The Moderating Effect of Family Business Ownership on the Relationship between Short-Selling Mechanism and Firm Value for Listed Companies in China

Abstract

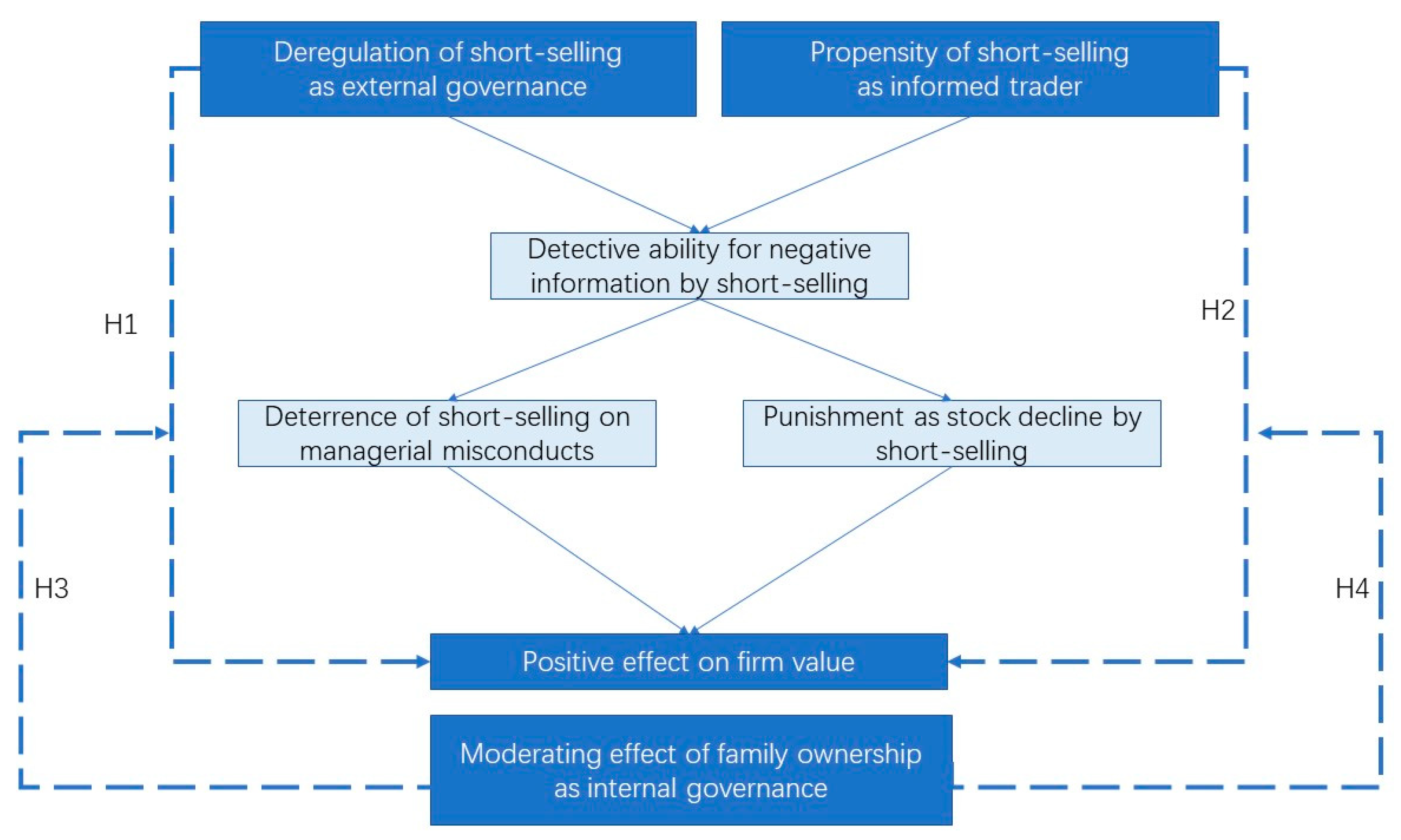

:1. Introduction

2. Literature Review and Hypothesis Development

2.1. Short Selling Mechanism

2.2. Family Business

3. Methodology

3.1. Data and Sample Sources

3.2. Measurement of Variables and Models

3.3. The Propensity Score Matching (PSM) Method

4. Results and Discussion

4.1. Empirical Results and Discussion

4.2. Robustness Test

4.2.1. Alternative Measures of Firm Value

4.2.2. Multicollinearity Test Using Variance Inflation Factor (VIF)

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Abrardi, Laura, and Laura Rondi. 2020. Ownership and performance in the Italian stock exchange: The puzzle of family firms. Journal of Industrial and Business Economics 47: 613–43. [Google Scholar] [CrossRef]

