1. Introduction

The stop strategy integrates components of both the stop-loss and take-profit strategies. The stop-loss strategy limits losses by selling a security when it reaches a predetermined price level below the current market price, while the take-profit strategy locks in profits by selling a security at a predetermined price level above the current market price (Eiteman, 1966) [

1]. Numerous scholarly works have been dedicated to examining the concept of the stop strategy, such as Tschoegl (1988), Osler (2003), and Bensaid and Olivier (2000) [

2,

3,

4]. However, the exit time remains uncertain because investors cannot predict when the price will reach the stopping point due to unpredictable market fluctuations.

The stop strategy is a popular risk management technique used by traders and investors in the stock market. Research conducted by Osler (2003) indicated that the clustering of stop-loss and take-profit orders can help elucidate certain patterns observed in financial markets [

3]. These patterns are commonly utilized by traders in technical analysis. Investors using hedge portfolios and the stop strategy to trade may find that traditional risk measures are not adequate for accurately measuring the risk of their portfolios. This is because hedge portfolios and stop strategies are designed to offset risks and limit losses, which can result in missed opportunities and increased transaction costs. Investors using stop strategies are often concerned with limiting their losses, and the stop point is set as a way to achieve that.

However, since the exit time is uncertain and can be influenced by market conditions, the investor’s focus is on managing risk before reaching the stop point. Once the transaction is closed, the risk measures become irrelevant because the investor is no longer exposed to the market. Traditional risk measures evaluate risk over the entire time horizon, which does not account for the uncertainty in the exit time caused by the stop strategy. Therefore, alternative risk measures may be needed to better capture the dynamics of managing risk with a stop strategy.

Entropy, a term first introduced in 1865 by the German physicist Rudolf Clausius for studying thermodynamics, has been used to gauge order, disorder, and uncertainty across diverse disciplines. Its initial application in finance, pioneered by Philippatos and Wilson for portfolio selection [

5], has since broadened to encompass asset pricing and option pricing, solidifying its role as a key tool in financial research and decision-making. Shannon entropy can be applied to measure the degree of uncertain of a portfolio’s return [

5]. However, it can also be used to measure the degree of diversification of investments [

6].

DEA is a nonparametric linear programming technique used to assess the efficiency and productivity of decision-making units (DMUs). Originally introduced as a managerial and performance measurement tool in the late 1970s, DEA has since seen extensive application and adaptations across diverse fields and industries. Notably, it has gained significance in portfolio and asset pricing research, where it aids in measuring the relative efficiencies and improving portfolios’ performance (Eberlein and Keller, 2023) [

7].

The conventional DEA models typically assume that all inputs and outputs are non-negative; however, in the case of asset returns, both positive and negative values may be encountered over a certain period. As a solution to this challenge, we utilized the range directional measure (RDM) model, which has been specifically designed to address negative rates of return, as recommended by Portela et al. (2004) [

8].

Markowitz (1952) developed the modern portfolio theory, which utilizes the expected return and risk to optimize portfolios and diversify investments [

9]. He introduced the mean-variance model to consider an asset’s anticipated return and risk. Various studies have investigated the optimization of stock portfolios using the mean-variance model introduced by Merton (1969, 1971), Magill and Constantinides (1976), and Davis and Norman (1990) [

10,

11,

12,

13]. However, the model has faced criticism due to its reliance on variance as a measure of risk.

The SPP risk measure is a proposed solution to the limitations of the existing risk measures in capturing the specific risks associated with stop strategies, such as price volatility and the uncertainty of the exit time [

14]. By accounting for these factors, the SPP risk measure aims to provide a more comprehensive and accurate evaluation of the risk for investors using stop strategies. This measure could be useful in helping investors make more informed decisions about their risk management strategies and potentially improve their overall portfolio performance.

