4.1. Evolution of Debates Concerning BD and DA in the Area of MA

The interest in DA of management accounting researchers is in an emerging phase; for this reason, papers from 2010–2016 are mostly conceptual. Starting with 2017 research interest in empirical quantitative management accounting has increased considerably; thus, case studies based on semi-structured interviews are revealing more as regard the MA perception about BD and DA (

i.e., Arnaboldi et al. 2017b;

Andreassen 2020;

Bergmann et al. 2020). The general conclusion of the studies is that not enough is known about how MAs are using DA, specifically, what tools they utilize, what type of analysis is being performed and what skills and competencies are required. DA represents, undeniably, a relatively new responsibility for MAs.

The scientific publications analyzed are from accounting and management area scientific journals, with three dedicated issues in top journals Accounting Horizons, Accounting, Auditing and Accountability Journal and Journal of Management Control.

In 2015, Accounting Horizons launched, in volume 29 issue 2, a forum dedicated to BD’s impact on accounting and audit.

Griffin and Wright (

2015), in the forum’s opening, consider BD as one of the profession’s most pressing and unyielding challenges (

Griffin and Wright 2015). BD and DA allow companies to process a billion data elements daily to comprehend their competitive environment for significant decision-making and business strategies. BD and DA fundamentally change the way companies understand and report information.

Vasarhelyi et al. (

2015) draw an overall framework of BD in accounting and auditing, concentrating on sources, ranging from the ERP’s structured data to unstructured and semi-structured information from the environment (

Vasarhelyi et al. 2015). More focused on the MA interaction with innovative data sources are

Warren et al. (

2015), who consider that the use of BD conducts managerial accounting practices, improves and advances effective management control systems and budgeting practices, and, subsequently, provides useful information for decision-making as the dynamic, real-time global economy evolves (

Warren et al. 2015).

Schneider et al. (

2015) also emphasize how BA fundamentally changed MAs’ tasks, predominantly those that provide inference, prediction and assurance to decision-makers (

Schneider et al. 2015).

Krahel and Titera (

2015) argue in the essay that a transformation in accounting and audit standards focusing on data, the innovative processes that generate them and their analysis, rather than their presentation, will add value and relevance to the accounting profession, empower end-users and increase the efficiency of the capital markets (

Krahel and Titera 2015). Concerning the practitioners,

Schmidt et al. (

2020) investigate their resistance to move beyond Excel and Adopt New Data Analytics Technology (

Schmidt et al. 2020).

Another Special Issue of the

Accounting, Auditing and Accountability Journal (

AAAJ) on Social Media and Big Data (see vol. 30, Issue 4, 2017) highlights some of the BD challenges for the accounting profession.

Arnaboldi et al. (

2017a) outline an agenda for those inspired to research the interplay between accounting and BD (

Arnaboldi et al. 2017a), highlighting the implications of Predictive Analytics for organizational decision-making; how numbers, narratives and visuals can communicate significant data performance indicators; and the role of accountants inside organizations in using BD. Concerning the accountants’ interaction with unstructured data,

Arnaboldi et al. (

2017a,

2017b) reveal the reluctance of accountants to see social media as a useful source of business development information (

Arnaboldi et al. 2017a,

2017b).

Until now, only

Journal of Management Control has issued a volume (April 2020) dedicated to DA and management accounting, and in the editorial,

Möller et al. (

2020) perceived a lack of empirical papers debating the effects of DA on the specific area of management accounting (

Möller et al. 2020).

Bhimani (

2020) begins with a summary of digital data and management accounting, specifically, why a reconsideration of research methods is needed (

Bhimani 2020). The papers’ approaches in this volume have been influential in the field because they have targeted the outcome of digitalization on main controlling processes: budgeting and reporting (

Bergmann et al. 2020), and on the overall control system (

Vitale et al. 2020).

Alternatively, the case studies approach allows a better, more profound understanding of the analyzed phenomena inside the entities.

Andreassen (

2020) uses the case of a technology-oriented finance sector company to debate the role of how digital technologies are influencing the MA’s role in the company (

Andreassen 2020). Focused on the case of an SME,

Vitale et al. (

2020) investigate whether and how BD affects the MAs’ tasks in management control and which drivers are involved in such interaction (

Vitale et al. 2020).

Heinzelmann (

2018) uses a qualitative case study to express his viewpoint about the impact of IT systems on MAs’ occupational identities (

Heinzelmann 2018).

Arnaboldi et al. (

2017b) conducted research based on two organizations to analyze how social media is reshaping departments’ relations (

Arnaboldi et al. 2017b).

Bergmann et al. (

2020) employed a quantitative methodology, which prescribes the use of surveys to investigate the factors that determine the use of BA in the budgeting process and its effect on satisfaction with the whole process (

Bergmann et al. 2020). A more comprehensive description is in another piece of research, where

Vitale et al. (

2020) empirically analyzed the BD impact on the SME’s management control (

Vitale et al. 2020).

Schneider et al. (

2015) scrutinized three clusters of features relating to DA, namely, design process, contingency and task performance (

Schneider et al. 2015).

In the light of the reported findings, it is conceivable that the unknowns are extensive when reflecting on what MAs need to discern in regard to DA. In this sense,

Arnaboldi et al. (

2017b) conducted semi-structured interviews with social media managers, department managers, analysts, financial controllers and senior executives (

Arnaboldi et al. 2017b).

Oesterreich et al. (

2019) used a text analytics methodology to determine patterns of Business Analytics competencies (

Appelbaum et al. 2017a) and information technology skills (

Oesterreich et al. 2019) for the controlling and management accounting profession.

Based on the review of the scientific articles, in the next section are summarized the main issues concerning the transformation of MA’s professional practice and knowledge because of the emerging new innovative sources of data.

