1. Introduction

A wide definition of basic education (foundation skills) includes all competences required for orientation in society. In a modern society, financial issues constitute an essential part of basic education: social risks and the responsibility to cover oneself financially have been individualized in almost all countries in recent years. Individual action in the daily increase of financially oriented situations therefore has a high significance for the entire well-being of a society (

Aprea 2012, p. 1;

Schürz and Weber 2005;

Buch 2017, p. 5). In addition to this, related to society as a whole, the significance of financial literacy has also increased. This is closely linked to the fact that people are increasingly confronted with online-based services in financially related fields. Especially in the banking sector, local branches are increasingly closing and online banking has been extended extensively in the last years (

Servon and Kaestner 2008; see

Gup and Agrrawal (

1994) for an impression of how trends in the bansking sector evolve over a long period of time). In contrast to financial affairs being settled with the help of a bank advisor, the use of online banking places high demands on the users: the self-determination of the usage and the variety of online services increase the complexity of the offers and of the access (

Featherman et al. 2010). Thus, these offers are accompanied by more responsibility for the individual’s decisions. Lusardi emphasizes the fact that the financial services offered have become more complex in this vein (

Lusardi 2019; see also

Lusardi and Mitchell 2014). As a result, financial literacy looms large in the digitized everyday life of individuals and constitute an essential part of basic knowledge. Due to the fact that the socio-economic environment of financially related decision-making has drastically changed over the last years, the overall goal of basic education, which is the safeguarding of participation for all members of society, becomes increasingly difficult to achieve across generations.

This assumption can be portrayed by means of the progressive use of online banking and the range of available online service offers in Germany (a trend denoted as Fintech (

Morgan 2022)) as well as by inflation processes. By now, more than 38 percent of Germans exclusively use online banking for transactions and 46 percent primarily rely on online banking (

Statista 2022a). According to a study conducted by Bitkom, this trend can be identified across age groups. Whilst 97 percent of Germans between the age of 16 and 29 used online banking on a regular basis in 2021, the number of equivalent answers of the respondents aged between 30 and 49 is almost the same (96 percent) (

Statista 2022b). If the individual’s contact to banks is increasingly shifted to the online world and if banks further expand their offers of online-based services for information collection and contract conclusion, the individual’s financial literacy is of vital importance in order to be able to benefit from the digitization-driven advantages. Benefits such as being able to inform themselves about loan interest, loan periods, installments or investment and financial products, as well as being able to calculate their potential pension gap and to compare different investment strategies with each other can only be realized by individuals if they are able to apply the respective services to their life situation. In addition, an increasing number of financial products which are exclusively offered online intensifies the need for sound financial literacy amongst individuals.

Furthermore, the uncertainties concerning the currency stability are reason enough to reflect upon the current and future financial situation and to draw conclusions from this for the situation of individuals. Worldwide inflation processes have immediate effects on financial investments and financing options; individuals with insufficient financial literacy cannot anticipate, let alone consider in their financial decisions. It is necessary that people are capable of acting in a financially independent way, making decisions, evaluating financial products and counselling, and handling financial instruments for information collecting, as well as for the carrying out of actions in daily life (e.g., the operation of a cash dispenser). From this perspective, basic education consists of various skills, for instance literacy, numeracy, problem solving, the handling of technical appliances and money management, as well as health-conscious conduct, in particular, with respect to sanitation and nutrition. Individuals of a society need to have basic competences that enable them to operate independently and autonomously within their environment and must, hence, possess a literacy which makes them responsible members of society that are able to act circumspectly. In conjunction with basic education, participation means that humans—individuals, population groups, organizations, unions and parties—are free and capable of taking a stake in all decision-making with an impact on their lives. Participation is conducive to exhibiting and accomplishing peoples’ interests (empowerment). Furthermore, it implies that people contribute their experiences and their ethic values to common enterprises, thus, appropriating these enterprises and taking responsibility for their outcome (ownership). The question that arises in this context comprises the literacy term and what connects this concept with the foundation skills in order to make literacy quantifiable and to identify individual competences.

In order to derive a definition of financial literacy that forms the basis for the study, we start with a narrow interpretation of basic education. A narrow definition of basic education only associates basic education/literacy with the problem of (functional) illiteracy and criticizes the “metaphorical“ use of the term literacy. According to the critics, this leads to a devaluation of the term (

Kress 1997, p. 115). The term “functional illiteracy” is used when—despite school attendance—a person is not able to apply his or her linguistic competence in his or her daily life or working life because the competence level is not high enough. Opposed to this, the term illiteracy in a strict sense is used when a person has never learned how to read or write. This especially applies to the so-called developing countries. According to the Level One Survey, 14% of the German population (7.5 million people) were on Alpha Level 1–3 in 2011 and are therefore affected by functional illiteracy (

Grotlüschen and Riekmann 2011). In 2018, this number slightly decreased to 6.2 million people being affected by functional illiteracy (

Grotlüschen and Buddeberg 2019).

With regard to this narrow definition, a term such as “Financial Literacy” takes away the constituent core of the term literacy in the actual sense. However, it can be argued that this risk only exists if one fails to put literacy in concrete terms within the respective context. Therefore, we will take a wide definition of literacy as a basis (

UNESCO Institute for Education 2006, p. 13). Within one culture, there are many different literacies in different areas of life (

Barton and Hamilton 2000, p. 9). Literacy (and also functional illiteracy) are subject to change over time. Whilst in the 19th century it might have been enough to be able to write one’s own name, the requirements have fundamentally changed due to social and economic change and the increased demands that they entail. For instance, in the context of digitization, the concept of a data literacy education has joined the scientific discourse on literacy-related concepts (e.g.,

Ridsdale et al. 2015). Furthermore, “literacy” is no globally determined value, but it always refers to a specific segment of society. This means that for different occupations, and in different environments, different competences are needed (

Rammstedt 2013).

In European societies, literacy is not only limited to reading, writing and calculating skills but also requires a certain level of media literacy and financial literacy in order for adults to be able to participate fully extensively in social life. Basic education implies the competences, which are adequate for the target audience to participate in their various living environments (

Basic Skills Agency 1993): coming to terms with society, achieving own goals, and developing one’s own knowledge and individual options (

OECD 2011).

If financial literacy is interpreted as basic education, the members of a society need to have the skills and abilities that are required of them to act monetarily conscious in their future professional and private surroundings and to be able to make sound decisions. This also includes the individual attitudes and the motivation to tackle (their own) financially oriented issues. The question, which poses itself here, is which consequences can arise when the individuals of a society show a low degree of financial literacy and—above all—which level is currently at the disposal of the members of society and what effect this has on their actions. In the course of the last few years, several national and international studies that attempt to measure the different sections of the population in different situational contexts concerning their financial competence, financial literacy, financial capability or financial culture have evolved from this context. Often, the terms quoted here are used synonymously in many studies and purport to examine a construct, without explicitly defining it however (

Schürkmann and Schuhen 2013; for an explanation of the little consensus about what the term “literacy” means see

Cude 2022). In the following, a brief summary of the research on the concept of financial literacy will be presented, followed by a depiction of how the construct of FILSA is designed and that it is valid. Individual findings will be discussed and conclusions with regard to basic education across all generations will be drawn.

Many of those surveys are based on questions stemming from

Lusardi et al. (

2017). Their validity has been checked within the context of the Health and Retirement Study of 2004. The questions focus on the individual financial decision-making power: “In designing the questions, we relied on economic models of saving and portfolio choice to identify three economic concepts that individuals should have some understanding of, if they are to use them when making financial decisions” (

Lusardi and Mitchell 2011, p. 499), such as the “(i) Understanding of interest compounding; [the] (ii) Understanding of inflation and (iii) [the] Understanding of risk diversification” (

Lusardi and Mitchell 2011, p. 499). For this study, however, Lusardi finds that the questions have to be simple, relevant and short, as well as that they should have the capacity to differentiate (

Lusardi and Mitchell 2011). Therefore, the testlet design with one stimulus and several individual tasks, as it is usually used in competence assessment (

Wainer et al. 2007;

Pommerich and Segall 2008;

Sireci et al. 1991), was not always applicable. Approaches can be seen in the following sequence of questions (

Lusardi 2008, p. 5):

Suppose you had $100 in a savings account and the interest rate was 2% per year. After 5 years, how much do you think you would have in the account if you left the money to grow: more than $102, exactly $102, less than $102?

