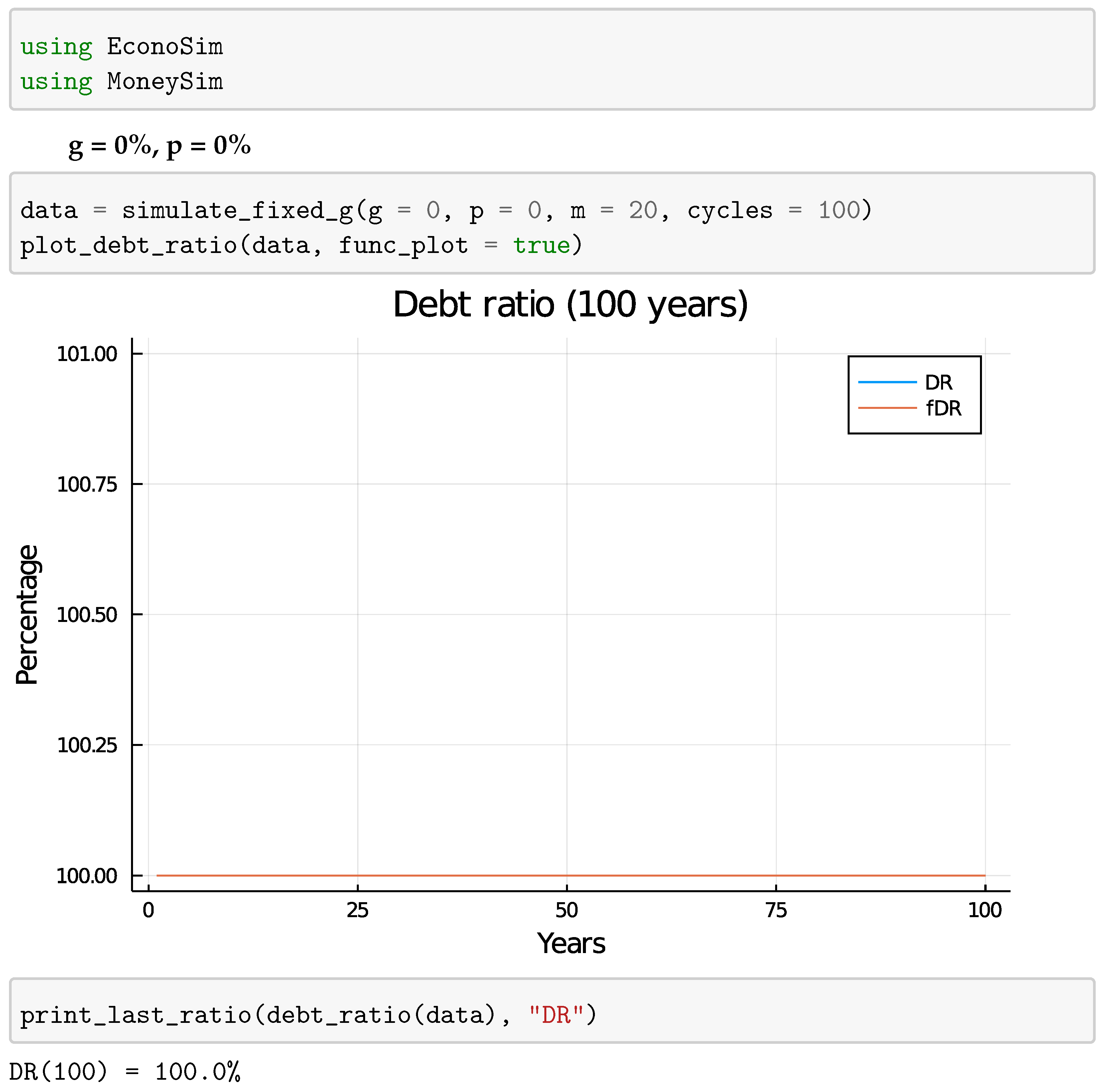

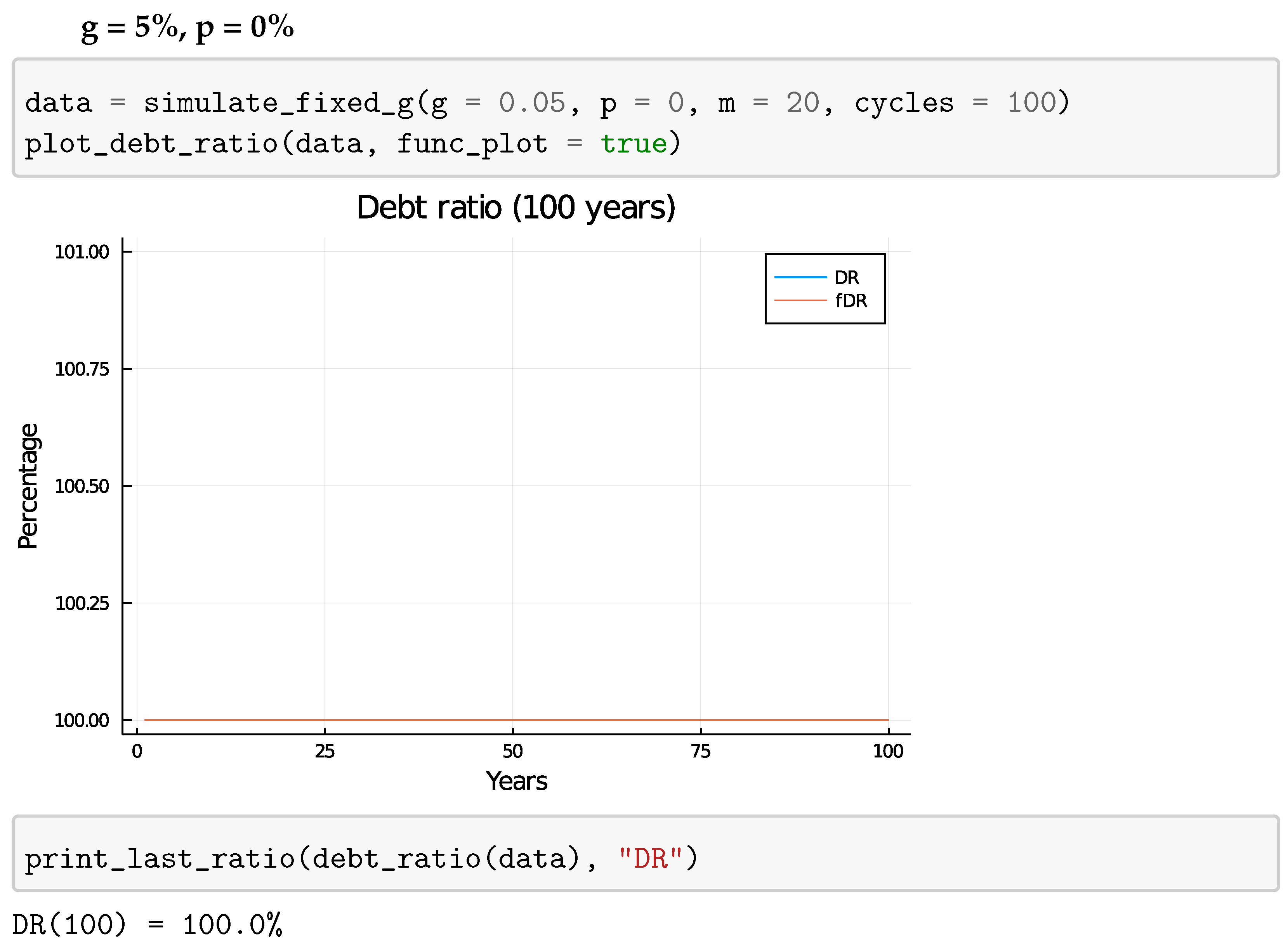

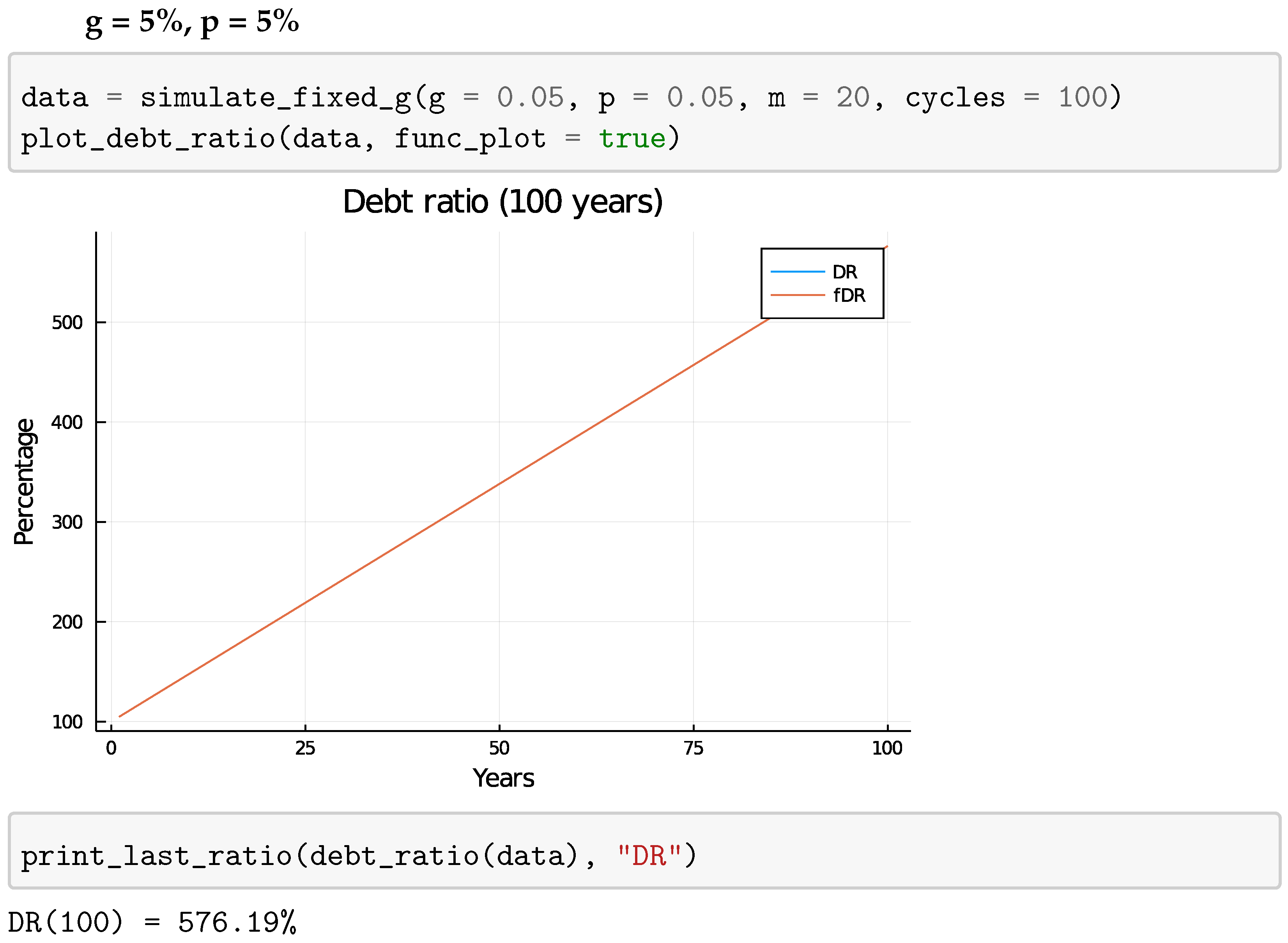

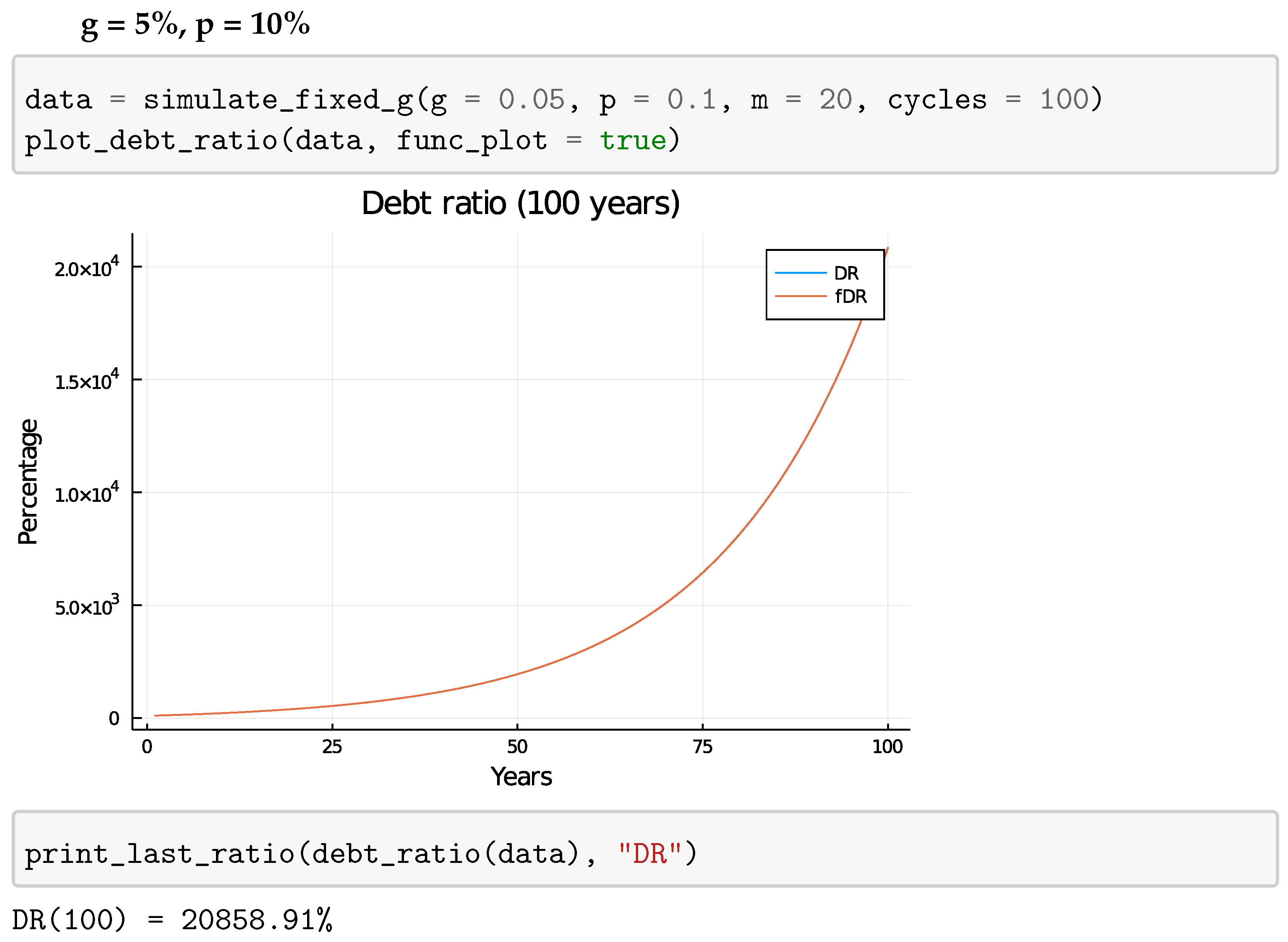

5.2. Steady-State Economy

It can clearly be stated that discussion about the possibility of a steady-state economy in conjunction with a debt-based, interest-bearing monetary system only makes sense if that monetary system is stable. The results from the simulations and the accompanying mathematical analyses therefore add a new perspective to the discussion.

Cahen-Fourot and Lavoie (

Cahen-Fourot and Lavoie 2016) stated that, in order to have a steady-state economy, banks and organisations must not accumulate wealth, i.e., a portion of accumulated wealth should be spent, resulting in zero net wealth accumulation.

This was not contradicted by the simulations. Zero net wealth accumulation for banks would result in , leading to a stable system . However, no definite conclusions can be reached about whether a steady-state economy can be reached since it is clear that the monetary system itself can be examined without taking economic parameters such as wages, production, consumption and private savings into account.

It is therefore suggested that the question about whether or not a post-Keynesian money supply model is inherently incompatible with a steady-state economy be restated as follows: Can a steady-state economy realistically support a stable post-Keynesian money supply model?

It was observed that the stability of the model is dependent on . For this to happen, a minimal needs to exist. This minimal is dependent on the behaviour of the economic actors in the private sector. While, theoretically, p and m could be part of monetary policy, cannot.

If the position is taken that in a steady-state economy, businesses should be able to cover operating and depreciation costs with their revenues, then there is a high likelihood that sufficient would be lacking, leading to a negative g. This in turn would require the banking sector to operate at a loss in order to maintain stability, an event that is unlikely to occur.

The fact that the banking sector does not always answer positively to a loan demand puts additional strain on achieving the necessary .