In 1995, Konno and Shirakawa used an optimization approach to find the optimal stock portfolio with minimum semi-variance [

15]. In the 1990s, the “value at risk” measure was proposed as another risk measure, which expresses the maximum potential losses an investor could face when choosing different assets or portfolios. The VaR model was first introduced as a means of managing risk in their own trading and investment portfolios [

16]. Baumol (1963) introduced the idea of value at risk (VaR) for the first time, although it was not widely used until much later [

17]. This was used while studying a model named “the confidence limit criterion of expected earnings,” which attempted to estimate the highest potential loss with a certain level of certainty. Artzner et al. (1999) introduced the concept of coherent risk measures, which are alternatives to the value at risk (VaR) measure [

18]. They argued that VaR lacks two important properties: subadditivity and convexity. Mausser and Rosen (1998) showed that the VaR measure has multiple local minima in the optimization process [

19].

The problem with local minima is that the optimization algorithm may not find the optimal combination of assets, leading to suboptimal portfolios and inaccurate risk estimates. VaR only considers the probability of a loss exceeding a certain threshold, but it does not account for the magnitude of the loss beyond that threshold or the tail risk associated with extreme events [

18].

Rockafellar and Uryasev (2002) suggested a risk measure called the conditional value at risk (CVaR) as a way to address the limitations of VaR [

20]. CVaR is a consistent risk measure that satisfies subadditivity and convexity, making it advantageous for dealing with securities. Its adoption can lead to more reliable risk management in securities markets [

21].

Pflug and Swietanowski (2000), Rockafellar and Uryasev (2002), and Ogryczak and Ruszczynski (2002) have contributed to the development of the CVaR method from different perspectives [

20,

21,

22]. Chekhlov, Uryasev, and Zabarankin, (2004) were the first to apply the CVaR minimization method to optimization problems [

23]. An important consideration often overlooked in existing portfolio optimization methods is the investor’s exit time. To address this issue, the SPP-CVaR measure was developed by Bin (2015), which builds on the strengths of the CVaR measure and incorporates the exit time as a key factor [

14].

This study investigated evaluations of the performance of assets when investors implement a stop strategy using the SPP-CVaR measure and Shannon entropy. In evaluating an asset’s efficacy, we utilized a model inspired by the range directional measure (RDM) model, which has been intricately adapted to cater to scenarios involving negative rates of return.

At the outset of our analysis, we computed the efficiency of an asset without considering its exit time, using the mean-CVaR model. Subsequently, we included the variable of exit time in our analysis and then added Shannon entropy to further enhance our approach. Calculation of the SPP-CVaR involves estimating the risk-neutral density using kernel density estimation, transforming it into the real-world density with a beta distribution, and calibrating the parameters. Price path simulations were generated, considering genuine market probabilities and risk. Real and SPP densities for prices and exit times were derived, incorporating predefined stop-profit points. Random entry times were simulated to improve the accuracy of the distribution of exit time. By applying the density transfer function, the SPP of the density of exit time was obtained.

Finally, the SPP-CVaR was calculated, focusing on critical investment exit times to quantify severe financial risk. Similarly, we calculated the mean return until the exit time, mirroring the process used for the SPP-CVaR. We then utilized the SPP-CVaR as an input and the mean return as an output in our model, enabling us to calculate the efficiency score of an asset. By incorporating the exit time and Shannon entropy, we found that the efficiency was more accurate. This enhancement could lead to several benefits, as we constructed a variety of portfolios catering to different time horizons, including short-term options (10 days, 20 days, 1 month, and 90 days), as well as a long-term portfolio.

These portfolios play a significant role in assisting investors and portfolio managers in their investment endeavors. By providing tailored investment strategies, they empower individuals to make informed decisions and effectively pursue their financial objectives. The incorporation of stop-profit points enables investors to secure profits and mitigate risks. Through the application of SPP-CVaR risk measures, we assessed the downside risk, facilitating informed allocation of the risk. Furthermore, incorporation of the exit time and the integration of Shannon entropy enhanced the decision-making efficiency. Efficiency scores were then utilized to optimize combinations of asset, aiding in the selection of suitable options. This comprehensive approach may empower investors to minimize risk, maximize returns, and make strategic choices aligned with their investment goals. Additionally, these measures provide valuable insights for company managers for informing risk reduction strategies and driving overall profitability.

The rest of this article is structured in the following manner.

Section 2 presents the mathematical definitions and formulas. The methodology is explained in

Section 3.

