Predicting Gold and Silver Price Direction Using Tree-Based Classifiers

Schulich School of Business, York University, Toronto, ON M3J 1P3, Canada

J. Risk Financial Manag. 2021, 14(5), 198; https://doi.org/10.3390/jrfm14050198

Submission received: 13 April 2021

/

Revised: 26 April 2021

/

Accepted: 27 April 2021

/

Published: 29 April 2021

(This article belongs to the Special Issue Machine Learning Applications in Finance)

Abstract

:Gold is often used by investors as a hedge against inflation or adverse economic times. Consequently, it is important for investors to have accurate forecasts of gold prices. This paper uses several machine learning tree-based classifiers (bagging, stochastic gradient boosting, random forests) to predict the price direction of gold and silver exchange traded funds. Decision tree bagging, stochastic gradient boosting, and random forests predictions of gold and silver price direction are much more accurate than those obtained from logit models. For a 20-day forecast horizon, tree bagging, stochastic gradient boosting, and random forests produce accuracy rates of between 85% and 90% while logit models produce accuracy rates of between 55% and 60%. Stochastic gradient boosting accuracy is a few percentage points less than that of random forests for forecast horizons over 10 days. For those looking to forecast the direction of gold and silver prices, tree bagging and random forests offer an attractive combination of accuracy and ease of estimation. For each of gold and silver, a portfolio based on the random forests price direction forecasts outperformed a buy and hold portfolio.

1. Introduction

A principal concern for investors in financial assets is how to protect their investment portfolios from adverse movements in the market. Gold is often used by investors as a hedge against inflation or adverse economic times (Baur and Lucey 2010; Baur and McDermott 2010; Bekiros et al. 2017; Ciner et al. 2013; Hood and Malik 2013; Junttila et al. 2018; Baur and McDermott 2016; Beckmann et al. 2015; Blose 2010; Hoang et al. 2016; Reboredo 2013; Iqbal 2017; O’Connor et al. 2015; Hillier et al. 2006; Tronzano 2021; Areal et al. 2015). For example, gold prices increased during the 2008–2009 global financial crisis (GFC) and during the COVID19 pandemic. In response to the COVID19 pandemic, London morning gold prices increased 35% from USD 1523 on 31 December 2019 to USD 2049 on 6 August 2020 (ICE Benchmark Administration Limited (IBA) 2021).

Given the interest in gold as an asset it is not surprising that there are many studies that forecast the price of gold. Examples of methods used to forecast gold prices include econometrics (Shafiee and Topal 2010; Aye et al. 2015; Hassani et al. 2015; Gangopadhyay et al. 2016), artificial neural networks (Kristjanpoller and Minutolo 2015; Alameer et al. 2019; Parisi et al. 2008), boosting (Pierdzioch et al. 2015, 2016a, 2016b), random forests (Liu and Li 2017; Pierdzioch and Risse 2020), support vector machines (Risse 2019), and other machine learning methods (Yazdani-Chamzini et al. 2012; Livieris et al. 2020; Mahato and Attar 2014).

Looking first at some representative research that uses traditional econometric methods to predict gold prices, Shafiee and Topal (2010) propose a time series model for monthly gold prices that consists of a long-term reversion component, a diffusion component, and a jump component. In a forecasting comparison, this model has lower root mean squared error (RMSE) than an ARIMA model. Aye et al. (2015) use dynamic model averaging, dynamic model selection and Bayesian model averaging to forecast monthly gold prices. They find that these models outperform a random walk. They use financial variables and real economic variables as explanatory variables and find that financial variables have stronger predictive power. Using time series techniques (vector autoregression, ARIMA, ETS, TBATS) to forecast monthly gold price Hassani et al. (2015) find, however, that it is difficult to beat a random walk. In a forecasting comparison of Indian gold prices, Gangopadhyay et al. (2016) find that a vector error correction model outperforms a random walk.

Representative research that uses machine learning (ML) methods to predict gold prices includes the following. Parisi et al. (2008) use artificial neural networks (ANN) to forecast the change in weekly gold prices. Lagged gold price changes and lagged changes in the Dow Jones Index are used as explanatory variables. They find that rolling ward networks have better forecasting accuracy than either recursive ward networks or feed forward networks. Yazdani-Chamzini et al. (2012) compare the monthly gold price forecasting performance of ANN, adaptive neuro-fuzzy inference system (ANFIS), and ARIMA. They find that ANFIS outperforms the other models and the results are robust to different training and test sets. Mahato and Attar (2014) predict gold prices using ensemble methods. Using stacking and hybrid bagging they find gold and silver price accuracy of 85% and 79%, respectively. Kristjanpoller and Minutolo (2015) use ANN-GARCH models to forecast daily gold price volatility. They find that the ANN-GARCH model results in a 25% reduction in mean average prediction error over the GARCH model. Pierdzioch et al. (2015) use regression boosting to forecast monthly gold prices. They find that the explanatory variables (inflation rates, exchange rates, stock market, interest rates) have predictive power, but the trading rules generated do not beat a simple buy and hold strategy. Pierdzioch et al. (2016a) use quantile regression boosting to forecast gold prices. Trading rules generated from this approach can, in some situations (low trading costs, and specific quantiles) beat that of a buy and hold strategy. Pierdzioch et al. (2016b) use a boosting regression to forecast gold price volatility. Boosting provides better forecasts compared to an autoregressive model. Alameer et al. (2019) use monthly data to forecast the price of gold using a neural network with a whale optimization algorithm. This approach has better forecasting performance compared to several other machine learning methods (classic neural network, particle swarm neural network, and grey wolf optimization) and ARIMA models. Risse (2019) takes a novel approach and combines wavelets and support vector machine (SVM) to predict monthly gold prices. The feature space includes variables for interest rates, exchange rates, commodity prices, and stock prices. Wavelets are applied to each of these predictors in order to generate additional features for the SVM. The wavelet SVM produces more accurate gold price forecasts than other models like SVM, random forest, or boosting. Livieris et al. (2020) combine deep learning with long short-term memory (LSTM) to predict gold prices. The addition of the LSTM layers to the deep learning process provides an increase in forecasting performance. Pierdzioch and Risse (2020) use random forests to predict the returns of gold, silver, platinum, and palladium. They find that forecasts from multivariate models are more accurate than forecasts from univariate models. Plakandaras et al. (2021) combine ensemble empirical mode decomposition with SVM to predict monthly gold prices. The feature set contains interest rates and asset price variables. They use a two-step process where in the first step the data are filtered and then in the second step the filtered data are used in a SVM. Forecast accuracy is higher than that obtained from ordinary least squares or least absolute shrinkage. This literature described above shows that machine learning methods appear to offer better gold price forecasting accuracy than traditional econometric methods.

The use of ML methods to evaluate investment trading strategies is becoming more widely adopted. Here, are a few representative examples. Jiang et al. (2020) use extreme gradient boosting to predict stock prices and combine this with a risk adjusted portfolio rebalancing. They find that their approach provides better risk adjusted returns relative to a buy and hold strategy. Kim et al. (2019) use hidden Markov models to devise global asset allocation strategies. They find that the hidden Markov model produces trading strategies that outperform (in terms of risk and return measure) traditional momentum strategies. Koker and Koutmos (2020) use reinforcement learning techniques to devise trading strategies for five cryptocurrencies. Compared to a buy and hold strategy this approach yields better risk adjusted returns. Suimon et al. (2020) use the autoencoder ML approach to investigate a long and short trading strategy for Japanese government bonds. This approach has better investment performance than a trend following strategy. Vezeris et al. (2019) develop an improved Turtle trading system that they call AdTurtle which outperforms the classic Turtle trading system. Zengeler and Handmann (2020) use recurrent long short term memory networks to trade contracts for difference. Their approach outperforms the market.

