1. Introduction

Let be a probability space and be a fixed terminal time. Let and be two mutually independent processes defined on , where is a one-dimensional Brownian motion and is a -valued Lévy process corresponding to a standard Lévy measure satisfying the following conditions:

- (i)

,

- (ii)

, for some and for every

Let be the natural filtration generated by and .

Throughout this paper, we consider the following integral equation:

where the terminal value

is a given

-measurable square integrable random variable,

is a given map, and

is the orthonormalized Teugel’s martingale of order

i associated with the Lévy process

. The above equation is called backward stochastic differential equations associated with Lévy processes (BSDELs) introduced by Bahlali et al. [

1]. When Equation (

1) is independent of Teugel’s martingales, then Equation (

1) is reduced to the following form:

which is the classical backward stochastic differential equations (BSDEs) introduced by Pardoux and Peng [

2] first. Pardoux and Peng [

2] proved that there exists a unique adapted and square integrable solution of the BSDE (

2) under uniform Lipschitz condition on

g. BSDELs can be seen as a natural generalization of BSDEs. Nualart and Schoutens [

3] provided a martingale representation theorem associated with Lévy processes. Furthermore, Nualart and Schoutens [

4] extended the classical BSDEs to BSDELs and established the existence and uniqueness of solutions for the BSDEL (

1) which is independent of Brownian motion. For more studies on BSDELs, see El Otmani [

5,

6], Ren et al. [

7], Ren and El Otmani [

8], and the references therein.

Briand et al. [

9] first studied the representation theorem for generators of BSDEs under the continuous assumption on the generators with respect to

t and

. Jiang [

10] obtained the representation theorem for Lipschitz generators of BSDEs. Zhang and Fan [

11] provided a representation theorem for generators of BSDEs with infinite time intervals and linear growth generators. For more studies on the representation theorem for generators of BSDEs, we refer to Song et al. [

12], Xiao and Fan [

13], Zheng and Li [

14], Wu and Zhang [

15], and the references therein. In this paper, we are concerned with representation theorem for generators of the BSDELs (

1). For this issue, to our best knowledge, there is no reference available in the literature.

Risk measures have been extensively researched in finance and in the insurance industry such as the adjustment of life insurance rates. To quantify the riskiness of financial positions, Artzner et al. [

16,

17] introduced the concept of coherent risk measure by proposing the theory of axiomatic system of capital requirements. By weakening coherence axioms, Föllmer and Schied [

18] and, independently, Frittelli and Rosazza Gianin [

19] introduced convex risk measures. Their work attracts many researcher’s interest. For example, see Delbaen [

20], Cheridito et al. [

21,

22], Riedel [

23], Rosazza Gianin [

24], Detlefsen and Scandolo [

25], Klöppel and Schweizer [

26], Delbaen et al. [

27], Acciaio et al. [

28], Föllmer and Schied [

29], Song et al. [

30], and the references therein.

BSDEs have become a popular tool for studying dynamic risk measures since Peng [

31] investigated BSDEs and g-expectations. For instance, El Karoui et al. [

32] studied dynamic risk measures for random variables via BSDEs. Jiang [

33] established the one-to-one relationship between the generators BSDEs and the corresponding dynamic risk measures for random variables. Penner and Réveillac [

34] established a link between risk measures for processes and BSDEs and studied the corresponding time-consistent dynamic risk measures for processes induced by BSDEs. Xu [

35] studied multidimensional dynamic convex risk measures induced by conditional g-expectations. Ji et al. [

36] provided some time-consistent dynamic risk measures for processes via BSDEs, and established the one-to-one relationship between the generators BSDEs and the corresponding dynamic risk measures for processes. A essential property for dynamic risk measures is time-consistency (see Bion-Nadal [

37,

38]). These time-consistent dynamic risk measures are constructed by BSDEs where the financial positions are random variables at some terminal time. However, time-inconsistent preference is realistic in financial markets. For example, see Yong [

39], Wang and Shi [

40], and Agram [

41].