4.2. Risks Concerning the Professional Interference in the Arena of BD and DA

Accountants are not the only professionals who could take on a more prominent role in dealing with data across organizations. Marketing or operations specialists in sundry organizations are starting to use BD and may undertake a more leading role than finance. Naturally, data science and IT functions also have a decisive part to play concerning data (

Heinzelmann 2018). All of the professions mentioned above are entering the expansive category of emerging information professions (

Vasarhelyi et al. 2015;

Furness 2019;

Moll and Yigitbasioglu 2019;

Wongsim et al. 2019) and might have or inquire about a role in the area of innovative data sources. Besides, any reluctance or failure of the profession to pursue new advances in data leaves open the likelihood of MAs being marginalized in regard to decision-making, with data scientists, for instance, playing a more significant role (

ICAEW 2019;

Moll and Yigitbasioglu 2019;

Möller et al. 2020).

In the information field, there is a tension between professions (

Abbott 1988); the profession’s jurisdictions are continually evolving and increasingly becoming weakly delineated (

Furness 2019) in handling and analyzing data. BD and DA increase the competition between the professions connected with data and information and act to weaken an existing profession’s jurisdiction or create an entirely new niche, as with the proliferation of computers and technologies (

Furness 2019). Because of the competition, maybe one profession will take over another profession’s attributes or several negotiated symbiosis forms (

Abbott 1988). Additionally, concerning MA, digitalization sparks tensions on the role and main challenges of MA in the digital era: the tensions on the centrality, authority and power of the MA function (i.e., the influence on decision-making processes) (

Andreassen 2020;

Cavelius et al. 2020;

Möller et al. 2020).

Within the system, professions are frequently in flux, wherein the boundaries between occupations are continually negotiated and contested. The professions are always vulnerable to changes in the objective character of their central tasks, and technology has the ability to divide tasks and regroup them (

Furness 2019). Many professions claim the “new territory” of BD and DA and react differently, including amalgamation or horizontal or vertical division (

Abbott 1988).

Some authors consider that BD and DA will have positive implications for extending access to different data types for the accounting profession and extending MAs’ expertise (

Warren et al. 2015). Others, on the contrary, suggest that they seem to be backstage, while other actors, namely, digital officers or marketing and communication managers, have crossed over to performance measurement (

Arnaboldi et al. 2017b).

Others consider that BD and DA are blurring professional boundaries (

Cockcroft and Russell 2018), which might create some tensions and pressures between them. For this reason, our study finds and describes competition over jurisdiction between MAs and other groups of employees, i.e., engineers’ expert knowledge, sales and customer relations department (

Andreassen 2020), IT personnel (

Heinzelmann 2018) and marketing department (

Arnaboldi et al. 2017b).

MAs might take on data management/governance (

Bhimani and Willcocks 2014). Information systems or IT departments have traditionally managed this role. A critical feature of handling BD is the design of periodic and ad-hoc dashboards, reports and scorecards, to assess performance (

Cockcroft and Russell 2018). Besides, the MA is well-positioned to exploit BD for fraud and risk management, data visualization, auditing and performance measurement (

Cockcroft and Russell 2018). MAs already excel at the problem-driven analysis of structured data. Moreover, they are well-placed to play a key role in the problem-driven analysis of unstructured data (

Bhimani and Willcocks 2014). They can back-up data scientists performing exploratory analysis on BD because MAs are acquainted with structured data-sets, enabling the transition to working with unstructured data. They possess knowledge of business essentials.

The challenge is immense and requires new knowledge in technical and programming areas of expertise. As leaders in the financial planning and analysis field, BD is part of a digital technology wave that can threaten many highly-skilled roles (

Cockcroft and Russell 2018). Some MAs might see a way to enrich their skills, but for sure, others will prefer to stay in the “Business Partner” role and contribute to value creation only in the traditional manner (

Rikhardsson and Yigitbasioglu 2018). While some consider that MAs only have to understand the unlocked potential of BD and DA and do not have to get specific technical expertise (

Bhimani and Willcocks 2014), others have a different view and foresee a paradigm shift for BD, where MAs will need to develop and acquire skills to be able to further support the decision-making process (

Rikhardsson and Yigitbasioglu 2018).

