On a New Corporate Bond Pricing Model with Potential Credit Rating Change and Stochastic Interest Rate

Abstract

:1. Introduction

2. The Derivation of the New Model

2.1. The Interest Rate Model

2.2. Further Value of a Corporation

3. The Mathematical Model

4. Stochastic Interest Rate in Vasicek Model

5. Simulation

5.1. Calibration

- The risk free interest rate r can be directly estimated from the market data. In practice, it can be taken by the rate of long term government bonds.

- can be estimated from the credit rating data and the firm’s balance sheet, where the proportion of the debt to the firm’s value is shown in different rating regions.

- The volatility of a firm’s asset value in different rating regions can be calibrated through the market quotes of the firm’s stock prices in different rating respectively. The details are shown as follows:

- Find equity volatilities from stock prices in the marketIf the firm is in ith rating, is defined as the kth day stock price. Then we denote by as the daily volatility, or the standard variance, of the stock price from N observations and an unbiased estimate of the variance rate per day are as follows :Then the volatility per annum is , where is the trading days in ith rating per annum.

- Estimate asset volatility from the equity volatility.Once obtained the equity values and volatilities, we can calibrate the firm’s volatility by using Merton’s model Merton (1974), where the relationship between firm’s volatility and equity one is given by the Black-Scholes formula. Then and can be estimated through the following equations:whereand D is the amount of debt to be paid at time T, and are the firm’s value and equity value at the initial time.