In this paper, we study dynamic risk measures induced by BSDELs. In a financial market, jump dynamics, which might be caused by policy interference, natural accidents, and so on, indeed exist. For instance, a stock’s price and its return show abnormal and sharp volatility. Thus, investors can be risk-averse and master the best time of those jump dynamics if they have sufficient awareness. Therefore, the processes of stock price and its return can be modeled by BSDELs (

1). Based on the above consideration, we construct dynamic risk measures by means of BSDELs (

1). First, the representation theorem for generators of BSDELs is provided. Second, the time-consistency of the coherent and convex dynamic risk measures for processes is characterized by means of the generators of BSDELs. Moreover, the coherency and convexity of dynamic risk measures for processes are characterized by the generators of BSDELs. Finally, we provide two numerical examples to illustrate the proposed dynamic risk measures. The obtained results extends the results of Briand et al. [

9], Jiang [

10], Penner and Réveillac [

34], and Ji et al. [

36].

The rest of the paper is organized as follows. In

Section 2, we briefly state some preliminaries including the definitions of time-consistent dynamic convex and coherent risk measures for processes and some results on BSDELs. The definition of dynamic risk measures for processes induced by BSDELs is also provided in

Section 2. In

Section 3, our main results are presented, that is, the coherency and convexity of dynamic risk measures for processes are characterized by the generators of BSDELs, and the representation theorem for generators of BSDELs is provided.

Section 4 contains all the proofs of the main results of this paper. We provide two numerical examples to illustrate the proposed dynamic risk measures in

Section 5. Finally, conclusions are summarized.

4. Proofs of Main Results

In this section, we will provide the proof of Lemma 1 and all proofs of the results stated in

Section 3.

Proof of Lemma 1. In order to prove the existence and uniqueness of the solution of BSDEL (

6), we define a new function

as

where

It is easy to see that

satisfies the Lipschitz condition (H2). Therefore, we only need to show that

satisfies assumption (H1). By using assumption (H2), we obtain for all

Notice that

g satisfies assumption (H1) and

. By taking mathematical expectation, we immediately deduce that

Thus,

satisfies assumption (H1). □

In order to prove Theorem 1, we need to have two additional results. The following Proposition 3 comes from Proposition 2.2 of Jiang [

33]. Proposition 4 concerning on a priori estimate for BSDELs is new and needs to be proved.

Proposition 3. Let and . For any ()-progressively measurable process satisfying , the following equalityholds true for almost every . Proposition 4. Assume that g satisfies (H1) and (H2). Denote by the solution of BSDEL (3) corresponding to . Then we havewhere C is a positive constant and . Proof. By Itô’s formula (see Theorem 32 of Protter [

43], Page 78), for any constant

, we have

Applying the Lipschitz condition (H2) to

g and then the inequality

, we deduce that

Taking

, from (

10) and (

11), we have

Therefore, we get

and

By Burkholder–Davis–Gundys inequality (see Theorem 48 of Protter [

43], Page 193) and then the inequality

, we have

Using Burkholder–Davis–Gundys inequality again, we easily deduce that

Similarly, by Burkholder–Davis–Gundys inequality,

and then Jensen’s inequality (see Theorem 19 of Protter [

43], Page 11), we have

Therefore, we have

Finally, combining (

13) and (

18), there exists a constant

such that

Thus, we have completed the proof of this proposition. □

Based on Propositions 3 and 4, we can prove Theorem 1.

Proof of Theorem 1. Let us pick

small enough such that

. Suppose that

g satisfies (H1) and (H2). For any given

, we consider the following BSDEL:

Then, there exists a unique adapted solution in

, denoted by

, solving BSDEL (

19)

For any given

and

, let us set

Applying Itô’s formula to

, we have

Then, there exists a unique adapted solution in

, denoted by

, solving BSDEL (

20).

By Proposition 4, Lipschitz condition (H2) and then Hölder’s inequality (see Proposition 1.3.2 of Zhang [

44], Page 13), we deduce that

where

is a positive constant. Therefore, taking the expectation in the previous inequality, we have

By Fubini Theorem, we have

Applying Fubini Theorem again and then Itô’s formula, we have

Combining (

23) and (

24), and absolute continuity of integral, we obtain

Set

Taking conditional expectation in the BSDEL (

20), we have

By Jensen’s inequality, Hölder’s inequality, Lipschitz condition (H2), and (

23)–(

25), we have

Using Proposition 3, (H1) and (H2), for any

and

, we have

Thus, we have completed the proof of the first part of Theorem 1.

By using the relationship between the almost sure convergence and the moment convergence with Fubini’s theorem, we can see that the first part of Theorem 1 directly implies the second part. The proof is complete. □

The proofs of Theorems 2 and 3 will be decomposed into several steps as outline below.