- Aguiar-Inmaculada Diaz, Ruiz-Mallorquí María Victoria, and Lourdes Trujillo. 2020. Ownership structure and financial performance of Spanish port service companies. Maritime Economics and Logistics 22: 674–98. [Google Scholar] [CrossRef]

- Brockman, Paul, Juan Luo, and Limin Xu. 2020. The impact of short-selling pressure on corporate employee relations. Journal of Corporate Finance 64: 101–667. [Google Scholar] [CrossRef]

- Cai, Tianyu, and Lixiong Guo. 2018. Short Selling and Real Earnings Management. Journal of International Accounting Research 19: 117–40. [Google Scholar]

- Caliendo, Marco, and Sabine Kopeinig. 2008. Some practical guidance for the implementation of propensity score matching. Journal of Economic Surveys 22: 31–72. [Google Scholar] [CrossRef] [Green Version]

- Chen, Jun, Palani-Rajan Kadapakkam, and Ting Yang. 2016. Short selling, margin trading, and the incorporation of new information into prices. International Review of Financial Analysis 44: 1–17. [Google Scholar] [CrossRef]

- Chen, Jun, Huimin Li, and Dazhi Zheng. 2020a. The Impact of Margin-Trading and Short-Selling on Stock Price Efficiency—Evidence from the Fifth-Round Ban Lift in the Chinese Stock Market. The Chinese Economy 53: 265–84. [Google Scholar] [CrossRef]

- Chen, Shenglan, Robin K. Chou, Xiaoling Liu, and Yuhui Wu. 2020b. Deregulation of short-selling constraints and cost of bank loans: Evidence from a quasi-natural experiment. Pacific Basin Finance Journal 64: 101460. [Google Scholar] [CrossRef]

- Cheng, Qiang. 2014. Family firm research–A review. China Journal of Accounting Research 7: 149–63. [Google Scholar] [CrossRef] [Green Version]

- Cordeiro, James J, Giorgia Profumo, and Ilaria Tutore. 2020. Board gender diversity and corporate environmental performance: The moderating role of family and dual-class majority ownership structures. Business Strategy and the Environment 29: 1127–44. [Google Scholar] [CrossRef]

- Ergün, Bahadır, and Ömer Tuğsal Doruk. 2020. Effect of financial constraints on the growth of family and nonfamily firms in Turkey. Financial Innovation 6: 1–24. [Google Scholar] [CrossRef]

- Gao, George, Qingzhong Ma, and David Ng. 2018. The informativeness of short sellers: An insider’s perspective. China Finance Review International 8: 354–86. [Google Scholar] [CrossRef]

- Gao, Hao, Jing He, Yong Li, and Yuanyu Qu. 2020. Family control and cost of debt: Evidence from China. Pacific Basin Finance Journal 60: 101286. [Google Scholar] [CrossRef]

- Gong, Rong. 2020. Short selling threat and corporate financing decisions. Journal of Banking and Finance 118: 105853. [Google Scholar] [CrossRef]

- Hair, Joseph F., Bill Black, Barry Babin, Rolph E. Anderson, and Ronald L. Tatham. 2006. Multivariate Data Analysis, 6th ed. London: Pearson University Press. [Google Scholar]

- Hamid, Arsalan Abdul, Rana Tahir Naveed, Tasawar Abdul Hamid, and Muhammad Waris Rao. 2020. The impact of cash management and corporate governance on firm performance, and the moderating role of family ownership on the emerging economy. International Journal of Innovation, Creativity and Change 13: 592–616. [Google Scholar]

- Harith, Samir, and Ruth Helen Samujh. 2020. Small Family Businesses: Innovation, Risk and Value. Journal of Risk and Financial Management 13: 240. [Google Scholar] [CrossRef]

- He, Jie, and Xuan Tian. 2015. SHO Time for Innovation: The Real Effects of Short Sellers. Kelley School of Business Research Paper. Bloomington: Kelley School. [Google Scholar]

- He, Jie, and Xuan Tian. 2018. Finance and corporate innovation: A survey. Asia-Pacific Journal of Financial Studies 47: 165–212. [Google Scholar] [CrossRef]

- Hughes-Morgan, Margaret, and Walter J. Ferrier. 2017. ‘Short Interest Pressure’and Competitive Behaviour. British Journal of Management 28: 120–34. [Google Scholar] [CrossRef] [Green Version]