The purpose of this paper is to predict gold and silver price direction using tree-based classifiers. This paper differs from the existing literature in six important ways. First, there is research showing that predicting stock price direction is more successful than predicting actual stock prices (Basak et al. 2019; Leung et al. 2000; Nyberg 2011; Nyberg and Pönkä 2016; Pönkä 2016; Ballings et al. 2015; Lohrmann and Luukka 2019; Sadorsky 2021). Unlike much of the existing literature on gold price forecasting that focusses on gold prices, this paper predicts gold price direction. Second, much of the existing literature on gold price forecasting uses macroeconomic variables for features. In the stock price forecasting literature, there is evidence that technical indicators are useful for predicting stock prices (Yin and Yang 2016; Yin et al. 2017; Neely et al. 2014; Wang et al. 2020; Bustos and Pomares-Quimbaya 2020). This paper uses technical indicators as features for predicting gold price direction. Feature selection is based on several well-known technical indicators like moving average, stochastic oscillator, rate of price change, MACD, RSI, and advance decline line (Bustos and Pomares-Quimbaya 2020). Third, this paper predicts gold and silver price direction using tree-based classifiers like random forests (RFs), bagging, and stochastic gradient boosting. Bagging, tree boosting, and RFs are based on the concept of a decision tree (James et al. 2013; Hastie et al. 2009) and often provide a good balance between ease of estimation and accuracy. While there is research on using these methods to predict gold prices, there is little known about how useful these methods are for forecasting gold price direction. Fourth, gold and silver prices are measured using exchange traded funds (ETFs). ETFs are convenient for investors who want to participate in commodity markets but do not want to deal with the intricacies of owning a futures account. Fifth, directional stock price forecasts are constructed from one day to twenty days in the future. A five day forecast horizon corresponds to one week of trading days, a 10 day forecast horizon corresponds to two weeks of trading days and a twenty day forecast horizon corresponds to approximately one month of trading days. Forecasting stock price direction over a multi-day horizon provides more information on how prediction accuracy changes across the forecast period. Sixth, the practical significance of these results is further investigated using a portfolio investment comparison.

The analysis from this research provides some interesting results. At all forecast horizons, RFs and tree bagging show much better gold and silver ETF price prediction accuracy then logit. The prediction accuracy from bagging and RFs is very similar indicating that either method is very useful for predicting the price direction of gold and silver ETFs. The prediction accuracy for RF and tree bagging models is over 85% for forecast horizons of 10 days or more. Stochastic gradient boosting accuracy is a few percentage points less than that of random forests for forecast horizons over 10 days. For a 20-day forecast horizon, tree bagging, stochastic gradient boosting, and random forests have accuracy rates of between 85% and 90% while logit models have accuracy rates of between 55% and 60%. For each of gold and silver, an investment portfolio based on the random forests price direction forecasts outperforms a buy and hold portfolio.

This paper is organized as follows. The next section sets out the methods and data. This is followed by the results. The last section of the paper provides some conclusions and suggestions for future research.

2. Methods and Data

2.1. The Logit Method for Prediction

The direction of stock price changes can be classified as either up (stock price change from one period to the next is positive) or down (stock price change from one period to the next is non-positive). A standard classification problem like this where the variable of interest can take on only one of two values (up or down) is easily coded as a binary variable. Logit models are one widely used approach to modelling and forecasting binary variables and logit models can be used to predict the direction of stock prices. Explanatory variables considered pertinent to predicting stock price direction can be used as features. Logit models are easy to estimate and widely used to predict binary classification outcomes (James et al. 2013).

yt+h = α + βXt + εt,

In Equation (1), yt+h = pt+h – pt is a binary variable that takes on the value of “up” if positive or “down” if non-positive and X is a vector of features. The variable pt represents the adjusted closing stock price on day t. The random error term is ε. The symbol h denotes the forecast horizon, h = 1, 2, 3, …, 20, and indicates the number of time periods into the future to predict. A multistep forecast horizon is used in order to see how forecast accuracy changes across the forecast horizon. A 5-day forecast corresponds to one week of trading data, a 10 day forecast corresponds to two weeks of trading data, and a 20 day forecast is consistent with the average number of trading days in a month. The features used in the analysis include familiar technical indicators like the relative strength indicator (RSI), stochastic oscillator (slow, fast), advance–decline line (ADX), moving average cross-over divergence (MACD), price rate of change (ROC), on balance volume (OBV), the 50-day moving average, 200-day moving average, money flow index (MFI), and Williams accumulation and distribution (WAD). The technical indicators used in this paper are widely used in academics and practice (Yin and Yang 2016; Yin et al. 2017; Neely et al. 2014; Wang et al. 2020; Bustos and Pomares-Quimbaya 2020). Achelis (2013) provides a detailed description of the calculation of these technical indicators.

2.2. Decision Trees and Bagging for Prediction

Logit regression classifies the dependent (response) variable using a linear boundary and this can be restrictive in circumstances where there is a nonlinear relationship between the response and the features. Decision trees are better able to capture the classification between the response and the features in nonlinear situations by bisecting the predictor space into smaller and smaller non-overlapping regions. The rules used to split the predictor space can be summarized in a tree diagram, and this approach is known as a decision tree method. Tree-based methods are easy to interpret but are not as competitive with other methods like bagging, boosting or random forests. The main ideas behind decision trees, bagging, boosting, and random forest methods is presented in the following paragraphs and a more complete treatment of these topics can be found in James et al. (2013) and Hastie et al. (2009).

A qualitative response can be predicted using a classification tree. A classification tree predicts that each observation belongs to the most commonly occurring class of training observations in the region to which it belongs. A majority voting rule is used for classification. The basic steps in building a classification tree can be described as follows.

1. The predictor space (for all possible values of X1, …, XP) is divided into J distinctive and non-overlapping regions, R1, …, RJ.

2. For every observation that falls into the region Rj, the same prediction is made. This prediction is that each observation belongs to the most commonly occurring class of training observations to which it belongs.

The construction of the regions R1, …, RJ proceeds as follows. The tree is grown using recursive binary splitting and the splitting rules are determined by a classification error rate. The classification error rate, E, is the fraction of training observations in a region that do not belong to the most common class.

In Equation (2), is the proportion of training observations in the mth region that are from the kth class. Splits can be classified using a Gini index. The Gini index (G) is defined as follows.

The total variance across the K classes can be measured using the Gini index. In this paper

K = 2 because there are only two classes (stock price direction positive or, not positive). For small values of the Gini index takes on a small value. For this reason, G is often referred to as a measure of node impurity since a small G value shows that a node mostly contains observations from a single class. The root node at the top of a decision tree can be found by trying every possible split of the predictor space and choosing the split that reduces the impurity as much as possible (has the highest gain in the Gini index). Successive nodes can be found using the same process and this is how recursive binary splitting is evaluated.

The entropy (D) is another way to classify splits. The entropy is defined as follows.

The entropy (D), like the Gini index, will take on small values if the mth node is pure. The Gini index and entropy produce numerically similar values. The classification error is not very sensitive to the growing of trees so in practice either the Gini index or entropy is used to classify splits. The analysis in this paper uses the entropy measure.

The process of building a decision tree typically results in a very deep and complex tree that may produce good predictions on the training data set but is likely to over fit the data leading to poor performance on unseen data. Decision trees suffer from high variance which means that if the training data set is split into two parts at random and a decision tree fit to both parts, the outcome would be very different. Bagging is one approach to addressing the problem of high variance. Bootstrap aggregation, or bagging as it is commonly referred to, is a statistical technique used to reduce the variance of a machine learning method. The idea behind bagging is to take many training sets, build a decision tree on each training data set, and average the predictions to obtain a single low-variance machine learning model (James et al. 2013). Since the researcher does not have access to many training data sets bootstrap replication is used to create many copies of the original training data set and a decision tree fit to each copy. Averaging the predictions from bootstrap trees reduces variance, even though each tree is grown deep and has high variance.

2.3. The Random Forests Method for Prediction

Random forests are an improvement over bagging trees by introducing decorrelation between the trees (Breiman 2001). As in the case of bagging, a large number of decision trees are built on bootstrapped training samples. Each time a split in a tree occurs a random sample of predictors is chosen as split candidates from the full set of predictors. The number of predictors chosen at random is calculated as the floor of the square root of the total number of predictors (James et al. 2013). While the choice of randomly choosing predictors may seem unusual, averaging results from non-correlated trees is more effective for reducing variance than averaging trees that are highly correlated.

