Propagation of Bankruptcy Risk over Scale-Free Economic Networks

Abstract

:1. Introduction

2. Related Work

3. Methodology

4. The Scale-Free Model of Financial Contagion Spreading

- (a)

- the network links are kept fixed along time with time-varying strength. The probability p of the diffusion of financial distress from a failed bank (node of the network) to a susceptible one is initially kept constant and, subsequently, we let it depend also on the (susceptible) node’s neighborhood structure. The rationale for this is that the financial distress of a defaultable node can be induced by a failed directly connected node, but it can be also triggered by the defaults of its neighbouring nodes. In a sense, we are arguing that (probably) the default of a big connected node has a much wider impact than that of a small one.In more detail, let be the degree of the i-th node, then the probability of a default of the i-th node at a certain time step is given as:where the sum is taken over all the infected nodes (of index j) connected to the i-th node, with and , with both g and d taking values in the real interval . This equation can be interpreted as follows. The term describes the probability of a spontaneous default. We expect smaller companies to be more volatile; hence, we assumed that the spontaneous default probability is a decreasing power law of the node’s degree k, with the constant Q and the exponent d being model parameters. The second term describes the default triggered by the defaults of the connected nodes; we expect big infected neighbours to have a stronger impact, hence the exponent . In addition, we expect big nodes to be less sensitive to the defaults of small neighbours, so the exponent . One can conclude that the exponents b and d must be equal by arguing that if a certain node of size k is linked to an infected node of equal size k, the probability of a triggered default should be independent of the node size k. To sum up, we have two more model parameters, the constant c and the exponent b, while .

- (b)

- At the simulation start, all the network nodes are susceptible to falling into a default status which is induced into the network by selecting a random node. The simulation run is deemed successful if at least a threshold fraction of 5% of the network nodes fall into default.

- (c)

- The period between the occurrence of financial distress and a subsequent default status is taken to be equal to one time step, which corresponds to an iteration, and each distressed node remains active for one time step. This means that if a node falls into distress at , it will default at time and will neither be susceptible to default again nor induce a bankruptcy risk for any . Here, the idea is that when a bank goes into bankruptcy, it is immediately rescued by ad-hoc financial support policies implemented either by national or international governance bodies;

- (d)

- The networks we use are characterized by the cumulative degree distribution exponent , i.e., the number of nodes n with degree exceeding k scales as ;

- (e)

