The Complexity Behavior of Big and Small Trading Orders in the Chinese Stock Market

Abstract

:1. Introduction

2. Data and Methodology

2.1. Data

2.2. MFDFA Method

- Step 1

- Construct a time series side, where

- Step 2

- Split the sub-interval

- Step 3

- Local trend elimination

- Step 4

- Calculates the volatility function, where q is not equal to 0

- Step 5

- Calculates the scale variable

2.3. MCCS Method

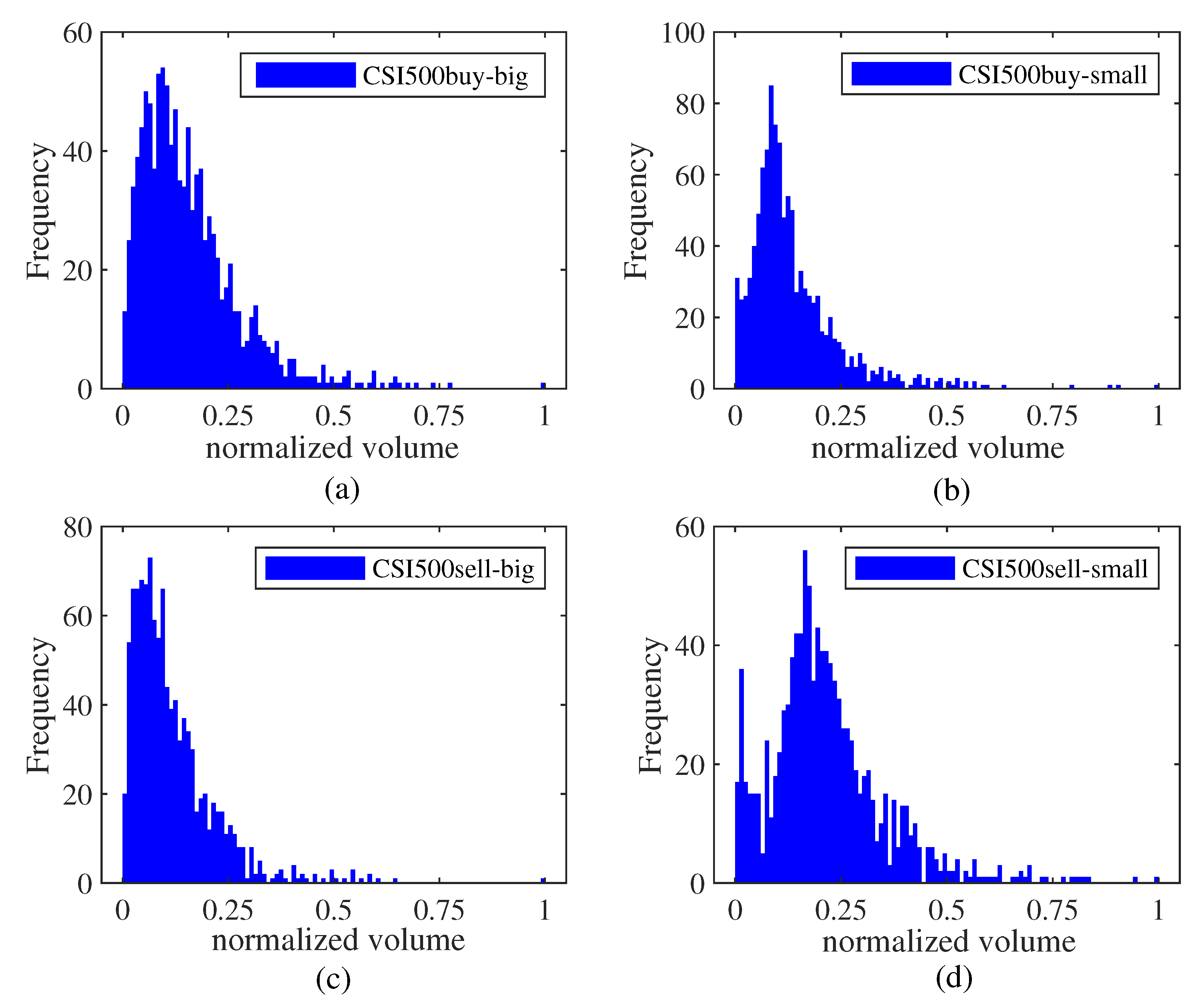

3. Explanatory Analysis

4. Results and Discussion

