Contagion Risks in Emerging Stock Markets: New Evidence from Asia and Latin America

Abstract

:1. Introduction

2. Review of Studies

3. Methodology

3.1. Dynamic Conditional Correlation Model

- is a k.1 column vector of residual returns of .

- is a k.k diagonal matrix of the time varying standard deviations of residual returns.

- is a column vector of standardized residual returns.

- is a k.k matrix of time-varying covariance.

- is a k.k matrix of time-varying conditional correlations.

- is the unconditional covariance of the standardized residuals resulting from the univariate GARCH(1,1) equation.

- and are positive parameters which satisfy + < 1.

3.2. Contagion Tests

- : =

- : >

4. Data and Descriptive Statistics

5. Empirical Findings

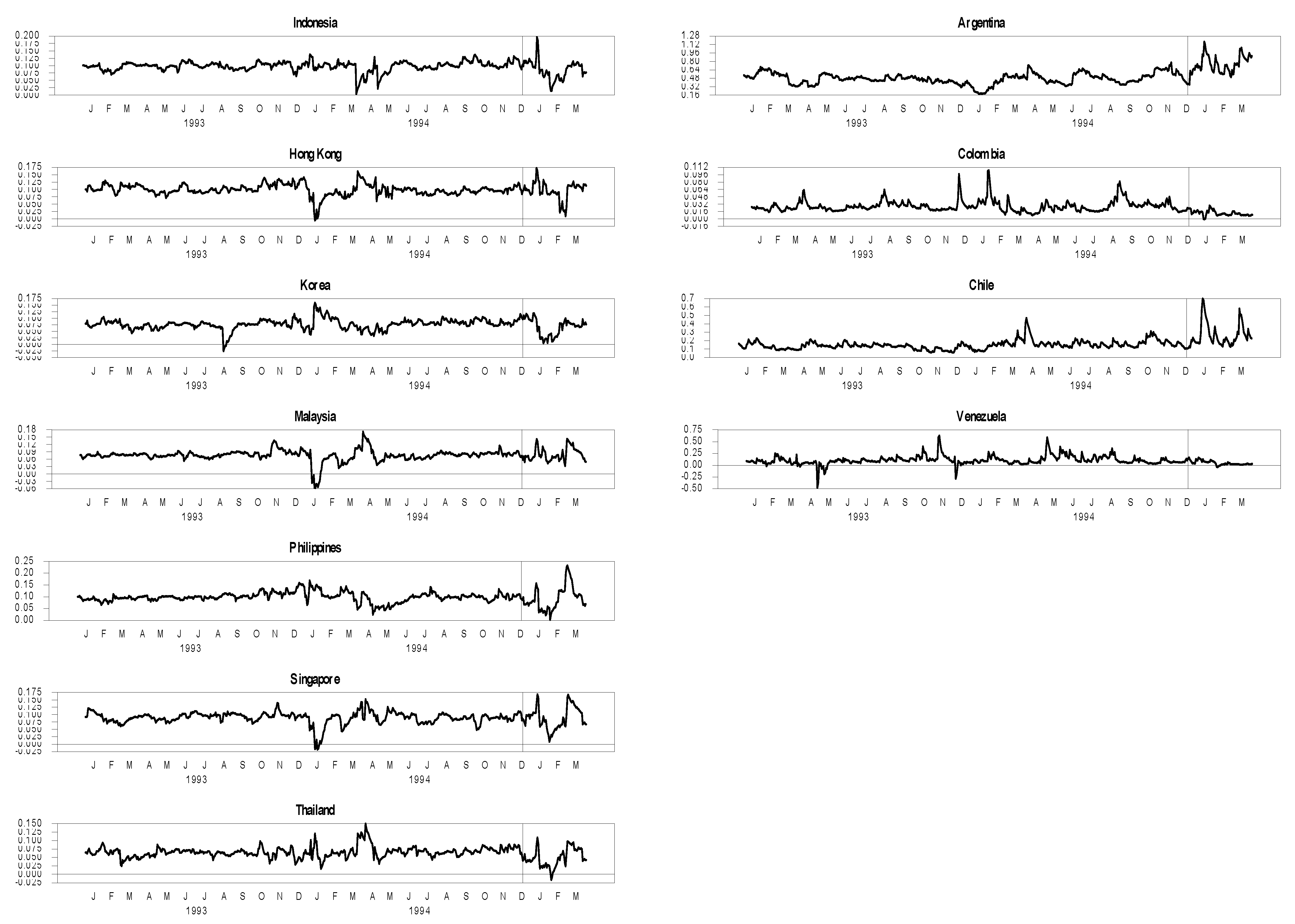

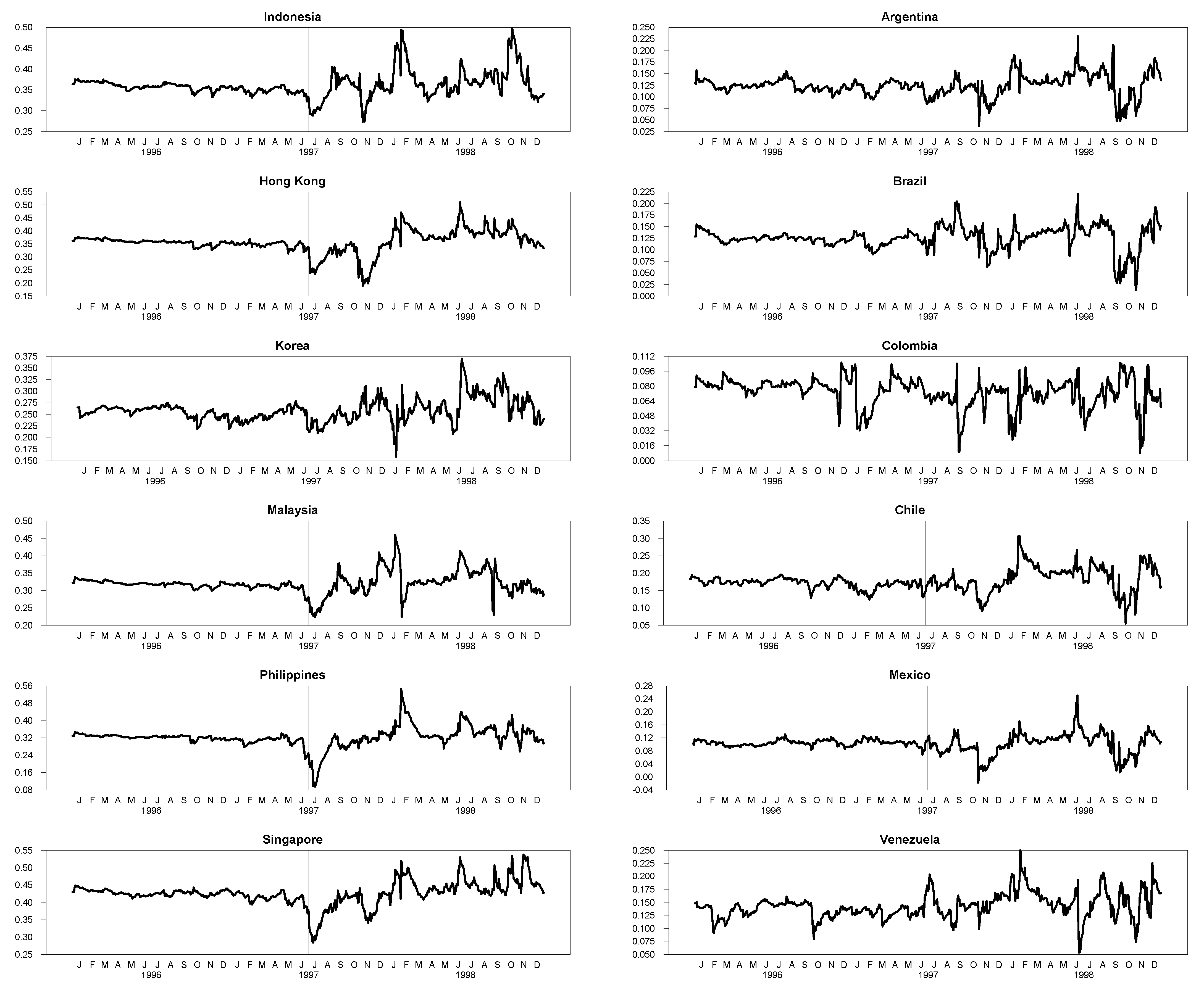

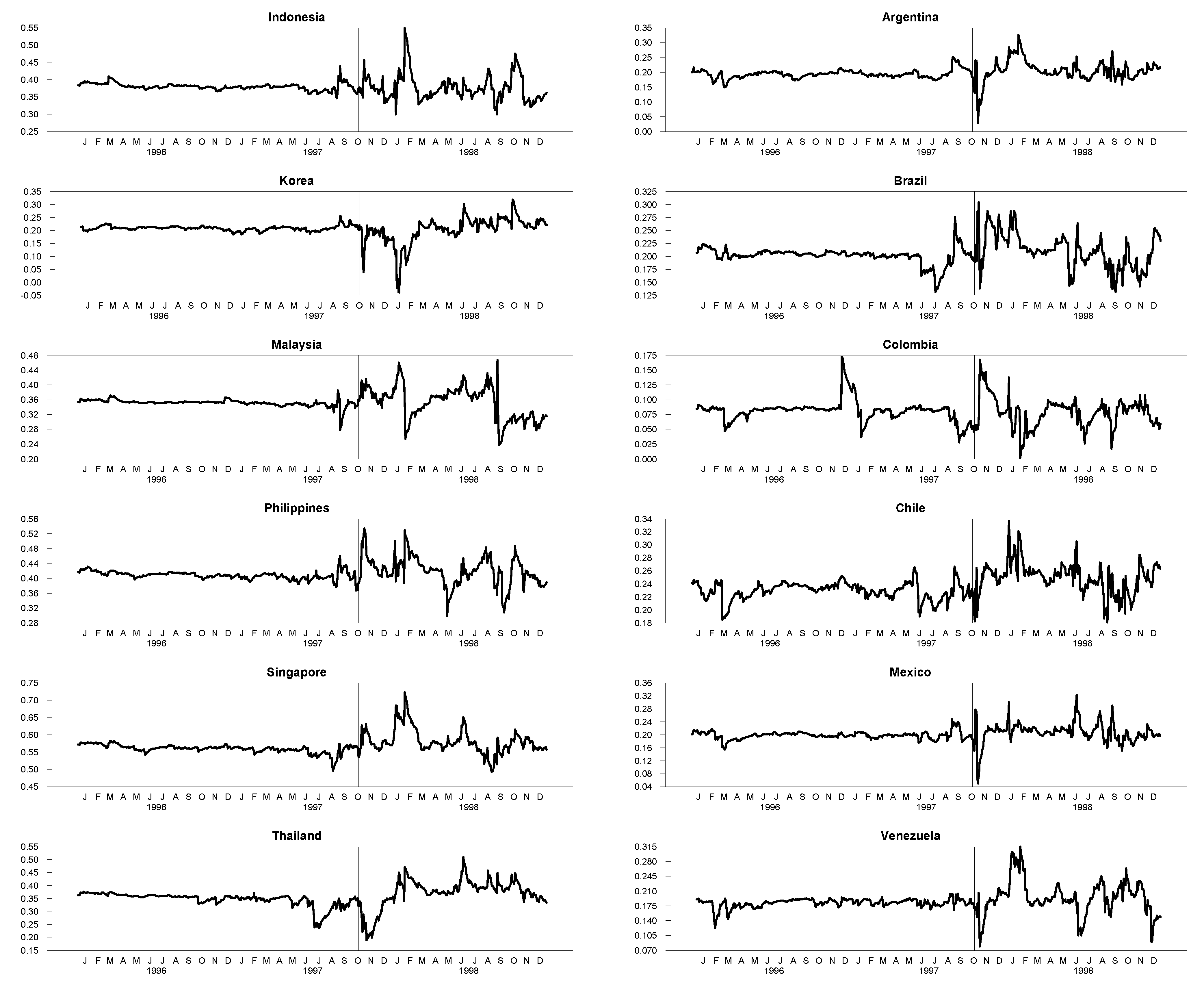

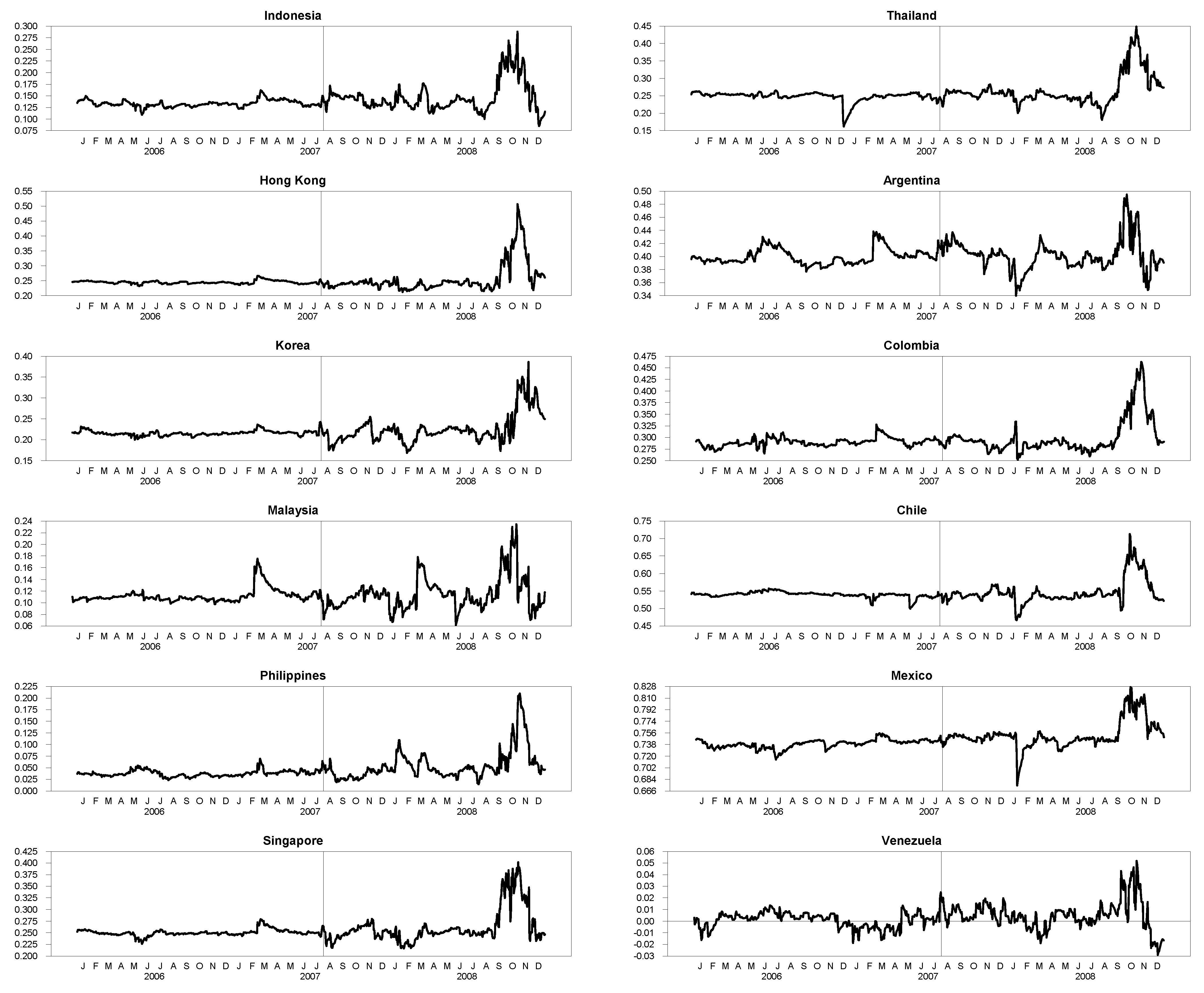

5.1. Dynamic Conditional Correlations

5.2. Contagion Tests

5.2.1. Contagion during the Mexican “Tequila” Crisis

5.2.2. Contagion during the Asian “flu” Crisis

5.2.3. Contagion during the US Subprime Crisis

6. Conclusions

Funding

Conflicts of Interest

References

- Baig, Taimur, and Ilan Goldfajn. 1999. Financial markets contagion in the Asian crisis. IMF Staff Papers 46: 167–95. [Google Scholar]

- Billio, Monica, and Loriana Pelizzon. 2003. Contagion and interdependence in stock markets: Have they been misdiagnosed? Journal of Economics and Business 55: 405–26. [Google Scholar] [CrossRef]

- Bodart, Vincent, and Bertrand Candelon. 2009. Evidence of interdependence and contagion using a frequency domain framework. Emerging Markets Review 10: 140–50. [Google Scholar] [CrossRef]