Section 4 includes the experimental testing of the methodology and a comparison of the two models. Finally,

Section 5 presents the conclusion.

3. DEA-Based Evaluation Model of Assets’ Performance

This section assesses assets’ performance in two distinct ways: first, over the entire time horizon using the CVaR risk measure, and second, up to the point of the investor’s exit time using the SPP-CVaR risk measure. The purpose was to compare performance between the two modes and assess the impact of the exit time on the assets’ performance. The subsequent subsections provide a detailed analysis and the results.

3.1. Evaluation of Assets’ Performance over the Entire Time Horizon Using Traditional Risk Measures

Based on the RDM model, the mean-CVaR model was proposed by Banihashemi and Navidi (2017) and can be described as follows [

25]:

In this model, is the expected return of the asset, is the proportion of the portfolio’s initial value invested in asset and is an n-vector of variable . Moreover, is the return of the asset and is a vector that shows the direction in which is to be maximized. The process of determining the is similar to the model. If the value of assigned to the asset being evaluated is zero, then that asset is considered to be efficient. Alternatively, the efficiency of an asset can be represented as .

3.2. SPP-CVaR-Based Evaluation of Portfolios’ Performance

In this section, we introduce a model to evaluate the performance of an asset (or a portfolio) in a mean return–risk framework under the exit time and entropy. Unlike the previous model, this model considers the risks before the exit point, as exiting a transaction eliminates further exposure to the associated risks. Our model was inspired by the RDM model, with the risk (SPP-CVaR) and mean return considered as the only input and output, respectively, that use the uncertainty of the exit time. We used a sophisticated framework to determine the input and output of this model.

The computation of the stop-profit point–conditional value at risk (SPP-CVaR) is a comprehensive process that amalgamates statistical techniques, calibration methodologies, and simulation procedures. The overarching aim of this algorithm is to provide a robust framework for assessing the potential downside risks and tail outcomes associated with a given investment. This is achieved by taking both the real-world dynamics and the stochastic nature of the stop-profit points into account.

