Understanding the Relationship between Financial Literacy and Chinese Rural Households’ Entrepreneurship from the Perspective of Credit Constraints and Risk Preference

Abstract

:1. Introduction

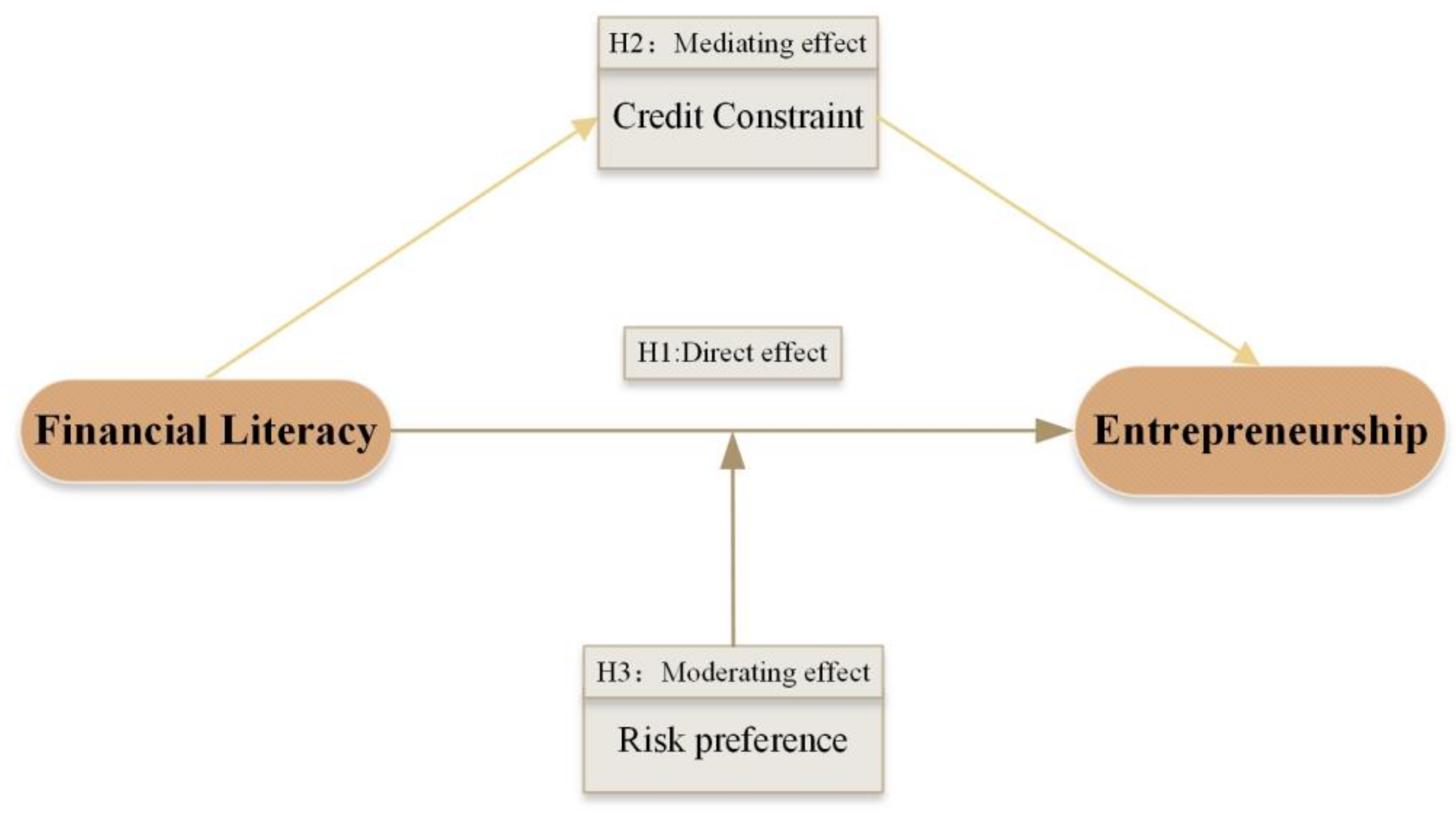

2. Theoretical Framework

2.1. Financial Literacy and Rural Households’ Entrepreneurship

2.2. The Mediating Role of Easing Credit Constraints

2.3. Moderating Role of Risk Preferences

3. Research Design

3.1. Research Data

3.2. Variable Definition and Description

3.2.1. Independent Variable

3.2.2. Dependent Variable

3.2.3. Control Variables

3.2.4. Instrumental Variable

3.2.5. Mediating Variable

3.2.6. Moderating Variable

3.3. Research Methods

3.3.1. Benchmark Method

3.3.2. Endogenous Treatment

3.3.3. Test Method of Mediating Effect and Moderating Effect

4. Results

4.1. Correlation between Financial Literacy and Rural Households’ Entrepreneurship

4.2. Mediating Role of Credit Constraints

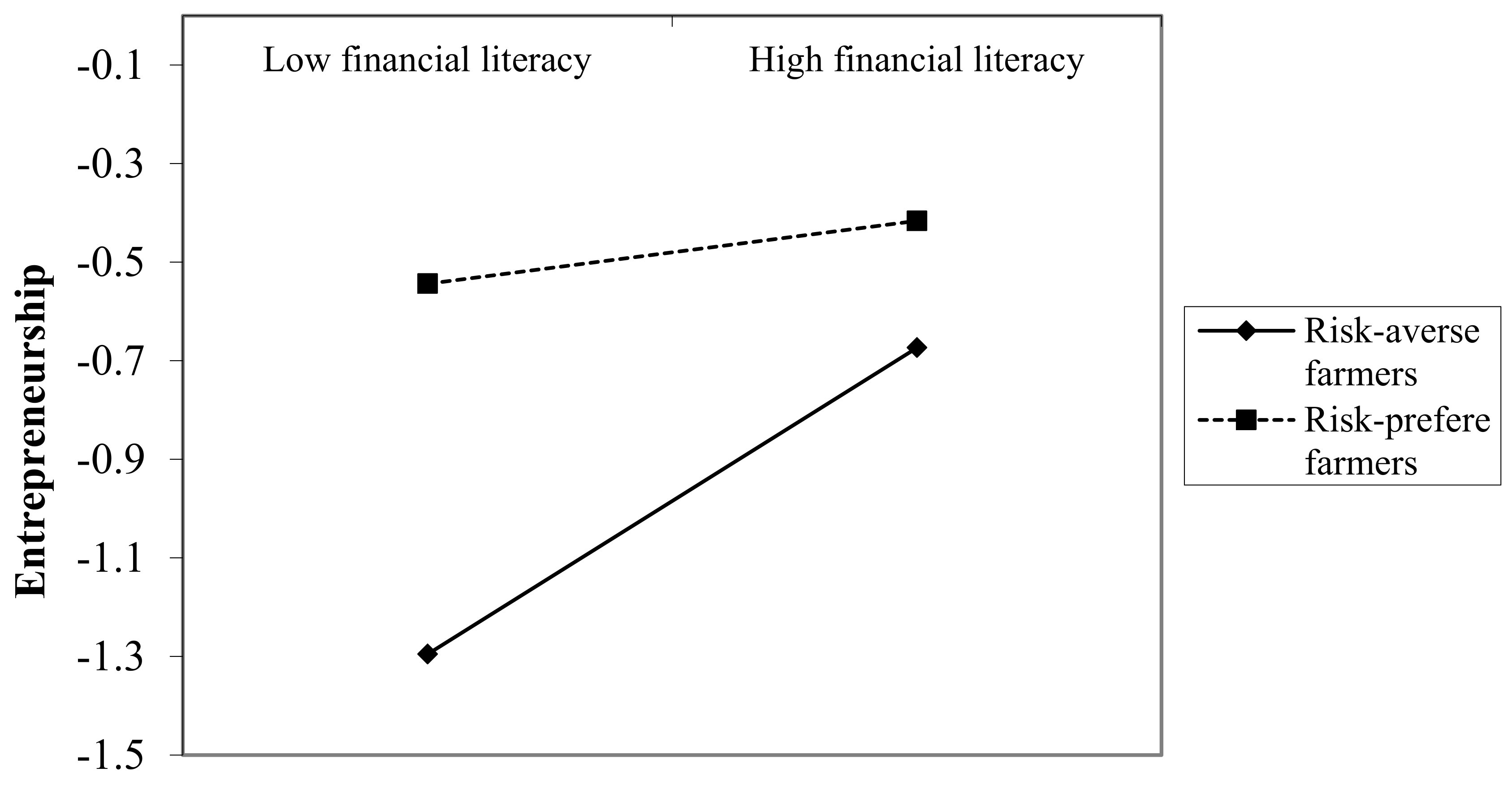

4.3. Moderating Role of Risk Preference

4.4. Robustness Test

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Secundo, G.; Mele, G.; Vecchio, P.D.; Elia, G.; Margherita, A.; Ndou, V. Threat or Opportunity? A Case Study of Digital-Enabled Redesign of Entrepreneurship Education in the COVID-19 Emergency. Technol. Forecast. Soc. Change 2021, 166, 120565. [Google Scholar] [CrossRef]