Imagine that the interest rate on your savings account was 1% per year and inflation was 2% per year. After 1 year, would you be able to buy more than, exactly the same as, or less than today with the money in this account?

Do you think that the following statement is true or false? “Buying a single company stock usually provides a safer return than a stock mutual fund.”

It is doubtful whether the questions chosen from Lusardi’s pool consisting of ten questions make sense in a financial literacy study and if their validity as well as their ability to give an explanation are guaranteed (for example

Bright and Keller 2012). It is surely possible that three questions about risk attitude and knowledge with regard to inflation and the calculation of interest can explain differences in old-age provision planning (

Bucher-Koenen and Lusardi 2011), but it is doubtful whether the decision-making power that is to be tested in Lusardi’s example above can be attributed to “domain knowledge” or whether general mathematical skills especially in the first task have a higher influence on the skill which is subject to testing (see also

Macha and Schuhen 2012). The logical connection of interest and inflation, however, refers to mathematical skills and at the same time requires dealing with both concepts. Yet, it does not become clear whether the participants actually applied their knowledge. Since they are given a selection of answers, they are robbed of the chance of performing a calculation of interest and, if necessary, of comparing it to inflation loss in the second task. An extensive measurement of financial skills in the sense of competence assessment requires problematic tasks and not pure knowledge tasks (

Weinert 2001, p. 27).

In many studies, financial literacy is analyzed in connection with different main emphases with regard to content. For the study FILSA (Financial Literacy Study of Adults), which is to be introduced here, these main emphases in terms of content have been assessed and brought together in five content areas that are relevant for financial literacy from the perspective of basic education. For Germany, the need for action in this field is demonstrated in several studies. These suggest that, although Germans score well as far as financial literacy is concerned compared with other countries, there are, nevertheless, great differences among socio-demographic groups (

Bucher-Koenen and Lusardi 2011;

Schmidt and Tzamourani 2017;

Stolper and Walter 2017). Financial literacy comprises the content areas: debt, creation of wealth, quality through money, insurance and taxes, monetary transfer and monetary policy. It has to be noted that the study was conducted in Germany and that the tasks from the content areas therefore take up German peculiarities.

Furthermore, the presented online tools offered with regard to financial services and their operations are indispensable for the participation in a European society. Thus, in the context of an intervention study,

Servon and Kaestner (

2008) analyze the influence of technological training and electronic banking on the financial literacy of people with low income. In times of increasing individualization, increasing social risks and the increasing responsibility to ensure one’s own individual financial security,

Schürz and Weber (

2005) also consider it a fundamental core element of basic financial skills to be able to deal with media-assisted tools, to be able to use them and to assess their results. In various studies by

Schürkmann and Schuhen (

2013) and

Schuhen and Schürkmann (

2014), it was demonstrated that the ability to use such online tools has an influence on financial literacy. These things considered, the educational background of individuals turned out to play a key role in the development of financial literacy (

Förster and Happ 2017).

2. Materials and Methods

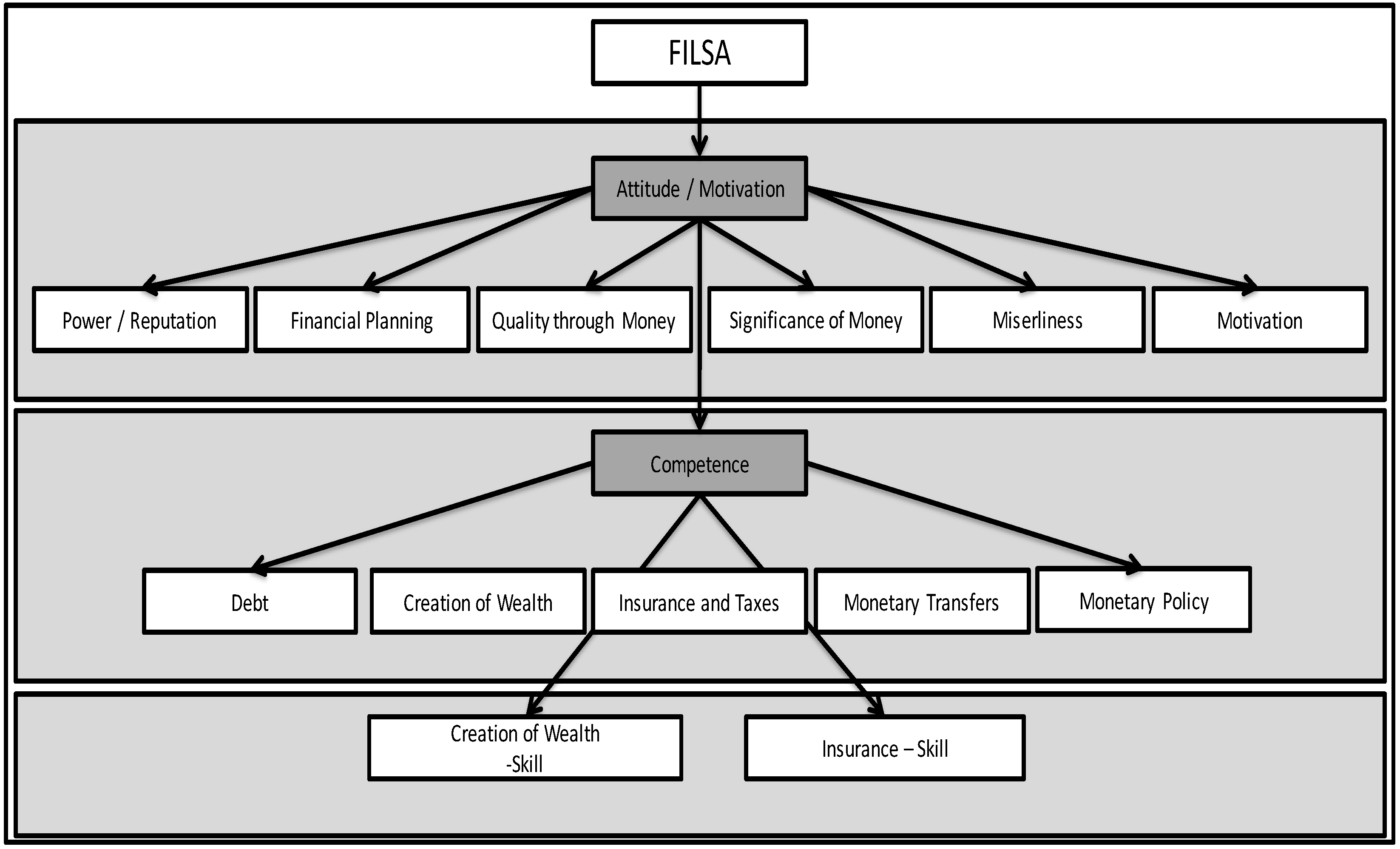

The Financial Literacy Study of Adults (FILSA) resumes the discussion about basic education of adults and specifies it for the area of basic financial education with a focus on Germany. Whilst the majority of studies on financial literacy focus on specific knowledge aspects such as old-age provision, FILSA pays special attention to basic knowledge-related aspects of financial literacy. In order to ensure this, the test design for FILSA about financial literacy contains three levels: an attitude test, a knowledge test and an action or behavior test (cf.

Figure 1).