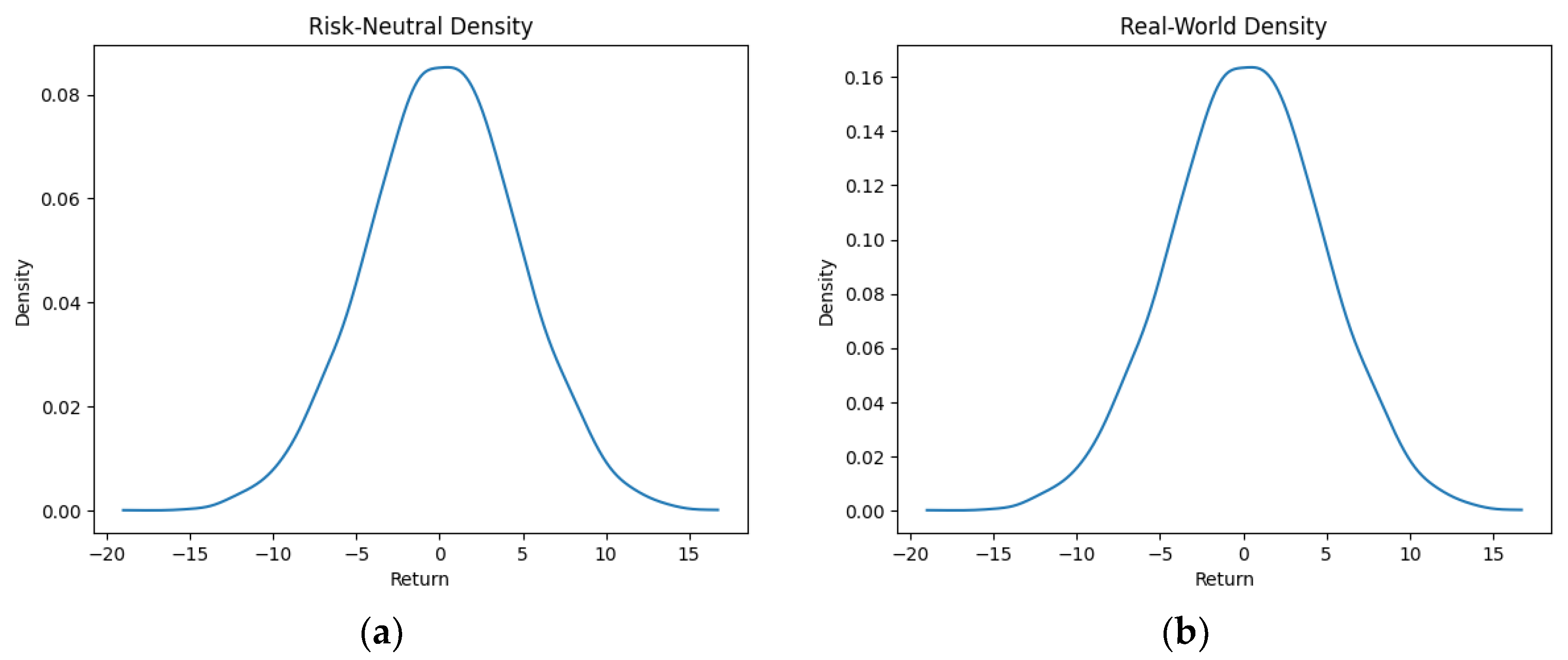

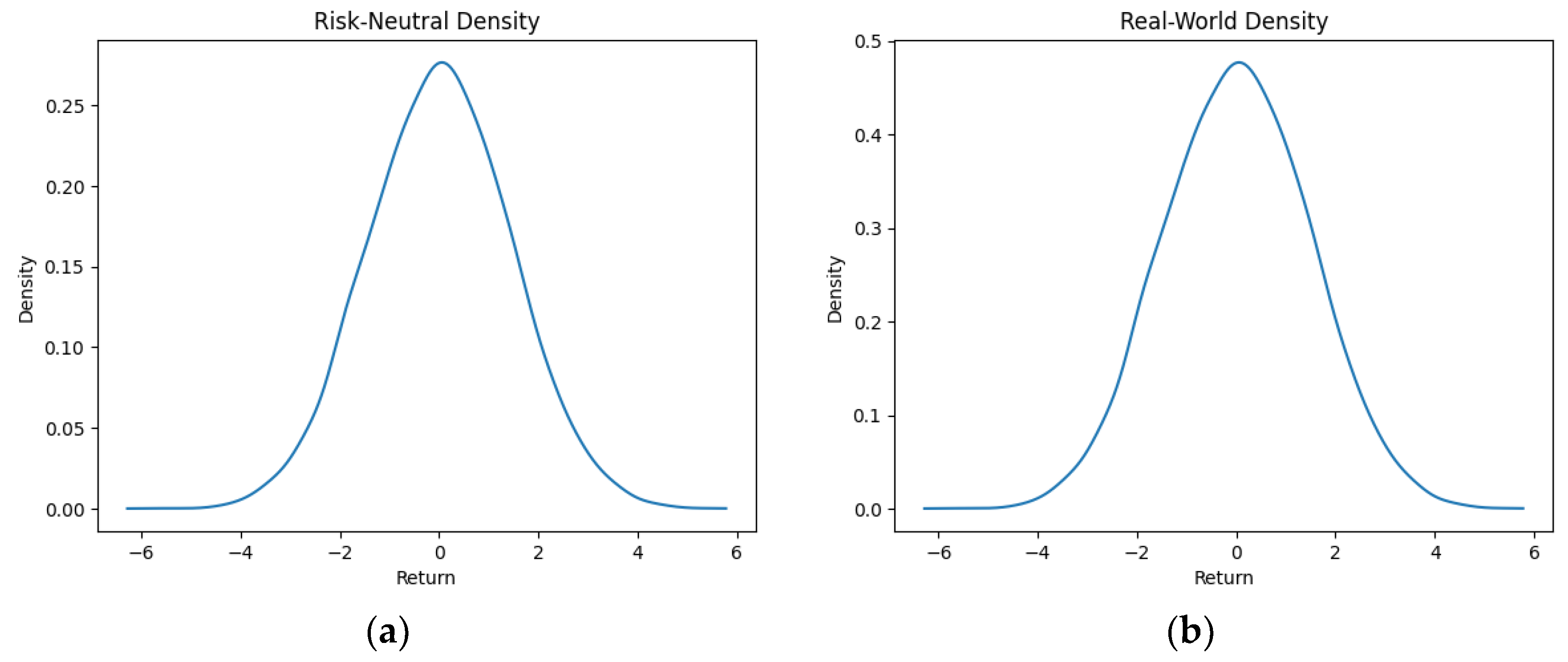

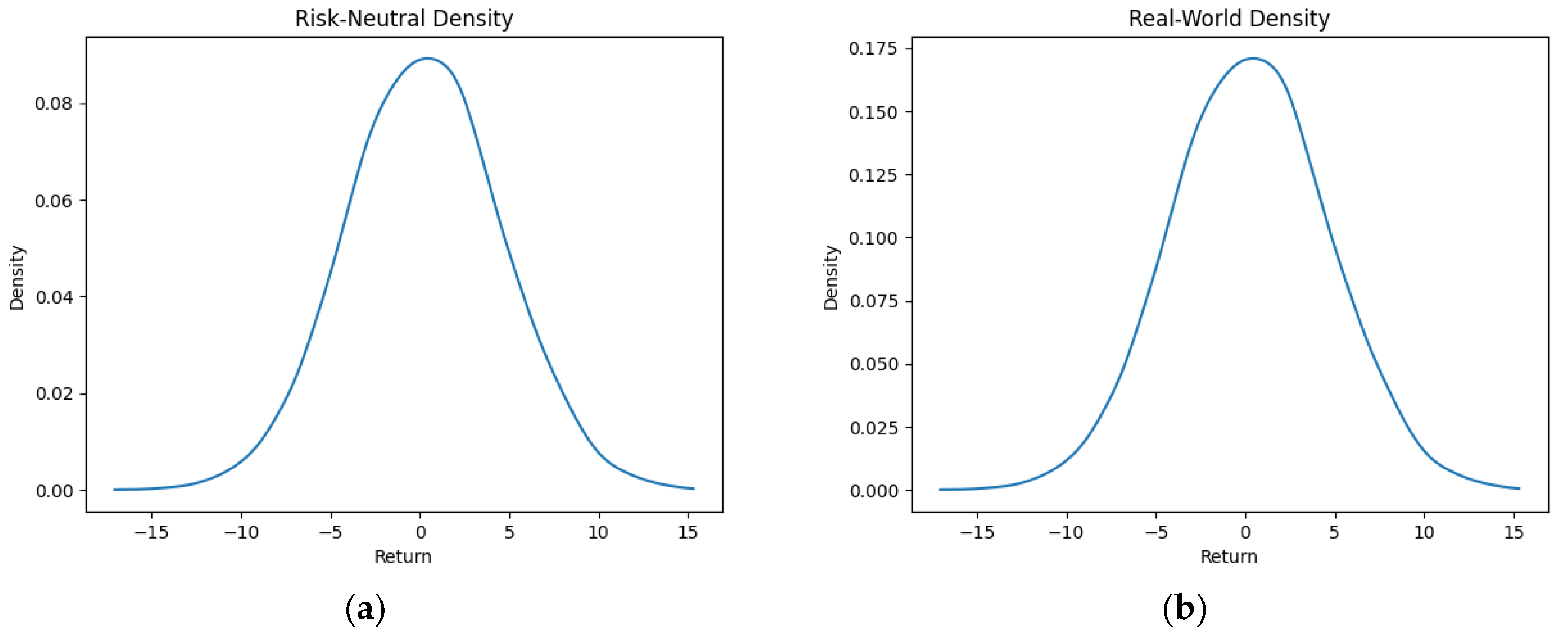

We began by obtaining the risk-neutral density through the application of kernel density estimation, a technique that captures the market’s sentiment and expectations by meticulously analyzing historical data. Subsequently, we utilized a beta distribution to transform this risk-neutral density into a real-world density. The parameters of a beta distribution that align with the risk-neutral density were determined using maximum likelihood estimation. We then computed the real-world density by applying the calibration function and the estimated parameters of the beta distribution.

