The Sustainability Narrative: A Multi Study Using Event Studies to Analyse the American Energy Companies Shareholder’s Reaction to Sustainability News

Abstract

:1. Introduction

1.1. Literature Review

1.1.1. News and the Stock Market

1.1.2. Sustainability and the Stock Market

1.1.3. Sustainability News and the Stock Market

2. Materials and Methods

2.1. Materials

2.2. Methods

- -

- Day of the event: The day of the event is the date when the news with the highest volume intensity was published. We wrote the code so that news with the same content as the peak news was not downloaded seven days before and seven days after to guarantee the event window.

- -

- Event window: (−7, 7). Following the research of [43] on Narrative Economics, we assumed that viral, high-volume news spread in a similar fashion to an epidemic curve, with published news before and after the news with the highest peak. Therefore, we used CAARS to understand the total effect of the spread rather than just the peak. The news spread could be different depending on the type of news. However, we assumed an event window of 14 days would catch the effect, as [90] argued that one advantage of averaging the results is that the law of large numbers offsets the errors of having very long or small windows.

- -

- The (mm) is commonly used for event study analysis. This model considers the actual returns of a baseline reference market and tracks the correlation of a company’s stock with the baseline. Equations (1) and (2) specify the model. The abnormal return on a particular day, ARit, in the event window describes the difference between the actual stock return, Rit, on day t, and the expected return, which is foretold based on two facts; the average relationship between the firm’s stock and its reference market (expressed by the α and β parameters), and the actual reference market’s return, Rmt.then

- -

- (mam) is used to handle the event’s potential consequences in the stock market. In the (mam), the followed return of the reference market on day t (Rmt) is extracted from the return Rit for the observation i on day t. Equation (3) establishes the ARit:

- -

- In the (cpmam), the abnormal return in the event window is the return of observation i on day t minus the average return of the observation i in the estimation window (Equations (4) and (5)):where

- -

- The (GARCH) uses a market model single factor with GARCH (1, 1) errors estimated, particularly:

- -

- The (EGARCH), Ref. [96] proposed the EGARCH model to include the asymmetric effect of changes in the prices of an asset on its volatility. The Garch (1, 1) model does not account for any asymmetry that may arise from the negative and positive moves of the market or as it is usually called, the leverage effect. To solve this, the EGARCH model applies a logarithmic conditional variance. Equation (8) is the conditional variance of the EGARCH (1, 1) model:where ω corresponds to a constant, β is the now logarithmic GARCH term, α is the ARCH term that no longer has to be positive. The γ is the so-called leverage term; if is significant and different from zero there will be asymmetry in the estimation period. The σ is the standard deviation.

3. Results and Discussion

3.1. Results

3.1.1. Cumulative Average Abnormal Returns (CAAR)

3.1.2. Abnormal Volatilities (AV)

3.2. Discussion

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Mallin, C. Institutional shareholders: Their role in the shaping of corporate governance. Int. J. Corp. Gov. 2008, 1, 97–105. [Google Scholar] [CrossRef]

- Gillet-Monjarret, C. Assurance of Sustainability Information: A Study of Media Pressure. Account. Eur. 2015, 12, 87–105. [Google Scholar] [CrossRef]

- Meixell, M.J.; Luoma, P. Stakeholder pressure in sustainable supply chain management. Int. J. Phys. Distrib. Logist. Manag. 2015, 45, 69–89. [Google Scholar] [CrossRef]

- Muralidharan, S.; Rejón-Guardia, F.; Xue, F. Understanding the Green Buying Behavior of Younger Millennials from India and the United States: A Structural Equation Modeling Approach. J. Int. Consum. Mark. 2016, 28, 54–72. [Google Scholar] [CrossRef]

- Rentizelas, A.; de Sousa Jabbour, A.B.L.; Al Balushi, A.D.; Tuni, A. Social sustainability in the oil and gas industry: Institutional pressure and the management of sustainable supply chains. Ann. Oper. Res. 2020, 290, 279–300. [Google Scholar] [CrossRef] [Green Version]

- Cañón-De-Francia, J.; Garcés-Ayerbe, C. ISO 14001 environmental certification, a sign valued by the market? Environ. Resour. Econ. 2009, 44, 245–262. [Google Scholar] [CrossRef]

- Oberndorfer, U.; Schmidt, P.; Wagner, M.; Ziegler, A. Does the stock market value the inclusion in a sustainability stock index? An event study analysis for German firms. J. Environ. Econ. Manag. 2013, 66, 497–509. [Google Scholar] [CrossRef] [Green Version]

- Sharma, G.D.; Talan, G.; Bansal, S.; Jain, M. Is there a cost for sustainable investments: Evidence from dynamic conditional correlation. J. Sustain. Finance Investig. 2021, 1, 21. [Google Scholar] [CrossRef]