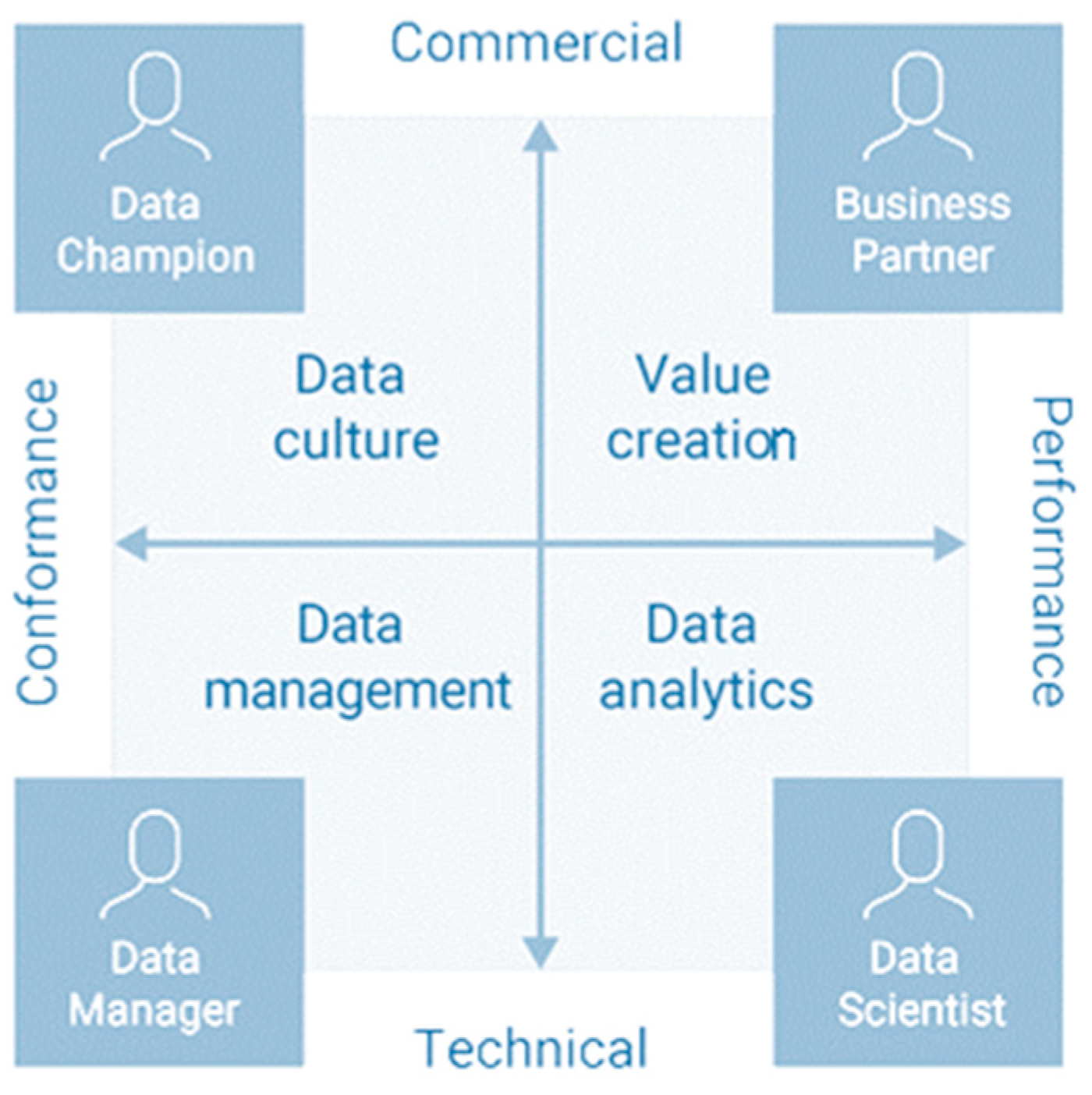

Acknowledging the four roles presented in

Figure 1 creates some concerns about the potential “de-professionalization” or a vertical division effect (

Abbott 1988) of greatly technically oriented work environments that have already been enunciated in the professionalization specialty literature (

Quattrone 2016;

Richins et al. 2018).

Abbott (

1988), for instance, highlighted how the dependence of mathematical techniques possibly weakens professional systems of knowledge and shrinks the image that professionals construct for themselves for the reason that it is grounded predominantly on their expert knowledge around which professionals build their jurisdictional authority legitimacy and public image (

Abbott 1988). The function of management accounting might become integrated into a broader analytical function in the organization, together with Customer Analytics, Process Analytics and Environmental Analytics (

Rikhardsson and Yigitbasioglu 2018).

Following the

Abbott (

1988) vertical division idea (

Abbott 1988), but from a profession inside the internal stratification perspective,

Andreassen (

2020) considers that BD and DA can transition to narrower and more specialized roles (

Andreassen 2020). Considering a large group of companies, the researchers describe a swing for divisional MAs towards narrower roles in their tasks and expectations. In contrast, at the group level, a business-oriented role entails expanding task expectations. Consequently, BD and DA conduct a vertical division of the MA profession, as

Abbott (

1988) considers, in the case of corporations (

Abbott 1988). As a result, MAs are split into two divergent categories facing different expectations: divisional and group level MAs (

Abbott 1988).

As part of a challenged profession, MAs can respond not only by fighting to gain a new area or change its level of abstraction but also by changing internally. Other possible effects of BD and DA over the profession might be amalgamating financial accounting with managerial accounting roles in organizations. By understanding the background of BD, more and more modern organizations have progressively understood the prominence of BD. In the process of financial management, financial accounting has slowly but surely shifted to management accounting (

Meng 2018). This transformation reflects an unavoidable trend when financial accounting performs its duties and obligations, but it still needs IT’s help. Simultaneously, against this backdrop, a systematic management model can be created and put into practice. Financial and accounting workforces might combine unswervingly and effectively strategic and systematic enterprise management thinking, understanding and recognizing enterprise value (

Meng 2018).

Whether BD and DA become a part of the MAs’ jurisdiction is hard to predict because it involves a delicate yet tantalizing balance amongst related jobs. The roles of “Data Scientist”, “Data Manager” and “Data Champion” are highly specialized (

ACCA 2016). Respectively, they represent technical areas that imply statistical, Data Analytics, programming and communication (

ACCA 2016;

Cockcroft and Russell 2018) that may not be necessary for the management accounting zone.

Nonetheless, what is sure is the support of accountancy professional organizations to prepare MAs for these new areas, providing abstract knowledge and credential-certifying expertise in the BDA area (

Arnaboldi et al. 2017b;

ICAEW 2019).

Professional associations such as CIMA (the Chartered Institute of Management Accountants) (

CIMA 2016) and professional accounting associations and bodies across Europe and America are continually asking for a role in the BD domain (

IMA 2013,

2019;

CGMA 2014;

ICAEW 2019). Thus, new domains emerge, as BDA creates opportunities for professionals to undergo professional growth by understanding these developments (

Abbott 1988).

Moreover, to ensure that their domain-specific knowledge or expertise stays current in light of environmental changes, the national professional accountancy professional organizations implemented BDA training in their continuing education (i.e., CPE courses) (

ICAEW 2019). Changing socio-environmental factors require professionals to permanent “reeducate” themselves in response to even incremental developments (

Abbott 1988). Accordingly, this continuous education requires professionals’ ongoing effort to ensure that their domain-specific knowledge remains up-to-date.

Another essential factor that will influence this is the market and companies’ requirements for MAs. Employers expect MAs to champion evidence-based decision-making, converting analytical insights into commercial insights and making sure these are used for improving business prospects and performance (

Oesterreich et al. 2019). This status means that MAs’ most significant opportunity is to use their combination of accounting and analysis skills with business understanding as business partners (

CIMA 2016;

Oesterreich et al. 2019;

ACCA 2020c).

DA and BD will inevitably change MAs’ roles, allowing them to direct their attention toward prospects of providing added value to a company and its clients (

Richins et al. 2018). However, at the same time, with the emergence of BD, MAs will face the problem of information storage space; information security; and other issues concerning data veracity (

Bhimani and Willcocks 2014), loss of data sovereignty, and loss and theft of data (

Wang and Song 2016).