- Galindo Martin, M.-A.; Méndez Picazo, M.T.; Alfaro Navarro, J.L. Entrepreneurship, Income Distribution and Economic Growth. Int. Entrep. Manag. J. 2010, 6, 131–141. [Google Scholar] [CrossRef]

- Soluk, J.; Kammerlander, N.; Darwin, S. Digital Entrepreneurship in Developing Countries: The Role of Institutional Voids. Technol. Forecast. Soc. Change 2021, 170, 120876. [Google Scholar] [CrossRef]

- Global Entrepreneurship Monitor 2021/2022 Global Report: Opportunity Amid Disruption—University of Strathclyde. Available online: https://pureportal.strath.ac.uk/en/publications/global-entrepreneurship-monitor-20212022-global-report-opportunit (accessed on 29 January 2023).

- Fuller-Love, N.; Midmore, P.; Thomas, D.; Henley, A. Entrepreneurship and rural economic development: A scenario analysis approach. Int. J. Entrep. Behav. Res. 2006, 12, 289–305. [Google Scholar] [CrossRef]

- Naminse, E.; Zhuang, J. Does farmer entrepreneurship alleviate rural poverty in China? Evidence from Guangxi Province. PLoS ONE 2018, 13, e0194912. [Google Scholar] [CrossRef] [Green Version]

