Factors Influencing Investments into Human Resources to Support Company Performance

Abstract

:1. Introduction

2. Theoretical Background

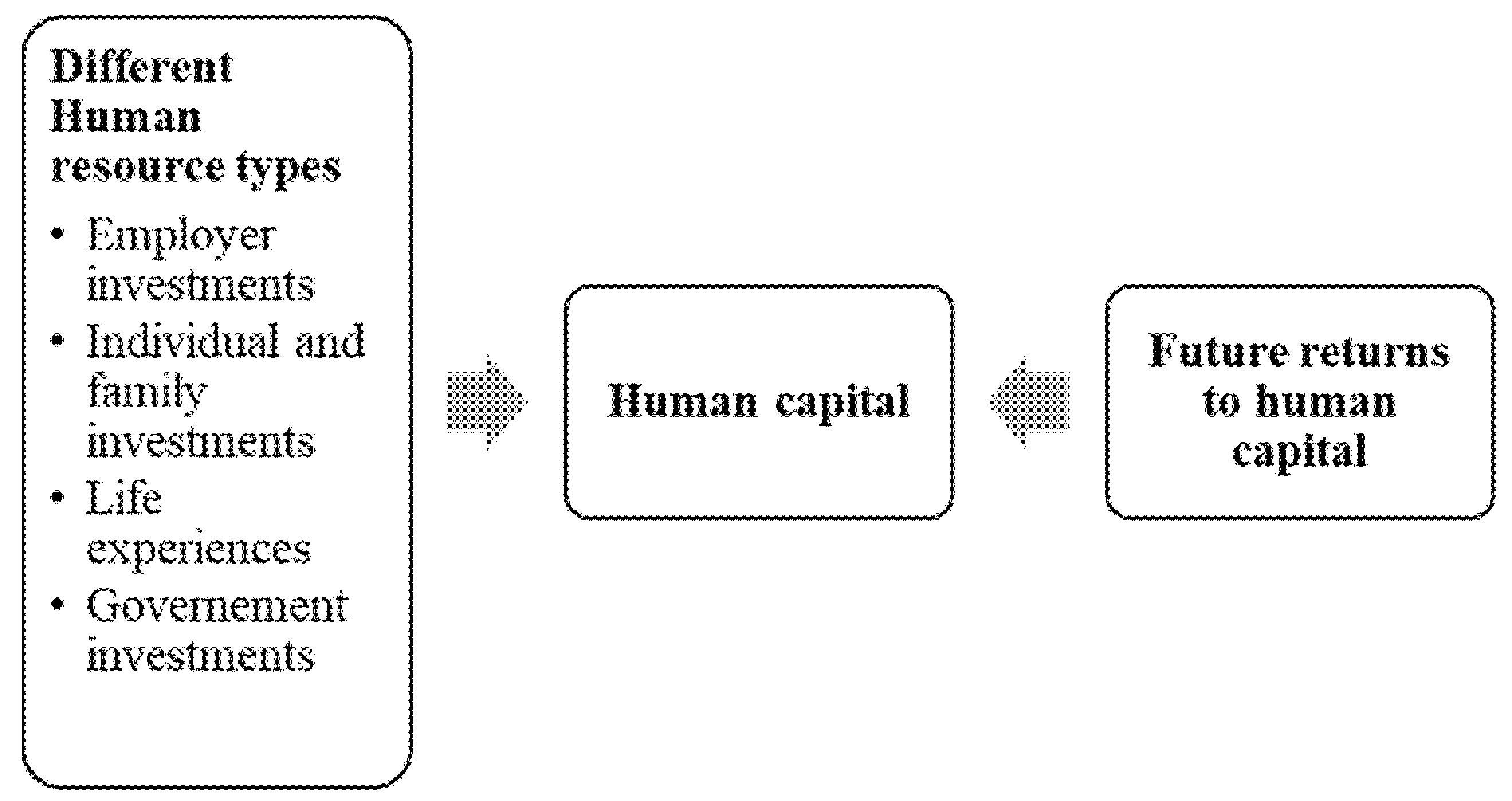

2.1. Human Resources as Investment

2.2. Human Resources Invesments and Relationship to Business Performance

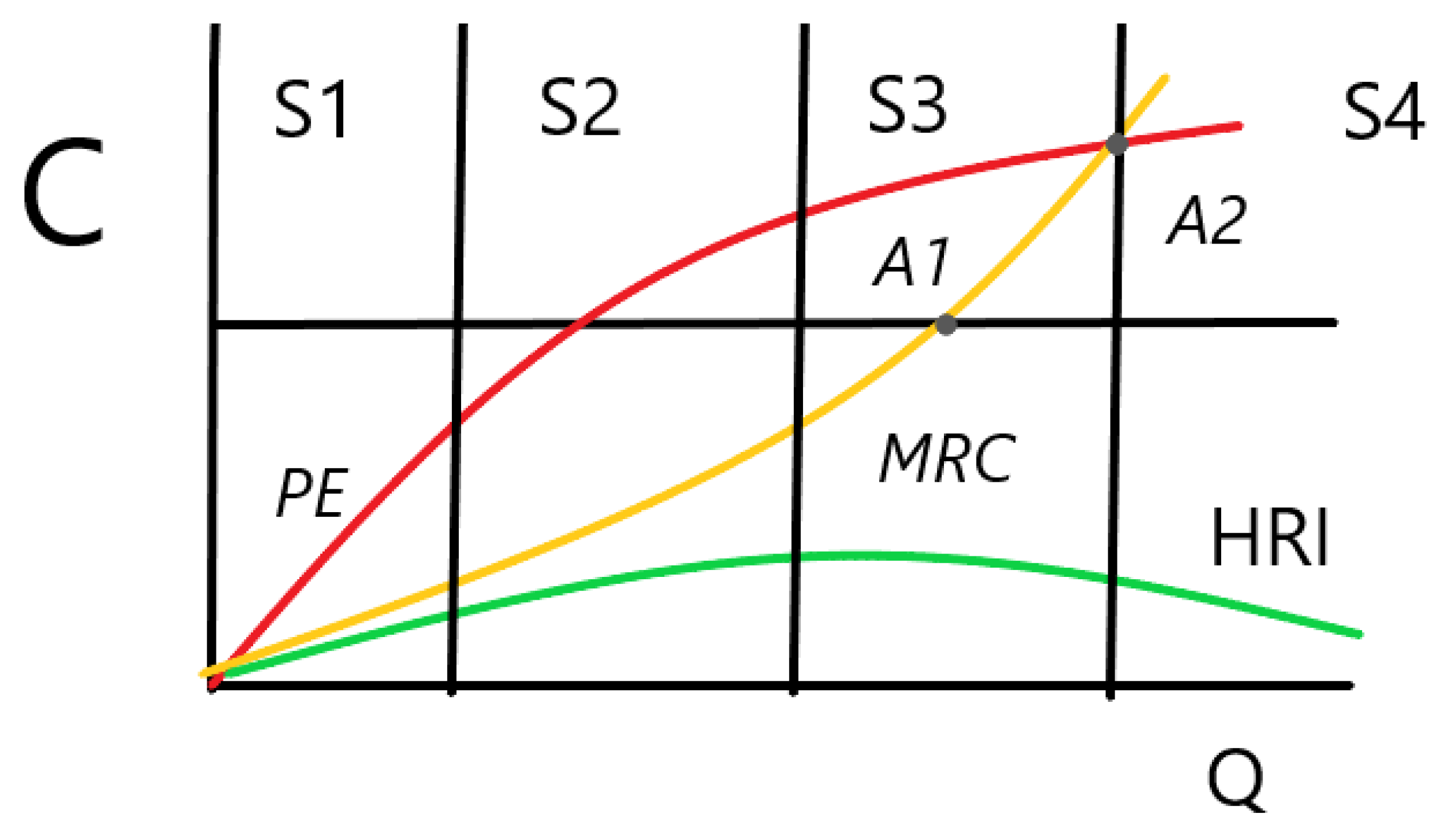

Measurement of Human Resources Investment

3. Materials and Methods

Research Methodology and Data Description

4. Results

4.1. Analysis of Profit Investments

4.2. Archetypes Creation

5. Discussion and Conclusions

5.1. Contribution to Business Practice

- Investment in HR = 1000 × 0.477 × 0.2 = 95.40 EUR

- 1/7 return = 95.4/7 = 13.63 EUR/year; i.e., 13.63 percent/year

5.2. Contribution to Theoretical Background

5.3. Limitation of the Study

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Conflicts of Interest

References

- Almeida, Rita, and Pedro Carneiro. 2009. The return to firm investments in human capital. Labour Economics 16: 97–106. [Google Scholar] [CrossRef] [Green Version]

