You Learn When It Hurts: Evidence in the Mutual Fund Industry

Abstract

:1. Introduction

2. Literature Review

3. Data

4. Methodology

4.1. Important Buys and Sells

4.2. Important Errors in Important Trading Decisions

4.3. Learning Process in the Mutual Fund Industry

β3Agei,t + β4No. of stocksi,t + β5Turnoveri,t + β6Market returnt + εi,t

+ β2 Sizei,t + β3 Agei,t + β4 No. of stocksi,t + β5 Turnoveri,t + β6 Market returnt

+ β7 (Familyi,t × Timet) + εi,t

5. Results

5.1. Learning in the Mutual Fund Industry

5.2. Learning in the Mutual Fund Industry: A Family Approach

5.3. Learning in the Mutual Fund Industry: An Approach Using the Characteristics of Fund Families

5.3.1. Learning Results by Size of Mutual Fund Families

5.3.2. Learning Process by Independence of Fund Families from Financial Service Groups

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

| Panel A: Euro Domestic Equity Mutual Funds | ||||

| Skewness | Kurtosis | Jarque–Bera Probability | p-Valor | |

| Fund_Size | 0.8171 | 3.2202 | 5.9193% | 0.0000 |

| Fund_age | 3.7782 | 5.3240 | 1.2964% | 0.0000 |

| Fund_No. of stocks | 2.8967 | 6.0312 | 6.0634% | 0.0000 |

| Fund_turnover | 1.2523 | 2.4632 | 4.9906% | 0.0000 |

| Panel B: Euro Non-Domestic Equity Mutual Funds | ||||

| Skewness | Kurtosis | Jarque–Bera Probability | p-Valor | |

| Fund_Size | 0.9403 | 5.3184 | 6.1410% | 0.0000 |

| Fund_age | 1.3917 | 4.4947 | 5.0643% | 0.0000 |

| Fund_No. of stocks | 4.3365 | 1.5865 | 2.0415% | 0.0000 |

| Fund_turnover | 3.1473 | 3.0231 | 4.4207% | 0.0000 |

Appendix B

Appendix C

| Panel A: Euro Domestic Equity Mutual funds_Important Errors in Buying Decisions | |||||||

| % Important Errors | Time | Age | Size | No. of Stocks | Turnover | Market Return | |

| % Important errors | 1.0000 | ||||||

| Time | −0.2784 | 1.0000 | |||||

| Age | −0.1529 | 0.0178 | 1.0000 | ||||

| Size | −0.1401 | −0.0662 | 0.0245 | 1.0000 | |||

| No. Of stocks | −0.0810 | 0.0305 | 0.0218 | 0.0789 | 1.0000 | ||

| Turnover | 0.0350 | −0.0040 | −0.0732 | −0.0874 | 0.0512 | 1.0000 | |

| Market return | −0.0423 | 0.0583 | 0.0098 | 0.0015 | 0.0055 | 0.0166 | 1.0000 |

| Panel B: Euro Domestic Equity Mutual Funds_Important Errors in Selling Decisions | |||||||

| % Important Errors | Time | Age | Size | No. of Stocks | Turnover | Market Return | |

| % Important errors | 1.0000 | ||||||

| Time | −0.3571 | 1.0000 | |||||

| Age | 0.0419 | −0.0526 | 1.0000 | ||||

| Size | −0.0198 | 0.0275 | 0.0924 | 1.0000 | |||

| No. Of stocks | −0.1005 | 0.0410 | 0.0912 | 0.0494 | 1.0000 | ||

| Turnover | 0.0970 | −0.0249 | −0.0784 | −0.0461 | 0.0570 | 1.0000 | |

| Market return | −0.0207 | 0.0560 | 0.0020 | 0.0059 | 0.0060 | 0.0170 | 1.0000 |

| Panel C: Euro Non-Domestic Equity Mutual Funds_Important Errors in Buying Decisions | |||||||

| % Important Errors | Time | Age | Size | No. of Stocks | Turnover | Market Return | |

| % Important errors | 1.0000 | ||||||

| Time | −0.3125 | 1.0000 | |||||

| Age | −0.0082 | 0.0380 | 1.0000 | ||||

| Size | −0.0359 | 0.0249 | 0.0761 | 1.0000 | |||

| No. Of stocks | −0.1153 | 0.0340 | 0.0214 | 0.0158 | 1.0000 | ||

| Turnover | 0.1555 | −0.0047 | −0.1344 | −0.0316 | 0.1243 | 1.0000 | |

| Market return | −0.0324 | 0.0925 | 0.0134 | 0.0034 | −0.0005 | 0.0477 | 1.0000 |

| Panel D: Euro Non-Domestic Equity Mutual Funds_Important Errors in Selling Decisions | |||||||

| % Important Errors | Time | Age | Size | No. of Stocks | Turnover | Market Return | |

| % Important errors | 1.0000 | ||||||

| Time | −0.2914 | 1.0000 | |||||

| Age | −0.0238 | 0.0357 | 1.0000 | ||||

| Size | −0.0276 | 0.0103 | 0.0847 | 1.0000 | |||

| No. Of stocks | −0.1421 | 0.0312 | 0.0278 | 0.0693 | 1.0000 | ||

| Turnover | 0.1405 | −0.0197 | −0.1309 | −0.0403 | 0.1199 | 1.0000 | |

| Market return | −0.0431 | 0.0875 | 0.0155 | 0.0021 | −0.0033 | 0.0498 | 1.0000 |

| 1 | European Union Directive 2009/65/EC of the European Parliament and the Council on the Coordination of Laws (2009) on the coordination of laws, regulations, and administrative provisions relating to the Undertakings for Collective Investment in Transferable Securities (UCITS). This Directive was implemented in all member countries of the European Union. |

| 2 | The Spanish Securities and Exchange Commission (CNMV) establishes a classification of mutual funds according to the types of assets included in the portfolios. Euro equity mutual funds must invest more than 75% of their portfolios in equities and at least 60% of the total equity exposure must be issued by companies in the euro area. However, within this category there are different investment policies (funds focused on Spanish stocks and funds focused on Euro stocks), thus, we split the Euro equity category into two subsamples according to their investment objective. We label Euro domestic equity funds a sub-sample of funds that self-report their investment objective in the Spanish market and the rest of the funds in the Euro equity category are labeled as Euro non-domestic equity funds. |

| 3 | The mutual fund holdings used in this study rely on the information on monthly portfolio holdings from the CNMV for each fund from December 1999 to December 2006. This information was provided for research purposes. However, the CNMV only provided us with quarterly portfolio holdings from March 2007 onwards. Therefore, we first matched the quarterly information provided by the CNMV with the information provided by Morningstar and, then, we included monthly information from Morningstar when it was available. |

| 4 | Datastream provides stock information about the main capital operations, such as splits and the payment of dividends. |

| 5 | To obtain the number of shares, we consider the main capital operations, such as splits and the payment of dividends. |

| 6 | To avoid any potential bias and to offer robust results, we considered different cutoffs (one lower, 5% and another higher, 20%) and we followed the same steps in the three filters using these alternative cutoffs. |