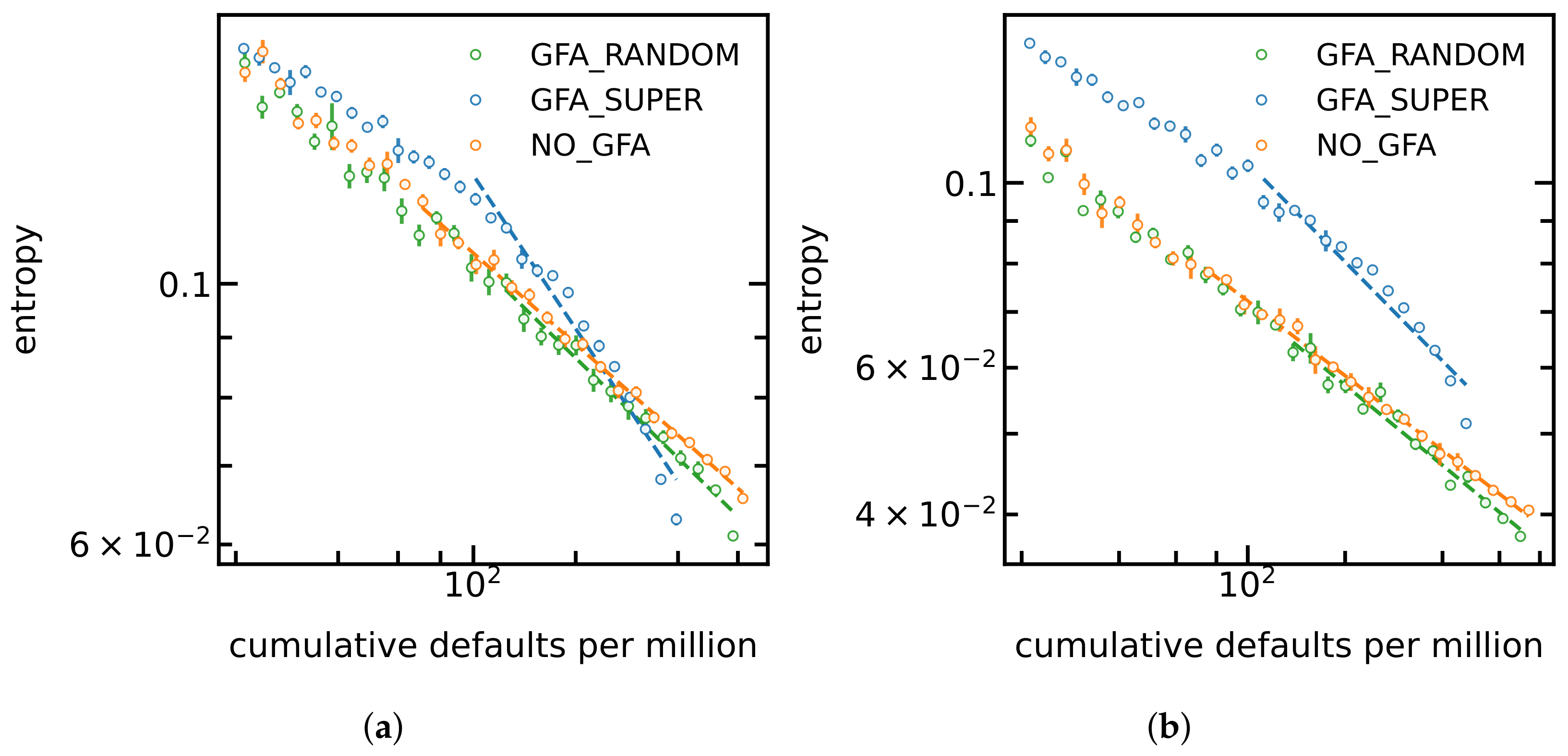

- We also introduce the Shannon Entropy (SE) in order to quantify the complexity of the effective remaining network of healthy nodes with a single number. The SE is a concept introduced by [42] and its applications in information theory as well as in other scientific disciplines are now countless. Entropy is a measure of the randomness in a system: the noisier a system is, the less predictable it becomes and the higher entropy it has. In our case, it reflects the diversity of the nodes.We define the entropy of the network as , where , denotes the number of nodes of degree k and N the total number of nodes in that network. We consider how entropy evolves under different scenarios. The way entropy changes over time basically reflects how many big nodes failed and were “removed” from the network. We expect it to start decreasing during the contagion spreading, as the network is initialized with the full spectrum of node sizes and, as the big nodes become unhealthy and enter into a financial distress/bankruptcy status, the system becomes distributed over a smaller number of states (i.e., nodes of different sizes). Hence, decreasing entropy would imply that self-targeting attacks have been successful in removing big infectious nodes (banks).

5. Results

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| NetworkX scale-free parameters | N = 1000 |

| = 0.1 | |

| = 0.8 | |

| = 0.1 | |

| delta_in = 4.5 | |

| delta_out = 4.5 | |

| Simulations parameters | nr. of runs = 100 |

| max_fails = 10,000 | |

| max_dur = 60 | |

| distress_dur = 1 | |

| min_overall_fail_frac = 5% |

6. Concluding Remarks

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Acemoglu, D.; Ozdaglar, A.; Tahbaz-Salehi, A. Systemic Risk and Stability in Financial Networks. Am. Econ. Rev. 2015, 105, 564–608. [Google Scholar] [CrossRef]

- Benkraiem, R.; Garfatta, R.; Lakhal, F.; Zorgati, I. Financial contagion intensity during the COVID-19 outbreak: A copula approach. Int. Rev. Financ. Anal. 2022, 81, 102136. [Google Scholar] [CrossRef]

- Gajurel, D.; Chawla, A. The oil price crisis and contagion effects on the Canadian economy. Appl. Econ. 2022, 54, 1527–1543. [Google Scholar] [CrossRef]

- Jiang, H.; Tang, S.; Li, L.; Xu, F.; Di, Q. Re-examining the Contagion Channels of Global Financial Crises: Evidence from the Twelve Years since the US Subprime Crisis. Res. Int. Bus. Financ. 2022, 60, 101617. [Google Scholar] [CrossRef]

- Rendón de la Torre, S.; Kalda, J.; Kitt, R.; Engelbrecht, J. On the topologic structure of economic complex networks: Empirical evidence from large scale payment network of Estonia. Chaos Solitons Fractals 2016, 90, 18–27, Challenges in Data Science. [Google Scholar] [CrossRef] [Green Version]

- Rendón de la Torre, S.; Kalda, J.; Kitt, R.; Engelbrecht, J. Fractal and multifractal analysis of complex networks: Estonian network of payments. Eur. Phys. J. B 2017, 90, 234. [Google Scholar] [CrossRef]

- Forte, F.D. Network topology of the Argentine interbank money market. J. Complex Netw. 2021, 8, 87. [Google Scholar] [CrossRef]

- Kolotilin, A.; Panchenko, V. Estimation of a Scale-Free Network Formation Model; UNSW Business School Research Paper; The University of New South Wales: Sydney, Australia, 2018. [Google Scholar]

