Investigating M-Payment Intention across Consumer Cohorts

Abstract

:1. Introduction

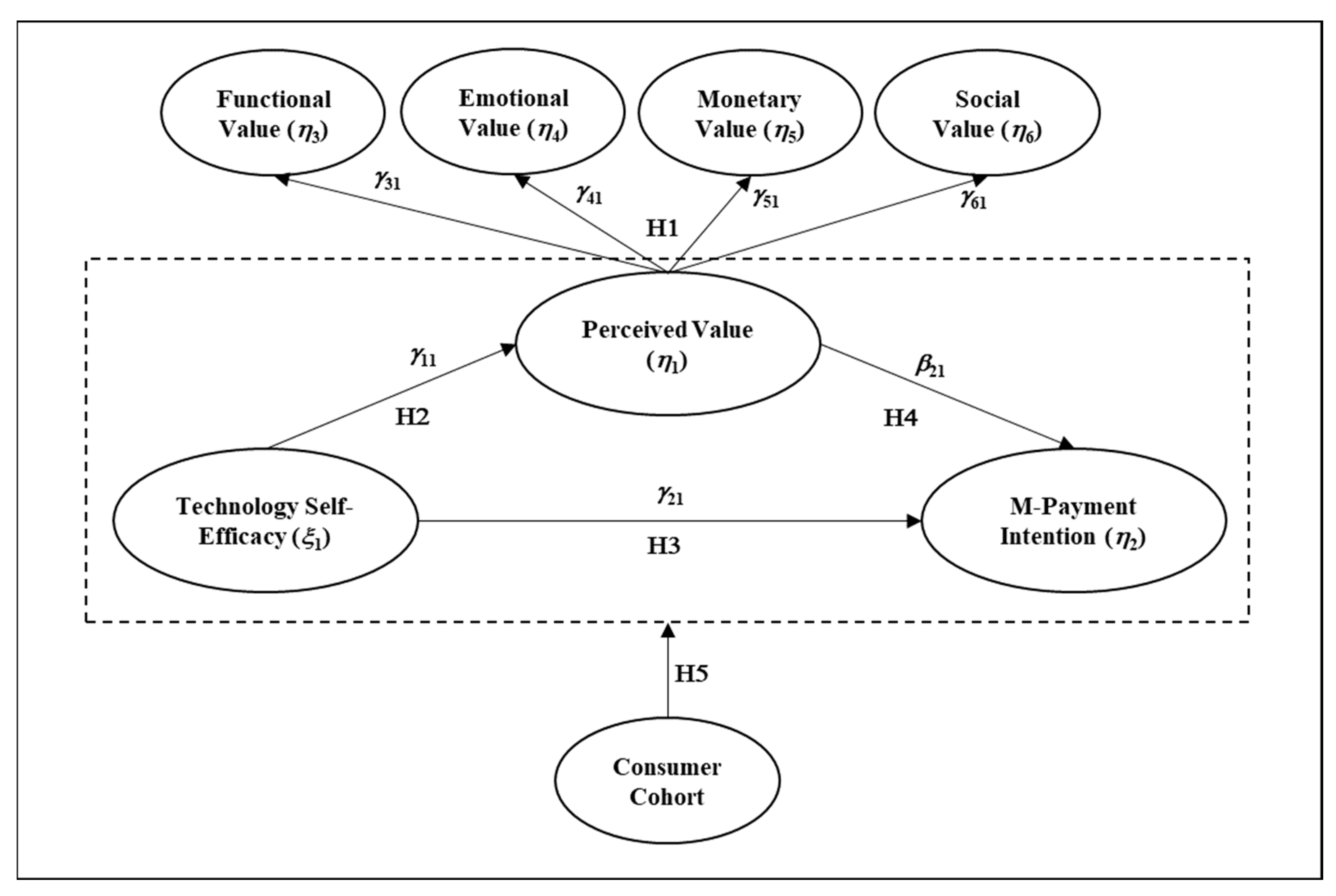

2. Literature Review and Hypothesis Development

2.1. Theoretical Underpinning

2.2. Technological Self-Efficacy

2.3. Perceived Value

2.3.1. Functional Value

2.3.2. Emotional Value

2.3.3. Monetary Value

2.3.4. Social Value

2.4. M-Payment Intention

3. Research Method

3.1. Sample and Data Collection

3.2. Research Instrument

3.3. Common Method Bias

4. Data Analysis and Results

4.1. Scale Assessment and Validation

4.2. Hypothesis Testing

5. Discussion and Conclusions

5.1. Theoretical Contributions

5.2. Practical Implications

6. Limitations and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- de Luna, I.R.; Liébana-Cabanillas, F.; Sánchez-Fernández, J.; Muñoz-Leiva, F. Mobile Payment Is Not All the Same: The Adoption of Mobile Payment Systems Depending on the Technology Applied. Technol. Forecast. Soc. 2019, 146, 931–944. [Google Scholar] [CrossRef]

