The United States and China Financial Communication and the Notion of Risk

Abstract

:1. Introduction

2. The Sociological Approach to Risk: Risk as an Object of Perception

3. Methodological Approach: A Textual Analysis of Financial Communication in a Financing Relationship

3.1. Textual Analysis Using Alceste Method

3.2. Discourse on Risk and Choice of Material

3.3. Collection and Creation of the Database

4. Textual Analysis Result and discussion: Words of Risk

4.1. Structuring Financial Communication Classes

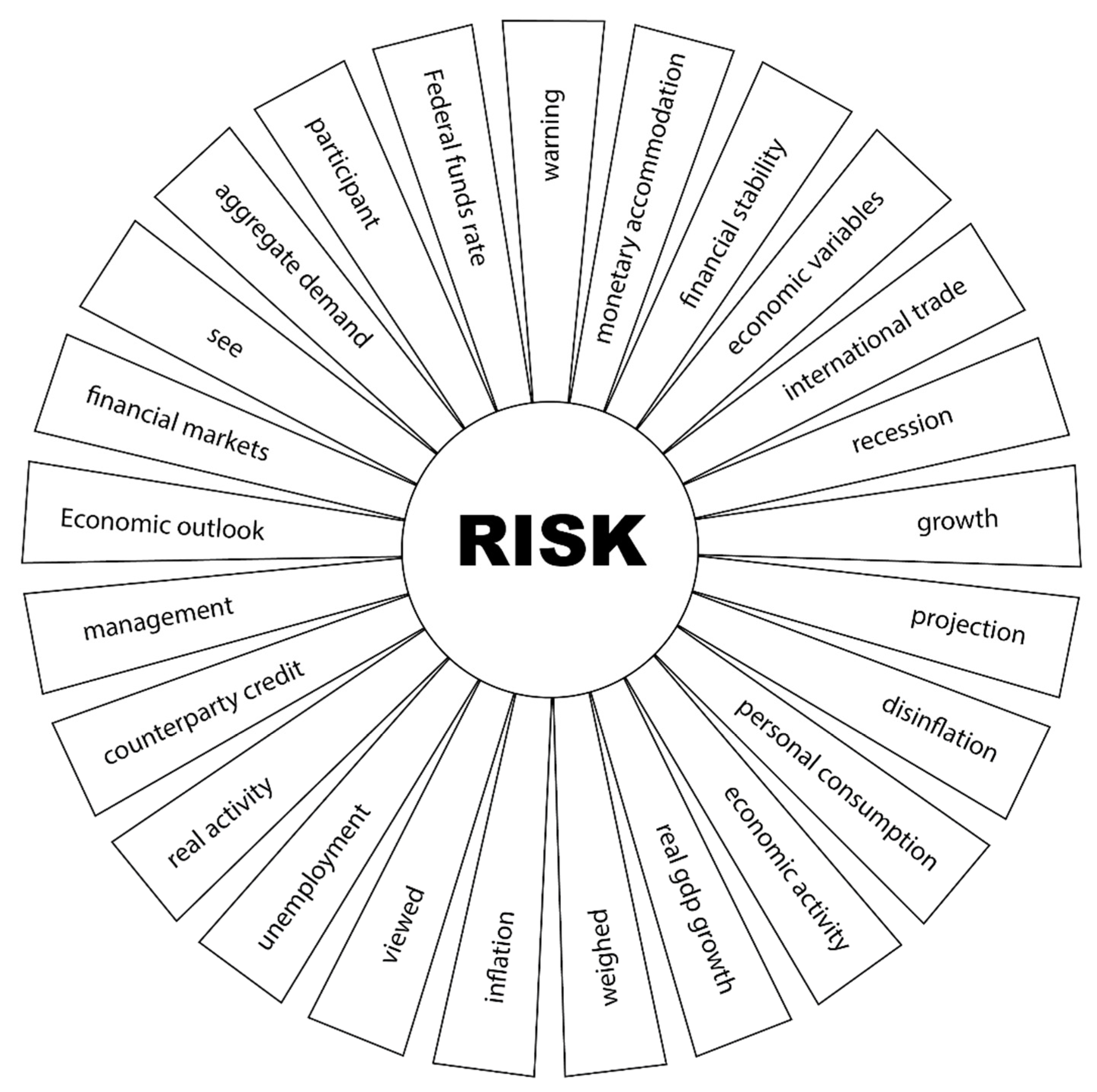

4.2. Place of “Risk” in the Discourse of the Two Countries and Their Central Banks: From Textual Analysis to a Return to the Cultural Theory of Risk

The Notion of Risk in the Annual Report

- 1.

- China;

- 2.