- Dong, X.; Liu, Y.; Wu, C.; Lian, Y. The topology of scale-free networks with an S-shaped nonlinear growth characteristic. Chaos Solitons Fractals 2019, 121, 137–148. [Google Scholar] [CrossRef]

- Farrell, H.; Newman, A. Weaponized interdependence: How global economic networks shape state coercion. Int. Secur. 2019, 44, 42–79. [Google Scholar] [CrossRef]

- Kalda, J.; Ratas, M.; Kalda, T.; Ramazanli, A.; Herrmann, H.; Belikov, J. The Importance of Superspreaders on the Spread of the Global COVID-19 Pandemic; Working Paper; Elseviaer: Amsterdam, The Netherlands, 2021. [Google Scholar] [CrossRef]

- Dungey, M.; Milunovich, G.; Thorp, S. Unobservable shocks as carriers of contagion. J. Bank. Financ. 2010, 34, 1008–1021. [Google Scholar] [CrossRef] [Green Version]

- Caporin, M.; Pelizzon, L.; Ravazzolo, F.; Rigobon, R. Measuring sovereign contagion in Europe. J. Financ. Stab. 2018, 34, 150–181. [Google Scholar] [CrossRef] [Green Version]

- Fratzscher, M. On currency crises and contagion. Int. J. Financ. Econ. 2003, 8, 109–129. [Google Scholar] [CrossRef] [Green Version]

- Huang, W.; Chen, Z. Modelling contagion of financial crises. North Am. J. Econ. Financ. 2020, 54, 779–831. [Google Scholar] [CrossRef]

- Arruda, B.P.; Pereira, P.L.V. Analysis of the volatility’s dependency structure during the subprime crisis. Appl. Econ. 2013, 45, 5031–5045. [Google Scholar] [CrossRef]

- Ribeiro, A.L.; Hotta, L. An analysis of contagion among Asian countries using the canonical model of contagion. Int. Rev. Financ. Anal. 2013, 29, 62–69. [Google Scholar] [CrossRef]

- Wang, P.; Zong, L. Contagion effects and risk transmission channels in the housing, stock, interest rate and currency markets: An Empirical Study in China and the US. North Am. J. Econ. Financ. 2020, 54, 101113. [Google Scholar] [CrossRef]

- Baur, D. Financial contagion and the real economy. J. Bank. Financ. 2012, 36, 2680–2692. [Google Scholar] [CrossRef] [Green Version]

- Hałaj, G.; Kok, C. Assessing interbank contagion using simulated networks. Comput. Manag. Sci. 2013, 10, 157–186. [Google Scholar] [CrossRef] [Green Version]

- MacDonald, R.; Sogiakas, V.; Tsopanakis, A. Volatility co-movements and spillover effects within the Eurozone economies: A multivariate GARCH approach using the financial stress index. J. Int. Financ. Mark. Institutions Money 2018, 52, 17–36. [Google Scholar] [CrossRef]

- Martin, V.; Gonzalez-Hermosillo, B.; Dungey, M.; Fry-McKibbin, R. Empirical Modelling of Contagion: A Review of Methodologies; Econometric Society 2004 Australasian Meetings 243; Econometric Society: Cleveland, OH, USA, 2004. [Google Scholar]

- Korniyenko, M.Y.; Patnam, M.; del Rio-Chanon, R.M.; Porter, M.A. Evolution of the Global financial Network and Contagion: A New Approach; International Monetary Fund: Washington, DC, USA, 2018. [Google Scholar]

- Bougheas, S. Contagion in networks: Stability and efficiency. Math. Soc. Sci. 2022, 115, 64–77. [Google Scholar] [CrossRef]

- Jiang, S.; Fan, H. Credit risk contagion coupling with sentiment contagion. Phys. A Stat. Mech. Its Appl. 2018, 512, 186–202. [Google Scholar] [CrossRef]

- Cabrales, A.; Gottardi, P.; Vega-Redondo, F. Risk Sharing and Contagion in Networks. Rev. Financ. Stud. 2017, 30, 3086–3127. [Google Scholar] [CrossRef]

- Gong, S.; Zou, H. Simulation of interactive contagion between depositors’ panic and banking risk. Int. J. Financ. Econ. 2022, in press. [Google Scholar] [CrossRef]

- Cerqueti, R.; Deffains-Crapsky, C.; Storani, S. Similarity-based heterogeneity and cohesiveness of networked companies issuing minibonds. Chaos Solitons Fractals 2022, 164, 112654. [Google Scholar] [CrossRef]

- Sharpanskykh, A.; Treur, J. Modelling and analysis of social contagion in dynamic networks. Neurocomputing 2014, 146, 140–150. [Google Scholar] [CrossRef] [Green Version]

