When Wrong Is Right: Leaving Room for Error in Innovation Measurement

Abstract

:1. Introduction

2. Theory Background

2.1. Innovation, KPIs and Organizational Errors

2.2. Innovation Measurement

2.3. Organizational Errors in Innovation Measurement

3. Methods

3.1. Research Design

3.2. Data Collection

3.3. Data Analysis

4. Results

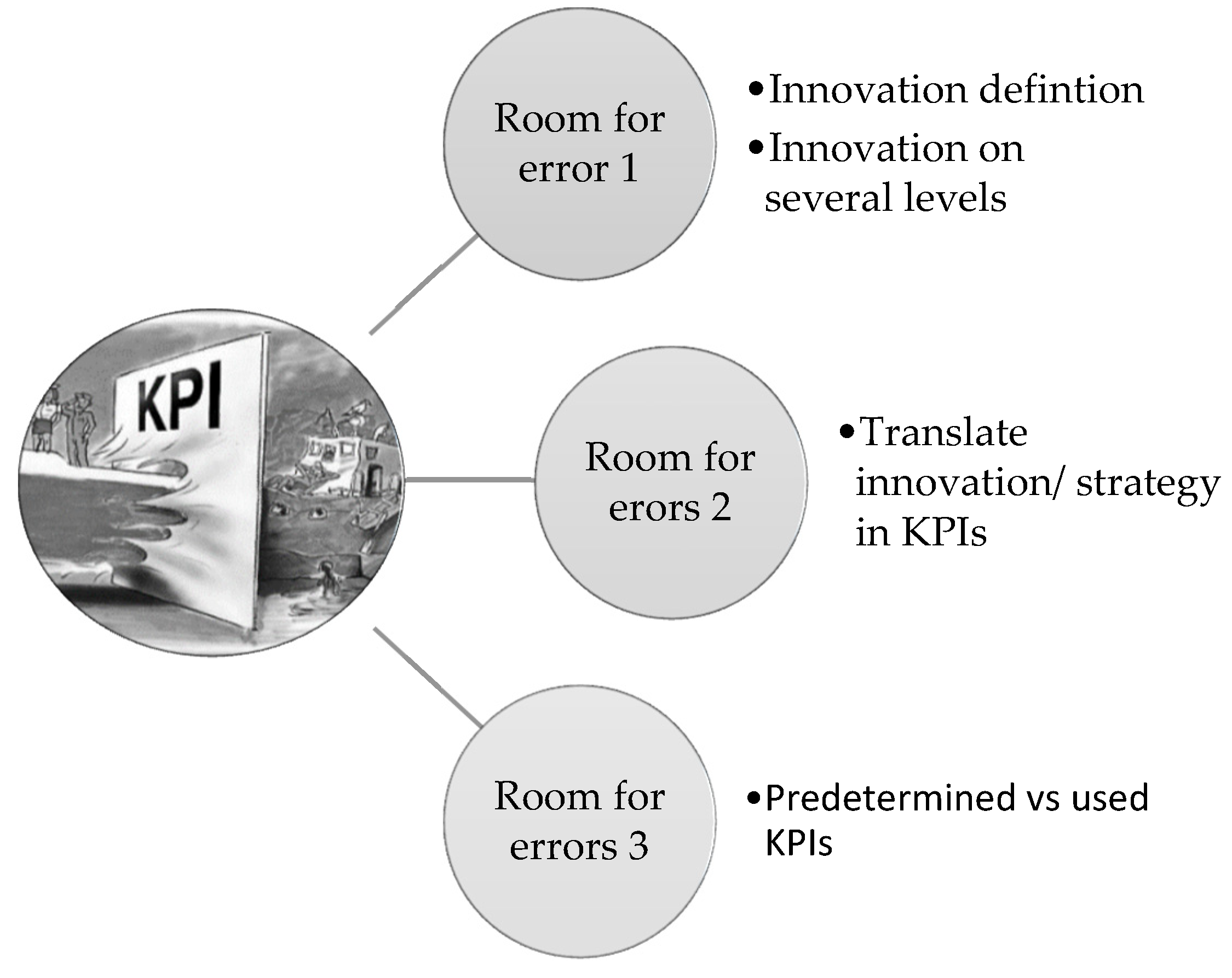

4.1. Room for Organizational Error 1: Innovation and Its Defintion

“We need to understand what innovation implies in our organization. We need to focus on our customer promise and deliver on it and understand how innovation delivers customer and business value. During my years as a controller [not in the process industry] I have never encountered such a complicated relationship between innovation and customer & business value.”Business controller