- Bollerslev, Tim, Ray Y. Chou, and Kenneth F. Kroner. 1992. ARCH modeling in finance: A review of the theory and empirical evidence. Journal of Econometrics 52: 5–59. [Google Scholar] [CrossRef]

- Boyer, Brian H., Michael S. Gibson, and Mico Loretan. 1997. Pitfalls in Tests for Changes in Correlations; International Finance Discussion Papers 597; Washington, DC: Board of Governors of the Federal Reserve System (U.S.).

- Calvo, Sara, and Carmen Reinhart. 1996. Capital Flows to Latin America: Is There Evidence of Contagion Effects? World Bank Policy Research Paper 1619. Washington, DC: World Bank. [Google Scholar]

- Chiang, Thomas C., Bang Nam Jeon, and Huimin Li. 2007. Dynamic correlation analysis of financial contagion: Evidence from Asian markets. Journal of International Money and Finance 26: 1206–28. [Google Scholar] [CrossRef]

- Cho, Jang Hyung, and Ali M. Parhizgari. 2008. East Asian financial contagion under DCC-GARCH. International Journal of Banking and Finance 6: 17–30. [Google Scholar]

- Corsetti, Giancarlo, Marcello Pericoli, and Massimo Sbracia. 2005. ‘Some contagion, some interdependence’: More pitfalls in tests of financial contagion. Journal of International Money and Finance 24: 1177–99. [Google Scholar] [CrossRef]

- Dornbusch, Rudiger, Yung Chul Park, and Stijn Claessens. 2001. Contagion: How it spreads and how it can be stopped? In International Cinancial Contagion. Boston: Klwer Academic Publishers. [Google Scholar]

- Engle, Robert F. 2002. Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. Journal of Business and Economics Statistics 20: 339–50. [Google Scholar] [CrossRef]