- Amit, Raphael, and Paul J. H. Schoemaker. 1993. Strategic assets and organizational rent. Strategic Management Journal 14: 33–46. [Google Scholar] [CrossRef]

- Ashenfelter, Orley, Colm Harmon, and Hessel Oosterbeek. 2003. A Review of Estimates of the Schooling/Earnings Relationship, with Tests for Publication Bias. Cambridge: National Bureau of Economic Research, pp. 1–24. [Google Scholar]

- Bapna, Ravi, Nishtha Langer, Amit Mehra, Ram Gopal, and Alok Gupta. 2013. Human Capital Investments and Employee Performance: An Analysis of IT Services Industry. Management Science 59: 641–58. [Google Scholar] [CrossRef] [Green Version]

- Bruce-Lockhart, Anna. 2016. Why Do We Call It Human Capital. World Economic Forum. Available online: https://medium.com/world-economic-forum/why-do-we-call-it-human-capital-dbf0077ab150 (accessed on 23 June 2019).

- Bruun, Eric Christian. 2013. Better Public Transit Systems: Analyzing Investments and Performance. London: Routledge. [Google Scholar]

- Bumberová, Veronika, and František Milichovský. 2020. Influence of Determinants on Innovations in Small KIBS Firms in the Czech Republic before COVID-19. Sustainability 12: 7856. [Google Scholar] [CrossRef]

- Castanias, Richard, and Constance Helfat. 1991. Managerial Resources and Rents. Journal Management 17: 155–71. [Google Scholar] [CrossRef]

- Coff, Russell W. 1997. Human assets and management dilemmas: Coping with hazards on the road to resource-based theory. Academy of Management Review 22: 374–402. [Google Scholar] [CrossRef]

- Conti, Gabriella. 2005. Training, productivity and wages in Italy. Labour Economics 12: 557–76. [Google Scholar] [CrossRef]

- Cornachione, Edgard. 2010. Investing in human capital: Integrating Intellectual capital architecture utility theory. The Journal of Human Resource and Adult Learning 6: 29–40. [Google Scholar]

- Corrocher, Nicoletta, Lucia Cusmano, and Andrea Morrison. 2009. Modes of innovation in knowledge-Intensive business services evidence from Lombardy. Journal of Evolutionary Economics 19: 173–96. [Google Scholar] [CrossRef]

- D’Este, Pablo, Simona Iammarino, Maria Savona, and Nick von Tunzelmann. 2012. What hampers innovation? Revealed barriers versus deterring barriers. Research Policy 41: 482–88. [Google Scholar] [CrossRef]

- Dearden, Lorraine, Howard Reed, and John Van Reenen. 2006. The impact of training on productivity and wages: Evidence from British Panel Data. Oxford Bulletin of Economics and Statistics 68: 397–421. [Google Scholar] [CrossRef] [Green Version]

- Dvořák, Marek, Patrik Rovný, Veronika Grebennikova, and Marina Faminskaya. 2020. Economic impacts of Covid-19 on the labor market and human capital. Terra Economicus 18: 78–96. [Google Scholar] [CrossRef]

- Dvouletý, Ondřej, and Ivana Blažková. 2020. Determinants of competitiveness of the Czech SMEs: Findings from the global competitiveness project. Competitiveness Review, ahead-of-print. [Google Scholar] [CrossRef]

- European Commission. 2017. Investment In Human Capital. Assessing the Efficiency of Public Spending on Education. pp. 1–11. Available online: https://www.consilium.europa.eu/media/31409/investment-in-human-capital_eurogroup_31102017_ares.pdf (accessed on 30 October 2021).