“In my previous organization I was responsible for delivering value to business through innovation [not in the process industry]. In this organization everything seems to be more unclear and the complexity of what is really innovation seem to make it more difficult.”Director innovation

“I am used to approximately 10 innovation projects per month passing a tollgate [not in the process industry] but those projects were usually homogeneous. Here at this organization all the projects seem to be unique and it takes longer time to understand them. This might explain why less projects pass a tollgate.”Innovation staff

“Before [the] innovation [department] was just supplying us with new products, now we want [the] innovation [department] to be our speaking partner.”Business account manager

“I have been to conferences on innovation management, and I have seen how other companies track their innovation. After this I have made a lot of suggestion to management how to change their KPIs.”Project manager

4.2. Room for Organizational Error 2: Innovation Strategy vs. Innovation KPIs

In industry, there is a generic triangle. At the center of the triangle are safety, health and the environment. […]. Each company defines a number of trends; they are connected [environmental] trends and [subsequently] described in our common strategy and our strategy for innovation. We currently have multiple production platforms. Then we have selected several market segments, and you should preferably fit this [innovation strategy] into a [scorecard with KPIs] which [portrays] areas we are adequately skilled at managing.

[…] Now one must instead pedagogically explain that the connection is [between innovation strategy and innovation KPIs]. I saw before when we linked the innovation strategy to the innovation KPI by means of the amount spent on innovation. The personal bonus was conditional on [this KPI] and we were not allowed to spend more than 70 percent in December. Suddenly, all staff disappeared. It was in this situation that [the linkages between innovation strategy and innovation KPIs] become clear. Most people during that time tried to do their best to change the margin and spent less. What happened was that, that year, the price of gasoline was just very high. Then you start to question the linkages, and how can I [on an individual level] affect innovation strategy or innovation KPIs? If you do not know these cycles, it can be difficult to motivate yourself towards the KPIs in innovation that you should reach.

4.3. Room for Organizational Error 3: Official KPIs vs. Used KPIs in Innovation

Actually, I do not really know what the KPIs in innovation are. So, I cannot really answer the question, is that a problem?Project manager

The information from KPIs that are relevant for my job is limited. I have been doing this job [managing the ideation part of innovation] for quite a while, so I know I have to keep an eye on tollgate 1 and tollgate 4. I know exactly how many ideas we need to deliver upon our own targets.Senior researcher

Can you please give me a definition of what a KPI is? I do not understand the difference between this and the goal and scorecard we use in the organization. And because I am new to this organization, I feel that I do not have access to all of the information and KPIs that I should know. In my previous organization everything was much more clear and accessible.Application manager

5. Discussion

6. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Adams, Richard, John Bessant, and Robert Phelps. 2006. Innovation management measurement: A review. International Journal of Management Reviews 8: 21–47. [Google Scholar] [CrossRef]

- Ahrens, Thomas, and Christopher S. Chapman. 2006. Doing qualitative field research in management accounting: Positioning data to contribute to theory. Accounting, Organizations and Society 31: 819–41. [Google Scholar] [CrossRef]

- Alfaro García, Víctor G., Anna María Gil-Lafuente, and Gerardo Alfaro Calderon. 2015. A fuzzy logic approach towards innovation measurement. Global Journal of Business Research 9: 53–71. [Google Scholar]