- Zhao, J.; Li, T. Social Capital, Financial Literacy, and Rural Household Entrepreneurship: A Mediating Effect Analysis. Front. Psychol. 2021, 12, 724605. [Google Scholar] [CrossRef] [PubMed]

- Jiang, X.; Ma, X.; Li, Z.; Guo, Y.; Xu, A.; Su, X. Why Do People Who Belong to the Same Clan Engage in the Same Entrepreneurial Activities?—A Case Study on the Influence of Clan Networks on the Content of Farmers’ Entrepreneurship. Front. Psychol. 2022, 13, 873583. [Google Scholar] [CrossRef] [PubMed]

- Van Der Sluis, J.; Van Praag, M.; Vijverberg, W. Education and Entrepreneurship Selection and Performance: A Review of the Empirical Literature. J. Econ. Surv. 2008, 22, 795–841. [Google Scholar] [CrossRef]

- Luo, Y.; Zeng, L. Digital Financial Capabilities and Household Entrepreneurship. Econ. Political Stud. 2020, 8, 165–202. [Google Scholar] [CrossRef]

- Ajide, F. Financial inclusion in Africa: Does it promote entrepreneurship? J. Financ. Econ. Policy 2020, 1, 687–706. [Google Scholar] [CrossRef]

- Liu, T.; He, G.; Turvey, C. Inclusive finance, farm households entrepreneurship, and inclusive rural transformation in rural poverty-stricken areas in China. Emerg. Mark. Financ. Trade 2021, 57, 1929–1958. [Google Scholar] [CrossRef]