2.4. The Stochastic Gradient Boosting Method for Prediction

Boosting is another way to improve the prediction accuracy of decision trees (James et al. 2013; Hastie et al. 2009). With boosting, trees are grown sequentially, and each tree is grown using information from previously grown trees. More specifically, the newly added decision tree fits the residuals from the current decision tree. The final model aggregates the results (predicted values) from each step in the sequence. Each tree is a weak learner but adding many trees together with each tree modelling the errors from the previous tree can produce a very accurate overall model. Unlike bagging, boosting does not use bootstrap sampling and instead each tree is fit to a modified version of the original tree (Friedman 2001). When adding trees, a gradient descent technique is used to minimize the loss function and this is referred to as gradient boosting. Boosting has tuning parameters for the number of trees, the shrinkage (learning rate) parameter, the number of splits in each tree, and the minimum number of observations in each node. Stochastic gradient boosting is an improvement over gradient boosting because boosting has a tendency to overfit the data. At the construction of each tree a subsample of the training data drawn at random without replacement is used to fit the base learner. Stochastic gradient boosting is used in this paper.

2.5. Model Setup

This paper compares the performance of logit, bagging decision tree, stochastic gradient boosting, and random forests for predicting the price direction of gold and silver ETFs. For the analysis, 80% of the data was used for training and 20% used for testing. The logit model uses all the features in predicting price direction. The bagging decision tree model was estimated with 500 trees. The random forests were estimated with 500 trees and 3 (the floor of the square root of the number of features, 13) randomly chosen predictors at each split. The results are not sensitive to the number of trees provided a large enough number of trees are chosen. A very large number of trees does not lead to overfitting, but a small number of trees results in high test error. In conducting sensitivity analysis, training control for the random forest and boosting was handled with 10-fold cross validation with 10 repeats. Stochastic gradient boosting was conducted with 3000 trees, shrinkage equal to 0.20, an interaction depth of 8, and the minimum number of observations in each node set to 10. The bag fraction was set at 0.5. Sensitivity analysis showed that these parameter settings worked well for most forecast horizons. Since boosting has more tuning parameters than random forests, finding optimal tuning parameter values for each forecast horizon can be time consuming.

Forecasting accuracy is evaluated using several measures obtained from the confusion matrix. Accuracy is the number of true positives and true negatives divided by the total number of predictions. The kappa statistic adjusts accuracy by accounting for the possibility of a correct prediction just by chance. The positive predictive value measures the proportion of positive predictions that were correctly classified as positive (true positives divided by the sum of true positives and false positives). The negative predictive value measures the proportion of negative predictions that were correctly classified (true negatives divided by the sum of true negatives and false negatives). All calculations were done in R (R Core Team 2019) using the random forests machine learning package (Breiman et al. 2018), the generalized boosted models package (Greenwell et al. 2020) and the caret package (Kuhn et al. 2020).

2.6. The Data

The data for this study consists of the prices of two popular, US listed, and widely traded commodity ETFs. The SPDR Gold Shares (GLD) ETF, with an inception date of 18 November 2004, is the most widely traded gold ETF. The GLD ETF is structured as a trust and holds a specific number of gold bars for each share of the ETF issued. Since GLD holds physical gold, its share price moves in tandem with the price of gold. GLD shares were worth one-tenth of the price of gold at inception but this value has eroded over time because the fund charges a 0.4% annual fee. GLD is an attractive investment for those who seek exposure to gold but do not want to trade in the commodity market. Silver prices are measured using the SLV silver trust ETF. SLV consists mostly of silver held by JPMorgan and a small amount of cash. Like GLD, SLV is passively managed and the price of SLV closely tracks that of silver. SLV began trading on 21 April 2006. Like GLD, SLV is a convenient low-cost alternative to investing in the silver futures market.

The daily data set for this study, consisting of 3714 observations, starts on 1 May 2006 and ends on 29 January 2021. The data was collected from Yahoo Finance. Several well-known technical indicators like the relative strength indicator (RSI), stochastic oscillator (slow, fast), advance–decline line (ADX), moving average cross-over divergence (MACD), price rate of change (ROC), on balance volume, money flow index (MFI), Williams accumulation and distribution (WAD), and the 50-day and 200-day moving averages, calculated from daily data, are used as features in the prediction models. The number of observations used to estimate the models varies and depends upon the calculation of the technical indicators (200 days are omitted due to the calculation of the 200-day moving average) and forecast periods (between 1 and 20 observations are omitted depending upon the forecast horizon). For a 20-day forecast horizon, there are 3475 observations. The training data set consists of 2780 observations (80% of the data) and the testing data set contains 695 observations (20% of the data).

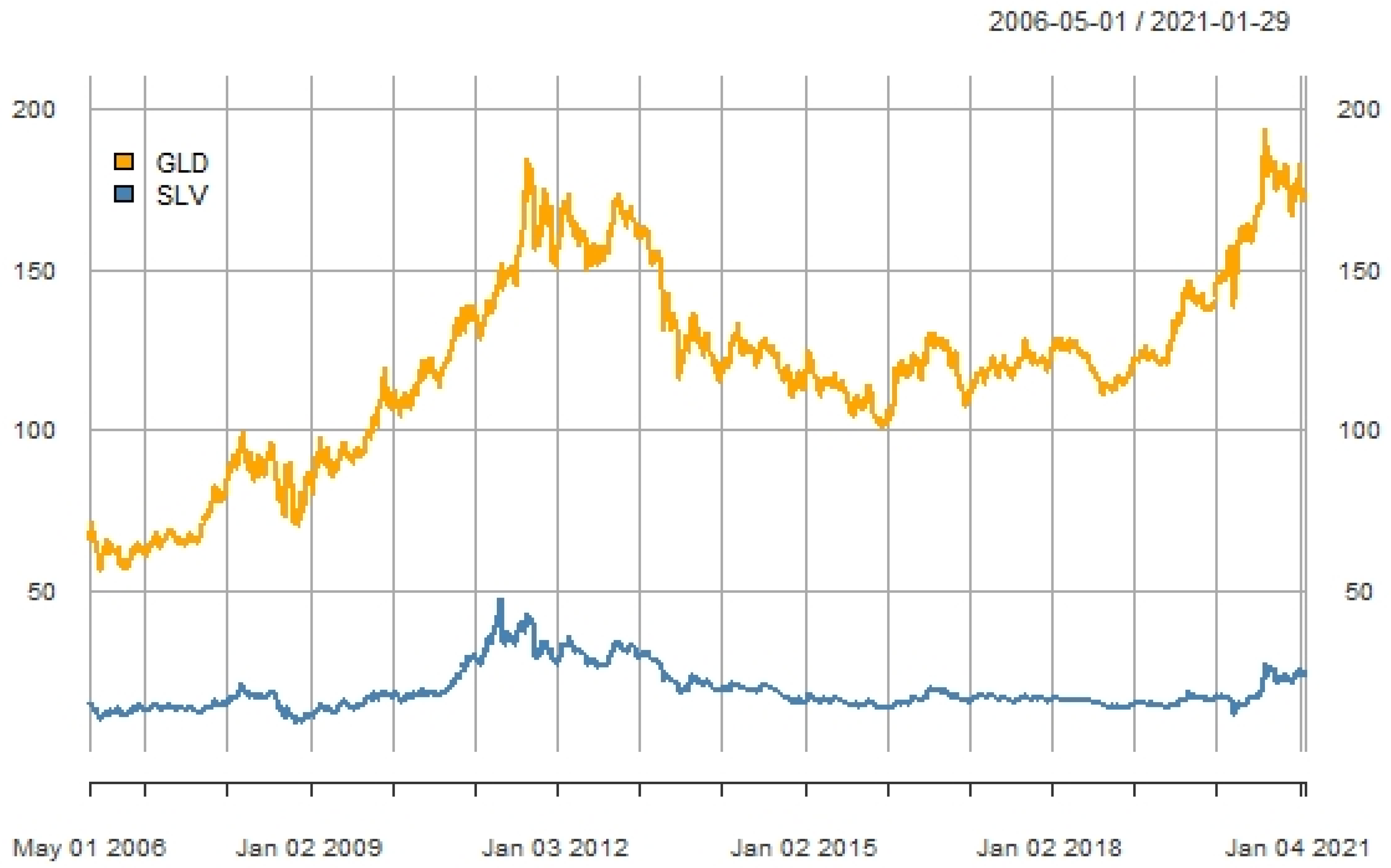

The time series pattern of GLD and SLV shows that the ETFs move together (Figure 1). There are two noticeable peaks in Figure 1. GLD and SLV reached high prices in August of 2011 partially due to debt issues in Europe and the United States and related concerns of inflation but also because real interest rates turned negative. In late 2020, GLD surpassed the 2011 peak as the COVID19 pandemic continued. SLV prices increased in 2020 but not by enough to match the previous high set in 2011. Notice that the price of GLD has risen sharply since the onset of the World Health Organization’s declaration of the COVID19 global pandemic (March 2020) which is consistent with gold being used as a hedge in adverse times.