In the first step, attitudes and motivations of the test persons are collected. The test items about attitude towards and dealing with money were taken from the German testing tools (

Barry and Breuer 2012), which lead back to test items from

Yamauchi and Templer (

1982),

Furnham (

1984) and

Tang (

1992), and contain item groups concerning topics such as power/reputation, financial planning, quality through money, significance of money and miserliness. Among the items regarding motivation, we differentiate between the motivation to deal with financial concerns and to take over responsibility for financial actions (3 tasks with 14 items) and the respondents’ internet affinity (2 tasks with 9 items). The necessity of internet affinity is justified by the increase of financial actions via computer or tablet, etc., on the internet. Online banking, online banks, as well as the use of the internet as a source of information about investment and credit products, are becoming more and more important (

Leichsenring 2011).

Within the construct, five content areas are tested: debt, creation of wealth, insurance and taxes, monetary transfer and monetary policy. In each of these content areas, we identified financial skills that are necessary for an adult to participate in a European society with regard to financial services. This includes thorough knowledge in the five mentioned areas, the ability to apply this knowledge in an individual situation and the competence to reflect on one’s own decisions and to correct them if necessary (

Schürkmann and Schuhen 2013).

The last part of the test deals with three different situations of action. A case study is presented to the test persons, and they have to solve the problem involved. For support, the test persons can consult online tools such as online calculators and a bank consultant that gives aid to decision-making in short video clips. Here too, the significance of a high affinity concerning online tools in order to be able to gather information and to understand it becomes evident. However, only people who have the competence to use the internet self-confidently can make use of this opportunity. The direct actions are analyzed in the third part of FILSA. The second part focuses on the competence test. It comprises fifteen items that belong to the five different content areas of financial literacy. The third part of the test contains three action areas: creation of wealth, loan and insurance. Here, the test persons are introduced to a problem situation and need to make a decision. They are given online calculators and short videos of a bank consultant for help. This way, they can gather information in order to turn the problem situation into a financially safe decision. After the decision-making process, the test persons are given one last item, which evaluates their actions in order to make the test persons’ intention and its influence part of the final analysis. Furthermore, sociodemographic factors such as age, gender and profession were gathered.

FILSA is constructed as an online study that was conducted independently by the test persons. This way, the online tools can also be directly implemented into the study. In order to measure this complex structure, different instruments from quantitative methods have to be combined. For one thing, financial literacy needs to be measured as a competence by means of Rasch modeling (

Rasch 1961, pp. 321–34), and for another, it has to be guaranteed that the connections existing within this construct are consistent within themselves and therefore form a valid measuring instrument, i.e., the connections between the competence and the attitudes and the motivation and the actions need to be referred to each other validly; only then an interpretation of results is legitimate.

In order to be able to test a respondent group as heterogeneously as possible, the link to the online questionnaire was sent via mail to households in Germany. We received the email addresses from mailing lists of a financial service provider. Via snowball procedure, each recipient was asked to forward the link to potentially interested people. The respondents independently carried out the study at home. It took approximately 30 min to fill out the online questionnaire. The survey was conducted in 2019.

In this way, answers of altogether N = 212 respondents were captured. Women (45%) and men (55%) are more or less equally dispersed in the sample. Despite our efforts to especially address older persons, the three age groups of interest for us were not equally well reached (n = 54 (26%) respondents represent the age group of the 18 to 20 years old, n = 130 (61%) were at the age of 21 to 64 and n = 28 (13%) formed the group of the persons above 65). Since the respondent group was <30, it is not Gaussian distributed (n > 30 central limit theorem). A closed answer format was deliberately chosen because, although Rasch modeling with open question formats is possible, the typical procedure for standardized test methods was used.

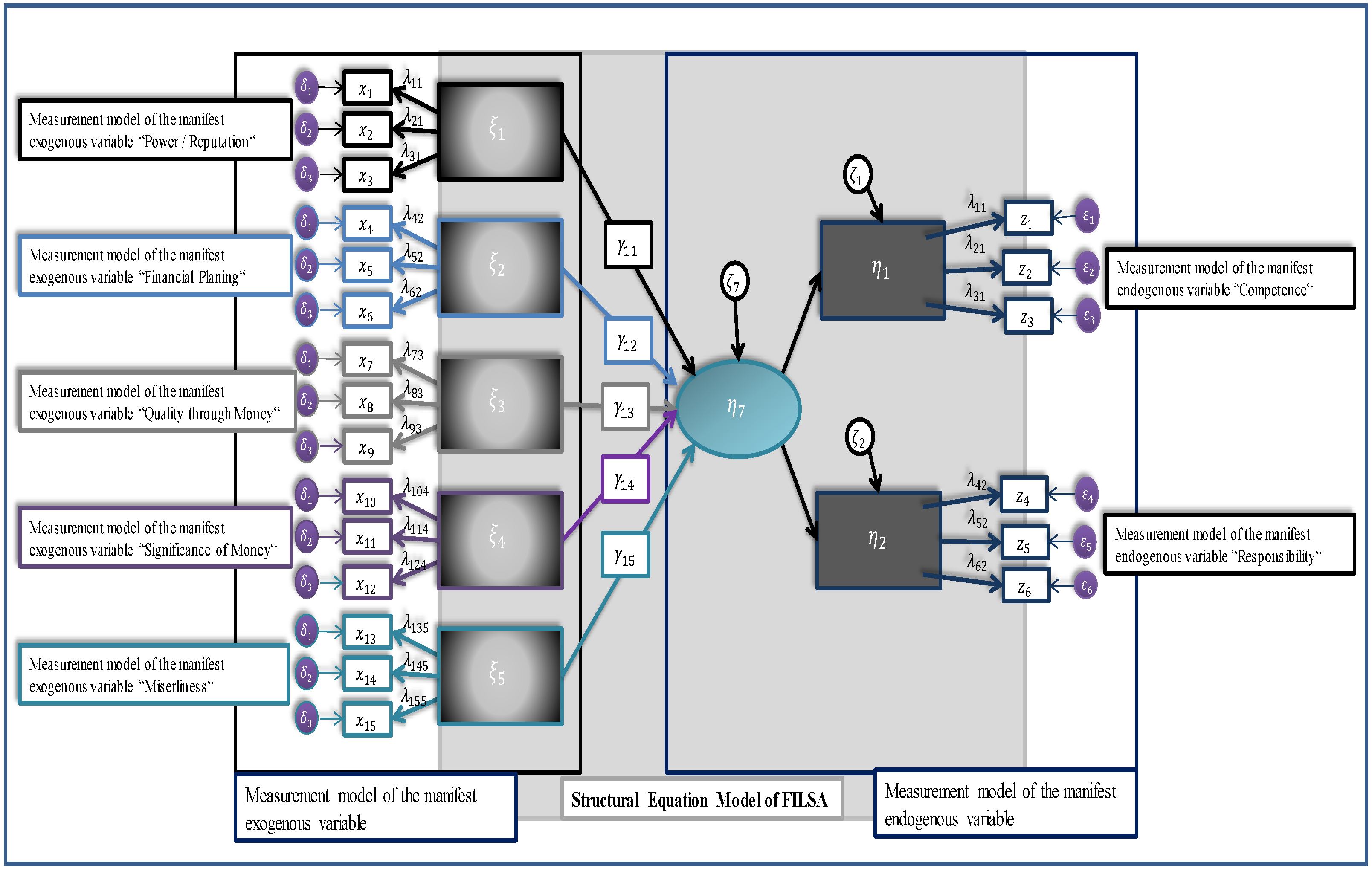

Two essential parts are to be described in the measurement of FILSA: the construct has to be measured with regard to content and external factors which have an influence on the actions that need to be taken into consideration as well. In order to meet these requirements, FILSA is validated by means of a theory-driven structural equation model (SEM), which is able to depict the evaluation with regard to content and the influence of external factors.

The structural equation model in

Figure 2 visualizes the relationships among the factors measured. The measuring model of the manifest exogenous variables consists of personal criteria such as attitude and the participants’ money management. This testing instrument is based on self-assessment in which the data are gathered by a five-step Likert scale (

Barry and Breuer 2012). It is to be investigated here in how far attitude criteria influence financial literacy or whether personal attitudes are irrelevant for financial literacy (see

Schuhen and Schürkmann 2014). For the exogenous variables, the impact on the latent variable financial literacy is measured, while the endogenous variables try to explain the latent variable financial literacy. The measurement model of the manifest endogenous variable incorporates two components. The first component is the competence test, and the second component represents the responsibility for financial decisions in a household.

