researcher on this topic in Bangladesh. Finally, this study improves the models of

Feldstein and Horioka (

1980) and

Feldstein (

1995) by adding the policy-relevant variable, namely the political terror scale that is proxied by the institutional quality.

For the empirical investigation, this study employs an augmented ARDL model, which was coined by

McNown et al. (

2018) and

Sam et al. (

2019), in order to explore the co-integrating nexus between the FDI flows and the domestic investment in Bangladesh. In addition, the dynamic ARDL simulations graph approach, which was developed by

Jordan and Philips (

2018), is also used to detect the counterfactual shocks to the independent variables (the inward and outward FDIs, the economic growth, the real interest rate, and the violation of political rights) and their impacts on the dependent variable (domestic investment) in both the long run and the short run. This study may be the first to use an augmented ARDL model to analyze the dynamic association among the variables and the dynamic ARDL simulations approach to measuring the counterfactual shocks (10% positive and negative) to the FDI flows and the other macroeconomic determinants and their impacts on the domestic investment in Bangladesh. Besides, for the ARDL bounds testing-based co-integration analysis, this study distinctively performs a

t-test for the lagged dependent variable and an

F-test for the lagged independent variables (

McNown et al. 2018;

Sam et al. 2019), along with the traditional

F-test for the overall model (

Pesaran et al. 2001). In addition, dummy variables have been used for the years in which structural breaks were detected. Furthermore, the ZA unit root test is utilized before implementing the augmented ARDL approach for co-integration. In the case of variable specification and methodology employment, this study represents more robust results on the nexus between the FDI flows and the domestic investment in Bangladesh. This study’s findings will provide helpful insights for policymakers and other stakeholders who are affiliated with the field of domestic and foreign investments. However, this study fills the research gaps by providing a solid understanding of the recurring debate on the efficiency of the FDI flows in Bangladesh under a new econometric framework.

2. Literature Review

The literature on foreign direct investment (FDI) mostly appears in investigating this indicator’s relationship with economic development from the standpoints of the endogenous and the neoclassical growth theories. According to the endogenous growth model, FDI stimulates economic growth by diffusing technology from the developed countries to the FDI recipient countries. Besides, the neoclassical growth framework reveals that inward FDI enhances the economic growth by raising both the quantity and the efficiency of investment (

Li and Liu 2005). However, the impact of the inward FDI on domestic investment (DI) is highly debatable in empirical investigations, but not in the theoretical literature (

Ali et al. 2019). Some argue that the IDI increases the DI, but other researchers opine to the contrary, demonstrating that the IDI decreases the DI (

Elheddad 2019). The existing literature also supports that the outward FDI (ODI) enhances the DI both positively and negatively. In addition, the inward FDI’s positive role in increasing the local firms’ ability to boost production by contesting with external companies and using up-to-date technologies crowds in the domestic investment (

Xu and Yuan 2012).

Utilizing macro data for OECD countries during the 1970s and 1980s,

Feldstein (

1995) found that more FDI outflows decrease the DI, while the inward FDI impacts the local investments positively while controlling some of the macroeconomic indicators of DI.

Andersen and Hainaut (

1998), utilizing data over the 1960s and 1990s, found that the outward FDI decreases the DI in the US, Germany, Japan, and the UK. When estimating the short- and long-term effects,

Herzer and Schrooten (

2008) found that outward FDI impacts German DI positively in the short runand negatively in the long run. Finally, the study of

Xu and Yuan (

2012) presents helpful insights by investigating the IDI–DI relationship in the Chinese economy. This study underlines that the government of China accepts a particular policy in order to allure foreign investors, which is helpful to increase the use of modern technology in creating competitive pressure on local firms. This positive mechanism of the inward FDI crowds in domestic investment. On the other hand,

Agosin and Machado (

2005),

Wang (

2010), and

Salim et al. (

2017) oppose that multinational enterprise (MNE) crowds-out domestic investment due to the lack of sophisticated technology usage and their mismanagement in a host economy.