- Alvesson, Mats. 2003. Beyond neopositivists, romantics, and localists: A reflexive approach to interviews in organizational research. Academy of Management Review 28: 13–33. [Google Scholar] [CrossRef]

- Bansal, Pratima, Wendy K. Smith, and Eero Vaara. 2018. New Ways of Seeing through Qualitative Research. New York: Academy of Management Briarcliff Manor. [Google Scholar]

- Baregheh, Anahita, Jennifer Rowley, and Sally Sambrook. 2009. Towards a multidisciplinary definition of innovation. Management Decision 47: 1323–39. [Google Scholar] [CrossRef]

- Bititci, Umit S., Michael Bourne, Jennifer A. Cross, Sai S. Nudurupati, and Kate Sang. 2018. Towards a theoretical foundation for performance measurement and management. International Journal of Management Reviews 20: 653–60. [Google Scholar] [CrossRef]

- Bititci, Umit S., Patrizia Garengo, Viktor Dörfler, and Sai Nudurupati. 2012. Performance Measurement: Challenges for Tomorrow*. International Journal of Management Reviews 14: 305–27. [Google Scholar] [CrossRef] [Green Version]

- Bledow, Ronald, Michael Frese, Neil Anderson, Miriam Erez, and James Farr. 2009. A dialectic perspective on innovation: Conflicting demands, multiple pathways, and ambidexterity. Industrial and Organizational Psychology 2: 305–37. [Google Scholar] [CrossRef]

- Bloomberg, Linda Dale, and Marie Volpe. 2018. Completing Your Qualitative Dissertation: A Road Map from Beginning to End. Thousand Oaks: Sage. [Google Scholar]

- Bourne, Mike, Steven Melnyk, and Umit S. Bititci. 2018. Performance measurement and management: Theory and practice. International Journal of Operations & Production Management 28: 2010–21. [Google Scholar]

- Brattström, Anna, Johan Frishammar, Anders Daniel Richtnér, Jennie Bjork, and Mats Magnusson. 2016. Boxing-In and Box-Breaking of Attention: A Process Model of Innovation Measurement. Academy of Management Annual Meeting Proceedings, 14566. [Google Scholar] [CrossRef]

- Brattström, Anna, Johan Frishammar, Anders Richtnér, and Dane Pflueger. 2018. Can innovation be measured? A framework of how measurement of innovation engages attention in firms. Journal of Engineering and Technology Management 48: 64–75. [Google Scholar] [CrossRef]

- Brinkmann, Svend, and Steinar Kvale. 2015. Conducting an interview. Interviews. Learning the Craft of Qualitative Research Interviewing, 149–66. [Google Scholar]

- Chandler, Alfred Dupont. 1990. Strategy and Structure: Chapters in the History of the Industrial Enterprise. Cambridge: MIT Press, vol. 120. [Google Scholar]

- Chenhall, Robert H. 2003. Management control systems design within its organizational context: Findings from contingency-based research and directions for the future. Accounting, Organizations and Society 28: 127–68. [Google Scholar] [CrossRef]

- Chenhall, Robert H. 2009. Theorizing Contingencies in Management Control Systems Research. Handbook of Management Accounting Research 1: 163–205. [Google Scholar]

- Chenhall, Robert H., and Frank Moers. 2015. The role of innovation in the evolution of management accounting and its integration into management control. Accounting, Organizations and Society 47: 1–13. [Google Scholar] [CrossRef]

- Choong, Kwee Keong. 2014. Has this large number of performance measurement publications contributed to its better understanding? A systematic review for research and applications. International Journal of Production Research 52: 4174–97. [Google Scholar] [CrossRef]

- Crossan, Mary M., and Marina Apaydin. 2010. A multi-dimensional framework of organizational innovation: A systematic review of the literature. Journal of Management Studies 47: 1154–91. [Google Scholar] [CrossRef]

- Dahlin, Kristina B., You-Ta Chuang, and Thomas J Roulet. 2018. Opportunity, motivation, and ability to learn from failures and errors: Review, synthesis, and ways to move forward. Academy of Management Annals 12: 252–77. [Google Scholar] [CrossRef] [Green Version]