- Dahlberg, T.; Guo, J.; Ondrus, J. A Critical Review of Mobile Payment Research. Electron. Commer. Res. Appl. 2015, 14, 265–284. [Google Scholar] [CrossRef]

- Shin, S.; Lee, W.-J. The Effects of Technology Readiness and Technology Acceptance on Nfc Mobile Payment Services in Korea. J. Appl. Bus. Res. 2014, 30, 1615–1626. [Google Scholar] [CrossRef]

- Yan, L.-Y.; Tan, G.W.-H.; Loh, X.-M.; Hew, J.-J.; Ooi, K.-B. Qr Code and Mobile Payment: The Disruptive Forces in Retail. J. Retail. Consum. Serv. 2021, 58, 102300. [Google Scholar] [CrossRef]

- Euromonitor International. Digital Consumer: Euromonitor from Trade Sources/National Statistics. Available online: https://www-portal-euromonitor-com.ejournal.mahidol.ac.th/statisticsevolution/index (accessed on 7 February 2023).

- Leong, L.-Y.; Hew, J.-J.; Wong, L.-W.; Lin, B. The Past and Beyond of Mobile Payment Research: A Development of the Mobile Payment Framework. Internet Res. 2022, 32, 1757–1782. [Google Scholar] [CrossRef]

- We Are Social. Digital 2023 Global Overview Report. 2023. Available online: https://wearesocial.com/uk/blog/2023/01/the-changing-world-of-digital-in-2023/ (accessed on 11 February 2023).

- Leong, C.-M.; Tan, K.-L.; Puah, C.-H.; Chong, S.-M. Predicting Mobile Network Operators Users M-Payment Intention. Eur. Bus. Rev. 2021, 33, 104–126. [Google Scholar] [CrossRef]

- Johnson, V.L.; Kiser, A.; Washington, R.; Torres, R. Limitations to the Rapid Adoption of M-Payment Services: Understanding the Impact of Privacy Risk on M-Payment Services. Comput. Hum. Behav. 2018, 79, 111–122. [Google Scholar] [CrossRef]

- Phonthanukitithaworn, C.; Sellitto, C.; Fong, M.W.L. An Investigation of Mobile Payment (M-Payment) Services in Thailand. Asia-Pac. J. Bus. Adm. 2016, 8, 37–54. [Google Scholar] [CrossRef]

- Hajek, P.; Abedin, M.Z.; Sivarajah, U. Fraud Detection in Mobile Payment Systems Using an Xgboost-Based Framework. Inf. Syst. Front. 2022, 25, 1985–2003. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; Singh, N.; Kalinic, Z.; Carvajal-Trujillo, E. Examining the Determinants of Continuance Intention to Use and the Moderating Effect of the Gender and Age of Users of Nfc Mobile Payments: A Multi-Analytical Approach. Inf. Technol. Manag. 2021, 22, 133–161. [Google Scholar] [CrossRef]

- Singh, A.K.; Sharma, P. A Study of Indian Gen X and Millennials Consumers’ Intention to Use Fintech Payment Services During COVID-19 Pandemic. J. Model. Manag. 2022, 18, 1177–1203. [Google Scholar] [CrossRef]

- Zhu, G.; Sangwan, S.; Lu, T.J. A New Theoretical Framework of Technology Acceptance and Empirical Investigation on Self-Efficacy-Based Value Adoption Model. Nankai Bus. Rev. Int. 2010, 1, 345–372. [Google Scholar] [CrossRef]

- Bank of Thailand. Payment Systems Report 2021: Thai Payments and the Next Step into the Digital World; Bank of Thailand: Bangkok, Thailand, 2021. [Google Scholar]

- Kaitawarn, C. Factor Influencing the Acceptance and Use of M-Payment in Thailand: A Case Study of Ais Mpay Rabbit. Rev. Integr. Bus. Econ. Res. 2015, 4, 222–230. [Google Scholar]

- Phonthanukitithaworn, C.; Sellitto, C.; Fong, M.W.A. Comparative Study of Current and Potential Users of Mobile Payment Services. Sage Open 2016, 6, 2158244016675397. [Google Scholar] [CrossRef]

- Chaveesuk, S.; Wutthirong, P.; Chaiyasoonthorn, W. The Model of Mobile Payment System Acceptance on Social Networks in Thailand: A Conceptual Framework. In Proceedings of the 2018 10th International Conference on Information Management and Engineering, Salford, UK, 22–24 September 2018; pp. 35–39. [Google Scholar] [CrossRef]

- Zhu, B.; Charoennan, W.; Embalzado, H. The Influence of Perceived Risks on Millennials’ Intention to Use M-Payment for Mobile Shopping in Bangkok. Int. J. Retail Distrib. Manag. 2022, 50, 479–497. [Google Scholar] [CrossRef]

- Mintel. Digital Lifestyles–Thai Consumer–2022. 2022. Available online: https://clients-mintel-com.ejournal.mahidol.ac.th/report/digital-lifestyles-thai-consumer-2022?fromSearch=%3Ffreetext%3Decommerce%2520thailand%26resultPosition%3D10 (accessed on 6 December 2022).