- Chang, D.; Chen, W.; Tai, X.; Si, Y. The Impact of Financial Literacy on Rural Household Self-Employment: The Mediating Role of Financial Ability. Emerg. Mark. Financ. Trade 2022, 58, 3297–3308. [Google Scholar] [CrossRef]

- Abubakar, H.A. Entrepreneurship Development and Financial Literacy in Africa. World J. Entrep. Manag. Sustain. Dev. 2015, 11, 281–294. [Google Scholar] [CrossRef]

- Deller, S.; Kures, M.; Conroy, T. Rural Entrepreneurship and Migration. J. Rural. Stud. 2019, 66, 30–42. [Google Scholar] [CrossRef]

- Oseifuah, E. Financial literacy and youth entrepreneurship in South Africa. Afr. J. Econ. Manag. Stud. 2010, 1, 164–182. [Google Scholar]

- Caliendo, M.; Fossen, F.; Kritikos, A. Risk attitudes of nascent entrepreneurs–new evidence from an experimentally validated survey. Small Bus. Econ. 2009, 32, 153–167. [Google Scholar] [CrossRef] [Green Version]

- Cai, D.; Song, Q.; Ma, S.; Dong, Y.; Xu, Q. The Relationship between Credit Constraints and Household Entrepreneurship in China. Int. Rev. Econ. Financ. 2018, 58, 246–258. [Google Scholar] [CrossRef]

- Lusardi, A.; Mitchell, O.S. The Economic Importance of Financial Literacy: Theory and Evidence. J. Econ. Lit. 2014, 52, 5–44. [Google Scholar] [CrossRef] [Green Version]

- Calcagno, R.; Alperovych, Y.; Quas, A. Financial literacy and entrepreneurship. New Front. Entrep. Financ. Res. 2020, 271–297. [Google Scholar]

- Jappelli, T.; Padula, M. Investment in Financial Literacy and Saving Decisions. J. Bank. Financ. 2013, 37, 2779–2792. [Google Scholar] [CrossRef] [Green Version]

- Cutler, N.; Devlin, S. Financial literacy 2000. J. Financ. Serv. Prof. 1996, 50, 32. [Google Scholar]

- Huston, S.J. Measuring Financial Literacy. J. Consum. Aff. 2010, 44, 296–316. [Google Scholar] [CrossRef]

- Huston, S.J. Financial Literacy and the Cost of Borrowing. Int. J. Consum. Stud. 2012, 36, 566–572. [Google Scholar] [CrossRef]

- Disney, R.; Gathergood, J. Financial Literacy and Consumer Credit Portfolios. J. Bank. Financ. 2013, 37, 2246–2254. [Google Scholar] [CrossRef]

- Korutaro, N.S.; Kasozi, D.; Nalukenge, I.; Tauringana, V. Lending Terms, Financial Literacy and Formal Credit Accessibility. Int. J. Soc. Econ. 2014, 41, 342–361. [Google Scholar] [CrossRef]

- Jensen, T.L.; Leth-Petersen, S.; Nanda, R. Financing Constraints, Home Equity and Selection into Entrepreneurship. J. Financ. Econ. 2022, 145 Pt A, 318–337. [Google Scholar] [CrossRef]

- Beck, T.; Lu, L.; Yang, R. Finance and Growth for Microenterprises: Evidence from Rural China. World Dev. 2015, 67, 38–56. [Google Scholar] [CrossRef] [Green Version]

- Lai, J.T.; Yan, I.K.M.; Yi, X.; Zhang, H. Digital Financial Inclusion and Consumption Smoothing in China. China World Econ. 2020, 28, 64–93. [Google Scholar] [CrossRef]

- Lee, J.-J.; Sawada, Y. Precautionary Saving under Liquidity Constraints: Evidence from Rural Pakistan. J. Dev. Econ. 2010, 91, 77–86. [Google Scholar] [CrossRef] [Green Version]