The histograms for the percentage of up days by forecast horizon shows little variation for GLD or SLV (Figure 2). The percentage of up days for GLD never gets higher than 55% while the percentage of up days for SLV never gets higher than 53%.

Descriptive statistics for continuously compounded daily returns show that GLD has a daily average return of 0.026% while SLV has a daily average return of 0.016% (Table 1). The coefficient of variation indicates that SLV is more variable. As is common with financial assets, GLD and SLV each have large kurtosis and non-normally distributed returns.

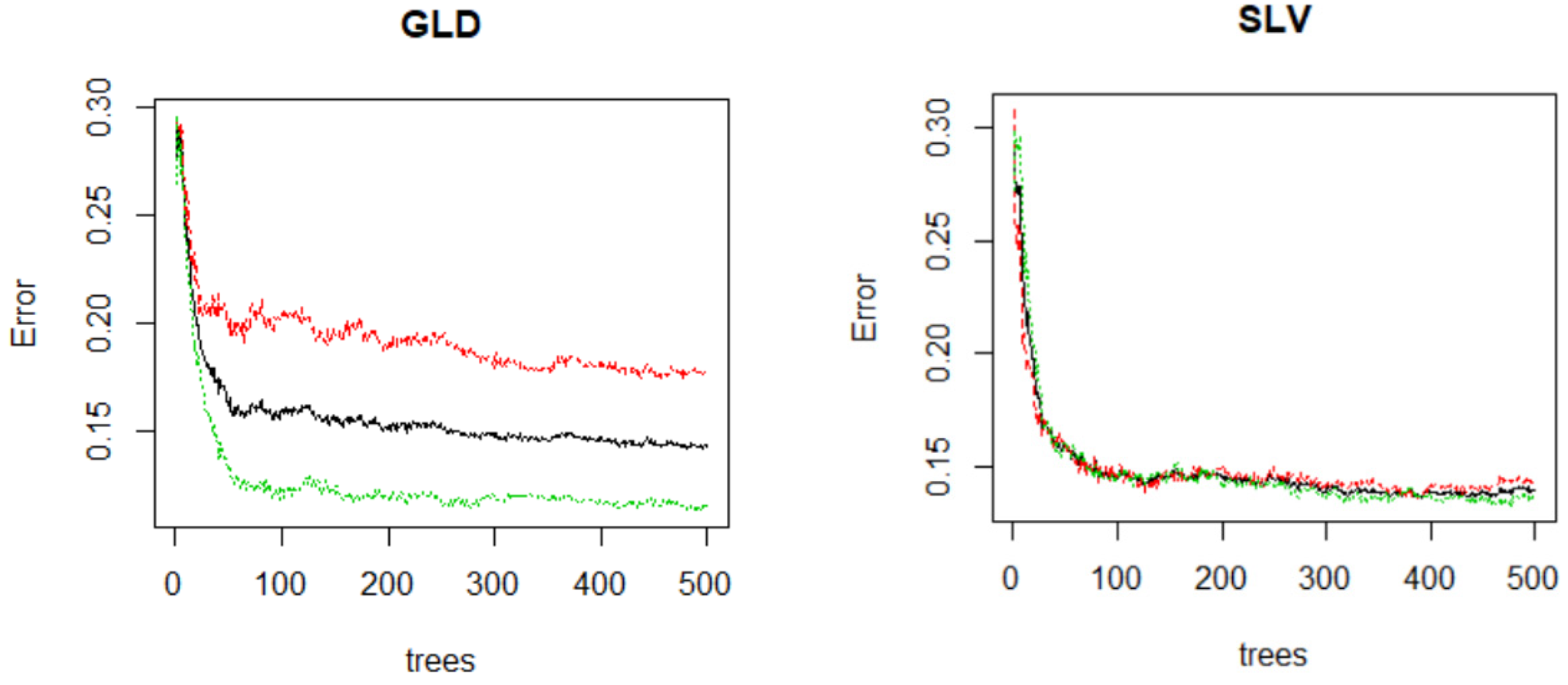

In order to investigate the impact of the number of trees on the random forests model, Figure 3 shows how the test error relates to the number of trees. The analysis is conducted for a 10-step forecast horizon where 80% of the data are used for training and 20% of the data are used for testing. For each ETF, the test error declines rapidly as the number of trees increases from one to 100. After 400 trees there is very small reduction in the test error. In Figure 3, out of bag (OOB) test error is reported along with test error for the up and down classification. The results for other forecast horizons are similar to those reported here. Consequently, 500 trees are used in estimating the RFs.

3. Results

This section reports the results from predicting price direction for gold and silver ETFs. Since this is a classification problem, the prediction accuracy is one of the most widely used measures of forecast performance. Prediction accuracy is a proportion of the number of true positives and true negatives divided by the total number of predictions. This measure can be obtained from the confusion matrix. Prediction accuracy ranges between 0 and 1 with higher values indicating greater accuracy. Other useful forecast accuracy measures like kappa and how well the models predict the up or down classification are also available and are reported since it is interesting to see if the forecast accuracy for predicting the up class is similar or different to that of predicting the down class.

Price direction prediction accuracy for GLD (Figure 4) shows large differences between the logit model and the tree-based classifiers (RF, Tree bag and Tree boost). The prediction accuracy for logit show that while there is some improvement in accuracy between 1 and 20 days ahead, the prediction accuracy never gets above 0.6 (60%). The prediction accuracy of the RFs and tree bagging methods show considerable improvement in accuracy between 1 day and 10 days. Prediction accuracy for predicting GLD price direction 10 days into the future is over 85%. There is little variation in RF and tree bagging prediction accuracy for predicting price direction between 10 and 20 days into the future and some accuracy measures are close to 90%. Notice that the prediction accuracy between tree bagging and RF is very similar. For predicting 15 to 20 days in the future, the RF, bagged, and boosting models have very similar accuracy. Overall, the RF has the highest accuracy for each of the forecast periods although for longer dated forecasts (over 10 days) the difference in accuracy between RF and bagged or boosting is between 1% and 3%.

The patterns of prediction accuracy for the SLV ETF (Figure 5) is very similar to that which was described for the GLD ETF. RF and tree bagging have the highest accuracy while logit has the lowest accuracy. Tree boosting accuracy is similar to RF and bagging for predicting 15 days to 20 days.

Figure 6 and Figure 7 show kappa accuracy values for predicting GLD and SLV price direction. For GLD the pattern of kappa values in Figure 6 is very similar to the pattern of accuracy values reported in Figure 4. RF and tree bagging have the highest kappa values while logit has the lowest. It is also the case that for SLV, RF and tree bagging have the highest kappa values while logit has the lowest.

In order to determine which variables are most important in the RFs method, variable importance measures are provided. Variable importance is ascertained by using the mean decrease in accuracy (MD accuracy) and the mean decrease in Gini (MD Gini). The OOB data are used to conduct the analysis. For each of GLD and SLV at a 10-period forecast horizon, MA200, MA50, and WAD are the three most important features in classifying gold and silver price direction because they have the largest values of MD accuracy and MD Gini (Table 2). In additional analysis MA200, MA50, and WAD are also important features in classifying gold and silver price direction for other forecast horizons.

The accuracy values shown in Figure 4 and Figure 5 show the overall prediction accuracy. It is also of interest to see how the prediction accuracy compares between positive prediction values and negative prediction values. Positive predictive value is the proportion of predicted positive cases that are actually positive. In other words, when a model predicts a positive case, how often is it correct? Negative predictive value is the proportion of predicted negative cases that are actually negative.

The positive prediction values for GLD are shown in Figure 8. The RFs and tree bagging methods show the highest accuracy across most of the forecast horizons. Tree boosting accuracy is also high. After just 5 days, the RFs and tree bagging methods have an accuracy of over 80%. Notice that the logit accuracy never reaches higher than 65%. The pattern of positive predictive value for the SLV ETF (Figure 9) is similar to that which is observed for SLV. For each ETF, after 10 days the positive predictive values for RFs and bagging are above 0.80 and in most cases above 0.85.