| 7 | In buys, we obtain the average after considering all the funds that are included in our sample in each period t but, in sells, we only consider the funds that hold the stock in the previous month, t − 1, because any fund can buy a stock but only the funds that hold a stock can sell it. |

| 8 | To obtain Jensen’s (1968) alpha, we use the Ibex 35 total return index and the Euro Stoxx-50 total return index as the benchmarks in Euro domestic and in Euro non-domestic equity mutual funds, respectively. We also use the daily return of one-day repos of Spanish Treasury bills as the proxy for the risk-free return. |

| 9 | |

| 10 | We run Equation (14) considering mutual funds as the decision-making units rather than mutual fund managers. Following Tindale and Winget (2019), decision-making and its quality are not individual affairs. Furthermore, we identify the manager replacements in our mutual fund sample and then, we apply the Chow test to study the effect of a manager replacement on the percentage of important errors in our sample. The Chow test provides evidence that 87% of the managers’ replacements in our sample do not represent a significant structural change in the percentage of important errors. Details are available on request. |

| 11 | In spite of the fund fee being a usual control variable in this kind of study, we do not consider it in our model because all funds included in the sample apply asset-based fees being these percentages similar among them. Other kinds of fee structures such as performance-based fees or redemption fees may affect the learning process. On the one hand, Lhabitant (2007) compared asset-based and performance-based fees, concluding that the latter could be used as a control of the portfolio risk. In addition, Agarwal et al. (2009a, 2009b) argue that performance-based fees provide better incentives to obtain superior performance. On the other hand, Cumming et al. (2019) also documents that fee structures that penalize investment withdrawal lead managers to feel less pressure from investor sentiment. |

| 12 | We apply alternative specifications of our model to confirm that our results are robust. First, we perform Equation (14) on a quarterly basis and we use also the fixed effects (FE) model on monthly, quarterly and annual frequency, and we obtain a significant negative relationship between the percentage of important errors and time. Second, we add a quadratic term of the time variable to Equation (14), and the main results remain similar to our original model specification. Third, we add the market volatility as an additional control variable to Equation (14) and obtain consistent results. The details are available on request. |

| 13 | We also apply Equation (14) to errors from non-important decisions. The results are different from the conclusions drawn from Table 3 and Table 4. That is, time does not influence the percentage of trading errors, thereby rejecting the evidence of significant learning from non-important decisions. Details are available on request. |

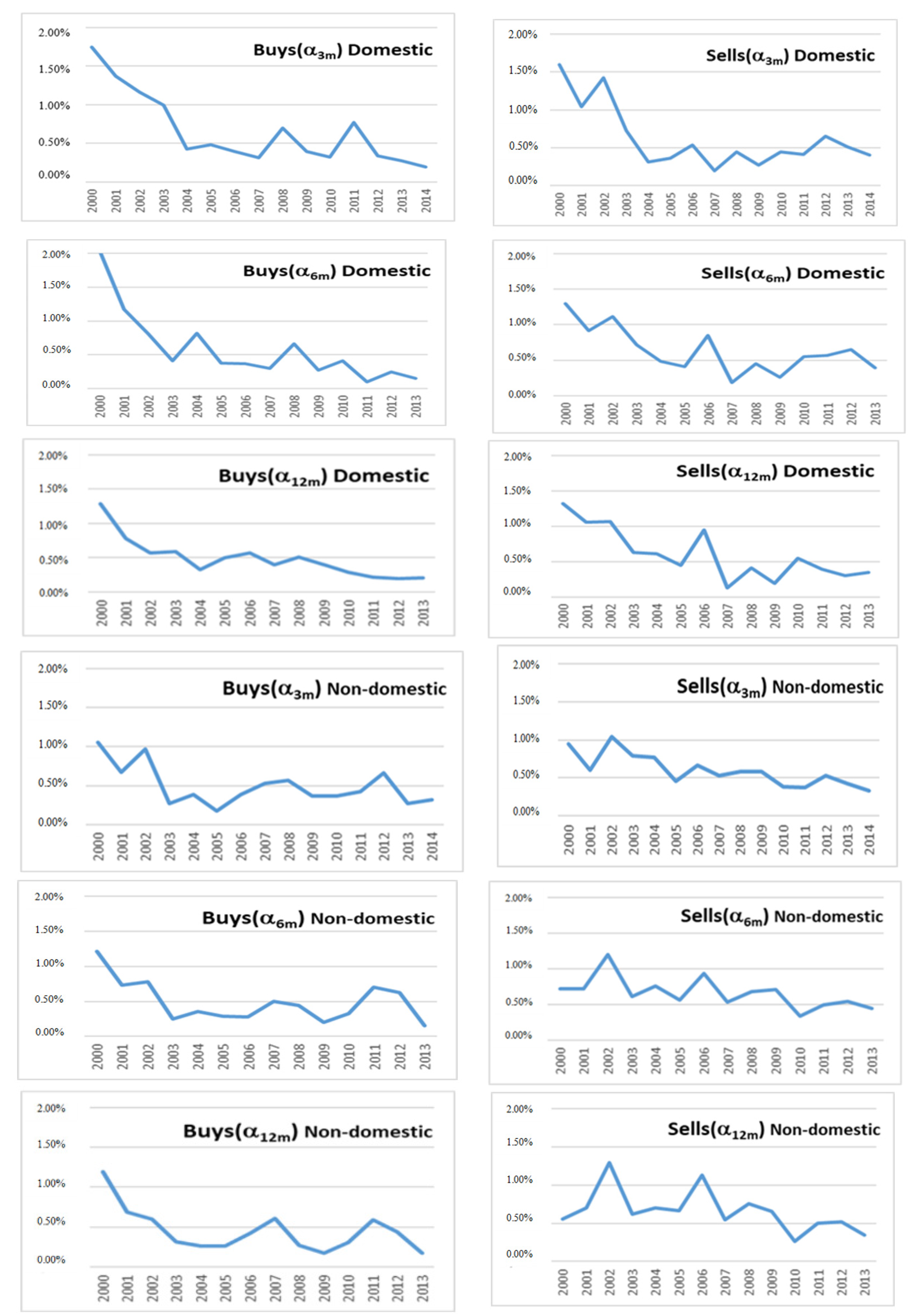

| 14 | The results shown in Table 3 and Table 4 consider the quintiles of important buys and sells with the most negative influence on the performance for all the funds across our sample period. We also obtained similar findings for quartiles and deciles, thereby providing even more robustness to this empirical evidence. |

References

- Adams, Garry L., and Bruce T. Lamont. 2003. Knowledge management systems and developing sustainable competitive advantage. Journal of Knowledge Management 7: 142–54. [Google Scholar] [CrossRef]

- Agarwal, Vikas, Naveen D. Daniel, and Narayan Y. Naik. 2009a. Role of managerial incentives and discretion in hedge fund performance. The Journal of Finance 64: 2221–56. [Google Scholar] [CrossRef] [Green Version]

- Agarwal, Vikas, Nicole M. Boyson, and Narayan Y. Naik. 2009b. Hedge funds for retail investors? An examination of hedged mutual funds. Journal of Financial and Quantitative Analysis 44: 273–305. [Google Scholar] [CrossRef] [Green Version]