- Gibson, R.; Krueger, P.; Mitali, S.F. The Sustainability Footprint of Institutional Investors: ESG Driven Price Pressure and Performance; Swiss Finance Institute Research Paper No. 17-05; Swiss Finance Institute: Zurich, Switzerland, 2020. [Google Scholar]

- Maiti, M. Is ESG the succeeding risk factor? J. Sustain. Finance Investig. 2020, 11, 199–213. [Google Scholar] [CrossRef]

- Muhmad, S.N.; Muhamad, R. Sustainable business practices and financial performance during pre-and post-SDG adoption periods: A systematic review. J. Sustain. Finance Investig. 2020, 11, 291–309. [Google Scholar] [CrossRef]

- Ashwin Kumar, N.C.; Smith, C.; Badis, L.; Wang, N.; Ambrosy, P.; Tavares, R. ESG factors and risk-adjusted performance: A new quantitative model. J. Sustain. Finance Investig. 2016, 6, 292–300. [Google Scholar] [CrossRef]

- Friede, G.; Busch, T.; Bassen, A. ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. J. Sustain. Finance Investig. 2015, 5, 210–233. [Google Scholar] [CrossRef] [Green Version]

- Flammer, C. Corporate social responsibility and shareholder reaction: The environmental awareness of investors. Acad. Manag. J. 2013, 56, 758–781. [Google Scholar] [CrossRef] [Green Version]

- Pinney, C.; Lawrence, S.; Lau, S. Sustainability and Capital Markets—Are We There Yet? J. Appl. Corp. Finance 2019, 31, 86–91. [Google Scholar] [CrossRef]

- Ruggie, J.G.; Middleton, E.K. Money, Millennials and Human Rights: Sustaining ‘Sustainable Investing’. Glob. Policy 2019, 10, 144–150. [Google Scholar] [CrossRef] [Green Version]

- Unruh, G.; Kiron, D.; Kruschwitz, N.; Reeves, M.; Rubel, H.; Zum Felde, A.M. Investing for a Sustainable Future: Investors Care More about Sustainability Than Many Executives Believe; Massachusetts Institute of Technology: Cambridge, MA, USA, 2016. [Google Scholar]

- Andersson, M.; Bolton, P.; Samama, F. Governance and Climate Change: A Success Story in Mobilizing Investor Support for Corporate Responses to Climate Change. J. Appl. Corp. Finance 2016, 28, 29–33. [Google Scholar] [CrossRef]

- Barnett, M.L.; Salomon, R.M. Beyond Dichotomy: The Curvilinear Relationship between Social Responsibility and Financial Performance. Strateg. Manag. J. 2006, 27, 1101–1122. [Google Scholar] [CrossRef]

- Glac, K. The impact and source of mental frames in socially responsible investing. J. Behav. Finance 2012, 13, 184–198. [Google Scholar] [CrossRef]

- Jo, H. Financial Analysts, Firm Quality, and Social Responsibility. J. Behav. Finance 2003, 4, 172–183. [Google Scholar] [CrossRef]

- Global Sustainable Investment Alliance. Global Sustainable Investment Review. 2018. Available online: www.gsi-alliance.org/wp-content/uploads/2019/03/GSIR_Review2018 (accessed on 20 April 2021).

- Capuano, L. International Energy Outlook 2018 (IEO2018); US Energy Information Administration (EIA): Washington, DC, USA, 2018; 21p. [Google Scholar]

- Sustainability Reporting Trends in North America, 2018–2019; Centre for Sustainability and Excellence: Chicago, IL, USA, 2022.

- Elmalt, D.; Igan, D.; Kirti, D. Limits to Private Climate Change Mitigation; CEPR Discussion Papers No. 16061; International Monetary Fund: Washington, DC, USA, 2021. [Google Scholar]

- Da, Z.; Engelberg, J.; Gao, P. The Sum of All Fears: Investor Sentiment, Noise Trading and Aggregate Volatility; Working Paper; Oxford University Press: Oxford, UK, 2009. [Google Scholar]

- Barber, B.M.; Odean, T.; Zhu, N. Systematic noise. J. Financ. Mark. 2009, 12, 547–569. [Google Scholar] [CrossRef]

- Tetlock, P.C. Information Transmission in Finance. Annu. Rev. Financ. Econ. 2014, 6, 365–384. [Google Scholar] [CrossRef] [Green Version]

- Oberlechner, T.; Hocking, S. Information Sources, News, and Rumors in Financial Markets: Insights into the Foreign Exchange Market. J. Econ. Psychol. 2004, 25, 407–424. [Google Scholar] [CrossRef]

- Shleifer, A.; Vishny, R.W. A survey of corporate governance. J. Finance 1997, 52, 737–783. [Google Scholar] [CrossRef]

- Olsen, R.A. Behavioral Finance and its Implications for Stock-Price Volatility. Financ. Anal. J. 1998, 54, 10–18. [Google Scholar] [CrossRef]