Figure 10 shows the negative predictive values for GLD. As in the case of the positive predictive values for GLD, RFs and tree bagging provide the most accurate negative predictive values. Tree boosting is slightly less accurate than RFs and tree bagging. The logit model has the lowest accuracy. Between 1 and 5 days, accuracy increases from 0.5 to 0.8 for the RFs and tree bagging models. After 10 days, negative predictive values for RFs and tree boosting varies between 0.85 and 0.90. The pattern of negative predictive value for SLV (Figure 11) is similar to what is observed for GLD (Figure 10). For each of GLD and SLV, after 10 days the negative predictive values for RFs and bagging are above 0.80 and in most cases above 0.85.

One concern about predicting stock price direction is that the usual machine learning approach of randomly splitting the data set into training and testing parts may not be representative of time series forecasting in practice. The question arises as to how to deal with serial correlation. Bergmeir et al. (2018) show that in autoregressive models k-fold cross validation is possible so long as the errors are uncorrelated. In the approach taken in this paper, the forecast variable is gold or silver ETF price direction (which is a classification rather than regression) and the features are technical indicators, some of which (like the MA200) embody a lot of past information on stock prices that helps to mitigate the residual serial correlation. To investigate this issue further, a time series cross validation analysis is conducted where the first 80% of the data are used to fit a RF model to GLD and SLV and price direction predictions are made. Then, the estimation sample is increased by one observation and the model re-fit and a new set of forecasts produced. This recursive approach is used until the end of the data set is reached. This approach is time consuming because the model is re-fit each time a prediction is made but representative of what an investor actually does in practice. The results from undertaking this analysis are presented in Table 3 for a 10- and 20-day GLD and SLV price direction prediction period. The accuracy values obtained from this approach are referred to as time series cross validation (tsCV).

In comparing CV (the approach of randomly selecting 80% of the data for training and 20% for testing) with tsCV for predicting GLD price direction over ten days using RFs, CV accuracy is 0.8698 while tsCV accuracy is 0.8061 (Table 3). In the case of a 20 day prediction for GLD, CV accuracy is 0.8906 and tsCV accuracy is 0.8609. These tsCV accuracy values are lower (by about 3% to 7%) than the CV values but not by much. This pattern where tsCV values are slightly less than their corresponding CV values is observed throughout Table 3. For each accuracy measure, the tsCV values are slightly less than their corresponding CV values but not enough to diminish the impressive accuracy of the RF model in predicting stock price direction. Similar results are observed for SLV.

In order to provide further practical information on the usefulness of using random forests to predict gold and silver price direction, a comparison was made between a buy and hold portfolio and a switching portfolio that followed a trading strategy based on the random forest 20 period price direction forecasts. If the predicted GLD price direction over the next 20 days was up, then the portfolio was invested in GLD. If the predicted GLD price direction over the next 20 days was down, then the portfolio was invested in 3-month US T bills. The chosen portfolio is held for 20 days after which time a new investment decision was made based on the random forests prediction of GLD price direction. Over the test period (2 March 2018 to 9 November 2020), the buy and hold portfolio generated annualized returns, standard deviation, Sharpe ratio, and Omega ratio values of 12.51%, 14.52%, 0.79, and 1.17, respectively. By comparison, the switching portfolio generated annualized returns, standard deviation, Sharpe ratio, and Omega ratio values of 18.56%, 9.53%, 1.84, and 1.67, respectively. The switching portfolio has a higher Sharpe ratio and Omega ratio indicating better risk and return tradeoffs as compared to a buy and hold portfolio. It was also the case that for SLV, the switching portfolio has a higher Sharpe ratio and Omega ratio. Over the test period, the buy and hold SLV portfolio generated annualized returns, standard deviation, Sharpe ratio, and Omega ratio values of 13.57%, 29.69%, 0.42, and 1.10, respectively. In comparison, the switching portfolio generated annualized returns, standard deviation, Sharpe ratio, and Omega ratio values of 35.31%, 20.01%, 1.70, and 1.66, respectively. Trading costs were not considered in the portfolio comparisons, but this is not likely a concern because many discount brokers allow ETF trades at zero or very low (a few basis points) cost. Equity curves are shown in Figure 12 and Figure 13. Both figures show that the random forests switching portfolio avoids some large drawdowns.

To summarize, the main take-away from this research is that RFs and tree bagging provide much better price direction predicting accuracy then logit. The prediction accuracy between bagging and RFs is very similar indicating that either method is very useful for predicting the price direction of gold and silver ETFs. The GLD and SLV price direction prediction accuracy for RF and tree bagging models is over 80% for forecast horizons of 10 days or more. The positive predictive values and negative predictive values are similar indicating that there is little asymmetry between the up and down prediction classifications. The prediction accuracy from tree boosting is much higher than that of the logit but slightly lower than that of RF or tree bagging. The prediction accuracy from random forests, bagging, and boosting, is very similar for forecast horizons greater than 12 days. Boosting accuracy could be improved by using a more refined tuning grid for each of the 20 forecast horizons and the two assets but this would involve a tradeoff with respect to increased computational time since boosting has more tuning parameters than random forests or bagging and a total of 40 boosted models would need to be trained.

The results in this paper are supportive of the research that shows that predicting stock price direction can be achieved with high accuracy (Basak et al. 2019; Leung et al. 2000; Nyberg 2011; Nyberg and Pönkä 2016; Pönkä 2016; Ballings et al. 2015; Lohrmann and Luukka 2019; Sadorsky 2021). Furthermore, the predictive gold price direction accuracy found in this paper adds to the literature showing the usefulness of using machine learning methods to predict gold price direction. The gold price direction prediction accuracy greater than 85% for forecast horizons of 10 to 20 days found in this paper is comparable to other studies. In predicting one step-ahead weekly gold price changes Parisi et al. (2008) find that ANN has an accuracy of 61%. Using stacking and hybrid bagging Mahato and Attar (2014) find one day-ahead gold and silver price accuracy of 85% and 79%, respectively. Unlike Pierdzioch et al. (2015) and Pierdzioch et al. (2016a) who find that gold price trading signals generated from regression boosting offer little to no improvement over a buy and hold strategy, the results of this present paper indicate a trading strategy based on RFs offers a substantial improvement over a buy and hold strategy.

4. Discussion and Summary

During turbulent economic times or when there is high inflation, investors often use gold to hedge their investment portfolios. Consequently, it is important for investors to have accurate forecasts of gold prices. Much of the existing literature on forecasting gold prices finds that machine learning methods have higher accuracy than econometric methods. This paper contributes to the literature by comparing the gold and silver price direction prediction accuracy of several tree-based classifiers. More specifically, RFs, decision tree bagging, and tree (stochastic gradient) boosting are used to predict gold and silver ETF price direction over a 20 period forecast horizon. The feature space consists of 13 widely used technical indicators.

The analysis from this paper yields several important findings. First, RFs and tree bagging show much better gold and silver price direction prediction accuracy then logit models. Stochastic gradient boosted models have higher accuracy than logit but not as high as RFs or tree bagged models. Bagging and RFs produce very similar prediction accuracy demonstrating that either method is very useful for predicting the price direction of gold and silver ETFs. RFs stochastic gradient boosting, and tree bagging methods produce forecast accuracy over 80% for forecast horizons of 10 days or more. For a 20-day forecast horizon, tree bagging stochastic gradient boosting, and random forests methods produce accuracy rates of between 85% and 90%. By comparison, logit models have accuracy rates of between 55% and 60%. These results are in agreement with other research that shows boosting (Pierdzioch et al. 2015, 2016a, 2016b) and random forests (Liu and Li 2017; Pierdzioch and Risse 2020) to have high accuracy for predicting gold prices. Second, the positive predictive values and negative predictive values indicate that there is little asymmetry between the up and down prediction classifications for gold and silver ETFs. This result is robust to the prediction method used. Third, tree bagging and random forests offer an attractive combination of accuracy and ease of estimation, for those looking to forecast the direction of gold and silver prices. Fourth, for each of GLD and SLV, a switching portfolio that uses the 20 period ahead price direction forecasts from a random forests model has better risk adjusted returns (a higher Sharpe ratio and Omega ratio) than that of a buy and hold portfolio.