- Engle, Robert F., and Kevin Sheppard. 2001. Theoretical and Empirical Properties of Dynamic Conditional Correlation Multivariate GARCH. NBER Working Paper No. 8554. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Forbes, Kristin J., and Roberto Rigobon. 2002. No contagion, only interdependence: Measuring stock market comovements. Journal of Finance 57: 2223–61. [Google Scholar] [CrossRef]

- Forbes, Kristin, and Roberto Rigobon. 2000. Contagion in Latin America: Definitions, Measurements and Policy Implications. NBER Working Paper, No. 7885. Cambridge: National Bureau of Economic Research, September. [Google Scholar]

- Forbes, Kristin, and Roberto Rigobon. 2001. Measuring contagion: Conceptual and empirical. In International Fiancial Contagion. Boston: Klwer Academic Publishers. [Google Scholar]

- Horta, Paulo, Carlos Mendes, and Isabel Vieira. 2008. Contagion Effects of the U.S. Subprime Crisis on Developped Countries. CEFAGE-UE Working Paper No. 2008/08. Évora: University of Evora. [Google Scholar]

- Kaminsky, Graciela L., and Carmen Reinhart. 2000. On crises, contagion, and confusion. Journal of International Economics 51: 145–68. [Google Scholar] [CrossRef]

- King, Mervyn A., and Sushil Wadhwani. 1990. Transmission of volatility between stock markets. Review of Financial Studies 3: 5–33. [Google Scholar] [CrossRef]

- Kumar, Manmohan S., and Avinash Persaud. 2001. Pure contagion and investors’ shifting risk appetite: Analytical issues and empirical evidence. International Finance 5: 401–36. [Google Scholar] [CrossRef]