- Fadhil, Rahmat, M. Syamsul Maarif, Tajuddin Bantacut, and Aji Hermawan. 2017. Model strategi pengembangan sumber daya manusia agroindustri kopi gayo dalam menghadapi masyarakat ekonomi ASEAN. Journal of Technology Management 16: 141–55. [Google Scholar] [CrossRef]

- Galunic, D. Charles, and Erin Anderson. 2000. From Security to Mobility: Generalized Investments in Human Capital and Agent Commitment. Organization Science 11: 1–20. [Google Scholar] [CrossRef]

- Ghemawat, Pankaj. 1986. Sustainable Advantage. Harvard Business Review 64: 53–58. [Google Scholar]

- Givoni, Moshe. 2014. Better Public Transit Systems—Analyzing Investments and Performance. Abingdon: Taylor & Francis. [Google Scholar]

- Grant, Robert M. 1996. Toward a Knowledge-Based Theory of the Firm. Strategic Management Journal 17: 109–22. [Google Scholar] [CrossRef]

- Haak-Saheem, Washika, and Marion Festing. 2020. Human resource management–A national business system perspective. The International Journal of Human Resource Management 31: 1863–90. [Google Scholar] [CrossRef]

- Hatch, Nile W., and Jeffrey D. Dyer. 2004. Human Capital and Learning as a Source of Sustainable Competitive Advantage. Strategic Management Journal 25: 1155–78. [Google Scholar] [CrossRef]

- Hazelkorn, Ellen, and Jeroen Huisman. 2008. Higher Education in the 21st Century–Diversity of Missions. Higher Education Policy 21: 147–50. [Google Scholar] [CrossRef]

- Heckman, James, Lance Lochner, and Christopher Taber. 1998. Tax Policy and Human Capital Formation. NBER Working Paper No. W6462. Cambridge: NBER. [Google Scholar]

- Heri, Eko Indra. 2019. Tantangan Pengembangan SDM Polri di Era Revolusi Industri 4.0. Jurnal Ilmu Kepolisian 13: 16. [Google Scholar]

- Hite, Linda M., and Kimberley S. McDonald. 2020. Careers after COVID-19: Challenges and changes. Human Resource Development International 23: 427–37. [Google Scholar] [CrossRef]

- Ichsan, Reza Nurul, Khaeruman, Sonny Santosa, Yuni Shara, and Fahrina Yustiasari Liriwati. 2020. Investigation of Strategic Human Resource Management Practices in Business after COVID-19 Disruption. PalArch’s Journal of Archaeology of Egypt/Egyptology 17: 13098–110. [Google Scholar]

- Irfan, Syed M., and Faysal Qadeer. 2020. Employers Investments in Job Crafting for Sustainable Employability in Pandemic Situation Due to COVID-19: A Lens of Job Demands-Resources Theory. Journal of Business & Economics 12: 124–40. [Google Scholar] [CrossRef]

- Susan E., Jackson, Deniz S. Ones, and Stephan Dilchert. 2012. Managing Human Resources for Environmental Sustainability. Hoboken: John Wiley & Sons, vol. 32. [Google Scholar]

- Jílková, Petra. 2021. Sustainable Corporate Strategy: The Role of Human Capital in the Time of COVID-19 Crisis. TEM Journal 10: 699–706. [Google Scholar] [CrossRef]

- Keeley, Brian. 2007. Human Capital. OECD Insights. Available online: https://www.oecd-ilibrary.org/education/human-capital_9789264029095-en (accessed on 20 October 2021).