- Alda, Mercedes. 2018. Pension fund manager skills over the economic cycle: The (non-) specialization cost. The European Journal of Finance 24: 36–58. [Google Scholar] [CrossRef]

- Alexander, Gordon J., Gjergji Cici, and Scott Gibson. 2007. Does motivation matter when assessing trade performance? An analysis of mutual funds. The Review of Financial Studies 20: 125–50. [Google Scholar] [CrossRef] [Green Version]

- Arellano, Manuel, and Stephen Bond. 1991. Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. The Review of Economic Studies 58: 277–97. [Google Scholar] [CrossRef] [Green Version]

- Arellano, Manuel, and Olympia Bower. 1995. Another look at the instrumental variable estimation of error-components models. Journal of Econometrics 68: 29–51. [Google Scholar] [CrossRef] [Green Version]

- Argote, Linda. 1999. Organizational learning: Creating, Retaining and Transferring Knowledge. Cham: Springer Science & Business Media, pp. 321–31. [Google Scholar]

- Argyris, Chris. 1993. Knowledge for Action: A Guide to Overcoming Barriers to Organizational Change. San Francisco: Jossey-Bass Inc. [Google Scholar]

- Ariely, Dan, and Dan Zakay. 2001. A timely account of the role of duration in decision making. Actapsychologica 108: 187–207. [Google Scholar] [CrossRef]

- Arrow, Kenneth Joseph. 1962. The economic implications of learning by doing. The Review of Economic Studies 29: 155–73. [Google Scholar] [CrossRef]

- Autio, Erkko, Harry J. Sapienza, and James G. Almeida. 2000. Effects of age at entry, knowledge intensity, and imitability on international growth. Academy of Management Journal 43: 909–24. [Google Scholar]

- Ayoubi, Charles, Michele Pezzoni, and Fabiana Visentin. 2017. At the origins of learning: Absorbing knowledge flows from within the team. Journal of Economic Behavior & Organization 134: 374–87. [Google Scholar]

- Barber, Brad M., and Terrance Odean. 2000. Trading is hazardous to your wealth: The common stock investment performance of individual investors. The Journal of Finance 55: 773–806. [Google Scholar] [CrossRef]

- Barber, Brad M., and Terrance Odean. 2013. The behavior of individual investors. Handbook of the Economics of Finance 2: 1533–70. [Google Scholar]

- Barras, Laurent, Patrick Gagliardini, and Olivier Scaillet. 2020. Skill, scale, and value creation in the mutual fund industry. Swiss Finance Institute Research Paper, 18–66. [Google Scholar] [CrossRef] [Green Version]

- Berk, Jonathan B., and Richard C. Green. 2004. Mutual fund flows and performance in rational markets. Journal of Political Economy 112: 1269–95. [Google Scholar] [CrossRef]

- Blasco, Natividad, Cristina Del Rio, and Rafael Santamaría. 1997. The random walk hypothesis in the Spanish stock market: 1980–1992. Journal of Business Finance & Accounting 24: 667–84. [Google Scholar]

- Blundell, Richard, and Stephen Bond. 1998. Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics 87: 115–43. [Google Scholar] [CrossRef] [Green Version]

- Boh, Wai Fong, Cheng-Jen Huang, and Anne Wu. 2020. Investor experience and innovation performance: The mediating role of external cooperation. Strategic Management Journal 41: 124–51. [Google Scholar] [CrossRef]

- Brown, David P., and Youchang Wu. 2016. Mutual fund flows and cross-fund learning within families. The Journal of Finance 71: 383–424. [Google Scholar] [CrossRef]

- Calvet, Laurent E., John Y. Campbell, and Paolo Sodini. 2009. Measuring the financial sophistication of households. American Economic Review 99: 393–98. [Google Scholar] [CrossRef] [Green Version]

- Cambon, M. Isabel, and Ramiro Losada. 2014. Competition and structure of the mutual fund industry in Spain: The role of credit institutions. The Spanish Review of Financial Economics 12: 58–71. [Google Scholar] [CrossRef] [Green Version]

- Campbell, John Y. 2006. Household finance. The Journal of Finance 61: 1553–604. [Google Scholar] [CrossRef] [Green Version]

- Cardon, Melissa S., Christopher E. Stevens, and D. Ryland Potter. 2011. Misfortunes or mistakes? Cultural sense making of entrepreneurial failure. Journal of Business Venturing 26: 79–92. [Google Scholar] [CrossRef]

- Chen, Joseph, Harrison Hong, Ming Huang, and Jeffrey D. Kubik. 2004. Does fund size erode mutual fund performance? The role of liquidity and organization. American Economic Review 94: 1276–302. [Google Scholar] [CrossRef] [Green Version]

- Chen, Jiao, Changqing Luo, Lurun Pan, and Jia Yun. 2021. Trading Strategy of Structured Mutual Fund based on Deep Learning Network. Expert Systems with Applications 183: 115390. [Google Scholar] [CrossRef]

- Cici, Gjergji, Laura K. Dahm, and Alexander Kempf. 2018. Trading efficiency of fund families: Impact on fund performance and investment behavior. Journal of Banking & Finance 88: 1–14. [Google Scholar]

- Cisse, Mamadou, Mamadou Abdoulaye Konte, Mohamed Toure, and Ismael Afolabi Assani. 2019. Contribution to the valuation of BRVM’s assets: A conditional CAPM approach. Journal of Risk and Financial Management 12: 27. [Google Scholar] [CrossRef] [Green Version]

- Crossan, Mary M., and Hari B. Bapuji. 2003. Examining the link between knowledge management, organizational learning and performance. Paper presented at the 5th International Conference on Organizational Learning and Knowledge, Lancaster University, Lancaster, UK, May 30–June 2. [Google Scholar]

- Crossan, Mary M., Henry W. Lane, and Roderick E. White. 1999. An organizational learning framework: From intuition to institution. Academy of Management Review 24: 522–37. [Google Scholar] [CrossRef]

- Cumming, Douglas, Sofia Johan, and Yelin Zhang. 2019. What is mutual fund flow? Journal of International Financial Markets, Institutions and Money 62: 222–51. [Google Scholar] [CrossRef]

- Cuthbertson, Keith, Dirk Nitzsche, and Niall O’Sullivan. 2016. A review of behavioural and management effects in mutual fund performance. International Review of Financial Analysis 44: 162–76. [Google Scholar] [CrossRef]

- Dangl, Thomas, Youchang Wu, and Josef Zechner. 2008. Market discipline and internal governance in the mutual fund industry. The Review of Financial Studies 21: 2307–43. [Google Scholar] [CrossRef] [Green Version]

- Dehghanpour, Siamak, and Akbar Esfahanipour. 2018. Dynamic portfolio insurance strategy: A robust machine learning approach. Journal of Information and Telecommunication 2: 392–410. [Google Scholar] [CrossRef] [Green Version]

- Dias, Rui, Nuno Teixeira, Veronika Machova, Pedro Pardal, Jakub Horak, and Marek Vochozka. 2020. Random walks and market efficiency tests: Evidence on US, Chinese and European capital markets within the context of the global COVID-19 pandemic. Oeconomia Copernicana 11: 585–608. [Google Scholar] [CrossRef]

- Droms, William G., and David A. Walker. 1995. Determinants of variation in mutual fund returns. Applied Financial Economics 5: 383–89. [Google Scholar] [CrossRef]

- Durusu-Ciftci, Dilek, M. Serdar Ispir, and Dundar Kok. 2019. Do stock markets follow a random walk? New evidence for an old question. International Review of Economics & Finance 64: 165–75. [Google Scholar]

- European Fund and Asset Management Association (EFAMA). 2018. International Statistical Release (Third Quarter of 2018), Brussels, Belgium. Available online: https://www.efama.org/previous-monthly-and-quarterly-statistics (accessed on 8 November 2018).