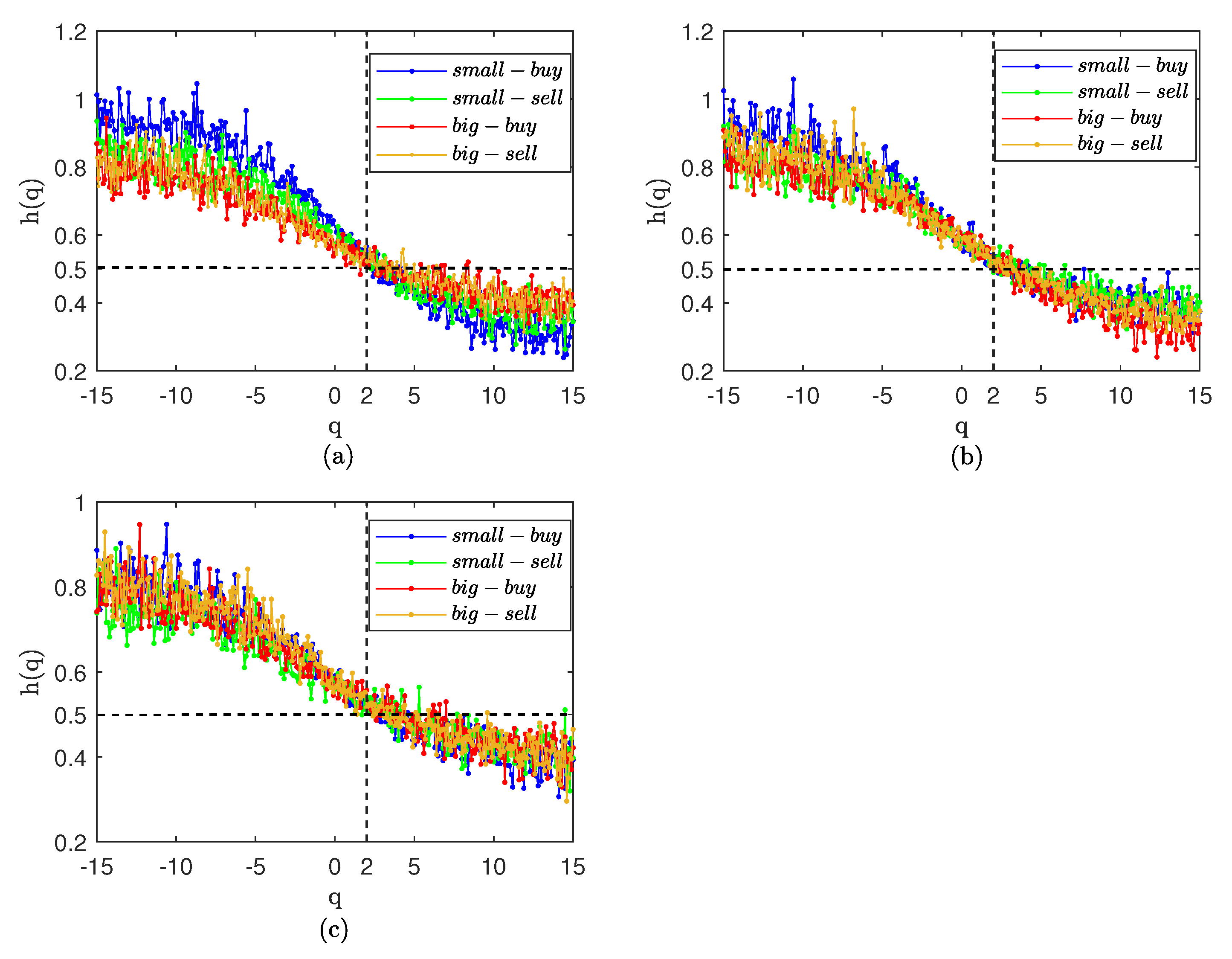

4.1. Fractal Characteristics of Big and Small Orders

4.2. The Complexity Synchronization Characteristic of Orders

4.3. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| CSI300 | China Securities 300 Index. |

| SSE50 | Shanghai Stock Exchange 50 Index |

| CSI500 | China Securities 500 Index |

References

- Zhang, S.W.; Fang, W. Multifractal Behaviors of Stock Indices and Their Ability to Improve Forecasting in a Volatility Clustering Period. Entropy 2021, 23, 1018. [Google Scholar] [CrossRef] [PubMed]