For all of these reasons, we consider inter-professional collaboration and collaborative learning as the key solution in this stage of the BD and DA knowledge and advance. The term “collaboration” expresses the idea of sharing and suggests a synergic and collective action-oriented toward a common goal in a spirit of harmony and trust. New teams of professionals need to mediate their collaboration at their professions’ boundaries, recognizing as the boundaries space and boundary zones. The interaction between professionals with different backgrounds implies the same joint goals in working together. The growing use of interdisciplinary groups extends expectations to business-oriented roles, connecting technology progress to business practices and analyzing information. As difficulties and hitches arise, MAs can employ their business knowledge to integrate structured and unstructured data into analyses. In a collaborative team, MAs can cooperate with data scientists by endorsing content to explore, and then by interpreting the outcomes in light of strategic goals (

Richins et al. 2018). In that connection,

Arnaboldi et al. (

2017b) highlight a change in the relationships and interactions between professions and organizational concerns regarding governance and control (

Arnaboldi et al. 2017b).

Briefly, the BD and DA are now in the diagnosis stage in terms of the MAs’ professional domain. If the BD and DA are “treated” using the available toolkit of the MAs’ profession, and MAs will be proactive to gain expertise and abstract knowledge in this area, then this topic will become under the MAs’ professional jurisdiction (

Arnaboldi et al. 2017b). Alternatively, perchance we will witness a hybridization of professions (

Arnaboldi et al. 2017a;

IMA 2019;

ACCA 2020a,

2020e), and the professional identity will disappear in the future digitalized era (

Heinzelmann 2018), enabling the emergence of new professions or career patterns (

Arnaboldi et al. 2017b;

Oesterreich et al. 2019) as a result of the interrelation, interaction or reaction of professions.

4.3. MAs New Privileged Position Concerning BD and DA—Opportunities

The accounting profession is embracing new information sources and digital technologies (

Moll and Yigitbasioglu 2019;

Schmidt et al. 2020) in its attempt to be promoted from a technician role to a “Business Partner” role (

Cockcroft and Russell 2018). BD and DA offer to MAs the prospect of shifting to a strategic, proactive future-oriented role in business (

Warren et al. 2015;

Nielsen 2018;

ACCA 2020a,

2020e) with both benefits and risks. The shifting from heavily investing in data-collection and reliability missions leaves less time for advising managers and challenges operational business units to master BD and digital analysis tools (

Cavelius et al. 2020). In this way, MAs might play an active role in their companies’ digital transformation by adding value to the emerging mass of data (by making sense of that data, reflecting on business opportunities and challenging operational units and top-management with their expert knowledge). MA tasks are grounded in data; thus, data provide accountants with an opportunity to revolutionize their role into a much broader guardianship of data across their respective organizations (

Bhimani 2020).

The configuration, discipline and ethical approach of the MA profession translates into the fact that the function is well placed to aid organizations to effectively use BD and advanced analytics. Furthermore, accountants’ inherent prudence and skepticism can ensure BD’s full and appropriate use (

ICAEW 2019). Exploring this perspective,

Rikhardsson and Yigitbasioglu (

2018) propose a framework for studying the relationship between management accounting and Business Intelligence and DA technologies (

Rikhardsson and Yigitbasioglu 2018). Since this is new territory,

Bhimani and Willcocks (

2014) caution concerning the real advantages and risks of reorienting accounting and finance functions to harness BD’s potential (

Bhimani and Willcocks 2014), revealing several gaps and shortcomings since there should be a clear delineation of information systems that provide these established accounting and finance capabilities (

Cockcroft and Russell 2018).

MA is concerned with cost management, planning, management, operational control, performance measurement, and decision-making (

Brands and Holtzblatt 2015). With innovative data sources and DA, the scope of MA is enlarged, based more actively on real-time data that add a predictive capacity (

Cokins 2013), useful for strategy formulation, implementation and monitoring (

Richins et al. 2018). The emergence of BD and DA in MA might trigger changes causing issues in cost structures (

Acito and Khatri 2014), and information excess, and cause the making of incorrect decisions at a faster pace (

Quattrone 2016). Additionally, costing architectures have altered due to the evolution of the links between information, data and knowledge (

Bhimani and Willcocks 2014;

Schneider et al. 2015;

Warren et al. 2015;

Arnaboldi et al. 2017b;

Richins et al. 2018;

Rikhardsson and Yigitbasioglu 2018).

In the management control field of study, BD’s use can induce significant managerial changes (

Bredmar 2017;

Rikhardsson and Yigitbasioglu 2018;

Möller et al. 2020). The literature debates concerning the opportunities and real benefits is in an emerging phase (

Vitale et al. 2020), with several questions remaining to be addressed. By tradition, the processes of decision-making are being supported by the management control systems that use historical and cumulative data (

Gärtner and Hiebl 2018), with a limited future-oriented view. Nevertheless, to reach efficiency, economy and effectiveness, management control needs real-time data (

Rikhardsson and Yigitbasioglu 2018). BD has this role, and therefore can greatly impact the management control systems.

Moreover,

Warren et al. (

2015) posit that BD will assist the development and evolution of effective management control systems and budgeting practices (

Warren et al. 2015). Since budgeting involves a routine procedure, it could integrate digitization’s effects comparatively quickly into companies’ budgeting processes. Budgeting will imply more than the traditional spreadsheet where the sales numbers received from other departments are transposed (

Warren et al. 2015).

Instead, MA might work diligently with the top managers for adding unquestionably more relevance to previsions considering the innovative mix of both external and internal sources of existing data and records (

Cokins 2013;

Bredmar 2017). MAs should use the synergy of their powerful management accounting abilities and make good use of their management accounting tools to translate the existing records and data into predictive insights (

Bergmann et al. 2020). In this way, MA can definitively contribute to an organization’s strategic direction (

Warren et al. 2015). Hereafter, together with an AI perspective, DA will make performance management more dynamic and customized.

Furthermore, analytic and data visualization software allow MAs to provide strategic decision support. Many other value-adding opportunities could arise for MAs in this area. Against this backdrop,

Bergmann et al. (

2020) highlight Business Analytics’ role in enhancing the relationship between planning, function and budgeting (

Appelbaum et al. 2017;

Bergmann et al. 2020). Thus, DA and DA’s use allows an increased budget function for organizations interested in planning, forecasting, coordination and resource allocation (

Bergmann et al. 2020).