- Elton, Edwin J., Martin J. Gruber, Christopher R. Blake, Yoel Krasny, and Sadi O. Ozelge. 2010. The effect of holdings data frequency on conclusions about mutual fund behavior. Journal of Banking & Finance 34: 912–22. [Google Scholar]

- European Union Directive 2009/65/EC of the European Parliament and the Council on the Coordination of Laws. 2009. Regulations and Administrative Provisions Relating to Undertakings for Collective Investment in Transferable Securities (UCITS) (recast). 2008/0153(COD), 13 July 2013. Available online: https://eur-lex.europa.eu/eli/dir/2009/65/oj (accessed on 25 September 2018).

- Fama, Eugene F. 1968. Risk, return and equilibrium: Some clarifying comments. The Journal of Finance 23: 29–40. [Google Scholar] [CrossRef]

- Ferreira, Miguel, Aneel Keswani, António F. Miguel, and Sofia B. Ramos. 2013. The determinants of mutual fund performance: A cross-country study. Review of Finance 17: 483–525. [Google Scholar] [CrossRef] [Green Version]

- Finkelstein, Sydney, and Shade H. Sanford. 2000. Learning from corporate mistakes: The rise and fall of Iridium. Organizational Dynamics 29: 138–48. [Google Scholar] [CrossRef]

- Fischer, Rene, and Ralf Gerhardt. 2007. Investment Mistakes of Individual Investors and the Impact of Financial Advice. Working Paper. London: European Business School. [Google Scholar]

- Gervais, Simon, and Terrance Odean. 2001. Learning to be overconfident. The Review of Financial Studies 14: 1–27. [Google Scholar] [CrossRef]

- Grinblatt, Mark, and Sheridan Titman. 1993. Performance measurement without benchmarks: An examination of mutual fund returns. Journal of Business 66: 47–68. [Google Scholar] [CrossRef]

- Grinblatt, Mark, and Sheridan Titman. 1994. A study of monthly mutual fund returns and performance evaluation techniques. Journal of Financial and Quantitative Analysis 29: 419–44. [Google Scholar] [CrossRef]

- Haq, Anwar Ul, Adnan Zeb, Zhenfeng Lei, and Defu Zhang. 2021. Forecasting daily stock trend using multi-filter feature selection and deep learning. Expert Systems with Applications 168: 114444. [Google Scholar] [CrossRef]

- Hatch, Nile W., and Jeffrey H. Dyer. 2004. Human capital and learning as a source of sustainable competitive advantage. Strategic Management Journal 25: 1155–78. [Google Scholar] [CrossRef]

- Hirshleifer, Jack. 2001. The Dark Side of the Force: Economic Foundations of Conflict Theory. Cambridge: Cambridge University Press. [Google Scholar]

- Inverco. 2018. Statistical of Mutual Funds, Madrid, Spain. Available online: https://www.inverco.es/38/39/101/2018 (accessed on 8 November 2018).

- Jashapara, Ashok. 2003. Cognition, culture and competition: An empirical test of the learning organization. The Learning Organization 10: 31–50. [Google Scholar] [CrossRef]

- Jensen, Michael C. 1968. The performance of mutual funds in the period 1945-1964. The Journal of Finance 23: 389–416. [Google Scholar] [CrossRef]

- Jiang, George J., Tong Yao, and Tong Yu. 2007. Do mutual funds time the market? Evidence from portfolio holdings. Journal of Financial Economics 86: 724–58. [Google Scholar] [CrossRef]

- Jones, Christopher S., and Jay Shanken. 2005. Mutual fund performance with learning across funds. Journal of Financial Economics 78: 507–52. [Google Scholar] [CrossRef] [Green Version]

- Kacperczyk, Marcin, Clemens Sialm, and Lu Zheng. 2006. Unobserved actions of mutual funds. The Review of Financial Studies 21: 2379–416. [Google Scholar] [CrossRef] [Green Version]

- Kacperczyk, Marcin, Van Nieuwerburgh, and Laura Veldkamp. 2014. Time-varying fund manager skill. The Journal of Finance 69: 1455–84. [Google Scholar] [CrossRef] [Green Version]

- Kahneman, Daniel. 1994. New challenges to the rationality assumption. Journal of Institutional and Theoretical Economics 150: 18–36. [Google Scholar]

- Kempf, Alexander, Stefan Ruenzi, and Tanja Thiele. 2009. Employment risk, compensation incentives, and managerial risk taking: Evidence from the mutual fund industry. Journal of Financial Economics 92: 92–108. [Google Scholar] [CrossRef] [Green Version]

- Kempf, Elisabeth, Alberto Manconi, and Oliver G. Spalt. 2017. Learning by Doing: The Value of Experience and the Origins of Skill for Mutual Fund Managers. Available online: https://ssrn.com/abstract=2124896 (accessed on 10 July 2021).

- Khorana, Ajay. 1996. Top management turnover an empirical investigation of mutual fund managers. Journal of Financial Economics 40: 403–27. [Google Scholar] [CrossRef]

- Koestner, Maximilian, Benjamin Loos, Steffen Meyer, and Andreas Hackethal. 2017. Do individual investors learn from their mistakes? Journal of Business Economics 87: 669–703. [Google Scholar] [CrossRef]

- Levitt, Barbara, and James G. March. 1988. Organizational learning. Annual Review of Sociology 14: 319–38. [Google Scholar] [CrossRef]

- Lhabitant, Francois-Serge. 2007. Delegated portfolio management: Are hedge fund fees too high? Journal of Derivatives & Hedge Funds 13: 220–32. [Google Scholar]

- List, John A. 2003. Does market experience eliminate market anomalies? The Quarterly Journal of Economics 118: 41–71. [Google Scholar] [CrossRef]

- Lucey, Brian M., and Michael Dowling. 2005. The role of feelings in investor decision-making. Journal of Economic Surveys 19: 211–37. [Google Scholar] [CrossRef]

- Markowitz, Harry M. 1952. Portfolio selection. The Journal of Finance 7: 77–91. [Google Scholar]

- Marsick, Victoria J., and Karen Watkins. 2015. Informal and Incidental Learning in the Workplace (Routledge Revivals). London: Routledge. [Google Scholar]

- Mason, Andrew, Sam Agyei-Ampomah, and Frank Skinner. 2016. Realism, skill, and incentives: Current and future trends in investment management and investment performance. International Review of Financial Analysis 43: 31–40. [Google Scholar] [CrossRef] [Green Version]

