Efficient Pricing of Spread Options with Stochastic Rates and Stochastic Volatility

Abstract

:1. Introduction

2. The Two-Asset Heston–Hull–White Model

3. The Result of Grzelak and Oosterlee

4. The Two-Asset Heston–Hull–White Characteristic Function

5. The Result of Hurd and Zhou Extended

| Algorithm 1 2D FFT Algorithm |

|

6. Numerical Results

6.1. Implementation Testing

6.2. Convergence

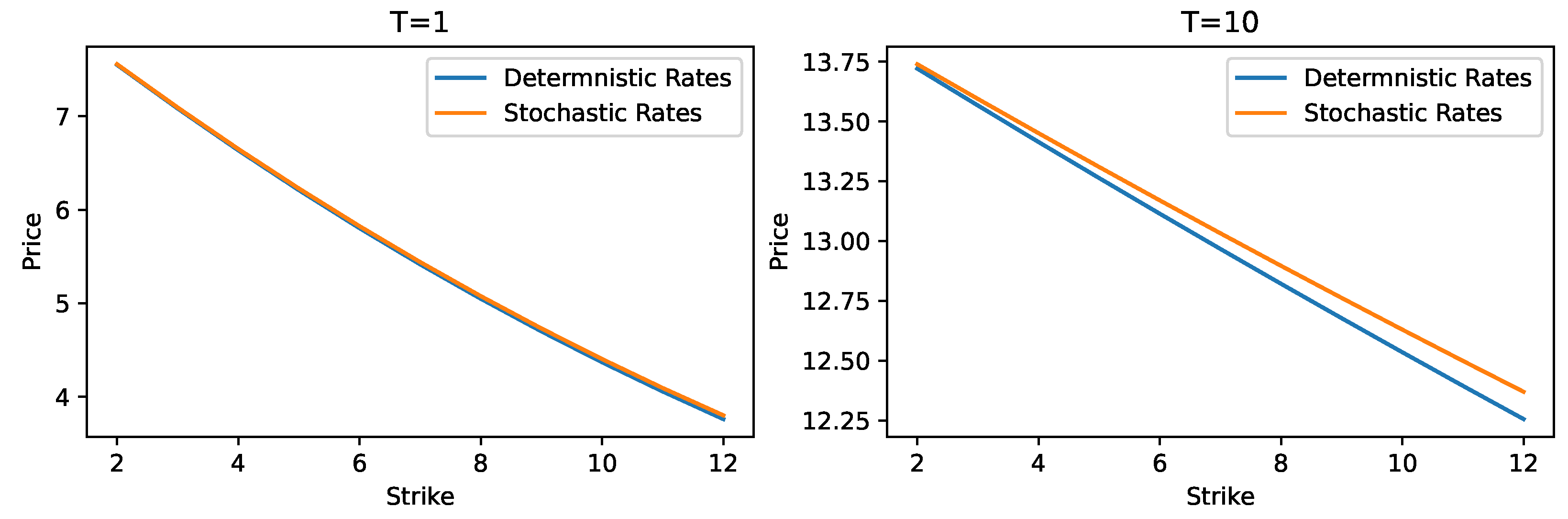

6.3. Impact of Stochastic Interest Rates

7. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Alam, Md. Mahmudul, and Gazi Uddin. 2009. Relationship between Interest Rate and Stock Price: Empirical Evidence from Developed and Developing Countries. International Journal of Business and Management 4: 43–51. [Google Scholar] [CrossRef] [Green Version]

- Alfeus, Mesias, and Erik Schlögl. 2018. On Numerical Methods for Spread Options. Research Paper Series 388; Sydney: Quantitative Finance Research Centre, University of Technology. [Google Scholar]

- Carr, Peter, and Dilip Madan. 1999. Option valuation using the fast Fourier transform. Journal of Computational Finance 2: 61–73. [Google Scholar] [CrossRef] [Green Version]

- Cox, John C., Jonathan E. Ingersoll Jr, and Stephen A. Ross. 1985. A Theory of the Term Structure of Interest Rates. Econometrica 53: 61–73. [Google Scholar] [CrossRef]

- Dempster, Michael Alan Howarth, and SS George Hong. 2002. Spread option valuation and the fast Fourier transform. In Mathematical Finance-Bachelier Congress 2000. Berlin/Heidelberg: Springer, pp. 203–220. [Google Scholar]

- Duffie, Darrell, Jun Pan, and Kenneth Singleton. 2000. Transform Analysis and Asset Pricing for Affine Jump-Diffusions. Econometrica 68: 1343–76. [Google Scholar] [CrossRef] [Green Version]