- Longin, Francois, and Bruno Solnik. 1995. Is the correlation in international equity returns constant: 1960–1990? Journal of International Money and Finance 14: 3–26. [Google Scholar] [CrossRef]

- Masson, Paul. 1998. Contagion: Monsoonal Effects, Spillovers, and Jumps between Multiple Equilibra. IMF Working Paper 98/142. Washington, DC: International Monetary Fund. [Google Scholar]

- Moser, Thomas. 2003. What is international financial contagion? International Finance 6: 157–78. [Google Scholar] [CrossRef]

- Naoui, Kamel, Naoufel Liouane, and Salem Brahim. 2010a. A dynamic conditional correlation analysis of financial contagion: The case of the subprime credit crisis. International Journal of Economics and Finance 2: 85–96. [Google Scholar] [CrossRef]

- Pericoli, Marcello, and Massimo Sbracia. 2003. A primer on financial contagion. Journal of Economic Surveys 17: 571–608. [Google Scholar] [CrossRef]

- Ramchand, Latha, and Raul Susmel. 1998. Volatility and cross correlation across major stock markets. Journal of Empirical Finance 5: 397–416. [Google Scholar] [CrossRef]

| 1. | The interdependence term here refers to a high level of market comovement in all periods. |

| 2. | See Pericoli and Sbracia (2003) for a review of contagion definition. |

| 3. | See Dornbusch et al. (2001). |

| 4. | See Forbes and Rigobon (2001). |

| 5. | Problem raised by Forbes and Rigobon (2002) as discussed above. |

| 6. | Lehman Brothers is the fourth largest U.S. Investment Bank, which filed for bankruptcy on 15 September 2008. |

| 7. | This result is consistent with the work of Cho and Parhizgari (2008). |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Stable Period 1 January 1993–16 December 1994 | Turnoil Period 19 December 1994–31 March 1995 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Mean | Std Dev | Skewness | Kurtosis | N | Mean | Std Dev | Skewness | Kurtosis | N | |

| Asian emerging markets | ||||||||||

| Indonesia | 0.1004 | 0.9222 | −0.4486 *** | 2.6498 *** | 511 | 0.0150 | 1.0549 | −0.6917 ** | 0.9270 | 75 |

| Hong Kong | 0.0802 | 1.5790 | −0.2401 ** | 1.7596 *** | 511 | 0.0528 | 1.7043 | 0.1988 | 0.9235 | 75 |

| Korea | 0.0929 | 1.2632 | 0.1009 | 1.1744 *** | 511 | −0.0995 | 1.3775 | −0.2445 | 0.6534 | 75 |

| Malaysia | 0.0811 | 1.4140 | 0.0312 | 7.9182 *** | 511 | 0.0554 | 1.5279 | 0.5262 * | 1.9441 *** | 75 |

| Philippines | 0.1901 | 1.1940 | −0.0740 | 1.4608 *** | 511 | −0.1428 | 1.4014 | −0.6524 ** | 1.1863 ** | 75 |

| Singapore | 0.0548 | 0.8429 | 0.0260 | 3.6975 *** | 511 | −0.0522 | 1.0070 | −1.3139 *** | 5.2778 *** | 75 |

| Taiwan | 0.1695 | 1.8683 | 0.3141 *** | 2.2656 *** | 511 | −0.0700 | 1.2675 | 0.0863 | 1.9812 *** | 75 |

| Thailand | 0.1344 | 1.6338 | −0.1610 | 3.3274 *** | 511 | −0.0396 | 1.5237 | 0.0994 | 1.1044* | 75 |

| Latin American emerging markets | ||||||||||

| Argentina | 0.0628 | 1.7080 | −0.4579 *** | 1.7082 *** | 511 | −0.3181 | 3.4888 | 0.5977 ** | 1.2190 ** | 75 |

| Chile | 0.1474 | 0.9804 | −0.1968 * | 1.4879 *** | 511 | −0.0893 | 1.9833 | 0.8658 *** | 2.1619 *** | 75 |

| Colombia | 0.1092 | 0.8248 | 0.6607 *** | 4.2164 *** | 511 | 0.0963 | 0.7902 | 1.8254 *** | 4.5397 *** | 75 |

| Mexico | 0.0588 | 1.3187 | −0.0576 | 2.2076 *** | 511 | −0.2413 | 2.5392 | 0.2928 | 0.6904 | 75 |

| Venezuela | 0.1356 | 2.8743 | 0.8210 *** | 8.0160 *** | 511 | 0.0285 | 1.4287 | 1.3654 ** | 7.0395 ** | 75 |

| Stable Period 1 January 1996–1 July 1997 | Turmoil Period 2 July 1997–31 December 1998 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Mean | Std Dev | Skewness | Kurtosis | N | Mean | Std Dev | Skewness | Kurtosis | N | |

| Asian emerging markets | ||||||||||

| Indonesia | 0.0782 | 1.0492 | −0.3121 ** | 2.3480 *** | 392 | −0.0727 | 3.1918 | 0.2923 ** | 3.2094 *** | 392 |

| Hong Kong | 0.1164 | 1.0426 | −1.2222 | 8.9774 | 392 | −0.1301 | 2.7824 | 0.4175 | 5.8187 | 392 |

| Korea | −0.0467 | 1.3586 | 0.1910 | 0.7480 *** | 392 | −0.0060 | 3.3631 | 0.3847 *** | 1.1348 *** | 392 |

| Malaysia | 0.0225 | 0.8135 | −0.4775 *** | 2.6060 *** | 392 | −0.1452 | 3.3526 | 0.6484 *** | 12.4451 *** | 392 |

| Philippines | 0.0406 | 0.9691 | −0.1981 | 2.5731 *** | 392 | −0.0839 | 2.2471 | 0.2459 ** | 2.1380 *** | 392 |

| Singapore | −0.0264 | 0.80150 | −0.1321 | 0.6031 ** | 392 | −0.0665 | 1.8973 | 0.3777 *** | 3.6296 *** | 392 |

| Taiwan | 0.1674 | 1.3831 | −0.0006 | 3.6794 *** | 392 | −0.0752 | 1.7950 | −0.0360 | 1.4828 *** | 392 |

| Latin American emerging markets | ||||||||||

| Argentina | 0.0976 | 1.2867 | −0.1673 | 1.9277 *** | 392 | −0.0763 | 2.3432 | −0.5134 *** | 6.2535 *** | 392 |

| Brazil | 0.1766 | 0.9540 | 0.14830 | 3.4620 *** | 392 | −0.1811 | 2.4182 | −0.6825 *** | 3.1787 *** | 392 |

| Chile | 0.0252 | 0.6937 | 0.4481 *** | 0.5236 ** | 392 | −0.1179 | 1.1195 | 0.1355 | 3.4237 *** | 392 |

| Colombia | 0.0587 | 1.0545 | −0.7724 *** | 47.0383 *** | 392 | −0.0800 | 1.0778 | −0.0039 | 9.7246 *** | 392 |