- Chaney, D.; Touzani, M.; Ben Slimane, K. Marketing to the (New) Generations: Summary and Perspectives. J. Strateg. Mark. 2017, 25, 179–189. [Google Scholar] [CrossRef]

- Lissitsa, S.; Laor, T. Baby Boomers, Generation X and Generation Y: Identifying Generational Differences in Effects of Personality Traits in on-Demand Radio Use. Technol. Soc. 2021, 64, 101526. [Google Scholar] [CrossRef]

- Meriac, J.P.; Woehr, D.J.; Banister, C. Generational Differences in Work Ethic: An Examination of Measurement Equivalence across Three Cohorts. J. Bus. Psychol. 2010, 25, 315–324. [Google Scholar] [CrossRef]

- Agárdi, I.; Alt, M.A. Do Digital Natives Use Mobile Payment Differently Than Digital Immigrants? A Comparative Study between Generation X and Z. Electron. Commer. Res. 2022, 1–28. [Google Scholar] [CrossRef]

- Ajzen, I.; Fishbein, M. Understanding Attitudes and Predicting Social Behavior; Prentice-Hall: Saddle River, NJ, USA, 1980. [Google Scholar]

- Ajzen, I. The Theory of Planned Behavior. Organ. Behav. Hum. Decis. Process. 1991, 50, 179–211. [Google Scholar] [CrossRef]

- Davis, F.D. Perceived Usefulness, Perceived Ease of Use, and User Acceptance of Information Technology. MIS Q. 1989, 13, 319–340. [Google Scholar] [CrossRef]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User Acceptance of Information Technology: Toward a Unified View. MIS Q. 2003, 27, 425–478. [Google Scholar] [CrossRef]

- Bandura, A. Social Foundations of Thought and Action: A Social Cognitive Theory; Prentice-Hall: Saddle River, NJ, USA, 1986. [Google Scholar]

- Bandura, A. Self-Efficacy Mechanism in Psychobiologic Functioning. In Self-Efficacy: Thought Control of Action; Schwarzer, R., Ed.; Taylor & Francis Group: New York, NY, USA, 1992; Volume 2, pp. 355–395. [Google Scholar]

- Maddux, J.E.; Gosselin, J.T. Self-Efficacy. In Handbook of Self and Identity, 2nd ed.; Leary, M.R., Tangney, J.P., Eds.; The Guilford Press: New York, NY, USA, 2003; pp. 218–238. [Google Scholar]

- Luszczynska, A.; Schwarzer, R. Social Cognitive Theory. In Predicting Health Behaviour: Research and Practice with Social Cognition Models; Conner, M., Norman, P., Eds.; Open University Press: New York, NY, USA, 2005; Volume 2, pp. 127–169. [Google Scholar]

- Bandura, A. Self-Efficacy: Toward a Unifying Theory of Behavioral Change. Psychol. Rev. 1977, 84, 191–215. [Google Scholar] [CrossRef]

- Bandura, A. Social Cognitive Theory: An Agentic Perspective. Asian J. Soc. Psychol. 1999, 2, 21–41. [Google Scholar] [CrossRef]

- Maddux, J.E. Self-Efficacy. In Handbook of Social and Clinical Psychology: The Health Perspective; Snyder, C.R., Donelson, R.F., Eds.; Pergamon Press: Tarrytown, NY, USA, 1991; pp. 57–78. [Google Scholar]

- Bandura, A. Social Cognitive Theory of Self-Regulation. Organ. Behav. Hum. Decis. Process. 1991, 50, 248–287. [Google Scholar] [CrossRef]

- Bandura, A.; Adams, N.E. Analysis of Self-Efficacy Theory of Behavioral Change. Cogn. Ther. Res. 1977, 1, 287–310. [Google Scholar] [CrossRef]

- Ariff, M.S.M.; Yeow, S.; Zakuan, N.; Jusoh, A.; Bahari, A.Z. The Effects of Computer Self-Efficacy and Technology Acceptance Model on Behavioral Intention in Internet Banking Systems. Procedia Soc. Behav. Sci. 2012, 57, 448–452. [Google Scholar] [CrossRef]

- Lin, H.-F. Understanding Behavioral Intention to Participate in Virtual Communities. Cyberpsychol. Behav. 2006, 9, 540–547. [Google Scholar] [CrossRef]