- McCombs, M.E.; Shaw, D.L. The agenda-setting function of mass media. Public Opin. Q. 1972, 36, 176–187. [Google Scholar] [CrossRef]

- Carroll, C.E.; McCombs, M. Agenda-setting effects of business news on the public’s images and opinions about major corporations. Corp. Reput. Rev. 2003, 6, 36–46. [Google Scholar] [CrossRef]

- Tetlock, P.C. Giving content to investor sentiment: The role of media in the stock market. J. Finance 2007, 62, 1139–1168. [Google Scholar] [CrossRef]

- Bushee, B.J.; Miller, G.S. Investor relations, firm visibility, and investor following. Account. Rev. 2012, 87, 867–897. [Google Scholar] [CrossRef] [Green Version]

- Chan, S. Stock price reaction to news and no-news: Drift and reversal after headlines. J. Financ. Econ. 2003, 70, 223–260. [Google Scholar] [CrossRef]

- Li, J.; Hendler, J.; Teall, J. Investor Attention on the Social Web. J. Behav. Finance 2016, 17, 45–59. [Google Scholar] [CrossRef]

- Lewis, J.; Williams, A.; Franklin, B. A compromised fourth estate? UK news journalism, public relations, and news sources. J. Stud. 2008, 9, 1–20. [Google Scholar] [CrossRef]

- Vettehen, P.H.; Beentjes, J.; Nuijten, K.; Peeters, A. Arousing news characteristics in Dutch television news 1990–2004: An exploration of competitive strategies. Mass Commun. Soc. 2010, 14, 93–112. [Google Scholar] [CrossRef]

- Scheufele, B.; Haas, A.; Brosius, H.B. Mirror or molder? A study of media coverage, stock prices, and trading volumes in Germany. J. Commun. 2011, 61, 48–70. [Google Scholar] [CrossRef]

- Thompson, J.B. Ideology and Modern Culture: Critical Social Theory in the Era of Mass Communication; John Wiley & Sons: Hoboken, NJ, USA, 2013. [Google Scholar]

- Strauß, N.; Vliegenthart, R.; Verhoeven, P. Newspapers lagging behind? Emotions in newspaper articles and stock market prices in the Netherlands. Public Relat. Rev. 2016, 42, 548–555. [Google Scholar] [CrossRef]

- Shiller, R. Narrative Economics: How Stories Go Viral and Drive Major Economic Events; Princeton University Press: Princeton, NJ, USA, 2019. [Google Scholar]

- Blacconiere, W.G.; Patten, D.M. Environmental disclosures, regulatory costs, and changes in firm value. J. Account. Econ. 1994, 18, 357–377. [Google Scholar] [CrossRef]

- Hamilton, J.T. Pollution as news: Media and stock market reactions to the toxics release inventory data. J. Environ. Econ. Manag. 1995, 28, 98–113. [Google Scholar] [CrossRef]

- Klassen, R.D.; McLaughlin, C.P. The impact of environmental management on firm performance. Manag. Sci. 1996, 42, 1199–1214. [Google Scholar] [CrossRef]

- Konar, S.; Cohen, M.A. Information as regulation: The effect of community right to know laws on toxic emissions. J. Environ. Econ. Manag. 1997, 32, 109–124. [Google Scholar] [CrossRef] [Green Version]

- Khanna, M.; Quimio, W.R.H.; Bojilova, D. Toxics release information: A policy tool for environmental protection. J. Environ. Econ. Manag. 1998, 36, 243–266. [Google Scholar] [CrossRef] [Green Version]

- Dasgupta, S.; Laplante, B.; Mamingi, N. Pollution and capital markets in developing countries. J. Environ. Econ. Manag. 2001, 42, 310–335. [Google Scholar] [CrossRef]

- Grand, M.C.; DElia, V.V. Environmental News and Stock Markets Performance: Further Evidence for Argentina. Ser. Doc. Trab. 2005, 300. [Google Scholar]

- Gupta, S.; Goldar, B. Do stock markets penalize environment-unfriendly behaviour? Evidence from India. Ecol. Econ. 2005, 52, 81–95. [Google Scholar] [CrossRef]

- Marciukaityte, D.; Szewczyk, S.H.; Uzun, H.; Varma, R. Governance and Performance Changes after Accusations of Corporate Fraud. CFA Dig. 2006, 36, 76–77. [Google Scholar] [CrossRef]

- Consolandi, C.; Jaiswal-Dale, A.; Poggiani, E.; Vercelli, A. Global Standards and Ethical Stock Indexes: The Case of the Dow Jones Sustainability Stoxx Index. J. Bus. Ethics 2009, 87, 185–197. [Google Scholar] [CrossRef] [Green Version]

- Farber, H.S.; Hallock, K.F. The changing relationship between job loss announcements and stock prices: 1970–1999. Labour Econ. 2009, 16, 1–11. [Google Scholar] [CrossRef] [Green Version]

