As these expressions verify the reasonable properties to be considered as suitable measures of uncertainty they have been used in a complementary way.

4.1. Hypothesis 1

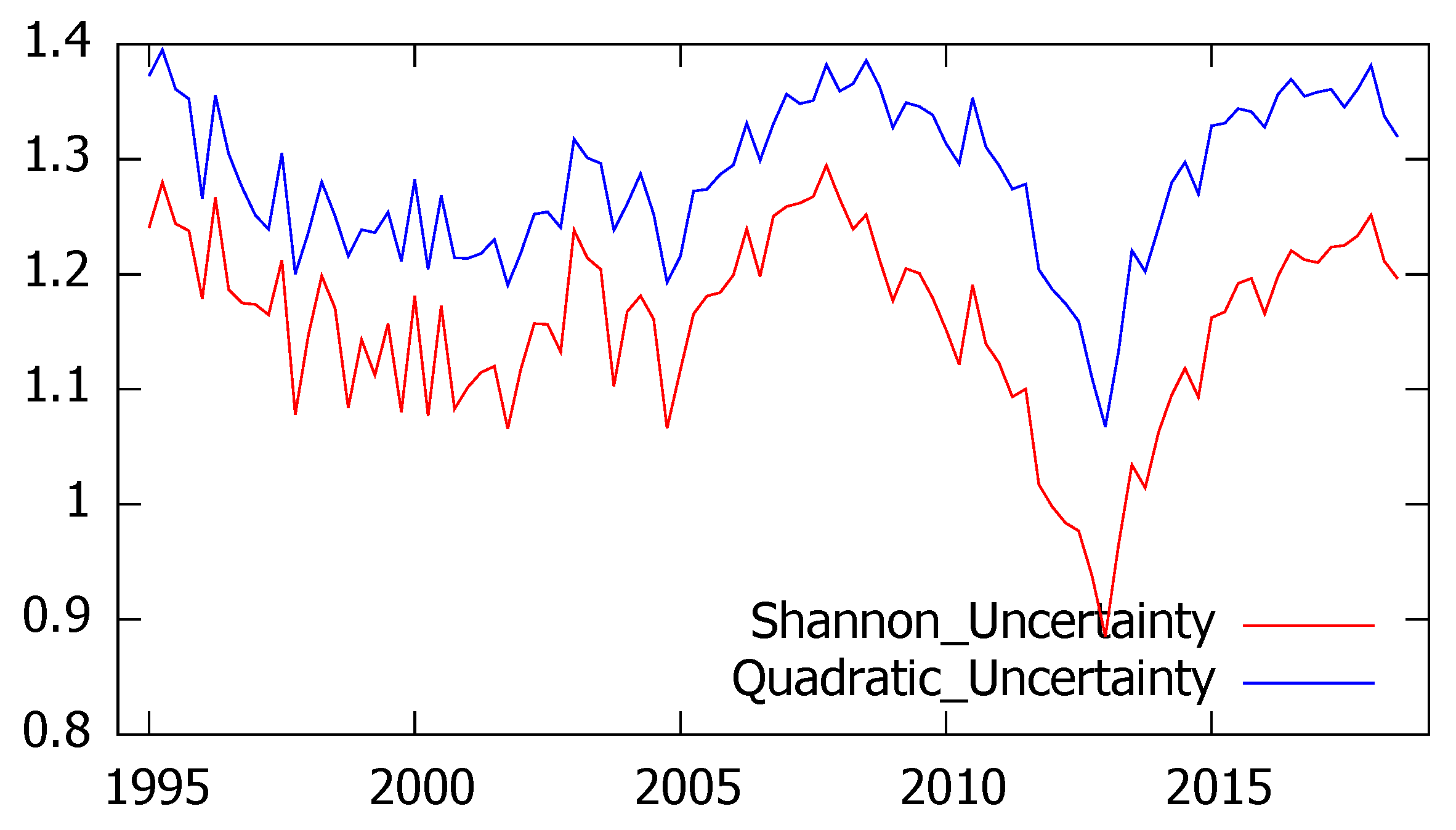

According to the first proposed hypothesis, confidence surveys allow an adequate estimate of the economic situation and the surrounding uncertainty. With the aim of testing this assumption we first consider the CIS Confidence barometers collecting extremely interesting information referred to respondents’ perception about both the economic situation in Spain and their personal situation. Since the CIS survey is not available in august, we have used quarterly series. The results of both entropy measures are represented in