- Douglas, E.J.; Shepherd, D.A. Entrepreneurship as a Utility Maximizing Response. J. Bus. Ventur. 2000, 15, 231–251. [Google Scholar] [CrossRef]

- Van Praag, C.M.; Cramer, J.S. The Roots of Entrepreneurship and Labour Demand: Individual Ability and Low Risk Aversion. Econ. 2001, 68, 45–62. [Google Scholar] [CrossRef]

- Dziuban, C.; Shirkey, E. When is a correlation matrix appropriate for factor analysis? Some decision rules. Psychol. Bull. 1974, 8, 358. [Google Scholar] [CrossRef]

- He, J. Promoting Rural Households’ Energy Use for Cooking: Using Internet. Technol. Forecast. 2022, 184, 121971. [Google Scholar] [CrossRef]

- Miao, S.; Chi, J.; Liao, J.; Qian, L. How Does Religious Belief Promote Farmer Entrepreneurship in Rural China? Econ. Model. 2021, 97, 95–104. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Dimension | Question | Variable | Assignment | Mean | SD |

|---|---|---|---|---|---|

| Interest rate | Suppose you have 100 now, and the annual interest rate of the bank is 4%. How much is the total amount of the five-year principal and interest? (A. Less than 120 yuan; B. More than 120 yuan; C. Equal to 120 yuan; D. I don’t know) | Answer the interest rate question | Choose D to be assigned 0, otherwise 1 | 0.234 | 0.424 |

| Answer the interest rate question correctly | Choose C to be assigned 0, otherwise 1 | 0.200 | 0.400 | ||

| Inflation and time value | Suppose you have 100 yuan now, the bank’s annual interest rate is 5%, and the inflation rate is 3% every year. After the 100 yuan is deposited in the bank for a year, what will you buy compared with what you buy now? (A. More; B. Less; C. Same; D. I don’t know) | Answer the inflation and time value question | Choose D to be assigned 0, otherwise 1 | 0.173 | 0.378 |

| Answer the inflation and time value question correctly | Choose A to be assigned 0, otherwise 1 | 0.051 | 0.220 | ||

| Stocks and funds | Do you think buying a stock alone is riskier than buying a stock fund? (A. Yes; B. No; C. I don’t know; D. I haven’t heard of stocks; E. I haven’t heard of funds; F. I haven’t heard of either) | Answer the stocks and funds question | Choose A or B to be assigned 0, otherwise 1 | 0.111 | 0.315 |

| Answer the stocks and funds question correctly | Choose A to be assigned 0, otherwise 1 | 0.089 | 0.284 | ||

| Venture portfolio | Do you think that, in general, planting (operating) multiple crops is less risky than planting (operating) one crop? (A. Yes; B. No; C. I don’t know) | Answer the venture portfolio question | Choose C to be assigned 0, otherwise 1 | 0.570 | 0.495 |

| Answer the venture portfolio question correctly | Choose A to be assigned 0, otherwise 1 | 0.397 | 0.489 | ||

| Financial information attention | Do you usually pay attention to economic and financial information? | Financial information attention | Very concerned, very concerned, general = 1; Little or no attention = 0 | 0.120 | 0.325 |

| Variable | Variable Definition | Mean | SD | |

|---|---|---|---|---|

| Dependent variable | Entrepreneurship | Does your family start a business? (1 = Yes, 0 = No) | 0.112 | 0.315 |

| Independent variable | Financial literacy | Calculated by factor analysis, the questions and answers are shown in Table 1 | 0 | 0.585 |

| Control variables—individual characteristics | Age of household head | Unit: Year old | 63.35 | 10.52 |

| Gender of household head | 1 = MaN; 0 = Female | 0.925 | 0.264 | |

| Health status of household head | Self-identified health status (1 = incapacity; 2 = poor; 3 = medium; 4 = good; 5 = excellent) | 4.013 | 1.092 | |

| Education of household head | Unit: year | 7.293 | 3.649 | |

| Risk perception | What do you think about the risk of failure faced by entrepreneurship? (1 = unknown; 2 = relatively small; 3 = average; 4 = relatively big; 5 = very big) | 3.566 | 1.477 | |

