A Hypothesis Test Method for Detecting Multifractal Scaling, Applied to Bitcoin Prices

Abstract

:1. Introduction

1.1. Monofractal vs. Multifractal Processes

1.2. Examination of Multifractality

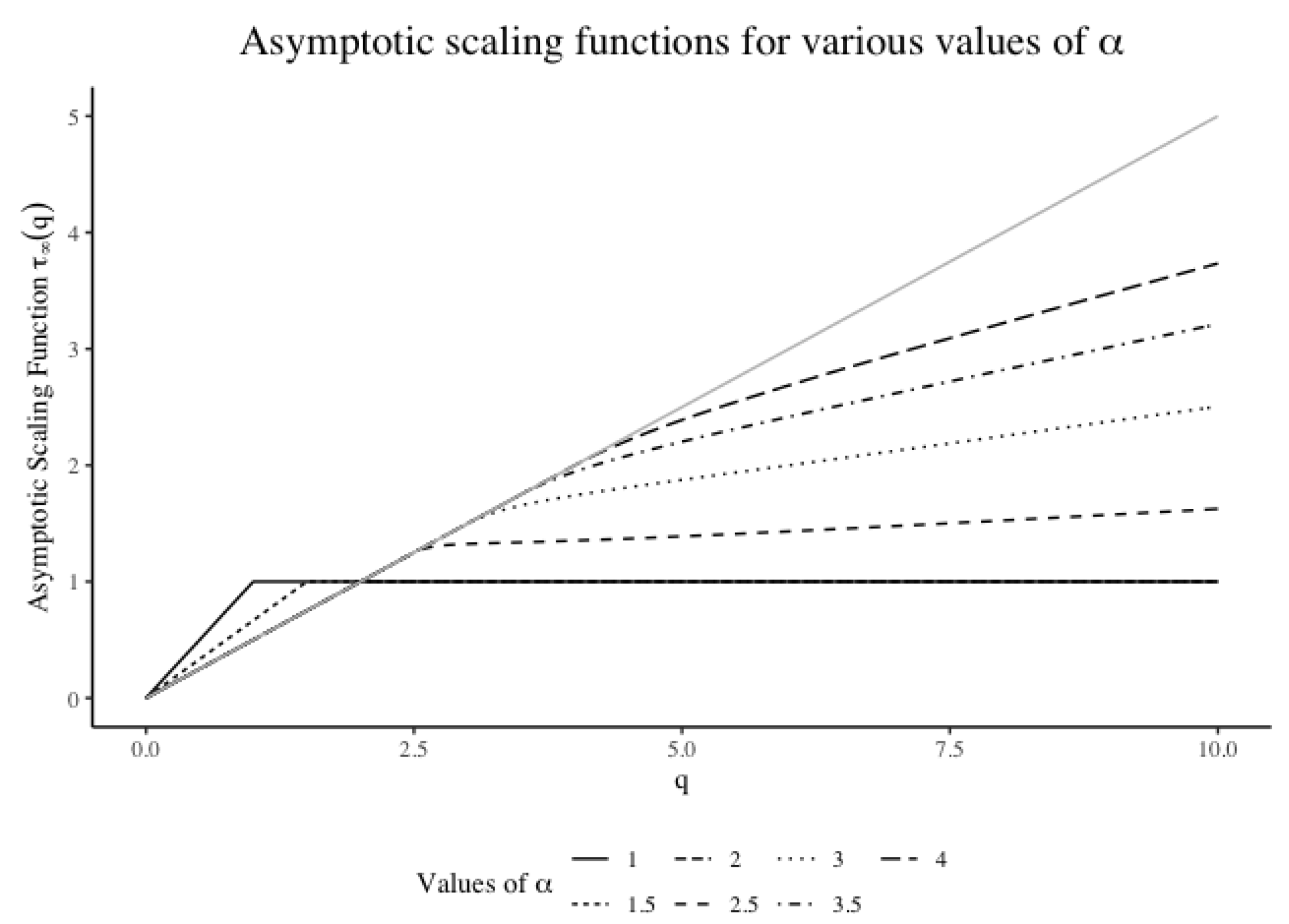

1.3. Simulation of Multifractal Processes

- In Stage 1, divide the time interval into non-overlapping subintervals with equal length . Assign multipliers to each subinterval, where the are random variables with distributions that are not necessarily discrete. For computational convenience, we assume the to be identically distributed with a common distribution M.

- In Stage 2, each of the b intervals is further divided into b subintervals of length . Again, we assign multipliers to each subinterval. The are assumed to be identically distributed with distribution M. Thus, after the second stage, the mass on an interval, for example , will be if and with probabilitysince the multipliers at different stages are independent. The measure represents the multiplicative measure at Stage 2.

- Repetition of this scheme generates a sequence of measures which converges to our desired multiplicative measure as .

1.4. Multifractality and Heavy Tails

2. Methodology

2.1. Measure of Concavity

- 1.

- there is an iid sample drawn from the joint distribution of the random variables , where ϵ is symmetrically distributed about 0 (conditional on x), so that ;

- 2.

- the observed sample is , where is generated by and the functional form of f is left unspecified.