Future research could expand the set of predictors. This paper used a set of well known technical indicators for features. The feature space could be expanded to include additional technical indicators or even macroeconomic variables. Whereas most of the previous literature uses macroeconomic variables as features to predict gold prices and this paper uses technical indicators, it may be interesting to do a comparison to see which group of variables (macroeconomic or technical indicators) is most important in predicting gold prices.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data are publicly available.

Acknowledgments

I thank the anonymous reviewers for their helpful comments. I thank the Schulich School of Business for internal financial support.

Conflicts of Interest

The author declares no conflict of interest.

Abbreviations

| ADX | Advance–decline line |

| ANN | Artificial neural network |

| ANFIS | Adaptive neuro-fuzzy inference system |

| ARIMA | Autoregressive integrated moving average |

| CV | Cross validation |

| ETF | Exchange traded fund |

| ETS | Error, trend, seasonality |

| GARCH | Generalized autoregressive conditional heteroskedasticity |

| GLD | Gold shares ETF |

| Logit | Logit regression |

| LSTM | Long short-term memory |

| MA50 | Moving average of length 50 |

| MA200 | Moving average of length 200 |

| MACD | Moving average cross-over divergence |

| MFI | Money flow index |

| ML | Machine Learning |

| OBV | On balance volume |

| OOB | Out of bag error |

| RF | Random Forest |

| ROC | Price rate of change |

| RSI | Relative strength indicator |

| SLV | Silver shares ETF |

| SVM | Support vector machine |

| TBATS | Exponential smoothing state space model with Box-Cox transformation, ARMA errors, trend and seasonal components |

| Tree bag | Decision tree bagging |

| Tree boost | Decision tree boosting (Stochastic gradient boosting) |

| tsCV | Time series cross validation |

| WAD | Williams accumulation and distribution |

References

- Achelis, Steven B. 2013. Technical Analysis from A to Z, 2nd ed. New York: McGraw-Hill Education. [Google Scholar]

- Alameer, Zakaria, Mohamed Abd Elaziz, Ahmed A. Ewees, Haiwang Ye, and Zhang Jianhua. 2019. Forecasting Gold Price Fluctuations Using Improved Multilayer Perceptron Neural Network and Whale Optimization Algorithm. Resources Policy 61: 250–60. [Google Scholar] [CrossRef]

- Areal, Nelson, Benilde Oliveira, and Raquel Sampaio. 2015. When Times Get Tough, Gold Is Golden. The European Journal of Finance 21: 507–26. [Google Scholar] [CrossRef]

- Aye, Goodness, Rangan Gupta, Shawkat Hammoudeh, and Won Joong Kim. 2015. Forecasting the Price of Gold Using Dynamic Model Averaging. International Review of Financial Analysis 41: 257–66. [Google Scholar] [CrossRef] [Green Version]

- Ballings, Michel, Dirk Van den Poel, Nathalie Hespeels, and Ruben Gryp. 2015. Evaluating Multiple Classifiers for Stock Price Direction Prediction. Expert Systems with Applications 42: 7046–56. [Google Scholar] [CrossRef]

- Basak, Suryoday, Saibal Kar, Snehanshu Saha, Luckyson Khaidem, and Sudeepa Roy Dey. 2019. Predicting the Direction of Stock Market Prices Using Tree-Based Classifiers. The North American Journal of Economics and Finance 47: 552–67. [Google Scholar] [CrossRef]

- Baur, Dirk G., and Brian M. Lucey. 2010. Is Gold a Hedge or a Safe Haven? An Analysis of Stocks, Bonds and Gold. Financial Review 45: 217–29. [Google Scholar] [CrossRef]

- Baur, Dirk G., and Thomas K. McDermott. 2010. Is Gold a Safe Haven? International Evidence. Journal of Banking & Finance 34: 1886–98. [Google Scholar] [CrossRef]

- Baur, Dirk G., and Thomas K. J. McDermott. 2016. Why Is Gold a Safe Haven? Journal of Behavioral and Experimental Finance 1: 63–71. [Google Scholar] [CrossRef]

- Beckmann, Joscha, Theo Berger, and Robert Czudaj. 2015. Does Gold Act as a Hedge or a Safe Haven for Stocks? A Smooth Transition Approach. Economic Modelling 48: 16–24. [Google Scholar] [CrossRef] [Green Version]

- Bekiros, Stelios, Sabri Boubaker, Duc Khuong Nguyen, and Gazi Salah Uddin. 2017. Black Swan Events and Safe Havens: The Role of Gold in Globally Integrated Emerging Markets. Journal of International Money and Finance 73: 317–34. [Google Scholar] [CrossRef] [Green Version]

- Bergmeir, Christoph, Rob J. Hyndman, and Bonsoo Koo. 2018. A Note on the Validity of Cross-Validation for Evaluating Autoregressive Time Series Prediction. Computational Statistics & Data Analysis 120: 70–83. [Google Scholar] [CrossRef]

- Blose, Laurence E. 2010. Gold Prices, Cost of Carry, and Expected Inflation. Journal of Economics and Business 62: 35–47. [Google Scholar] [CrossRef]

- Breiman, Leo. 2001. Random Forests. Machine Learning 45: 5–32. [Google Scholar] [CrossRef] [Green Version]

- Breiman, Leo, Adele Cutler, Andy Liaw, and Matthew Wiener. 2018. RandomForest: Breiman and Cutler’s Random Forests for Classification and Regression. R Package Version 4.6-14. (version 4.6-14). Available online: https://www.stat.berkeley.edu/~breiman/RandomForests/ (accessed on 30 March 2021).

- Bustos, O, and A. Pomares-Quimbaya. 2020. Stock Market Movement Forecast: A Systematic Review. Expert Systems with Applications 156: 113464. [Google Scholar] [CrossRef]

- Ciner, Cetin, Constantin Gurdgiev, and Brian M. Lucey. 2013. Hedges and Safe Havens: An Examination of Stocks, Bonds, Gold, Oil and Exchange Rates. International Review of Financial Analysis 29: 202–11. [Google Scholar] [CrossRef]

- Friedman, Jerome H. 2001. Greedy Function Approximation: A Gradient Boosting Machine. The Annals of Statistics 29: 1189–232. [Google Scholar] [CrossRef]

- Gangopadhyay, Kausik, Abhishek Jangir, and Rudra Sensarma. 2016. Forecasting the Price of Gold: An Error Correction Approach. IIMB Management Review 28: 6–12. [Google Scholar] [CrossRef] [Green Version]

- Greenwell, Brandon, Bradley Boehmke, Jay Cunningham, and G. B. M. Developers. 2020. Gbm: Generalized Boosted Regression Models (version 2.1.8). Available online: https://CRAN.R-project.org/package=gbm (accessed on 30 March 2021).

- Hassani, Hossein, Emmanuel Sirimal Silva, Rangan Gupta, and Mawuli K. Segnon. 2015. Forecasting the Price of Gold. Applied Economics 47: 4141–52. [Google Scholar] [CrossRef]

- Hastie, Trevor, Robert Tibshirani, and Jerome Friedman. 2009. The Elements of Statistical Learning: Data Mining, Inference, and Prediction, 2nd ed. Springer Series in Statistics; New York: Springer. [Google Scholar] [CrossRef]

- Hillier, David, Paul Draper, and Robert Faff. 2006. Do Precious Metals Shine? An Investment Perspective. Financial Analysts Journal 62: 98–106. [Google Scholar] [CrossRef]

- Hoang, Thi Hong Van, Amine Lahiani, and David Heller. 2016. Is Gold a Hedge against Inflation? New Evidence from a Nonlinear ARDL Approach. Economic Modelling 54: 54–66. [Google Scholar] [CrossRef] [PubMed]

- Hood, Matthew, and Farooq Malik. 2013. Is Gold the Best Hedge and a Safe Haven under Changing Stock Market Volatility? Review of Financial Economics 22: 47–52. [Google Scholar] [CrossRef]

- ICE Benchmark Administration Limited (IBA). 2021. Gold Fixing Price 10:30 a.m. (London Time) in London Bullion Market, Based in U.S. Dollars. FRED, Federal Reserve Bank of St. Louis. FRED, Federal Reserve Bank of St. Louis. 1 April 2021. Available online: https://fred.stlouisfed.org/series/GOLDAMGBD228NLBM (accessed on 30 March 2021).