- Jiang, Haiyan, and Jun Chen. 2019. Short selling and financial reporting quality: Evidence from Chinese AH shares. Journal of Contemporary Accounting & Economics 15: 118–30. [Google Scholar]

- Kamaludin, Kamilah, Izani Ibrahim, and Sheela Sundarasen. 2020. Moderating Effects of Family Business on Audit Committee Diligence and Firm Performance: A Middle Eastern Perspective. International Journal of Economics & Management 14: 173–88. [Google Scholar]

- Koji, Kojima, Bishnu Kumar Adhikary, and Le Tram. 2020. Corporate Governance and Firm Performance: A Comparative Analysis between Listed Family and Non-Family Firms in Japan. Journal of Risk and Financial Management 13: 215. [Google Scholar] [CrossRef]

- Leitterstorf, Max P., and Sabine B. Rau. 2014. Socioemotional wealth and IPO underpricing of family firms. Strategic Management Journal 35: 751–60. [Google Scholar] [CrossRef]

- Li, Zijin. 2018. Lifting of Short Selling Constraints and Accounting Policy Options—Empirical Data from Asset Impairment Provision. Modern Economy 9: 1776–91. [Google Scholar] [CrossRef] [Green Version]

- Li, Rui, Jiahui Li, and Jinjian Yuan. 2017. Short-sale prohibitions, firm characteristics and stock returns: Evidence from Chinese market. China Finance Review International 7: 407–28. [Google Scholar] [CrossRef]

- Li, Chuntao, Hongmei Xu, Liwei Wang, and Peng Zhou. 2019. Short-selling and corporate innovation: Evidence from the Chinese market. China Journal of Accounting Studies 7: 293–316. [Google Scholar] [CrossRef]

- Liu, Fei, Jianhua Du, and Chao Bian. 2019. Don’t Touch My Cheese: Short Selling Pressure, Executive Compensation Justification, and Real Activity Earnings Management. Emerging Markets Finance and Trade 55: 1969–90. [Google Scholar] [CrossRef]

- Lu, Jinzhi. 2018. Short Selling, Earnings Management, and Firm Value. Earnings Management, and Firm Value 23: 2018. [Google Scholar] [CrossRef]

- Mai, Wenzhen, and Nik Intan Norhan Binti Abdul Hamid. 2020. Understanding the Effect of Short Selling Mechanism on Market Value of Pharmaceutical Industry in China Under Covid-19. Paper presented at the Basic & Clinical Pharmacology& Toxicology, Toronto, ON, Canada, June 26. [Google Scholar]

- Mai, Wenzhen, and Nik Intan Norhan Binti Abdul Hamid. 2021a. Short-Selling and Financial Performance of SMEs in China: The Mediating Role of CSR Performance. International Journal of Financial Studies 9: 22. [Google Scholar] [CrossRef]

- Mai, Wenzhen, and Nik Intan Norhan Binti Abdul Hamid. 2021b. Short-selling deregulation and corporate social responsibility of tourism industry in China. Paper presented at E3S Web of Conferences, Shenzhen, China, November 26–28. [Google Scholar]

- Massa, Massimo, Bohui Zhang, and Hong Zhang. 2015. The invisible hand of short selling: Does short selling discipline earnings management? The Review of Financial Studies 28: 1701–36. [Google Scholar] [CrossRef]

- Meng, Qingbin, Ying Li, Xuanyu Jiang, and Kam C. Chan. 2017. Informed or speculative trading? Evidence from short selling before star and non-star analysts’ downgrade announcements in an emerging market. Journal of Empirical Finance 42: 240–55. [Google Scholar] [CrossRef]

- Miroshnychenko, Ivan, Roberto Barontini, and De Alfredo Massis. 2020. Investment opportunities and R&D investments in family and nonfamily firms. R and D Management 50: 447–61. [Google Scholar] [CrossRef]

- Mustafa, Adeel, Abubakr Saeed, Muhammad Awais, and Shahab Aziz. 2020. Board-Gender Diversity, Family Ownership, and Dividend Announcement: Evidence from Asian Emerging Economies. Journal of Risk and Financial Management 13: 62. [Google Scholar] [CrossRef] [Green Version]

- Ni, Xiaoran, and Sirui Yin. 2020. The unintended real effects of short selling in an emerging market. Journal of Corporate Finance 64: 101659. [Google Scholar] [CrossRef]