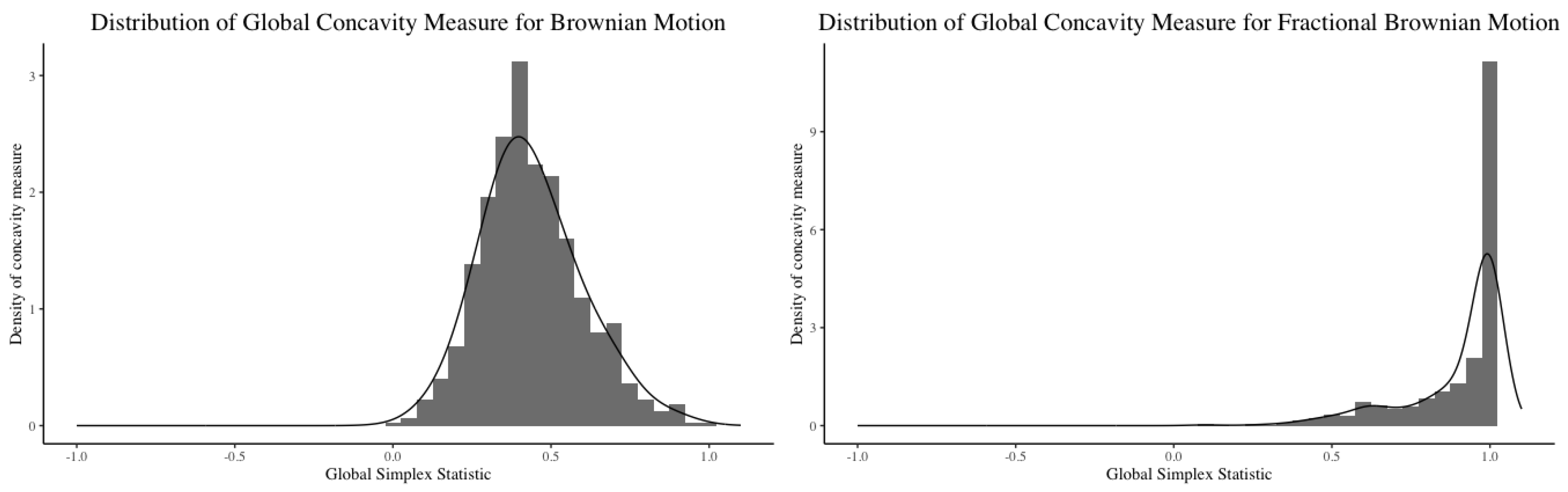

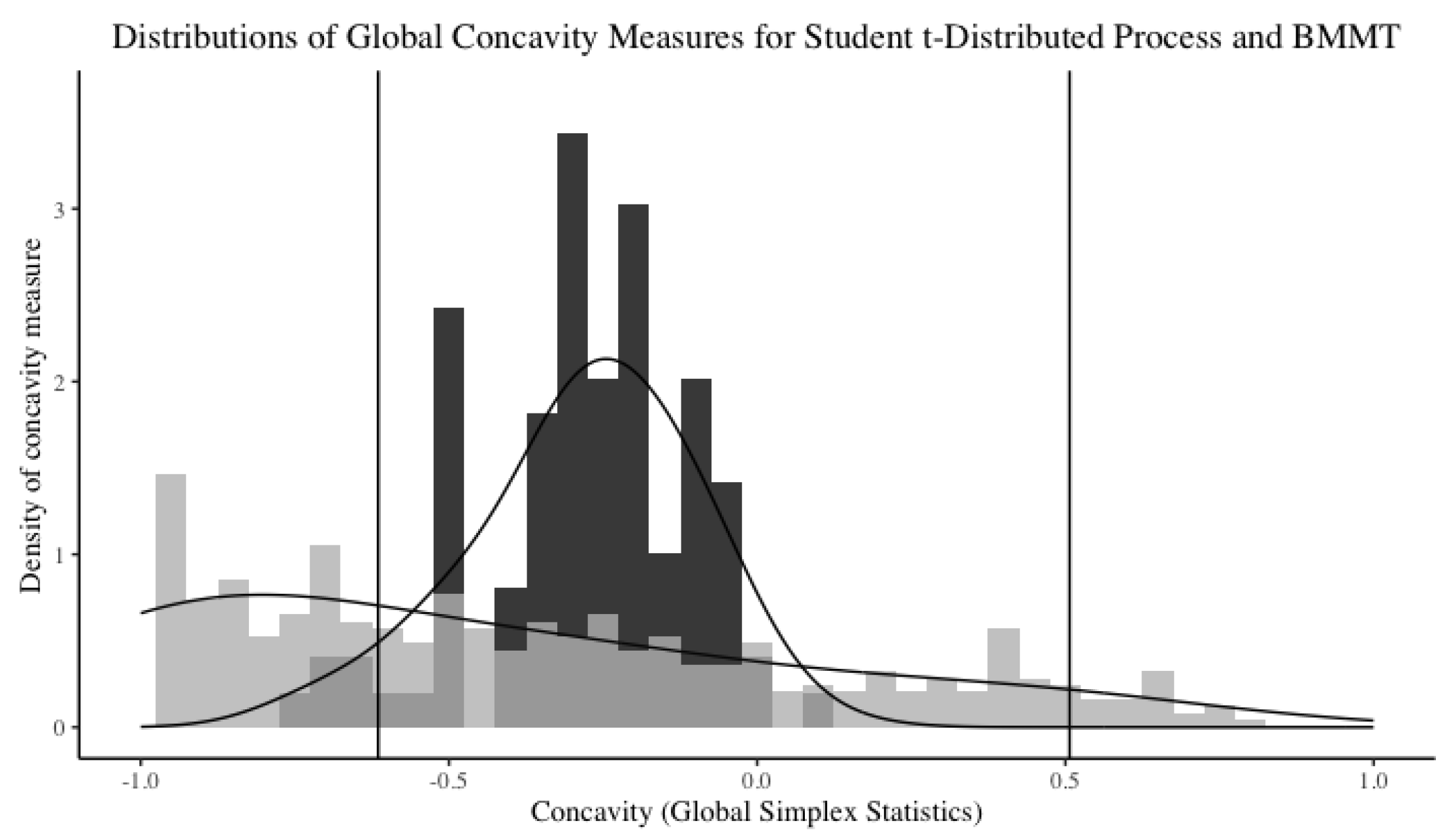

2.2. Simulation Results

2.3. Look-Up Table

3. Results

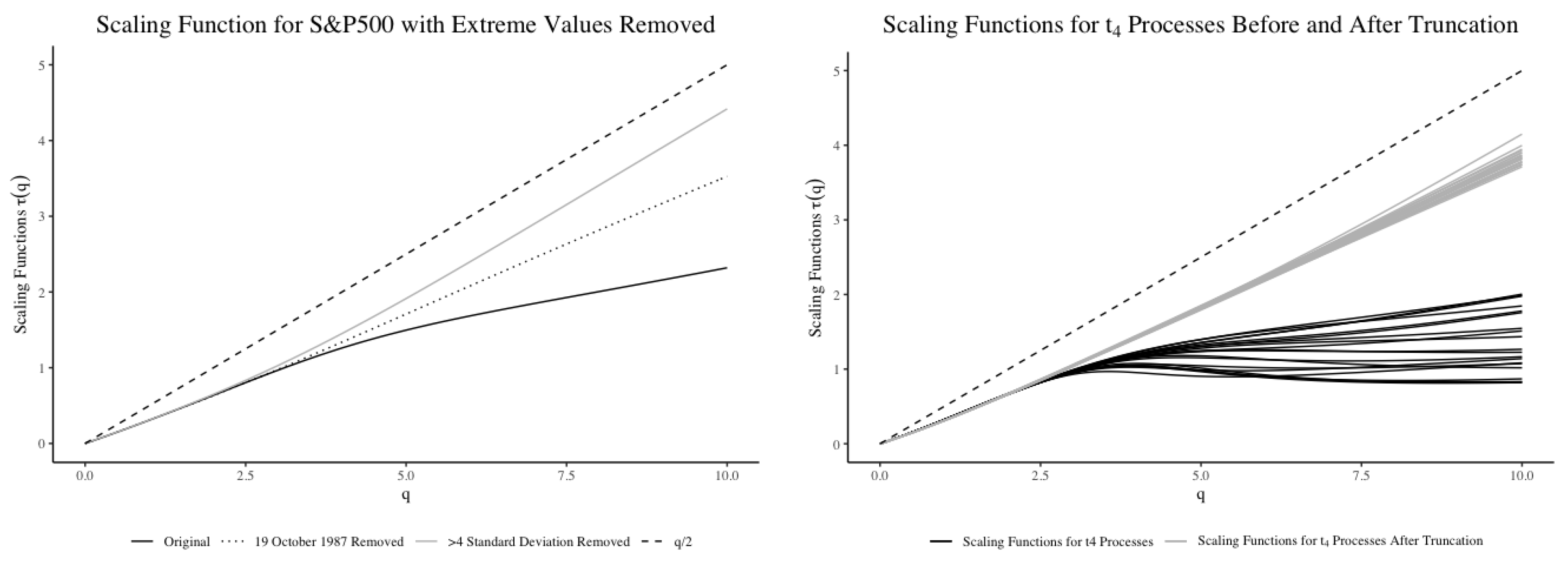

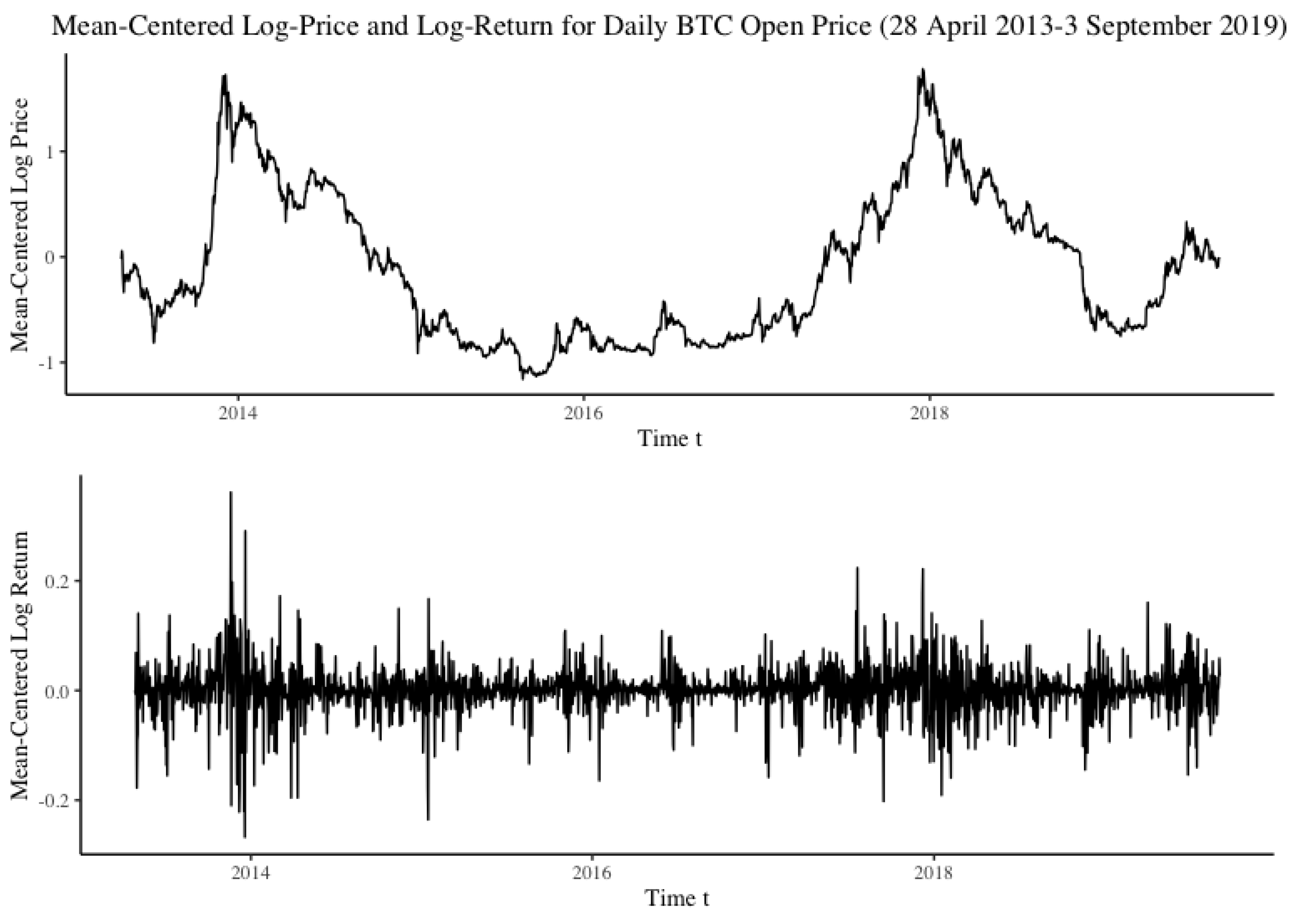

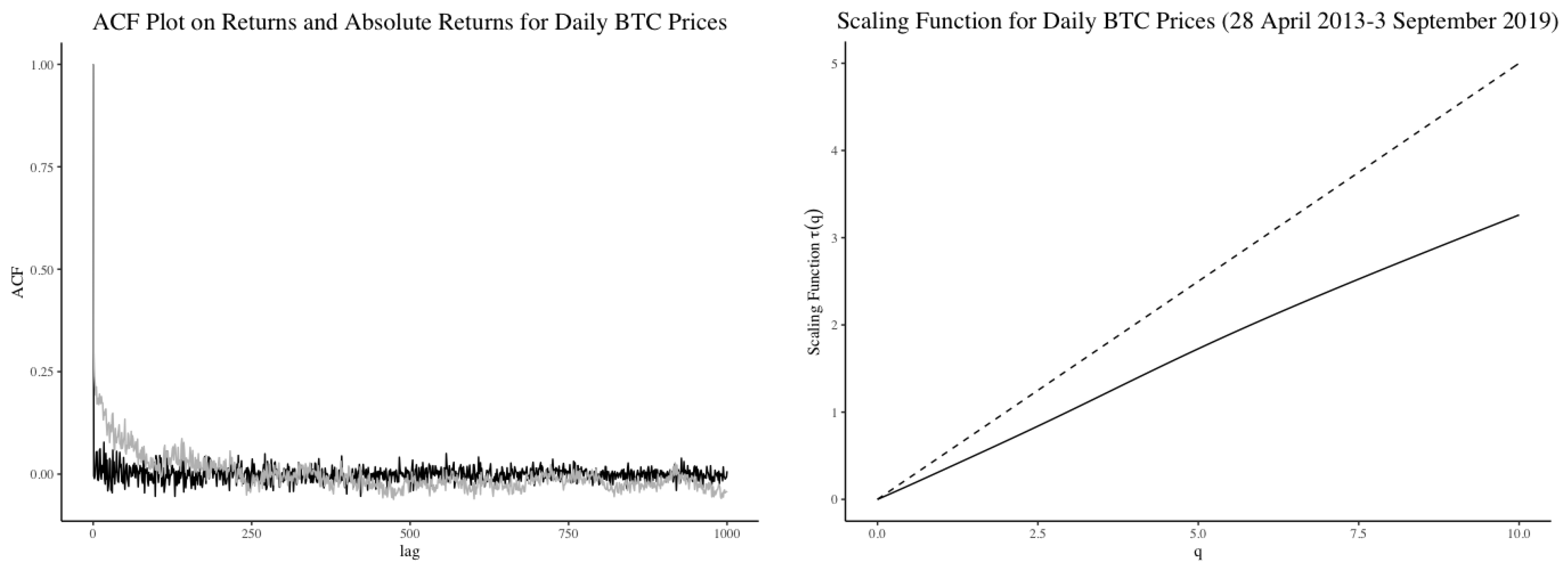

3.1. Application to Bitcoin