Figure 1, showing a very similar evolution. As expected, Shannon’s and quadratic entropy appear to be highly correlated (the linear correlation coefficient between them reaches the value 0.91) and the level of uncertainty significantly increases between 2005 and 2007 according to both measures. Subsequently, since the end of 2007, a decreasing pattern is observed until the first quarter of 2013 when both indicators reach their minimum value and the uncertainty starts a new rise.

The analysis of these time series confirms that seasonality does not affect the levels of perceived uncertainty (the Kruskal–Wallis test fails to reject the null hypothesis of non seasonality and the same conclusion is obtained through an OLS regression with periodic dummy variables, that are found to be non-significant). It is also interesting to remark that the “herding effect” which has been largely studied in panels of forecasters does not appear in this case, as the respondents have been randomly selected and there is no influence among them.

A similar analysis has been performed on the industrial trend survey that, as we have previously described, aims at catching industrial managers’ opinions about the present and future economic situation. In this case we analyze the information referred to the region of Asturias from January 1990 to December 2018 and, although the questionnaire includes qualitative information related to several variables, we mainly focus on industrial production.

Experts’ answers were used to compute the probabilities associated to the three alternative options for the current output level (high, normal and low), leading to the estimation of monthly series for Shannon and quadratic uncertainty whose results are plot in

Figure 2.

As expected, both entropy measures provide quite similar results when measuring uncertainty referred to the current industrial production, leading to a linear correlation coefficient of 0.98.