| Mexico | 0.1178 | 0.9133 | 0.5029 *** | 1.6971 *** | 392 | −0.0380 | 1.7365 | 0.0213 | 7.6136 *** | 392 |

| Venezuela | 0.3457 | 1.6706 | 1.0121 *** | 3.7608 *** | 392 | −0.1866 | 2.7841 | 1.1492 *** | 12.5781 *** | 392 |

| Stable Period 1 January 1996–16 October 1997 | Turnoil Period 17 October 1997–31 December 1998 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Mean | Std Dev | Skewness | Kurtosis | N | Mean | Std Dev | Skewness | Kurtosis | N | |

| Asian emerging markets | ||||||||||

| Indonesia | 0.0166 | 1.4280 | 0.6768 *** | 12.7077 *** | 469 | −0.0178 | 3.3212 | 0.1758 | 2.8525 *** | 315 |

| Hong Kong | 0.0663 | 1.2338 | −0.7219 *** | 7.0780 *** | 469 | −0.1157 | 2.9568 | 0.4178 *** | 5.3991 *** | 315 |

| Korea | −0.1033 | 1.3825 | 0.0313 | 0.9223 *** | 469 | 0.0882 | 3.6760 | 0.3107 ** | 0.5446 * | 315 |

| Malaysia | −0.0367 | 1.2673 | 1.5841 *** | 25.3818 *** | 469 | −0.0981 | 3.5274 | 0.5284 *** | 12.0150 *** | 315 |

| Philippines | −0.0352 | 1.2483 | −0.3863 *** | 7.4819 *** | 469 | −0.0015 | 2.2680 | 0.2740 ** | 1.9341 *** | 315 |

| Singapore | −0.0393 | 0.9059 | −0.2921 ** | 1.8088 *** | 469 | −0.0572 | 2.0150 | 0.4080 *** | 3.3187 *** | 315 |

| Taiwan | 0.1163 | 1.4502 | −0.1110 | 2.5102 *** | 469 | −0.0584 | 1.8105 | 0.0031 | 1.9019 *** | 315 |

| Thailand | −0.1493 | 2.0219 | 0.6848 *** | 3.3557 *** | 469 | −0.1054 | 3.2393 | 0.7468 *** | 2.1230 *** | 315 |

| Latin American emerging markets | ||||||||||

| Argentina | 0.1020 | 1.2704 | −0.1831 | 1.7405 *** | 469 | −0.1255 | 2.5457 | −0.4468 *** | 5.2178 *** | 315 |

| Brazil | 0.1530 | 1.1524 | −0.3935 *** | 6.2960 *** | 469 | −0.2335 | 2.5350 | −0.6586 *** | 2.9229 *** | 315 |

| Chile | 0.0041 | 0.6880 | 0.4351 *** | 0.5212 ** | 469 | −0.1215 | 1.2074 | 0.1294 | 2.8595 *** | 315 |

| Colombia | 0.0850 | 0.9906 | −0.8211 *** | 50.7480 *** | 469 | −0.1530 | 1.1604 | 0.1292 | 8.7253 *** | 315 |

| Mexico | 0.1322 | 0.9512 | 0.3708 *** | 1.2385 *** | 469 | −0.0975 | 1.8516 | 0.0865 | 7.1560 *** | 315 |

| Venezuela | 0.3240 | 1.6112 | 0.9646 *** | 3.8058 *** | 469 | −0.2844 | 3.0353 | 1.1840 *** | 10.8894 *** | 315 |

| Stable Period 1 January 2006–31 July 2007 | Turnoil Period 1 July 2007–31 December 2008 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Mean | Std Dev | Skewness | Kurtosis | N | Mean | Std Dev | Skewness | Kurtosis | N | |

| Asian emerging markets | ||||||||||

| Indonesia | 0.1522 | 1.2398 | −0.7613 *** | 4.3101 *** | 411 | −0.1525 | 2.3802 | −0.4674 *** | 4.1386 *** | 371 |

| Hong Kong | 0.1202 | 0.9329 | −0.7289 *** | 2.4423 *** | 411 | −0.1491 | 2.5215 | 0.0562 | 3.1464 *** | 371 |

| Korea | 0.0724 | 1.0974 | −0.4801 *** | 1.3515 *** | 411 | −0.1397 | 2.2650 | −0.2754 ** | 4.6030 *** | 371 |

| Malaysia | 0.1043 | 0.7091 | −1.2220 *** | 7.4879 *** | 411 | −0.1226 | 1.2308 | −1.3304 *** | 10.6139 *** | 371 |

| Philippines | 0.1311 | 1.1670 | −0.863 *** | 5.8259 *** | 411 | −0.1711 | 1.7675 | −0.6680 *** | 5.8814 *** | 371 |

| Singapore | 0.1081 | 0.8867 | −0.9309 *** | 2.9231 *** | 411 | −0.1902 | 1.8069 | −0.1860 | 3.0287 *** | 371 |

| Taiwan | 0.0665 | 1.0303 | −0.8786 | 3.1950 *** | 411 | −0.1804 | 1.9659 | −0.0510 | 0.8381 *** | 371 |

| Thailand | 0.0488 | 1.5232 | −2.8566 *** | 53.3222 *** | 411 | −0.1798 | 2.1168 | −0.6096 *** | 5.6193 *** | 371 |

| Latin American emerging markets | ||||||||||

| Argentina | 0.0882 | 1.0504 | −0.9743 *** | 5.9111 *** | 411 | −0.1113 | 1.3972 | −0.0210 *** | 3.3975 *** | 371 |

| Brazil | 0.1365 | 1.2836 | −0.3056 ** | 1.5830 *** | 411 | −0.1121 | 2.4737 | −0.0278 | 2.9948 *** | 371 |

| Chile | 0.1152 | 0.7406 | −1.1789 *** | 5.9941 *** | 411 | −0.0788 | 1.3721 | 0.5007 *** | 7.4257 *** | 371 |

| Colombia | 0.0333 | 1.6017 | −0.0702 | 12.4863 *** | 411 | −0.0312 | 1.4454 | −0.4301 *** | 6.7485 *** | 371 |

| Mexico | 0.1359 | 1.1573 | −0.1752 | 3.0393 *** | 411 | −0.0828 | 1.7243 | 0.3276 ** | 3.6350 *** | 371 |

| Venezuela | 0.1247 | 1.5929 | −3.0199 *** | 33.0170 *** | 411 | −0.0758 | 0.6730 | 0.5511 *** | 3.1822 *** | 371 |

| US stock market | ||||||||||

| US | 0.0397 | 0.6747 | −0.5250 *** | 2.5716 *** | 411 | −0.1268 | 2.2007 | −0.1491 | 5.2257 *** | 371 |

| Parameter | ||||||

| Asian emerging markets | ||||||

| Indonesia | 0.0629 *** | 0.2630 *** | 0.2332 *** | 0.4799 *** | 0.2687 *** | 0.2094 ** |