Next to competence as a manifest construct, which is described by the estimated person parameters, there is the construct of “responsibility”. Since the dealing with financial resources in daily life is strongly related to the responsibility and task of the respective person in a household, it plays a significant role and influences the individual competence.

The participants’ answers of the variable “Competence” (

Figure 2) are dichotomized and modelled according to Rasch. They constitute the endogenous latent variables

. The Rasch model is based on the following basic assumption of this model, β corresponding to ability and Ө corresponding to difficulty (

de Ayala 2009):

The person and difficulty parameters of the Rasch models were estimated by the conditional maximum likelihood approach, of which the mathematical estimation procedure is based on the following formula, β again corresponding to ability and Ө corresponding to difficulty:

The verification of the Rasch models was completed by the Wald test (

Kodde and Palm 1986) and by the likelihood ratio test (

Andersen 1973). In the competence area, the estimated data were sufficient for the model and there were no significant deviations or violations of the Rasch model. Based on these results, the construct of financial literacy is tested with an SEM by means of a confirmatory factor analysis (CFA) (

Muthén and Muthén 2012).

The exogenous manifest variables show the influence on financial literacy in FILSA. For the evaluation, the values on the left were bundled in order to determine individual scores for each attitude criterion (

Little et al. 2002). Bundling the items is justified by the verification of the Cronbachs alpha values for each attitude criterion or for motivation (values between 0.785 and 0.902) (

Cortina 1993). The scores were generated from the means that were determined from the respondents’ coded answers. To ensure comparability the means were scaled in five levels.

3. Results

The results of FILSA are presented in a two-step procedure. To present valid results, the SEM’s validity criteria are shown by means of the SEM’s criteria of model accuracy (

Schürkmann 2017). Based on this, the competence test results were listed in order to project the influence of external factors and individual motivation on the results followed by their discussion. The random sample contains 166 data sets, which can be assigned to professions such as pensioners, public officials, self-employed persons, jobseekers, etc.

3.1. Results of the SEM of FILSA

The SEM results are represented by model accuracy values that show whether or not the hypothetic SEM is a valid construct. The

test value is supposed to be not significant and therefore the significance parameter should be higher than 0.05. Thus, the

index can be considered a badness-of-fit criterion in the sense that a high

value is a bad adjustment, whereas a low value is a good adjustment. When

equals zero, it is a perfect adjustment (

Wang and Wang 2012, p. 17). Another criterion is the value represented by

. It should be lower than two, but still acceptable as long as it is lower than three. Furthermore, the root mean square error of approximation (RMSEA) is a factor that is relevant for model accuracy. It should be lower than 0.05 (cf.

Reinecke 2005;

Wang and Wang 2012). The last criterion is the comparative fit index (CFI). It is one of the goodness-of-fit indices. The CFI should be at least higher than 0.90 in order to be acceptable (

Wang and Wang 2012, p. 19) or higher than 0.95 to be considered good (

Ullmann and Bentler 2012).

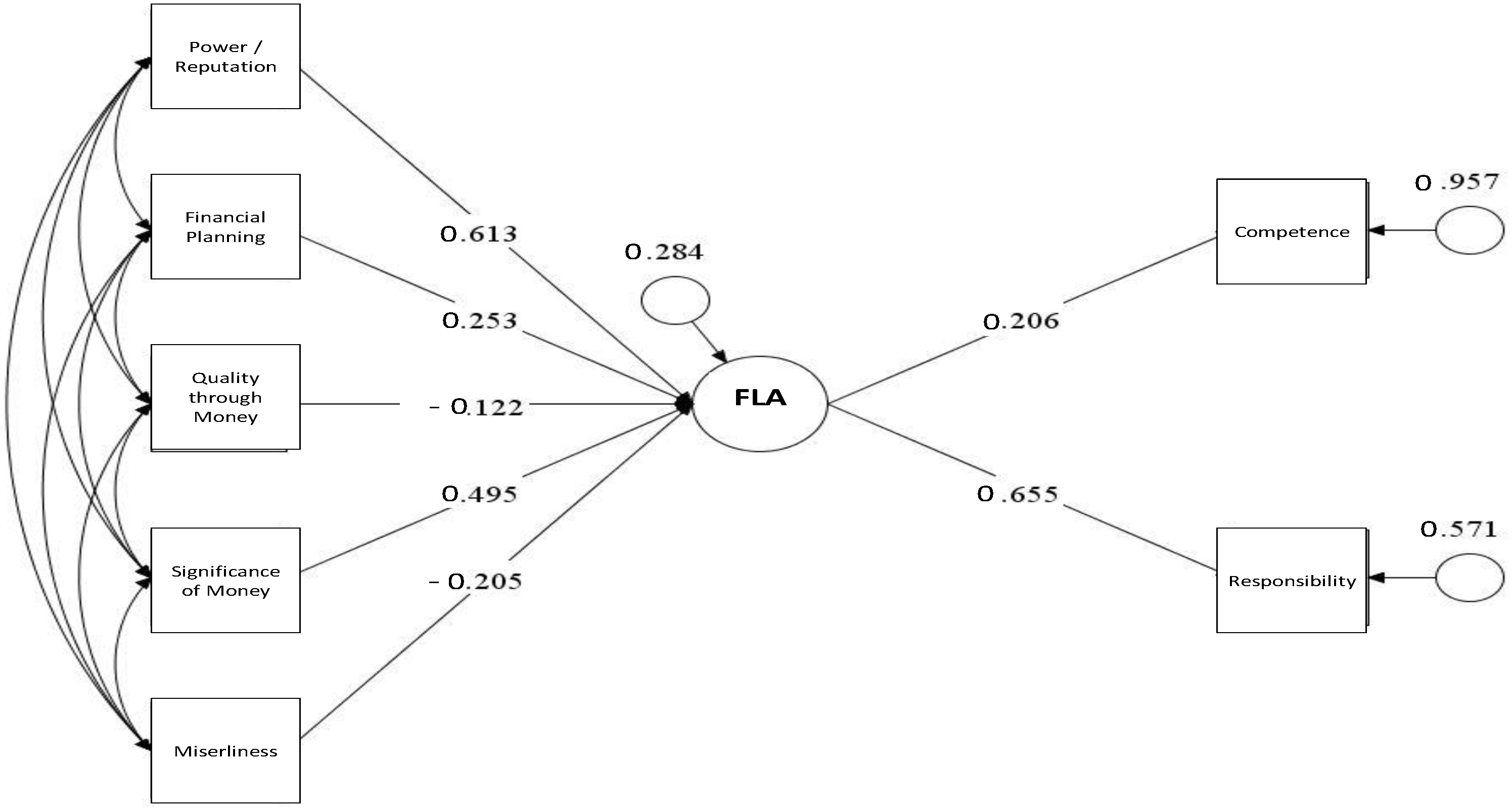

The model quality criteria for the latent variable FLA (Financial Literacy of Adults) for FILSA are in a good range and can, thus, be accepted. The value for

is 1.2725 and RMSEA is 0.041. Additionally, CFI and TLI with 0.982 and 0.950, respectively, lie in an acceptably good range (cf.

Figure 3). Hence, the measurement model for FILSA is valid and specific conclusions can be drawn from the model.

On the left side, the attitude areas power/reputation and significance of money have a high effect on the latent variable financial literacy. The importance of money and the power that the test persons acquire through money show a positive effect on the latent variable financial literacy in FILSA. The other attitude items only have a minor effect on the latent variable financial literacy, but they are still significant.

The right side represents the areas of competence and responsibility. It is evident that the factor loading of responsibility has a high effect on financial literacy. Thus, competence and responsibility are explained by the latent variable financial literacy. This is revealed by the R-square, where the R-square is represented, which are the squared factor loadings, on a percentage basis with the latent variable financial literacy. Personal responsibility is explained by the latent variable financial literacy for 42.9% and reveals the coherence between personal responsibility for financial matters and financial competence. This shows that personal responsibility influences financial literacy in a positive way and that it contributes to rendering people better at dealing with their financial resources.