- Cheung, A.W.K.; Roca, E. The Effect on Price, Liquidity and Risk When Stocks are Added to and Deleted from a Sustainability Index: Evidence from the Asia Pacific Context. J. Asian Econ. 2013, 24, 51–65. [Google Scholar] [CrossRef] [Green Version]

- Jory, S.R.; Ngo, T.N.; Wang, D.; Saha, A. The Market Response to Corporate Scandals Involving CEOs. Appl. Econ. 2015, 47, 1723–1738. [Google Scholar] [CrossRef]

- Krüger, P. Corporate Goodness and Shareholder Wealth. J. Financ. Econ. 2015, 115, 304–329. [Google Scholar] [CrossRef]

- Capelle-Blancard, G.; Petit, A. Every Little Helps? ESG News and Stock Market Reaction. J. Bus. Ethics 2019, 157, 543–565. [Google Scholar] [CrossRef]

- Wingender, J.R.; Woodroof, E.A. When firms publicize energy management projects their stock prices go up. Strateg. Plan. Energy Environ. 1997, 17, 38–51. [Google Scholar] [CrossRef]

- Yamashita, M.; Sen, S.; Roberts, M.C. The rewards for environmental conscientiousness in the US capital markets. J. Finance Strateg. Decis. 1999, 12, 73–82. [Google Scholar]

- Filbeck, G.; Gorman, R.F. The relationship between the environmental and financial performance of public utilities. Environ. Resour. Econ. 2004, 29, 137–157. [Google Scholar] [CrossRef]

- Nagayama, S.; Takeda, F. An empirical study on the impact of environmentally friendly news on stock prices in Japan. In Proceedings of the Asia-Pacific Economic Association 2006 Meeting, Hanoi, Vietnam, 19 November 2006. [Google Scholar]

- Chollet, P.; Cellier, A. The Impact of Corporate Social Responsibility Rating Announcements on European Stock Prices. In Proceedings of the International Conference of the French Finance Association (AFFI), Montpellier, France, 11–13 May 2011. [Google Scholar] [CrossRef] [Green Version]

- Yin, H.; Li, M.; Ma, Y.; Zhang, Q. The Relationship between Environmental Information Disclosure and Profitability: A Comparison between Different Disclosure Styles. Int. J. Environ. Res. Public Health 2019, 16, 1556. [Google Scholar] [CrossRef] [Green Version]

- Eccles, R.G.; Ioannou, I.; Serafeim, G. The impact of corporate sustainability on organizational processes and performance. Manag. Sci. 2014, 60, 2835–2857. [Google Scholar] [CrossRef] [Green Version]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate social and financial performance: A meta-analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. Misery loves companies: Rethinking social initiatives by business. Adm. Sci. Q. 2003, 48, 268–305. [Google Scholar] [CrossRef] [Green Version]

- Maignan, I.; Ferrell, O.C.; Ferrell, L. A stakeholder model for implementing social responsibility in marketing. Eur. J. Mark. 2005, 39, 956–977. [Google Scholar] [CrossRef] [Green Version]

- Marom, I.Y. Toward a unified theory of the CSP–CFP link. J. Bus. Ethics 2006, 67, 191–200. [Google Scholar] [CrossRef]

- Wu, M.W.; Shen, C.H. Corporate social responsibility in the banking industry: Motives and financial performance. J. Bank. Finance 2013, 37, 3529–3547. [Google Scholar] [CrossRef]

- Van Beurden, P.; Gössling, T. The worth of values—A literature review on the relation between corporate social and financial performance. J. Bus. Ethics 2008, 82, 407. [Google Scholar] [CrossRef] [Green Version]

- Abu Bakar, A.S.; Ameer, R. Readability of corporate social responsibility communication in Malaysia. Corp. Soc. Responsib. Environ. Manag. 2011, 18, 50–60. [Google Scholar] [CrossRef]

- Oeyono, J.; Samy, M.; Bampton, R. An examination of corporate social responsibility and financial performance: A study of the top 50 Indonesian listed corporations. J. Glob. Responsib. 2011, 2, 100–112. [Google Scholar] [CrossRef]

- Gillan, S.L.; Koch, A.; Starks, L.T. Firms and social responsibility: A review of ESG and CSR research in corporate finance. J. Corp. Fin. 2021, 66, 101889. [Google Scholar] [CrossRef]

- Xu, X.; Chen, Y.; Zhao, J.; Wang, J. The Effect of ESG News on the Chinese Stock Market. J. Global Inform. Managm. 2022, 30, 1–21. [Google Scholar] [CrossRef]

- Ahsan, T.; Qureshi, M.A. The nexus between policy uncertainty, sustainability disclosure and firm performance. Appl. Econ. 2021, 53, 441–453. [Google Scholar] [CrossRef]

- Aouadi, A.; Marsat, S. Do ESG controversies matter for firm value? Evidence from international data. J. Bus. Ethics 2018, 151, 1027–1047. [Google Scholar] [CrossRef]