4.2. Hypothesis 2

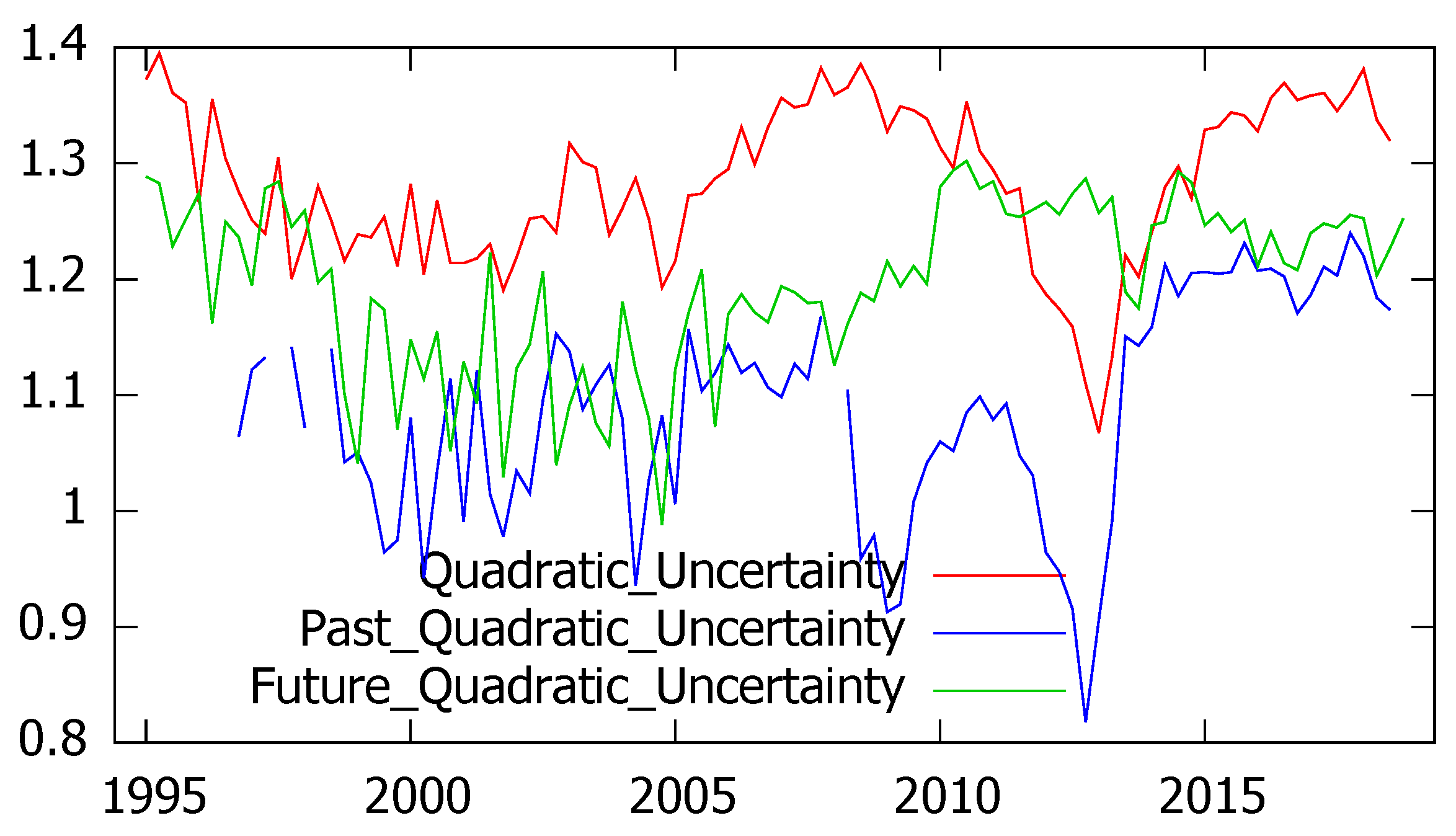

The second hypothesis refers to the ability of survey’s respondents to distinguish between current and prospective uncertainty and between general and personal uncertainty. Since the CIS barometers include current, retrospective and prospective assessments of the economic situation in Spain, we have compared the corresponding levels of Shannon’s and quadratic uncertainty, represented in

Figure 3 and

Figure 4. As it can be seen, according to both entropy measures current uncertainty is found to be higher than prospective uncertainty, which generally exceeds past uncertainty. However, some exceptions are found, corresponding to years 2012 and 2013 when the present uncertainty reaches its minimum values and is exceeded by prospective uncertainty.

As we have seen in the previous figures, Shannon’s and quadratic entropy mostly agree in the quantification of uncertainty. No matter if we consider the general or the personal situation or if uncertainty refers to present, past or future periods, the correlation coefficients always exceed 90% as summarized in

Table 3.