- McDevitt, Roselie, Catherine Giapponi, and Cheryl Tromley. 2007. A Model Ethical Decision Making: The Integration of Process and Content. Journal of Business Ethics 73: 219–29. [Google Scholar] [CrossRef]

- Mileva, Elitza. 2007. Using Arellano-Bond Dynamic Panel GMM Estimators in Stata. New York: Economics Department, Fordham University, pp. 1–10. [Google Scholar]

- Nanda, Vikram, Z. Jay Wang, and Lu Zheng. 2004. Family values and the star phenomenon: Strategies of mutual fund families. The Review of Financial Studies 17: 667–98. [Google Scholar] [CrossRef]

- Nichita, Anca; Batrancea Larissa, Marcel Pop Ciprian, Batrancea Ioan, Morar Ioan Dan, Masca Ema, Roux-Cesar Ana Maria, Forte Denis, Formigoni Henrique, and Aderito da Silva Adilson. 2019. We learn not for school but for life: Empirical evidence of the impact of tax literacy on tax compliance. Eastern European Economics 57: 397–429. [Google Scholar] [CrossRef]

- Nicolosi, Gina, Liang Peng, and Ning Zhu. 2009. Do individual investors learn from their trading experience? Journal of Financial Markets 12: 317–36. [Google Scholar] [CrossRef]

- Offerman, Theo, and Joep Sonnemans. 1998. Learning by experience and learning by imitating successful others. Journal of Economic Behavior & Organization 34: 559–75. [Google Scholar]

- Park, Hyungjun, Min Kyu Sim, and Dong Gu Choi. 2020. An intelligent financial portfolio trading strategy using deep Q-learning. Expert Systems with Applications 158: 113573. [Google Scholar] [CrossRef]

- Pástor, Ľuboš, Robert F. Stambaugh, and Lucian A. Taylor. 2015. Scale and skill in active management. Journal of Financial Economics 116: 23–45. [Google Scholar] [CrossRef]

- Pilbeam, Keith, and Hamish Preston. 2019. An empirical investigation of the performance of Japanese mutual funds: Skill or luck? International Journal of Financial Studies 7: 6. [Google Scholar] [CrossRef] [Green Version]

- Pollet, Joshua M., and Mungo Wilson. 2008. How does size affect mutual fund behavior? The Journal of Finance 63: 2941–69. [Google Scholar] [CrossRef]

- Reason, Peter. 1999. Integrating action and reflection through co-operative inquiry. Management Learning 30: 207–25. [Google Scholar] [CrossRef] [Green Version]

- Roodman, David. 2009a. A note on the theme of too many instruments. Oxford Bulletin of Economics and Statistics 71: 135–58. [Google Scholar] [CrossRef]

- Roodman, David. 2009b. How to do xtabond2: An introduction to Difference and System GMM in Stata. The Stata Journal 9: 86–136. [Google Scholar] [CrossRef] [Green Version]

- Rousseau, Peter L., and Paul Wachtel. 2002. Inflation thresholds and the finance–growth nexus. Journal of International Money and Finance 21: 777–93. [Google Scholar] [CrossRef]

- Sargan, John D. 1958. The estimation of economic relationships using instrumental variables. Econometrica: Journal of the Econometric Society 26: 393–415. [Google Scholar] [CrossRef]

- Sargent, Thomas J. 1993. Bounded Rationality in Macroeconomics: The Arne Ryde Memorial Lectures. Stanford: OUP Catalogue, Hoover Institution. [Google Scholar]

- Schoenmaker, Dirk, and Willem Schramade. 2019. Investing for long-term value creation. Journal of Sustainable Finance & Investment 9: 356–77. [Google Scholar]

- Seru, Amit, Tyler Shumway, and Noah Stoffman. 2009. Learning by trading. The Review of Financial Studies 23: 705–39. [Google Scholar] [CrossRef]

- Sevcenko, Victoria, and Sendil Ethiraj. 2018. How do firms appropriate value from employees with transferable skills? A study of the appropriation puzzle in actively managed mutual funds. Organization Science 29: 775–95. [Google Scholar] [CrossRef] [Green Version]

- Shantha, Kalugala Vidanalage Aruna. 2019. Individual investors’ learning behavior and its impact on their herd bias: An integrated analysis in the context of stock trading. Sustainability 11: 1448. [Google Scholar] [CrossRef] [Green Version]

- Sharpe, William F. 1964. Capital asset prices: A theory of market equilibrium under conditions of risk. The Journal of Finance 19: 425–42. [Google Scholar]

- Shiller, Robert J. 2003. From efficient markets theory to behavioral finance. Journal of Economic Perspectives 17: 83–104. [Google Scholar] [CrossRef] [Green Version]

- Singh, Smita, Patricia Corner, and Kathryn Pavlovich. 2007. Coping with entrepreneurial failure. Journal of Management & Organization 13: 331–44. [Google Scholar]

- Sirri, Erik R., and Peter Tufano. 1998. Costly search and mutual fund flows. The Journal of Finance 53: 1589–622. [Google Scholar] [CrossRef]

- Stanovich, Keith E., and Richard F. West. 2000. Individual differences in reasoning: Implications for the rationality debate? Behavioral and Brain Sciences 23: 645–65. [Google Scholar] [CrossRef] [PubMed]

- Statman, Meir. 2014. Behavioral finance: Finance with normal people. Borsa Istanbul Review 14: 65–73. [Google Scholar] [CrossRef] [Green Version]

- Subrahmanyam, Avanidhar. 2008. Behavioural finance: A review and synthesis. European Financial Management 14: 12–29. [Google Scholar] [CrossRef]

- Tegtmeier, Lars. 2021. Testing the Efficiency of Globally Listed Private Equity Markets. Journal of Risk and Financial Management 14: 313. [Google Scholar] [CrossRef]

- Tindale, R. Scott, and Jeremy R. Winget. 2019. Group Decision-Making. In Oxford Research Encyclopedia of Psychology. Oxford: Oxford University Press. [Google Scholar]

- Tjosvold, Dean, Zi-you Yu, and Chun Hui. 2004. Team learning from mistakes: The contribution of cooperative goals and problem-solving. Journal of Management Studies 41: 1223–45. [Google Scholar] [CrossRef]

- Tversky, Amos, and Eldar Shafir. 1992. Choice under conflict: The dynamics of deferred decision. Psychological Science 3: 358–61. [Google Scholar] [CrossRef]

- Wang, Shin-Yun, and Cheng-Few Lee. 2011. Fuzzy multi-criteria decision-making for evaluating mutual fund strategies. Applied Economics 43: 3405–14. [Google Scholar] [CrossRef]

- Wang, Yingxu, and Guenther Ruhe. 2007. The cognitive process of decision making. International Journal of Cognitive Informatics and Natural Intelligence 1: 73–85. [Google Scholar] [CrossRef] [Green Version]

- Weick, Karl E., and Susan J. Ashford. 2001. Learning in organizations. The new handbook of organizational communication: Advances in Theory, Research, and Methods 704: 731. [Google Scholar]