- Iqbal, Javed. 2017. Does Gold Hedge Stock Market, Inflation and Exchange Rate Risks? An Econometric Investigation. International Review of Economics & Finance 48: 1–17. [Google Scholar] [CrossRef]

- James, Gareth, Daniela Witten, Trevor Hastie, and Robert Tibshirani. 2013. An Introduction to Statistical Learning: With Applications in R. Springer Texts in Statistics. New York: Springer. [Google Scholar] [CrossRef]

- Jiang, Zhenlong, Ran Ji, and Kuo-Chu Chang. 2020. A Machine Learning Integrated Portfolio Rebalance Framework with Risk-Aversion Adjustment. Journal of Risk and Financial Management 13: 155. [Google Scholar] [CrossRef]

- Junttila, Juha, Juho Pesonen, and Juhani Raatikainen. 2018. Commodity Market Based Hedging against Stock Market Risk in Times of Financial Crisis: The Case of Crude Oil and Gold. Journal of International Financial Markets, Institutions and Money 56: 255–80. [Google Scholar] [CrossRef]

- Kim, Eun-chong, Han-wook Jeong, and Nak-young Lee. 2019. Global Asset Allocation Strategy Using a Hidden Markov Model. Journal of Risk and Financial Management 12: 168. [Google Scholar] [CrossRef] [Green Version]

- Koker, Thomas E., and Dimitrios Koutmos. 2020. Cryptocurrency Trading Using Machine Learning. Journal of Risk and Financial Management 13: 178. [Google Scholar] [CrossRef]

- Kristjanpoller, Werner, and Marcel C. Minutolo. 2015. Gold Price Volatility: A Forecasting Approach Using the Artificial Neural Network–GARCH Model. Expert Systems with Applications 42: 7245–51. [Google Scholar] [CrossRef]

- Kuhn, Max, Jed Wing, Steve Weston, Andre Williams, Chris Keefer, Allan Engelhardt, and Tony Cooper. 2020. Caret: Classification and Regression Training (version 6.0-86). Available online: https://CRAN.R-project.org/package=caret (accessed on 30 March 2021).

- Leung, Mark T., Hazem Daouk, and An-Sing Chen. 2000. Forecasting Stock Indices: A Comparison of Classification and Level Estimation Models. International Journal of Forecasting 16: 173–90. [Google Scholar] [CrossRef]

- Liu, Dan, and Zhi Li. 2017. Gold Price Forecasting and Related Influence Factors Analysis Based on Random Forest. In Proceedings of the Tenth International Conference on Management Science and Engineering Management. Advances in Intelligent Systems and Computing. Edited by Jiuping Xu, Asaf Hajiyev, Stefan Nickel and Mitsuo Gen. Singapore: Springer, pp. 711–23. [Google Scholar] [CrossRef]

- Livieris, Ioannis E., Emmanuel Pintelas, and Panagiotis Pintelas. 2020. A CNN–LSTM Model for Gold Price Time-Series Forecasting. Neural Computing and Applications 32: 17351–60. [Google Scholar] [CrossRef]

- Lohrmann, Christoph, and Pasi Luukka. 2019. Classification of Intraday S&P500 Returns with a Random Forest. International Journal of Forecasting 35: 390–407. [Google Scholar] [CrossRef]

- Mahato, P. K., and V. Attar. 2014. Prediction of Gold and Silver Stock Price Using Ensemble Models. Paper presented at the 2014 International Conference on Advances in Engineering Technology Research (ICAETR 2014), Unnao, Kanpur, India, August 1–2; pp. 1–4. [Google Scholar] [CrossRef]

- Neely, Christopher J., David E. Rapach, Jun Tu, and Guofu Zhou. 2014. Forecasting the Equity Risk Premium: The Role of Technical Indicators. Management Science 60: 1772–91. [Google Scholar] [CrossRef] [Green Version]

- Nyberg, Henri. 2011. Forecasting the Direction of the US Stock Market with Dynamic Binary Probit Models. International Journal of Forecasting 27: 561–78. [Google Scholar] [CrossRef]

- Nyberg, Henri, and Harri Pönkä. 2016. International Sign Predictability of Stock Returns: The Role of the United States. Economic Modelling 58: 323–38. [Google Scholar] [CrossRef] [Green Version]

- O’Connor, Fergal A., Brian M. Lucey, Jonathan A. Batten, and Dirk G. Baur. 2015. The Financial Economics of Gold—A Survey. International Review of Financial Analysis 41: 186–205. [Google Scholar] [CrossRef]

- Parisi, Antonino, Franco Parisi, and David Díaz. 2008. Forecasting Gold Price Changes: Rolling and Recursive Neural Network Models. Journal of Multinational Financial Management 18: 477–87. [Google Scholar] [CrossRef]

- Pierdzioch, Christian, and Marian Risse. 2020. Forecasting Precious Metal Returns with Multivariate Random Forests. Empirical Economics 58: 1167–84. [Google Scholar] [CrossRef]

- Pierdzioch, Christian, Marian Risse, and Sebastian Rohloff. 2015. Forecasting Gold-Price Fluctuations: A Real-Time Boosting Approach. Applied Economics Letters 22: 46–50. [Google Scholar] [CrossRef]

- Pierdzioch, Christian, Marian Risse, and Sebastian Rohloff. 2016a. A Quantile-Boosting Approach to Forecasting Gold Returns. The North American Journal of Economics and Finance 35: 38–55. [Google Scholar] [CrossRef]

- Pierdzioch, Christian, Marian Risse, and Sebastian Rohloff. 2016b. A Boosting Approach to Forecasting the Volatility of Gold-Price Fluctuations under Flexible Loss. Resources Policy 47: 95–107. [Google Scholar] [CrossRef]

- Plakandaras, Vasilios, Periklis Gogas, and Theophilos Papadimitriou. 2021. Gold Against the Machine. Computational Economics 57: 5–28. [Google Scholar] [CrossRef]

- Pönkä, Harri. 2016. Real Oil Prices and the International Sign Predictability of Stock Returns. Finance Research Letters 17: 79–87. [Google Scholar] [CrossRef] [Green Version]

- R Core Team. 2019. R: A Language and Environment for Statistical Computing, Version R Version 3.6.0 (26 April 2019); Vienna: The R Project for Statistical Computing. Available online: https://www.r-project.org/ (accessed on 30 March 2021).

- Reboredo, Juan C. 2013. Is Gold a Safe Haven or a Hedge for the US Dollar? Implications for Risk Management. Journal of Banking & Finance 37: 2665–76. [Google Scholar] [CrossRef]

- Risse, Marian. 2019. Combining Wavelet Decomposition with Machine Learning to Forecast Gold Returns. International Journal of Forecasting 35: 601–15. [Google Scholar] [CrossRef]

- Sadorsky, Perry. 2021. A Random Forests Approach to Predicting Clean Energy Stock Prices. Journal of Risk and Financial Management 14: 48. [Google Scholar] [CrossRef]

- Shafiee, Shahriar, and Erkan Topal. 2010. An Overview of Global Gold Market and Gold Price Forecasting. Resources Policy 35: 178–89. [Google Scholar] [CrossRef]

- Suimon, Yoshiyuki, Hiroki Sakaji, Kiyoshi Izumi, and Hiroyasu Matsushima. 2020. Autoencoder-Based Three-Factor Model for the Yield Curve of Japanese Government Bonds and a Trading Strategy. Journal of Risk and Financial Management 13: 82. [Google Scholar] [CrossRef]

- Tronzano, Marco. 2021. Financial Crises, Macroeconomic Variables, and Long-Run Risk: An Econometric Analysis of Stock Returns Correlations (2000 to 2019). Journal of Risk and Financial Management 14: 127. [Google Scholar] [CrossRef]

- Vezeris, Dimitrios, Ioannis Karkanis, and Themistoklis Kyrgos. 2019. AdTurtle: An Advanced Turtle Trading System. Journal of Risk and Financial Management 12: 96. [Google Scholar] [CrossRef] [Green Version]

- Wang, Yudong, Li Liu, and Chongfeng Wu. 2020. Forecasting Commodity Prices Out-of-Sample: Can Technical Indicators Help? International Journal of Forecasting 36: 666–83. [Google Scholar] [CrossRef]

- Yazdani-Chamzini, Abdolreza, Siamak Haji Yakhchali, Diana Volungevičienė, and Edmundas Kazimieras Zavadskas. 2012. Forecasting Gold Price Changes by Using Adaptive Network Fuzzy Inference System. Journal of Business Economics and Management 13: 994–1010. [Google Scholar] [CrossRef] [Green Version]

- Yin, Libo, and Qingyuan Yang. 2016. Predicting the Oil Prices: Do Technical Indicators Help? Energy Economics 56: 338–50. [Google Scholar] [CrossRef]

- Yin, Libo, Qingyuan Yang, and Zhi Su. 2017. Predictability of Structural Co-Movement in Commodity Prices: The Role of Technical Indicators. Quantitative Finance 17: 795–812. [Google Scholar] [CrossRef]

- Zengeler, Nico, and Uwe Handmann. 2020. Contracts for Difference: A Reinforcement Learning Approach. Journal of Risk and Financial Management 13: 78. [Google Scholar] [CrossRef] [Green Version]

Figure 1.