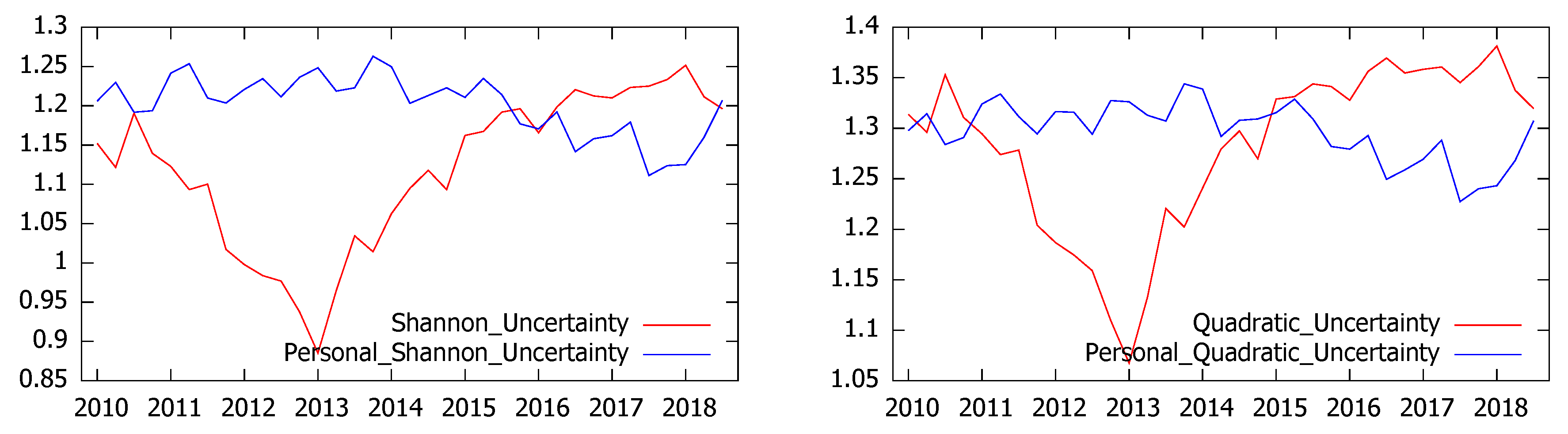

In order to analyze to which extent survey’s respondents can properly distinguish between general and personal uncertainty we have also studied the perceptions about their personal economic situation. Although these series, represented in

Figure 5 were quite short (they are only available since 2010) and therefore should be considered cautiously, the results show that until 2015 the level of uncertainty was higher when it refers to the personal situation. However, the perception of personal uncertainty seems to be more stable than that referred to the general economic situation and both measures are negatively correlated (

and

for Shannon and quadratic uncertainty respectively).

It is also interesting to mention that this situation changes when we focus on uncertainty about the future. In this case, we find no significant correlation between personal and general uncertainties, measured either with Shannon or quadratic entropy.