- Barroso del Toro, A.; Tort-Martorell, X.; Canela, M.A. How shareholders react to sustainable narratives about leading European energy companies? An event study using sentiment data from the global database for events, language, and tone (GDELT). Appl. Econ. 2022, 54, 3482–3494. [Google Scholar] [CrossRef]

- Kwak, H.; An, J. Revealing the hidden patterns of news photos: Analysis of millions of news photos using GDELT and deep learning-based vision APIS. arXiv 2016, arXiv:1603.04531. [Google Scholar] [CrossRef]

- Stone, P.J.; Dunphy, D.C.; Smith, M.S. The General Inquirer: A Computer Approach to Content Analysis; MIT Press: Cambridge, MA, USA, 1996. [Google Scholar]

- Strapparava, C.; Valitutti, A. WordNet-Affect: An affective extension of WordNet. In Proceedings of the 4th International Conference on Language Resources and Evaluation (LREC 2004), Lisbon, Portugal, 26–28 May 2004; pp. 1083–1086. [Google Scholar]

- Valitutti, A.; Strapparava, C.; Stock, O. Developing affective lexical resources. Psych. Nology J. 2004, 2, 61–83. [Google Scholar]

- Loughran, T.; McDonald, B. When is a liability not a liability? Textual analysis, dictionaries and 10-ks. J. Finance 2011, 66, 35–65. [Google Scholar] [CrossRef]

- Loughran, T.; McDonald, B. Textual analysis in accounting and finance: A survey. J. Account. Res. 2016, 54, 1187–1230. [Google Scholar] [CrossRef]

- Rockström, J.; Steffen, W.; Noone, K.; Persson, Å.; Chapin, F.S., III; Lambin, E.; Lenton, T.M.; Scheffer, M.; Folke, C.; Schellnhuber, H.J.; et al. Planetary boundaries: Exploring the safe operating space for humanity. Ecol. Soc. 2009, 14, 1–33. [Google Scholar] [CrossRef]

- Brown, S.J.; Warner, J.B. Using Daily Stock Returns: The Case of Event Studies. J. Finance Econ. 1985, 14, 3–31. [Google Scholar] [CrossRef]

- Ball, B.; Brown, P. An Empirical Evaluation of Accounting Income Numbers. J. Account. Res. 1968, 6, 159–178. [Google Scholar] [CrossRef] [Green Version]

- Fama, E.F.; Fisher, L.; Jensen, M.; Roll, R. The adjustment of stock prices to new information. Int. Econ. Rev. 1969, 10, 1–21. [Google Scholar] [CrossRef]

- Fama, E. Efficient Capital Markets: A Review of Theory and Empirical Work. J. Finance 1970, 31, 143–145. [Google Scholar] [CrossRef]

- Krivin, D.; Patton, R.; Rose, E.; Tabak, D. Determination of the Appropriate Event Window Length in Individual Stock Event Studies. 2003. Available online: https://ssrn.com/abstract=466161 (accessed on 7 April 2021).

- Castro-Iragorri, C. Does the market model provide a good counterfactual for event studies in finance? Financ. Mark. Portf. Manag. 2019, 33, 71–91. [Google Scholar] [CrossRef]

- Cable, J.; Holland, K. Modelling normal returns in event studies: A model-selection approach and pilot study. Eur. J. Financ. 1999, 5, 331–341. [Google Scholar] [CrossRef]

- Coutts, J.A.; Mills, T.C.; Roberts, J. The market model and the event study method: A synthesis of the econometric criticisms. Int. Rev. Financ. Anal. 1994, 3, 149–171. [Google Scholar] [CrossRef]

- Andrew Coutts, J.; Mills, T.C.; Roberts, J. Misspecification of the market model: The implications for event studies. Appl. Econ. Lett. 1995, 2, 163–165. [Google Scholar] [CrossRef]

- Bollerslev, T. Generalised Autoregressive Conditional Heteroskedasticity. J. Econom. 1986, 31, 307–327. [Google Scholar] [CrossRef] [Green Version]

- Nelson, D.B. Conditional heteroskedasticity in asset returns: A new approach. Econometrica. J. Econom. Soc. 1991, 59, 347–370. [Google Scholar] [CrossRef]

- Hall, P. On the removal of skewness by transformation. J. R. Stat. Soc. Ser. B 1992, 54, 221–228. [Google Scholar] [CrossRef]

- Lyon, J.D.; Barber, B.M.; Tsai, C.L. Improved methods for tests of long-run abnormal stock returns. J. Finance 1999, 54, 165–201. [Google Scholar] [CrossRef]

- Banik, S.; Kibria, B.G. Estimating the population coefficient of variation by confidence intervals. Commun. Stat.-Simul. Comput. 2011, 40, 1236–1261. [Google Scholar] [CrossRef]

- Cojbasic, V.; Loncar, D. One-sided confidence intervals for population variances of skewed distributions. J. Stat. Plan. Inference 2011, 141, 1667–1672. [Google Scholar] [CrossRef]

- Bartholdy, J.; Olson, D.; Peare, P. Conducting Event Studies on a Small Stock Exchange. Eur. J. Finance 2007, 13, 227–252. [Google Scholar] [CrossRef]

- Balaban, E.; Constantinou, C.T. Volatility Clustering and Event-Induced Volatility: Evidence from UK Mergers and Acquisitions. Eur. J. Finance 2006, 12, 449–453. [Google Scholar] [CrossRef]

- Schimmer, M.; Levchenko, A.; Müller, S. EventStudyTools (Research Apps), St. Gallen. 2014. Available online: http://www.eventstudytools.com (accessed on 15 June 2020).