- The United States of America;

4.3. The Positioning of the Countries and the Central Banks in the Matrix of “Cultural Theory”

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Adams, John. 1995. Risk. London: University College London Press. [Google Scholar]

- Af WÅhlberg, Anders E. 2001. The theoretical features of some current approaches to risk perception. Journal of Risk Research 4: 237–50. [Google Scholar] [CrossRef]

- An, Jaehyung, Alexey Mikhaylov, and Ulf H. Richter. 2020. Trade war effects: Evidence from sectors of energy and resources in Africa. Heliyon 6: e05693. [Google Scholar] [CrossRef]

- Bank for International Settlements. 2006. Basel Committee on Banking Supervision (BCBS). Available online: https://www.bis.org/publ/bcbs128.pdf (accessed on 5 January 2020).

- Bank for International Settlements. 2010. Basel Committee on Banking Supervision (BCBS). Available online: https://www.bis.org/publ/bcbs188.pdf (accessed on 5 January 2020).

- Bank for International Settlements. 2017. Basel Committee on Banking Supervision (BCBS): Basel III: Post-Crisis Reforms Finalization. Available online: https://www.bis.org/bcbs/publ/d424.pdf (accessed on 5 January 2020).

- Beck, Ulrich. 1986. Risikogesellschaft. Auf Weg in Eine Andere Moderne. Suhrkamp, Frankfurt Am Main; Trad. It. (2000) La Società Del Rischio: Verso Una Seconda Modernità. Roma: Carocci. [Google Scholar]

- Boholm, Åsa. 1996. Risk perception and social anthropology: Critique of cultural theory. Ethnos 61: 64–84. [Google Scholar] [CrossRef]

- Bouzon, Arlette. 1999. Communication de crise et maîtrise des risques dans les organisations. Communication et Organization 16: 45. [Google Scholar] [CrossRef] [Green Version]

- Corvoisier, Sandrine, and Reint Gropp. 2002. Bank concentration and retail interest rates. Journal of Banking & Finance 26: 2155–89. [Google Scholar]

- Dake, Karl. 1992. Myths of nature: Culture and the social construction of risk. Journal of Social Issues 48: 21–37. [Google Scholar] [CrossRef]

- Douglas, Mary. 1970. Natural Symbols. London: The Cresset Press. [Google Scholar]

- Douglas, Mary. 1982. Introduction to Grid/Group Analysis. London: Routledge. [Google Scholar]

- Douglas, Mary. 1997. The depoliticization of risk. In Culture Matters: Essays in Honor of Aaron Wildavsky. Edited by Richard. J. Ellis and Michael Thompson. Boulder: Westview Press. [Google Scholar]

- Douglas, Mary, and Aaron Wildavsky. 1983. Risk and Culture: An Essay on the Selection of Technological and Environmental Dangers. Berkeley: University of California Press. [Google Scholar]

- Dryhurst, Sarah, Claudia R. Schneider, John Kerr, Alexandra L. J. Freeman, Gabriel Recchia, Anne Marthe Van Der Bles, David Spiegelhalter, and Sander van der Linden. 2020. Risk perceptions of COVID-19 around the world. Journal of Risk Research 23: 994–1006. [Google Scholar] [CrossRef]

- Duclos, Denis. 1994. Quand la tribu des modernes sacrifie au dieu risque. Déviance et Société 18: 345–64. [Google Scholar] [CrossRef]

- Durkheim, Emile. 1893. The Division of Labor in Society. Translated by George Simpson. New York: Free Press. [Google Scholar]

- Evans-Pritchard, Edward Evan. 1968. Les Nuer. Description Des Modes de Vie Et Des Institutions D’un Peuple Nilotique, (Trad. fr. L. Evrard). Paris: Gallimard. [Google Scholar]

- Ewald, François. 2000. Le Risque Dans La Société Contemporaine. Paris: Cité des Sciences et de l’Industrie de Paris, pp. 55–72. [Google Scholar]

- Franzosi, Roberto. 2012. Quantitative Narrative Analysis. Thousand Oaks: Sage publications, Inc. [Google Scholar]

- Gavard-Perret, Marie-Laure, and Agnès Helme-Guizon. 2008. Choisir Parmi Les Techniques Spécifiques D’analyse Qualitative. Montreuil: Pearson, pp. 247–79. [Google Scholar]

- Gavard-Perret, Marie-Laure, David Gotteland, Christophe Haon, and Alain Jolibert. 2008. Méthodologie de La Recherche. Montreuil: Pearson, pp. 87–138. [Google Scholar]

- Hallvarsson and Halvarson. 2010. Consultancy (2010) Storbankernas och Myndigheternas Kommunikation under Finanskrisen. Stockholm: H&H Group. [Google Scholar]

- Hardy, Cynthia, and Nelson Phillips. 1999. No joking matter: Discursive struggle in the Canadian refugee system. Organization Studies 20: 1–24. [Google Scholar] [CrossRef]