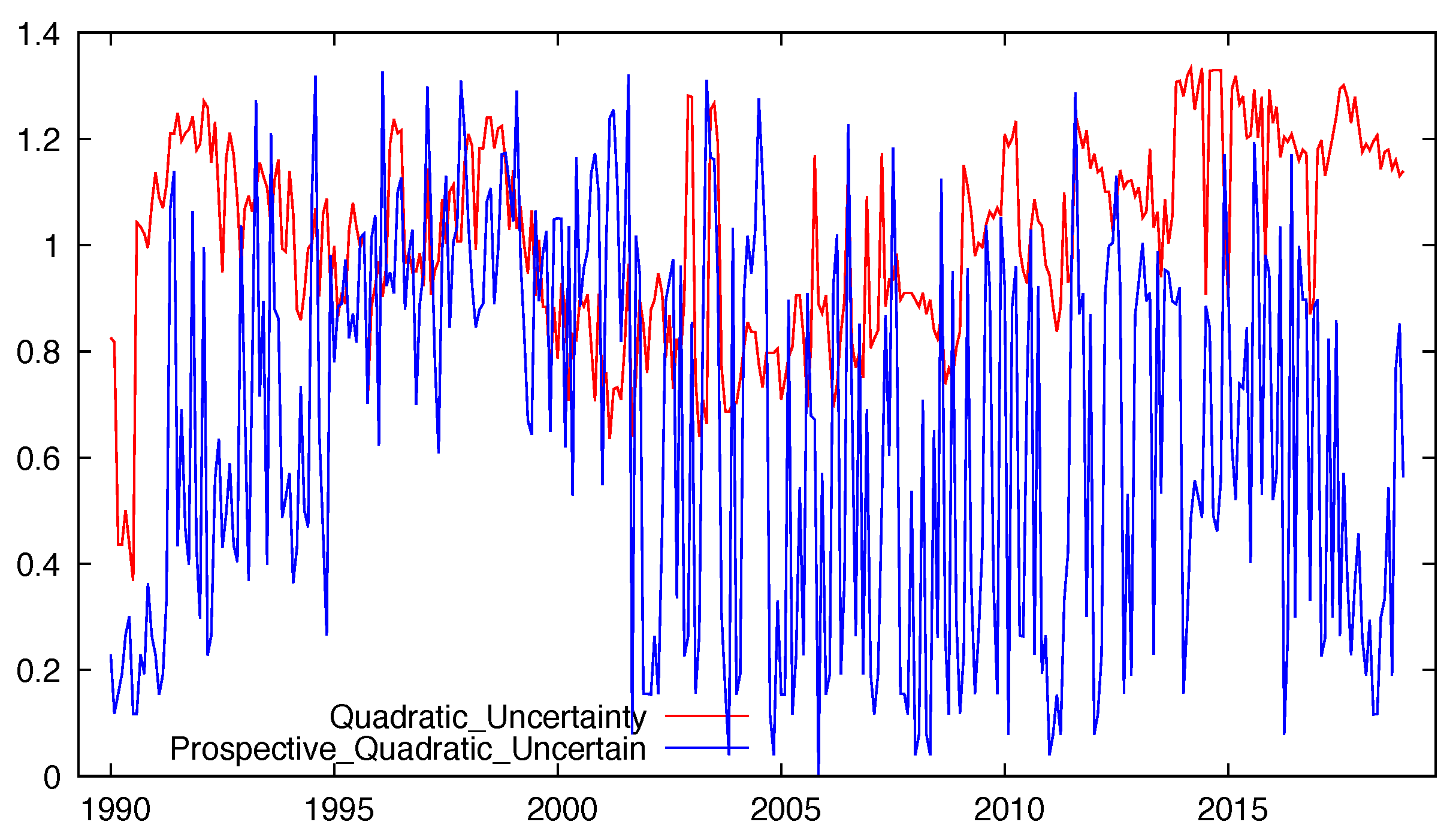

Regarding the relationship between current and prospective uncertainty, the findings differ from personal to country’s uncertainty (

Table 4). It is interesting to remark that—independently of the measure of entropy used—when we pay attention to the personal situation there is a strong relationship between current and prospective uncertainty while this correlation does not exist when we focus on the assessment of the general economic situation. These findings confirm that the respondents were able to properly distinguish the perceptions related to their own economic situation and prospects from those referred to the country as a whole.

With regard to the industrial trend surveys, the experts’ answers referred to future prospects (whose alternative options are to increase, to stay and to decrease) allow the estimation of future uncertainty, leading to similar results for Shannon’s and quadratic entropy (the correlation coefficient amounted to 0.99). As in the previous application, the obtained results show that the respondents clearly distinguished between present and prospective uncertainty. In fact, regardless of the entropy measure considered, uncertainty referred to the present industrial output is found to be higher and more stable than uncertainty referred to the future industrial production.

These findings, represented in

Figure 6 for the quadratic entropy, have been corroborated through paired difference tests, leading to the conclusion that the expected current uncertainty significantly exceeds prospective uncertainty.

4.3. Hypothesis 3

According to the third hypothesis, which we consider especially interesting, uncertainty negatively affects economic growth. In order to analyze this assumption we first focus on the CIS barometer, considering the estimated Shannon’s and quadratic entropy together with two additional quarterly series: the annual GDP growth rate and a synthetic indicator.

Denoting by the quarterly GDP, the related annualized growth rate is given by the expression .

Furthermore, following a widely extended practice in this kind of surveys, a synthetic index can be computed in order to summarize the answers. Focusing on the assessment of the current economic situation in Spain, this indicator can be easily obtained as follows: , where represent the probabilities assigned to each of the considered categories, estimated through the corresponding relative frequencies.

Once this indicator has been computed we can analyze the relationship between the perceived economic situation and the corresponding level of uncertainty. Although these quarterly series appear to be contemporaneously uncorrelated, the scatter diagram represented in

Figure 7 provides some interesting hints about the parabolic pattern of uncertainty regarding the synthetic index.

As it can be seen in this graph, low uncertainty with low dispersion is associated with very negative perceptions of the economic situation, whilst as perceptions of economic situation increase, so too do measures of uncertainty with associated increasing dispersion.

With the aim of examining how uncertainty impacts on economic activity, a more detailed analysis has been developed through VAR models. More specifically, we propose VAR models involving the economic growth, the synthetic index and the uncertainty measure, and we run two versions by using either Shannon’s entropy or quadratic entropy as the measure of uncertainty. We estimated both VAR models on quarterly data from 1996 to 2018 (T = 89) and, following the commonly used information criteria (Akaike, Schwartz and Hannah–Quinn), we considered two lags (

p = 2).