- Tierney, J.; Baumeister, R.F. The Power of Bad: And How to Overcome It; Allen Lane: Penguin, UK, 2019. [Google Scholar]

- Corns, J. Rethinking the negativity bias. Rev. Philos. Psychol. 2018, 9, 607–625. [Google Scholar] [CrossRef] [Green Version]

- Metcalf, G.E. On the economics of a carbon tax for the United States. Brook. Pap. Econ. Act. 2019, 1, 405–484. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Companies | North American companies included in the Thomson Reuters Top 100 Global Energy Leaders Ranking 2019 |

| News | GDELT (The Global Database of Events, Language, and Tone), package: GDELT Global Knowledge Graph (GKG) Version 2.0 |

| Stock data | Yahoo Finance |

| USA Companies | Energy | Environmental Consequences Keywords |

|---|---|---|

| Anadarko | Gas | Nitrogen |

| Marathon oil corp | Fossil Fuels | Phosphorus |

| Avangrid | Renewables | Carbon dioxide |

| Chevron corp | Nuclear | CO2 |

| CMS Energy | Coal | Methane |

| ConocoPhillips | Solar | Ozone |

| ExxonMobil | Hydro | Pollution |

| Covia Holding | Wind | Waste |

| First Solar | Biomass | Plastic |

| Halliburton Comp | Geothermal | Footprint |

| Hess Corp | Marine | Aerosol |

| Marathon Oil Corp | Tidal | Global warming |

| Ni Source | Petrochemical | Emissions |

| Occidental Petroelum Corp | Petrol | Greenhouse gas |

| Philips 66 | Petroleum | Air quality |

| Schlumberger | Ethanol | Sea level |

| Sempra Energy | Climate change | |

| Sun Power | Extreme weather | |

| Vestas | Natural resources | |

| Enel | Biodiversity | |

| Toxic | ||

| Extinction | ||

| Nitrogen cycle | ||

| Ocean acidification | ||

| Land use | ||

| Fresh water | ||

| Depletion | ||

| Chemical Pollution | ||

| Overexploitation | ||

| Sustainability | ||

| Ecosystem |

| Tone | Average of Skewness Corrected T | Average of CAAR Value | Average of p Value |

|---|---|---|---|

| Negative | −2.4517 * | −0.0168 | 0.0240 |

| Neutral | −2.2449 * | −0.0142 | 0.0175 |

| Positive | −0.0207 | 0.0001 | 0.0255 |

| Energy | Negative | Neutral | Positive | |||

|---|---|---|---|---|---|---|

| No Statistical Significance | Statistical Significance | No Statistical Significance | Statistical Significance | No Statistical Significance | Statistical Significance | |