- Li, Y.; Vilela, A.L.M.; Stanley, H.E. The institutional characteristics of multifractal spectrum of China’s stock market. Phys. A 2020, 550, 124129. [Google Scholar] [CrossRef]

- Easley, D.; de Prado, M.L.; O’Hara, M. Discerning information from trade data. J. Financ. Econ. 2016, 120, 269–285. [Google Scholar] [CrossRef]

- Guasoni, P.; Weber, M. Dynamic Trading Volume. Math. Financ. 2017, 27, 313–349. [Google Scholar] [CrossRef]

- Barclay, M.J.; Hendershott, T. A comparison of trading and non-trading mechanisms for price discovery. J. Emp. Financ. 2008, 15, 839–849. [Google Scholar] [CrossRef]

- Gagnon, L.; Karolyi, G.A. Information, Trading Volume, and International Stock Return Comovements: Evidence from Cross-Listed Stocks. J. Financ. Quant. Anal. 2009, 44, 953–986. [Google Scholar] [CrossRef] [Green Version]

- Koubaa, Y.; Slim, S. The relationship between trading activity and stock market volatility: Does the volume threshold matter? Econ. Model 2019, 82, 168–184. [Google Scholar] [CrossRef]

- Sheng, X.; Brzeszczynski, J.; Ibrahim, B.M. International stock return co-movements and trading activity. Financ. Res. Lett. 2017, 23, 12–18. [Google Scholar] [CrossRef]

- Han, Y.F.; Huang, D.S.; Huang, D.Y.; Zhou, G.F. Expected return, volume, and mispricing. J. Financ. Econ. 2022, 143, 1295–1315. [Google Scholar] [CrossRef]

- Zhong, A.; Chai, D.; Li, B.; Chiah, M. Volume shocks and stock returns: An alternative test. Pac-Basin. Financ. J. 2018, 48, 1–16. [Google Scholar] [CrossRef]

- Rodriguez, E.; Alvarez-Ramirez, J. Time-varying cross-correlation between trading volume and returns in US stock markets. Phys. A 2021, 581, 126211. [Google Scholar] [CrossRef]

- Graczyk, M.B.; Duarte Queirós, S.M. Volatility-Trading volume intraday correlation profiles and its nonstationary features. Phys. A 2018, 508, 28–34. [Google Scholar] [CrossRef]

- Bouri, E.; Lau, M.C.K.; Lucey, B.; Roubaud, D. Trading volume and the predictability of return and volatility in the cryptocurrency market. Financ. Res. Lett. 2019, 29, 340–346. [Google Scholar] [CrossRef] [Green Version]

- Sensoy, A.; Serdengeçti, S. Intraday volume-volatility nexus in the FX markets: Evidence from an emerging market. Int. Rev. Financ. Anal. 2019, 64, 1–12. [Google Scholar] [CrossRef]

- Hrdlicka, C. Trading Volume and Time Varying Betas. Rev. Financ. 2022, 26, 79–116. [Google Scholar] [CrossRef]

- Li, D.; Li, G. Whose Disagreement Matters? Household Belief Dispersion and Stock Trading Volume. Rev. Financ. 2021, 25, 1859–1900. [Google Scholar] [CrossRef]

- Chiah, M.; Zhong, A. Trading from home: The impact of COVID-19 on trading volume around the world. Financ. Res. Lett. 2020, 37, 101784. [Google Scholar] [CrossRef]

- Covrig, V.; Ng, L. Volume autocorrelation, information, and investor trading. J. Bank Financ. 2004, 28, 2155–2174. [Google Scholar] [CrossRef]