The empirical literature on ODI–DI association is comparatively limited in the case of developing economies but abundant from the perspective of developed economies (

Li et al. 2016;

You and Solomon 2015; and

Al-sadiq 2013). Among others,

Desai et al. (

2005) found that ODI decreases the production cost of commodities as the production-related activities are conducted in association with both local and foreign companies. This mood of production-related activities promotes competition between the local and the external firms, stimulating domestic investment. The study results from

Desai et al. (

2005) are more or less supported by

Herzer and Schrooten (

2008), who opine that the ODI crowds in the DI in the US due to the utilization of technology importation via ODI. However, ODI crowds out because of the lack of technology spillover effects in Germany, utilizing time-series data within a bivariate model.

Al-sadiq (

2013) employed a panel data analysis technique for 121 developing economies from 1990 to 2010 and found that the outward FDI impacts the DI negatively. Utilizing Vietnamese firm-level data for 2001–2011,

Ni et al. (

2017) examined the differential impacts of external investors on the domestic investment in Vietnam. Overall, the findings revealed that foreign investors from Asian countries play a significantly positive role in the local firms, but North American investors have no significant effects on the DI. Finally, this study argues that investments from China and Taiwan affect the local firms significantly in Vietnam.

Ali et al. (

2019) found that both the IDI and the ODI have complementary effects on the domestic investment in the context of China.

Ali et al. (

2019) analyzed the impacts of the inward and outward FDI on the DI in China using annual time series data from 1982 to 2016. The study outcomes depict that inbound FDI substitutes the DI. At the same time, outbound FDI complements it, and the complementary effects of FDI outflows on domestic investment are higher than that of the FDI inflows in China.

Shah et al. (

2020) investigated the role of sectoral FDI on the DI in Pakistan during 1980–2012 by using the ARDL model. This study found that sectoral FDI crowds in the DI in Pakistan, and the study also concluded that the impact of aggregate FDI on domestic investment cannot be generalized.

The literature above highlights the positive and negative effects of the inward and outward FDI on domestic investment from the perspectives of different countries. In addition, some studies explore FDI’s complementary crowding-in and crowding-out effects on the domestic investment in diverse economies. A summary of the most significant and recent studies is shown in

Table 1. More importantly, no existing literature examines the relationship between the FDI and the domestic investment in Bangladesh. The effects of the decomposed measures of FDI (inward and outward FDI) on the domestic investment are also nonexistent in Bangladesh. Therefore, the current study is expected to contribute to the existing literature in a significant way by estimating the dynamic ARDL simulations model in order to investigate the actual changes in the inward and outward FDI on the domestic investment in Bangladesh.

3. Theoretical Framework

The effects of FDI in the host country have drawn significant attention from both academics and policymakers. Theoretically, FDI transfers both the physical capital and the intangible assets, including proper skills in technology and management (

Feldstein 1995). Some researchers have investigated the effects of inbound FDI on the recipient economy’s economic growth and domestic productivity. In addition, some economists have explored the influence of FDI inflow on the domestic investment (

Wang 2010). The current study extends the theoretical model that was coined by

Feldstein (

1995) in order to investigate the effect of the inward and outward FDIs on the domestic investment in the context of Bangladesh. The initial regression model that was measured by

Feldstein (

1995) can be expressed as follows:

where,

Ln denotes the natural logarithm,

DI represents the domestic investment,

IDI represents the inward FDI, ODI illustrates the outward FDI,

is an intercept term, and

corresponds to the error term. We transform all variables into logarithm form to avoid likely heteroscedasticity and linearize the model. Linearization of the model helps measure the elasticity coefficients of the variables efficiently, as the calculated coefficients contain the change in the percentage of the variables concerned (

Gujarati and Porter 2010).

Feldstein (

1995) developed this framework following

Feldstein and Horioka’s (

1980) model. As the FDI flow has been a significant predictor of domestic investment,

Feldstein (

1995) expanded this model to include IDI and ODI. Following

Ali et al. (

2019), the current study uses the gross domestic product (GDP) and the real interest rates (RIR) as control variables. Now, we can write the equation as follows:

The human rights issues of a country affect the institutional quality and become a significant factor in the movement of domestic investment. Hence, the present study also includes this variable, e.g., the violation of human rights proxied by the political terror scale (PTS), in order to measure the institutional quality. Therefore, the model can be specified in the following equation:

In our empirical model, Equation (2) includes the gross domestic product as GDP and the real interest rate as RIR with the initial specification appearing in Equation (1). Equation (3) is the final model that includes the institutional quality, which is determined by the violation of political rights (VPR).