Once the real-world density had been derived, we calibrated the real-world parameters through an optimization procedure. This procedure aimed to minimize a specific objective function and was designed to quantify the discrepancy between the real-world density and the density of the returns simulated from a normal distribution with predetermined drift and volatility parameters.

After calibration, we generated a price path simulation with the real-world measure. This measure was based on the genuine probabilities of events occurring in reality, and it also accounted for the inherent risk and uncertainty in the financial market.

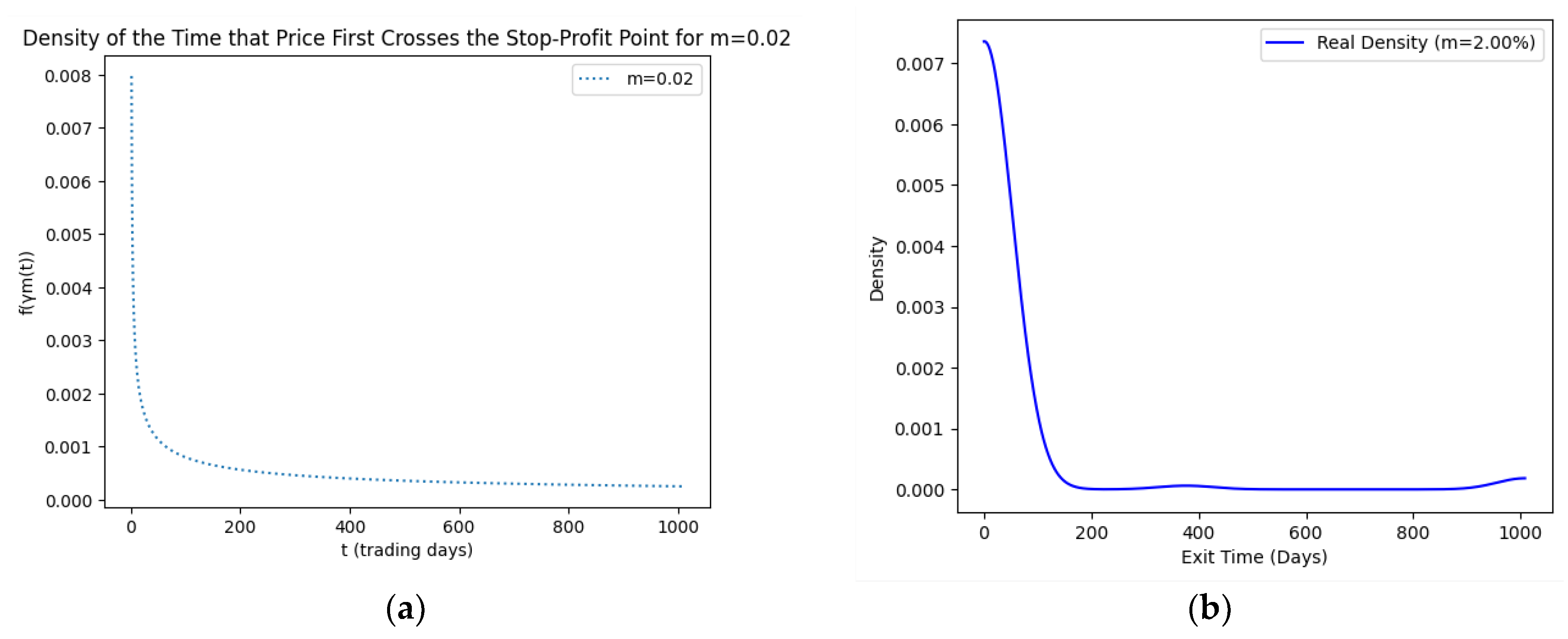

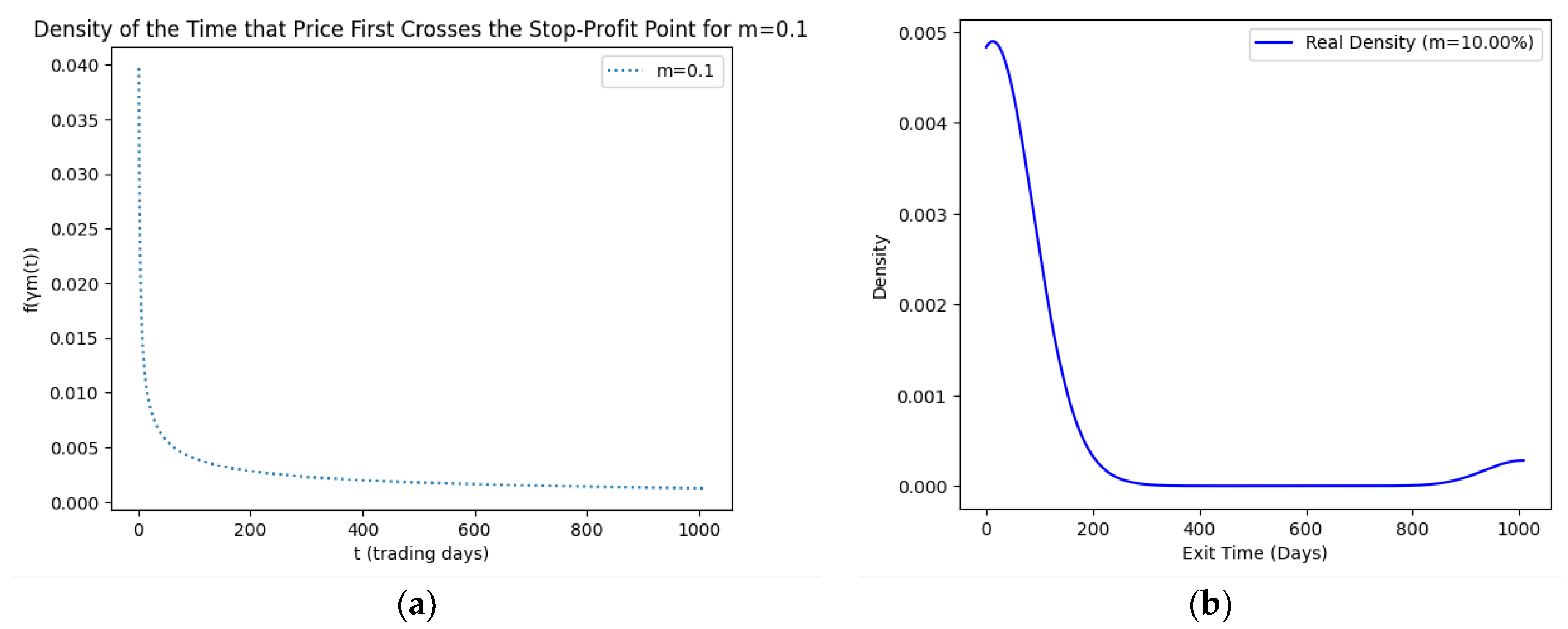

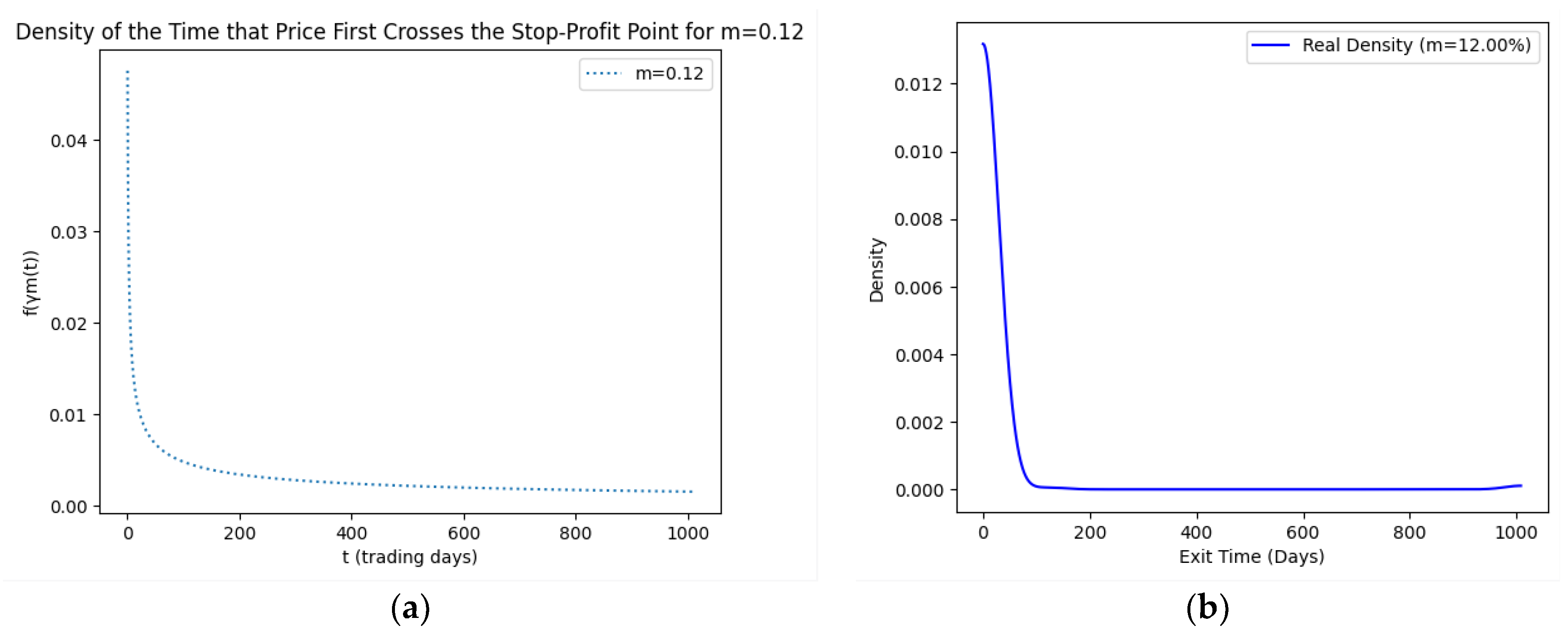

In the subsequent step, we derived both the real and SPP density for the distribution of the price and exit time. This is a critical step for the computation of the SPP-CVaR. The real density reflects the true probability distribution of prices, while the SPP density integrates the concept of stop-profit points based on predefined profit levels. The stop-profit point was defined as a set that included 2%, 4%, 6%, 8%, 10%, and 12%.