- Ntoung, Lious Agbor Tabot, Santos de Helena Maria Oliveira, Benjamim Manuel Ferreira de Sousa, Liliana Marques L. M. Pimentel, and Susana Adelina Moreira Carvalho Bastos. 2020. Are Family Firms Financially Healthier Than Non-Family Firm? Journal of Risk and Financial Management 13: 5. [Google Scholar] [CrossRef] [Green Version]

- Park, KoEun. 2017. Earnings quality and short selling: Evidence from real earnings management in the United States. Journal of Business Finance & Accounting 44: 1214–40. [Google Scholar]

- Pittino, Daniel, Francesco Chirico, Bart Henssen, and Wouter Broekaert. 2020. Does Increased Generational Involvement Foster Business Growth? The Moderating Roles of Family Involvement in Ownership and Management. European Management Review 17: 785–801. [Google Scholar] [CrossRef]

- Ramos, Hazel Melanie, William Peter Buck, and Saw Leng Ong. 2016. The influence of family ownership and involvement on Chinese family firm performance: A systematic literature review. International Journal of Management Practice 9: 365–93. [Google Scholar] [CrossRef]

- Rennekamp, Kristina, Kathy Rupar, and Nicholas Seybert. 2019. Short Selling Pressure, Reporting Transparency, and the Use of Real and Accruals Earnings Management to Meet Benchmarks. Journal of Behavioral Finance 21: 186–204. [Google Scholar] [CrossRef]

- Swanpitak, Tanapond, Xiaofei Pan, and Sandy Suardi. 2020a. Family control and cost of debt: Evidence from Thailand. Pacific Basin Finance Journal 62: 101376. [Google Scholar] [CrossRef]

- Swanpitak, Tanapond, Xiaofei Pan, and Sandy Suardi. 2020b. The value of family control during political uncertainty: Evidence from Thailand’s constitutional change in 2014. Emerging Markets Review 44: 100721. [Google Scholar] [CrossRef]

- Tang, Liang, Kangyin Lu, and Wei Wu. 2017. Comparison of family ownership and non-family ownership private firm performance. Transformations in Business and Economics 16: 381–96. [Google Scholar]

- Tseng, Chih-Yang -. 2020. Family firms and long-term orientation of SG& A expenditures. Review of Quantitative Finance and Accounting 55: 1181–206. [Google Scholar] [CrossRef]

- Villalonga, Belén, and Raphael Amit. 2010. Family control of firms and industries. Financial Management 39: 863–904. [Google Scholar] [CrossRef]

- Xiang, Dong, Jiakui Chen, David Tripe, and Ning Zhang. 2019. Family firms, sustainable innovation and financing cost: Evidence from Chinese hi-tech small and medium-sized enterprises. Technological Forecasting and Social Change 144: 499–511. [Google Scholar] [CrossRef]

- Yang, Jie, Jieqiong Ma, and D. Harold Doty. 2020. Family Involvement, Governmental Connections, and IPO Underpricing of SMEs in China. Family Business Review 33: 175–93. [Google Scholar] [CrossRef]

- Zhou, Yan, Haoze Ding, and Jiawei Hao. 2019. Short-Sellers’ Private Information Research: Based on the Perspective of Earnings Announcement. Paper presented at 2019 16th International Conference on Service Systems and Service Management (ICSSSM), Shenzhen, China, July 13–15. [Google Scholar]

- Zhu, Zhu, and Feifei Lu. 2020. Family Ownership and Corporate Environmental Responsibility: The Contingent Effect of Venture Capital and Institutional Environment. Journal of Risk and Financial Management 13: 110. [Google Scholar] [CrossRef]

- Zou, Ying, Zhuoming Zhong, and Jia Luo. 2021. Ethnic diversity, investment efficiency, mediating roles of trust and agency cost. Economic Analysis and Policy 69: 410–20. [Google Scholar] [CrossRef]

- Zulfiqar, Muhammad, Khalid Hussain, Muhammad Usman Yousaf, Nadeem Sohail, and Sadeen Ghafoor. 2020. Moderating role of CEO compensation in lean innovation strategies of Chinese listed family firms. Corporate Governance 20: 887–902. [Google Scholar] [CrossRef]