- Lee, S.Y.; Hwang, D.I.; Kim, M.J.; Koh, I.G.; Kim., S.Y. Cross-correlations in volume space: Differences between buy and sell volumes. Phys. A 2011, 390, 837–846. [Google Scholar] [CrossRef]

- Plerou, V.; Gopikrishnan, P.; Rosenow, B.; Amaral, L.; Stanley, H.E. Econophysics: Financial time series from a statistical physics point of view. Phys. A 2000, 279, 443–456. [Google Scholar] [CrossRef]

- Peters, E. Fractal Market Analysis. Applying Chaos Theory to Investment and Analysis; Wiley: New York, NY, USA, 1994. [Google Scholar]

- Hurst, H.E. A suggested statistical model of some time series which occur in nature. Nature 1951, 180, 494. [Google Scholar] [CrossRef]

- Mandelbrot, B.B.; Ness, J.W.V. Fractional Brownian motions: Fractional noises and applications. SIAM Rev. 1968, 10, 422–437. [Google Scholar] [CrossRef]

- Peng, C.K.; Buldyrev, S.; Havlin, S.; Simons, M.; Stanley, H.E.; Goldberger, A.L. Mosaic organization of DNA nucleotides. Phys. Rev. E 1994, 49, 1685–1689. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Kantelhardt, J.W.; Zschiegner, S.A.; Koscienlny-Bunde, E.; Bunde, A.; Havlin, S.; Stanley, H.E. Multifractal detrended fluctuation analysis of nonstationary. Phys. A 2002, 316, 87–114. [Google Scholar] [CrossRef] [Green Version]

- Chorowski, M.; Kutner, R. Multifractal Company Market: An Application to the Stock Market Indices. Entropy 2022, 24, 130. [Google Scholar] [CrossRef]

- Xu, C.; Ke, J.; Peng, Z.; Fang, W.; Duan, Y. Asymmetric Fractal Characteristics and Market Efficiency Analysis of Style Stock Indices. Entropy 2022, 24, 969. [Google Scholar] [CrossRef]

- Fernandes, L.H.S.; de Araújo, F.H.A.; Silva, I.E.M. The (in)efficiency of NYMEX energy futures: A multifractal analysis. Phys. A 2020, 556, 124783. [Google Scholar] [CrossRef]

- Li, J.F.; Lu, X.S.; Jiang, W.; Petrova, V.S. Multifractal Cross-correlations between foreign exchange rates and interest rate spreads. Phys. A 2021, 574, 125983. [Google Scholar] [CrossRef]

- Zhang, X.; Yang, L.S.; Zhu, Y.M. Analysis of multifractal characterization of Bitcoin market based on multifractal detrended fluctuation analysis. Phys. A 2019, 523, 973–983. [Google Scholar] [CrossRef]

- Fang, W.; Tian, S.L.; Wang, J. Multiscale fluctuations and complexity synchronization of Bitcoin in China and US markets. Phys. A 2018, 512, 109–120. [Google Scholar] [CrossRef]

- Thompson, J.R.; Wilson, J.R. Multifractal detrended fluctuation analysis: Practical applications to financial time series. Math. Comput. Simul. 2016, 126, 63–88. [Google Scholar] [CrossRef]

- Deng, Y. Deng entropy. Chaos Soliton. Fract. 2016, 91, 549–553. [Google Scholar] [CrossRef]

- Rostaghi, M.; Azami, H. Dispersion Entropy: A Measure for Time-Series Analysis. IEEE Signal. Proc. Let. 2016, 23, 610–614. [Google Scholar] [CrossRef]

- Wu, S.D.; Wu, C.W.; Lin, S.G.; Wang, C.C.; Lee, K.Y. Time Series Analysis Using Composite Multiscale Entropy. Entropy 2013, 15, 1069–1084. [Google Scholar] [CrossRef] [Green Version]

- Philippatos, G.C.; Wilson, C.J. Entropy, market risk, and the selection of efficient portfolios. Appl. Econ. 1972, 4, 209–220. [Google Scholar] [CrossRef]

- Gulko, L. The entropy theory of stock option pricing. Int. J. Theoretical. Appl. Financ. 1999, 2, 331–355. [Google Scholar] [CrossRef]