- Lew, S.; Tan, G.W.-H.; Loh, X.-M.; Hew, J.-J.; Ooi, K.-B. The Disruptive Mobile Wallet in the Hospitality Industry: An Extended Mobile Technology Acceptance Model. Technol. Soc. 2020, 63, 101430. [Google Scholar] [CrossRef]

- Holden, H.; Rada, R. Understanding the Influence of Perceived Usability and Technology Self-Efficacy on Teachers’ Technology Acceptance. J. Res. Technol. Educ. 2011, 43, 343–367. [Google Scholar] [CrossRef]

- Tao, D.; Shao, F.; Wang, H.; Yan, M.; Qu, X. Integrating Usability and Social Cognitive Theories with the Technology Acceptance Model to Understand Young Users’ Acceptance of a Health Information Portal. J. Health Inform. 2020, 26, 1347–1362. [Google Scholar] [CrossRef]

- Hong, J.-C.; Lin, P.-H.; Hsieh, P.-C. The Effect of Consumer Innovativeness on Perceived Value and Continuance Intention to Use Smartwatch. Comput. Hum. Behav. 2017, 67, 264–272. [Google Scholar] [CrossRef]

- Zhang, X.; Han, X.; Dang, Y.; Meng, F.; Guo, X.; Lin, J. User Acceptance of Mobile Health Services from Users’ Perspectives: The Role of Self-Efficacy and Response-Efficacy in Technology Acceptance. Inform. Health. Soc. Care. 2017, 42, 194–206. [Google Scholar] [CrossRef]

- Zhu, G.; So, K.K.F.; Hudson, S. Inside the Sharing Economy: Understanding Consumer Motivations Behind the Adoption of Mobile Applications. Int. J. Contemp. Hosp. Manag. 2017, 29, 2218–2239. [Google Scholar] [CrossRef]

- Cao, J.; Li, J.; Wang, Y.; Ai, M. The Impact of Self-Efficacy and Perceived Value on Customer Engagement under Live Streaming Commerce Environment. Secur. Commun. Netw. 2022, 2022, 2904447. [Google Scholar] [CrossRef]

- Zeithaml, V.A. Consumer Perceptions of Price, Quality, and Value: A Means-End Model and Synthesis of Evidence. J. Mark. 1988, 52, 2–22. [Google Scholar] [CrossRef]

- Kim, Y.; Park, Y.; Choi, J. A Study on the Adoption of Iot Smart Home Service: Using Value-Based Adoption Model. Total Qual. Manag. Bus. 2017, 28, 1149–1165. [Google Scholar] [CrossRef]

- Lin, C.H.; Sher, P.J.; Shih, H.Y. Past Progress and Future Directions in Conceptualizing Customer Perceived Value. Int. J. Serv. Ind. Manag. 2005, 16, 318–336. [Google Scholar] [CrossRef]

- Hernandez-Ortega, B.; Aldas-Manzano, J.; Ruiz-Mafe, C.; Sanz-Blas, S. Perceived Value of Advanced Mobile Messaging Services: A Cross-Cultural Comparison of Greek and Spanish Users. Inf. Technol. People 2017, 30, 324–355. [Google Scholar] [CrossRef]

- Sheth, J.N.; Newman, B.I.; Gross, B.L. Why We Buy What We Buy: A Theory of Consumption Values. J. Bus. Res. 1991, 22, 159–170. [Google Scholar] [CrossRef]

- Sweeney, J.C.; Soutar, G.N. Consumer Perceived Value: The Development of a Multiple Item Scale. J. Retail. 2001, 77, 203–220. [Google Scholar] [CrossRef]

- Rintamäki, T.; Kirves, K. From Perceptions to Propositions: Profiling Customer Value across Retail Contexts. J. Retail. Consum. Serv. 2017, 37, 159–167. [Google Scholar] [CrossRef]

- Watanabe, E.A.d.M.; Alfinito, S.; Curvelo, I.C.G.; Hamza, K.M. Perceived Value, Trust and Purchase Intention of Organic Food: A Study with Brazilian Consumers. Br. Food. J. 2020, 122, 1070–1184. [Google Scholar] [CrossRef]

- Zhang, Q.; Ariffin, S.K.; Richardson, C.; Wang, Y. Influencing Factors of Customer Loyalty in Mobile Payment: A Consumption Value Perspective and the Role of Alternative Attractiveness. J. Retail. Consum. Serv. 2023, 73, 103302. [Google Scholar] [CrossRef]

- Zhong, J.; Chen, T. Antecedents of Mobile Payment Loyalty: An Extended Perspective of Perceived Value and Information System Success Model. J. Retail. Consum. Serv. 2023, 72, 103267. [Google Scholar] [CrossRef]