{kind=link}

| Variables | Measurement | Sources |

|---|---|---|

| Independent Variables | ||

| Deregulation of short selling (SHORT) | A dummy variable (0,1), equals to 1 if the firm is shortable, and 0 otherwise | Shanghai and Shenzhen Stock exchange |

| Time factor of short selling (TREAT) | A dummy variable (0,1), equals to 1 for the years after firm is shortable, and 0 otherwise. | Shanghai and Shenzhen Stock exchange |

| SHORT*TREAT | Interactive item of SHORT and TREAT | Shanghai and Shenzhen Stock exchange |

| Short Interest (SIR) | number of stocks sold by short-sellers minus the number of stocks repaid, divided by trading volume of the prior day. | CSMAR Database |

| Family ownership (FO) | A dummy variable (0,1), equals 1 if the firm is family-owned, and 0 otherwise; Family business is defined as the founder and his family possesses more than 25% of this total ownership. | Annual Reports |

| Dependent Variables | ||

| Tobin’s Q | Market value of total assets divided by asset value | CSMAR Database |

| ROA | Net income divided by total assets | CSMAR Database |

| Control Variables | ||

| Firm size (SIZE) | Natural logarithm of the market capitalisation | CSMAR Database |

| Firm growth (GROWTH) | Sales growth | CSMAR Database |

| Leverage (LEV) | Total liability divided by total assets | CSMAR Database |

| R&D investment (RD) | R&D expenditures divided by total expenses | CSMAR Database |

| Board size (b-size) | Natural logarithm of the number of board members | CSMAR Database |

| board independence(b-ind) | independent directors divided by corporate board | CSMAR Database |

| state-ownership (SOE) | A dummy variable (0,1), equals to 1 if the firm’s largest shareholder is state-owned, and 0 otherwise | CSMAR Database |

| Institutional ownership (IO) | A dummy variable (0,1), equals to 1 if the firm’s largest shareholder is institution, and 0 otherwise | CSMAR Database |

| Firm effect | ||

| Year effect |

| Before PSM | After PSM | |||||||

|---|---|---|---|---|---|---|---|---|

| Variables | Treatment | Control | Diff | T-Statistics | Treatment | Control | Diff | T-Statistics |

| SIZE | 22.6435 | 21.4996 | 1.1440 *** | 81.4867 | 22.6273 | 22.6304 | −0.0031 | −0.1958 |

| GROWTH | 0.1213 | 0.0433 | 0.0780 *** | 4.4002 | 0.1206 | 0.1107 | 0.0099 * | 2.9007 |

| LEV | 0.4559 | 0.3848 | 0.0711 *** | 27.5174 | 0.4555 | 0.4647 | −0.0091 | −3.4203 |

| RD | 0.0625 | 0.0913 | −0.0288 *** | −8.7765 | 0.0627 | 0.0579 | 0.0047 * | 1.6472 |

| TURNOVER | 21.4475 | 20.6484 | 0.7992 *** | 59.4930 | 21.4351 | 21.3271 | 0.1079 ** | 8.4327 |

| VOLATILITY | 6.4023 | 6.9809 | −0.5786 *** | −9.6234 | 6.3758 | 6.8646 | −0.4888 ** | −7.6344 |

| b-size | 2.1746 | 2.1098 | 0.0648 *** | 24.9848 | 2.1737 | 2.1730 | 0.0007 | 0.2598 |

| b-ind | 0.3710 | 0.3728 | −0.0018 ** | −2.4779 | 0.3710 | 0.3695 | 0.0015 * | 2.0150 |