- Damanpour, Fariborz, and J. Daniel Wischnevsky. 2006. Research on innovation in organizations: Distinguishing innovation-generating from innovation-adopting organizations. Journal of Engineering and Technology Management 23: 269–91. [Google Scholar] [CrossRef]

- Davila, Antonio. 2012. New trends in performance measurement and management control. In Performance Measurement and Management Control: Global Issues. Bingley: Emerald Group Publishing Limited, pp. 65–87. [Google Scholar]

- Davila, Antonio, and Daniel Oyon. 2009. Introduction to the special section on accounting, innovation and entrepreneurship. European Accounting Review 18: 277–80. [Google Scholar] [CrossRef]

- Davila, Antonio, George Foster, and Daniel Oyon. 2009. Accounting and control, entrepreneurship and innovation: Venturing into new research opportunities. European Accounting Review 18: 281–311. [Google Scholar] [CrossRef]

- Davila, Tony, Marc Epstein, and Robert Shelton. 2012. Making Innovation Work: How to Manage it, Measure it, and Profit from It. Upper Saddle River: FT Press. [Google Scholar]

- Dewangan, Vikas, and Manish Godse. 2014. Towards a holistic enterprise innovation performance measurement system. Technovation 34: 536–45. [Google Scholar] [CrossRef]

- Drucker, Peter F. 1998. The discipline of innovation. Harvard Business Review 76: 149–57. [Google Scholar] [CrossRef] [PubMed]

- Dziallas, Marisa, and Knut Blind. 2019. Innovation indicators throughout the innovation process: An extensive literature analysis. Technovation 80: 3–29. [Google Scholar] [CrossRef]

- Edison, Henry, Nauman Bin Ali, and Richard Torkar. 2013. Towards innovation measurement in the software industry. Journal of Systems and Software 86: 1390–407. [Google Scholar] [CrossRef] [Green Version]

- Edmondson, Amy C., and Paul J. Verdin. 2018. The Strategic Imperative of Psychological Safety and Organizational Error Management. In How Could This Happen? Berlin: Springer, pp. 81–104. [Google Scholar]

- Eurostat, O. 2018. Oslo Manual 2018: Guidelines for Colleting, Reporting and Using Data on Innovation. Luxembourg: OECD Publishing. [Google Scholar]

- Ferreira, Aldónio, and David Otley. 2009. The design and use of performance management systems: An extended framework for analysis. Management Accounting Research 20: 263–82. [Google Scholar] [CrossRef]

- Franco-Santos, Monica, Lorenzo Lucianetti, and Mike Bourne. 2012. Contemporary performance measurement systems: A review of their consequences and a framework for research. Management Accounting Research 23: 79–119. [Google Scholar] [CrossRef] [Green Version]

- Frese, Michael, and Nina Keith. 2015. Action errors, error management, and learning in organizations. Annual Review of Psychology 66: 661–87. [Google Scholar] [CrossRef]

- Fried, Andrea. 2017. Terminological distinctions of ‘control’: A review of the implications for management control research in the context of innovation. Journal of Management Control 28: 5–40. [Google Scholar] [CrossRef] [Green Version]

- Garcia, Rosanna, Karin Wigger, and Roberto Rivas Hermann. 2019. Challenges of creating and capturing value in open eco-innovation: Evidence from the maritime industry in Denmark. Journal of Cleaner Production 220: 642–54. [Google Scholar] [CrossRef]

- Gimbert, Xavier, Josep Bisbe, and Xavier Mendoza. 2010. The role of performance measurement systems in strategy formulation processes. Long Range Planning 43: 477–97. [Google Scholar] [CrossRef]

- Goodman, Paul S., Rangaraj Ramanujam, John S. Carroll, Amy C Edmondson, David A. Hofmann, and Kathleen M. Sutcliffe. 2011. Organizational errors: Directions for future research. Research in Organizational Behavior 31: 151–76. [Google Scholar] [CrossRef]