- Kolumber, Štefan, and Lenka Tkačíková. 2020. Measuring Company Performance by Using the Balance Scorecard Concept. Paper presented at International Days of Science 2020—Economics, Management, Innovation, the International Scientific Conference, Olomouc, Czech Republic, November 12–13. [Google Scholar]

- Kolumber, Štefan, and Petr Briš. 2014. Improving the Competitiveness of Organizations by Using a Link between Established Quality Management System and Balanced Scorecard. Paper presented at 4th International Conference on Industrial Engineering and Operations Management, Bali, Indonesia, January 7–9; pp. 1982–89. [Google Scholar]

- Krejčí, Petra. 2018. Alternative approach for evaluation of innovations: Pure and combined innovations in social enterprises. Paper presented at 11th International Scientific Conference “Karviná Ph.D. Conference on Business and Economics”, Karviná, Czech Republic, November 7–9. [Google Scholar]

- Kucharcikova, Alzbeta. 2014. Investment in the human capital as the source of economic growth. Periodica Polytechnica 22: 29–35. [Google Scholar] [CrossRef] [Green Version]

- Lentjushenkova, Oksana, and Inga Lapina. 2014. The Classification of the Intellectual Capital Investments of an Enterprise. Procedia-Social and Behavioral Sciences 156: 53–57. [Google Scholar] [CrossRef] [Green Version]

- Lillard, Lee, and Hong Tan. 1986. Training: Who Gets It and What Are Its Effects on Employment and Earnings? Santa Monica: RAND Corporation. [Google Scholar]

- MacGregor Pelikánová, Radka. 2019. Corporate Social Responsibility Information in Annual Reports in the EU—A Czech Case Study. Sustainability 11: 237. [Google Scholar] [CrossRef] [Green Version]

- Markjackson, Dumani, and Alhassan Odiniya Innocent. 2020. An Exploratory Study On Human Capital Investments. International Journal of Scientific and Research Publications (IJSRP) 10: 663–67. [Google Scholar] [CrossRef]

- Matiušaitytė, Raimundė, and Ingrida Šarkiūnaitė. 2003. Human capital significance for economy and management. Tiltai. Priedas 2: 293–304. [Google Scholar]

- Mikhailov, Fedor B., Olena V. Yurieva, and Dmitrii A. Miasnikov. 2018. Human capital development strategies in conditions of accelerating diffusion of technical innovation under influence processes of globalization, Globalization and Its Socio-Economic Consequences. Paper presented at 18th International Scientific Conference, PTS I–VI, Žilina, Slovakia, October 2–4; pp. 2236–43. [Google Scholar]

- Mikhailov, Fedor, and Dmitrii Miasnikov. 2019. The Importance of Investments in Human Capital in the Process of Innovation in Production. Advances in Economics, Business and Management Research 131: 1–9. [Google Scholar]

- OECD. 2012. Policy Framework for Investment User’s Toolkit. Chapter 8. Human Resource Development. pp. 1–37. Available online: https://www.oecd.org/investment/toolkit/policyareas/humanresourcedevelopment/Chapter%208%20HR%20Development.pdf (accessed on 10 November 2021).

- OECD. 2020. Pillar B–Entrepreneurial human capital. In SME Policy Index: Eastern Partner Countries 2020: Assessing the Implementation of the Small Business Act for Europe. Paris: OECD Publishing, Brussels: European Union. [Google Scholar] [CrossRef]

- Pakšiová, Renata, and Denisa Oriskóová. 2020. Capital Maintenance Evolution using Outputs from Accounting System. Scientific Annals of Economics and Business 67: 311–31. [Google Scholar] [CrossRef]

- Pan, Shan L., and Sixuan Zhang. 2020. From fighting COVID-19 pandemic to tackling sustainable development goals: An opportunity for responsible information systems research. International Journal of Information Management 55: 102196. [Google Scholar] [CrossRef]

- Petković, Miloš, Bojan Krstić, and Tamara Rađenović. 2021. Intellectual Capital Investments as the Driver of Future Company Performance. Ekonomika 67: 13–22. [Google Scholar] [CrossRef]

- Pokorná, Pavla. 2020. Financial Sources for Company Scale-Up. In Developing Entrepreneurial Competencies for Start-Ups and Small Business. Hershey: IGI Global, pp. 97–108. [Google Scholar]

- Popescu, Cristina Raluca Gh. 2019a. Intellectual Capital, Integrated Strategy and Performance: Focusing on Companies’ Unique Value Creation Mechanism and Promoting Better Organizational Reporting In Romania: A Framework Dominated by the Impact of Green Marketing and Green Marketing Strategies. Paper presented at 33rd International-Business-Information-Management-Association (IBIMA) Conference, Granada, Spain, April 10–11; pp. 1540–55. [Google Scholar]