- Jameel, A.S.; Karem, M.A. Perceived Trust and Enjoyment: Predicting Behavioural Intention to Use Mobile Payment Systems. In Proceedings of the 2022 International Conference on Intelligent Technology, System and Service for Internet of Everything (ITSS-IoE), Hadhramaut, Yemen, 3–5 December 2022; pp. 1–6. [Google Scholar] [CrossRef]

- Boateng, H.; Adam, D.R.; Okoe, A.F.; Anning-Dorson, T. Assessing the Determinants of Internet Banking Adoption Intentions: A Social Cognitive Theory Perspective. Comput. Hum. Behav. 2016, 65, 468–478. [Google Scholar] [CrossRef]

- Liu, T.-L.; Lin, T.T.; Hsu, S.-Y. Continuance Usage Intention toward E-Payment During the COVID-19 Pandemic from the Financial Sustainable Development Perspective Using Perceived Usefulness and Electronic Word of Mouth as Mediators. Sustainability 2022, 14, 7775. [Google Scholar] [CrossRef]

- Saprikis, V.; Avlogiaris, G.; Katarachia, A. A Comparative Study of Users Versus Non-Users’ Behavioral Intention Towards M-Banking Apps’ Adoption. Information 2022, 13, 30. [Google Scholar] [CrossRef]

- Anastasiei, B.; Dospinescu, N.; Dospinescu, O. Word-of-Mouth Engagement in Online Social Networks: Influence of Network Centrality and Density. Electronics 2023, 12, 2857. [Google Scholar] [CrossRef]

- Bilal, M.; Jianqiu, Z.; Dukhaykh, S.; Fan, M.; Trunk, A. Understanding the Effects of Ewom Antecedents on Online Purchase Intention in China. Information 2021, 12, 192. [Google Scholar] [CrossRef]

- Davis, F.D.; Bagozzi, R.P.; Warshaw, P.R. User Acceptance of Computer Technology: A Comparison of Two Theoretical Models. Manag. Sci. 1989, 35, 982–1003. [Google Scholar] [CrossRef]

- Upadhyay, N.; Upadhyay, S.; Abed, S.S.; Dwivedi, Y.K. Consumer Adoption of Mobile Payment Services during COVID-19: Extending Meta-Utaut with Perceived Severity and Self-Efficacy. Int. J. Bank Mark. 2022, 40, 960–991. [Google Scholar] [CrossRef]

- Kim, S.; Jang, S.; Choi, W.; Youn, C.; Lee, Y. Contactless Service Encounters among Millennials and Generation Z: The Effects of Millennials and Gen Z Characteristics on Technology Self-Efficacy and Preference for Contactless Service. J. Res. Interact. Mark. 2021, 16, 82–100. [Google Scholar] [CrossRef]

- Santosa, A.D.; Taufik, N.; Prabowo, F.H.E.; Rahmawati, M. Continuance Intention of Baby Boomer and X Generation as New Users of Digital Payment during COVID-19 Pandemic Using Utaut2. J. Financ. Serv. Mark. 2021, 26, 259–273. [Google Scholar] [CrossRef]

- Cheung, M.L.; Leung, W.K.S.; Chan, H. Driving Healthcare Wearable Technology Adoption for Generation Z Consumers in Hong Kong. Young Consum. 2021, 22, 10–27. [Google Scholar] [CrossRef]

- Nguyen Ngoc, T.; Viet Dung, M.; Rowley, C.; Pejić Bach, M. Generation Z Job Seekers’ Expectations and Their Job Pursuit Intention: Evidence from Transition and Emerging Economy. Int. J. Eng. Bus. Manag. 2022, 14, 18479790221112548. [Google Scholar] [CrossRef]

- Marton, Z.; Ernszt, I.; Rodek, N.; Máhr, T. Change in Responsible Consumer Behaviour through Generations? ENTRENOVA-Enterp. Res. Innov. 2019, 5, 393–401. [Google Scholar] [CrossRef]

- Klopotan, I.; Aleksić, A.; Vinković, N. Do business ethics and ethical decision making still matter: Perspective of different generational cohorts. Bus. Syst. Res. J. 2020, 11, 31–43. [Google Scholar] [CrossRef]

- Reynolds, N.L.; Simintiras, A.C.; Diamantopoulos, A. Theoretical Justification of Sampling Choices in International Marketing Research: Key Issues and Guidelines for Researchers. J. Int. Bus. Stud. 2003, 34, 80–89. [Google Scholar] [CrossRef]

- Venkatesh, V.; Thong, J.Y.L.; Xu, X. Consumer Acceptance and Use of Information Technology: Extending the Unified Theory of Acceptance and Use of Technology. MIS Q. 2012, 36, 157–178. [Google Scholar] [CrossRef]

- Compeau, D.R.; Higgins, C.A. Computer Self-Efficacy: Development of a Measure and Initial Test. MIS Q. 1995, 19, 189–211. [Google Scholar] [CrossRef]