- Goshu, Yitagesu Yilma, and Daniel Kitaw. 2017. Performance measurement and its recent challenge: A literature review. International Journal of Business Performance Management 18: 381–402. [Google Scholar] [CrossRef]

- Harris, Michael, and Bill Tayler. 2019. Don’t Let Metrics Undermine Your Business. Harvard Business Review 97: 63–69. [Google Scholar]

- Harrison, Helena, Melanie Birks, Richard Franklin, and Jane Mills. 2017. Case study research: Foundations and methodological orientations. Forum Qualitative Sozialforschung/Forum: Qualitative Social Research 18. [Google Scholar] [CrossRef]

- Henri, Jean-François, and Marc J. F. Wouters. 2017. Coexistence of Management Control Practices and Successful Product Innovation. Paper presented at 2017 Canadian Academic Accounting Association (CAAA) Annual Conference, Montreal, QC, Canada, June 1–3. [Google Scholar]

- Hofmann, David A., and Michael Frese. 2011. Errors, error taxonomies, error prevention, and error management: Laying the groundwork for discussing errors in organizations. Errors in Organizations 1: 44. [Google Scholar]

- Janssen, Sebastian, Klaus Moeller, and Marten Schlaefke. 2011. Using performance measures conceptually in innovation control. Journal of Management Control 22: 107. [Google Scholar] [CrossRef] [Green Version]

- Jørgensen, Brian, and Martin Messner. 2010. Accounting and strategising: A case study from new product development. Accounting, Organizations and Society 35: 184–204. [Google Scholar] [CrossRef]

- Keong Choong, Kwee. 2014. The fundamentals of performance measurement systems: A systematic approach to theory and a research agenda. International Journal of Productivity and Performance Management 63: 879–922. [Google Scholar] [CrossRef]

- Khanna, Rajat, Isin Guler, and Atul Nerkar. 2016. Fail often, fail big, and fail fast? Learning from small failures and R&D performance in the pharmaceutical industry. Academy of Management Journal 59: 436–59. [Google Scholar]

- Kvale, Steinar, and Svend Brinkmann. 2009. Interviews: Learning the Craft of Qualitative Research Interviewing. Thousand Oaks: Sage. [Google Scholar]

- Lei, Zhike, Eitan Naveh, and Zhanna Novikov. 2016. Errors in organizations: An integrative review via level of analysis, temporal dynamism, and priority lenses. Journal of Management 42: 1315–43. [Google Scholar] [CrossRef]

- Liao, Shu-Hsien, and Chi-chuan Wu. 2010. System perspective of knowledge management, organizational learning, and organizational innovation. Expert Systems with Applications 37: 1096–103. [Google Scholar] [CrossRef]

- McKinnon, Jill. 1988. Reliability and validity in field research: Some strategies and tactics. Accounting, Auditing & Accountability Journal 1: 34–54. [Google Scholar]

- Melendez, Karin, Abraham Dávila, and Andrés Melgar. 2019. Literature Review of the Measurement in the Innovation Management. Journal of Technology Management & Innovation 14: 81–87. [Google Scholar]

- Melnyk, Steven A., Roger J. Calantone, Joan Luft, Douglas M. Stewart, George A. Zsidisin, John Hanson, and Laird Burns. 2005. An empirical investigation of the metrics alignment process. International Journal of Productivity and Performance Management 54: 312–24. [Google Scholar] [CrossRef]

- Melnyk, Steven A., Umit Bititci, Ken Platts, Jutta Tobias, and Bjørn Andersen. 2014. Is performance measurement and management fit for the future? Management Accounting Research 25: 173–86. [Google Scholar] [CrossRef]

- Micheli, Pietro, and Luca Mari. 2014. The theory and practice of performance measurement. Management Accounting Research 25: 147–56. [Google Scholar] [CrossRef]

- Neely, Andy, and Mike Bourne. 2000. Why measurement initiatives fail. Measuring Business Excellence 4: 3–7. [Google Scholar] [CrossRef]