- the daily Bitcoin open price, daily data (in USD) from 28 April 2013 to 3 September 2019 with 2,320 observations, retrieved from CoinMarketCap (2019); and

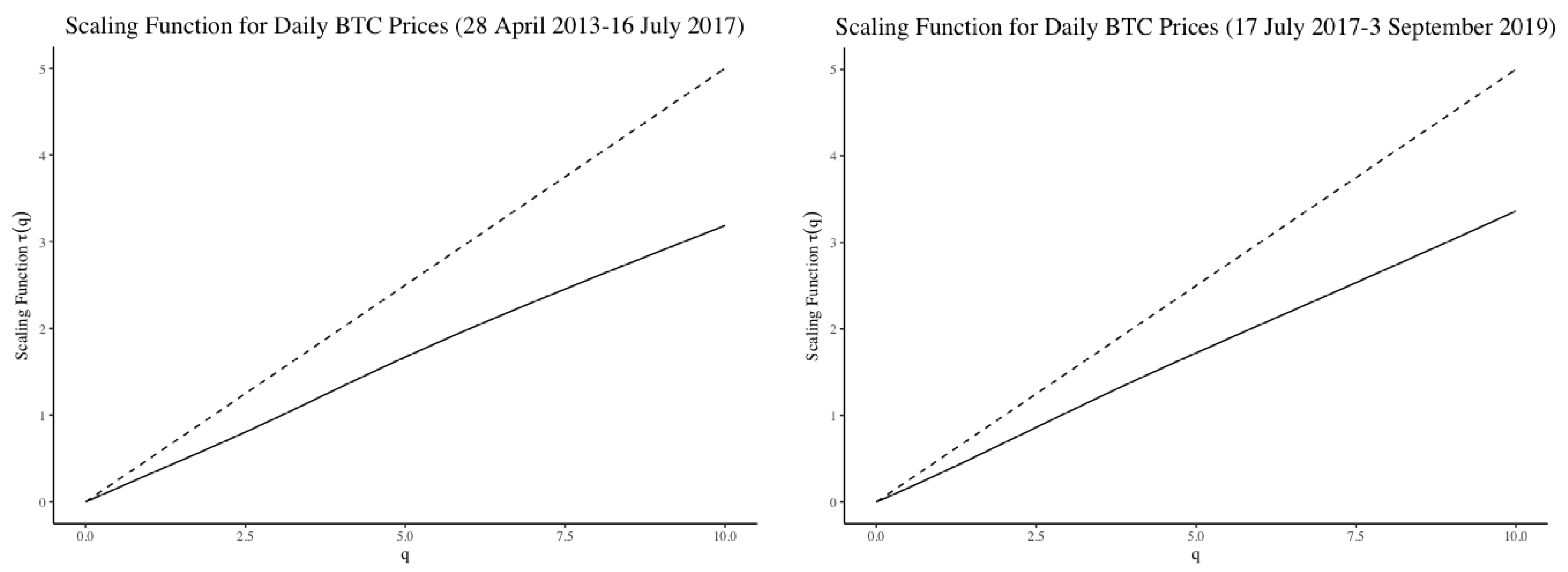

3.1.1. Daily Bitcoin Price Data

- from 28 April 2013 to 16 July 2017 with 1541 observations; and,

- from 17 July 2017 to 3 September 2019 with 779 observations.