| SOE | 0.4728 | 0.2732 | 0.1997 *** | 31.5082 | 0.4707 | 0.4851 | −0.0145 * | −2.2142 |

| IO | 0.6765 | 0.4354 | 0.2411 *** | 37.4953 | 0.6751 | 0.6410 | 0.0341 * | 5.4941 |

| Variables | Sample | Mean | Sd | Min | Max |

|---|---|---|---|---|---|

| Tobin’s Q | 22,468 | 1.7047 | 0.8614 | 0.9106 | 6.6414 |

| ROA | 22,468 | 0.0483 | 0.0434 | −0.1046 | 0.1872 |

| SHORT | 22,468 | 0.5226 | 0.4103 | 0.0000 | 1.0000 |

| TREAT | 22,468 | 0.2523 | 0.4632 | 0.0000 | 1.0000 |

| SIR | 5680 | 0.0139 | 0.0135 | 0.0000 | 0.3442 |

| FO | 22,468 | 0.3534 | 0.4780 | 0.0000 | 1.0000 |

| SIZE | 22,468 | 22.6289 | 1.1986 | 19.7432 | 26.1355 |

| GROWTH | 22,468 | 0.1160 | 0.2750 | 0.0177 | 0.6743 |

| LEV | 22,468 | 0.4601 | 0.2035 | 0.0515 | 0.8616 |

| RD | 22,468 | 0.0603 | 0.1826 | 0.0010 | 0.9660 |

| b-size | 22,468 | 2.1734 | 0.2011 | 1.3863 | 2.8904 |

| b-ind | 22,468 | 0.3702 | 0.0535 | 0.0000 | 0.8000 |

| SOE | 22,468 | 0.4779 | 0.4995 | 0.0000 | 1.0000 |

| IO | 22,468 | 0.6581 | 0.4744 | 0.0000 | 1.0000 |

| Variables | Tobin’s Q | ROA | TREAT*SHORT | FO | Size | Growth | LEV | RD | b-size | b-ind | SOE | IO |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Tobin’s Q | 1.0000 | |||||||||||

| ROA | 0.2753 *** | 1.0000 | ||||||||||

| TREAT*SHORT | 0.2436 *** | 0.0641 ** | 1.0000 | |||||||||

| FO | 0.1505 *** | 0.1923 *** | −0.0580 *** | 1.0000 | ||||||||

| SIZE | −0.5104 *** | −0.1661 *** | 0.2438 *** | −0.2821 *** | 1.0000 | |||||||

| GROWTH | 0.4002 *** | 0.2178 *** | −0.1311 *** | 0.1333 *** | −0.2276 *** | 1.0000 | ||||||

| LEV | −0.3776 *** | −0.4268 *** | 0.0275 *** | −0.2592 *** | 0.5602 *** | −0.1178 *** | 1.0000 | |||||

| RD | 0.0047 ** | 0.0749 *** | 0.0985 *** | 0.0376 *** | 0.0108 | −0.0542 *** | −0.0913 *** | 1.0000 | ||||

| b-size | −0.1379 *** | −0.0349 *** | 0.0270 *** | −0.2493 *** | 0.2520 *** | −0.1455 *** | 0.1523 *** | −0.0584 *** | 1.0000 | |||

| b-ind | 0.0182 *** | −0.0306 *** | 0.0388 *** | 0.0471 *** | 0.0320 *** | 0.0370 *** | 0.0142 ** | 0.0027 | −0.4531 *** | 1.0000 | ||

| SOE | −0.1981 *** | −0.1791 *** | 0.0480 *** | −0.7069 *** | 0.3328 *** | −0.1722 *** | 0.3170 *** | −0.0821 *** | 0.2572 *** | −0.0274 *** | 1.0000 | |

| IO | −0.0115 * | −0.1845 *** | 0.1655 *** | −0.3207 *** | 0.2156 *** | −0.2399 *** | 0.2516 *** | −0.0468 *** | 0.1238 *** | −0.0481 *** | 0.3390 *** | 1.0000 |