- Duan, W.; Chen, Z.; Liu, Z.; Jin, W. Efficient target strategies for contagion in scale-free networks. Phys. Rev. E Stat. Nonlinear Soft Matter Phys. 2005, 72, 026133. [Google Scholar] [CrossRef]

- D’Agostino, G.; Scala, A.; Zlatić, V.; Caldarelli, G. Robustness and assortativity for diffusion-like processes in scale-free networks. EPL (Europhys. Lett.) 2012, 97, 68006. [Google Scholar] [CrossRef] [Green Version]

- Philippas, D.; Koutelidakis, Y.; Leontitsis, A. Insights into European interbank network contagion. Manag. Financ. 2015, 41, 754–772. [Google Scholar] [CrossRef]

- Li, F.; Li, B.; Xu, J. Reinsurance strategy and network contagion: A macroprudential perspective. Appl. Econ. Lett. 2022, 29, 651–656. [Google Scholar] [CrossRef]

- Li, Y.; Guo, C. The Contagion of Associated Credit Risk Based on the Real Estate Companies Network. Procedia Comput. Sci. 2022, 199, 479–486. [Google Scholar] [CrossRef]

- Li, S.; Wang, C. Network structure, portfolio diversification and systemic risk. J. Manag. Sci. Eng. 2021, 6, 235–245. [Google Scholar] [CrossRef]

- Dou, W.; Johnson, S.; Wu, W. Competition Network: Distress Spillovers and Predictable Industry Returns; Working paper; Wharton Finance Faculty: Philadelphia, PA, USA, 10 August 2022. [Google Scholar]

- Barrot, J.N.; Sauvagnat, J. Input Specificity and the Propagation of Idiosyncratic Shocks in Production Networks *. Q. J. Econ. 2016, 131, 1543–1592. [Google Scholar] [CrossRef] [Green Version]

- Atalay, E.; Hortaçsu, A.; Roberts, J.; Syverson, C.; Hansen, L.P. Network structure of production. Proc. Natl. Acad. Sci. USA 2011, 108, 5199–5202. [Google Scholar] [CrossRef] [Green Version]

- Albert, R.; Jeong, H.; Barabási, A.L. Error and attack tolerance of complex networks. Nature 2000, 406, 378–382. [Google Scholar] [CrossRef] [Green Version]

- Crucitti, P.; Latora, V.; Marchiori, M.; Rapisarda, A. Efficiency of scale-free network: Error and attack tolerance. Phys. A Stat. Mech. Its Appl. 2003, 320, 622–642. [Google Scholar] [CrossRef] [Green Version]

- Albert, R.; Barabási, A.L. Statistical mechanics of complex networks. Rev. Mod. Phys. 2002, 74, 47–97. [Google Scholar] [CrossRef] [Green Version]

- Shannon, C.E. A Mathematical Theory of Communication. Bell Syst. Tech. J. 1948, 27, 379–423. [Google Scholar] [CrossRef] [Green Version]

- Hagberg, A.; Schult, D.; Swart, P. Exploring network structure, dynamics, and function using NetworkX. In Proceedings of the 7th Python in Science Conference (SciPy2008), Pasadena, CA, USA, 19–24 August 2008; Varoquaux, G., Vaught, T., Millman, J., Eds.; Los Alamos National Laboratory: Los Alamos, Mexico, 2008; pp. 11–15. [Google Scholar]

- Broido, A.; Clauset, A. Scale-free networks are rare. Nat. Commun. 2019, 10, 1017. [Google Scholar] [CrossRef] [Green Version]

- Cao, J.; Wen, F.; Stanley, H.E. Measuring the systemic risk in indirect financial networks. Eur. J. Financ. 2022, 28, 1053–1098. [Google Scholar] [CrossRef]

- Cont, R.; Schaanning, E. Monitoring indirect contagion. J. Bank. Financ. 2019, 104, 85–102. [Google Scholar] [CrossRef]

- Hagberg, A.; Dan, S.; Swart, P. NetworkX Reference. Available online: https://networkx.org/ (accessed on 1 November 2022).

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Andria, J.; di Tollo, G.; Kalda, J. Propagation of Bankruptcy Risk over Scale-Free Economic Networks. Entropy 2022, 24, 1713. https://doi.org/10.3390/e24121713

Andria J, di Tollo G, Kalda J. Propagation of Bankruptcy Risk over Scale-Free Economic Networks. Entropy. 2022; 24(12):1713. https://doi.org/10.3390/e24121713

Chicago/Turabian StyleAndria, Joseph, Giacomo di Tollo, and Jaan Kalda. 2022. "Propagation of Bankruptcy Risk over Scale-Free Economic Networks" Entropy 24, no. 12: 1713. https://doi.org/10.3390/e24121713