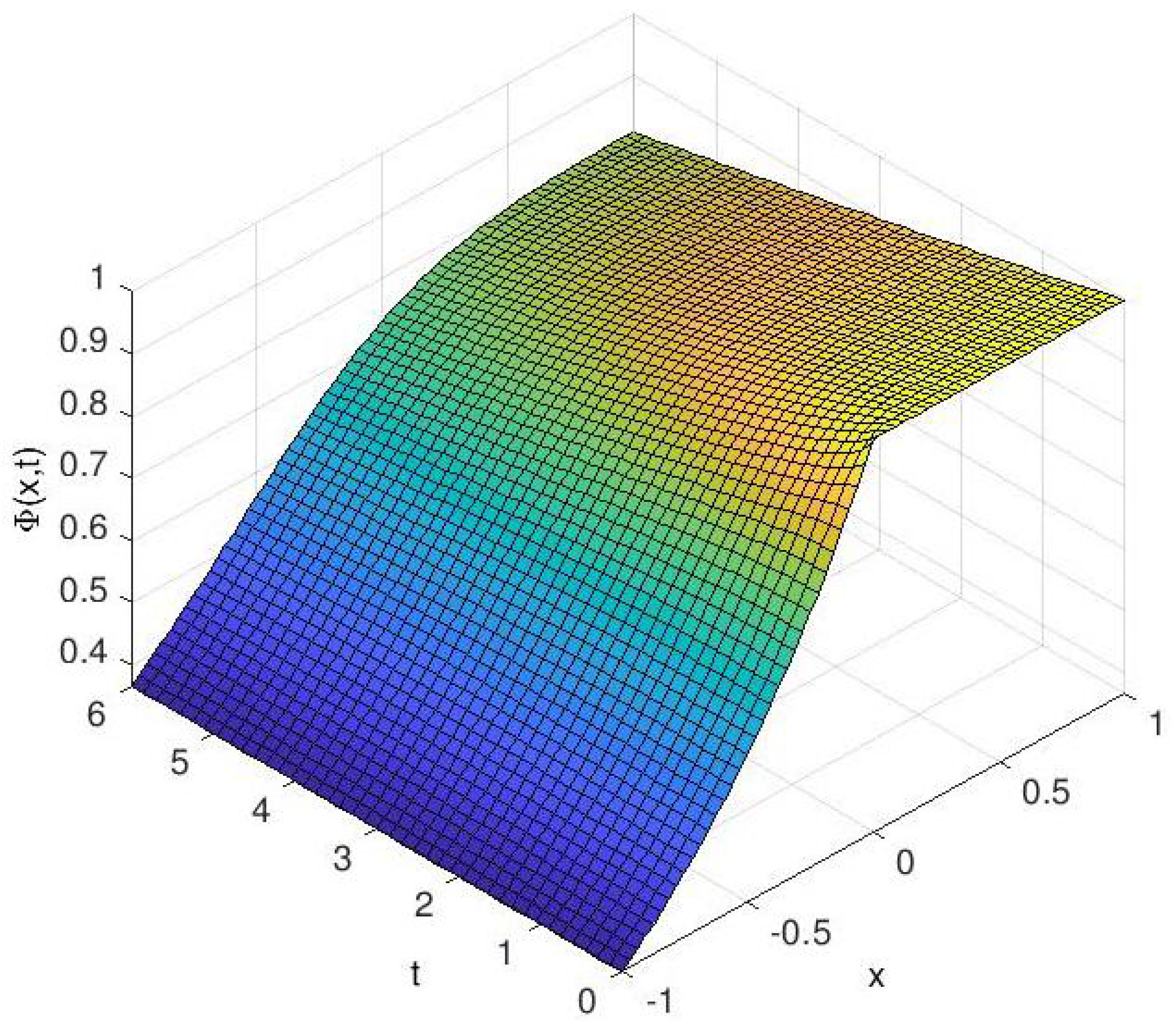

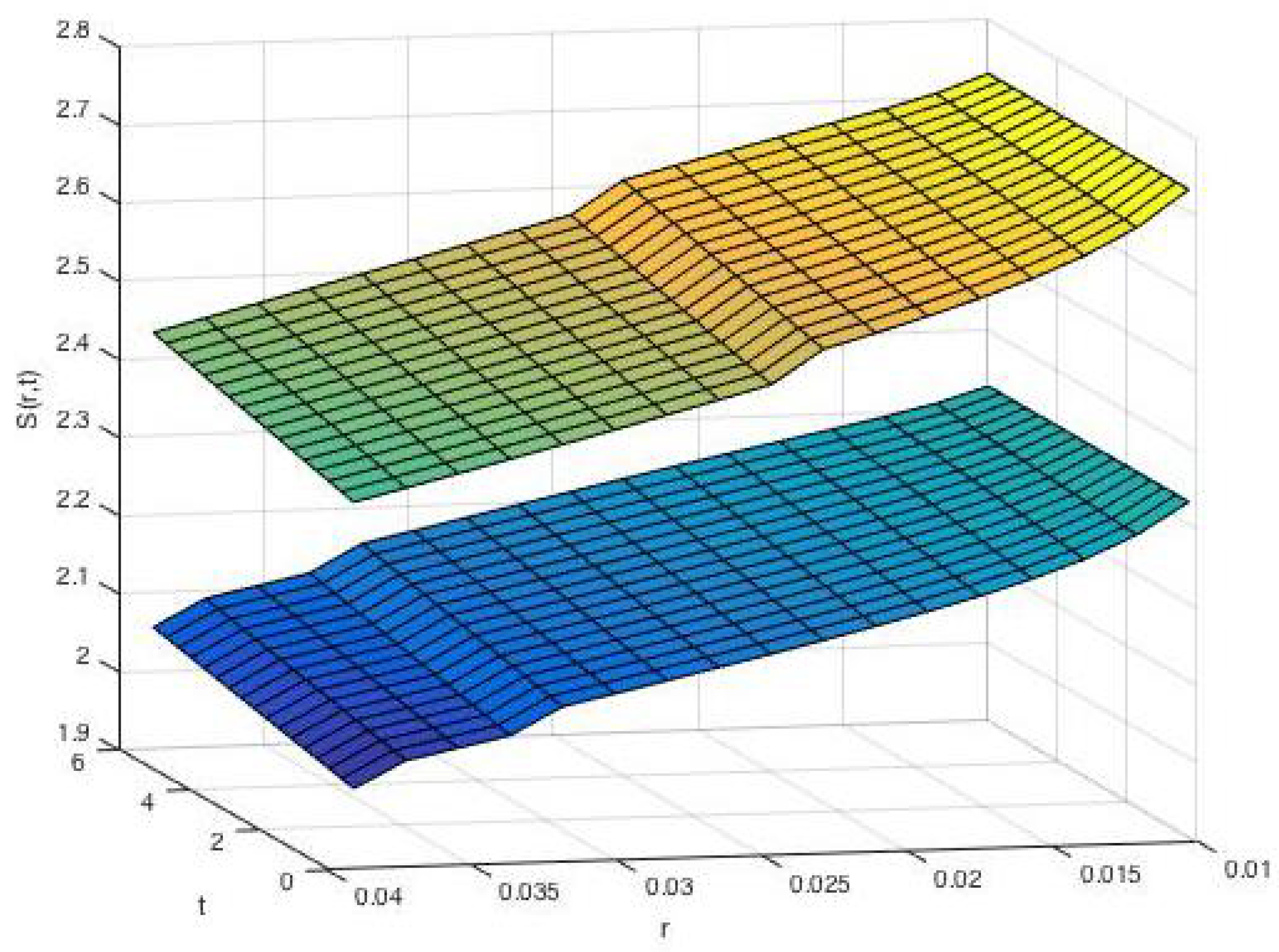

5.2. A Real Example

5.3. Migration Free Interfaces

6. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Black, Fischer, and John C. Cox. 1976. Some Effects of Bond Indenture Provisions. Journal of Finance 31: 351–67. [Google Scholar] [CrossRef]

- Bessembinder, Hendrik, Stacey Jacobsen, William Maxwell, and Kumar Venkataraman. 2018. Venkataraman, Capital Commitment and Illiquidity in Corporate Bonds. The Journal of Finance 73: 1665–61. [Google Scholar] [CrossRef]

- Briys, Eric, and François De Varenne. 1997. Valuing Risky Fixed Rate Debt: An Extension. Journal of Financial and Quantitative Analysis 32: 239–49. [Google Scholar] [CrossRef]

- Das, Sanjiv, and Peter Tufano. 1996. Pricing credit-sensitive debt when interest rates, credit ratings, and credit spreads are stochastic. Journal of Financial Engineering 5: 161–98. [Google Scholar]

- Dixit, Avinash K., and Robert S. Pindyck. 1994. Investment under Uncertainty. Princeton: Princeton University Press. [Google Scholar]

- Duffie, Darrell, and Kenneth J. Singleton. 1999. Modeling Term Structures of Defaultable Bonds. The Review of Financial Studies 12: 687–720. [Google Scholar] [CrossRef]

- Elton, Edwin J., Martin J. Gruber, Deepak Agrawal, and Christopher Mann. 2001. Explaining the Rate Spread on Corporate Bonds. The Journal of Finance 56: 247–77. [Google Scholar] [CrossRef]

- Hall, John. 1989. Options, Futures, and Other Derivatives. Upper Saddle River: Prentice-Hall, Inc. [Google Scholar]