- Wermers, Russ, Tong Yao, and Jane Zhao. 2012. Forecasting stock returns through an efficient aggregation of mutual fund holdings. The Review of Financial Studies 25: 3490–529. [Google Scholar] [CrossRef] [Green Version]

- Wooldridge, Jeffrey M. 2010. Econometric Analysis of Cross Section and Panel Data. Cambridge: MIT Press. [Google Scholar]

- Zhang, Yuchen, and Shigeyuki Hamori. 2020. The predictability of the exchange rate when combining machine learning and fundamental models. Journal of Risk and Financial Management 13: 48. [Google Scholar] [CrossRef] [Green Version]

- Zhao, Bin. 2011. Learning from errors: The role of context, emotion, and personality. Journal of Organizational Behavior 32: 435–63. [Google Scholar] [CrossRef]

- Zhao, Bin, and Fernando Olivera. 2006. Error reporting in organizations. Academy of Management Review 31: 1012–30. [Google Scholar] [CrossRef]

| Panel A: Euro Domestic Equity Mutual Funds | Panel B: Euro Non-Domestic Equity Mutual Funds | ||||||

|---|---|---|---|---|---|---|---|

| 2000–2007 | 2008–2011 | 2012–2014 * | 2000–2007 | 2008–2011 | 2012–2014 * | ||

| No. of Funds | 144 | 106 | 74 | No. of Funds | 124 | 91 | 56 |

| No. of Families | 79 | 58 | 49 | No. of Families | 71 | 51 | 36 |

| Fund_size | Fund_size | ||||||

| Mean | 69.67 | 41.72 | 67.93 | Mean | 65.08 | 23.95 | 43.49 |

| Q1 | 100.32 | 45.03 | 70.16 | Q1 | 75.48 | 24.15 | 52.12 |

| Q5 | 7.46 | 6.38 | 7.92 | Q5 | 5.05 | 3.47 | 5.37 |

| Fund_age | Fund_age | ||||||

| Mean | 8 | 12 | 16 | Mean | 6 | 10 | 12 |

| Q1 | 11 | 17 | 20 | Q1 | 9 | 13 | 16 |

| Q5 | 3 | 7 | 12 | Q5 | 2 | 5 | 5 |

| Fund_No. of stocks | Fund_No. of stocks | ||||||

| Mean | 43 | 40 | 38 | Mean | 60 | 50 | 50 |

| Q1 | 52 | 45 | 43 | Q1 | 71 | 60 | 62 |

| Q5 | 33 | 31 | 29 | Q5 | 48 | 39 | 40 |

| Fund_turnover | Fund_turnover | ||||||

| Mean | 41% | 40% | 41% | Mean | 55% | 50% | 43% |

| Q1 | 61% | 60% | 55% | Q1 | 80% | 85% | 71% |

| Q5 | 19% | 17% | 17% | Q5 | 28% | 18% | 11% |

| Panel A: Euro Domestic Equity Mutual Funds | |||

| 2000–2007 | 2008–2011 | 2012–2014 * | |

| Average no. buys | 14,728 | 11,896 | 8635 |

| Average no. buys by fund | 141 | 131 | 137 |

| Average % important buys | 7.86% | 5.52% | 5.72% |

| Average no. sells | 14,106 | 13,536 | 6459 |

| Average no. sells by fund | 135 | 147 | 100 |

| Average % important sells | 7.32% | 6.69% | 7.20% |

| Panel B: Euro Non-Domestic Equity Mutual Funds | |||

| 2000–2007 | 2008–2011 | 2012–2014 * | |

| Average no. buys | 14,086 | 11,006 | 7877 |

| Average no. buys by fund | 198 | 155 | 176 |

| Average % important buys | 7.26% | 4.86% | 6.25% |

| Average no. sells | 15,479 | 14,454 | 6146 |

| Average no. sells by fund | 218 | 201 | 132 |

| Average % important sells | 5.44% | 4.47% | 5.05% |

| BUYS | SELLS | |||||

|---|---|---|---|---|---|---|

| Important Errors with 3-Month Alpha | Important Errors with 6-Month Alpha | Important Errors with 12-Month Alpha | Important Errors with 3-Month Alpha | Important Errors with 6-Month Alpha | Important Errors with 12-Month Alpha | |

| Constant | 0.0175 *** | 0.0082 *** | 0.0094 *** | 0.0209 *** | 0.0256 *** | 0.0103 *** |

| % Important errorsi,t−1 | 0.1060 *** | 0.0823 *** | 0.0799 *** | 0.2591 *** | 0.2042 *** | 0.1086 *** |

| Timet | −0.0004 ** | −0.0002 *** | −0.0005 *** | −0.0004 * | −0.0006 ** | −0.0003 *** |

| Sizei,t | −0.0015 * | −0.0012 *** | −0.0013 ** | 0.0008 | 0.0013 | −0.0006 |

| Agei,t | −0.0030 | 0.0011 | 0.0027 | 0.0019 | −0.0035 | −0.0009 |

| No. stocksi,t | −0.0003 *** | −0.0002 *** | −0.0003 *** | −0.0005 *** | −0.0005 *** | −0.0002 *** |

| Turnoveri,t | 0.0197 *** | 0.0199 *** | 0.0274 *** | 0.0214 *** | 0.0137 *** | 0.0071 *** |

| Market returnt | −0.0060 *** | −0.0074 *** | −0.0055 *** | −0.0089 *** | −0.0035 | −0.0013 *** |

| Wald Chi-Squared Test | 193.85 *** | 114.41 *** | 445.37 *** | 348.10 *** | 106.59 *** | 113.48 *** |

| Breusch–Pagan Test | 101.59 *** | 105.54 *** | 87.89 *** | 107.10 *** | 120.04 *** | 103.70 *** |

| Hausman Test | 22.10 *** | 29.11 *** | 26.33 *** | 19.92 *** | 21.67 *** | 28.80 *** |

| Sargan Test | 94.50 | 95.24 | 92.48 | 92.39 | 88.56 | 88.32 |

| Autocorrelation (1) | −2.42 ** | −2.31 ** | −2.36 ** | −4.32 *** | −4.87 *** | −3.45 *** |

| Autocorrelation (2) | 0.26 | 0.96 | 0.93 | 1.08 | 0.46 | −1.27 |

| No. observations | 1081 | 1049 | 966 | 1234 | 1216 | 1247 |

| BUYS | SELLS | |||||

|---|---|---|---|---|---|---|

| Important Errors with 3-Month Alpha | Important Errors with 6-Month Alpha | Important Errors with 12-Month Alpha | Important Errors with 3-Month Alpha | Important Errors with 6-Month Alpha | Important Errors with 12-Month Alpha | |

| Constant | 0.0267 *** | 0.0305 *** | 0.0137 ** | 0.0306 *** | 0.0385 *** | 0.0381 *** |

| % Important errorsi,t−1 | 0.0500 ** | 0.1018 *** | 0.1076 *** | 0.1120 *** | 0.1011 * | 0.1439 *** |

| Timet | −0.0002 | −0.0008 *** | −0.0007 *** | −0.0013 *** | −0.0013 *** | −0.0012 *** |