Table A1 and

Table A2 in the

Appendix A collect the VAR estimation results.

It is interesting to notice that the Granger causality test (whose null hypothesis is “no Granger causality”) leads to the

p-values collected in

Table 5 and

Table 6, showing that variations in GDP are explained by both the synthetic index and the level of uncertainty, regardless of the entropy measure used. Moreover, uncertainty was found to Granger cause the synthetic index at the 10% level.

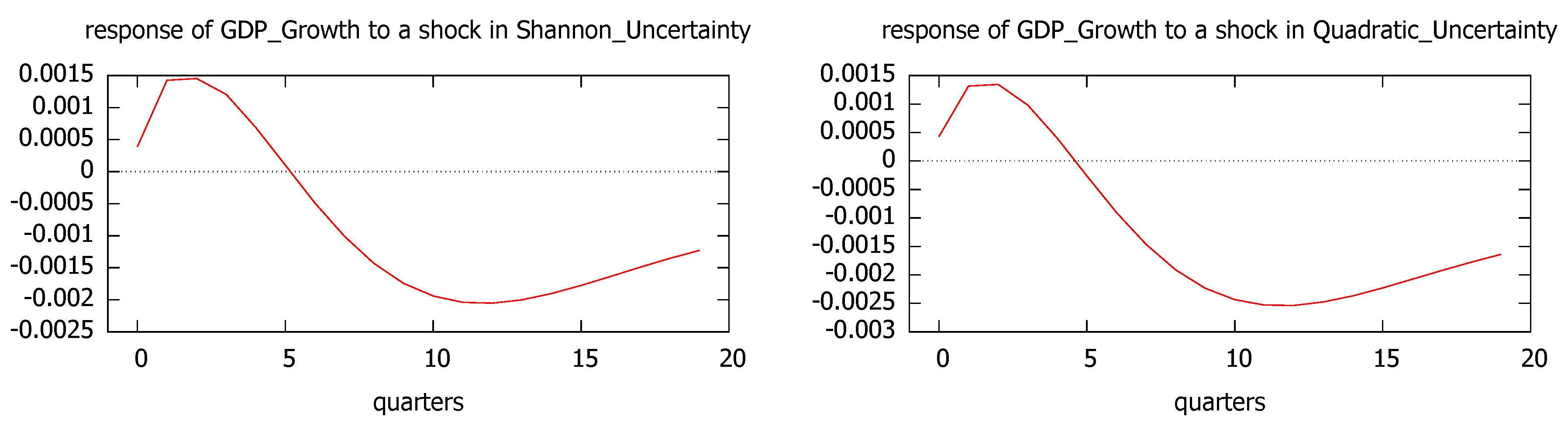

Since uncertainty causes economic growth, we have also analyzed the impulse responses for GDP growth and the synthetic index to a one standard deviation shock in the uncertainty level, measured both by Shannon and quadratic entropy. The results are plot in

Figure 8 and

Figure 9, showing that the effects of one standard deviation shock to the uncertainty in economic growth are mostly negative with their largest impacts around 12–15 months.

According to the impulse-response analysis, the behavior is quite robust with regard both to the economic indicator (GDP growth and synthetic index) and the uncertainty measure (Shannon’s and quadratic entropy).