- Sheraz, M.; Dedu, S.; Preda, V. Entropy Measures for Assessing Volatile Markets. Procedia Econ. Financ. 2015, 22, 655–662. [Google Scholar] [CrossRef] [Green Version]

- Abbas, A.E. Entropy methods for adaptive utility elicitation. IEEE Trans. Syst. 2004, 34, 169–178. [Google Scholar] [CrossRef]

- Lv, Q.; Han, L.; Wan, Y.; Yin, L. Stock Net Entropy: Evidence from the Chinese Growth Enterprise Market. Entropy 2018, 20, 805. [Google Scholar] [CrossRef] [Green Version]

- Vinte, C.; Ausloos, M. The Cross-Sectional Intrinsic Entropy—A Comprehensive Stock Market Volatility Estimator. Entropy 2022, 24, 623. [Google Scholar] [CrossRef]

- Shternshis, A.; Mazzarisi, P.; Marmi, S. Efficiency of the Moscow Stock Exchange before 2022. Entropy 2022, 24, 1184. [Google Scholar] [CrossRef] [PubMed]

- Olbrys, J.; Majewska, E. Regularity in Stock Market Indices within Turbulence Periods: The Sample Entropy Approach. Entropy 2022, 24, 921. [Google Scholar] [CrossRef] [PubMed]

- Bian, S.H.; Shang, P.J. Refined two-index entropy and multiscale analysis for complex system. Commun. Nonlinear. Sci. 2016, 39, 233–247. [Google Scholar] [CrossRef]

- Wang, J.; Wang, J. Cross-correlation complexity and synchronization of the financial time series on Potts dynamics. Phys. A 2020, 541, 123286. [Google Scholar] [CrossRef]

- Xing, Y.N.; Wang, J. Linkages between global crude oil market volatility and financial market by complexity synchronization. Empir. Econ. 2019, 59, 2405–2421. [Google Scholar] [CrossRef]

- Pincus, S.M. Approximate entropy as a measure of system complexity. Proc. Natl. Acad. Sci. USA 1991, 88, 2297–2301. [Google Scholar] [CrossRef] [Green Version]

- Richman, J.S.; Moorman, J.R. Physiological time-series analysis using approximate entropy and sample entropy. Am. J. Physiol.-Heart C 2000, 278, 2039–2049. [Google Scholar] [CrossRef] [Green Version]

- Costa, M.; Goldberger, A.L.; Peng, C.K. Multiscale entropy analysis of complex physiologic time series. Phys. Rev. Lett. 2002, 89, 068102. [Google Scholar] [CrossRef] [Green Version]

- Xu, K.X.; Wang, J. Nonlinear multiscale coupling analysis of financial time series based on composite complexity synchronization. Nonlinear Dynam 2016, 86, 441–458. [Google Scholar] [CrossRef]

- Louhichi, W. What drives the volume-volatility relationship on Euronext Paris? Int. Rev. Financ. Anal. 2011, 20, 200–206. [Google Scholar] [CrossRef]

- Suominen, M. Trading volume and information revelation in stock markets. J. Financ. Quant. Anal. 2001, 36, 545–565. [Google Scholar] [CrossRef]

- Wang, S.S.; Xu, K.; Zhang, H. A microstructure study of circuit breakers in the Chinese stock markets. Pac.-Basin Financ. J. 2019, 57, 101174. [Google Scholar] [CrossRef] [Green Version]

- Ormos, M.; Timotity, D. Market microstructure during financial crisis: Dynamics of informed and heuristic-driven trading. Financ. Res. Lett. 2016, 19, 60–66. [Google Scholar] [CrossRef] [Green Version]

- Xu, C.K. The microstructure of the Chinese stock market. China Econ. Rev. 2000, 11, 79–97. [Google Scholar] [CrossRef]

- Alvarez-Ramirez, J.; Rodriguez, E. Temporal variations of serial correlations of trading volume in the US stock market. Phys. A 2012, 391, 4128–4135. [Google Scholar] [CrossRef]