Proposition 5. Assume that g satisfies (H1) and (H2). Denote by the solution of BSDEL (6) corresponding to . Then, the following statements are equivalent: - (i)

For all , .

- (ii)

g satisfies (H3), that is,

Proof. By the uniqueness of the solution of BSDEL (

6), it is clearly seen that (ii) ⇒ (i) holds. Let us prove that (i) ⇒ (ii) holds. Suppose that (i) holds, that is, for all

,

. Then, for all

,

. Following from Theorem 1, we can see that (ii) holds. □

For conditional cash invariance and time-consistency of , we have the following result.

Proposition 6. Assume that g satisfies (H1) and (H2). Denote by the solution of BSDEL (6) corresponding to . Then, we have the following statements: - (i)

For any , .

- (ii)

If g also satisfies (H3), then is time-consistent, i.e.,for all and all .

Proof. Let us prove that (i) holds. For each

,

, we consider the following BSDEL:

Obviously, we have

Thanks to uniqueness of the solution of BSDEL (

6), we get

and

. Thus, for each

,

,

Now we prove that (ii) holds. Suppose that

g satisfies (H3). To this end, we first prove that

Let us denote by

the solution of BSDEL (

6) corresponding to

. Following from the uniqueness of the solution of BSDEL (

6), we obtain

Let

Then, we get

. Now, we denote by

the solution of BSDEL (

6) corresponding to

. Then we have

Due to the uniqueness of the solution, we have

By Propositions 5 and 6(i), we get

Finally, we have

for all

. □

For conditional convexity of , we have the following result.

Proposition 7. Assume that g satisfies (H1), (H2), and (H3). Denote by the solution of BSDEL (6) corresponding to . Then, the following statements are equivalent: - (i)

For any , is conditional convex in , i.e., for each , - (ii)

For any , is conditional convex in , i.e., for each , - (iii)

g satisfies (H4), i.e., g is convex in .

Proof. First, we prove that (iii) ⇒ (i) holds. Suppose that

g satisfies (H4). Let

. Denote by

and

the solutions of BSDEL (

6) corresponding to

and

, respectively. Then, we have

For all

and

, we set

By assumption (H4), we get

Thus, we have

Note that

. By Proposition 2, we get for all

,

Second, let us prove that (i) ⇒ (iii) holds. For each

, we set

Then,

. Consider the following BSDELs:

By the uniqueness of solutions of BSDELs, we get

Then, by using the conditional convexity of

, we have for each

,

For all

, let

Using Theorem 1, we get that there exists a subsequence

such that

-

,

Using Theorem 1 again, we get

Furthermore, there exists a subsequence

such that

-

,

Similarly, there exists a subsequence

such that

-

,

Due to the uniqueness of the solution and assumption (H3), for all

,

, we get

Thus, combining (

34) and (

39), for all

, we have

Thus, using Theorem 1, we deduce that for all

,

,

That is,

g satisfies assumption (H4).

Obviously, (iii)

implies (iii) ⇒ (ii). Finally, we prove that (ii) ⇒ (iii) holds. Suppose that

is conditional convex in

. Then, we get

for all

Let

Then, we have

and

in

sense. With the help of Proposition 1 and the similar argument as in (

35)–(

38), we deduce that (

34) holds. By using assumption (H3) and Proposition 1, we also obtain that (

39) holds. Thus, with the same method as in the proof of (i) ⇒ (iii), we see that

g satisfies assumption (H4). □

Following the similar argument of conditional convexity of in Proposition 7, we get the following proposition.

Proposition 8. Assume that g satisfies (H1), (H2), and (H3). Denote by the solution of BSDEL (6) corresponding to . Then, the following statements are equivalent: - (i)

For any , is subadditive in , i.e., for each , - (ii)

For any , is subadditive in , i.e., for each , - (iii)

g satisfies (H5), i.e., g is subadditive in .

For monotonicity of , we have the following result.

Proposition 9. Assume that g satisfies (H1), (H2), and (H3). Denote by the solution of BSDEL (6) corresponding to . Then, the following statements are equivalent: - (i)

For each , , if .

- (ii)

For each , , if .

- (iii)

g satisfies (H7), i.e., g is nonincreasing in y.