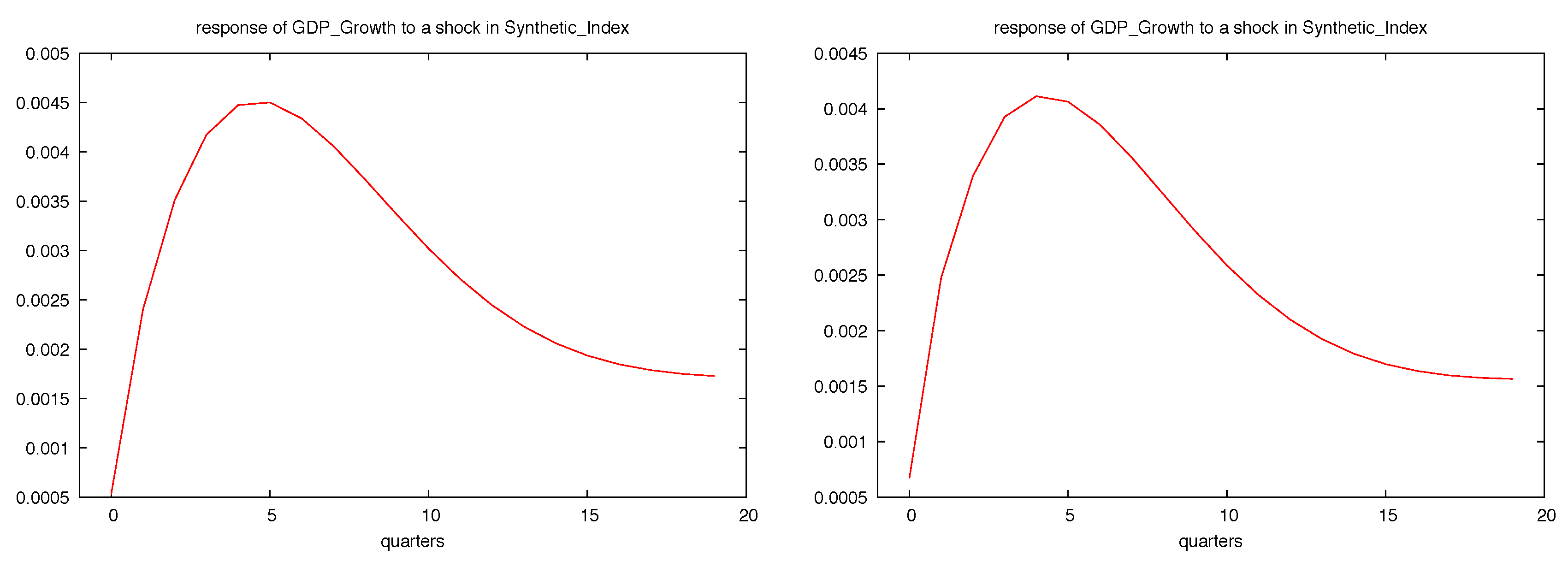

Regarding the impact of the synthetic index on GDP growth,

Figure 10 represents the impulse-response analysis for one standard deviation shock in the synthetic index. As expected, the response in this case is positive and faster, with its largest impact taking place around five months.

Following the same method we examine the relationship between uncertainty and industrial production. As in the previous analysis we estimate two VAR models including, in this case, four monthly series, corresponding to the regional IPI, the ICI, the synthetic index (SI) and the level of uncertainty.

These series have been obtained from SADEI [

21], the regional statistical office of Asturias which provides monthly information about the industrial production index (currently referred to year 2010) and the ICI, a leading indicator of economic activity [

16] computed as an arithmetic mean of the balances of the portfolio orders, the production expectations and—with the opposite sign—the level of stocks. Regarding the Synthetic Index, it has been computed as in the previous subsection from the balance of positive and negative answers referred to industrial output, using the estimated frequency probabilities.

Finally, with regard to the level of uncertainty, two VAR models have been estimated, using Shannon’s entropy in the first one and quadratic entropy in the second. Since Shannon’s index cannot be computed for some months with null probability in any of the categories we have restricted the sample size in both models (T = 124) in order to provide fully homogeneous results.

It is interesting to remark that, taking into account the series analyzed, VAR specification includes in this case constant, trend and seasonality. Following the information criteria, only one lag was considered.

The estimation results are collected in the

Appendix A (

Table A3 and

Table A4) and the conclusions show outstanding similarities for the two uncertainty measures, as it can be seen in

Figure 11. As expected, the impulse responses of the regional industrial production index to a one standard deviation shock to the uncertainty level are negative with their largest impacts during the first two periods and a quick recovery in the medium run.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}