| (2.6687) | (8.7874) | (6.6515) | (6.9350) | (5.2765) | (2.4816) | |

| Korea | −0.0016 | 0.0926 *** | 0.0944 | 0.0748 *** | 0.0586 *** | 0.8927 *** |

| (−0.0453) | (2.8503) | (1.6300) | (2.8749) | (4.2400) | (34.4931) | |

| Malaysia | 0.0466 ** | 0.0656 *** | 0.3697 *** | 0.0417 *** | 0.0752 *** | 0.8974 *** |

| (1.9780) | (2.8854) | (8.9527) | (3.1666) | (5.2569) | (44.3229) | |

| Philippines | 0.0709 ** | 0.1821 *** | 0.2813 *** | 0.0176 *** | 0.0458 *** | 0.9394 *** |

| (2.3330) | (5.7971) | (5.2114) | (2.7262) | (4.3183) | (72.2894) | |

| Singapore | 0.0113 | −0.0098 | 0.2945 *** | 0.1085 *** | 0.1297 *** | 0.7113 *** |

| (0.6121) | (−0.3630) | (8.4910) | (4.8621) | (5.0067) | (15.1351) | |

| Taiwan | 0.0413 | −0.0324 | 0.2365 *** | 0.1313 *** | 0.0628 *** | 0.8874 *** |

| (0.8180) | (−1.0263) | (2.7341) | (3.1662) | (5.1356) | (38.8341) | |

| Hong Kong | 0.0502 * | −0.0493 * | 0.7935 *** | 0.0117 *** | 0.0444 *** | 0.9503 *** |

| (1.7065) | (−1.7108) | (18.8004) | (2.8495) | (7.5667) | (168.3592) | |

| Thailand | 0.0211 | 0.0780 ** | 0.4172 *** | 0.0372 ** | 0.0674 *** | 0.9193 *** |

| (0.6028) | (2.5041) | (6.6277) | (2.1545) | (4.9942) | (50.8437) | |

| Latin American emerging markets | ||||||

| Argentina | 0.0554 | 0.0738 *** | 0.3022 *** | 0.1122 *** | 0.0865 *** | 0.8827 *** |

| (1.2221) | (2.6945) | (4.0964) | (3.1756) | (5.2608) | (41.3832) | |

| Chile | 0.0201 | 0.2549 *** | 0.0988 ** | 0.0595 *** | 0.1957 *** | 0.7527 *** |

| (0.8533) | (8.9928) | (2.3914) | (5.4924) | (8.2280) | (28.7125) | |

| Colombia | −0.0175 | 0.4280 *** | −0.0162 | 0.0700 *** | 0.2050 *** | 0.6914 *** |

| (−1.1340) | (11.8014) | (−0.6823) | (7.4205) | (7.5636) | (21.9471) | |

| Venezuela | 0.0334 | 0.1197 *** | 0.1559 * | 0.4403 *** | 0.3591 *** | 0.6256 *** |

| (0.5934) | (3.7851) | (1.7650) | (5.1880) | (7.3100) | (15.6333) | |

| Mexico | 0.0748 ** | 0.1240 *** | 0.0867 | 0.0540 *** | 0.0772 *** | 0.8957 *** |

| (2.1861) | (4.4517) | (1.4082) | (2.9099) | (4.7209) | (41.8666) | |

| Parameter | ||||||

| Asian emerging markets | ||||||

| Indonesia | 0.0738 | 0.1152 *** | 0.4308 *** | 0.0355 *** | 0.1043 *** | 0.9056 *** |

| (1.6114) | (5.2387) | (9.4292) | (2.9913) | (7.1851) | (79.3786) | |

| Hong Kong | 0.1029 *** | 0.0702 *** | 0.6562 *** | 0.0500 *** | 0.1086 *** | 0.8900 *** |

| (2.9622) | (−2.6696) | (16.3620) | (3.7141) | (6.8789) | (58.8206) | |

| Korea | 0.0153 | 0.0932 *** | 0.2868 *** | 0.0276 ** | 0.0725 *** | 0.9281 *** |

| (0.2672) | (2.7627) | (5.1863) | (1.9922) | (6.8351) | (89.4653) | |

| Malaysia | 0.0484 * | 0.0590 ** | 0.3088 *** | 0.0128 *** | 0.1229 *** | 0.8934 *** |

| (1.6858) | (1.9972) | (8.1332) | (3.2957) | (8.8803) | (97.8157) | |

| Philippines | 0.0494 | 0.1459 *** | 0.3143 *** | 0.1023 *** | 0.2091 *** | 0.7831 *** |

| (1.4304) | (4.9254) | (8.4482) | (5.1229) | (7.7183) | (32.4725) | |

| Singapore | 0.0495 | 0.0086 | 0.3732 *** | 0.0344 *** | 0.0715 *** | 0.9202 *** |

| (1.5878) | (−0.3252) | (9.9155) | (3.0880) | (4.9210) | (58.3597) | |

| Taiwan | 0.0989 ** | 0.0259 | 0.2771 *** | 0.1180 ** | 0.0662 *** | 0.8918 *** |

| (2.0661) | (0.7897) | (6.2478) | (2.5499) | (4.3803) | (33.6636) | |

| Thailand | 0.0321 | 0.0344 | 0.3467 *** | 0.0913 *** | 0.1073 *** | 0.8932 *** |

| (−0.5486) | (1.0719) | (4.8863) | (2.5801) | (6.7971) | (61.1801) | |

| Latin American emerging markets | ||||||

| Argentina | 0.0967 ** | 0.0681 *** | 0.0867 ** | 0.2440 *** | 0.1284 *** | 0.8076 *** |

| (2.4066) | (2.6343) | (2.1024) | (5.6291) | (7.4994) | (35.4268) | |

| Brazil | 0.1461 *** | 0.0513 ** | 0.1783 *** | 0.1234 *** | 0.1427 *** | 0.8349 *** |

| (4.1852) | (2.1644) | (4.6334) | (4.8453) | (6.7531) | (37.5869) | |

| Chile | 0.0207 | 0.2515 *** | 0.0852 *** | 0.0241 *** | 0.0764 *** | 0.8968 *** |

| (0.8866) | (9.0373) | (3.8795) | (3.4661) | (5.2825) | (51.0718) | |

| Colombia | 0.0128 | 0.2275 *** | 0.0769 *** | 0.1084 *** | 0.2233 *** | 0.7303 *** |

| (−0.8760) | (9.8500) | (3.9644) | (6.2665) | (5.9507) | (21.8016) | |

| Mexico | 0.1073 *** | 0.0873 *** | 0.1191 *** | 0.0968 *** | 0.1067 *** | 0.8522 *** |

| (3.2568) | (3.4749) | (3.4945) | (3.9108) | (6.5547) | (38.7641) | |

| Venezuela | 0.0253 | 0.2219 *** | 0.2545 *** | 0.2062 *** | 0.2084 *** | 0.7679 *** |