Proof. First, we prove that (iii) ⇒ (i) holds. Let

, and

. Then, we have

and

. Notice that g is nonincreasing in

y. We have

for all

. By Proposition 2, we get

Second, we prove that (i) ⇒ (iii) holds. Let

where

and

. Then, we have

and

.

Suppose that (i) holds, For any

, we have

Similar to obtaining (

39), due to the uniqueness of the solution of BSDEL and assumption (H3), we get

for all

. With the help of Theorem 1 and the similar argument as in (

35)–(

38), we have for all

,

Notice that the choice of

a and

b is arbitrary and

, we have that g is nonincreasing in

y.

Obviously, (iii) ⇒ (i) implies (iii) ⇒ (ii). Finally, we prove that (ii) ⇒ (iii) holds. Suppose that (ii) holds. Let

where

and

. Then we have

and

. Using Proposition 1 and the similar argument as in (

35)–(

38), we have

where

Thus, by using Proposition 1, Theorem 1, and the same method as in the proof of (i) ⇒ (iii), we can see that

g satisfies assumption (H7). □

For conditional positive homogeneity of , we have the following result.

Proposition 10. Assume that g satisfies (H1) and (H2). Denote by the solution of BSDEL (6) corresponding to . Then, the following statements are equivalent: - (i)

For any , is positively homogeneous in , i.e., for each , - (ii)

For any , is positively homogeneous in , i.e., for each , - (iii)

g satisfies (H6), i.e., g is positively homogeneous in .

Proof. First, we prove that (iii) ⇒ (i) holds. Let

,

and

. Then, we have

. Let us denote by

and

the adapted solution of BSDEL (

6) corresponding to

and

, respectively. Notice that

g satisfies the assumption (H6), that is,

g is positively homogeneous in

. Then, we have

Due to uniqueness of the solution, we get for any

,

,

Second, we prove that (i) ⇒ (iii) holds. Suppose that

is positively homogeneous in

. We obtain

for all

. By proposition 5, we know that

g satisfies (H3). Due to uniqueness of the solution and assumption (H3), we also get

for all

,

. Applying the positive homogeneity of

in

, for all

we have

With the help of Lemma 1 and the similar argument as in (

35)–(

38), we have for any

,

That is,

g satisfies assumption (H6).

Obviously, (iii) ⇒ (i) implies (iii) ⇒ (ii). Finally, we prove that (ii) ⇒ (iii) holds. Suppose that (ii) holds. Then, we have

for any

Applying the positive homogeneity of

in

, we obtain

for all

. Let

, where

. Then, we have

and

in

sense. Using Theorem 1, we get

for any

With the help of the same method as in the proof of (i) ⇒ (iii), we can see that

g satisfies assumption (H6). □

Proof of Theorem 2. Using Propositions 5, 6(i), 7, and 9, we can directly see that (i) is right. Furthermore, (ii) is implied by Theorem 2(i) and Proposition 6(ii). □

Proof of Theorem 3. Using Propositions 5, 6(i), and 8–10, we can directly see that (i) is right. Furthermore, (ii) is implied by Theorem 3(i) and Proposition 6(ii). □

5. Numerical Illustrations

In this section, we will provide two numerical examples to illustrate the proposed dynamic risk measures.

Example 1. We suppose that the generator of the BSDEL (6) is independent of and is given by Let , . For any and , we consider the following equation: The solution of (

44) is

Let

By Theorem 2, we obtain that

is a dynamic convex risk measure.