This research also follows the earlier studies of

Adams (

2009),

Ullah et al. (

2014),

Wang (

2010),

Ivanović (

2015),

Szkorupová (

2015),

Tan et al. (

2016),

Ali and Mna (

2019),

Ali et al. (

2019), and

Shah et al. (

2020).

First, these researchers examined the influence of the inward FDI on the domestic investment.

Next,

Herzer and Schrooten (

2008),

Al-sadiq (

2013),

Tan et al. (

2016),

Ameer et al. (

2017), and

Ali et al. (

2019) analyzed the effect of the outward FDI on the domestic investment.

Then,

Adams (

2009),

Wang (

2010),

Ivanović (

2015),

Szkorupová (

2015),

Ullah et al. (

2014),

Ameer et al. (

2017), and

Ali et al. (

2019) investigated the impact of the economic growth on the domestic investment.

Wang (

2010), and

Ali et al. (

2019) examined the role of the real interest rates on the domestic investment.

Finally,

Adams (

2009) and

Ali et al. (

2019) inquired into the impact of the institutional quality, which was measured by the political terror scale (PTS), on the domestic investment.

6. Conclusions and Policy Recommendations

The underlying view of this research is that the FDI flows help to accelerate the movement of the domestic investment in developing economies, such as Bangladesh. In establishing this statement, this study aimed to investigate the effect of FDI flows (inward and outward FDI) on the domestic investment in Bangladesh over the period of 1976–2019. Using an augmented ARDL model approach, this study has scrutinized co-integrating associations among the variables. The shocks arising in the independent variables and their effects on the dependent variable have also been investigated and represented through simulation graphs utilizing the dynamic ARDL simulations approach in this study. The stationarity problem of the data was checked using ADF and ZA unit root tests. The test results indicate that the time series are stationary at I(0) and I(1), and none of the series are stationary at I(2). This stationarity status of the time series variables allows us to implement the augmented ARDL approach to co-integration and the dynamic ARDL simulations approach to measuring counterfactual shocks.

Within an augmented ARDL model framework, this study has additionally used a t-test for the lagged dependent variable and an F-test for the lagged independent variables, along with the traditional F-test for the overall model, in order to check for co-integration among the variables. Besides, the dummy for the ‘structural-break’ years using the ZA unit root test has also been utilized in the augmented ARDL approach to co-integration. For checking the normality, the heteroscedasticity, the autocorrelation, and the stability, different diagnostic tests (e.g., Jarque–Bera, Breusch–Pagan–Godfrey, ARCH, LM, and the CUSUM and CUSUM squares) are applied.