- Shadkhoo, S.; Jafari, G.R. Multifractal detrended cross-correlation analysis of temporal and spatial seismic data. Eur. Phys. J. B 2009, 72, 679–683. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Study | Market | Microstructure Variable | Method | Main Findings |

|---|---|---|---|---|

| Koubaa and Slim [7] | Developed and emerging stock market | Volume and volatility | Non-linear STFIGARCH model | Large volume drives the high volatility regime |

| Barclay and Hendershott [5] | US stock market | Volume and open price | Econometric model | Pre-open trading contributes to the efficiency of the opening price |

| Sheng et al. [8] | Major stock markets | Volume and return | AR-GARCH model | International return spillover effects are sensitive to different levels of trading activity |

| Suominen [52] | / | Volume, volatility and price | Game equilibrium model | Explanation of trading volume containing useful information for predicting volatility |

| Ormos and Timotity [54] | Budapest Stock Exchange | Investor trading | Probabilistic model | Evidence of changes in investors’ trading in the financial crisis |

| Wang et al. [53] | Chinese stock market | Price, volatility and volume | Econometric model | The circuit-breakers do not affect bid-ask spreads and reduce volume and trades |

| Louhichi [51] | CAC40 Index stock market | Volume and volatility | GARCH model | Supporting evidence for strategic asymmetric information hypothesis |

| Xu [55] | Chinese stock market | Volatility and volume | VAR model | High volatility is explained by its lagged volatilities and trading volume |

| Covrig and Ng [18] | US stock market | Volume | Dynamic regressive model | Institutional trading generates a more pronounced effect on volume autocorrelation than individual investor trading |

| Alvarez-Ramírez and Rodríguez [56] | US stock market | Volume | Detrended fluctuation analysis | The strength of correlations exhibits important temporal variations |

| Lee et al. [19] | Korean stock market | Volume | Correlation function | The properties of the correlations of buy and sell volumes differ |

| This study | Chinese stock market | Volume | MFDFA and MCCS |

| Panel A: CSI300 | Buy-Small | Buy-Big | Sell-Small | Sell-Big |

|---|---|---|---|---|

| Obs | 1069 | 1069 | 1069 | 1069 |

| Mean | ||||

| Max | ||||

| Min | ||||

| S.D. | ||||

| Skewness | 3.27 | 2.00 | 2.05 | 1.86 |

| Kurtosis | 17.66 | 7.36 | 6.02 | 5.69 |

| Jarque–Bera | 15,802.23 *** | 3123.95 *** | 2364.75 *** | 2055.29 *** |

| Panel B: SSE50 | buy-small | buy-big | sell-small | sell-big |

| Obs | 1069 | 1069 | 1069 | 1069 |

| Mean | ||||

| Max | ||||

| Min | ||||

| S.D. | ||||

| Skewness | 2.60 | 2.85 | 2.15 | 2.04 |

| Kurtosis | 10.58 | 15.51 | 7.30 | 6.71 |

| Jarque–Bera | 6187.74 *** | 12,162.79 *** | 3192.14 *** | 2745.94 *** |

| Panel C: CSI500 | buy-small | buy-big | sell-small | sell-big |

| Obs | 1069 | 1069 | 1069 | 1069 |

| Mean | ||||

| Max | ||||

| Min | ||||

| S.D. | ||||

| Skewness | 2.52 | 1.80 | 1.42 | 2.33 |

| Kurtosis | 10.73 | 5.24 | 3.66 | 9.90 |

| Jarque–Bera | 6256.93 *** | 1800.07 *** | 955.60 *** | 5333.14 *** |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhu, Y.; Fang, W. The Complexity Behavior of Big and Small Trading Orders in the Chinese Stock Market. Entropy 2023, 25, 102. https://doi.org/10.3390/e25010102

Zhu Y, Fang W. The Complexity Behavior of Big and Small Trading Orders in the Chinese Stock Market. Entropy. 2023; 25(1):102. https://doi.org/10.3390/e25010102

Chicago/Turabian StyleZhu, Yu, and Wen Fang. 2023. "The Complexity Behavior of Big and Small Trading Orders in the Chinese Stock Market" Entropy 25, no. 1: 102. https://doi.org/10.3390/e25010102