- Hargadon, Andrew B., and Yellowlees Douglas. 2001. When innovations meet institutions: Edison and the design of the electric light. Administrative Science Quarterly 46: 476–501. [Google Scholar] [CrossRef]

- Joffe, Hélène. 2003. Risk: From perception to social representation. British Journal of Social Psychology 42: 55–73. [Google Scholar] [CrossRef]

- Kasperson, Roger E., Ortwin Renn, Paul Slovic, Halina S. Brown, Jacque Emel, Robert Goble, Jeanne X. Kasperson, and Samuel Ratick. 1988. The social amplification of risk: A conceptual framework. Risk Analysis 8: 177–87. [Google Scholar] [CrossRef] [Green Version]

- Lawrence, Thomas B., and Nelson Phillips. 2004. From Moby Dick to Free Willy: Macro-cultural discourse and institutional entrepreneurship in emerging institutional fields. Organization 11: 689–711. [Google Scholar] [CrossRef] [Green Version]

- Le Breton, David. 2017. Sociologie du Risque:«Que Sais-je?» n° 3016. Que sais-je. Paris: Presses Universitaires de France/Humensis. [Google Scholar]

- Leiserowitz, Anthony. 2006. Climate change risk perception and policy preferences: The role of affect, imagery, and values. Climatic Change 77: 45–72. [Google Scholar] [CrossRef] [Green Version]

- Libaert, Thierry. 1999. Communication de crise: Le choix des messages. Humanisme et Entreprise 236: 33–50. [Google Scholar]

- Loewenstein, George F., Elke U. Weber, Christopher K. Hsee, and Ned Welch. 2001. Risk as feelings. Psychological Bulletin 127: 267. [Google Scholar] [CrossRef]

- Maguire, Steve, and Cynthia Hardy. 2009. Discourse and deinstitutionalization: The decline of DDT. Academy of Management Journal 52: 148–78. [Google Scholar] [CrossRef]

- Marris, Claire, Ian H. Langford, and Timothy O’riordan. 1998. A quantitative test of the cultural theory of risk perceptions: Comparison with the psychometric paradigm. Risk Analysis 18: 635–47. [Google Scholar] [CrossRef]

- Mikhaylov, Alexey, Nikita Moiseev, Kirill Aleshin, and Thomas Burkhardt. 2020. Global climate change and greenhouse effect. Entrepreneurship and Sustainability Issues 7: 2897. [Google Scholar] [CrossRef]

- Moiseev, Nikita, Alexey Mikhaylov, Igor Varyash, and Abdul Saqib. 2020. Investigating the relation of GDP per capita and corruption index. Entrepreneurship and Sustainability Issues 8: 780. [Google Scholar] [CrossRef]

- Munir, Kamal A., and Nelson Phillips. 2005. The birth of the’Kodak Moment’: Institutional entrepreneurship and the adoption of new technologies. Organization Studies 26: 1665–87. [Google Scholar] [CrossRef]

- Oakes, Leslie S., Barbara Townley, and David J. Cooper. 1998. Business planning as pedagogy: Language and control in a changing institutional field. Administrative Science Quarterly 1: 257–92. [Google Scholar] [CrossRef]

- Peretti-Watel, Patrick. 2000. Sociologie Du Risque. Paris: Armand Colin. [Google Scholar]

- Peretti-Watel, Patrick. 2010. La Société Du Risque, Nouvelle Édition. Paris: La Découverte (Collection Repères). [Google Scholar]

- Perren, Lew, and Jonathan Sapsed. 2013. Innovation as politics: The rise and reshaping of innovation in UK parliamentary discourse 1960–2005. Research Policy 42: 1815–28. [Google Scholar] [CrossRef]

- Petit, Emmanuel. 2011. L’apport de la psychologie sociale à l’analyse économique. Revue D’économie Politique 121: 797–837. [Google Scholar] [CrossRef] [Green Version]

- Phillips, Nelson, Thomas B. Lawrence, and Cynthia Hardy. 2004. Discourse and institutions. Academy of Management Review 29: 635–52. [Google Scholar] [CrossRef]

- Rayner, Steve. 1992. Cultural Theory and Risk Analysis. Westport: Praeger. [Google Scholar]

- Reinert, Max. 2007. Subjective Postures and Stable Lexical Worlds in Statistical Discourse Analysis. Langage et Societe 3: 189–202. [Google Scholar] [CrossRef]

- Richardson, John. 2006. Analysing Newspapers: An Approach from Critical Discourse Analysis. London: Palgrave. [Google Scholar]

- Schwarz, Michiel, and Michael Thompson. 1990. Divided We Stand: Redefining Politics, Technology, and Social Choice. Philadelphia: University of Pennsylvania Press. [Google Scholar]