| M1a | M1b | |||

|---|---|---|---|---|

| Tobin’s Q | ROA | |||

| Variables | Coefficient | Probability | Coefficient | Probability |

| Intercept | 6.8401 *** | 0.000 | −0.0966 *** | 0.000 |

| SHORT | 0.2176 *** | 0.000 | 0.0027 *** | 0.000 |

| TREAT*SHORT | 0.5087 *** | 0.000 | 0.0046 *** | 0.000 |

| SIZE | −0.2597 *** | 0.000 | 0.0081 *** | 0.000 |

| GROWTH | 11.0309 *** | 0.000 | 0.4074 *** | 0.000 |

| LEV | −0.5509 *** | 0.000 | −0.1147 *** | 0.000 |

| RD | 0.0161 ** | 0.032 | 0.0119 *** | 0.000 |

| b-size | −0.5139 *** | 0.000 | −0.0060 *** | 0.000 |

| b-ind | 0.2552 *** | 0.004 | 0.0199 *** | 0.002 |

| SOE | −0.2972 *** | 0.000 | −0.0125 *** | 0.000 |

| IO | −0.0182 * | 0.063 | −0.0135 *** | 0.000 |

| Firm-fixed | yes | yes | ||

| Year-fixed | yes | yes | ||

| R-square | 0.501365 | 0.276921 | ||

| Adj R-square | 0.500171 | 0.272055 | ||

| F-statistics | 5856.637 | 2229.85 | ||

| N | 22468 | 22468 | ||

| M2a | M2b | |||

|---|---|---|---|---|

| Tobin’s Q | ROA | |||

| Variables | Coefficient | Probability | Coefficient | Probability |

| Intercept | 6.2755 *** | 0.000 | −0.2106 *** | 0.000 |

| SIR | 4.4419 *** | 0.000 | 0.2668 *** | 0.000 |

| SIZE | −0.1874 *** | 0.000 | 0.0133 *** | 0.000 |

| GROWTH | 22.5524 *** | 0.000 | 0.5337 *** | 0.000 |

| LEV | −1.6376 *** | 0.000 | −0.1267 *** | 0.000 |

| RD | 0.0153 * | 0.062 | 0.0122 *** | 0.000 |

| b-size | −0.4899 *** | 0.000 | −0.0062 *** | 0.000 |

| b-ind | 0.2433 *** | 0.004 | −0.0205 *** | 0.000 |

| SOE | −0.2833 *** | 0.000 | −0.0128 *** | 0.000 |

| IO | −0.0174 * | 0.060 | −0.0139 *** | 0.000 |

| Firm-fixed | yes | yes | ||

| Year-fixed | yes | yes | ||

| R-square | 0.692211 | 0.285828 | ||

| Adj R-square | 0.688559 | 0.280504 | ||

| F-statistics | 3097.965 | 550.754 | ||

| N | 5680 | 5680 | ||

| M3a | M3b | M4a | M4b | |

|---|---|---|---|---|

| Tobin’s Q | ROA | Tobin’s Q | ROA | |

| Variables | Coefficient | Coefficient | Coefficient | Coefficient |

| Intercept | 7.1748 *** (0.000) | −0.1025 *** (0.000) | 5.2974 *** (0.000) | 0.2026 *** (0.000) |

| SHORT | 0.2249 *** | 0.0027 *** | ||

| (0.000) | (0.000) | |||

| TREAT*SHORT | 0.4073 *** (0.000) | 0.0079 *** (0.000) | ||

| TREAT*SHORT* FO | −0.0890 *** (0.000) | −0.0087 *** (0.000) | ||

| SIR | 4.4454 *** (0.000) | 0.3605 *** (0.000) | ||

| SIR*FO | −0.3561 * (0.051) | −0.2907 *** (0.000) | ||

| SIZE | −0.2377 *** (0.000) | 0.0083 *** (0.000) | −0.1675 *** (0.000) | 0.0125 *** (0.000) |

| GROWTH | 10.3988 *** (0.000) | 0.3783 *** (0.000) | 20.9496 *** (0.000) | 0.4954 *** (0.000) |

| LEV | −0.5434 *** (0.000) | −0.1062 *** (0.000) | −1.3233 *** (0.000) | −0.1298 *** (0.000) |

| RD | 0.0166 * | 0.0121 *** | 0.0145 * | 0.0122 *** |

| (0.082) | (0.000) | (0.071) | (0.000) | |

| b-size | −0.5311 *** | −0.0062 *** | −0.5295 *** | −0.0062 *** |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| b-ind | 0.2637 *** | −0.0204 *** | 0.2629 *** | −0.0205 *** |

| (0.004) | (0.000) | (0.007) | (0.000) | |

| SOE | −0.3071 *** | −0.0128 *** | −0.3062 *** | −0.0128 *** |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| IO | −0.0188 * | −0.0138 *** | −0.0188 * | −0.0139 *** |

| (0.064) | (0.000) | (0.055) | (0.000) | |

| Firm-fixed | yes | yes | yes | yes |

| Year-fixed | yes | yes | yes | yes |

| R-square | 0.484504 | 0.284432 | 0.685413 | 0.27678 |

| Adj R-square | 0.492699 | 0.27627 | 0.692603 | 0.285283 |

| F-statistics | 4609.131 | 1776.662 | 2516.156 | 450.1694 |

| N | 22468 | 22468 | 5680 | 5680 |

| FO/Non-FO | SHORT*TREAT | SIR | |

|---|---|---|---|

| Coefficient | Coefficient | ||

| Tobin’s Q | Family-owned | 0.3183 ** | 4.0893 *** |

| Non- Family-owned | 0.4073 *** | 4.4454 *** | |

| ROA | Family-owned | −0.0008 | 0.0698 * |

| Non- Family-owned | 0.0079 *** | 0.3605 *** |

| PB | ROE | PB | ROE | |

|---|---|---|---|---|

| Variables | Coefficient | Coefficient | Coefficient | Coefficient |

| Intercept | −1.0819 (0.299) | −0.3905 *** (0.000) | 7.8102 *** (0.000) | −0.5131 *** (0.000) |