3.2. Results of the Competence Test of FILSA

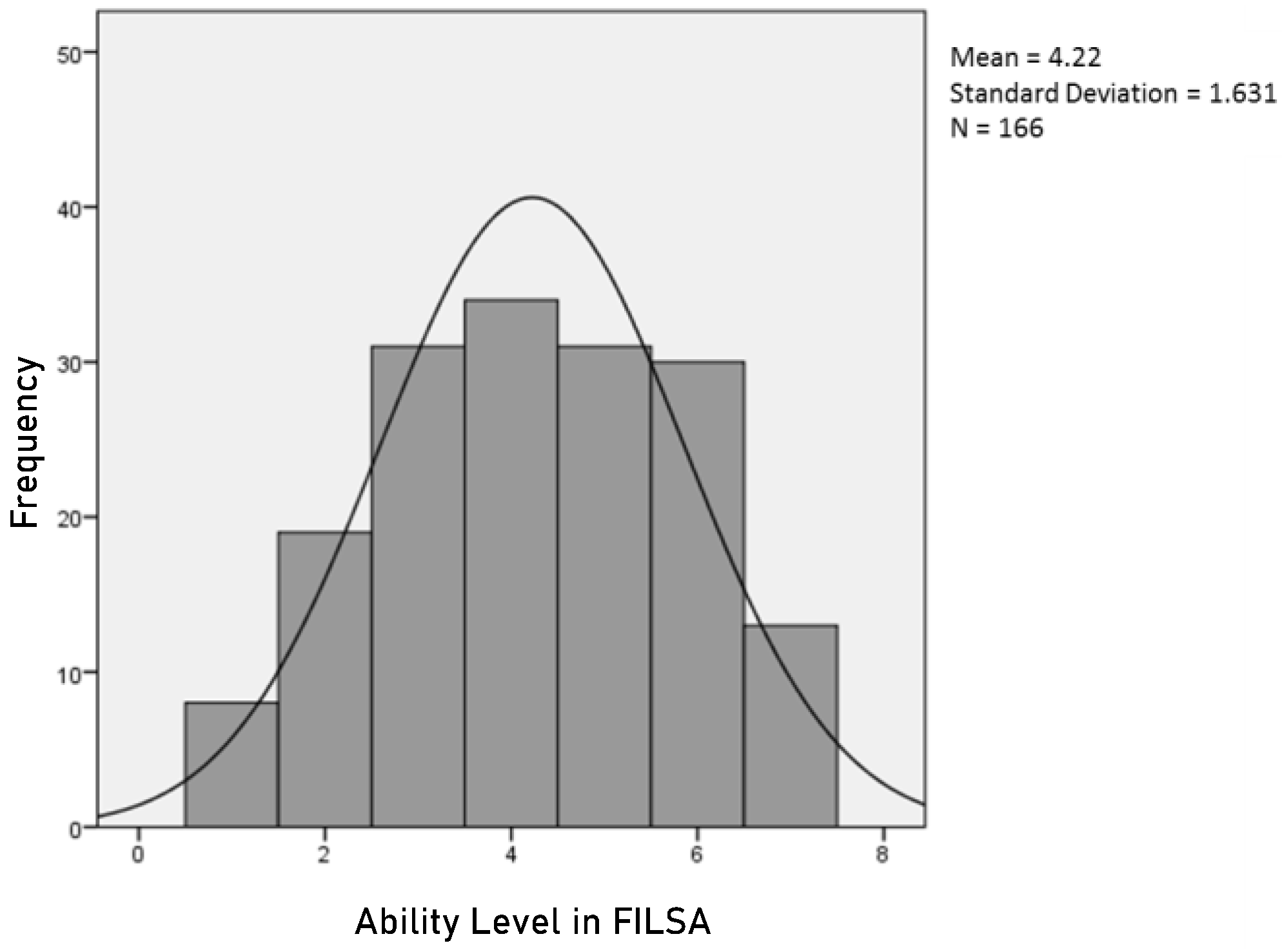

Given the fact that the construct is valid, the competence dimension can now be analyzed by means of the estimated person ability parameters in FILSA.

Figure 4 shows the distribution of the person parameters according to the latent dimension of one to seven for the current respondents of FILSA. The adaption to the Rasch model was determined with the likelihood ratio test so that the test values with a significance value of

p = 0.59 (model is not significant) were sufficient for the Rasch model.