For financial reporting purposes, the most suitable category of DA is Descriptive Analytics, since it summarizes and describes a business’s financial situation. However, in the field of performance measurement (

Schläfke et al. 2013;

Nielsen 2018) and controlling (

Oesterreich et al. 2019), MAs can use Predictive Analytics, which can implement inputs from Descriptive Analytics with Machine Learning algorithms, to deliver a forecast of future organizational performance. By using outcomes from performance measurement and cost accounting, Prescriptive Analytics are assimilated into planning and decision-making to offer evidence regarding the optimized solution.

BD comprises both external and internal data. External data is data gathered outside the company (i.e., news, social media or the Internet of Things). Habitually, external data are unstructured data that can only provide information after being processed by analytics tools (

Appelbaum et al. 2017). Conversely, internal data embodies data collected from sources inside the entity (i.e., the company’s database), which is usually structured and familiar to MAs.

The era before digitization restricted accounting’s access to organizational data, especially to financial data, and limited MAs in their use of existing management accounting techniques and tools.

One of the first to highlight the challenge of non-traditional sources of data’s incorporation into accounting was

Vasarhelyi et al. (

2015). From this standpoint, MA’s tasks may include collecting and handling new unstructured sources of information (

Vasarhelyi et al. 2015), managing the interaction between traditional, structured data and the new data while also integrating the latter (

Richins et al. 2018). In this sense, MAs need to acknowledge the content of large unstructured data-sets collected from untraditional sources (i.e., emails, audio and video files, internet click streams, social media, news media, etc.). Secondly, they have to take into consideration all its characteristics: immense volume, high velocity, wide variety and uncertain veracity. Not least, MAs need to comprehend that all the data need to be of high-quality—respectively, complete, valid, accurate, precise, consistent, relevant and timely (

Appelbaum et al. 2017).

Therefore, MAs’ biggest BA challenge is to pass from exclusive structured data to a mix composed of structured, unstructured and semi-structured data. While structured data refers to data stereotypically spawned through the company’s transaction processing systems, unstructured data originate from a wide variety of sources and may be in numerous forms (i.e., text, audio and video) (

Vasarhelyi et al. 2015). Structured data are organized so that they can effortlessly be encompassed in a traditional relational database. Contrariwise, unstructured data, which embody the most considerable share of actual data, refers to data that lack structured data’s organizational rigor (

Bhimani and Willcocks 2014;

Vasarhelyi et al. 2015;

Richins et al. 2018).

In this context, extrapolating ample information unused in the past because it was not connected to an economic transaction can provide further insight into customers’ preferences and how purchase decisions are made.

Hence, MAs should provide a joint framework for handling this information to extract meaning and create structured data about the data. Software that makes machine-processable structures exploits the linguistic, auditory and visual systems inherent in all forms of human communication. Algorithms can infer this inherent structure from the text, for example, by scrutinizing sentence syntax, word morphology and other patterns, either on small scale or on large scale (

Richins et al. 2018). In this spirit, some researchers have suggested that unstructured information can then be deepened and tagged to address ambiguities and relevancy-based methods used to enable search and discovery (

Bhimani and Willcocks 2014;

Vasarhelyi et al. 2015;

Richins et al. 2018).

Henceforth, MAs might have to rethink the way the information is gathered and processed; particularly, how they can capture and use real-time data and entire data-sets (

Bhimani and Willcocks 2014;

Korhonen et al. 2020). Conversely, the danger arises that MAs get locked into technical tasks such as data collecting and processing instead of becoming more involved in managerial decision-making processes (

Schläfke et al. 2013;

Zhou and Xia 2018). Nevertheless, we observe that MAs, once they have mastered BD and new tools, can become actively involved in their companies’ digital transformation. As such, several researchers have recognized that they can add value to the emerging mass of data by making sense of that data, reflecting on business opportunities and challenging operational units and managers with their expert knowledge (

Griffin and Wright 2015;

Moll and Yigitbasioglu 2019;

Andreassen 2020;

Cavelius et al. 2020;

Korhonen et al. 2020).

In this framework,

Brands and Holtzblatt (

2015) debate and analyze how MAs can place themselves to play a critical role in implementing and applying Business Analytics within their organizations (

Brands and Holtzblatt 2015) as they move beyond traditional, transaction-based accounting to analytics. This trend will transform the way MAs’ analyze and interpret data for their organizations in the future, not only concerning financial accounting (e.g., accounts receivable and payment monitoring) and especially regarding the visualization of data.

In conclusion, due to the MA function’s unique position, MAs are the best placed within an organization to manage BD/DA organizations (

Bhimani and Willcocks 2014) because there is already existing general professional trust in accountants.

4.4. Challenges to Adapt the MA’s Skills to the New Tasks and Responsibilities Regarding BD and DA

To investigate the relationship between a profession and its work is no simple task. To be sure, professions’ tasks have foreordained objective qualities that resist professions’ efforts to redefine them. However, numerous elementary qualities of tasks turn out to be subjective qualities assigned by the profession with current jurisdiction. These objective and subjective properties have a dynamic and synergic liaison in which neither one prevails.

According to

Abbott (

1988), by using knowledge, a profession solves novel problems and adapts its practices to new niches by expanding its cognitive domain (

Abbott 1988). Thus, by using its knowledge, the profession extends its capabilities in new areas and defines them as its proper work. Nowadays, in conjunction with the extensive use of emerging technologies, the MA’s role in the company in general, and the MA’s tasks in particular, have become more significant and, as a result, the MA profession may take the opportunity to extend its capabilities in the BD and DA areas. MAs must link theory and already existing concepts and knowledge to real-world application, in the context of digitalization (

Richins et al. 2018;

Schmidt et al. 2020). Being equipped with new tools and innovative processes enables MAs to build value in companies (

Dilla et al. 2010;

IBM 2013;

Griffin and Wright 2015;

Krahel and Titera 2015;

Drew 2018;

Knudsen 2020). Instead of being limited to routine spreadsheet analysis tools, it will transform management accounting analysis into more strategic decision support.