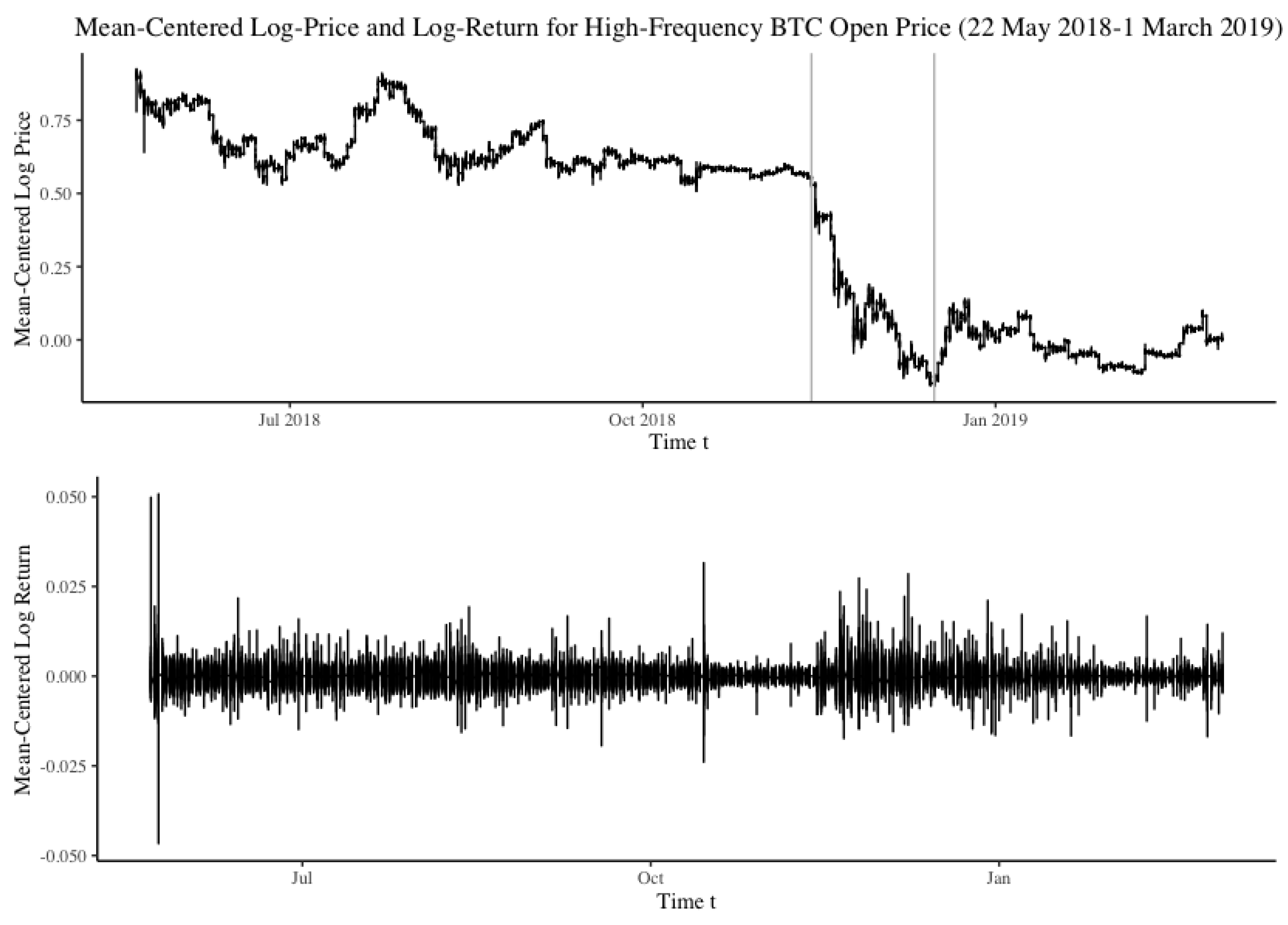

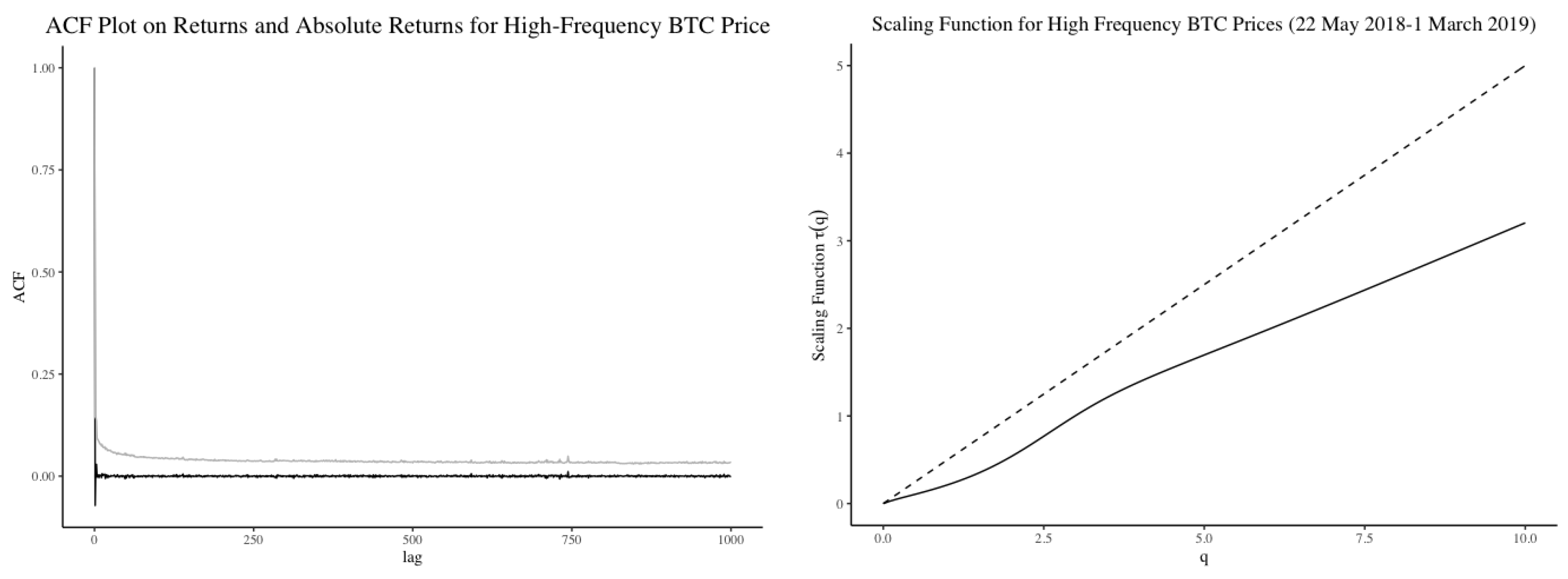

3.1.2. High-Frequency Bitcoin Price Data

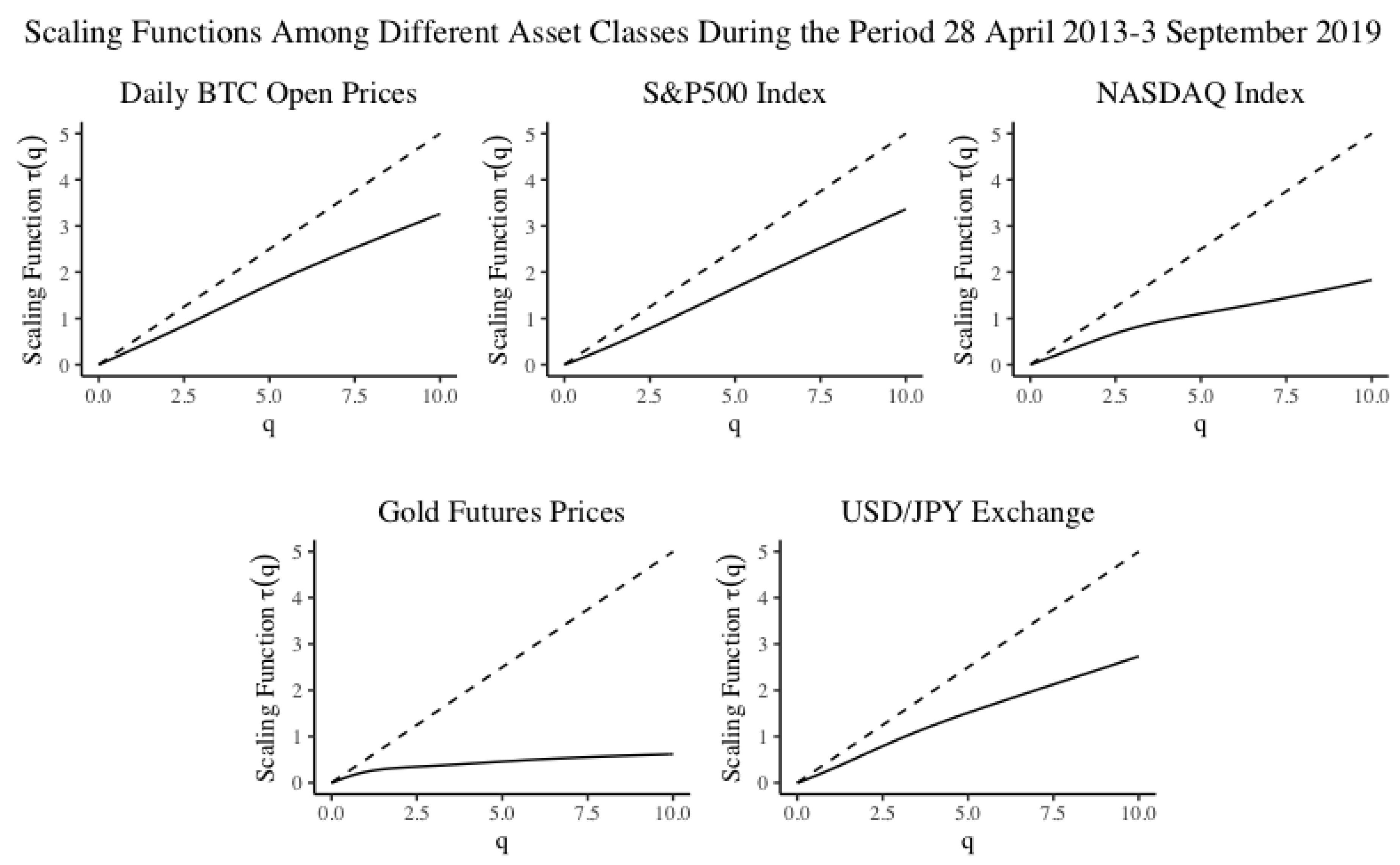

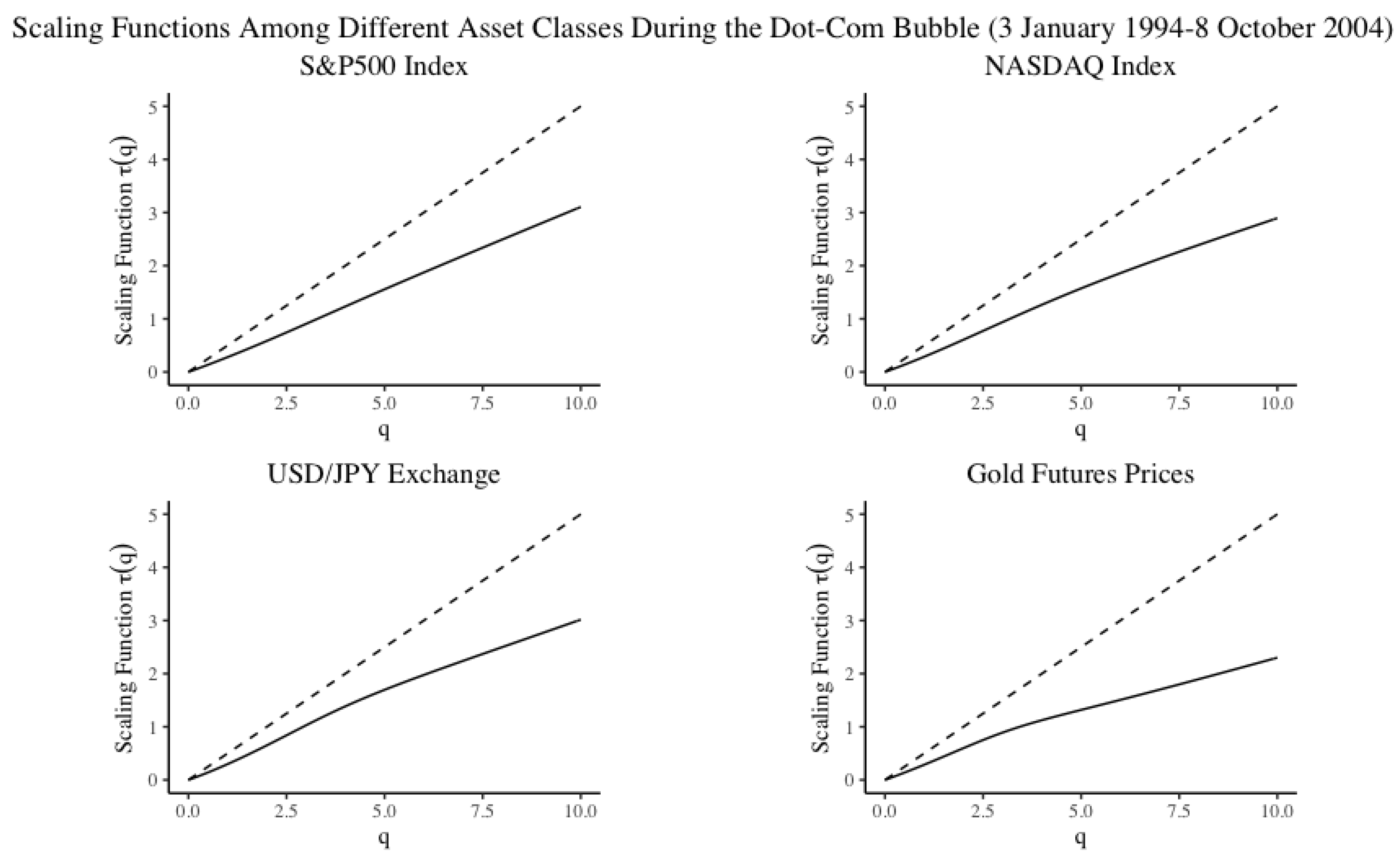

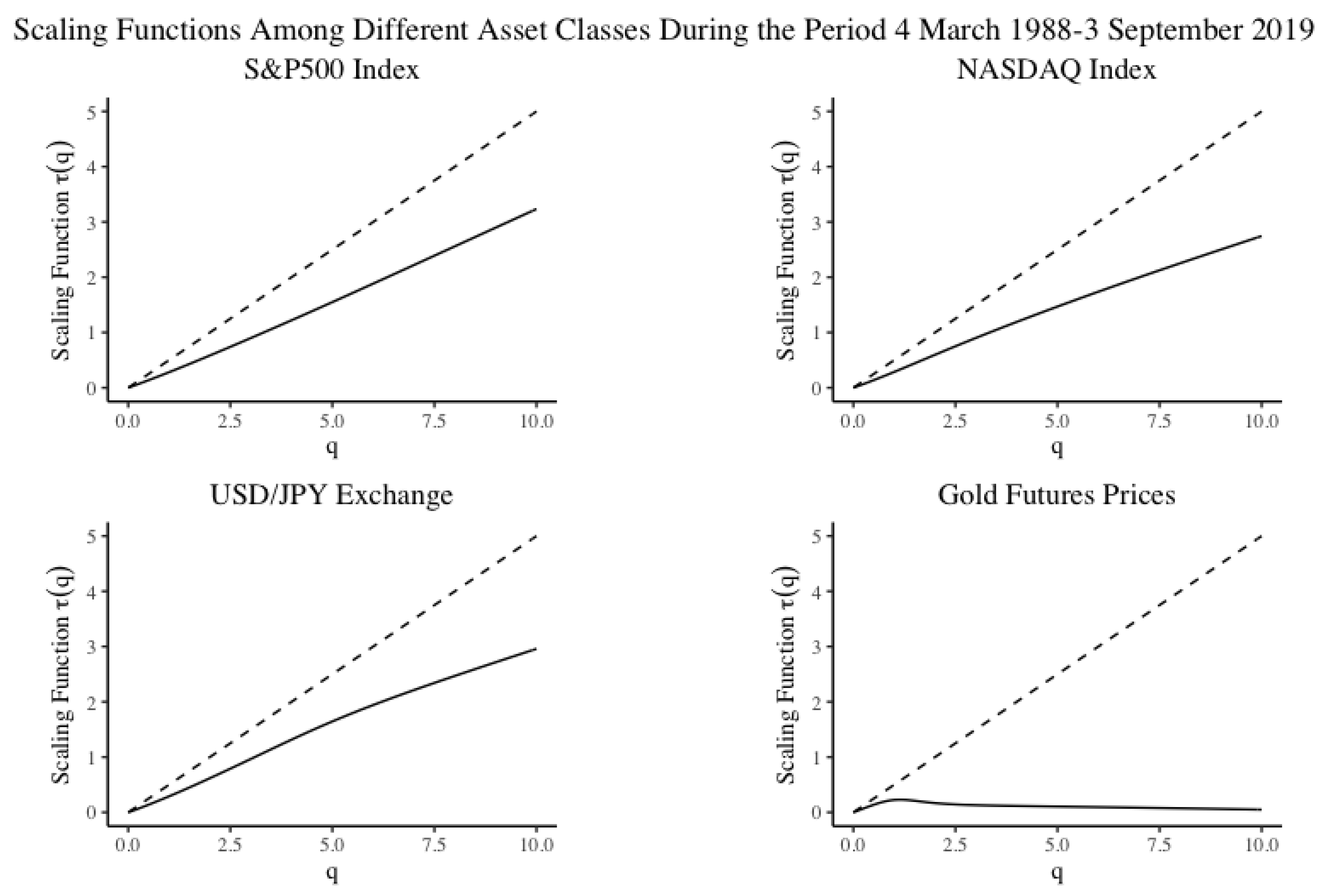

3.2. Bitcoin Compared to Other Financial Assets

4. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A. Look-Up Table

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Localised Concavity Measure | Global Concavity Measure | ||

|---|---|---|---|

| Tail Index | Critical Value | Tail Index | Critical Value |

| 0.50 | −0.8889 | 0.50 | −0.9979 |

| 0.75 | −0.8889 | 0.75 | −0.9987 |

| 1.00 | −0.8333 | 1.00 | −0.9987 |

| 1.25 | −0.7778 | 1.25 | −0.9986 |

| 1.50 | −0.6667 | 1.50 | −0.9963 |

| 1.75 | −0.5556 | 1.75 | −0.8543 |

| 2.00 | −0.3889 | 2.00 | −0.7503 |

| 2.25 | −0.3333 | 2.25 | −0.5482 |

| 2.50 | −0.2222 | 2.50 | −0.5264 |

| 2.75 | −0.1111 | 2.75 | −0.4992 |

| 3.00 | −0.0556 | 3.00 | −0.6231 |

| 3.25 | −0.1111 | 3.25 | −0.7011 |

| 3.50 | −0.1667 | 3.50 | −0.7562 |

| 3.75 | −0.2222 | 3.75 | −0.8330 |

| 4.00 | −0.2778 | 4.00 | −0.8791 |

| 4.25 | −0.3333 | 4.25 | −0.9274 |

| 4.50 | −0.3889 | 4.50 | −0.9291 |