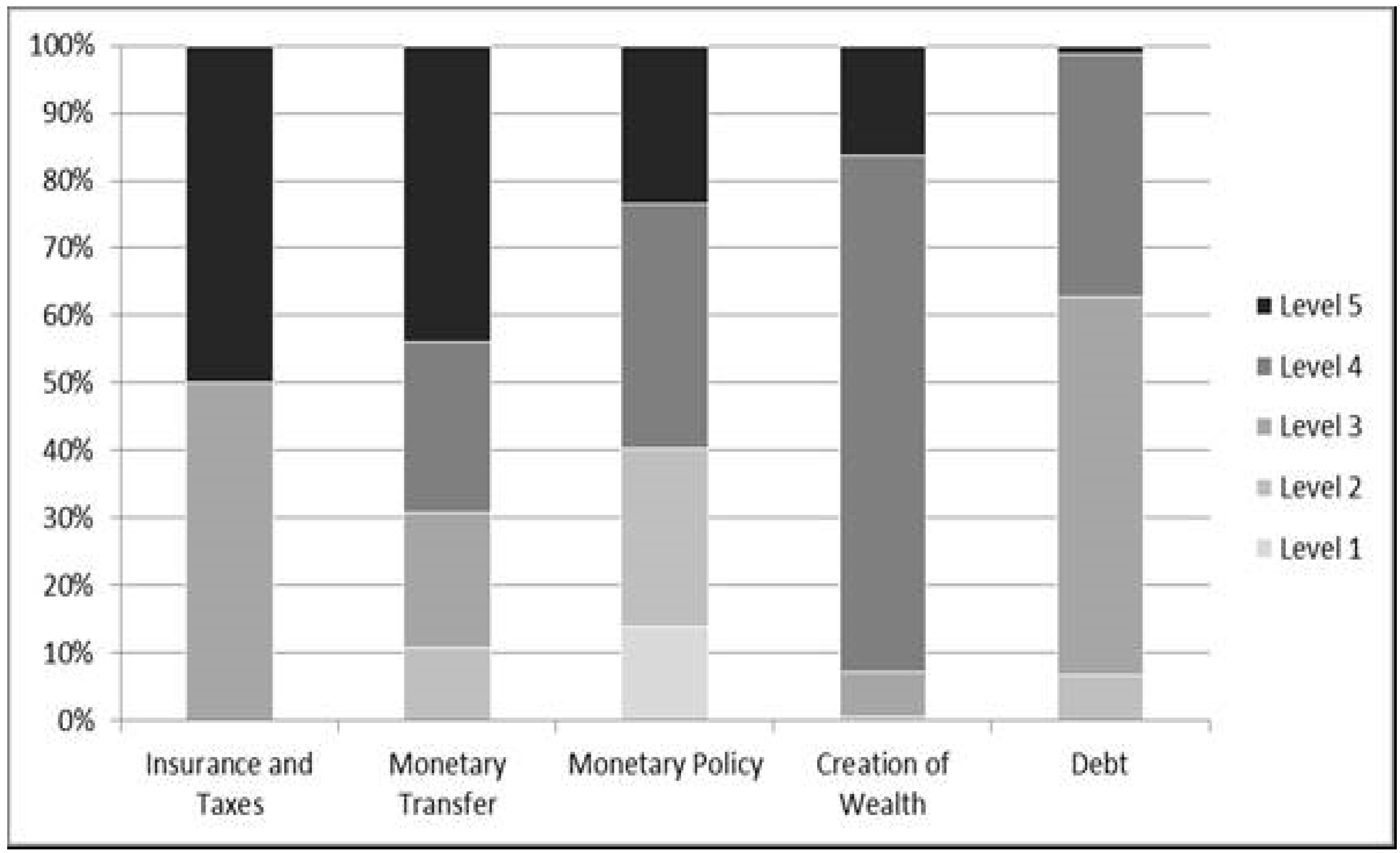

Most respondents have an average financial literacy, whereas 74.6% are responsible for their own financial actions and only 2.89% leave the responsibility to their partner. External consultants are practically not used. There were no significant differences with regard to gender. The means of the results of the five individual content fields of financial literacy were scaled. The scale’s subdivision consists of five areas, whereas the first level corresponds to a low level (0–20.0% right answers), which corresponds to level (1), the second to a lower average level (2.0–40.0% right answers), which corresponds to level (2), the third to an average level (40.0–60.0% right answers), which corresponds to level (3), the fourth to a high average level (50.0–75.0% right answers), which corresponds to level (4) and the last one corresponds to a high level (75.0–100.0% right answers), which corresponds to level (5). In the content areas, debt, creation of wealth, insurance and taxes, monetary transfer and monetary policy the majority of respondents reached a high average level.

Figure 5 shows that the highest level (level 5) is underrepresented, especially in the areas debt and creation of wealth, whilst both of the lowest levels (level 1 and level 2) are overrepresented in the areas of debt. Deficits can be spotted in the field of monetary policy as well. Here, on average, the test persons remain below the medium level 3.

Merely in the area of monetary transfer, 40% of the test persons exhibit high values and do better than average. The results seem to be influenced by external factors. Looking at the correlations between content areas and sociodemographic factors, it becomes clear that highly significant connections exist between the two areas in deficit, debt and insurance and taxes and age. The correlations are at −0.321 and −0.303 (age in connection with debt and insurance and taxes).

The results of the actions in the areas creation of wealth, loans and insurances show that the perception of financial institutions does not match that of the respondents. It is assumed that the consumers increasingly use the internet as an information source for financial products (

Stobbe and Meyer 2010). However, the study reveals that only 48.50% of the respondents make use of these tools. Nearly 50% calculated themselves or estimated, which led to considerably worse results.

When it comes to purchasing a car on credit, one fifth of the test persons would not borrow the money from a financial institution but would try to borrow it from a relative. Approximately 30% would make use of a special car loan and another fifth of an installment credit. If the question is how to invest money, a split pattern appears when risk disposition is concerned. Approximately 20% of the test persons would take a chance on stocks, whereas one fifth would choose the safe alternative of a building loan contract, even if the current interest rates are low and no high yield can be attained. However, for the most part, test persons reveal a risk-averse attitude and prefer secure investments such as fixed deposits or savings accounts.

3.3. Results Concerning Age-Related Differences

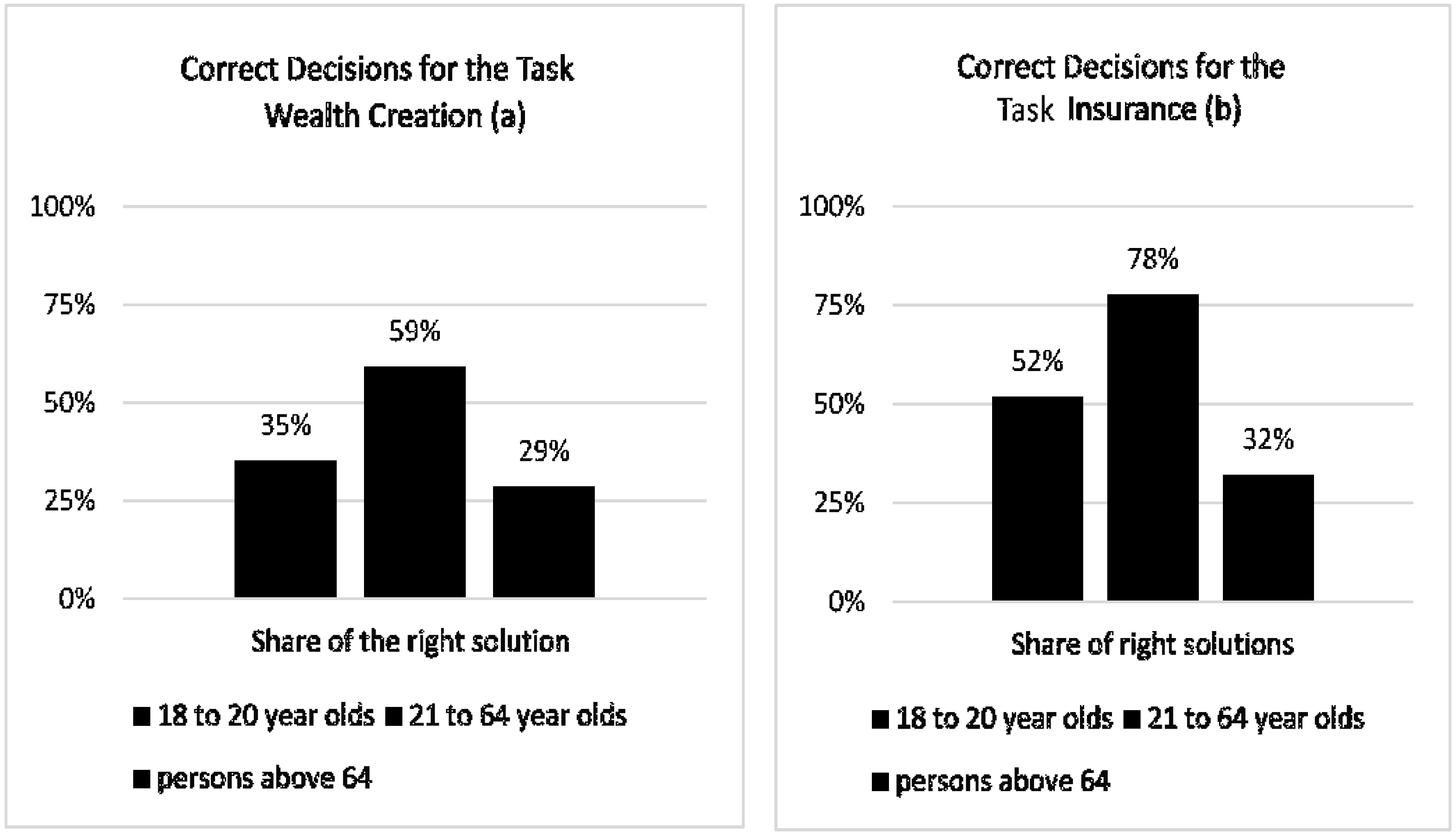

In the first step, we were interested in the quality of the financial decisions of the three described age groups in the two areas ‘wealth creation’ and ‘insurance’. In the FILSA study, these answers had already been coded as wrong (=0) or right (=1). In

Figure 6a (wealth creation) and

Figure 6b (insurance), the results of the three age groups are illustrated.

We conducted an ANOVA with the share of correct decisions in the respective area as a dependent variable and the age groups as an independent variable in order to statistically verify these differences. The results demonstrate a significant main effect of the age groups for the decisions concerning wealth creation (F (2, 209) = 7.53, p = 0.001) as well as for the area of insurance (F (2, 209) = 15.01, p < 0.001). Subsequently, we conducted a Bonferroni post hoc test for both areas. The results show a statistically significant difference for the decisions in the area wealth creation between the group of the 21 to 64 years old and the two other groups. The same pattern can be seen in the post hoc tests for the area insurance. The share of respondents with a correct problem solution is significantly higher in the group of the 21 to 64 years old than in the two other groups. The younger and older respondent groups do not differ significantly from each other here either. Evidently, the younger and older groups make worse financial decisions in our study if they have to use an online tool for decision-making. On the basis of our considerations made in the previous parts, we assume that these differences are to be attributed to the varying distinct financial literacy between the three age groups as well as to different skills of adequately using online services. Furthermore, we are able to analyze a third possible cause on the basis of the FILSA data—the attitude towards money and the dealing with it.