The following challenges related to BD and DA that influence the enhanced MA job description in a digital environment are related to new skills concerning the management and governance of traditional and innovative sources of information, and techniques to analyze the mix of data, business analytics process, and function structure (

Appelbaum et al. 2017).

BD will have gradually important accounting implications, even as new types of data become accessible (

Warren et al. 2015). As a part of the massive surge of digital technology, BD has the potential to endanger some highly skilled roles but, at the same time, open new career challenges in the analytics field (

IMA 2013;

Bhimani and Willcocks 2014). This is due to the elimination of distance between analysis and execution in organizations adopting BD technologies (

Appelbaum et al. 2017).

A profession’s ability to withstand its jurisdictions lies largely in the influence, authority and prestige of its academic, abstract knowledge (

Abbott 1988). In academia, there is general agreement concerning the call to the accountancy profession regarding gaining a new set of skills in technologies and digitalization that will enhance the accountant’s role in the business (

Griffin and Wright 2015;

Vasarhelyi et al. 2015;

Lin 2016;

Drew 2018). MAs’ know-how in collecting, integrating and inferring data from manifold sources is expected to make them even more valuable with BD and DA’s emergence (

Richins et al. 2018).

Business Analytics (BA) and Information Technology (IT) skills have gained prominence as two major skill areas of the MA’s job profile, becoming mandatory capabilities for this profession (

Bhimani and Willcocks 2014;

Appelbaum et al. 2017). However, the practitioners’ community seems not to be prepared since many were slow to leave behind the traditional manner of performing their tasks, showing some unwillingness to move from looking backward to looking forward (

ACCA 2020b,

2020d). The current competence profiles (e.g., controller/management accountant) do not comply with the recent requirements regarding Business Analytics competencies (

IMA 2019). At least in the German-speaking area, according to

Oesterreich et al. (

2019), competencies in Business Analytics and IT professionals do not supply skills because they are not included in their web profiles on a business social network (

Oesterreich et al. 2019).

Business strategy and understanding of business models and the accountant’s role in business and Information Systems regard the development of a new generation of information technology that changes the traditional business model and resource integration model while also expanding the scope of service of management accounting to a certain extent, so that the MAs’ work is extended from the enterprise internal management to the whole value chain management, from the tactical level to strategic layer and from profit maximization to the sustainable value realization of the enterprise; it involves effective use of IT, design systems structure and data warehouses, and the evaluation, recommendation and implementation of the apposite ERP system (

Bhimani and Willcocks 2014;

Wang and Song 2016;

Heinzelmann 2018).

Schneider et al. (

2015) consider that MAs can leverage existing technologies to scrutinize information (

Schneider et al. 2015). They succeed in combining collecting and storing operational data in enterprise information systems and/or data warehouses with analytical tools to put forward multifarious information to decision-makers.

Data Governance encompasses the ability of managing, generating and storing large amounts of structured, semi-structured and unstructured data (

Bhimani and Willcocks 2014;

Appelbaum et al. 2017) by using adequate tools (i.e., SQL, Hadoop, MongoDB, R, and SAS) and the capability of designing and implementing systems to warrant the availability, utility, integrity and security of data (

Gärtner and Hiebl 2018;

Oesterreich et al. 2019). In the context of rapid digitalization, the spread of BD is shifting MAs’ tasks, respectively, changing their techniques and analyses used to mix sources of information (

Knudsen 2020).

Data Analytics skills lie in the ability of making use (by processing, verifying and analyzing) of quantitative and qualitative techniques (

Bhimani and Willcocks 2014;

ACCA 2016;

Appelbaum et al. 2017), such as multiple queries, scripted or interpreted languages (i.e., SQL, Python, R), and advanced statistical tools for exploratory data analysis (i.e., cluster analysis, time-series analysis and Monte Carlo analysis) for the development of predictive models, through data mining, in order to identify patterns, relationships and text and voice analytics (

Bhimani and Willcocks 2014;

Oesterreich et al. 2019). Exploiting BD entails a blend of skills and abilities spread across three wide-ranging areas: statistical skills, to construct the algorithms and apprehend the robustness of models; data and technology skills, to excerpt and deploy data; and domain knowledge, to make the right inquiries and gain insights from analysis (

Brands and Holtzblatt 2015;

Richins et al. 2018). In this framework, DA provides MAs with the tools to scrutinize data from three different perspectives: inference, prediction and assurance. While inferring is enhanced by improving the revelation of operational efficiencies and augmenting decision support by compliance, regulatory reporting, narrative reporting and activity-based costing, predictive power is boosted by improving the process of spotting new products, as well as segment trends (

Schneider et al. 2015;

Appelbaum et al. 2017;

Oesterreich et al. 2019). Respectively, assurance is enriched through a more remarkable capability of identifying performance gaps (

Schneider et al. 2015). Currently, Excel and Access are most commonly utilized to execute a wide variety of DA activities, from simple descriptive reporting to more advanced data modeling, trend analysis and forecasting (

Luen et al. 2015;

Appelbaum et al. 2017;

Richins et al. 2018;

Rikhardsson and Yigitbasioglu 2018;

Schmidt et al. 2020).

Finally, data visualization embodies the ability of envisioning data adequately and effectively interpreting and communicating the results of multifarious analyses for decision-making. Reporting and communication have always been important focuses for MAs and are seen as business language (

Bhimani and Willcocks 2014;

Gärtner and Hiebl 2018;

Bhimani 2020). Other Business Intelligence tools and further sophisticated techniques are used in the third and fourth stages—Visual Analytics and Predictive Analytics (i.e., IMB’s Cognos Analytics, SAP’s Business Objects or Visualization Tableau), as outlined by several researchers (

Luen et al. 2015;

Appelbaum et al. 2017;

Rikhardsson and Yigitbasioglu 2018).