- Grzelak, Lech Aleksander. 2011. Equity and Foreign Exchange Hybrid Models for Pricing Long-Maturity Financial Derivatives. Ph.D. thesis, Delft University of Technology, Delft, The Netherlands. [Google Scholar]

- Grzelak, Lech A., and Cornelis W. Oosterlee. 2011. On the Heston Model with Stochastic Interest Rates. SIAM Journal on Financial Mathematics 2: 255–86. [Google Scholar] [CrossRef] [Green Version]

- Heston, Steven L. 1993. A Closed-Form Solution for Options with Stochastic Volatility with Applications to Bond and Currency Options. The Review of Financial Studies 6: 327–43. [Google Scholar] [CrossRef] [Green Version]

- Hull, John, and Alan White. 1990. Pricing Interest-Rate-Derivative Securities. The Review of Financial Studies 3: 573–92. [Google Scholar] [CrossRef] [Green Version]

- Hurd, Thomas R., and Zhuowei Zhou. 2010. A Fourier transform method for spread option pricing. SIAM Journal on Financial Mathematics 1: 142–57. [Google Scholar] [CrossRef]

- Kammeyer, Holger, and Joerg Kienitz. 2012. The Heston-Hull-White Model Part I: Finance and Analytics. Wilmott Magazine 2012: 46–53. [Google Scholar] [CrossRef]

- Roberts, Jessica Ellen. 2018. Fourier Pricing of Two-Asset Options: A Comparison of Methods. Master’s thesis, University of Cape Town, Cape Town, South Africa. Available online: http://hdl.handle.net/11427/28126 (accessed on 25 February 2022).

{kind=link}

{kind=link}

{kind=link}

| Strike | Hurd and Zhou Price | Model Price | Absolute Difference | Relative Difference |

|---|---|---|---|---|

| 2.0 | 7.548502 | 7.549344 | 0.000842 | 0.011155% |

| 2.2 | 7.453536 | 7.454381 | 0.000845 | 0.011337% |

| 2.4 | 7.359381 | 7.360137 | 0.000756 | 0.010273% |

| 2.6 | 7.266037 | 7.266787 | 0.000749 | 0.010308% |

| 2.8 | 7.173501 | 7.174295 | 0.000794 | 0.011069% |

| 3 | 7.081775 | 7.082660 | 0.000885 | 0.012497% |

| 3.2 | 6.990857 | 6.991678 | 0.000821 | 0.011744% |

| 3.4 | 6.900745 | 6.901351 | 0.000606 | 0.008782% |

| 3.6 | 6.811440 | 6.812176 | 0.000736 | 0.010805% |

| 3.8 | 6.722939 | 6.723817 | 0.000878 | 0.013060% |

| 4.0 | 6.635242 | 6.635881 | 0.000639 | 0.009630% |

| N | FFT Price | FFT Price | FFT Price | Time (seconds) |

|---|---|---|---|---|

| 4 | 4.354906 | 6.532359 | 8.709812 | 0.012491 |

| 8 | 1.488913 | 2.233370 | 2.977827 | 0.013598 |

| 16 | 0.697647 | 1.046470 | 1.395293 | 0.041658 |

| 32 | 0.450374 | 0.675562 | 0.900749 | 0.059231 |

| 64 | 0.936496 | 1.404743 | 1.872991 | 0.206991 |

| 128 | 7.553730 | 7.087006 | 6.640188 | 0.787242 |

| 256 | 7.549344 | 7.082660 | 6.635881 | 3.233390 |

| 512 | 7.549344 | 7.082660 | 6.635881 | 12.481379 |

| 1024 | 7.549344 | 7.082660 | 6.635881 | 50.788263 |

| 2048 | 7.549344 | 7.082660 | 6.635881 | 203.205588 |

| 4096 | 7.549344 | 7.082660 | 6.635881 | 817.879709 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Levendis, A.; Maré, E. Efficient Pricing of Spread Options with Stochastic Rates and Stochastic Volatility. J. Risk Financial Manag. 2022, 15, 504. https://doi.org/10.3390/jrfm15110504

Levendis A, Maré E. Efficient Pricing of Spread Options with Stochastic Rates and Stochastic Volatility. Journal of Risk and Financial Management. 2022; 15(11):504. https://doi.org/10.3390/jrfm15110504

Chicago/Turabian StyleLevendis, Alexis, and Eben Maré. 2022. "Efficient Pricing of Spread Options with Stochastic Rates and Stochastic Volatility" Journal of Risk and Financial Management 15, no. 11: 504. https://doi.org/10.3390/jrfm15110504