- Mainardes, E.W.; de Almeida, C.M.; de-Oliveira, M. E-Commerce: An Analysis of the Factors That Antecede Purchase Intentions in an Emerging Market. J. Int. Consum. Mark. 2019, 31, 447–468. [Google Scholar] [CrossRef]

- Podsakoff, P.M.; MacKenzie, S.B.; Lee, J.-Y.; Podsakoff, N.P. Common Method Biases in Behavioral Research: A Critical Review of the Literature and Recommended Remedies. J. Appl. Psychol. 2003, 88, 879–903. [Google Scholar] [CrossRef] [PubMed]

- Behling, O.; Law, K.S. Translating Questionnaires and Other Research Instruments; Sage Publications, Inc.: Thousand Oaks, CA, USA, 2000. [Google Scholar]

- Bagozzi, R.; Yi, Y. Specification, Evaluation, and Interpretation of Structural Equation Models. J. Acad. Mark. Sci. Rev. 2012, 40, 8–34. [Google Scholar] [CrossRef]

- Wong, N.; Rindfleisch, A.; Burroughs, J.E. Do Reverse-Worded Items Confound Measures in Cross-Cultural Consumer Research? The Case of the Material Values Scale. J. Consum. Res. 2003, 30, 72–91. [Google Scholar] [CrossRef]

- Diamantopoulos, A.; Siguaw, J.A. Introducing Lisrel; SAGE: Newcastle upon Tyne, UK, 2000. [Google Scholar]

- Fornell, C.; Larcker, D.F. Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Singh, J. Measurement Issues in Cross-National Research. J. Int. Bus. Stud. 1995, 26, 597–619. [Google Scholar] [CrossRef]

- Francis, T.; Hoefel, F. The Influence of Gen Z—The First Generation of True Digital Natives—Is Expanding. 2018. Available online: https://www.mckinsey.com/industries/consumer-packaged-goods/our-insights/true-gen-generation-z-and-its-implications-for-companies#/ (accessed on 23 April 2023).

{kind=link}

| Functional | Emotional | Social | Monetary | Others | |

|---|---|---|---|---|---|

| Sheth, Newman, and Gross [51] | ✕ | ✕ | ✕ | Condition Epistemic | |

| Sweeney and Soutar [52] | ✕ | ✕ | ✕ | ✕ | |

| Zhu, Sangwan, and Lu [14]; Zhu, So, and Hudson [45] | ✕ | ✕ | ✕ | ||

| Hernandez-Ortega, Aldas-Manzano, Ruiz-Mafe, and Sanz-Blas [50] | ✕ | ✕ | ✕ | ✕ | |

| Rintamäki and Kirves [53] | ✕ | ✕ | ✕ | ✕ | |

| Watanabe, Alfinito, Curvelo, and Hamza [54] | ✕ | ✕ | ✕ | ✕ | |

| Zhang, Ariffin, Richardson, and Wang [55] | ✕ | ✕ | ✕ | ✕ | Epistemic |

| Zhong and Chen [56] | ✕ | ✕ | ✕ |

| Characteristics | Total (n = 716) | Gen B (n = 143) | Gen X (n = 163) | Gen Y (n = 203) | Gen Z (n = 207) |

|---|---|---|---|---|---|

| Gender | |||||

| Male | 332 (46.4%) | 73 (51.1%) | 73 (44.8%) | 96 (47.3%) | 90 (43.5%) |

| Female | 377 (52.7%) | 70 (49%) | 90 (55.2%) | 102 (50.2%) | 115 (55.6%) |

| Prefer not to say | 7 (0.9%) | - | - | 5 (2.5%) | 2 (1%) |

| Age (years) | |||||

| Mean | 36.5 | 59.6 | 46.7 | 27.4 | 21.4 |

| S.D. | 15.2 | 3.7 | 4.7 | 3.9 | 1.7 |

| Monthly income (THB) | |||||

| <15,000 | 191 (26.7%) | 31 (21.7%) | 11 (6.7%) | 34 (16.7%) | 115 (55.6%) |

| 15,001–30,000 | 231 (32.3%) | 19 (13.3%) | 46 (28.2%) | 87 (42.9%) | 79 (38.2%) |

| 30,001–45,000 | 91 (12.7%) | 30 (21%) | 20 (12.3%) | 34 (16.7%) | 7 (3.4%) |

| >45,000 | 203 (28.3%) | 63 (44%) | 86 (52.7%) | 48 (23.6%) | 6 (2.8%) |

| Highest Education | |||||

| Below undergraduate | 158 (22.1%) | 56 (39.2%) | 51 (31.3%) | 17 (8.4%) | 34 (16.4%) |

| Bachelor degree | 463 (64.6%) | 60 (41.9%) | 81 (49.7%) | 152 (74.9%) | 170 (82.1%) |