Consequently, MA’s tasks refer to different types of analysis presented below in a bottom-up approach in terms of difficulty and value added by each of them, from descriptive level (the lowest) to the prescriptive level (the highest), including all MA functions: cost control, budgeting, performance management, planning and forecasting (

Acito and Khatri 2014;

Krahel and Titera 2015;

Warren et al. 2015;

Arnaboldi et al. 2017b;

Bergmann et al. 2020). As possible applications,

Brands and Holtzblatt (

2015) have suggested that DA can be used internally in different analyses (i.e., sales, accounts receivable and credit, accounts payable and payment monitoring), as well as in due diligence with mergers and acquisitions and forensic accounting (

Brands and Holtzblatt 2015). The novelty bought by the innovative sources of information is reflected in the highest type of analyses (prescriptive) performed by an MA (

Appelbaum et al. 2017;

Nielsen 2018).

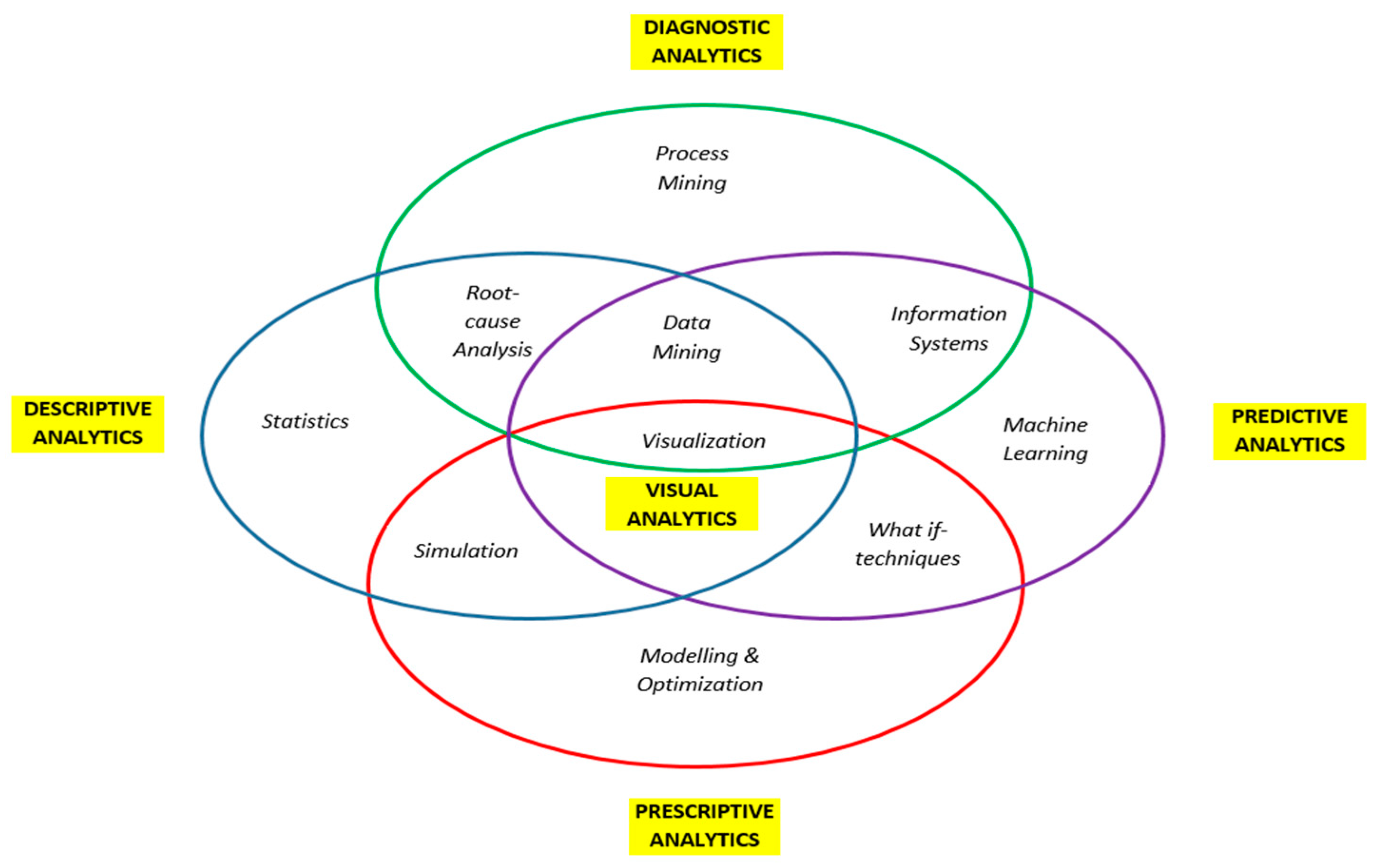

Accordingly, with BD mined from both internal and external data sources, MAs could now employ BD and DA techniques to offer hindsight—Descriptive Analytics and Diagnostic Analytics, respectively, to offer foresight into Predictive Analytics and Prescriptive Analytics (

Appelbaum et al. 2017;

Nielsen 2018). In addition, Visual Analytics offers insight by enhancing rapid decision in real-time (

Figure 2).

Descriptive Analytics presents what happened, when it happened and where it happened, with the aid of descriptive statistics, dashboards and other visual forms (

IBM 2013;

Appelbaum et al. 2017). Tools and techniques that the MA uses are: ratio analysis, text mining models, reporting, data mining and data aggregation (

Xu 2017;

Zhou and Xia 2018).

Diagnostic Analytics reveals the motives underlying the events that took place, respectively, other areas for further investigations. MAs might use the following procedures: discovery and alerts, query and drill-downs, clustering models, process mining, rank correlation measurement, what–if analysis and root cause analysis (

Spraakman et al. 2015;

Bergmann et al. 2020). Output data (i.e., ad-hoc reports) may include not standardized analysis, comprising more detailed information than the current standardized one, especially concerning specific issues. These reports still represent a snapshot of the past, with MAs having limited ability in guiding decisions. However, MAs need to develop new reports on Key Performance Indicators and adequate scorecards, and flexible steering approaches, such as the Objective and Key Results system (

Spraakman et al. 2015;

Bergmann et al. 2020).