- Popescu, Cristina Raluca Gh. 2019b. Intellectual Capital: Major Role, Key Importance and Decisive Influences on Organizations’ Performance. Journal of Human Resources Management Research 2019: 509857. [Google Scholar] [CrossRef]

- Popescu, Cristina Raluca Gh. 2020. Sustainability Assessment: Does the OECD/G20 Inclusive Framework for BEPS (Base Erosion and Profit Shifting Project) Put an End to Disputes over the Recognition and Measurement of Intellectual Capital? Sustainability 12: 10004. [Google Scholar] [CrossRef]

- Popescu, Cristina Raluca Gh., and Jarmila Duháček Šebestová. 2022. Fiscally Responsible Businesses as a Result of COVID-19 Pandemic Shock: Taking Control of Countries’ Tax Systems by Putting an End to Corporate Tax Evasion and Tax Havens. In Handbook of Research on Changing Dynamics in Responsible and Sustainable Business in the Post-COVID-19 Era. Hershey: IGI Global, pp. 161–92. [Google Scholar] [CrossRef]

- Popescu, Cristina Raluca Gh., and Gheorghe N. Popescu. 2019. An exploratory study on a questionnaire concerning green and sustainable finance, corporate social responsibility, and performance: Evidence from the Romanian business environment. Journal of Risk and Financial Management 12: 162. [Google Scholar] [CrossRef] [Green Version]

- Prakapavičiūtė, Justina, and Renata Korsakienė. 2016. The investigation of human capital and investments into human capital: Lithuania in the context of the EU. Entrepreneurship and Sustainability Issues 3: 350–67. [Google Scholar] [CrossRef]

- Psacharopoulos, George, and Harry Anthony Patrinos. 2004. Returns to Investment in Education: A Further Update. Education Economics 12: 111–34. [Google Scholar] [CrossRef] [Green Version]

- Sawulski, Jakub, and Wojtek Paczos. 2021. Investments in Human Capital Should Be at the Heart of Europe’s Covid-19 Recovery Strategy. LSE European Politics and Policy (EUROPP) Blog. Available online: https://blogs.lse.ac.uk/europpblog/2021/07/30/investments-in-human-capital-should-be-the-heart-of-europes-covid-19-recovery-strategy/ (accessed on 20 October 2021).

- Sichel, D. 2008. Intangible Capital. In The Palgrave Dictionary of Economics, 2nd ed. London: Palgrave Macmillan. [Google Scholar]

- Stroombergen, Adolf, William Dennis Rose, and Ganesh Nana. 2003. Review of the Statistical Measurement of Human Capital. Wellington: Statistics New Zealand, Infometrics Consulting, Business and Economic Research Ltd. [Google Scholar]

- Su, Yaqin, and Zhiqiang Liu. 2016. The impact of foreign direct investment and human capital on economic growth: Evidence from Chinese cities. China Economic Review 37: 97–109. [Google Scholar] [CrossRef]

- Tadic, Ivana, Željana Aljinović Barac, and Nikolina Plazonic. 2015. Relations between human capital investments and business excellence in Croatian companies. International Journal of Mechanical and Industrial Engineering 9: 850–55. [Google Scholar]

- Teece, David J., Gary Pisano, and Amy Shuen. 1997. Dynamic capabilities and strategic management. Strategic Management Journal 18: 509–33. [Google Scholar] [CrossRef]

- Toumashev, A. R., M. V. Toumasheva, E. R. Valeev, and D. A. Miasnikov. 2015. Development of Russian economy in conditions of globalization and investment policy. Mediterranean Journal of Social Sciences 6: 700–4. [Google Scholar] [CrossRef] [Green Version]

- Umana, Etebong Attah, Ijeoma Catherine Okoli, Ubong Udo-Johnson Mbak, Ikenna Anthony Onah, and Rasheed Olanrewaju Zubair. 2021. Investigating the Impact of Covid-19 on Human Resource Development and Management of Godfather Investments Ltd., Calabar, Nigeria. International Journal of Public Administration and Management Research 6: 25–39. [Google Scholar] [CrossRef]