3.4. Attitude towards Money and Related Behavior

Initially, we were interested in the question whether these differences in the quality of financial decisions can possibly be explained by a different attitude of the age groups towards money, and the dealing with it. It might be conceivable that with the different stage of life, money has a different importance for people as well. This importance could find expression in the motivation to make correct financial decisions.

Using the FILSA instrument, the relevant attitude was recorded in the five dimensions power/reputation, financial planning, quality through money, significance of money, and miserliness.

Table 1 presents the mean values of the relating answers in the age groups. Furthermore, we conducted an ANOVA with the mean value of the according answers to these dimensions as dependent variable and the age group as independent variable for each recorded dimension.

The mean values demonstrate that not only the three age groups, but all respondents are close together in their attitudes. The two attitude dimensions financial planning and significance of money, according to which the significance of the control of their own financial situation is emphasized and money is considered as a good worth striving for, reached the highest approval. In contrast, money as a symbol of success and power (power/reputation) and saving as a means to an end in itself (miserliness) play a less important role in all age groups. Interestingly, the three age groups statistically differ from each other in a significant way only in one dimension. The ensuing Bonferroni post hoc test shows that money is less often perceived as a necessary condition to be able to acquire products of high quality (quality through money) in the oldest respondent group of persons aged above 65 than in the two younger age groups. One can argue that quality through money is the only dimension in which the three age groups statistically differ from each other in a significant way because the oldest respondent group is less likely to primarily judge the quality of a product on the basis of its price (for marketing-based expectancies such as price and product quality see, e.g.,

Ariely and Norton 2009). Nonetheless, this difference only shows a low effect size of eta2 = 0.053 as well. Thus, apart from this last dimension, all three age groups do not significantly differ in their attitude towards money.

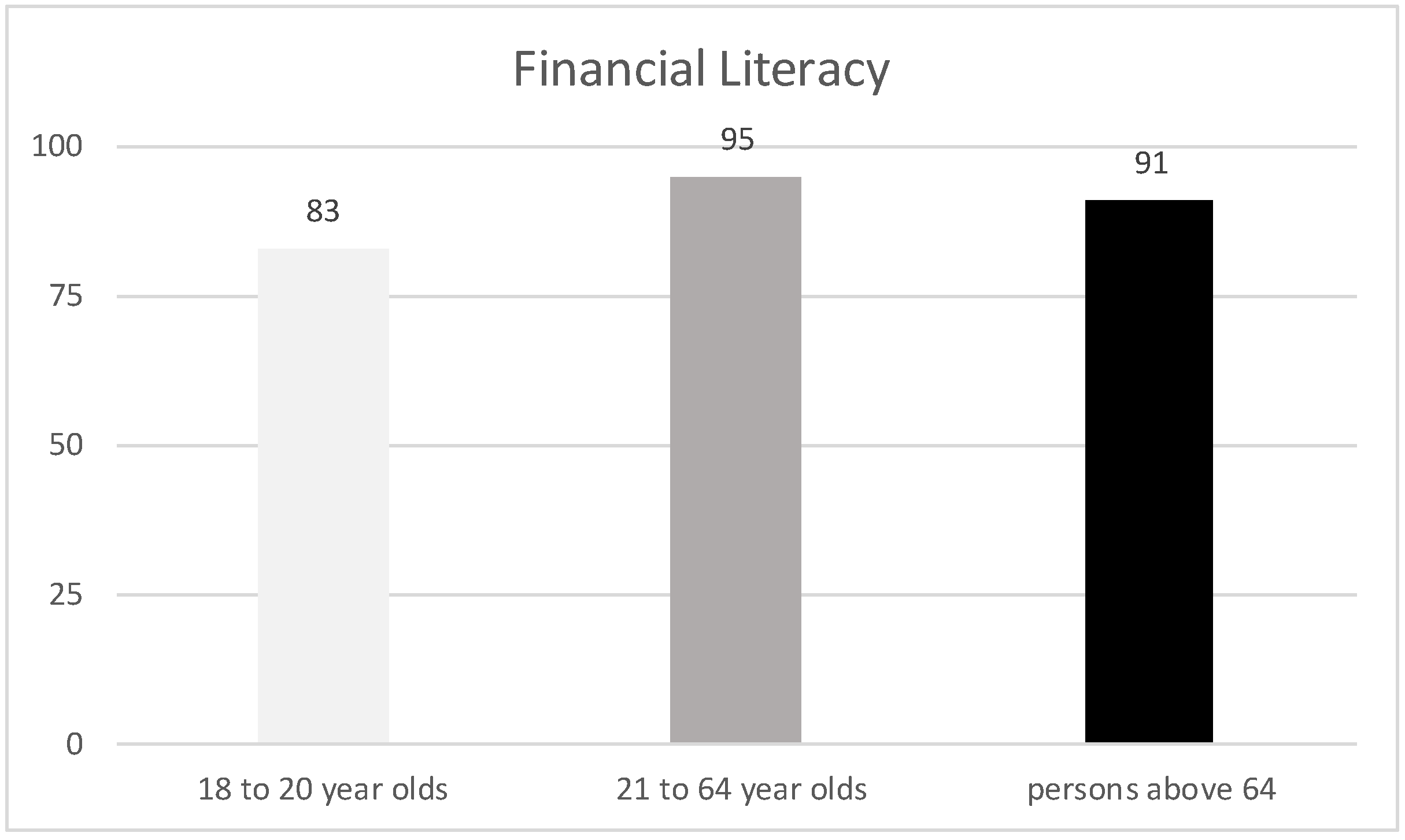

We assume that one reason for the differences in the quality of the financial decisions in the online tool is grounded in the varying degree of financial literacy between the age groups. Especially the previously discussed literature, which suggests that, in particular, younger people make worse financial decisions than older people because of their lower financial literacy. Using the FILSA instrument, financial literacy was recorded by 147 knowledge questions, which were each answered completely right (=1), or completely wrong (=0). Thus, the recorded score as a measure of financial literacy can, hence, take values from 0 (no question answered correctly) to 147 (all answers correct).

Figure 7 presents the score achieved on average in the three age groups.

The points achieved on average in the age group as a measure of financial literacy are represented (scaled from 0 to 147); higher values stand for a higher financial literacy.

As expected, the results show that the youngest age group of people aged 18 to 20 exhibits the lowest financial literacy. An ANOVA with the achieved score as a dependent variable and the age group as an independent variable demonstrates a significant main effect of the age groups (F (2, 209) = 27.46, p < 0.001, eta2 = 0.208). In an ensuing Bonferroni post hoc test, the difference between the youngest group and the two other age groups becomes significant (p < 0.001), whilst financial literacy does not significantly differ between people aged 21 to 64 and people above 65 (p = 0.144).