| Control variable—family characteristics | Number of families | How many people live in your family (for 6 months or more in a year)? | 3.057 | 1.600 |

| Cadre | Are there any cadres in your family? (1 = Yes, 0 = No) | 0.157 | 0.364 | |

| Party member | Are there any Party members in your family? (1 = Yes, 0 = No) | 0.309 | 0.462 | |

| Number of entrepreneurs among relatives | How many of your relatives and friends start businesses? | 0.560 | 2.413 | |

| Entrepreneurship failure experience | Has your family experienced any entrepreneurial failure since 2015? (1 = Yes, 0 = No) | 0.0160 | 0.124 | |

| Control variable—village characteristics | Distance from the village to the nearest bank | Distance from the village committee to the nearest bank (available for counter business) (km) | 3.344 | 2.942 |

| Entrepreneurship training | Number of entrepreneurship training organized by township governments in 2020 (times) | 1.887 | 1.347 | |

| Financial Lectures | How many lectures on financial knowledge have been held in the village in 2020? (times) | 1.147 | 1.192 | |

| Instrumental variables | Financial literacy level at a village level | Average financial literacy of others in the same village except himself | −0.002 | 0.206 |

| Mediating variable | Traditional credit constraints | Do you understand the traditional credit business launched by banks and other formal financial institutions? (No application or application but no credit = 1; others = 0) | 0.957 | 0.204 |

| Digital credit constraints | Do you understand the digital credit business launched by banks and other formal financial institutions? (No application or application but no credit = 1; others = 0) | 0.995 | 0.072 | |

| Bank credit constraints | Do you understand the online credit business launched by Alipay, WeChat, and other network platforms? (No application or application but no credit = 1; others = 0) | 0.983 | 0.128 | |

| Moderating variable | Risk preference | Which of the following investments would you prefer? (1 = investment with low risk, low risk, low return, and low loss; 2 = investment with medium risk, medium risk, medium return, and medium loss; 3 = investment with high risk, high risk, high return, and high loss) | 1.279 | 0.544 |

| Model 1 | Model 2 | Model 3 | Model 4 | |

|---|---|---|---|---|

| Probit | Probit | IV-Probit | IV-Probit | |

| Financial literacy | 0.346 *** | 0.173 *** | 1.026 *** | 0.746 ** |

| (0.054) | (0.063) | (0.211) | (0.320) | |

| Age of household head | −0.015 *** | −0.012 *** | ||

| (0.004) | (0.004) | |||

| Gender of household head | 0.120 | 0.172 | ||

| (0.153) | (0.158) | |||

| The health level of household head | 0.119 *** | 0.105 *** | ||

| (0.040) | (0.041) | |||

| Education level of household head | −0.007 | −0.022 | ||

| (0.012) | (0.015) | |||

| Risk perception | −0.029 | −0.043 | ||

| (0.027) | (0.028) | |||

| Number of families | 0.075 *** | 0.065 *** | ||

| (0.023) | (0.024) | |||

| Cadre | 0.060 | −0.002 | ||

| (0.107) | (0.114) | |||

| party member | −0.019 | −0.127 | ||

| (0.091) | (0.110) | |||

| Number of entrepreneurs among relatives | 0.135 *** | 0.124 *** | ||

| (0.017) | (0.019) | |||

| Entrepreneurship failure experience | 1.215 *** | 1.091 *** | ||

| (0.224) | (0.240) | |||

| Distance from the village to the nearest bank | 0.024 * | 0.027 ** | ||

| (0.013) | (0.013) | |||

| Entrepreneurship training | −0.014 | −0.017 | ||

| (0.029) | (0.029) | |||

| Financial lectures | −0.040 | −0.024 | ||

| (0.034) | (0.036) | |||

| Financial literacy at the village level | 0.819 *** | 0.600 *** | ||

| (0.057) | (0.056) | |||

| Constant | −1.238 *** | −1.128 *** | −1.245 *** | −1.147 *** |

| (0.036) | (0.399) | (0.037) | (0.406) | |

| LRχ2/Wald χ2 | 40.583 *** | 219.150 *** | 23.640 *** | 174.479 *** |

| First stage F value | / | / | 207.70 | 39.01 |

| endogenous Wald χ2 | / | / | 11.92 *** | 3.46 * |

| N | 2278 | 2278 | 2278 | 2278 |

| Path 1: Ease Traditional Credit Constraints | Path 2: Ease Digital Credit Constraints | Path 3: Ease Online Credit Constraints | |||||