| (0.4845) | (6.6611) | (4.5883) | (4.6099) | (6.4188) | (26.0453) | |

| Parameter | ||||||

| Asian emerging markets | ||||||

| Indonesia | 0.2265 *** | −0.0371 | 0.4390 *** | 0.1915 *** | 0.1371 *** | 0.8175 *** |

| (5.7232) | (−1.3703) | (14.8630) | (2.7140) | (3.9892) | (16.3024) | |

| Korea | 0.1426 *** | −0.0591 *** | 0.4602 *** | 0.0451 *** | 0.0677 *** | 0.9227 *** |

| (4.2410) | (−2.7507) | (16.6541) | (3.7266) | (6.3664) | (80.1653) | |

| Malaysia | 0.1051 *** | 0.0245 | 0.2148 *** | 0.0277 *** | 0.1524 *** | 0.8425 *** |

| (5.5955) | (0.9712) | (15.0682) | (3.1640) | (6.1689) | (30.6932) | |

| Philippines | 0.1073 *** | 0.0432 ** | 0.4816 *** | 0.1307 *** | 0.2038 *** | 0.7557 *** |

| (3.6841) | (2.0841) | (24.7262) | (4.1638) | (7.1927) | (24.0974) | |

| Singapore | 0.1526 *** | −0.1309 *** | 0.4332 *** | 0.0370 *** | 0.0719 *** | 0.9157 *** |

| (5.7167) | (−7.1061) | (19.0871) | (5.9154) | (9.3246) | (110.2176) | |

| Taiwan | 0.1129 *** | −0.0351 | 0.4178 *** | 0.0308 *** | 0.0490 *** | 0.9431 *** |

| (3.2060) | (−1.4837) | (16.4201) | (3.0436) | (5.1028) | (80.4188) | |

| Hong Kong | 0.1726 *** | −0.0933 *** | 0.5775 *** | 0.0474 *** | 0.0915 *** | 0.9057 *** |

| (5.4715) | (−5.1091) | (21.4708) | (4.6845) | (8.9123) | (92.2507) | |

| Thailand | 0.1680 *** | −0.0329 | 0.3372 *** | 1.0153 *** | 0.2215 *** | 0.4901 *** |

| (4.2402) | (−1.2364) | (11.6561) | (4.5281) | (4.2943) | (4.7025) | |

| Latin American emerging markets | ||||||

| Argentina | 0.1442 *** | 0.0375 | 0.1114 *** | 0.1799 *** | 0.0746 *** | 0.8276 *** |

| (4.0163) | (1.1469) | (4.2305) | (4.9710) | (4.8060) | (27.1994) | |

| Brazil | 0.2432 *** | −0.1042 *** | 0.1159 *** | 0.0944 *** | 0.0599 *** | 0.9090 *** |

| (6.2098) | (−5.2976) | (3.4103) | (4.1900) | (6.3348) | (62.2301) | |

| Chile | 0.1276 *** | 0.0995 *** | 0.0496 *** | 0.0650 *** | 0.1224 *** | 0.8094 *** |

| (5.6065) | (3.8369) | (2.9036) | (5.0398) | (6.9301) | (31.73603) | |

| Colombia | 0.1238 *** | 0.0370 | 0.1040 *** | 0.1820 *** | 0.2388 *** | 0.6475 *** |

| (4.2682) | (1.0867) | (5.4842) | (7.4010) | (8.2245) | (20.6911) | |

| Mexico | 0.1784 *** | −0.0144 | 0.0521 *** | 0.0569 *** | 0.0611 *** | 0.9105 *** |

| (5.7761) | (−0.6505) | (1.8097) | (4.2185) | (6.6728) | (67.41723) | |

| Venezuela | −0.0111 | 0.1535 *** | 0.0535 *** | 0.1026 *** | 0.5049 *** | 0.5477 *** |

| (−0.7179) | (5.7888) | (4.4745) | (5.8995) | (9.9013) | (14.22591) | |

| US | 0.0946 *** | −0.1055 *** | 0.0199 *** | 0.0823 *** | 0.9067 *** | |

| (3.7963) | (−3.8855) | (4.8415) | (8.6645) | (88.7960) | ||

| Stable Period 1 January 1993–16 December 1994 | Turnoil Period 19 December 1994–31 March 1995 | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Mean | Std Dev | N | Mean | Std Dev | N | Mean Increase (%) | t Statictis | Contagion | |

| Asian emerging markets | |||||||||

| Korea | 0.0775 | 0.0197 | 511 | 0.0668 | 0.0316 | 75 | −13.7570 | −2.8409 | N |

| Malaysia | 0.0762 | 0.0235 | 511 | 0.0802 | 0.0261 | 75 | 5.2683 | 1.2577 | N |

| Philippines | 0.0989 | 0.0198 | 511 | 0.0933 | 0.0509 | 75 | −5.6818 | −0.9455 | N |

| Singapore | 0.0897 | 0.0202 | 511 | 0.0891 | 0.0377 | 75 | −0.6939 | −0.1401 | N |

| Taiwan | 0.0425 | 0.0153 | 511 | 0.0355 | 0.0370 | 75 | −16.4346 | −1.6127 | N |

| Thailand | 0.0659 | 0.0156 | 511 | 0.0491 | 0.0274 | 75 | −25.5032 | −5.1963 | N |

| Latin American emerging markets | |||||||||

| Argentina | 0.4734 | 0.6880 | 511 | 0.7406 | 0.1717 | 75 | 56.4643 | 13.1390 | C *** |

| Chile | 0.1494 | 0.3865 | 511 | 0.2638 | 0.1381 | 75 | 76.5546 | 7.1045 | C *** |

| Colombia | 0.0279 | 0.1669 | 511 | 0.0126 | 0.0056 | 75 | −54.8510 | −18.0838 | N |

| Venezuela | 0.1070 | 0.3271 | 511 | 0.0490 | 0.0456 | 75 | −54.1615 | −8.6066 | N |

| Stable Period 1 January 1996–1 July 1997 | Turnoil Period 2 July 1997–31 December 1998 | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Mean | Std Dev | N | Mean | Std Dev | N | Mean Increase (%) | t Statictis | Contagion | |

| Asian emerging markets | |||||||||

| Indonesia | 0.3559 | 0.0097 | 392 | 0.3673 | 0.0411 | 392 | 3.2073 | 5.3562 | C *** |

| Hong Kong | 0.3547 | 0.0116 | 392 | 0.3593 | 0.0586 | 392 | 1.2997 | 1.5284 | C * |

| Korea | 0.2529 | 0.0129 | 392 | 0.2640 | 0.0314 | 392 | 4.3660 | 6.4443 | C *** |

| Malaysia | 0.3175 | 0.0092 | 392 | 0.3252 | 0.0404 | 392 | 2.4180 | 3.6650 | C *** |