- Vodák, Jozef, and Alžbeta Kucharčíková. 2011. Efektivní vzdělávání zaměstnanců. 2., aktualiz. a rozš. vyd. Praha: Grada. [Google Scholar]

- Werner, Jon M., and Rendy L. DeSimone. 2012. Human Resource Development. Boston: Cengage Learning. [Google Scholar]

- World Bank. 2020. The Human Capital Index 2020 Update: Human Capital in the Time of COVID-19. Washington, DC: World Bank, Available online: https://openknowledge.worldbank.org/handle/10986/34432 (accessed on 1 November 2021).

- Wotschack, Philip. 2020. When do companies train low-skilled workers? The role of institutional arrangements at the company and sectoral level. British Journal of Industrial Relations 58: 587–616. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

| Author/s | Study Description | Study Orientation (Company vs. Employees) |

|---|---|---|

| Keeley (2007) | HR return ratio | Company view |

| Werner and DeSimone (2012) | Relationship between HR management, profit and company strategy | Company view |

| Jackson et al. (2012) | HR management improvements | Company/employee view |

| Bruun (2013) | Employee abilities and evaluation | Employee view |

| Givoni (2014) | Evaluation of competencies | Employee view |

| Fadhil et al. (2017) | Models of HR development | Employee view |

| Heri (2019) | HR development and public sector influence | Company/employee view |

| Hite and McDonald (2020) | Relationship of company strategy on HR managers | Employee view |

| Wotschack (2020) | Training of low-skilled staff to support employment | Employee view |

| Pan and Zhang (2020) | Internal processes of HR management | Employee view |

| Haak-Saheem and Festing (2020) | International importance of HR development and company profit | Company/employee view |

| Ichsan et al. (2020) | Strategy goals vs. HR development | Company view |

| Umana et al. (2021) | 102 respondents, COVID-19 influence on training of employees and company productivity, employee point of view | Employee view |

| Jílková (2021) | Company working benefits, COVID-19 influence | Employee view |