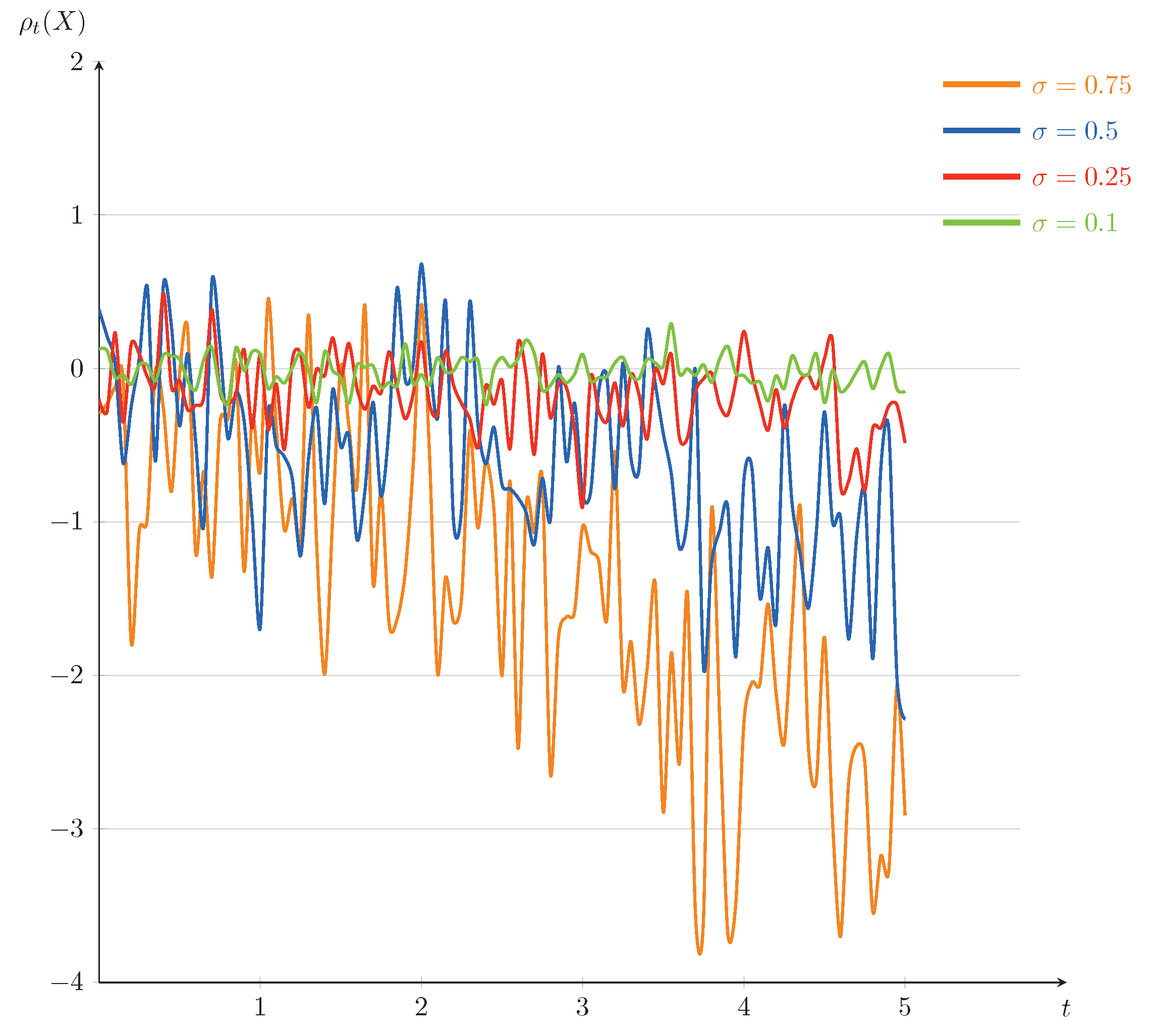

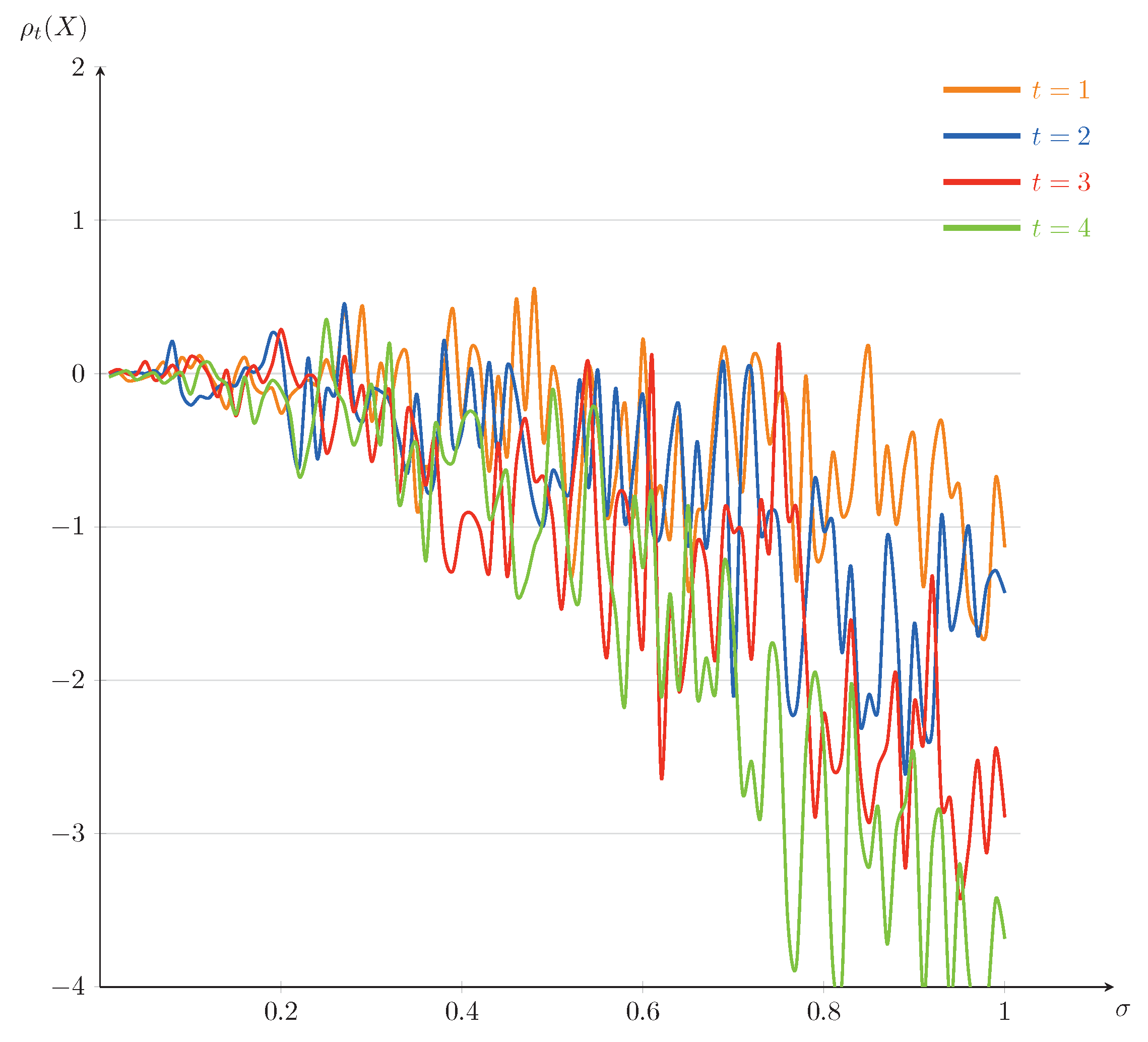

In the following, we will present some numerical illustrations for this example. Set

. The curves of

as a function of

t (for

) and as a function of

(for

) are plotted in

Figure 1 and

Figure 2, respectively. From

Figure 1 and

Figure 2, it is interesting to note that the dynamic risk measures

tend to decline on the whole, which is consistent with our intuitive understanding: in securities trading, when the stock price drops, the loss of investors increases and the corresponding cost risk also increases, as a result, the absolute value of the dynamic risk measure becomes larger. Furthermore, we find that the values of the dynamic risk measures

appear positive on some time interval, which can be interpreted by the effect of the large disturbance of Brownian motion at some point. We mention that the fluctuations of the dynamic risk measures

become more stable in

Figure 1 when

becomes smaller, and the downward trends of the dynamic risk measures

become more obvious in

Figure 2 when

t becomes bigger. That is because of choosing to invest in low-risk assets and increasing of investment risk, respectively.

In a financial market, some investors may venture among certain European-type contingent claims, some bonds, some stocks, and so on. Depending on an investor’s appetite for risk, he/she may choose a curve in

Figure 1 as their investment target, or choose a reasonable time of trading based on the impact of level of risk appetite in

Figure 2. For example, in order to get more returns, a risk-lover may choose a curve of

in

Figure 1 as his/her investment target in high-risk assets such as certain European-type contingent claims and some stocks. On the contrary, a risk-averse investor may choose a curve of

in

Figure 1 as his/her investment target.

Example 2. We suppose that the generator of the BSDEL (6) is independent of and is given by Let , . For any and , we consider the following equation: The solution of (

45) is

Let

From Theorem 2, we obtain that

is a dynamic convex risk measure.