|---|---|---|---|---|---|---|---|

| Model 5 | Model 6 | Model 7 | Model 8 | Model 9 | Model 10 | Model 11 | |

| Entrepreneur | TCC | Entrepreneur | DCC | Entrepreneur | OCC | Entrepreneur | |

| FL | 0.173 *** | −0.370 *** | 0.149 ** | −0.632 *** | 0.168 *** | −0.452 *** | 0.168 *** |

| (0.064) | (0.076) | (0.065) | (0.121) | (0.065) | (0.096) | (0.065) | |

| TCC | −0.466 *** | ||||||

| (0.154) | |||||||

| DCC | −0.301 | ||||||

| (0.448) | |||||||

| OCC | −0.164 | ||||||

| (0.249) | |||||||

| Controls | YES | YES | YES | YES | YES | YES | YES |

| Wald χ2 | 146.414 *** | 136.305 *** | 157.059 *** | 93.708 *** | 146.839 *** | 87.285 *** | 148.005 *** |

| Pseudo R2 | 0.137 | 0.138 | 0.143 | 0.256 | 0.137 | 0.153 | 0.137 |

| N | 2278 | 2278 | 2278 | 2107 | 2278 | 2278 | 2278 |

| Entrepreneurship | ||

|---|---|---|

| Model 13 | Model 14 | |

| Financial literacy | / | 0.745 ** |

| / | (0.311) | |

| Risk preference | 0.294 *** | 0.252 *** |

| (0.062) | (0.071) | |

| Risk preference * Financial literacy | / | −0.212 * |

| / | (0.114) | |

| Controls | YES | YES |

| Constant | −1.617 *** | −1.235 *** |

| (0.397) | (0.419) | |

| Wald χ2 | 166.86 *** | 189.970 *** |

| First stage F value | / | 40.04 |

| endogenous Wald χ2 | / | 3.75 * |

| N | 2187 | 2187 |

| CMP | IV-Probit | |

|---|---|---|

| Financial literacy | 0.568 *** | |

| (0.209) | ||

| New financial literacy | 0.489 ** | |

| (0.213) | ||

| Constant | −1.057 *** | −1.480 *** |

| (0.392) | (0.439) | |

| Financial literacy at the village level | 0.819 *** | 0.907 *** |

| (0.057) | (0.106) | |

| atanhrho_12/ F value | −0.242 * | 31.45 |

| (0.129) | ||

| LRχ2/Wald χ2 | 381.928 *** | 171.234 *** |

| Endogenous Wald χ2 | / | 3.46 * |

| N | 2278 | 2278 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, S.; He, J.; Xu, D. Understanding the Relationship between Financial Literacy and Chinese Rural Households’ Entrepreneurship from the Perspective of Credit Constraints and Risk Preference. Int. J. Environ. Res. Public Health 2023, 20, 4981. https://doi.org/10.3390/ijerph20064981

Liu S, He J, Xu D. Understanding the Relationship between Financial Literacy and Chinese Rural Households’ Entrepreneurship from the Perspective of Credit Constraints and Risk Preference. International Journal of Environmental Research and Public Health. 2023; 20(6):4981. https://doi.org/10.3390/ijerph20064981

Chicago/Turabian StyleLiu, Silin, Jia He, and Dingde Xu. 2023. "Understanding the Relationship between Financial Literacy and Chinese Rural Households’ Entrepreneurship from the Perspective of Credit Constraints and Risk Preference" International Journal of Environmental Research and Public Health 20, no. 6: 4981. https://doi.org/10.3390/ijerph20064981