| Post bachelor degree | 95 (13.3%) | 27 (18.9%) | 31 (19%) | 34 (16.7%) | 3 (1.4%) |

| Latest online shopping | |||||

| Today | 106 (14.8%) | 5 (3.5%) | 18 (11.0%) | 50 (24.6%) | 33 (15.9%) |

| Yesterday | 121 (16.9% | 8 (5.6%) | 23 (14.1%) | 42 (20.7%) | 48 (23.2%) |

| Within the past one week | 216 (30.2%) | 38 (26.6%) | 54 (33.1%) | 59 (29.1%) | 65 (31.4%) |

| Within the past one month | 155 (21.6%) | 38 (26.6%) | 40 (24.5%) | 34 (16.7%) | 43 (20.8%) |

| Within the past three months | 51 (7.1%) | 20 (14.0%) | 13 (8.0%) | 10 (4.9%) | 8 (3.9%) |

| Within the past six months | 27 (3.8%) | 10 (7.0%) | 8 (4.9%) | 3 (1.5%) | 6 (2.9%) |

| Within the past one year | 14 (2.0%) | 6 (4.2%) | 2 (1.2%) | 2 (1.0%) | 4 (1.9%) |

| More than one year ago | 26 (3.6%) | 18 (12.6%) | 5 (3.1%) | 3 (1.5%) | 0 (0%) |

| Research Constructs and Items | Standardized Loadings a | Item-to-Total Correlation |

|---|---|---|

| 1. Perceived value (α = 0.80; CR = 0.91; AVE = 0.66) (Seven-point Likert scale, anchored “strongly disagree” and “strongly agree”) Source: Venkatesh, Thong, and Xu [72] | ||

| Functional value (α = 0.89; CR = 0.95; AVE = 0.86) | 0.72 b | |

| I find mobile payment useful in my daily life. | 0.88 b | 0.79 |

| Using mobile payment helps me accomplish payment quickly. | 0.85 (27.70) | 0.79 |

| Using mobile payment increases my payment productivity. | 0.89 (29.59) | 0.81 |

| Emotional value (α = 0.93; CR = 0.97; AVE = 0.90) | 0.74 (18.94) | |

| Using mobile payment is fun. | 0.81 b | 0.86 |

| Using mobile payment is enjoyable. | 0.91 (37.19) | 0.86 |

| Using mobile payment is very entertaining. | 0.91 (36.96) | 0.86 |

| Monetary value (α = 0.81; CR = 0.91; AVE = 0.84) | 0.95 (21.22) | |

| Using mobile payment is reasonably priced | 0.92 b | 0.68 |

| Using mobile payment is a good value for money. | 0.80 (22.72) | 0.68 |

| Social value (α = 0.90; CR = 0.94; AVE = 0.79) | 0.65 (16.06) | |

| The use of mobile payment helps me feel acceptable. | 0.86 b | 0.79 |

| The use of mobile payment makes a good impression on other people. | 0.87 (29.80) | 0.81 |

| The use of mobile payment gives me social approval | 0.86 (29.32) | 0.81 |

| 2. Technology self-efficacy (α = 0.96; CR = 0.97; AVE = 0.85) I could complete the tasks using online… (Seven-point scale anchored, “not at all confident” and “totally confident”) Source: Compeau and Higgins [73] | ||

| … if there was no one around to tell me what to do as I go.c | ||

| … if I had never used a platform like it before.c | ||

| … if I had only the instructions/manuals for reference.c | ||

| … if I had seen someone else using it before trying it myself. | 0.81 b | 0.79 |

| … if I could call someone for help if I got stuck. | 0.87 (28.21) | 0.85 |

| … if someone else had helped me get started. | 0.88 (28.77) | 0.85 |

| … if I had a lot of time to complete the task for which the platform was provided. | 0.89 (29.68) | 0.87 |

| … if I had just the build-in help facility for assistance. | 0.90 (30.19) | 0.88 |

| … if someone showed me how to do it first. | 0.86 (27.94) | 0.84 |

| … if I had used similar platform before this one to do the same task. | 0.86 (27.94) | 0.84 |

| 3. M-Payment Intention (α = 0.81; CR = 0.94; AVE = 0.97) (Seven-point Likert scale, anchored “strongly disagree” and “strongly agree”) Source: Mainardes, de Almeida, and de-Oliveira [74] | ||

| In the future, I intend to use mobile payment to make purchases. | 0.90 b | 0.68 |

| If I am in need of a product/service, I will use the mobile payment to make the purchase. | 0.89 (28.16) | 0.68 |

| In the near future, I do not intend to use the mobile payment to do my shopping.c | ||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | |

|---|---|---|---|---|---|---|---|

| 1. Perceived value | 0.81 | ||||||

| 2. Functional Value | 0.67 * | 0.93 | |||||

| 3. Emotional Value | 0.84 * | 0.39 * | 0.95 | ||||

| 4. Monetary Value | 0.85 * | 0.59 * | 0.59 * | 0.92 | |||

| 5. Social Value | 0.79 * | 0.25 * | 0.61 * | 0.55 * | 0.89 | ||

| 6. M-payment Intention | 0.61 * | 0.60 * | 0.47 * | 0.53 * | 0.38 * | 0.97 | |

| 7. Technological Efficacy | 0.42 * | 0.51 * | 0.30 * | 0.43 * | 0.16 * | 0.45 * | 0.92 |

| Mean | 5.02 | 5.83 | 4.66 | 5.14 | 4.500 | 5.4 | 4.8 |

| SD | 1.13 | 1.24 | 1.58 | 1.30 | 1.6 | 1.4 | 1.4 |

| Paths | Full Sample (n = 716) | Gen B (n = 143) | Gen X (n = 163) | Gen Y (n = 203) | Gen Z (n = 207) |

|---|---|---|---|---|---|

| Perceived Value→Functional Value (γ31) | 0.63 0.73 ** (0.05) | 0.69 0.86 ** (0.12) | 0.72 0.91 ** (0.11) | 0.52 0.55 ** (0.09) | 0.43 0.45 ** (0.09) |

| Perceived Value→Emotional Value (γ41) | 0.76 1.05 ** (0.05) | 0.78 1.12 ** (0.12) | 0.77 1.08 ** (0.11) | 0.75 1.02 * (0.10) | 0.70 0.95 ** (0.11) |

| Perceived Value→Monetary Value (γ51) | 0.73 0.95 ** (0.05) | 0.72 0.94 ** (0.12) | 0.76 1.03 ** (0.08) | 0.72 0.93 ** (0.10) | 0.68 0.88 ** (0.10) |

| Perceived Value→Social Value (γ61) | 0.71 0.92 * (0.05) | 0.77 1.09 ** (0.13) | 0.78 1.11 ** (0.11) | 0.72 0.94 * (0.10) | 0.67 0.87 ** (0.11) |

| Direct Effect Technological Self-Efficacy→Perceived Value (γ11) | 0.44 0.36 * (0.04) | 0.42 0.36 * (0.11) | 0.45 0.35 * (0.08) | 0.42 0.38 * (0.09) | 0.27 0.23 * (0.12) |

| Technological Self-Efficacy→M-Payment Intention (γ21) | 0.16 0.16 ** (0.04) | 0.05 0.06 (0.11) | 0.11 0.11 (0.08) | 0.20 0.21 * (0.08) | 0.22 0.21 * (0.08) |

| Perceived Value→M-Payment Intention (β21) | 0.59 0.73 ** (0.05) | 0.69 0.89 * (0.13) | 0.69 0.91 ** (0.05) | 0.49 0.57 ** (0.09) | 0.47 0.54 * (0.10) |

| Indirect Effect Technological Self-Efficacy→Perceived Value→M-Payment Intention (γ11 * β21) | 0.26 0.27 * (0.04) | 0.29 0.32 ** (0.10) | 0.31 0.32 ** (0.07) | 0.21 0.22 ** (0.07) | 0.13 0.12 * (0.07) |

| Total Effect Technological Self-Efficacy→M-Payment Intention [γ21 + (γ11 * β21)] | 0.42 0.43 * (0.04) | 0.34 0.37 ** (0.12) | 0.42 0.44 * (0.08) | 0.41 0.42 * (0.08) | 0.35 0.33 ** (0.07) |

| Hypothesis | Results |

|---|---|

| H1. Functional value, emotional value, monetary value, and social value are salient dimensions of perceived value. | Supported |

| H2. Technological self-efficacy positively influences perceived value. | Supported |

| H3. Technological self-efficacy positively influences m-payment intention. | Supported |

| H4. Perceived value positively influences m-payment intention. | Supported |

| H5. The relationships among technological self-efficacy, perceived value, and m-payment differ across consumer cohorts. | Supported |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Thoumrungroje, A.; Suprawan, L. Investigating M-Payment Intention across Consumer Cohorts. J. Theor. Appl. Electron. Commer. Res. 2024, 19, 431-447. https://doi.org/10.3390/jtaer19010023

Thoumrungroje A, Suprawan L. Investigating M-Payment Intention across Consumer Cohorts. Journal of Theoretical and Applied Electronic Commerce Research. 2024; 19(1):431-447. https://doi.org/10.3390/jtaer19010023

Chicago/Turabian StyleThoumrungroje, Amonrat, and Lokweetpun Suprawan. 2024. "Investigating M-Payment Intention across Consumer Cohorts" Journal of Theoretical and Applied Electronic Commerce Research 19, no. 1: 431-447. https://doi.org/10.3390/jtaer19010023