| Sizei,t | −0.0020 | −0.0029 *** | −0.0014 * | −0.0001 | −0.0022 ** | −0.0012 |

| Agei,t | −0.0021 | 0.0004 | 0.0067 | 0.0052 | 0.0072 | 0.0067 |

| No. stocksi,t | −0.0003 *** | −0.0004 *** | −0.0003 *** | −0.0005 *** | −0.0006 *** | −0.0006 *** |

| Turnoveri,t | 0.0091 *** | 0.0059 *** | 0.0092 *** | 0.0173 *** | 0.0177 *** | 0.0154 *** |

| Market returnt | −0.0067 *** | −0.0138 *** | 0.0013 | −0.0069 *** | −0.0086 *** | −0.0093 *** |

| Wald Chi-Squared Test | 66.65 *** | 139.77 *** | 50.47 *** | 102.74 *** | 88.93 *** | 86.84 *** |

| Breusch–Pagan Test | 14.03 *** | 15.50 *** | 14.42 *** | 10.82 *** | 21.15 *** | 14.78 *** |

| Hausman Test | 20.92 *** | 12.97 ** | 12.07 ** | 32.90 *** | 27.45 *** | 86.22 *** |

| Sargan Test | 77.09 | 39.98 | 23.08 | 79.78 | 69.64 | 16.83 |

| Autocorrelation (1) | −2.04 ** | −2.78 ** | −4.05 *** | −3.94 *** | −3.42 *** | −4.19 *** |

| Autocorrelation (2) | −1.42 | −0.39 | −0.50 | −1.89 | −1.87 | −1.42 |

| No. observations | 927 | 897 | 796 | 1050 | 1102 | 1143 |

| Panel A: Euro Domestic Equity Mutual Funds | ||||||

| Buys | Sells | |||||

| Important Errors 3-Month Alpha | Important Errors 6-Month Alpha | Important Errors 12-Month Alpha | Important Errors 3-Month Alpha | Important Errors 6-Month Alpha | Important Errors 3-Month Alpha | |

| Familyi,txTimet Negative and Stat. Significant β7 | 35.21% | 32.00% | 33.33% | 27.40% | 30.67% | 32.39% |

| Familyi,txTimet Non Significant β7 | 35.21% | 37.33% | 38.67% | 35.62% | 41.33% | 42.25% |

| Familyi,txTimet Positive and Stat. Significant β7 | 29.58% | 30.67% | 28.00% | 36.99% | 28.00% | 25.35% |

| Panel B: Euro Non-Domestic Equity Mutual Funds | ||||||

| Buys | Sells | |||||

| Important Errors 3-Month Alpha | Important Errors 6-Month Alpha | Important Errors 12-Month Alpha | Important Errors 3-Month Alpha | Important Errors 6-Month Alpha | Important Errors 3-Month Alpha | |

| Familyi,txTimet Negative and Stat. Significant β7 | 30.65% | 37.78% | 23.88% | 17.91% | 35.94% | 30.65% |

| Familyi,txTimet Non Significant β7 | 25.81% | 24.44% | 17.91% | 29.85% | 26.56% | 27.42% |

| Familyi,txTimet Positive and Stat. Significant β7 | 43.55% | 37.78% | 58.21% | 52.24% | 37.50% | 41.94% |

| BUYS | SELLS | |||||

|---|---|---|---|---|---|---|

| Important Errors with 3-Month Alpha | Important Errors with 6-Month Alpha | Important Errors with 12-Month Alpha | Important Errors with 3-Month Alpha | Important Errors with 6-Month Alpha | Important Errors with 12-Month Alpha | |

| Constant | 0.0271 *** | 0.0085 *** | 0.0137 *** | 0.0094 *** | 0.0143 *** | 0.0209 *** |

| % Important errorsi,t−1 | 0.1008 *** | 0.0730 *** | 0.0700 *** | 0.0912 *** | 0.1850 *** | 0.0838 *** |

| Timet | −0.0005 ** | −0.0003 *** | −0.0007 *** | −0.0002 ** | −0.0003 ** | −0.0003 ** |

| Sizei,t | −0.0010 | −0.0011 ** | −0.0010 ** | −0.0009 ** | 0.0009 ** | 0.0016 ** |

| Agei,t | −0.0159 *** | 0.0008 | −0.0003 | −0.0011 | 0.0029 | −0.0066 |

| No. stocksi,t | −0.0002 *** | −0.0002 *** | −0.0003 *** | −0.0002 *** | −0.0004 *** | −0.0003 *** |

| Turnoveri,t | 0.0206 *** | 0.0202 *** | 0.0285 *** | 0.0177 *** | 0.0158 *** | 0.0077 *** |

| Market returnt | −0.0051 *** | −0.0072 *** | −0.0069 *** | −0.0041 *** | −0.0040 *** | −0.0015 |

| TOP-10i,txTimet | 0.0008 ** | 0.0004 *** | 0.0004 *** | 0.0001 | −0.0001 | 0.0003 |

| Wald Chi-Squared Test | 396.44 *** | 118.83 *** | 446.14 *** | 493.53 *** | 368.74 *** | 254.43 *** |

| Breusch–Pagan Test | 103.82 *** | 17.21 *** | 16.53 *** | 39.44 *** | 54.49 *** | 76.59 *** |

| Hausman Test | 19.03 *** | 36.22 *** | 33.63 *** | 28.48 *** | 9.02 ** | 9.09 ** |

| Sargan Test | 93.14 | 93.77 | 89.18 | 96.64 | 89.75 | 89.15 |

| Autocorrelation (1) | −2.42 ** | −2.32 ** | −2.36 ** | −4.28 *** | −4.87 *** | −3.46 *** |

| Autocorrelation (2) | 0.24 | 0.34 | 0.96 | 1.77 | 0.46 | −1.29 |

| No. observations | 1081 | 1049 | 966 | 1234 | 1216 | 1247 |

| BUYS | SELLS | |||||

|---|---|---|---|---|---|---|

| Important Errors with 3-Month Alpha | Important Errors with 6-Month Alpha | Important Errors with 12-Month Alpha | Important Errors with 3-Month Alpha | Important Errors with 6-Month Alpha | Important Errors with 12-Month Alpha | |

| Constant | 0.0285 *** | 0.0319 *** | 0.0394 *** | 0.0311 *** | 0.0336 *** | 0.0394 *** |

| % Important errorsi,t−1 | 0.0418 *** | 0.0502 *** | 0.1907 *** | 0.1125 *** | 0.1475 *** | 0.1907 *** |

| Timet | −0.0001 | −0.0005 ** | −0.0010 ** | −0.0012 *** | −0.0011 *** | −0.0010 ** |

| Sizei,t | −0.0016 | −0.0024 | 0.0002 | −0.0001 | −0.0006 | 0.0002 |

| Agei,t | −0.0041 | −0.0087 ** | 0.0037 | 0.0049 | 0.0093 | 0.0037 |

| No. stocksi,t | −0.0003 *** | −0.0003 *** | −0.0007 *** | −0.0005 *** | −0.0007 *** | −0.0007 *** |

| Turnoveri,t | 0.0096 *** | 0.0087 ** | 0.0173 *** | 0.0173 *** | 0.0189 *** | 0.0173 *** |