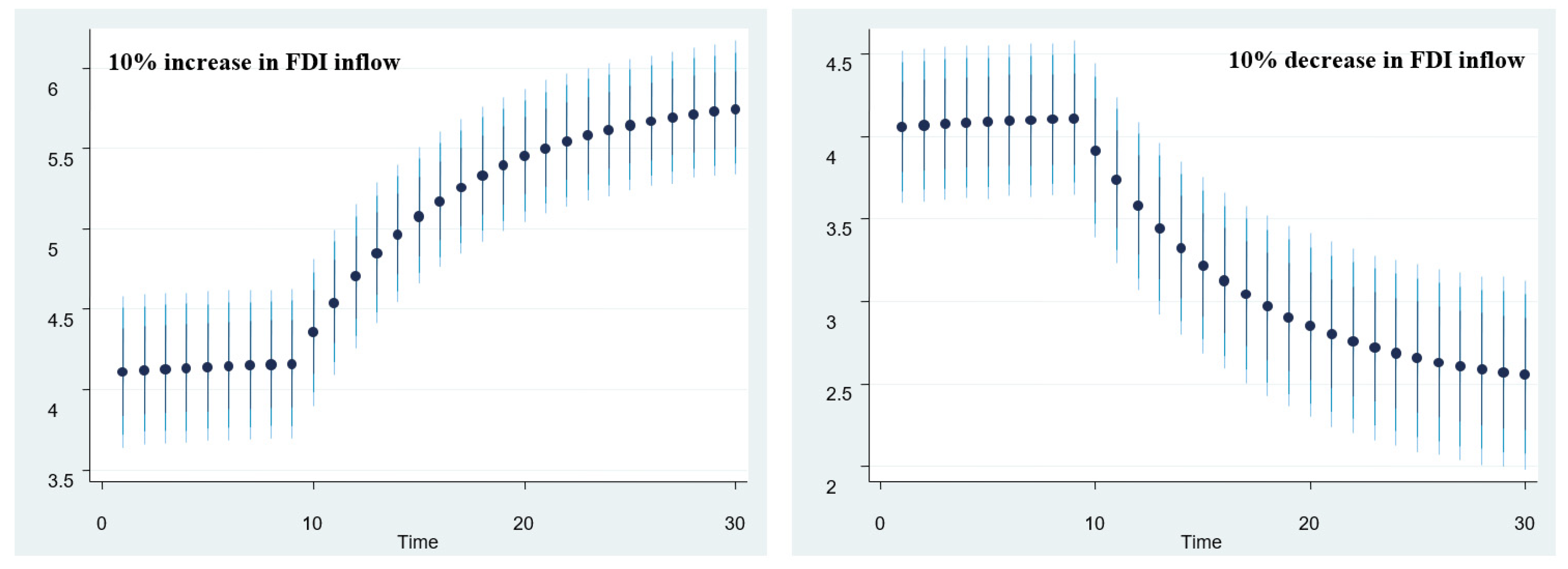

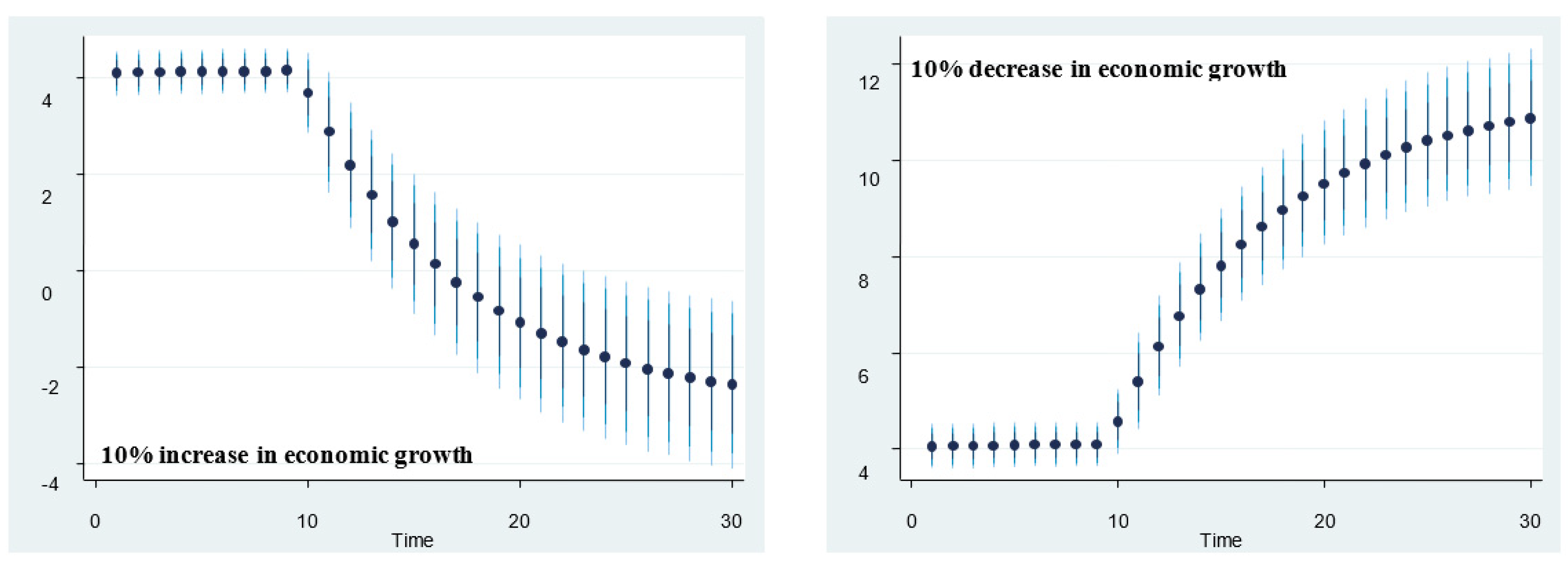

The investigated results that were obtained from the augmented ARDL model suggest that the inward FDI has a significantly positive effect on the domestic investment in both the short run and in the long run. At the same time, the outward FDI has no significant role in spurring domestic investment in both the long run and the short run. Besides, the long-run positive impacts of the inward FDI in both the 10% positive and the 10% adverse shocks that emerged from the dynamic ARDL simulations graph suggest that the inward FDI crowds in the domestic investment in Bangladesh. In addition, economic growth affects the domestic investment positively in the long run and in the short run in Bangladesh, whereas the real interest rate and the institutional quality, as measured by the scale of the violation of political rights (VPR), have no significant influence.

Since the 1980s, the trade liberalization policy of Bangladesh has opened the gateway for foreign firms to invest in the country. Therefore, Bangladesh-based enterprises/MNEs took this opportunity to penetrate the global arena in order to utilize their investments. As a result, this policy measure has somewhat led to a spectacular growth in Bangladesh’s FDI flows. However, as Bangladesh’s growth process is highly dependent on its formation of domestic capital, such capital inflows via FDI, which has a complementary effect on local investments. However, the capital outflow via outward FDI has been a concern of policymakers regarding its consequences on domestic investment. Against this backdrop, this paper has striven to respond to how Bangladesh’s domestic investment corresponds to its rising FDI inflow and outflow trend.

According to the results, this study argues that the Bangladesh government’s policy to attract foreign direct investment is pertinent, as the FDI inflow has contributed to the crowding-in effect on the domestic investment. The IDI has brought the local firms to the competition and has allowed them to utilize sophisticated technology in their production. The inward FDI has, thus, increased the local firms’ ability to spur domestic investment. The positive, but insignificant, effect of the ODI has become an issue for the policymakers of Bangladesh concerning the utilization of the ODI for domestic investment growth. It