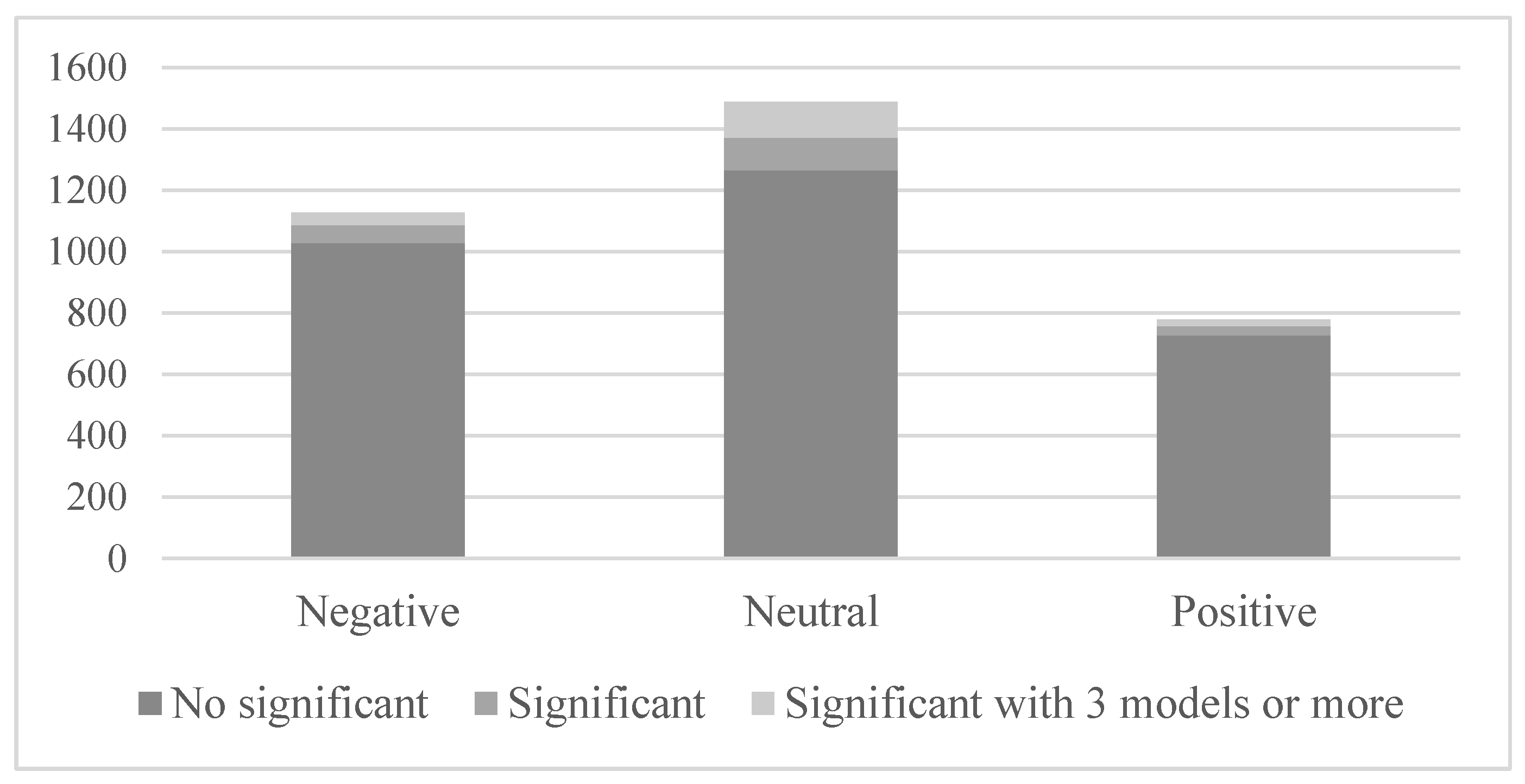

| Fossil fuels | 425 | 26 | 468 | 71 | 319 | 17 |

| Renewables | 488 | 69 | 689 | 141 | 353 | 30 |

| Nuclear | 115 | 4 | 109 | 10 | 55 | 4 |

| Energy | Negative | Neutral | Positive | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Average of Skewness Corrected T | Average of CAAR Value | Average of p Value | Average of Skewness Corrected T | Average of CAAR Value | Average of p Value | Average of Skewness Corrected T | Average of CAAR Value | Average of p Value | |

| Renewables | −2.4699 * | −0.0172 | 0.0221 | −2.4483 * | −0.0152 | 0.0156 | 0.0236 | 0.0006 | 0.0222 |

| Fossil fuels | −2.3697 * | −0.0151 | 0.0293 | −1.7788 | −0.0117 | 0.0177 | 2.1176 * | 0.0114 | 0.0371 |

| Nuclear | −2.4968 * | −0.0132 | 0.0198 | ||||||

| Tone | Average of Cross-Sectional-Corrected-Vy-t-Test | Average of p Value |

|---|---|---|

| Negative | 2.5984 * | 0.0181 |

| Neutral | 2.4758 * | 0.0206 |

| Positive | 2.5231 * | 0.0200 |

| Type of Energy | Negative | Neutral | Positive | |||

|---|---|---|---|---|---|---|

| No Statistical Significance | Statistical Significance | No Statistical Significance | Statistical Significance | No Statistical Significance | Statistical Significance | |