This figure shows gold (GLD) and silver (SLV) ETF prices across time. Data are sourced from Yahoo Finance.

Figure 1.

This figure shows gold (GLD) and silver (SLV) ETF prices across time. Data are sourced from Yahoo Finance.

Figure 2.

This figure shows histograms of gold (GLD) and silver (SLV) ETF percentage of up days. Data sourced from Yahoo Finance. Author’s own calculations.

Figure 2.

This figure shows histograms of gold (GLD) and silver (SLV) ETF percentage of up days. Data sourced from Yahoo Finance. Author’s own calculations.

Figure 3.

This figure shows RFs test error vs. the number of trees. OOB (Red), down classification (Black), up classification (Green). Calculations are done for predicting stock price direction over a 10-step forecast horizon.

Figure 3.

This figure shows RFs test error vs. the number of trees. OOB (Red), down classification (Black), up classification (Green). Calculations are done for predicting stock price direction over a 10-step forecast horizon.

Figure 4.

This figure shows the multi-period prediction accuracy for GLD price direction.

Figure 5.

This figure shows the multi-period prediction accuracy for SLV price direction.

Figure 6.

This figure shows the multi-period kappa accuracy for GLD price direction.

Figure 7.

This figure shows the multi-period kappa accuracy for SLV price direction.

Figure 8.

This figure shows the multi-period positive predictive values accuracy value for GLD price direction.

Figure 8.

This figure shows the multi-period positive predictive values accuracy value for GLD price direction.

Figure 9.

This figure shows the multi-period positive predictive values accuracy for SLV price direction.

Figure 9.

This figure shows the multi-period positive predictive values accuracy for SLV price direction.

Figure 10.

This figure shows the multi-period negative predictive value for GLD price direction.

Figure 11.

This figure shows the multi-period negative predictive value for SLV price direction.

Figure 12.

This figure shows GLD equity curves comparing the buy and hold portfolio with the random forests switching portfolio.

Figure 12.

This figure shows GLD equity curves comparing the buy and hold portfolio with the random forests switching portfolio.

Figure 13.

This figure shows SLV equity curves comparing the buy and hold portfolio with the random forests switching portfolio.

Figure 13.

This figure shows SLV equity curves comparing the buy and hold portfolio with the random forests switching portfolio.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Descriptive statistics of daily returns.

| GLD | SLV | |

|---|---|---|

| median | 0.0527 | 0.0962 |

| mean | 0.0262 | 0.0159 |

| std.dev | 1.1613 | 2.0436 |

| coef.var | 44.2617 | 128.8832 |

| skewness | −0.3345 | −1.0015 |

| kurtosis | 6.4282 | 8.4359 |

| normtest.W | 0.9394 | 0.9147 |

| normtest.p | <0.001 | <0.001 |

Daily data on continuously compounded daily returns for the period 2 May 2006 to 29 January 2021 (3713 observations).

Table 2.

Variable importance for predicting GLD and SLV price direction.

| GLD | DOWN | UP | MD Accuracy | MD Gini |

| RSI | 20.173 | 29.138 | 41.748 | 83.854 |

| StoFASTK | 15.784 | 20.268 | 28.364 | 72.086 |

| StoFASTD | 16.770 | 22.636 | 32.413 | 73.554 |

| StoSLOWD | 20.669 | 23.290 | 35.770 | 79.595 |

| ADX | 36.884 | 45.997 | 58.702 | 112.804 |

| MACD | 32.026 | 34.362 | 49.794 | 100.971 |

| MACDSignal | 37.177 | 35.449 | 53.509 | 109.645 |

| PriceRateOfChange | 20.357 | 27.748 | 38.655 | 89.875 |

| OnBalanceVolume | 31.622 | 33.133 | 56.289 | 128.120 |

| MA200 | 46.703 | 33.859 | 62.001 | 160.118 |

| MA50 | 38.525 | 35.569 | 62.455 | 151.582 |

| MFI | 23.270 | 35.455 | 44.288 | 91.704 |

| WAD | 34.989 | 39.088 | 66.054 | 131.950 |

| SLV | DOWN | UP | MD Accuracy | MD Gini |

| RSI | 21.973 | 29.103 | 42.251 | 80.768 |

| StoFASTK | 16.743 | 23.763 | 32.791 | 73.615 |

| StoFASTD | 16.543 | 23.463 | 32.193 | 72.895 |

| StoSLOWD | 23.559 | 24.950 | 37.327 | 80.689 |

| ADX | 39.325 | 42.789 | 50.931 | 114.854 |

| MACD | 32.813 | 39.336 | 51.095 | 113.236 |

| MACDSignal | 37.227 | 37.563 | 51.289 | 113.466 |

| PriceRateOfChange | 20.979 | 32.039 | 42.128 | 92.992 |

| OnBalanceVolume | 41.042 | 34.133 | 52.971 | 127.660 |

| MA200 | 49.461 | 33.258 | 64.580 | 151.835 |

| MA50 | 39.074 | 40.194 | 65.836 | 150.612 |

| MFI | 21.369 | 26.593 | 37.392 | 80.974 |

| WAD | 45.073 | 33.248 | 58.787 | 143.667 |

This table shows the RFs variable importance of the technical analysis indicators measured using mean decrease in accuracy (MD accuracy) and mean decrease in GINI (MD Gini). Values reported for a 10-period forecast horizon.

Table 3.

Comparing CV with tsCV from random forests prediction.

| 10 Day | 20 Day | |||||||

|---|---|---|---|---|---|---|---|---|

| GLD CV | GLD tsCV | SLV CV | SLV tsCV | GLD CV | GLD tsCV | SLV CV | SLV tsCV | |

| Accuracy | 0.8698 | 0.8061 | 0.8455 | 0.7959 | 0.8906 | 0.8609 | 0.9036 | 0.8522 |

| Kappa | 0.7353 | 0.6085 | 0.6898 | 0.5904 | 0.7791 | 0.7211 | 0.8072 | 0.7043 |

| Pos Pred Value | 0.8805 | 0.7803 | 0.8379 | 0.7768 | 0.8871 | 0.8434 | 0.8864 | 0.8488 |

| Neg Pred Value | 0.8621 | 0.8276 | 0.8522 | 0.8132 | 0.8935 | 0.8771 | 0.9213 | 0.8555 |

This table shows random forests forecast accuracy values computed from cross validation (CV) and time series cross validation (tsCV) for gold (GLD) and silver (SLV) price direction.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Sadorsky, P. Predicting Gold and Silver Price Direction Using Tree-Based Classifiers. J. Risk Financial Manag. 2021, 14, 198. https://doi.org/10.3390/jrfm14050198

AMA Style

Sadorsky P. Predicting Gold and Silver Price Direction Using Tree-Based Classifiers. Journal of Risk and Financial Management. 2021; 14(5):198. https://doi.org/10.3390/jrfm14050198

Chicago/Turabian StyleSadorsky, Perry. 2021. "Predicting Gold and Silver Price Direction Using Tree-Based Classifiers" Journal of Risk and Financial Management 14, no. 5: 198. https://doi.org/10.3390/jrfm14050198