- Neely, Andy, Mike Gregory, and Ken Platts. 1995. Performance measurement system design: A literature review and research agenda. International Journal of Operations & Production Management 15: 80–116. [Google Scholar]

- Neely, Andy, Mike Gregory, and Ken Platts. 2005. Performance measurement system design: A literature review and research agenda. International Journal of Operations & Production Management 25: 1228–63. [Google Scholar]

- Nixon, Bill, and John Burns. 2012. The paradox of strategic management accounting. Management Accounting Research 23: 229–44. [Google Scholar] [CrossRef]

- Nudurupati, Sai S., Umit S. Bititci, Vikas Kumar, and Felix T. S. Chan. 2011. State of the art literature review on performance measurement. Computers & Industrial Engineering 60: 279–90. [Google Scholar]

- Okwir, Simon, Sai S. Nudurupati, Matías Ginieis, and Jannis Angelis. 2018. Performance measurement and management systems: A perspective from complexity theory. International Journal of Management Reviews 20: 731–54. [Google Scholar] [CrossRef] [Green Version]

- Ollila, Susanne, and Anna Yström. 2020. Action research for innovation management: Three benefits, three challenges, and three spaces. R&d Management. [Google Scholar] [CrossRef] [Green Version]

- Ortt, J. Roland, and Patrick A. van der Duin. 2008. The evolution of innovation management towards contextual innovation. European Journal of Innovation Management 11: 522–38. [Google Scholar] [CrossRef] [Green Version]

- Porter, Michael E. 1990. The competitive advantage of nations. Competitive Intelligence Review 1: 14–14. [Google Scholar] [CrossRef]

- Richtnér, Anders, Anna Brattström, Johan Frishammar, Jennie Björk, and Mats Magnusson. 2017. Creating better innovation measurement practices. MIT Sloan Management Review 59: 45. [Google Scholar]

- Schrage, Michael, and David Kiron. 2018. Leading with next-generation key performance indicators. MITSloan Management Review and Google June, 1–2. [Google Scholar]

- Taticchi, Paolo, Kashi Balachandran, and Flavio Tonelli. 2012. Performance measurement and management systems: State of the art, guidelines for design and challenges. Measuring Business Excellence 16: 41–54. [Google Scholar] [CrossRef]

- Tidd, Joe, and John R. Bessant. 2018. Managing Innovation: Integrating Technological, Market and Organizational Change. Hoboken: John Wiley & Sons. [Google Scholar]

- Weick, Karl E. 2012. Errors in Organizations. Edited by David A. Hofmann and Michael Frese. Los Angeles: Sage Publications Sage. [Google Scholar]

- Yin, Robert K. 2014. Case Study Research: Design and Methods, 5th ed. Thousand Oaks: Sage publications. [Google Scholar]

{kind=link}

| Date of Interviews | Number of Interviews | Average Time Interview | Job Title | Data Collected |

|---|---|---|---|---|

| Autumn 2017 Spring 2018 | 28 | 1/2–½ h | Innovation personnel (5), controller (3), sales manager (3), R&D manager, sales and technical support manager, senior consultant innovation, project manager (4), program manager, business managers, production managers (2), patent manager, CEO, director of innovation. | Interviews, Notes, Reports Powerpoints Presentation Emails |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Svensson de Jong, I. When Wrong Is Right: Leaving Room for Error in Innovation Measurement. J. Risk Financial Manag. 2021, 14, 332. https://doi.org/10.3390/jrfm14070332

Svensson de Jong I. When Wrong Is Right: Leaving Room for Error in Innovation Measurement. Journal of Risk and Financial Management. 2021; 14(7):332. https://doi.org/10.3390/jrfm14070332

Chicago/Turabian StyleSvensson de Jong, Ilse. 2021. "When Wrong Is Right: Leaving Room for Error in Innovation Measurement" Journal of Risk and Financial Management 14, no. 7: 332. https://doi.org/10.3390/jrfm14070332