| Philippines | 0.3182 | 0.0166 | 392 | 0.3266 | 0.0615 | 392 | 2.6663 | 2.6372 | C *** |

| Singapore | 0.4230 | 0.0120 | 392 | 0.4298 | 0.0472 | 392 | 1.6002 | 2.7536 | C *** |

| Taiwan | 0.1475 | 0.0001 | 392 | 0.1665 | 0.0015 | 392 | 12.8759 | 9.2121 | C *** |

| Latin American emerging markets | |||||||||

| Argentina | 0.1228 | 0.0112 | 392 | 0.1267 | 0.0302 | 392 | 3.1683 | 2.3918 | C *** |

| Brazil | 0.1231 | 0.0108 | 392 | 0.1290 | 0.0338 | 392 | 4.8054 | 3.2968 | C *** |

| Chile | 0.1714 | 0.0140 | 392 | 0.1854 | 0.0406 | 392 | 8.1982 | 6.4719 | C *** |

| Colombia | 0.0784 | 0.0126 | 392 | 0.0688 | 0.0172 | 392 | −12.2519 | −8.9302 | N |

| Mexico | 0.1045 | 0.0088 | 392 | 0.1012 | 0.0365 | 392 | −3.1670 | −1.7448 | N |

| Venezuela | 0.1341 | 0.0142 | 392 | 0.1513 | 0.0287 | 392 | 12.8308 | 10.6444 | C *** |

| Stable Period 1 January 1996–16 October 1997 | Turnoil Period 17 October 1997–31 December1998 | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Mean | Std Dev | N | Mean | Std Dev | N | Mean Increase (%) | t Statictis | Contagion | |

| Asian emerging markets | |||||||||

| Indonesia | 0.3802 | 0.0094 | 469 | 0.3766 | 0.0379 | 315 | −0.9470 | −1.6517 | N |

| Korea | 0.2086 | 0.0089 | 469 | 0.2023 | 0.0518 | 315 | −3.0045 | −2.1265 | N |

| Malaysia | 0.3517 | 0.0090 | 469 | 0.3524 | 0.0442 | 315 | 0.1975 | 0.2748 | N |

| Philippines | 0.4080 | 0.0105 | 469 | 0.4199 | 0.0390 | 315 | 2.8981 | 5.2614 | C *** |

| Singapore | 0.5599 | 0.0118 | 469 | 0.5807 | 0.0362 | 315 | 3.7174 | 9.8697 | C *** |

| Taiwan | 0.2336 | 0.0157 | 469 | 0.2499 | 0.0486 | 315 | 6.9547 | 5.7406 | C *** |

| Thailand | 0.3468 | 0.0252 | 469 | 0.3723 | 0.0558 | 315 | 7.3427 | 7.5909 | C *** |

| Latin American emerging markets | |||||||||

| Argentina | 0.1939 | 0.0136 | 469 | 0.2056 | 0.0353 | 315 | 6.0226 | 5.6008 | C *** |

| Brazil | 0.2016 | 0.0153 | 469 | 0.2102 | 0.0342 | 315 | 4.3050 | 4.2230 | C *** |

| Chile | 0.2297 | 0.0131 | 469 | 0.2494 | 0.0237 | 315 | 8.5714 | 13.4455 | C *** |

| Colombia | 0.0811 | 0.0175 | 469 | 0.0781 | 0.0251 | 315 | −3.7808 | −1.8855 | N |

| Mexico | 0.1983 | 0.0111 | 469 | 0.2071 | 0.0306 | 315 | 4.4270 | 4.8752 | C *** |

| Venezuela | 0.1983 | 0.0111 | 469 | 0.2071 | 0.0306 | 315 | 4.4270 | 5.1917 | C *** |

| Stable Period 1 January 2006–31 July 2007 | Turnoil Period 1 August 2007–31 December 2008 | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Mean | Std Dev | N | Mean | Std Dev | N | Mean Increase (%) | t Statictis | Contagion | |

| Asian emerging markets | |||||||||

| Indonesia | 0.1337 | 0.0073 | 411 | 0.1468 | 0.0324 | 371 | 9.8224 | 7.6402 | C *** |

| Hong Kong | 0.2451 | 0.0053 | 411 | 0.2555 | 0.0494 | 371 | 4.2302 | 4.0262 | C *** |

| Korea | 0.2159 | 0.0058 | 411 | 0.2255 | 0.0350 | 371 | 4.4430 | 5.2203 | C *** |

| Malaysia | 0.1119 | 0.0116 | 411 | 0.1147 | 0.0283 | 371 | 2.4937 | 1.7711 | C ** |

| Philippines | 0.0378 | 0.0067 | 411 | 0.0548 | 0.0332 | 371 | 45.0331 | 9.6879 | C *** |

| Singapore | 0.2502 | 0.0069 | 411 | 0.2617 | 0.0371 | 371 | 4.6221 | 5.9123 | C *** |

| Taiwan | 0.1233 | 0.0056 | 411 | 0.1326 | 0.0274 | 371 | 7.4918 | 6.3644 | C *** |

| Thailand | 0.2485 | 0.0143 | 411 | 0.2651 | 0.0443 | 371 | 6.6707 | 6.8943 | C *** |

| Latin American emerging markets | |||||||||

| Argentina | 0.3998 | 0.6323 | 411 | 0.4016 | 0.0237 | 371 | 0.4424 | 1.2989 | C * |

| Brazil | 0.7134 | 0.8447 | 411 | 0.7146 | 0.0350 | 371 | 0.1562 | 0.6085 | N |

| Chile | 0.5401 | 0.7349 | 411 | 0.5463 | 0.0350 | 371 | 1.1536 | 3.3411 | C *** |

| Colombia | 0.2901 | 0.5386 | 411 | 0.2997 | 0.0386 | 371 | 3.3137 | 4.6816 | C *** |

| Mexico | 0.7391 | 0.8597 | 411 | 0.7523 | 0.0212 | 371 | 1.7914 | 11.5450 | C *** |

| Venezuela | 0.0008 | 0.0290 | 411 | 0.0048 | 0.0125 | 371 | 472.0685 | 5.4992 | C *** |

© 2018 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

TRAN, T.B.N. Contagion Risks in Emerging Stock Markets: New Evidence from Asia and Latin America. J. Risk Financial Manag. 2018, 11, 89. https://doi.org/10.3390/jrfm11040089

TRAN TBN. Contagion Risks in Emerging Stock Markets: New Evidence from Asia and Latin America. Journal of Risk and Financial Management. 2018; 11(4):89. https://doi.org/10.3390/jrfm11040089

Chicago/Turabian StyleTRAN, Thi Bich Ngoc. 2018. "Contagion Risks in Emerging Stock Markets: New Evidence from Asia and Latin America" Journal of Risk and Financial Management 11, no. 4: 89. https://doi.org/10.3390/jrfm11040089