- Seignour, Amélie. 2011. Méthode d’analyse des discours. Revue Française de Gestion 2: 29–45. [Google Scholar] [CrossRef]

- Sjoberg, Lennart. 1998. World views, political attitudes and risk perception. Risk 9: 137. [Google Scholar]

- Sjöberg, Lennart. 2002. Are received risk perception models alive and well? Risk Analysis: An International Journal 22: 665–69. [Google Scholar] [CrossRef]

- Slovic, Paul. 2010. The Feeling of Risk: New Perspectives on Risk Perception. London: Routledge. [Google Scholar]

- Slovic, Paul, Baruch Fischhoff, and Sarah Lichtenstein. 1982. Why study risk perception? Risk Analysis 2: 83–93. [Google Scholar] [CrossRef]

- Thompson, Michael. 1980. Aesthetics of Risk: Context or Culture. New York: Plenum, pp. 273–86. [Google Scholar]

- Van der Linden, Sander. 2015. The social-psychological determinants of climate change risk perceptions: Towards a comprehensive model. Journal of Environmental Psychology 41: 112–24. [Google Scholar] [CrossRef]

- Van der Linden, Sander. 2016. A conceptual critique of the cultural cognition thesis. Science Communication 38: 128–38. [Google Scholar] [CrossRef] [Green Version]

- Van der Linden, Sander. 2017. Determinants and measurement of climate change risk perception, worry, and concern. In The Oxford Encyclopedia of Climate Change Communication. Oxford: Oxford University Press. [Google Scholar]

- Varyash, Igor, Alexey Mikhaylov, Nikita Moiseev, and Kirill Aleshin. 2020. Triple bottom line and corporate social responsibility performance indicators for Russian companies. Entrepreneurship and Sustainability 2020: 8. [Google Scholar] [CrossRef]

- Wildavsky, Aaron, and Karl Dake. 1990. Theories of risk perception: Who fears what and why? Daedalus 1: 41–60. [Google Scholar]

- World Health Organization. 2015. General Information on Risk Communication. Geneva: World Health Organization, vol. 2015. [Google Scholar]

- Xu, Sifan. 2018. When individual cultural orientation and mediated portrayal of risk intersect: Effects of individualism–collectivism and media framing on risk perception and attribution of responsibility. Journal of Contingencies and Crisis Management 26: 499–509. [Google Scholar] [CrossRef]

- Zeng, Jingjing, Meiquan Jiang, and Meng Yuan. 2020. Environmental risk perception, risk culture, and pro-environmental behavior. International Journal of Environmental Research and Public Health 17: 1750. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | Entities | Number of Annual Reports Analyzed |

|---|---|---|

| The U.S.A. | Federal Reserve | 13 (2007–2019) |

| Federal Government | 13 (2007–2019) | |

| China | People’s Bank of China | 09 (2011–2019) |

| Central Government | 13 (2007–2019) | |

| Total report analyzed | 48 |

| Classification | The U.S.A. | China | ||

|---|---|---|---|---|

| Federal Reserve | Federal Government | Central Government | People’s Bank of China | |

| Number of stable classes | 4 | 4 | 4 | 4 |

| Number of text segments | 29,554 | 49,255 | 5018 | 14,498 |

| Number of forms | 8407 | 12,706 | 6505 | 10,678 |

| Number of occurrences | 1,068,466 | 1,789,068 | 181,253 | 519,446 |

| Number of lexemes | 6173 | 9140 | 5083 | 7735 |

| Number of active forms | 4793 | 7557 | 3110 | 6236 |

| Number of additional forms | 1380 | 1583 | 1973 | 1499 |

| Number of active forms with frequency | >=7: 2862 | >=13: 2881 | >=3: 1967 | >=6: 2677 |

| Average of forms per segment | 36.153008 | 36.322566 | 36.120566 | 35.828804 |

| Percentage of elementary context units (U.C.E.) classified | 79.76% | 90.99% | 86.23% | 76.38% |

| Number of hapaxes (forms present only once in the corpus) | 2245 | 927 | 1677 | 2253 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zheng, C.; Kouadio, K.R.; Kombate, B. The United States and China Financial Communication and the Notion of Risk. J. Risk Financial Manag. 2021, 14, 143. https://doi.org/10.3390/jrfm14040143

Zheng C, Kouadio KR, Kombate B. The United States and China Financial Communication and the Notion of Risk. Journal of Risk and Financial Management. 2021; 14(4):143. https://doi.org/10.3390/jrfm14040143

Chicago/Turabian StyleZheng, Changjun, Konan Richard Kouadio, and Bienmali Kombate. 2021. "The United States and China Financial Communication and the Notion of Risk" Journal of Risk and Financial Management 14, no. 4: 143. https://doi.org/10.3390/jrfm14040143