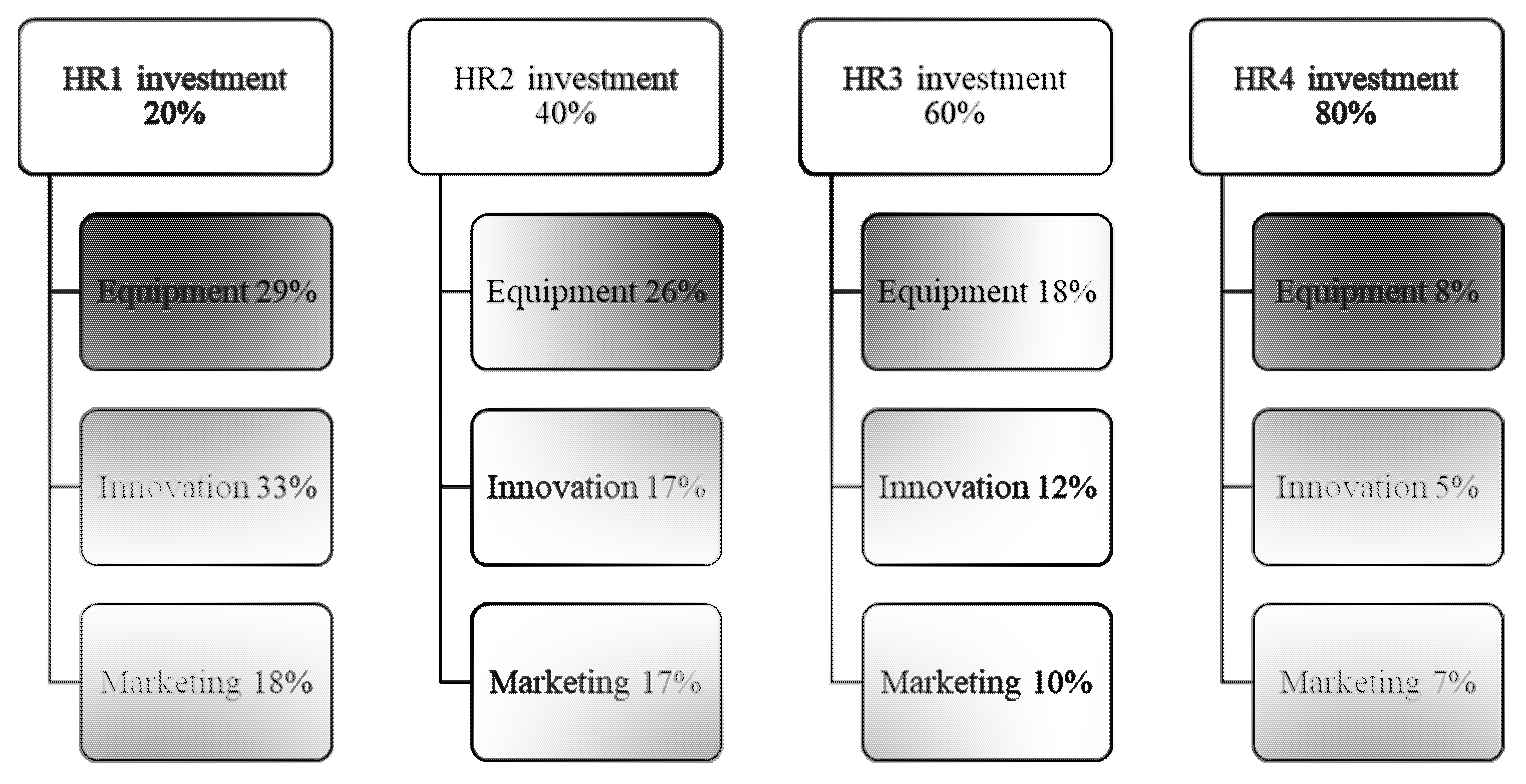

| Profit Investment Group (PIG) | PIG1:20% | PIG2:40% | PIG3:60% | PIG4:80% | Total Respondents |

|---|---|---|---|---|---|

| HR1 investment 20%, (N = 192) | 26% | 31% | 21% | 22% | 192 |

| HR2 investment 40%, (N = 56) | 20% | 35.5% | 24.5% | 20% | 56 |

| HR3 investment 60%, (N = 19) | 21% | 16% | 42% | 21% | 19 |

| HR4 investment 80%, (N = 11) | 9.5% | 45% | 9.5% | 36% | 11 |

| Archetype | Innovations First | People and Work | People-Oriented | People in the First Place |

|---|---|---|---|---|

| HR investment 20% | HR investment 40% | HR investment 60% | HR investment 80% | |

| Personal profile | ||||

| Business owner | Man | Man | Man | Man |

| Age | 41–55 | 26–40 | 26–40 | 41–55 |

| Business experience (years) | 20+ years | till 10 years | 10–20 years | till 10 years |

| Education | University | Secondary school | Secondary school | University |

| Main motives to invest profit into HR | ||||

| Interest rates in bank | √ | × | √ | × |

| Payback period | √√ | √√ | √√ | √ |

| Tax reduction | √ | √ | √ | ×× |

| Efficiency analysis (value-added) | √√ | √√ | √√ | √√ |

| Competitive advantage | √ | √ | √√ | √√ |

| Financial decisions based on indicators | √ | √ | √ | √√ |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Šebestová, J.D.; Popescu, C.R.G. Factors Influencing Investments into Human Resources to Support Company Performance. J. Risk Financial Manag. 2022, 15, 19. https://doi.org/10.3390/jrfm15010019

Šebestová JD, Popescu CRG. Factors Influencing Investments into Human Resources to Support Company Performance. Journal of Risk and Financial Management. 2022; 15(1):19. https://doi.org/10.3390/jrfm15010019

Chicago/Turabian StyleŠebestová, Jarmila Duháček, and Cristina Raluca Gh. Popescu. 2022. "Factors Influencing Investments into Human Resources to Support Company Performance" Journal of Risk and Financial Management 15, no. 1: 19. https://doi.org/10.3390/jrfm15010019