- Hu, Bei, Jin Liang, and Yuan Wu. 2015. A Free Boundary Problem for Corporate Bond with Credit Rating Migration. Journal of Mathematical Analysis and Applications 428: 896–909. [Google Scholar] [CrossRef]

- Hurd, Tom, and Alexey Kuznetsov. 2007. Affine Markov chain models of multifirm credit migration. Journal of Credit Risk 3: 3–29. [Google Scholar] [CrossRef]

- Jarrow, Robert, and Stuart Turnbull. 1995. Pricing Derivatives on Financial Securities Subject to Credit Risk. Journal of Finance 50: 53–86. [Google Scholar] [CrossRef]

- Jarrow, Robert A., David Lando, and Stuart M. Turnbull. 1997. A Markov model for the term structure of credit risk spreads. Review of Financial Studies 10: 481–523. [Google Scholar] [CrossRef] [Green Version]

- Jiang, Lishang. 2005. Mathematical Modeling and Methods for Option Pricing. Singapore: World Scientific. [Google Scholar]

- Kang, Johnny, and Carolin E. Pflueger. 2015. Inflation Risk in Corporate Bonds. The Journal of Finance 70: 115–62. [Google Scholar] [CrossRef]

- Kariya, Takeaki, Yoko Tanokura, Hideyuki Takada, and Yoshiro Yamamura. 2016. Measuring Credit Risk of Individual Corporate Bonds in US Energy Sector. Asia-Pacific Finan Markets 23: 229–62. [Google Scholar] [CrossRef]

- Kenneth, J. Kopecky, Zhichuan Li, Timothy F. Sugrue, and Alan L. Tucker. 2018. Revising M&M with Taxes: An alternative equilibriusm process. International Journal of Financial Studies 6: 1–12. [Google Scholar]

- Lando, David. 1998. On Cox Processes and Credit-risky Securities. Review of Derivatives Research 2: 99–120. [Google Scholar] [CrossRef]