Assuming that the investment entry time, represented as t, followed a uniform distribution, we executed a simulation of 250 random entry times. This simulation was crucial in deriving a more precise distribution of the exit times. The exit time for all 250 random entry times was computed to generate an exit time series, which aided in acquiring the distribution of real exit times using the kernel method. By implementing the density transfer function, we obtained the of density the SPP exit time.

The final stage of our process involved calculating the SPP-CVaR, a metric that quantifies the risk of severe financial loss linked to the stop-profit points. The SPP-CVaR is determined by the exit time, meaning it does not consider the full investment period. This approach offers a unique advantage, as it focuses on the critical moments of exiting from the investment, providing a more targeted and relevant measure of extreme risk, rather than diluting the risk assessment over the entire investment timeline.

In a similar vein to the SPP-CVaR, we also computed the mean return of the asset up until the point of the investor’s exit time.

Assuming that

are the log of the returns of a specific asset up to the exit time and regarding the negative return, we defined the vector

such that

where

This vector is a range of possible improvements in the input and output. The

is the value of the risk, and

is the mean return of the asset. Then we solvef the following nonlinear model:

where

,

.

The optimal solution indicates the inefficiency score of the asset under evaluation, and the asset is efficient when the inefficiency score is zero. The term for entropy was incorporated into the model conditionally, with ranging between zero and the natural logarithm of . This proves beneficial when investors encounter numerous inefficiencies across a wide range of assets, making the construction of a portfolio challenging. Thus, entropy enhances efficiency, clarifying the investment process by aiding in the selection of the best assets from the available pool.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}