| 4.75 | −0.5000 | 4.75 | −0.9228 |

| 5.00 | −0.5556 | 5.00 | −0.9259 |

| 5.25 | −0.5556 | 5.25 | −0.9149 |

| 5.50 | −0.5556 | 5.50 | −0.9133 |

| 5.75 | −0.5556 | 5.75 | −0.9086 |

| 6.00 | −0.5083 | 6.00 | −0.9006 |

| 6.25 | −0.5000 | 6.25 | −0.8835 |

| 6.50 | −0.4444 | 6.50 | −0.8548 |

| 6.75 | −0.4444 | 6.75 | −0.8233 |

| 7.00 | −0.4444 | 7.00 | −0.8047 |

| 7.25 | −0.3333 | 7.25 | −0.7321 |

| 7.50 | −0.3333 | 7.50 | −0.7018 |

| 7.75 | −0.2528 | 7.75 | −0.6804 |

| 8.00 | −0.2222 | 8.00 | −0.6545 |

| 8.25 | −0.2222 | 8.25 | −0.6203 |

| 8.50 | −0.2528 | 8.50 | −0.5517 |

| 8.75 | −0.2222 | 8.75 | −0.4959 |

| 9.00 | −0.2222 | 9.00 | −0.4449 |

| 9.25 | −0.2222 | 9.25 | −0.4065 |

| 9.50 | −0.2222 | 9.50 | −0.3928 |

| 9.75 | −0.1167 | 9.75 | −0.3969 |

| 10.00 | −0.1111 | 10.00 | −0.3293 |

Appendix B. Multifractality Test Results

Appendix B.1. Hypothesis Test Results on Daily Bitcoin Open Price Data—Annual Breakdown

| Time Period | Tail Index | Localised Measure | Sample Size | Test Result |

|---|---|---|---|---|

| 28/04/2013–31/12/2013 | 2.0886 | −0.5556 | 2026 | Multifractal |

| 01/01/2014–31/12/2014 | 1.4785 | −0.3333 | 1904 | Non-Multifractal |