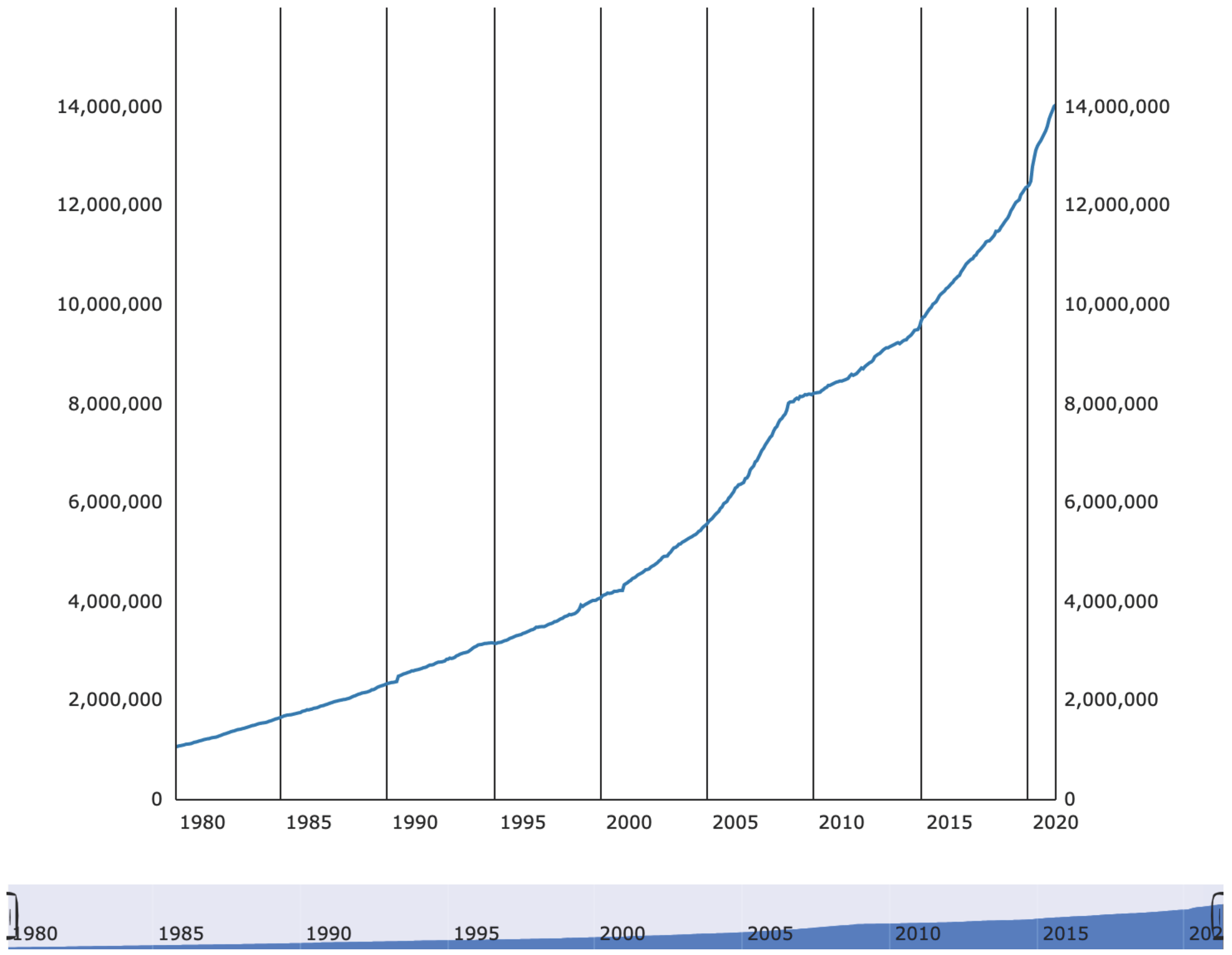

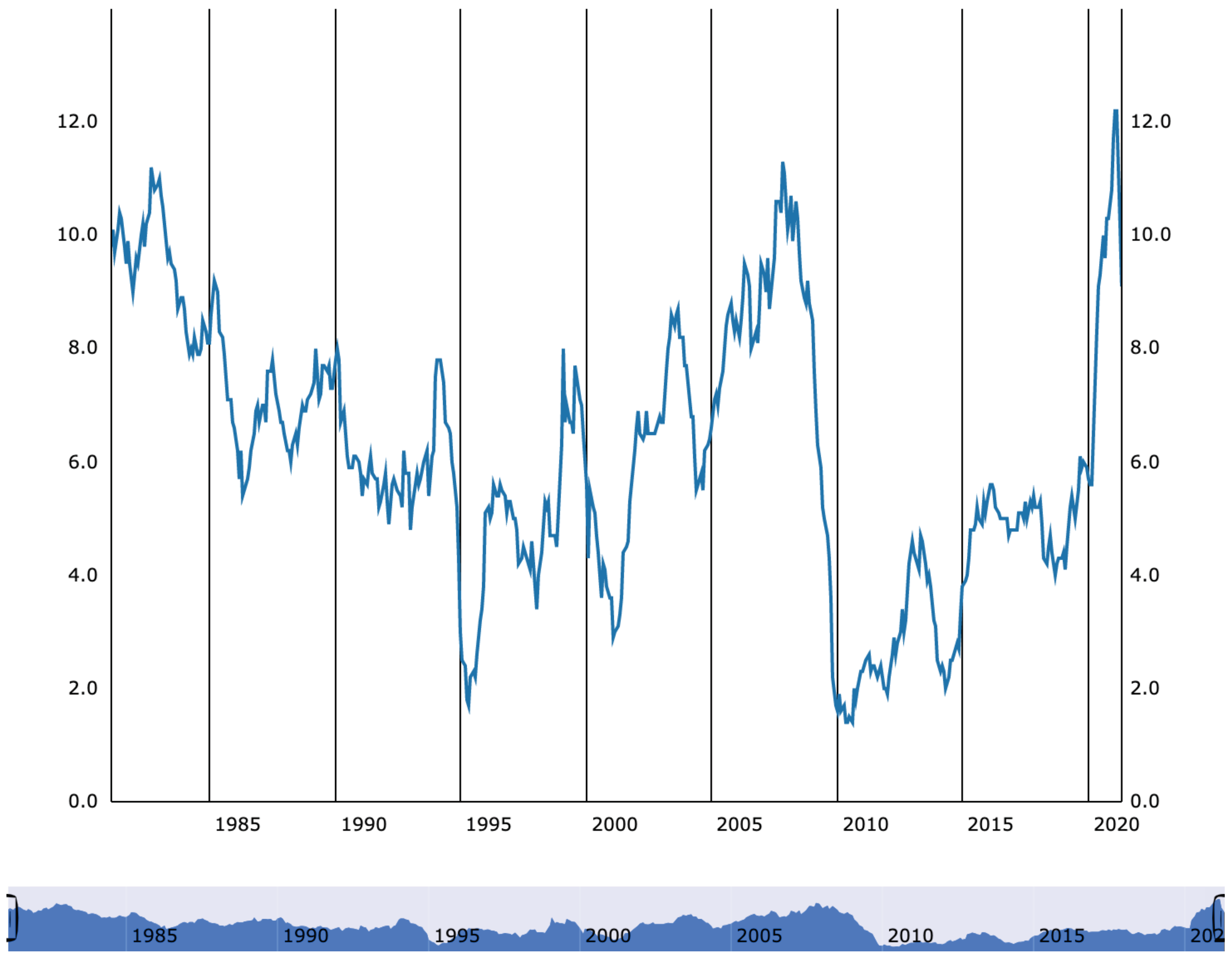

Furthermore, if the balance sheet recession of Japan (

Koo 2013) is any indication, things appear bleak. However, a declining

M could be the incentive needed to raise

, but more research would be required before stating definitive conclusions.

The behaviour of the economic actors—the private sector demanding loans and the banking sector approving loans and determining p—should be included in the model. Is the banking sector willing to subject p to g? Is the private sector willing to borrow sufficient amounts in order to satisfy the necessary ? Which are the underlying incentives that drive borrowing, and how strong are they in a steady-state economy?

The most heated discussions in the debate about whether or not an inherent growth imperative exists in debt-based, interest-bearing monetary systems seems to be rooted in the definition of “inherent growth imperative”. This definition is not the same for opposing sides of the argument. For those who claim there is no growth imperative, the real-world behaviour of the economic actors interacting with the monetary system is not taken into consideration when determining the existence of the growth imperative.

On the opposite side of the discussion, the necessary conditions for a steady-state economy—banks and organisations freely distributing their profits—are claimed to be unrealistic, and therefore, a steady state can not be reached when using a debt-based, interest-bearing monetary system.

Realistically, behaviour cannot merely be assumed to match the requirements of a mathematical model. Excluding real-world behaviour and the underlying incentives of the economic actors would make this behaviour external to the model and thereby result in money creation, driven by externalised behaviour, to lean towards exogeneity rather than endogeneity, thereby undermining the endogenous character of post-Keynesian money supply models. The articles from the literature study stating the absence of a growth imperative in a post-Keynesian money supply model all assumed that the behaviour of the economic actors falls in line with the needs of the model, but no supportive arguments for the validity of these assumptions were made.