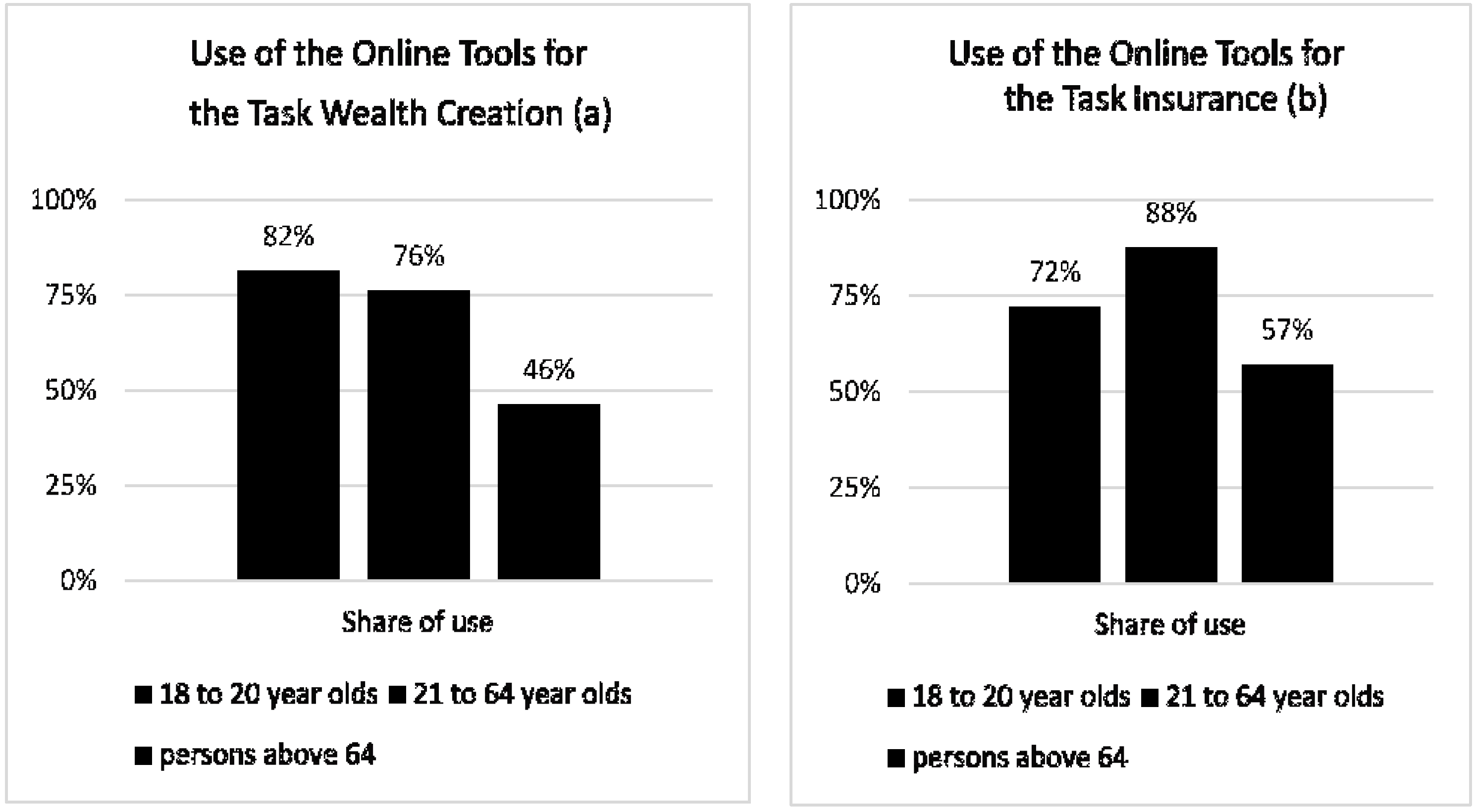

We assume that a further reason for the differences in the quality of the financial decisions in the online tool lies in the varying degree of the ability to use the online environment according to the task between the age groups. We use the usage of the online aids, which were available for support in the financial decision-making via the FILSA instrument, as an indicator for this ability. The problem fields to be solved were compiled in a way that a decision was also possible without the use of the online tools, although, the information presented in the online tools clearly simplified correct (optimal) decision-making.

Figure 8 shows the respective share of those respondents who used the online tools in the decision-making, per age group.

As expected, it becomes evident that the oldest group of the respondents, the people aged above 65, use the offered online tools the least. The differences in usage appeared in both decisions and were obviously independent from the decision area or the type of offered aids. Furthermore, we conducted an ANOVA for each area with the dependent variable share of respondents with use of the online aids and the independent variable age groups. Both results show a significant main effect of the age group (wealth creation: F (2, 209) = 6.71, p = 0.001; insurance: F (2, 209) = 8.42, p < 0.001). The ensuing Bonferroni post hoc test supported our assumption. The share of people aged above 65 that used the support of the online aids in decision-making differed significantly from the two other age groups in the two areas.

4. Discussion

The results show that the construct underlying FILSA is valid and that the depicted areas can be assigned to the construct. The findings of FILSA reveal that the respondents show considerable knowledge deficits in the areas of debt, creation of wealth, monetary transfer and monetary policies. From a socio-economic perspective, it is important to emphasize that these deficits in financial literacy are age independent. Against the background of the increasing importance of online financial services, older respondents (in FILSA above the age of 65), especially, run the risk of suffering from their lack of financial literacy. This assumption is closely linked to the digital divide phenomenon (

Schmidt 2015, p. 98). In contrast to adolescents and young adults, people above the age of 65 do not have many opportunities which enable them to keep pace with their rapidly changing environment (e.g., by means of school lessons, studies or on-the-job training). The associations of senior citizens or adult education centers can be sources of information here. However, initiatives such as senior citizens’ associations highly depend on voluntary commitment. As a consequence, senior citizens are likely to be especially vulnerable when it comes to dealing with the new financial-related challenges of their socio-economic environment such as developing technological skills. However, this does not imply that adolescents are not confronted with challenges and a lack of skills when it comes to financial decision-making in technologically shaped environments. It is therefore equally important to accelerate financial literacy among people as soon as possible. With regard to the usage of techniques in business development,

Gilbert et al. (

2021) found out that a practical approach (internships) accelerates the usage of techniques. Similarly, practical approaches to foster financial literacy among adolescents should be promoted rather than pure theory in a class. Furthermore, it is of crucial importance that school development decision-makers recognize the relevance of financial literacy for all students, irrespective of their type of school. Schools on the high school/gymnasium level, lack financial literacy-related contents in their curricula (see, e.g.,

Pitthan and De Witte (

2021) who suggest financial literacy treatments on a systematic basis).

The establishment and increasing dominance of online financial services question the financial literacy approach current studies rely on (see research summary). Perhaps, the holistic approach oriented towards the real world chosen here based on a basic financial education represents a new instrument, maybe even a new intellectual approach to think about financial literacy, especially with regard to questions of social participation/non-participation and possible risks for the individual as well as for society as a whole. In the near future, financial literacy as an essential part of basic economic education will be inseparably connected to technological literacy. It is therefore questionable to what extent the current financial literacy approach serves social participation and an empowerment of consumers. Therefore, future research should focus on broadening the current understanding of financial literacy by taking into account all skills involved in financial decision-making. This involves identifying which skills are to be considered in the first place. A more complex understanding of financial literacy can, thus, provide a more realistic representation of financial decision-making. In this vein, revising the understanding of financial literacy as a concept can help meet the risks associated with a too-narrow understanding of financial literacy, such as failing to demonstrate which individual skills play a role in financial decision-making. The FILSA study provides a starting point for the suggested approach. It broadens the understanding of financial literacy by considering the socioeconomic environment individuals make financial decisions in.

In order to highlight the risk management’s perspective, it is expedient to understand that a lack of financial literacy among individuals, as an essential part of basic education, entails risks on a societal level. Individuals have to make financial decisions on a daily basis. If these decisions are based on knowledge and competence deficits and are, thus, made by (to a greater or lesser extent) financially illiterate individuals, society as a whole is confronted and has to deal with individuals who are not able to manage their everyday life. Educating people systematically in the area of financial literacy and recognizing it as an essential part of basic education is therefore a useful approach to minimize the risk of passing over individuals with a low financial literacy. Ideally, by educating oneself, individuals will then be put into a position to minimize their own risks related to a low financial literacy, e.g., getting into debt.

The current online tools of banks and finance portals provided in the study can also be of help; however, they often fail to meet the consumers’ interests and abilities. The results show that financial advice would have been necessary because the consumers achieved worse results without it. This is where the current portfolios of financial institutions need to be reconsidered and, if necessary, replaced by innovative intervention measures.

As far as younger individuals are concerned, education providers in Germany should offer more classes in the areas of basic economic education so that they can discover and take advantage of the opportunities with regard to financial assets on the one hand, and that they are enabled to make financial decisions for themselves according to certain criteria on the other hand.

As far as research limitations are concerned, there are two aspects to be highlighted. The FILSA study examined only two selected areas in which financial decisions can be made—insurance and creation of wealth. Furthermore, only one specific environment of online financial services was examined.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}