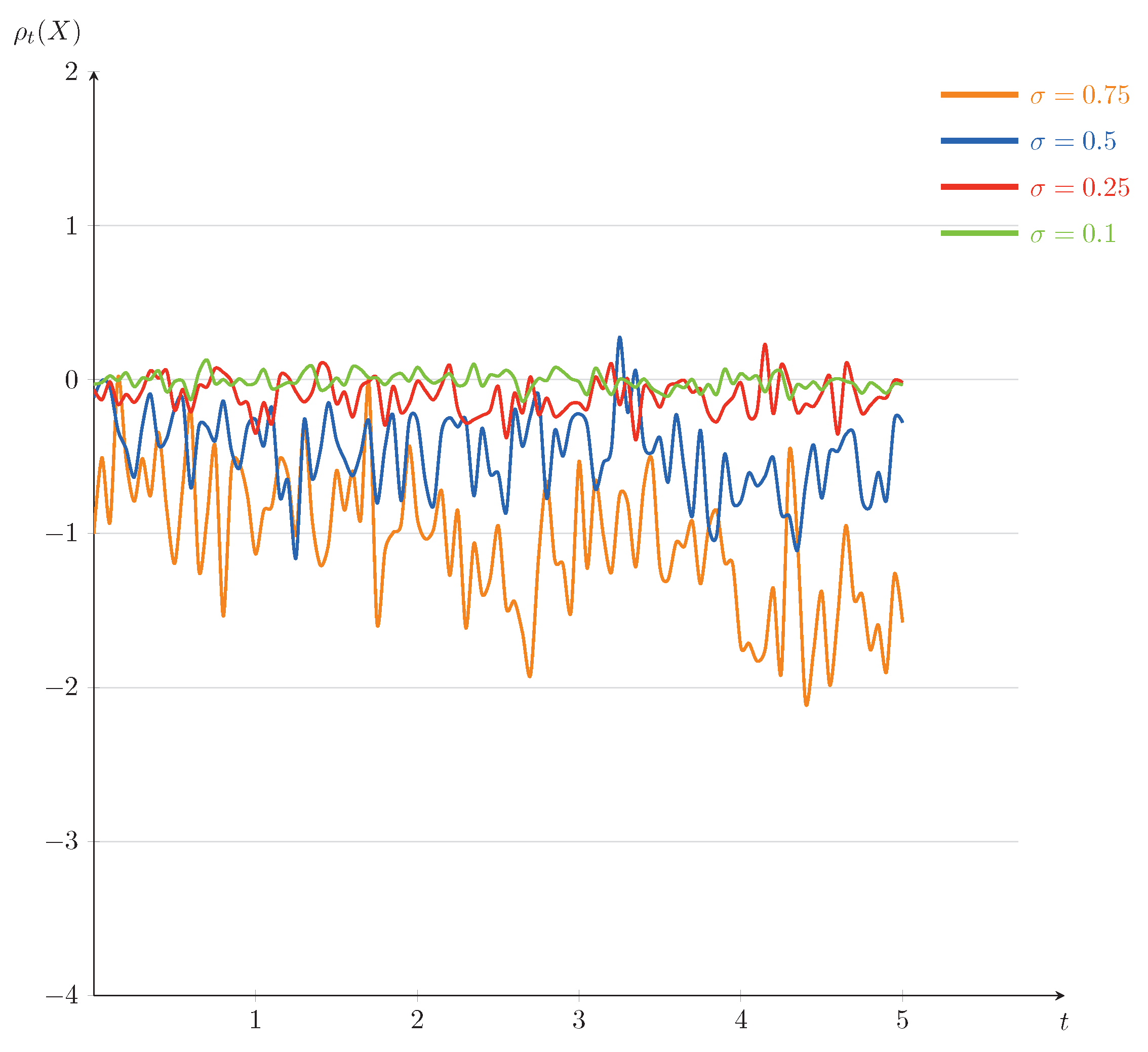

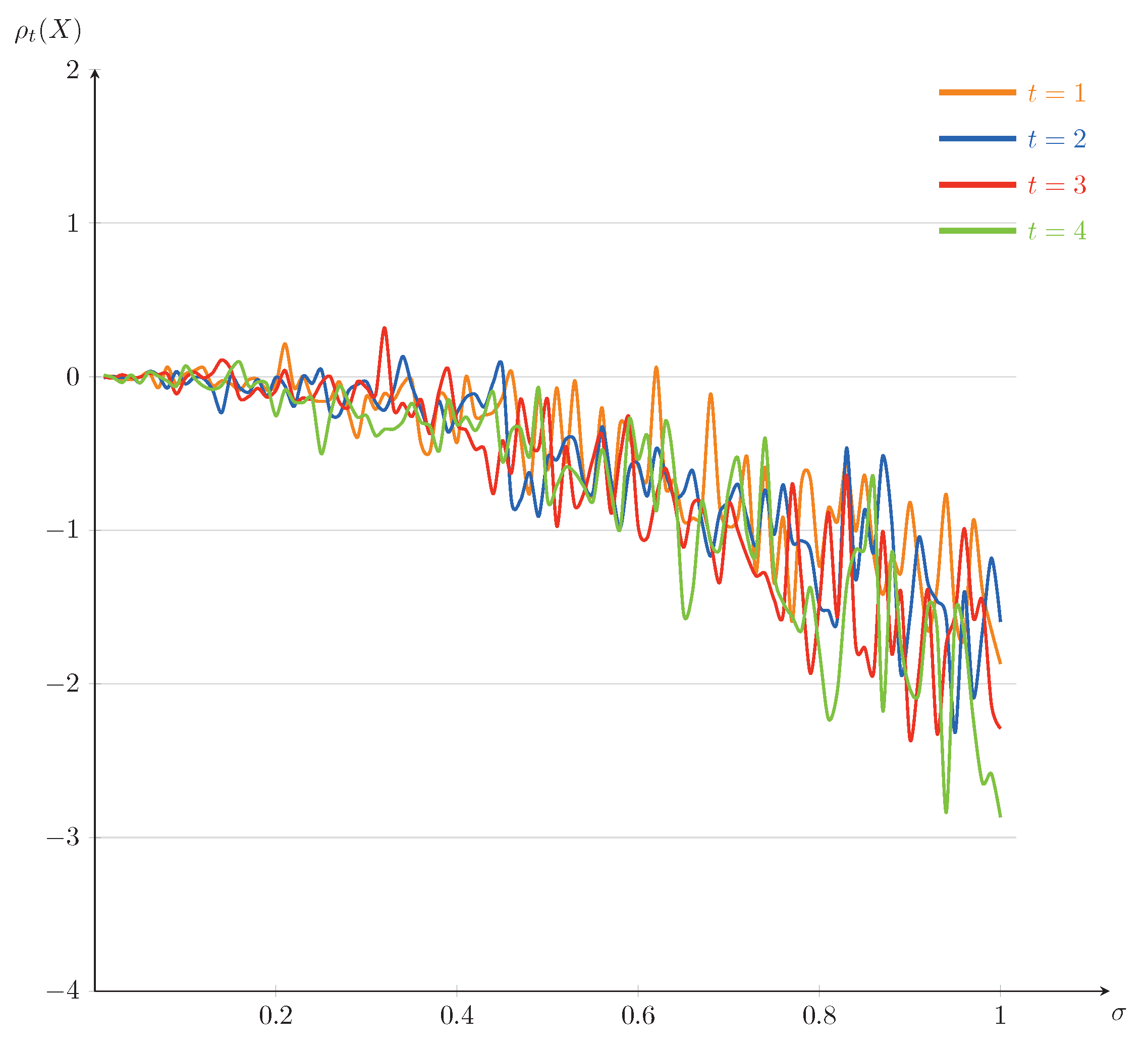

In the following, we will also present some numerical illustrations for the example. Set

. The curves of

as a function of

t (for

) and as a function of

(for

) are plotted in

Figure 3 and

Figure 4, respectively. It is interesting to note that, comparing with

Figure 3, the downward trends of the dynamic risk measures

are clearly obvious in

Figure 4. We mention that the fluctuations of the dynamic risk measures

become more stable in

Figure 3 when

becomes smaller, and there are no significant differences among the dynamic risk measures

in

Figure 4 when

t changes. Further, comparing

Figure 3 and

Figure 4 with

Figure 1 and

Figure 2, although the changing trends of the corresponding figures are similar, the fluctuation range of the former is smaller. This is because the solution of the current example is less affected by the diffusion term, which leads to a slower evolution speed than that of Example 1.

In a financial market, depending on investors’ appetite for risk, they may choose different investments in

Figure 3.

Figure 4 suggests that there may not be much difference for investors who choose a reasonable time of trading. Thus, the risk lovers, taking more risks, may choose the time

of trading to get more returns.

{kind=link}

{kind=link}

{kind=link}

{kind=link}