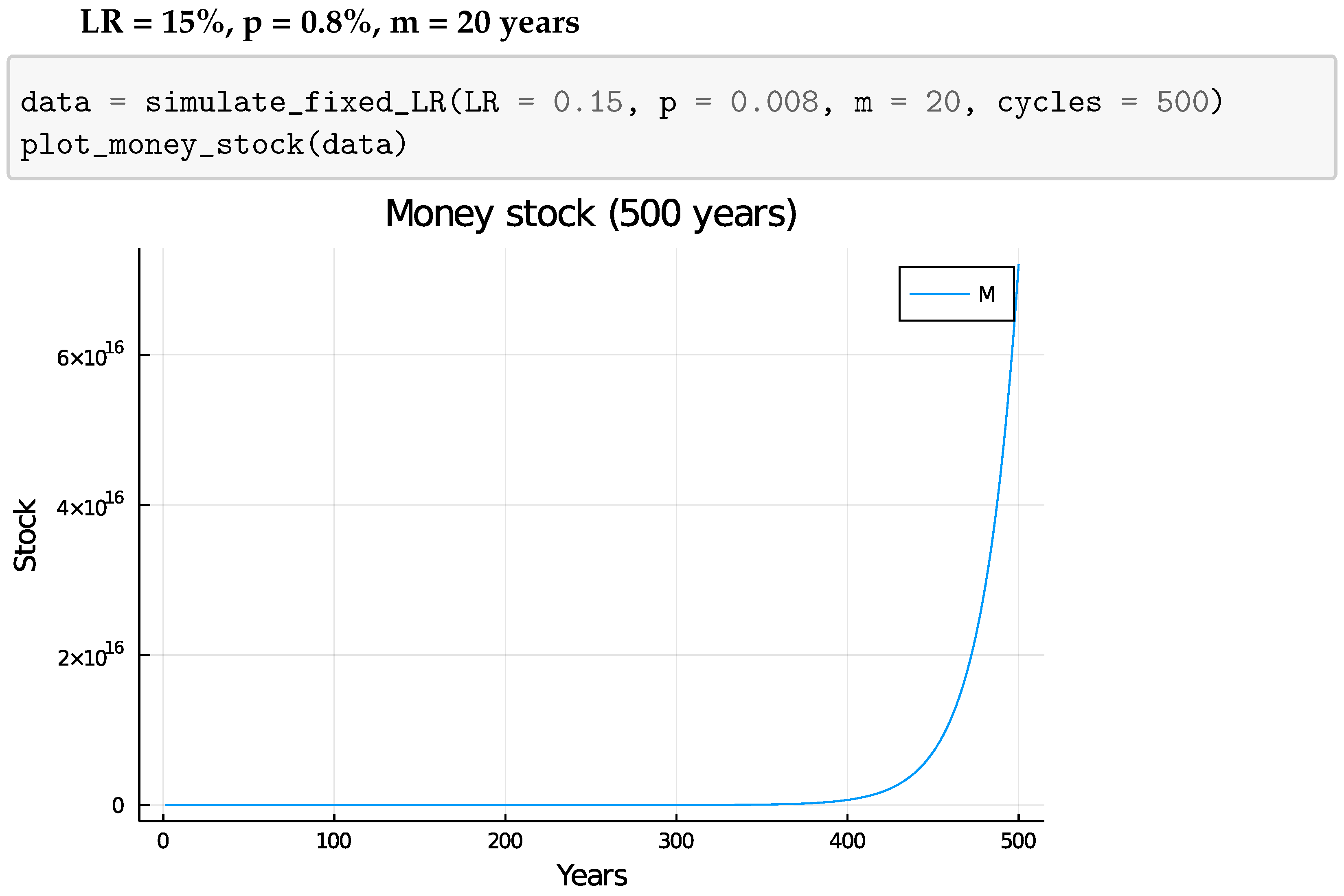

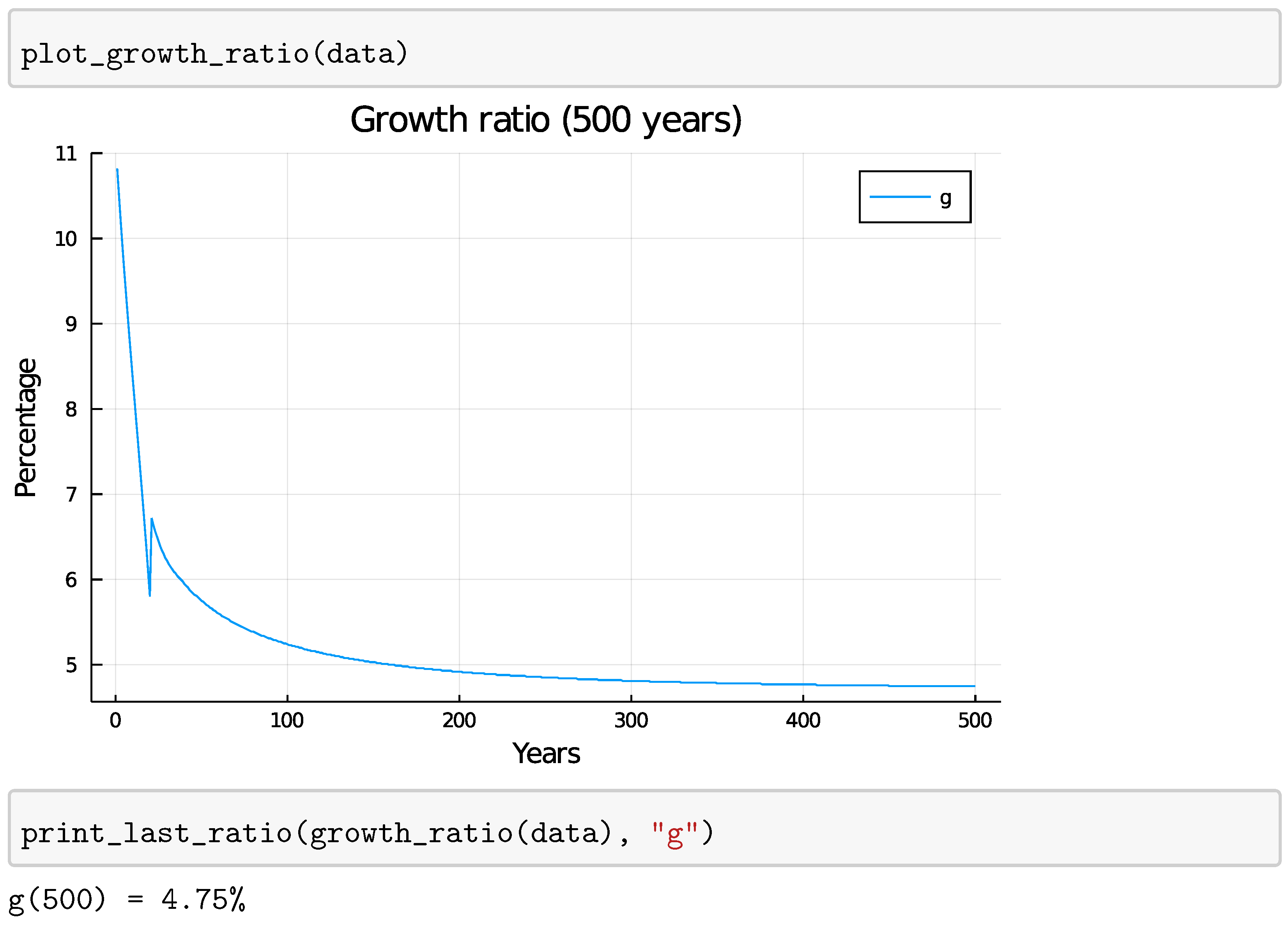

5.5. Model Limitations

The destabilised outcomes of the presented simulations do not unfold themselves in the real economy today.

This indicates that either or that other elements, missing from the model, are responsible for avoiding a collapse. What follows is a brief overview of those elements that could restore balance to the model.

5.5.1. Quantitative Easing

Quantitative easing (QE), which has been applied extensively by central banks during the COVID-19 pandemic, increases M without resulting in increased debt. This reduces the ratio and also lowers the required , thereby reducing stress on the model. However, when the debt is settled or it is cleared from the balance sheets of central banks by reselling it to the financial markets, the reverse would happen. M would decrease and increase stress on the model.

5.5.2. Government Spending

Government spending can, under certain conditions, alleviate stress from the model.

When the government can spend money into existence, as claimed by MMT advocates (

Kelton 2020),

M can be increased in order to alleviate stress from the model. Decreasing

M through taxation holds the same risks, as reselling debt bought up through QE would do, namely to increase stress on the model.

M decreases while

D remains the same, thereby raising

.

In case the government cannot spend money into existence, they either have to borrow it from the private sector by issuing bonds or borrow it from banks.

When money is borrowed by issuing bonds and that money is then spent, no effects on the model occur. Money has moved from private investors to the government and back to private actors who are paid by the government. Both private investors and actors paid by the government are part of the private sector, and M does not change.

When the government borrows from a bank and then spends that money it has the same effect as a private actor making a bank loan.

Should governments hold on to money they borrowed, it can be considered to be the same as accumulated wealth, i.e., “dead” money.