is also realistic to state that the negative impact of the ODI on the domestic investment in the short run is caused by the inadequate utilization of the ODI to import intermediary goods and purchase advanced technology from foreign countries. More importantly, the local firms’ inability to meet the demand for desired products has given room for foreign enterprises to invest in the host countries. However, this employment flow of external investments creates a barrier to exploiting the potential of internal investment channels/sources. Thus, the ODI has not contributed to stimulating the domestic investment in Bangladesh. The positive effect of economic growth on the domestic investment in Bangladesh shows the efficiency of the overall growth process to materialize the country’s vision to be a developed economy by 2041. Finally, the interest rates remain ineffective in impacting the domestic investment, whereas the violation of political rights takes part on an equal footing in Bangladesh.

Overall, the findings of this study imply that the IDI can energize local finance channels by investing in different government mega projects, such as Metrorail, bridge constructions, road constructions, and power plants for energy production. In this regard, the policymakers should formulate pragmatic policies to attract foreign investors in order to boost Bangladesh’s domestic investment. In addition, a national open-door policy would also be more conducive to foreign investors. The potential of the outward FDI flow is critical to strengthening the value-added industry by utilizing technology diffusion. Moreover, the inward FDI may fuel the domestic investment activities by improving the positive spillovers of technology and new outputs. This ultimately fortifies the local firms’ ability to increase production and sustain domestic investment growth.

This study has some limitations. First, this study does not integrate ‘trade’ and ‘net savings’ variables into its (study) model. Secondly, this research covers data ranging from 1976 to 2019 and excludes some recent years, including 2020, 2021, and 2022, which is another shortcoming of this investigation. Therefore, the extant drawbacks of this study require further research by adding ‘trade’ and ‘net savings’ variables to this study’s model with an up-to-date data span.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}