| 01/01/2015–31/12/2015 | 0.9464 | 0.2222 | 980 | Non-Multifractal |

| 01/01/2016–31/12/2016 | 1.7584 | −0.7778 | 2036 | Multifractal |

| 01/01/2017–31/12/2017 | 2.2187 | −0.6111 | 1997 | Multifractal |

| 01/01/2018–31/12/2018 | 1.6145 | 0.1667 | 1977 | Non-Multifractal |

| 01/01/2019–03/09/2019 | 1.4411 | 0.6111 | 1867 | Non-Multifractal |

| Time Period | Tail Index | Global Measure | Sample Size | Test Result |

|---|---|---|---|---|

| 28/04/2013–31/12/2013 | 2.0886 | −0.9260 | 72 | Multifractal |

| 01/01/2014–31/12/2014 | 1.4785 | −0.7300 | 77 | Non-Multifractal |

| 01/01/2015–31/12/2015 | 0.9464 | −0.0511 | 50 | Non-Multifractal |

| 01/01/2016–31/12/2016 | 1.7584 | −0.9473 | 80 | Multifractal |

| 01/01/2017–31/12/2017 | 2.2187 | −0.9551 | 70 | Multifractal |

| 01/01/2018–31/12/2018 | 1.6145 | 0.2706 | 74 | Non-Multifractal |

| 01/01/2019–03/09/2019 | 1.4411 | 0.8439 | 80 | Non-Multifractal |

Appendix B.2. Hypothesis Test Results on High Frequency Bitcoin Price Data

| Time Period | Tail Index | Localised | Sample Size | Test Result |

|---|---|---|---|---|

| 22/05/2018 14:01–08/07/2018 23:23 | 2.1226 | 0.0000 | 2015 | Non-Multifractal |