Visual Analytics enables gaining insights into the data both from the past and present in real-time. Data visualization will change the way MAs work with data. Expectation will be for them to be able to respond to issues faster while also be able to dig for more insights by looking at data differently and with more imagination (

Cockcroft and Russell 2018;

Nielsen 2018). While visualization is at the center of Business Analytics, MAs are in the data explosion center (

Warren et al. 2015;

Bergmann et al. 2020;

Cavelius et al. 2020). They are poised to become ever more vital to stakeholders in enabling data and insight-driven organizations (

Figure 3).

MAs will need to learn how to use data visualization tools to analyze data, gain new insights from visual analytics and communicate those insights effectively by identifying irregular and potentially fraudulent accounts payable transactions (

Cockcroft and Russell 2018)—hence the need for automated and dynamic reporting to be made available, allowing one to make use of intelligent dashboards that consider data visualization methods that are engaging for the audience (

Warren et al. 2015;

Bergmann et al. 2020;

Cavelius et al. 2020).

Predictive Analytics aims to uncover certain patterns and certain relationships between data, therefore helping to answer the question of what might happen (

Appelbaum et al. 2017;

Cockcroft and Russell 2018;

Nielsen 2018), specifically, when and why. As depicted by

Vasarhelyi et al. (

2015),

Zhou and Xia (

2018) and

Wongsim et al. (

2019), methods used by MAs typically cover predictive modeling techniques, statistical modeling techniques (i.e., regression, factor analysis and clustering), causal forecasting techniques and ML techniques (i.e., neural networks) (

Vasarhelyi et al. 2015;

Zhou and Xia 2018;

Wongsim et al. 2019;

Bertsimas and Kallus 2020). Predictive Analytics compared with others is a proactive focus on forecasting (

Dinan 2015), while the latter two mainly focus on the analysis and reporting of historical data (

Bergmann et al. 2020). To conclude, Predictive Analytics makes use of inductive logic rather than deductive logic (

Spraakman et al. 2015), enabling MAs to determine trends in relationships between variables, ascertain the strength of their correlation and hypothesize causality. MAs usually use Predictive Analytics techniques to make an educated guess at likely results (a guess at the future), thus permitting them to help inform low-complexity decisions regarding predicting the future progression of events and taking necessary actions (

Cockcroft and Russell 2018). An example of forecasting and trend analysis lies in budget projection or planning, respectively, in identifying patterns (that have changed) in trends by expenditure (

Spraakman et al. 2015).

Prescriptive Analytics refers to ways of benefiting from predictions that have already been made, and the best course of action, specifically, the impact of a decision on everything else (

Dinan 2015;

Appelbaum et al. 2017;

Nielsen 2018;

Bertsimas and Kallus 2020). These encapsulate what MAs should do following an optimizing approach, its main objectives being optimization, simulation and actionable information, for critical, complex or time-sensitive decision-making (

Dinan 2015;

Coyne et al. 2018;

Nielsen 2018). Prescriptive Analytics is the process of collecting BD and using them. Thus, for the MAs job profile, mastering tasks related to prescriptive analysis represents a new achievement for the profession,

Cokins (

2014) mentioned “predictive accounting” as a trend area for management accounting (

Cokins 2014), together with BA embedded in ERP systems (

Vasarhelyi et al. 2015;

Heinzelmann 2018). In this instance, MA uses techniques such as stochastic techniques, heuristics procedures, optimization, random testing, simulation algorithms, streamlining, Game Theory, decision analysis and rule-based systems (

Appelbaum et al. 2017;

Nielsen 2018) to advise on possible outcomes, recommend numerous possible solutions to a problem and lead one to consider the best possible course of action (

Appelbaum et al. 2017;

Nielsen 2018).

The step from the Predictive to Prescriptive approach is significant. Whereas Predictive Analytics and, implicitly, statistical modeling of scenarios is more about measuring correlation to test a hypothesis (

Spraakman et al. 2015), ML is about predicting outcomes founded on several variables. BD, staggeringly large sets of information often reflecting crowd behavior and sourced from outside the company in question, is essential to ML (

Dilla et al. 2010). It is intricate enough to improve AI’s decisions over time (

Moll and Yigitbasioglu 2019;

Korhonen et al. 2020). AI can give probable answers to what–if questions; may be able to detect, for example, eventual frauds (

Spraakman et al. 2015); and can suggest courses of action.

Mastering Predictive Analytics, MAs have the opportunity to own, analyze and drive a larger part of an organization’s data, using procedures arraying from simple financial ratios to more forward-thinking techniques such as regression, clustering and factor analysis (

Cokins 2014;

Pickard and Cokins 2017). Thus, Prescriptive Analytics goes beyond the Predictive Analytics by endorsing one or more recommendation and solution and displaying the potential outcome (

Appelbaum et al. 2017). More significantly, Prescriptive Analytics can use all forms of new data to re-prescribe and then refine prescriptions based on a feedback loop. In this context, by using Prescriptive Analytics, MAs will automatically offer the best decision choice scenarios and improve prediction accuracy by using deliverables such as reports, algorithms, models, codes and recommended actions (

Cokins 2014;

Spraakman et al. 2015;

Appelbaum et al. 2017;

Pickard and Cokins 2017).

BA undertaken by MAs where BD is existing may conduct to a Prescriptive Analytics tactic where a set of procedures and methods computationally identifies numerous alternative actions to be taken by management, given their complex goals and limits, to reduce business risk (

Arnaboldi et al. 2017b). For instance, it could use social media to project the optimal marketing budget and diminish the risk of directing resources in the wrong market segment (

Arnaboldi et al. 2017a;

Arnaboldi et al. 2017b). Social media, as well as other novel and innovative exogenous data, could also be employed to re-run and re-estimate models based on variations in the socio-economic conditions, business environment, government policies and any other unforeseen events (

Appelbaum et al. 2017;

Oesterreich et al. 2019). Perceptibly, the Prescriptive Analytics approach is the most effective where the MA has more control over what is being modeled (

Table 3).

Briefly, to conclude, the application of analytics to business problems is in its infancy in terms of development and dissemination. Opportunities for employing data assets to reduce costs, enhance revenue and manage risks abound and will continue to grow (

Acito and Khatri 2014).

{kind=link}

{kind=link}

{kind=link}