| Market returnt | −0.0065 *** | −0.0122 *** | −0.0079 *** | −0.0069 *** | −0.0075 *** | −0.0079 *** |

| TOP-10i,txTimet | −0.0007 | 0.0001 | 0.0001 | −0.0001 | 0.0001 | 0.0001 |

| Wald Chi-Squared Test | 554.90 *** | 518.39 *** | 503.90 *** | 103.34 *** | 109.49 *** | 123.80 *** |

| Breusch–Pagan Test | 14.54 *** | 25.08 *** | 14.75 *** | 65.05 *** | 48.54 *** | 60.98 *** |

| Hausman Test | 81.85 *** | 20.22 *** | 19.90 *** | 19.55 *** | 23.71 *** | 22.90 *** |

| Sargan Test | 80.48 | 48.72 | 84.30 | 77.40 | 81.36 | 84.30 |

| Autocorrelation (1) | −2.10 ** | −3.05 *** | −4.61 *** | −3.93 *** | −3.51 *** | −4.61 *** |

| Autocorrelation (2) | −0.88 | 0.24 | −1.06 | −1.89 | −1.73 | −1.06 |

| No. observations | 927 | 897 | 796 | 1050 | 1102 | 1143 |

| BUYS | SELLS | |||||

|---|---|---|---|---|---|---|

| Important Errors with 3-Month Alpha | Important Errors with 6-Month Alpha | Important Errors with 12-Month Alpha | Important Errors with 3-Month Alpha | Important Errors with 6-Month Alpha | Important Errors with 12-Month Alpha | |

| Constant | 0.0096 *** | 0.0078 *** | 0.0092 *** | 0.0207 *** | 0.0270 *** | 0.0097 ** |

| % Important errorsi,t−1 | 0.0984 *** | 0.0835 *** | 0.0753 *** | 0.2653 *** | 0.2114 *** | 0.1593 *** |

| Timet | −0.0003 *** | −0.0002 ** | 0.0005 *** | −0.0005 ** | −0.0007 *** | −0.0006 *** |

| Sizei,t | −0.0008 * | −0.0012 ** | −0.0012 ** | 0.0009 | 0.0013 | 0.0008 |

| Agei,t | −0.0016 | 0.0007 | 0.0021 | 0.0015 | −0.0049 | −0.0004 |

| No. stocksi,t | −0.0002 *** | −0.0002 *** | −0.0007 *** | −0.0005 *** | −0.0005 *** | −0.0002 *** |

| Turnoveri,t | 0.0183 *** | 0.0199 *** | 0.0279 *** | 0.0222 *** | 0.0153 *** | 0.0075 ** |

| Market returnt | −0.0036 *** | −0.0074 *** | −0.0054 *** | −0.0090 *** | −0.0038 ** | −0.0014 * |

| Independenti,txTimet | 0.0009 * | 0.0004 ** | 0.0008 | 0.0011 * | 0.0012 ** | 0.0015 ** |

| Wald Chi-Squared Test | 732.02 *** | 113.53 *** | 464.11 *** | 347.03 *** | 220.56 *** | 611.20 *** |

| Breusch–Pagan Test | 93.48 *** | 39.59 *** | 39.72 *** | 63.68 *** | 63.55 *** | 62.54 *** |

| Hausman Test | 23.79 *** | 41.63 *** | 32.22 *** | 23.05 *** | 23.28 *** | 23.75 *** |

| Sargan Test | 96.87 | 94.46 | 92.86 | 96.41 | 91.05 | 88.62 |

| Autocorrelation (1) | −2.42 ** | −2.31 ** | −2.37 ** | −4.27 *** | −4.87 *** | −3.45 *** |

| Autocorrelation (2) | 0.25 | 0.95 | 0.93 | 1.81 | 0.48 | −1.28 |

| No. observations | 1081 | 1049 | 966 | 1234 | 1216 | 1247 |

| BUYS | SELLS | |||||

|---|---|---|---|---|---|---|

| Important Errors with 3-Month Alpha | Important Errors with 6-Month Alpha | Important Errors with 12-Month Alpha | Important Errors with 3-Month Alpha | Important Errors with 6-Month Alpha | Important Errors with 12-Month Alpha | |

| Constant | 0.0348 *** | 0.0298 *** | 0.0139 ** | 0.0302 *** | 0.0332 *** | 0.0387 *** |

| % Important errorsi,t−1 | 0.0209 * | 0.0563 ** | 0.0978 ** | 0.1125 *** | 0.1504 *** | 0.1920 *** |

| Timet | −0.0004 | −0.0006 ** | −0.0006 ** | −0.0013 *** | −0.0011 *** | −0.0008 ** |

| Sizei,t | −0.0028 *** | −0.0026 | −0.0013 | −0.0001 | −0.0006 | 0.0001 |

| Agei,t | −0.0007 | −0.0056 | 0.0061 | 0.0058 | 0.0089 | 0.0037 |

| No. stocksi,t | −0.0005 *** | −0.0003 *** | −0.0002 *** | −0.0005 *** | −0.0007 *** | −0.0007 *** |

| Turnoveri,t | 0.0079 *** | 0.0071 * | 0.0090 *** | 0.0174 *** | 0.0190 *** | 0.0174 *** |

| Market returnt | −0.0074 *** | −0.0127 *** | 0.0013 | −0.0069 *** | −0.0075 *** | −0.0081 *** |

| Independenti,txTimet | −0.0006 | −0.0003 | −0.0008 | −0.0003 | 0.0001 | −0.0006 |

| Wald Chi-Squared Test | 745.40 *** | 216.29 *** | 525.50 *** | 102.21 *** | 108.18 *** | 122.71 *** |

| Breusch–Pagan Test | 60.96 *** | 28.91 *** | 39.35 *** | 48.54 *** | 58.33 *** | 52.95 *** |

| Hausman Test | 25.98 *** | 25.70 *** | 27.75 *** | 26.78 *** | 31.89 *** | 25.22 *** |

| Sargan Test | 80.13 | 53.67 | 60.33 | 78.76 | 80.90 | 84.56 |

| Autocorrelation (1) | −2.06 ** | −3.10 *** | −4.02 *** | −3.94 *** | −3.50 ** | −4.62 *** |

| Autocorrelation (2) | −1.06 | 0.31 | −0.54 | −1.89 | −1.69 | −1.05 |

| No. observations | 927 | 897 | 796 | 1,050 | 1,102 | 1,143 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gimeno, R.; Sarto, J.L.; Vicente, L. You Learn When It Hurts: Evidence in the Mutual Fund Industry. J. Risk Financial Manag. 2022, 15, 33. https://doi.org/10.3390/jrfm15010033

Gimeno R, Sarto JL, Vicente L. You Learn When It Hurts: Evidence in the Mutual Fund Industry. Journal of Risk and Financial Management. 2022; 15(1):33. https://doi.org/10.3390/jrfm15010033

Chicago/Turabian StyleGimeno, Ruth, José Luis Sarto, and Luis Vicente. 2022. "You Learn When It Hurts: Evidence in the Mutual Fund Industry" Journal of Risk and Financial Management 15, no. 1: 33. https://doi.org/10.3390/jrfm15010033