| 08/07/2018 23:24–24/08/2018 23:24 | 2.9599 | −0.3333 | 1572 | Multifractal |

| 24/08/2018 23:25–11/10/2018 00:25 | 2.5649 | −0.4444 | 1889 | Multifractal |

| 11/10/2018 00:26–27/11/2018 10:56 | 2.5984 | −0.6667 | 1847 | Multifractal |

| 27/11/2018 10:57–13/01/2019 10:57 | 2.8381 | −0.2778 | 1654 | Multifractal |

| 13/01/2019 10:58–01/03/2019 10:58 | 2.6245 | −0.5000 | 1845 | Multifractal |

| Time Period | Tail Index | Global | Sample Size | Test Result |

|---|---|---|---|---|

| 22/05/2018 14:01–08/07/2018 23:23 | 2.1226 | −0.4811 | 72 | Non-Multifractal |

| 08/07/2018 23:24–24/08/2018 23:24 | 2.9599 | −0.3872 | 96 | Non-Multifractal |

| 24/08/2018 23:25–11/10/2018 00:25 | 2.5649 | −0.5587 | 74 | Multifractal |

| 11/10/2018 00:26–27/11/2018 10:56 | 2.5984 | −0.8287 | 74 | Multifractal |

| 27/11/2018 10:57–13/01/2019 10:57 | 2.8381 | −0.6690 | 88 | Multifractal |

| 13/01/2019 10:58–01/03/2019 10:58 | 2.6245 | −0.4125 | 75 | Non-Multifractal |

References

- Abrevaya, Jason, and Wei Jiang. 2005. A nonparametric approach to measuring and testing curvature. Journal of Business & Economic Statistics 23: 1–19. [Google Scholar]

- Bariviera, Aurelio F. 2017. The inefficiency of bitcoin revisited: A dynamic approach. Economics Letters 161: 1–4. [Google Scholar] [CrossRef] [Green Version]

- Bariviera, Aurelio F., María José Basgall, Waldo Hasperué, and Marcelo Naiouf. 2017. Some stylized facts of the bitcoin market. Physica A: Statistical Mechanics and Its Applications 484: 82–90. [Google Scholar] [CrossRef] [Green Version]

- Binance. 2019. BTC/USDT. Available online: https://www.binance.com/en/trade/BTC_USDT (accessed on 20 March 2019).

- Bouchaud, Jean-Philippe, Marc Potters, and Martin Meyer. 2000. Apparent multifractality in financial time series. The European Physical Journal B-Condensed Matter and Complex Systems 13: 595–99. [Google Scholar] [CrossRef] [Green Version]

- Calvet, Laurent E., Adlai J. Fisher, and Benoit B. Mandelbrot. 1997. Large Deviations and the Distribution of Price Changes. Cowles Foundation Discussion Paper No. 1165. New Haven: Cowles Foundation for Research in Economics Yale University. [Google Scholar]

- Chambers, Clem. 2019. Bitcoin Is Fractal. Available online: https://www.forbes.com/sites/investor/2019/01/23/bitcoin-is-fractal/#27bbcc49208d (accessed on 30 April 2019).

- CoinMarketCap. 2019. Bitcoin (BTC) Price, Charts, Market Cap, and Other Metrics. Available online: https://coinmarketcap.com/currencies/bitcoin/ (accessed on 5 September 2019).

- Embrechts, Paul, and Makoto Maejima. 2000. An introduction to the theory of self-similar stochastic processes. International Journal of Modern Physics B 14: 1399–420. [Google Scholar] [CrossRef]

- Grahovac, Danijel, and Nikolai N. Leonenko. 2014. Detecting multifractal stochastic processes under heavy-tailed effects. Chaos, Solitons & Fractals 65: 78–89. [Google Scholar]

- Heyde, Chris C. 2009. Scaling issues for risky asset modelling. Mathematical Methods of Operations Research 69: 593–603. [Google Scholar] [CrossRef]

- investing.com Australia. 2020a. Gold Futures—Apr 20 (GCJ0). Available online: https://au.investing.com/commodities/gold-historical-data (accessed on 27 February 2020).

- investing.com Australia. 2020b. USD JPY Historical Data—Investing.com AU. Available online: https://au.investing.com/currencies/usd-jpy-historical-data (accessed on 27 February 2020).

- Kantelhardt, Jan W., Stephan A. Zschiegner, Eva Koscielny-Bunde, Shlomo Havlin, Armin Bunde, and H. Eugene Stanley. 2002. Multifractal detrended fluctuation analysis of nonstationary time series. Physica A: Statistical Mechanics and Its Applications 316: 87–114. [Google Scholar] [CrossRef] [Green Version]

- Lahmiri, Salim, and Stelios Bekiros. 2018. Chaos, randomness and multi-fractality in bitcoin market. Chaos, Solitons & Fractals 106: 28–34. [Google Scholar]

- Mandelbrot, Benoit B., Adlai J. Fisher, and Laurent E. Calvet. 1997. A Multifractal Model of Asset Returns. Cowles Foundation Discussion Paper No. 1164. New Haven: Cowles Foundation for Research in Economics Yale University. [Google Scholar]

- Matia, Kaushik, Yosef Ashkenazy, and H. Eugene Stanley. 2003. Multifractal properties of price fluctuations of stocks and commodities. EPL (Europhysics Letters) 61: 422. [Google Scholar] [CrossRef] [Green Version]

- Mensi, Walid, Yun-Jung Lee, Khamis Hamed Al-Yahyaee, Ahmet Sensoy, and Seong-Min Yoon. 2019. Intraday downward/upward multifractality and long memory in bitcoin and ethereum markets: An asymmetric multifractal detrended fluctuation analysis. Finance Research Letters 31: 19–25. [Google Scholar] [CrossRef]

- Milutinović, Monia. 2018. Cryptocurrency. Екoнoмика-Часoпис за екoнoмску теoрију и праксу и друштвена питањаа 1: 105–122. [Google Scholar] [CrossRef] [Green Version]

- Nadarajah, Saralees, and Jeffrey Chu. 2017. On the inefficiency of bitcoin. Economics Letters 150: 6–9. [Google Scholar] [CrossRef] [Green Version]

- Nakamoto, Satoshi. 2009. Bitcoin: A Peer-to-Peer Electronic Cash System. Available online: https://bitcoin.org/bitcoin.pdf (accessed on 20 November 2018).

- Patterson, Michael. 2018. Crypto’s 80% Plunge Is Now Worse Than the Dot-Com Crash. Available online: https://www.bloomberg.com/news/articles/2018-09-12/crypto-s-crash-just-surpassed-dot-com-levels-as-losses-reach-80 (accessed on 7 August 2019).

- Platen, Eckhard, and Renata Rendek. 2008. Empirical evidence on student-t log-returns of diversified world stock indices. Journal of Statistical Theory and Practice 2: 233–251. [Google Scholar] [CrossRef] [Green Version]

- Popken, Ben. 2018. Bitcoin Loses More Than Half Its Value Amid Crypto Crash. Available online: https://www.nbcnews.com/tech/internet/bitcoin-loses-more-half-its-value-amid-crypto-crash-n844056 (accessed on 7 August 2019).