- Lando, David. 2000. Some elements of rating based credit risk modeling. In Advanced Fixed-Income Valuation Tools. New York: John Wiley & Sons, Inc., pp. 193–215. [Google Scholar]

- Leland, Hayne, and Klaus Bjerre Toft. 1996. Optimal capital structure, endogenous bankruptcy, and the term strcuture of credit spreads. Journal of Finance 51: 987–1019. [Google Scholar] [CrossRef]

- Li, Zhichuan Frank, Shannon Lin, Shuna Sun, and Alan Tucker. 2018. Risk-adjusted inside debt. Global Finance Journal 35: 12–42. [Google Scholar] [CrossRef]

- Liang, Jin, and Chukun Zeng. 2015. Corporate bonds pricing under credit rating migration and structure framework. A Journal of Chinese University (A) 30: 61–70. [Google Scholar]

- Liang, Jin, Yuejuan Zhao, and Xudan Zhang. 2016a. Utility Indifference Valuation of Corporate Bond with Credit Rating Migration by Structure Approach. Economic Modelling 54: 339–46. [Google Scholar] [CrossRef]

- Liang, Jin, Yuan Wu, and Bei Hu. 2016b. Asymptotic Traveling Wave Solution for a Credit Rating Migration Problem. Journal of Differential Equations 261: 1017–45. [Google Scholar] [CrossRef]

- Liang, Jin, Hong-Ming Yin, Xinfu Chen, and Yuan Wu. 2017. On a corporate bond pricing model with credit rating migration risks and stochastic interest rate. Qualitative Finance and Economics 1: 300–19. [Google Scholar] [CrossRef]

- Longstaff, Francis, and Eduardo Schwartz. 1995. A Simple Approach to Valuing Risky Fixed and Floating Rate Debt. Journal of Finance 50: 789–819. [Google Scholar] [CrossRef] [Green Version]

- Merton, Robert C. 1974. On the Pricing of Corporate Debt: The Risk Structure of Interest Rates. Journal of Finance 29: 449–70. [Google Scholar]

- Richelson, Hildy, and Stan Richelson. 2011. Bonds: The Unbeaten Path to Secure Investment Growth, 2nd ed. Hoboken: John Wiley & Sons, Inc. [Google Scholar]

- Thomas, Lyn, David Allen, and Nigel Morkel-Kingsbury. 2002. A hidden Markov chain model for the term structure of bond credit risk spreads. International Review of Financial Analysis 11: 311–29. [Google Scholar] [CrossRef]

- Tsiveriotis, Kostas, and Chris Fernandes. 1998. Valuing convertible bonds with credit risk. The Journal of Fixed Income 8: 95–102. [Google Scholar] [CrossRef]

- Wu, Yuan, and Jin Liang. 2018. A new model and its numerical method to identify multi credit migration boundaries. International Journal of Computer Mathematics 95: 1688–702. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Date | Close Price | Rating | D | ||||

|---|---|---|---|---|---|---|---|

| 3 January 2001 | 9.14 | Low | 18.64 | 45.35 | 10.66 | ||

| ... | ... | (A3) | |||||

| 30 December 2002 | 5.8 | ||||||

| 2 January 2004 | 7.65 | Middle | 18.79 | 40.46 | 8.88 | ||

| ... | ... | (A1) | |||||

| 29 December 2005 | 12.26 | ||||||

| 3 January 2011 | 25.33 | High | 41.32 | 146.22 | 16.05 | ||

| ... | ... | (A1a) | |||||

| 31 December 2012 | 228.03 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yin, H.-M.; Liang, J.; Wu, Y. On a New Corporate Bond Pricing Model with Potential Credit Rating Change and Stochastic Interest Rate. J. Risk Financial Manag. 2018, 11, 87. https://doi.org/10.3390/jrfm11040087

Yin H-M, Liang J, Wu Y. On a New Corporate Bond Pricing Model with Potential Credit Rating Change and Stochastic Interest Rate. Journal of Risk and Financial Management. 2018; 11(4):87. https://doi.org/10.3390/jrfm11040087

Chicago/Turabian StyleYin, Hong-Ming, Jin Liang, and Yuan Wu. 2018. "On a New Corporate Bond Pricing Model with Potential Credit Rating Change and Stochastic Interest Rate" Journal of Risk and Financial Management 11, no. 4: 87. https://doi.org/10.3390/jrfm11040087