5.5.3. Banks Selling Debt at a Loss

If banks were to sell their debt to the financial market at a loss, this would effectively create “debtless money” from credit money. Consider the following balance sheets to be the initial state:

Bank balance sheet:| Assets | Liabilities |

| Private debt = 100,000 | Deposits = 80,000 |

| | Equity = 20,000 |

Private sector balance sheet:| Assets | Liabilities |

| Deposits = 80,000 | Private debt to bank = 100,000 |

| | Equity = −20,000 |

If the bank were to sell 20,000 of its private debt for 15,000, renaming it as a security, the resulting balance sheets would look like this:

Bank balance sheet:| Assets | Liabilities |

| Private debt = 80,000 | Deposits = 65,000 |

| | Equity = 15,000 |

Private sector balance sheet:| Assets | Liabilities |

| Deposits = 65,000 | Private debt to bank = 80,000 |

| Security = 20,000 | Private debt to investor = 20,000 |

| | Equity = −15,000 |

The equity of the bank has been lowered by 5000, and private sector equity has risen by an equal amount. From the perspective of systemic stability, it does not matter that the debt is ever settled. Settlement of a debt held by private actors merely moves money around instead of destroying it, which is the case when a bank debt is paid off.

This process lowers from 125% to 123.08%, thereby alleviating stress from the model. Banks selling debt at a loss is beneficial for the stability of the model. It is even better for the long-term stability of the model when compared to QE and government spending because it essentially lowers p and no trivial reverse process exists.

The solvency of banks would however be jeopardised should they lose more than they hold in equity.

5.5.4. Loan Defaulting

When private actors default on their loans, a process similar to selling debt as a loss occurs. In this case, the loss incurred by the bank equals the value of the loan minus the price for which they can sell claimed assets.

This is beneficial for the long-term stability of the model.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}