- Salat, Hadrien, Roberto Murcio, and Elsa Arcaute. 2017. Multifractal methodology. Physica A: Statistical Mechanics and Its Applications 473: 467–487. [Google Scholar] [CrossRef]

- Sly, Allan. 2006. Self-similarity, multifractionality and multifractality. Master’s thesis, Australian National University, Canberra, Australia. [Google Scholar]

- Sreenivasan, Katepalli. 1991. Fractals and multifractals in fluid turbulence. Annual Review of Fluid Mechanics 23: 539–604. [Google Scholar] [CrossRef]

- Stavroyiannis, Stavros, Vassilios Babalos, Stelios Bekiros, Salim Lahmiri, and Gazi Salah Uddin. 2019. The high frequency multifractal properties of bitcoin. Physica A: Statistical Mechanics and Its Applications 520: 62–71. [Google Scholar] [CrossRef]

- Yahoo Finance. 2019. S&P 500 (^GSPC) Historical Data. Available online: https://au.finance.yahoo.com/quote/^GSPC/history?p=^GSPC (accessed on 27 February 2020).

- Yahoo Finance. 2020. NASDAQ Composite (^IXIC) Historical Data. Available online: https://finance.yahoo.com/quote/%5Eixic/history?ltr=1 (accessed on 27 February 2020).

- Zhang, Wei, Pengfei Wang, Xiao Li, and Dehua Shen. 2018. The inefficiency of cryptocurrency and its cross-correlation with dow jones industrial average. Physica A: Statistical Mechanics and Its Applications 510: 658–670. [Google Scholar] [CrossRef]

| 1. | “False positive” corresponds to the scenario that we mistakenly detect multifractality when the underlying process does not possess the multifractal property. |

| 2. | For convenience, in the rest of this paper, we call uniscaling multifractal processes monofractal processes while referring to multiscaling multifractal processes as multifractal processes. |

| 3. | We compared the scaling functions of the Bitcoin and other financial assets with the ones of BMMTs simulated using multiplicative cascades with Poisson distribution, Gamma distribution and Normal distribution. The scaling function of the BMMT simulated through log-Normal multiplicative cascade displays the most similar behaviour. |

| 4. | The choice of Student’s t-distribution with 4 degrees of freedom is suggested by the findings of Platen and Rendek (2008). |

| 5. | Knots were chosen so that the function is evaluated on 18 equal sub-intervals. This gave the best approximation considering computational efficiency. |

| 6. | For example, if Hill’s estimator takes value , we generate simulated student t-distributed processes with 2 degrees of freedom, select those with tail indices in the interval , and construct the null distribution using the empirical distribution of their concavity measures. |

| 7. | Retrieved from Yahoo Finance (2019) for the period 30 December 1927 to 26 February 2020 with 23,147 observations. |

| 8. | Retrieved from Yahoo Finance (2020) for the period 5 February 1971 to 25 February 2020 with 12,372 observations. |

| 9. | Retrieved from investing.com Australia (2020b) for the period 4 March 1988 to 28 February 2020 with 8337 observations. |

| 10. | Retrieved from investing.com Australia (2020a) for the period 27 December 1979 to 28 February 2020 with 10,190 observations. |

| Tail Index | 3.0630 | |||

|---|---|---|---|---|

| Sample Size 1 | Test Statistic | Rejection Region | Test Result | |

| Localised Test | 1479 | Multifractal | ||

| Global Test | 99 | Multifractal |

| Tail Index | 3.2791 | |||

|---|---|---|---|---|

| Sample Size | Test Statistic | Rejection Region | Test Result | |

| Localised Test | 1403 | Multifractal | ||

| Global Test | 98 | Non-Multifractal |

| Tail Index | 1.6528 | |||

|---|---|---|---|---|

| Sample Size | Test Statistic | Rejection Region | Test Result | |

| Localised Test | 1992 | Multifractal | ||

| Global Test | 75 | Multifractal |

| Tail Index | 2.7759 | |||

|---|---|---|---|---|

| Sample Size | Test Statistic | Rejection Region | Test Result | |

| Localised Test | 1682 | Non-multifractal | ||

| Global Test | 83 | Non-multifractal |

| Financial Asset | Tail Index | Test | Test Statistics | Rejection Region | Test Result (Local) |

|---|---|---|---|---|---|

| BTC Daily | 3.06 | Local | −0.22 | [−1, −0.06) | Multifractal |

| Global | −0.63 | [−1, −0.61) | Multifractal | ||

| S&P500 | 3.13 | Local | −0.11 | [−1, −0.11) | Non-Multifractal |

| Global | −0.14 | [−1, −0.66) | Non-Multifractal | ||

| NASDAQ | 3.19 | Local | 0.11 | [−1, −0.11) | Non-Multifractal |

| Global | −0.44 | [−1, −0.66) | Non-Multifractal | ||

| USD/JPY | 2.69 | Local | −0.28 | [−1, −0.17) | Multifractal |

| Global | −0.86 | [−1, −0.49) | Multifractal | ||

| Gold Futures | 1.35 | Local | −0.67 | [−1, −0.72) | Non-Multifractal |

| Global | −0.89 | [−1, −0.9979) | Non-Multifractal |

| Financial Asset | Tail Index | Test | Test Statistics | Rejection Region | Test Result (Local) |

|---|---|---|---|---|---|

| S&P500 | 3.41 | Local | −0.22 | [−1, −0.17) | Multifractal |

| Global | −0.40 | [−1, −0.71) | Non-Multifractal | ||

| NASDAQ | 2.81 | Local | −0.44 | [−1, −0.06) | Multifractal |

| Global | −0.79 | [−1, −0.52) | Multifractal | ||

| USD/JPY | 3.50 | Local | −0.33 | [−1, −0.17) | Multifractal |

| Global | −0.80 | [−1, −0.76) | Multifractal | ||

| Gold Futures | 3.48 | Local | 0.22 | [−1, −0.17) | Non-Multifractal |

| Global | −0.48 | [−1, −0.71) | Non-Multifractal |

| Financial Asset | Tail Index | Test | Test Statistics | Rejection Region | Test Result (Local) |

|---|---|---|---|---|---|

| S&P500 | 3.20 | Local | 0.78 | [−1, −0.11) | Non-Multifractal |

| Global | 0.93 | [−1, −0.66) | Non-Multifractal | ||

| NASDAQ | 3.84 | Local | −0.61 | [−1, −0.22) | Multifractal |

| Global | −0.93 | [−1, −0.84) | Multifractal | ||

| USD/JPY | 3.33 | Local | −0.28 | [−1, −0.17) | Multifractal |

| Global | −0.72 | [−1, −0.70) | Multifractal | ||

| Gold Futures | 1.36 | Local | −0.11 | [−1, −0.72) | Non-Multifractal |

| Global | 0.11 | [−1, −0.9979) | Non-Multifractal |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Jiang, C.; Dev, P.; Maller, R.A. A Hypothesis Test Method for Detecting Multifractal Scaling, Applied to Bitcoin Prices. J. Risk Financial Manag. 2020, 13, 104. https://doi.org/10.3390/jrfm13050104

Jiang C, Dev P, Maller RA. A Hypothesis Test Method for Detecting Multifractal Scaling, Applied to Bitcoin Prices. Journal of Risk and Financial Management. 2020; 13(5):104. https://doi.org/10.3390/jrfm13050104

Chicago/Turabian StyleJiang, Chuxuan, Priya Dev, and Ross A. Maller. 2020. "A Hypothesis Test Method for Detecting Multifractal Scaling, Applied to Bitcoin Prices" Journal of Risk and Financial Management 13, no. 5: 104. https://doi.org/10.3390/jrfm13050104