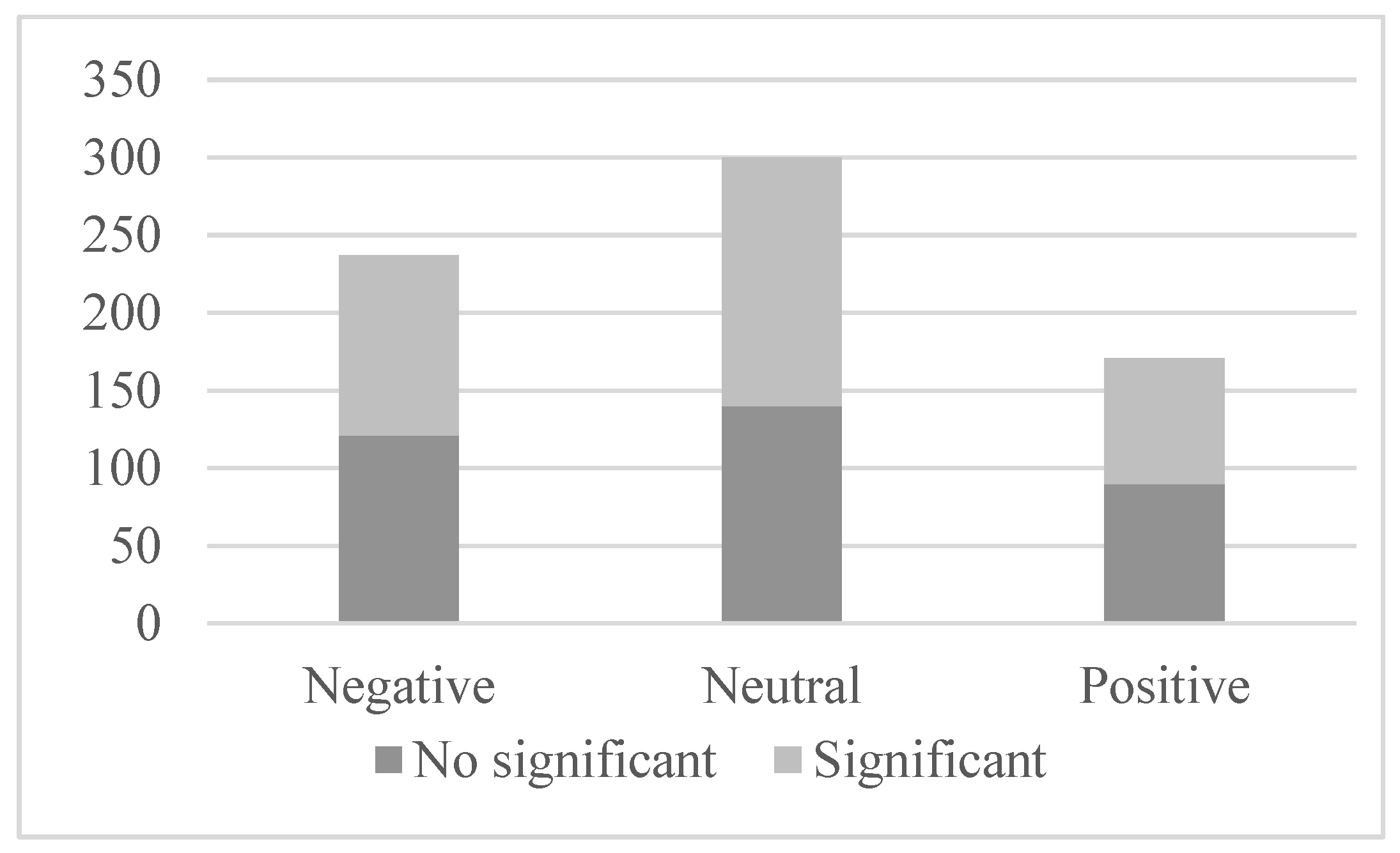

| Fossil fuels | 39 | 52 | 51 | 57 | 32 | 42 |

| Renewables | 72 | 50 | 81 | 87 | 51 | 34 |

| Nuclear | 10 | 14 | 8 | 16 | 7 | 5 |

| Type of Energy | Negative | Neutral | Positive | |||

|---|---|---|---|---|---|---|

| Average of Cross-Sectional-Corrected-Vy-t-Test | Average of p Value | Average of Cross-Sectional-Corrected-Vy-t-Test | Average of p Value | Average of Cross-Sectional-Corrected-Vy-t-Test | Average of p Value | |

| Renewables | 2.4264 * | 0.0217 | 2.3692 * | 0.0237 | 2.3526 * | 0.0272 |

| Fossil fuels | 2.6500 * | 0.0188 | 2.5443 * | 0.0191 | 2.5156 * | 0.0214 |

| Nuclear | 2.4961 * | 0.0175 | 2.5598 * | 0.0179 | 2.3002 * | 0.0270 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Barroso Del Toro, A.; Vivas Crisol, L.; Tort-Martorell, X. The Sustainability Narrative: A Multi Study Using Event Studies to Analyse the American Energy Companies Shareholder’s Reaction to Sustainability News. Int. J. Environ. Res. Public Health 2022, 19, 15489. https://doi.org/10.3390/ijerph192315489

Barroso Del Toro A, Vivas Crisol L, Tort-Martorell X. The Sustainability Narrative: A Multi Study Using Event Studies to Analyse the American Energy Companies Shareholder’s Reaction to Sustainability News. International Journal of Environmental Research and Public Health. 2022; 19(23):15489. https://doi.org/10.3390/ijerph192315489

Chicago/Turabian StyleBarroso Del Toro, Alberto, Laura Vivas Crisol, and Xavier Tort-Martorell. 2022. "The Sustainability Narrative: A Multi Study Using Event Studies to Analyse the American Energy Companies Shareholder’s Reaction to Sustainability News" International Journal of Environmental Research and Public Health 19, no. 23: 15489. https://doi.org/10.3390/ijerph192315489