| SHORT | −0.4644 *** (0.000) | 0.0033 *** (0.000) | ||

| TREAT*SHORT | 0.1018 * (0.073) | 0.0191 *** (0.000) | ||

| TREAT*SHORT* FO | −0.1939 * (0.068) | −0.0189 *** (0.000) | ||

| SIR | 7.5322 *** (0.000) | 0.7819 *** (0.000) | ||

| SIR*FO | −2.3574 ** (0.040) | −0.6833 *** (0.000) | ||

| SIZE | 0.0458 (0.332) | 0.0203 *** (0.000) | −0.2554 *** (0.000) | 0.0270 *** (0.000) |

| GROWTH | 72.2093 *** (0.000) | 0.8964 *** (0.000) | 69.7196 *** (0.000) | 1.0069 *** (0.000) |

| LEV | 1.5528 *** (0.000) | −0.0638 *** (0.000) | 0.6751 *** (0.000) | −0.0814 *** (0.000) |

| RD | −0.7636 *** (0.001) | 0.0129 *** (0.000) | −0.7226 *** (0.001) | 0.0127 *** (0.000) |

| b-size | 1.8901 *** (0.000) | 0.0001 (0.781) | 1.7885 *** (0.000) | 0.0001 (0.769) |

| b-ind | −4.2970 *** (0.000) | −0.0066 (0.358) | −4.0660 *** (0.000) | −0.0065 (0.352) |

| SOE | 0.0639 (0.441) | −0.0086 *** (0.000) | 0.0604 (0.418) | −0.0084 *** (0.000) |

| IO | −2.0428 *** (0.000) | −0.0106 *** (0.000) | −1.9330 *** (0.000) | −0.0105 *** (0.000) |

| Firm-fixed | yes | yes | yes | yes |

| Year-fixed | yes | yes | yes | yes |

| R-square | 0.112722 | 0.112938 | 0.8386 | 0.1434 |

| Adj R-square | 0.113555 | 0.116671 | 0.8347 | 0.1450 |

| F-statistics | 610.9079 | 605.8619 | 5416.794 | 193.0208 |

| N | 22468 | 22468 | 5680 | 5680 |

| FO/Non-FO | SHORT*TREAT | SIR | |

|---|---|---|---|

| Coefficient | Coefficient | ||

| PB | Family-owned | −0.0921 * | 5.1748 *** |

| Non-Family-owned | 0.1018 * | 7.5322 *** | |

| ROE | Family-owned | 0.0002 * | 0.0819 *** |

| Non-Family-owned | 0.0191 *** | 0.0986 *** |

| Model 1 | Model 2 | Model 3 | Model4 | |

|---|---|---|---|---|

| Variables | VIF | VIF | VIF | VIF |

| SHORT | 1.923 | 1.625 | ||

| TREAT*SHORT | 2.234 | |||

| TREAT*SHORT*FO | 1.558 | |||

| SIR | 1.153 | 1.558 | ||

| SIR*FO | 1.716 | |||

| SIZE | 2.664 | 2.162 | 2.660 | 2.175 |

| GROWTH | 1.262 | 1.316 | 1.264 | 1.310 |

| LEV | 1.560 | 1.528 | 1.562 | 1.522 |

| RD | 2.143 | 2.050 | 2.145 | 2.032 |

| b-size | 1.375 | 1.285 | 1.377 | 1.286 |

| b-ind | 1.520 | 1.412 | 1.533 | 1.425 |

| SOE | 1.367 | 1.239 | 1.552 | 1.520 |

| IO | 1.423 | 1.359 | 1.436 | 1.345 |

| Mean VIF | 1.693 | 1.500 | 1.722 | 1.589 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mai, W.; Hamid, N.I.N.B.A. The Moderating Effect of Family Business Ownership on the Relationship between Short-Selling Mechanism and Firm Value for Listed Companies in China. J. Risk Financial Manag. 2021, 14, 236. https://doi.org/10.3390/jrfm14060236

Mai W, Hamid NINBA. The Moderating Effect of Family Business Ownership on the Relationship between Short-Selling Mechanism and Firm Value for Listed Companies in China. Journal of Risk and Financial Management. 2021; 14(6):236. https://doi.org/10.3390/jrfm14060236

Chicago/Turabian StyleMai, Wenzhen, and Nik Intan Norhan Binti Abdul Hamid. 2021. "The Moderating Effect of Family Business Ownership on the Relationship between Short-Selling Mechanism and Firm Value for Listed Companies in China" Journal of Risk and Financial Management 14, no. 6: 236. https://doi.org/10.3390/jrfm14060236